|

시장보고서

상품코드

1861052

동물용 생물제제 시장 : 제품 유형별, 동물 유형별, 투여 경로별, 용도별, 최종사용자별, 지역별 - 예측(-2030년)Veterinary Biologics Market by Product (Monoclonal Antibodies, Diagnostic Kits, Immunoglobulins & Antitoxins), RoA (Injectable, Oral), Application (Infectious Disease Prevention, Dermatology, Pain Management), Animal, End User - Global Forecast to 2030 |

||||||

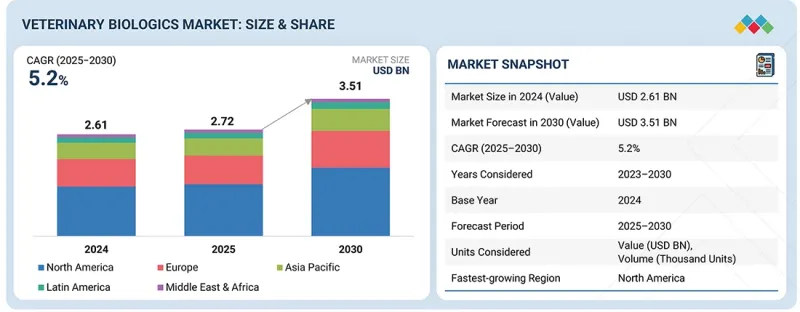

세계의 동물용 생물제제 시장 규모는 예측 기간중 CAGR이 5.2%를 보이며 2025년 27억 2,000만 달러에서 2030년에는 35억 1,000만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2033년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 제품 유형별, 동물 유형별, 투여 경로별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

동물용 생물학적 제제 시장은 반려동물 인구 증가와 반려동물 양육률 상승에 힘입어 괄목할 만한 성장세를 보이고 있습니다. 만성질환에 대한 관심이 높아지면서 수의학적 치료에 대한 수요가 더욱 증가하고 있습니다. 정부 및 동물보호단체는 동물보호 캠페인을 적극적으로 추진하여 반려동물과 가축의 피부질환을 조기에 진단하고 치료할 수 있도록 장려하고 있습니다.

또한, 반려동물 보험의 보급과 동물 건강관리에 대한 높은 지출이 전문적인 수의학 서비스에 대한 접근성을 향상시켜 시장 확대를 뒷받침하고 있습니다. 하지만 반려동물 의료비 상승이 치료의 보급을 가로막는 등의 문제도 있습니다. 또한, 엄격한 규제 지침과 긴 의약품 승인 절차는 시장 성장을 더욱 억제하고 있습니다.

단클론 항체는 표적 작용, 높은 효능, 가축 건강 관리에서의 채택 증가로 인해 동물용 생물학적 제제 시장에서 급성장할 것으로 예측됩니다. 이러한 생물학적 제제는 병원체나 독소를 정확하게 표적화하여 특정 질병을 예방하고 치료하는 데에 사용되며, 항생제와 같은 기존 치료법에 대한 보다 선택적이고 효과적인 대안을 제공합니다. 가축에 적용될 때, 단클론 항체는 신속한 면역 지원이 필요한 질병에 특히 유용하며, 그 결과 이환율이 감소하고 생산성이 향상됩니다. 단클론 항체의 사용은 지속 가능한 축산 관행으로의 전환과 항균제 내성(AMR)의 감소에 따른 전 세계적인 추세와 일치하며, 첨단 생물학적 치료제로서 선호되는 선택이 되고 있습니다.

반려동물의 아토피 피부염, 옴, 벼룩 및 진드기 매개 피부질환 등 피부질환의 높은 유병률로 인해 피부과 분야가 동물용 생물학적 제제 시장을 주도할 것으로 예측됩니다. 반려동물을 키우는 인구 증가와 동물 건강에 대한 인식이 높아지면서 첨단 피부과 치료에 대한 수요가 증가하고 있습니다. 단일클론항체와 같은 생물학적 제제는 기존 약물에 비해 부작용이 적고 효과적인 표적치료제로서 인기가 높아지고 있습니다. 만성 피부 알레르기를 타겟으로 한 동물용 생물학적 제제의 승인이 증가하면서 이 분야는 더욱 강화되고 있습니다. 또한, 피부과 질환은 동물병원을 찾는 가장 흔한 이유 중 하나로 안정적인 수요를 확보하고 있습니다. 반려동물에 대한 보험 적용 확대도 고가의 생물학적 제제 채택을 촉진하고 있습니다. 전반적으로 이러한 요인들은 피부과를 동물용 생물학적 제제 시장의 주요 부문으로 자리매김하고 있습니다.

북미는 잘 구축된 수의학 의료 인프라와 높은 반려동물 보유율에 힘입어 2024년 가장 큰 시장 점유율을 차지했습니다. 이 지역에는 혁신적인 단일클론항체 치료제 연구개발에 투자하는 주요 시장 관계자들이 존재감을 드러내고 있습니다. 반려동물의 건강에 대한 인식이 높아지고 동물 의료에 대한 지출이 증가하면서 시장 성장을 견인하고 있습니다. 또한, 고급 펫케어 제품에 대한 수요 증가로 인해 세계 동물용 단일클론항체 산업에서 북미가 우위를 점하고 있습니다.

세계의 동물용 생물학적 제제 시장을 조사했으며, 제품 유형별, 동물 유형별, 투여 경로별, 용도별, 최종사용자별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 기술 분석

- 고객의 비즈니스에 영향을 미치는 동향/파괴적 변화

- 밸류체인 분석

- 무역 분석

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 규제 분석

- 특허 분석

- 가격 분석

- 2025-2026년 주요 컨퍼런스 및 이벤트

- 생태계 분석

- 상환 분석

- 미충족 요구

- AI/생성형 AI가 동물용 생물제제 시장에 미치는 영향

- 투자 및 자금조달 시나리오

- 파이프라인 분석

- 2025년 미국 관세가 동물용 생물제제 시장에 미치는 영향

제6장 동물용 생물제제 시장(제품 유형별)

- 서론

- 단일클론항체

- 면역글로불린 및 항독소

- 면역조절제 및 면역자극제

- 진단 키트

제7장 동물용 생물제제 시장(동물 유형별)

- 서론

- 반려동물

- 가축

제8장 동물용 생물제제 시장(투여 경로별)

- 서론

- 주사 투여 경로

- 경구 투여

- 기타

제9장 동물용 생물제제 시장(용도별)

- 서론

- 피부과

- 진단 검사

- 통증 관리

- 감염증 예방

- 종양학

- 기타

제10장 동물용 생물제제 시장(최종사용자별)

- 서론

- 동물 병원 및 클리닉

- 수의 진단실험실

- 기타

제11장 동물용 생물제제 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 일본

- 중국

- 인도

- 호주

- 한국

- 뉴질랜드

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 기타

제12장 경쟁 구도

- 서론

- 주요 시장 진출기업의 전략/강점

- 매출 분석, 2022년-2024년

- 시장 점유율 분석, 2024년

- 주요 시장 진출기업 순위

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2023년

- 브랜드/제품 비교

- 기업 평가와 재무 지표

- 경쟁 시나리오

제13장 기업 개요

- 주요 시장 진출기업

- ZOETIS SERVICES LLC

- IDEXX

- ELANCO

- MERCK & CO., INC.

- THERMO FISHER SCIENTIFIC INC.

- BOEHRINGER INGELHEIM INTERNATIONAL GMBH

- NEOGEN CORPORATION

- BIO-RAD LABORATORIES, INC.

- IMMUCELL CORPORATION

- INNOVATIVE DIAGNOSTICS

- 기타 기업

- BIONOTE USA INC.

- BIOCHEK

- PLASVACC USA

- NOVAVIVE INC.

- MG BIOLOGICS

- STALLERGENES GREER

- BIOSTONE ANIMAL HEALTH

- COLORADO SERUM COMPANY

- PADULA SERUMS PTY LTD.

- LAKE IMMUNOGENICS

- INBIOS INTERNATIONAL, INC.

- PRINCETON BIOMEDITECH CORPORATION

- TETRACORE, INC.

- VMRD, INC.

- ANIMAB

제14장 부록

LSH 25.11.18The global veterinary biologics market is projected to reach USD 3.51 billion by 2030 from USD 2.72 billion in 2025, at a CAGR of 5.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product type, Animal Type, Route of Administration, Application, End user, Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

The veterinary biologics market is experiencing significant growth, driven by an expanding companion animal population and rising pet ownership. Increasing concerns about chronic diseases have further boosted demand for veterinary treatments. Government and animal welfare organizations actively promote awareness campaigns, encouraging early diagnosis and treatment of dermatological conditions in both pets and farm animals.

Additionally, the growing adoption of pet insurance and high expenditure on animal healthcare support market expansion by improving access to specialized veterinary services. However, the market faces challenges such as the rising cost of pet care, which can limit treatment adoption. Moreover, strict regulatory guidelines and lengthy drug approval processes further restrain market growth.

"The monoclonal antibodies segment has accounted for the largest market share in the veterinary biologics market."

Monoclonal antibodies are projected to experience rapid growth in the veterinary biologics market, driven by their targeted action, high effectiveness, and increasing adoption in livestock health management. These biologics are increasingly used to prevent and treat specific diseases by precisely targeting pathogens or toxins, providing a more selective and effective alternative to traditional therapies like antibiotics. In livestock applications, monoclonal antibodies are especially valuable for conditions that require swift immune support, resulting in decreased morbidity and higher productivity. Their use aligns with the global shift toward sustainable animal farming practices and the reduction of antimicrobial resistance (AMR), making them a preferred choice for advanced biologic treatments.

"The dermatology segment accounted for the largest market share in 2024 in the veterinary biologics market."

The dermatology segment is expected to dominate the veterinary biologics market because of the high prevalence of skin disorders like atopic dermatitis, mange, and flea- or tick-borne skin infections in companion animals. Increasing pet ownership and greater awareness of animal health have boosted demand for advanced dermatological treatments. Biologics, such as monoclonal antibodies, are becoming more popular as effective, targeted therapies with fewer side effects compared to traditional drugs. More approvals of dermatology-focused veterinary biologics, including those targeting chronic skin allergies, further strengthen this segment. Additionally, dermatological issues are among the most common reasons for veterinary visits, ensuring steady demand. Growth in companion animal insurance coverage is also supporting the adoption of high-cost biologics. Overall, these factors position dermatology as the leading segment in the veterinary biologics market.

"North America has accounted for the largest market share in 2024."

North America held the largest market share in 2024, supported by a well-established veterinary healthcare infrastructure and high pet ownership rates. The region has a strong presence of leading market players investing in research and development for innovative monoclonal antibody therapies. Rising awareness about pet health, along with increasing spending on veterinary care, drives market growth. Additionally, the growing demand for premium pet care products further contributes to North America's dominance in the global veterinary monoclonal antibody industry.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-75%, Tier 2-15%, and Tier 3- 10%

- By Designation: C-level-30%, Director-level-23%, and Other Designations-47%

- By Region: North America-35%, Europe-20%, Asia Pacific-25%, Latin America-13%, and Middle East & Africa-7%

The major players operating in the veterinary biologics market are Zoetis (US), Elanco (US), and Merck & Co., Inc. (US).

Research Coverage

This report studies the veterinary biologics market based on animal type, route of administration, product, application, end user, and region. The report also examines factors such as drivers, restraints, opportunities, and challenges that affect market growth. It analyzes the opportunities and challenges within the market and provides details about the competitive landscape for market leaders. Additionally, the report analyzes micro markets in terms of their individual growth trends and forecasts the revenue of market segments across five main regions and their respective countries.

Reasons to Buy the Report

The report can help established firms, as well as new entrants/smaller firms, gauge the pulse of the market, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the five strategies mentioned below.

This report provides insights into the following points:

- Analysis of key drivers (Surge in companion animal population and pet ownership. Increasing incidence of infectious zoonotic diseases, Innovations in monoclonal antibodies targeting infectious diseases, Supportive initiatives by government agencies and animal health organization, Growing demand for animal-derived food products), restraints (High cost of veterinary diagnostic tests, Regulatory hurdles and long approval timelines), opportunities (evolving landscape of strategic collaborations and partnerships, untapped growth potential in emerging markets, challenges (Limited Awareness and Shortage of Trained Veterinarians in Low-Income Countries.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the veterinary biologics market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of biologic treatments across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary biologics market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary biologics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary sources

- 2.1.2.2 Key objectives of primary research

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primaries

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 REVENUE SHARE ANALYSIS (BOTTOM-UP APPROACH)

- 2.2.2 EPIDEMIOLOGY-BASED APPROACH

- 2.2.3 COMPANY INVESTOR PRESENTATIONS AND PRIMARY INTERVIEWS

- 2.2.4 TOP-DOWN APPROACH

- 2.2.5 BOTTOM-UP APPROACH

- 2.3 MARKET GROWTH RATE PROJECTION

- 2.4 DATA TRIANGULATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 VETERINARY BIOLOGICS MARKET OVERVIEW

- 4.2 NORTH AMERICA: VETERINARY BIOLOGICS MARKET, BY ANIMAL TYPE AND COUNTRY

- 4.3 VETERINARY BIOLOGICS MARKET SHARE, BY PRODUCT TYPE, 2025 VS. 2030

- 4.4 VETERINARY BIOLOGICS MARKET, BY ANIMAL TYPE, 2025 VS. 2030 (USD MILLION)

- 4.5 VETERINARY BIOLOGICS MARKET, BY ROUTE OF ADMINISTRATION, 2025 VS. 2030 (USD MILLION)

- 4.6 VETERINARY BIOLOGICS MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- 4.7 VETERINARY BIOLOGICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Surge in companion animal population and pet ownership

- 5.2.1.2 Increasing incidence of infectious zoonotic diseases

- 5.2.1.3 Innovations in monoclonal antibodies targeting infectious diseases

- 5.2.1.4 Supportive initiatives by government agencies and animal health organizations

- 5.2.1.5 Rising demand for animal-derived food products

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of veterinary diagnostic tests

- 5.2.2.2 Regulatory hurdles and long approval timelines

- 5.2.2.3 Rising pet care costs

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Evolving landscape of strategic collaborations and acquisitions

- 5.2.3.2 Untapped growth potential in emerging economies

- 5.2.4 CHALLENGES

- 5.2.4.1 Limited awareness and shortage of trained veterinarians in low-income countries

- 5.2.4.2 Stringent regulatory requirements for licensing veterinary biologics

- 5.2.1 DRIVERS

- 5.3 TECHNOLOGY ANALYSIS

- 5.3.1 KEY TECHNOLOGIES

- 5.3.1.1 Hybridoma technology

- 5.3.1.2 Biosensor-based diagnostic systems

- 5.3.2 COMPLEMENTARY TECHNOLOGIES

- 5.3.2.1 Long-acting injectables

- 5.3.2.2 Next-generation sequencing

- 5.3.3 ADJACENT TECHNOLOGIES

- 5.3.3.1 Wearable biosensors & remote monitoring devices

- 5.3.1 KEY TECHNOLOGIES

- 5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA FOR HS CODE 300214, 2021-2024

- 5.6.2 EXPORT DATA FOR HS CODE 300214, 2021-2024

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 THREAT OF SUBSTITUTES

- 5.7.3 BARGAINING POWER OF SUPPLIERS

- 5.7.4 BARGAINING POWER OF BUYERS

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.8.2 KEY BUYING CRITERIA

- 5.9 REGULATORY ANALYSIS

- 5.9.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.2 REGULATORY FRAMEWORK

- 5.9.2.1 North America

- 5.9.2.2 Europe

- 5.9.2.3 Asia Pacific

- 5.9.2.4 Latin America

- 5.9.2.5 Middle East & Africa

- 5.10 PATENT ANALYSIS

- 5.10.1 PATENT PUBLICATION TREND

- 5.10.2 JURISDICTION AND TOP APPLICANT ANALYSIS

- 5.10.3 INNOVATIONS AND PATENT REGISTRATIONS

- 5.11 PRICING ANALYSIS

- 5.11.1 INDICATIVE PRICE OF VETERINARY MONOCLONAL ANTIBODIES, BY KEY PLAYER, 2024

- 5.11.2 INDICATIVE PRICE OF VETERINARY MONOCLONAL ANTIBODIES, BY REGION, 2022-2024

- 5.12 KEY CONFERENCES & EVENTS, 2025-2026

- 5.13 ECOSYSTEM ANALYSIS

- 5.13.1 ROLE IN ECOSYSTEM

- 5.14 REIMBURSEMENT ANALYSIS

- 5.15 UNMET NEEDS

- 5.16 IMPACT OF AI/GEN AI ON VETERINARY BIOLOGICS MARKET

- 5.16.1 POTENTIAL OF AI IN VETERINARY BIOLOGICS

- 5.16.2 AI USE CASES

- 5.16.3 KEY COMPANIES IMPLEMENTING AI

- 5.17 INVESTMENT & FUNDING SCENARIO

- 5.18 PIPELINE ANALYSIS

- 5.19 IMPACT OF 2025 US TARIFF ON VETERINARY BIOLOGICS MARKET

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.4 IMPACT ON COUNTRY/REGION

- 5.19.5 IMPACT ON END-USE INDUSTRIES

- 5.19.5.1 Veterinary hospitals & clinics

- 5.19.5.2 Veterinary diagnostic labs

- 5.19.5.3 Other end users

6 VETERINARY BIOLOGICS MARKET, BY PRODUCT TYPE

- 6.1 INTRODUCTION

- 6.2 MONOCLONAL ANTIBODIES

- 6.2.1 INCREASED PET OWNERSHIP AND HUMANIZATION TO RAISE HEALTH AWARENESS AND SPENDING ON ANTIBODY THERAPIES

- 6.3 IMMUNOGLOBULINS & ANTITOXINS

- 6.3.1 INCREASED PREVALENCE OF ZOONOTIC AND TOXIN-MEDIATED DISEASES TO FUEL MARKET GROWTH

- 6.4 IMMUNOMODULATORS & IMMUNOSTIMULANTS

- 6.4.1 IMMUNOMODULATORS & IMMUNOSTIMULANTS TO CORRECT IMMUNE DYSFUNCTIONS AND CONTROL OVERACTIVE IMMUNE CONDITIONS

- 6.5 DIAGNOSTIC KITS

- 6.5.1 DIAGNOSTIC KITS TO IMPROVE DISEASE SURVEILLANCE AND MANAGEMENT IN COMPANION ANIMALS, LIVESTOCK, AND POULTRY

7 VETERINARY BIOLOGICS MARKET, BY ANIMAL TYPE

- 7.1 INTRODUCTION

- 7.2 COMPANION ANIMALS

- 7.2.1 CANINE

- 7.2.1.1 Widespread ownership of pet dogs to generate consistent demand for preventive care and advanced biologics

- 7.2.2 FELINE

- 7.2.2.1 Rising pet cat population and increasing feline diseases to propel market growth

- 7.2.1 CANINE

- 7.3 LIVESTOCK ANIMALS

- 7.3.1 BOVINE

- 7.3.1.1 Need for better herd healthcare and introduction of antibody-based biologics to fuel segment growth

- 7.3.2 SMALL RUMINANT

- 7.3.2.1 Increasing global demand for sheep & goat meat and expanding herd size to boost market growth

- 7.3.3 PORCINE

- 7.3.3.1 Innovation in monoclonal antibodies for infectious diseases to drive market

- 7.3.4 POULTRY

- 7.3.4.1 Rising frequency of poultry diseases to augment market growth for better poultry health and improved food security

- 7.3.5 EQUINE

- 7.3.5.1 Equestrian sports, recreational riding, and managing failure of passive transfer (FPT) in foals to drive market

- 7.3.1 BOVINE

8 VETERINARY BIOLOGICS MARKET, BY ROUTE OF ADMINISTRATION

- 8.1 INTRODUCTION

- 8.2 INJECTABLE ROUTE OF ADMINISTRATION

- 8.2.1 SUBCUTANEOUS ROUTE OF ADMINISTRATION

- 8.2.1.1 Ease of administration, reduced pain, and lower risk of tissue damage to aid market growth

- 8.2.2 INTRAMUSCULAR ROUTE OF ADMINISTRATION

- 8.2.2.1 Better immune response and lower rate of injection-site reactions to fuel market growth

- 8.2.3 INTRAVENOUS ROUTE OF ADMINISTRATION

- 8.2.3.1 Rapid action and targeted therapy to drive adoption of intravenous biologics

- 8.2.4 OTHER INJECTABLE ROUTES OF ADMINISTRATION

- 8.2.1 SUBCUTANEOUS ROUTE OF ADMINISTRATION

- 8.3 ORAL ROUTE OF ADMINISTRATION

- 8.3.1 EASE OF ADMINISTRATION AND COST-EFFECTIVENESS TO FOCUS ON LARGE-SCALE, NON-INVASIVE ORAL DELIVERY

- 8.4 OTHER ROUTES OF ADMINISTRATION

9 VETERINARY BIOLOGICS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 DERMATOLOGY

- 9.2.1 PREVALENCE OF CHRONIC SKIN CONDITIONS TO AUGMENT VETERINARY DERMATOLOGY MARKET GROWTH

- 9.3 DIAGNOSTIC TESTING

- 9.3.1 RISING PREVALENCE OF ZOONOTIC AND VIRAL DISEASES TO INCREASE DEMAND FOR BIOLOGIC-BASED DIAGNOSTIC TOOLS

- 9.4 PAIN MANAGEMENT

- 9.4.1 NEED FOR NON-OPIOID, SIDE-EFFECT-FREE PAIN SOLUTIONS AMONG PET OWNERS TO DRIVE MARKET

- 9.5 INFECTIOUS DISEASE PREVENTION

- 9.5.1 RISING INCIDENCE OF ZOONOTIC DISEASES AND ACUTE INFECTIONS TO ACCELERATE USE OF VETERINARY BIOLOGICS

- 9.6 ONCOLOGY

- 9.6.1 FOCUS ON IMMUNE-TARGETED CONTROL OF AGGRESSIVE CANCEROUS TUMORS TO AID MARKET GROWTH

- 9.7 OTHER APPLICATIONS

10 VETERINARY BIOLOGICS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 VETERINARY HOSPITALS & CLINICS

- 10.2.1 INCREASE IN VETERINARY SPECIALISTS AND RISE IN PET OWNERSHIP TO PROPEL MARKET GROWTH

- 10.3 VETERINARY DIAGNOSTIC LABS

- 10.3.1 VETERINARY DIAGNOSTIC LABS TO BECOME ESSENTIAL IN DISEASE DETECTION WITH PREVENTIVE BIOLOGIC INTERVENTIONS

- 10.4 OTHER END USERS

11 VETERINARY BIOLOGICS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 US

- 11.2.2.1 US to dominate North American veterinary biologics market during forecast period

- 11.2.3 CANADA

- 11.2.3.1 Ongoing developments in veterinary monoclonal antibodies and increasing animal health expenditure to fuel market growth

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 GERMANY

- 11.3.2.1 Established veterinary infrastructure and innovation funding to provide favorable environment for biologics adoption

- 11.3.3 UK

- 11.3.3.1 Strong regulatory framework and high pet population to boost market growth

- 11.3.4 FRANCE

- 11.3.4.1 Increase in companion animal health spending by pet owners to propel market growth

- 11.3.5 ITALY

- 11.3.5.1 Better availability of pet products through large-scale outlets to augment market growth

- 11.3.6 SPAIN

- 11.3.6.1 Increased pet population and favorable government regulations to drive market

- 11.3.7 NETHERLANDS

- 11.3.7.1 Focus on meat export to positively influence veterinary biologics market

- 11.3.8 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 JAPAN

- 11.4.2.1 Growing consumption of animal-derived products to propel market growth

- 11.4.3 CHINA

- 11.4.3.1 Large pool of food-producing animals and high companion animal ownership to propel market growth

- 11.4.4 INDIA

- 11.4.4.1 Rising demand for dairy products to fuel market growth

- 11.4.5 AUSTRALIA

- 11.4.5.1 Rise in pet ownership to support increased spending on veterinary care

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Expanding pet care industry and increasing chronic veterinary diseases to drive market

- 11.4.7 NEW ZEALAND

- 11.4.7.1 Increased pet ownership and demand for advanced veterinary treatments to drive market

- 11.4.8 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 Large-scale livestock operations and strong veterinary infrastructure to drive market

- 11.5.3 MEXICO

- 11.5.3.1 Increasing demand for targeted biologics in livestock and pets to drive market growth

- 11.5.4 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 11.6.2 GCC COUNTRIES

- 11.6.2.1 Kingdom of Saudi Arabia (KSA)

- 11.6.2.1.1 Technology advancements in veterinary diagnostics to boost demand

- 11.6.2.2 United Arab Emirates (UAE)

- 11.6.2.2.1 Favorable government support to drive market

- 11.6.2.3 Rest of GCC Countries

- 11.6.2.1 Kingdom of Saudi Arabia (KSA)

- 11.6.3 REST OF MIDDLE EAST & AFRICA

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN VETERINARY BIOLOGICS MARKET

- 12.3 REVENUE ANALYSIS, 2022-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.4.1 VETERINARY BIOLOGICS MARKET SHARE ANALYSIS

- 12.4.2 US: VETERINARY BIOLOGICS MARKET SHARE ANALYSIS, 2024

- 12.4.3 VETERINARY DIAGNOSTICS KITS MARKET SHARE ANALYSIS

- 12.4.4 US: VETERINARY DIAGNOSTIC KITS MARKET SHARE ANALYSIS, 2024

- 12.5 RANKING OF KEY PLAYERS

- 12.5.1 VETERINARY BIOLOGICS MARKET RANKING

- 12.5.2 VETERINARY DIAGNOSTIC KITS MARKET RANKING

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.6.5.1 Company footprint

- 12.6.5.2 Region footprint

- 12.6.5.3 Product type footprint

- 12.6.5.4 Animal type footprint

- 12.6.5.5 Application footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.7.5.1 Detailed list of key startup/SMEs

- 12.7.5.2 Competitive benchmarking of key startups/SMEs

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 COMPANY VALUATION & FINANCIAL METRICS

- 12.9.1 FINANCIAL METRICS

- 12.9.2 COMPANY VALUATION

- 12.10 COMPETITIVE SCENARIO

- 12.10.1 PRODUCT LAUNCHES & APPROVALS

- 12.10.2 DEALS

- 12.10.3 EXPANSIONS

- 12.10.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 ZOETIS SERVICES LLC

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches & approvals

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.3.4 Other developments

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 IDEXX

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 ELANCO

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 MERCK & CO., INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 THERMO FISHER SCIENTIFIC INC.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Right to win

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses & competitive threats

- 13.1.6 BOEHRINGER INGELHEIM INTERNATIONAL GMBH

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Deals

- 13.1.6.3.2 Expansions

- 13.1.7 NEOGEN CORPORATION

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.8 BIO-RAD LABORATORIES, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.9 IMMUCELL CORPORATION

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Other developments

- 13.1.10 INNOVATIVE DIAGNOSTICS

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.1 ZOETIS SERVICES LLC

- 13.2 OTHER PLAYERS

- 13.2.1 BIONOTE USA INC.

- 13.2.2 BIOCHEK

- 13.2.3 PLASVACC USA

- 13.2.4 NOVAVIVE INC.

- 13.2.5 MG BIOLOGICS

- 13.2.6 STALLERGENES GREER

- 13.2.7 BIOSTONE ANIMAL HEALTH

- 13.2.8 COLORADO SERUM COMPANY

- 13.2.9 PADULA SERUMS PTY LTD.

- 13.2.10 LAKE IMMUNOGENICS

- 13.2.11 INBIOS INTERNATIONAL, INC.

- 13.2.12 PRINCETON BIOMEDITECH CORPORATION

- 13.2.13 TETRACORE, INC.

- 13.2.14 VMRD, INC.

- 13.2.15 ANIMAB

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 AVAILABLE CUSTOMIZATIONS

- 14.3.1 GEOGRAPHIC ANALYSIS

- 14.3.2 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 14.3.3 COMPANY INFORMATION

- 14.3.4 PRODUCT ANALYSIS

- 14.3.5 COUNTRY-LEVEL VOLUME ANALYSIS

- 14.3.6 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 14.3.7 BY PRODUCT TYPE MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS