|

시장보고서

상품코드

1887993

벡터 데이터베이스 시장(-2030년) : 벡터 데이터베이스 솔루션(벡터 생성 및 인덱싱, 벡터 검색 및 쿼리 처리, 벡터 저장 및 검색), AI 언어 처리, 컴퓨터 비전, 추천 시스템별Vector Database Market By Vector Database Solution (Vector Generation & Indexing, Vector Search & Query Processing, Vector Storage & Retrieval), AI Language Processing, Computer Vision, Recommendation Systems - Global Forecast to 2030 |

||||||

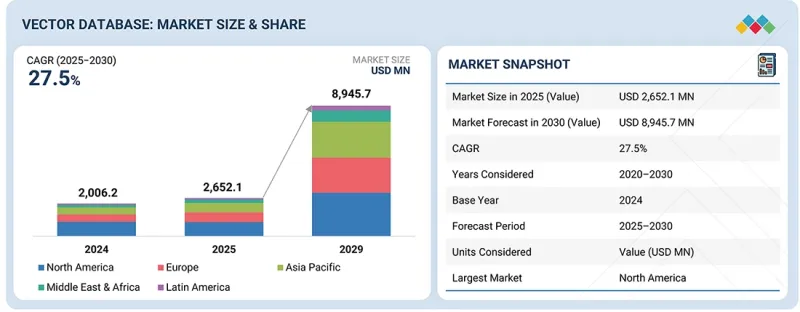

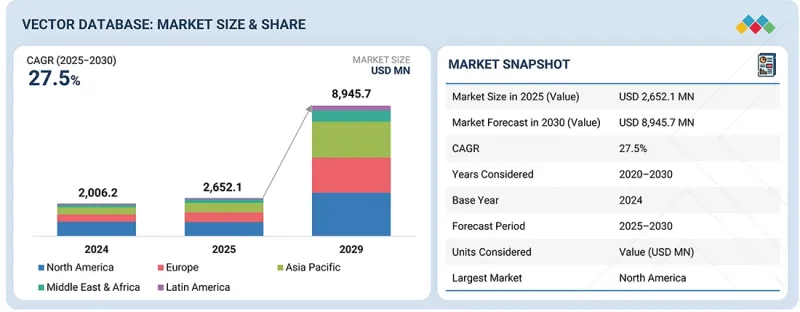

세계의 벡터 데이터베이스 시장 규모는 예측 기간 동안 CAGR 27.5%로 성장하여 2025년 26억 5,210만 달러에서 2030년까지 89억 4,570만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2030년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 가치(달러) |

| 부문 | 제공 구분, 유형, 기술 및 AI 용도, 도입 형태, 데이터 유형, 산업 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동, 아프리카, 라틴아메리카 |

AI, 멀티모달 모델, 실시간 용도 도입이 확대됨에 따라 세계 기업의 고급 벡터 데이터베이스에 대한 수요가 가속화되고 있습니다. 조직은 추천 엔진, RAG 파이프라인, 사기 감지, 개인화된 사용자 경험을 제공하기 위해 고성능 벡터 검색, 효율적인 인덱싱 및 저지연 검색 기능에 대한 투자를 강화하고 있습니다. 이러한 시스템은 현대 AI 워크로드에 필수적인 확장성 향상, 추론 속도 향상, 복잡한 임베디드 데이터 지원을 제공합니다.

그러나 많은 기업들이 기존의 관계형 데이터베이스와 문서 데이터베이스에 의존하는 것은 여전히 제약 요인이 되고 있습니다. 많은 기업들은 벡터 워크로드를 효율적으로 실행하는 능력을 제한하는 레거시 아키텍처를 계속 운영하고 있습니다. 벡터 네이티브 시스템으로의 전환에는 대규모 재설계, 임베디드 파이프라인 구축, 통합 작업이 필요하며 비용과 구현 복잡성이 주요 과제가 되었습니다. AI 도입이 확대됨에 따라 수요는 계속 급증하고 있지만, 레거시 데이터 인프라의 전환은 벡터 데이터베이스 시장 성장의 주요 장벽 중 하나입니다.

"데이터 유형별로는 하이브리드 및 멀티모달이 2025년 최대 시장 점유율을 차지할 전망"

하이브리드 및 멀티모달 데이터는 벡터 데이터베이스 시장의 최첨단 분야 중 하나로, 텍스트, 이미지, 음성, 동영상, 구조화된 데이터와 같은 다양한 데이터 유형을 통합된 검색 및 획득 프레임워크 내에서 원활하게 통합 및 분석할 수 있습니다. 벡터 데이터베이스는 각 모달리티를 공유 또는 비교 가능한 벡터 공간에서 포함된 표현으로 변환합니다. 이렇게 하면 텍스트 설명과 관련된 이미지를 검색하고 음성 스니펫과 일치하는 동영상을 캡처하는 것과 같은 크로스 모달 쿼리가 가능합니다. 이 기능은 멀티모달 검색 엔진, AI 코파일럿, 다양한 포맷에 걸친 컨텍스트 이해에 의존하는 개인화된 추천 시스템 등의 용도를 지원합니다. 하이브리드 데이터 처리는 기존의 구조화된 검색과 키워드 기반 검색과 벡터 유사성을 결합하여 정확도와 의미심도를 모두 보장합니다. 예를 들어, 기업은 메타데이터 필터링과 의미 검색을 융합하여 컨텍스트가 풍부하고 설명 가능한 결과를 생성할 수 있습니다. 크고 복잡한 벡터에 최적화된 HNSW 및 디스크 기반 스토리지 아키텍처와 같은 확장 가능한 인덱싱 및 검색 메커니즘을 통해 멀티모달 임베디드를 효율적으로 처리할 수 있습니다. AI 모델이 언어와 시각을 융합시키는 경향이 강해지는 가운데(예 : CLIP, GPT-4V), 벡터 데이터베이스는 동적인 멀티모달 데이터 파이프라인을 지원하는 방향으로 진화하고 있습니다. 이 통합은 전자상거래, 미디어, 의료 등 다양한 분야의 혁신을 촉진하여 종합적이고 지적인 데이터 상호작용과 발견을 가능하게 합니다.

"기술 유형별로는 컴퓨터 비전 분야가 예측 기간 동안 가장 높은 CAGR을 나타낼 전망"

컴퓨터 비전은 이미지나 동영상 등의 시각 데이터를 기계가 해석 및 분석하고 거기에서 지견을 도출할 수 있게 함으로써 벡터 데이터베이스의 기능 확장에 있어 매우 중요한 역할을 합니다. 이미지 및 동영상 임베디드 기술을 활용함으로써 시각 입력은 의미를 포착한 고차원 벡터로 변환되어 벡터 데이터베이스는 메타데이터나 라벨이 아닌 컨텐츠를 기반으로 유사성 검색을 수행할 수 있습니다. 이 변환은 비주얼 추천 엔진, 이미지 검색, 자동 태깅 시스템과 같은 애플리케이션을 제공합니다. 또 다른 중요한 구성 요소인 물체 검출은 시각 프레임 내의 물체를 식별 및 분류함으로써 컴퓨터 비전의 분석 정밀도를 높여 실시간 감시, 방범 감시, 산업 자동화 등의 이용 사례를 지원합니다. 이 외에도 벡터 데이터베이스의 컴퓨터 비전은 얼굴 인식, 비정상 감지, 장면 이해와 같은 고급 애플리케이션을 지원하며 의미 적으로 유사한 시각 데이터를 검색하는 능력이 분석을 가속화합니다. 컴퓨터 비전과 벡터 데이터베이스를 통합하면 텍스트와 시각적 쿼리가 공존하는 멀티모달 검색이 가능해져 사용자 상호작용과 AI 워크플로우가 향상됩니다. 딥러닝 모델과 확장 가능한 벡터 인덱스를 결합함으로써 조직은 엄청난 양의 비구조화된 시각적 컨텐츠를 효율적으로 처리할 수 있어 소매, 의료, 자율 시스템, 디지털 미디어 분석 등 다양한 분야에서 혁신을 가져올 수 있습니다.

"지역별로는 북미가 시장 점유율로 주도적 입장을 유지하는 한편 아시아태평양이 가장 빠르게 성장하는 시장으로 대두"

북미는 벡터 데이터베이스의 최대 시장으로, AI 워크로드의 급속한 배포, 대규모 기업 현대화, 클라우드 및 하이퍼스케일 플랫폼의 이점에 의해 견인되고 있습니다. 미국과 캐나다에서는 고성능 벡터 검색과 확장 가능한 임베디드 스토리지를 필요로 하는 멀티모달 AI, 실시간 분석, RAG 기반 용도에 많은 투자가 이루어지고 있습니다. 성숙한 디지털 에코시스템, 광범위한 GPU 인프라, 엔터프라이즈급 벡터 솔루션의 조기 도입이 이 지역의 주도적 입장을 더욱 강화하고 있습니다.

한편, 아시아태평양은 중국, 인도, 일본, 한국, 싱가포르 등에서 디지털 전환의 가속화로 가장 급속한 성장을 이루고 있습니다. AI를 활용한 개인화, 전자상거래 인텔리전스, 핀테크 사기 감지, 자율 시스템에 대한 수요 급증이 확장 가능하고 비용 효율적인 벡터 검색 플랫폼의 도입을 촉진하고 있습니다. 정부 주도의 AI 혁신 시책, 클라우드 인프라의 확충, 스타트업 활동의 활성화가 도입을 더욱 뒷받침하고, 이 지역은 고성장 벡터 데이터베이스 기술의 중요한 거점으로 자리매김하고 있습니다.

본 보고서에서는 세계의 벡터 데이터베이스 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- 미충족 요구와 화이트 스페이스

- 관련 시장 및 이업종과의 분야 횡단적 기회

- 새로운 비즈니스 모델과 생태계의 변화

- Tier 1/2/3 기업의 전략적 움직임

제6장 업계 동향

- Porter's Five Forces 분석

- 거시경제지표

- 공급망 분석

- 생태계 분석

- 가격 분석

- 2026년 주요 컨퍼런스 및 이벤트

- 고객의 비즈니스에 영향을 미치는 동향/혁신

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향 - 벡터 데이터베이스 시장

제7장 기술의 진보 : AI에 의한 영향, 특허, 혁신

- 주요 신기술

- 임베디드 모델(텍스트, 이미지, 음성, 멀티모달)

- 근사 최근접 이웃(ANN) 탐색 알고리즘

- 벡터 인덱스 및 스토리지 엔진

- GPU 및 AI 가속기

- 보완적 기술

- 대규모 언어 모델(LLMS)

- 검색 확장 생성(RAG) 프레임워크

- 데이터 오케스트레이션 및 ETL 파이프라인

- 기술/제품 로드맵

- 특허 분석

- AI/생성형 AI가 벡터 데이터베이스 시장에 미치는 영향

제8장 규제 상황

- 지역 규제 및 규정 준수

제9장 고객정세와 구매행동

- 의사결정 프로세스

- 구매 프로세스에 참여하는 주요 이해관계자와 그 평가 기준

- 채용 장벽과 내부 과제

- 다양한 최종 사용자 산업에서의 미충족 요구

제10장 벡터 데이터베이스 시장 : 유형별

- 네이티브 벡터 DBS

- 멀티모달 벡터 DBS

제11장 벡터 데이터베이스 시장 : 제공 구분별

- 벡터 데이터베이스 솔루션

- 벡터 생성 및 인덱싱

- 벡터 검색 및 쿼리 처리

- 벡터 저장 및 검색

- 서비스

- 전문 서비스

- 매니지드 서비스

제12장 벡터 데이터베이스 시장 : 기술 및 AI 용도별

- 자연어 처리

- 시맨틱 검색

- 텍스트 포함

- 감정 분석

- 채팅봇과 가상 어시스턴트

- 기타

- 컴퓨터 비전

- 이미지 및 동영상 포함

- 물체 검출

- 기타

- 추천 시스템

- 협조 필터링

- 컨텐츠 기반 필터링

- 세션 기반 추천

- 기타

- 기타(그래프 확장 검색 및 음성 및 연설)

제13장 벡터 데이터베이스 시장 : 도입 유형별

- 클라우드

- On-Premise

제14장 벡터 데이터베이스 시장 : 데이터 유형별

- 간단한 텍스트 데이터

- 하이브리드 및 멀티 모달 데이터

- 고급 데이터

제15장 벡터 데이터베이스 시장 : 산업별

- BFSI

- 소매 및 E커머스

- 헬스케어 및 생명과학

- IT 및 ITES

- 미디어 및 엔터테인먼트

- 제조 및 IIoT

- 정부 및 방위

- 자동차 및 운송

- 기타

제16장 벡터 데이터베이스 시장 : 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 중국

- 일본

- 호주 및 뉴질랜드

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타

- 라틴아메리카

- 브라질

- 멕시코

- 기타

제17장 경쟁 구도

- 주요 진입기업의 전략/강점

- 수익 분석

- 시장 점유율 분석

- 제품 비교

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업/중소기업

- 기업평가와 재무지표

- 경쟁 시나리오

제18장 기업 프로파일

- 주요 기업

- MICROSOFT

- ELASTIC

- MONGODB

- AWS

- REDIS

- ALIBABA CLOUD

- DATASTAX

- SINGLESTORE

- PINECONE

- 기타 기업

- ZILLIZ

- KX

- MARQO.AI

- ACTIVELOOP

- SUPABASE

- JINA AI

- TYPESENSE

- GSI TECHNOLOGY

- KINETICA

- QDRANT

- WEAVIATE

- CLICKHOUSE

- OPENSEARCH

- VESPA.AI

- LANCEDB

제19장 인접 시장/관련 시장

제20장 부록

JHS 25.12.26The global vector database market is projected to grow from USD 2,652.1 million in 2025 to USD 8,945.7 million by 2030, at a compound annual growth rate (CAGR) of 27.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2025 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) |

| Segments | By Offering, By Type, By Technology/AI Application, By Deployment Type, By Data Type, By Vertical |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and Latin America |

The rising adoption of AI, multimodal models, and real-time applications is accelerating the demand for advanced vector databases among global enterprises. Organizations are increasingly investing in high-performance vector search, efficient indexing, and low-latency retrieval to power recommendation engines, RAG pipelines, fraud detection, and personalized user experiences. These systems enhance scalability, improve inference speed, and support complex embeddings, which are essential for modern AI workloads.

However, reliance on traditional relational and document databases remains a restraint, as many enterprises still operate legacy architectures that limit the ability to run vector workloads efficiently. Migrating to vector-native systems requires significant re-engineering, embedding pipelines, and integration efforts, making both cost and implementation complexity key challenges. While demand continues to surge with the expansion of AI adoption, the transition from legacy data infrastructure remains one of the primary barriers to the growth of the vector database market.

"Based on data type, the hybrid & multimodal is estimated to hold the largest market share in 2025"

Hybrid and multimodal data represent one of the most advanced frontiers of the vector database market, enabling seamless integration and analysis of diverse data types-text, images, audio, video, and structured inputs-within a unified search and retrieval framework. Vector databases transform each modality into embeddings within a shared or comparable vector space, enabling cross-modal queries such as finding images relevant to a text description or retrieving videos that match an audio snippet. This capability powers applications such as multimodal search engines, AI copilots, and personalized recommendation systems that rely on contextual understanding across various formats. Hybrid data processing also combines traditional structured or keyword-based search with vector similarity, ensuring both precision and semantic depth. For instance, an enterprise can blend metadata filtering with semantic retrieval to produce context-rich, explainable results. The ability to handle multimodal embeddings efficiently is made possible through scalable indexing and retrieval mechanisms, such as HNSW or disk-based storage architectures, which are optimized for large and complex vectors. As AI models increasingly fuse language and vision (e.g., CLIP, GPT-4V), vector databases are evolving to support dynamic, multimodal data pipelines. This integration drives innovation across various sectors, including e-commerce, media, and healthcare, enabling holistic and intelligent data interaction and discovery.

"Based on technology type, the computer vision segment is expected to grow at the highest CAGR during the forecast period."

Computer vision plays a pivotal role in expanding the capabilities of vector databases by enabling machines to interpret, analyze, and derive insights from visual data such as images and videos. Through the use of image and video embeddings, visual inputs are transformed into high-dimensional vectors that capture semantic meaning, allowing vector databases to perform similarity searches based on content rather than metadata or labels. This transformation enables applications such as visual recommendation engines, image-based search, and automated tagging systems. Object detection, another key component, enhances the analytical precision of computer vision by identifying and classifying objects within visual frames, supporting real-time monitoring, surveillance, and industrial automation use cases. Beyond these, computer vision in vector databases underpins advanced applications such as facial recognition, anomaly detection, and scene understanding, where the ability to retrieve semantically similar visual data accelerates analysis. The integration of computer vision with vector databases enables multimodal search, where textual and visual queries coexist, thereby enriching user interaction and AI workflows. By combining deep learning models with scalable vector indexing, organizations can efficiently process massive volumes of unstructured visual content, driving breakthroughs across retail, healthcare, autonomous systems, and digital media analytics.

"North America will lead in terms of market share, while Asia Pacific will emerge as the fastest-growing market."

North America is the largest market for vector databases, driven by the rapid deployment of AI workloads, large-scale enterprise modernization, and the dominance of cloud and hyperscale platforms. The US and Canada are witnessing substantial investment in multimodal AI, real-time analytics, and RAG-based applications, which require high-performance vector search and scalable embedding storage. Mature digital ecosystems, extensive GPU infrastructure, and early adoption of enterprise-grade vector solutions further reinforce the region's leading position.

In contrast, the Asia Pacific represents the fastest-growing vector database market, driven by accelerated digital transformation in countries such as China, India, Japan, South Korea, and Singapore. Surging demand for AI-enabled personalization, e-commerce intelligence, fintech fraud detection, and autonomous systems is driving the adoption of scalable and cost-efficient vector search platforms. Government initiatives in AI innovation, the expansion of cloud infrastructure, and rising startup activity are further boosting uptake, positioning the APAC region as a significant hub for high-growth vector database technologies.

Breakdown of primaries

Chief Executive Officers (CEOs), directors of innovation and technology, system integrators, and executives from several significant companies in the vector database market were interviewed to gain insights into this market.

- By Company: Tier I: 40%, Tier II: 25%, and Tier III: 35%

- By Designation: C-Level Executives: 45%, Director Level: 30%, and Others: 25%

- By Region: North America: 30%, Europe: 20%, Asia Pacific: 25%, Rest of the World: 15%

Some of the significant vector database market vendors are Microsoft (US), Elastic (US), MongoDB (US), Google (US), AWS (US), Redis (US), Alibaba Cloud (US), DataStax (US), SingleStore (US), Pinecone (US), Zilliz (US), KX (US), Marqo.ai (US), ActiveLoop (US), Supabase (US), Jina AI (Germany), Typesense (US), Weaviate (Netherlands), GSI Technology (US), Kinetica (US), Qdrant (Germany), ClickHouse (US), OpenSearch(US), Vespa.ai (Norway), and LanceDB (US).

Research Coverage

The market report covered the vector database market across segments. We estimated the market size and growth potential for many segments based on offering, type, technology/AI application, deployment type, data type, vertical, and region. It contains a thorough competition analysis of the major market participants, information about their businesses, essential observations about their product and service offerings, current trends, and critical market strategies.

Reasons to buy this report:

This research provides the most accurate revenue estimates for the entire vector database industry and its subsegments, benefiting both established leaders and new entrants. Stakeholders will gain valuable insights into the competitive landscape, enabling them to position their companies better and develop effective go-to-market strategies. The report outlines key market drivers, constraints, opportunities, and challenges, helping industry players understand the current state of the market.

The report provides insights into the following pointers:

- Analysis of key drivers (explosion of unstructured and high-dimensional data), restraints (rapidly evolving AI and embedding models), opportunities (growing need for scalable storage and retrieval of LLM embeddings), and challenges (data privacy and security concerns) influencing the growth of the vector database market

- Product Development/Innovation: Comprehensive analysis of emerging technologies, R&D initiatives, and service and product introductions in the market

- Market Development: In-depth details regarding profitable markets, examining the global vector database market

- Market Diversification: Comprehensive details regarding recent advancements, investments, unexplored regions, and new solutions and services

- Competitive Assessment: Thorough analysis of the market shares, expansion plans, and offerings of the top competitors in the vector database industry, such as Microsoft (US), Elastic (US), MongoDB (US), Google (US), AWS (US), Redis (US), Alibaba Cloud (US), DataStax (US), SingleStore (US), Pinecone (US), Zilliz (US), KX (US), Marqo.ai (US), ActiveLoop (US), Supabase (US), Jina AI (Germany), Typesense (US), Weaviate (Netherlands), GSI Technology (US), Kinetica (US), Qdrant (Germany), ClickHouse (US), OpenSearch(US), Vespa.ai (Norway), and LanceDB (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary profiles

- 2.1.2.3 Key industry insights

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.3.3 MARKET ESTIMATION APPROACHES

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: STRATEGIC INSIGHTS

- 3.3 DISRUPTIVE TRENDS SHAPING MARKET

- 3.4 HIGH-GROWTH SEGMENTS

- 3.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN VECTOR DATABASE MARKET

- 4.2 VECTOR DATABASE MARKET, BY TYPE

- 4.3 VECTOR DATABASE MARKET, BY OFFERING

- 4.4 VECTOR DATABASE MARKET, BY VERTICAL

- 4.5 VECTOR DATABASE MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Explosion of unstructured and high-dimensional data

- 5.2.1.2 Demand for real-time search and personalization

- 5.2.1.3 Growing demand for solutions to process low-latency queries

- 5.2.1.4 Huge investments in vector databases

- 5.2.2 RESTRAINTS

- 5.2.2.1 High compute and storage costs

- 5.2.2.2 Rapidly evolving AI and embedding models

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing need for scalable storage and retrieval of LLM embeddings in AI workflows

- 5.2.3.2 Expansion of retrieval-augmented generation (RAG) to enable more accurate AI outputs

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of standardization across vector indexing techniques

- 5.2.4.2 Data privacy and security concerns

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN VECTOR DATABASES

- 5.3.2 WHITE SPACE OPPORTUNITIES

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 5.5.1 EMERGING BUSINESS MODELS

- 5.5.2 ECOSYSTEM SHIFTS

- 5.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

6 INDUSTRY TRENDS

- 6.1 PORTER'S FIVE FORCES ANALYSIS

- 6.1.1 THREAT OF NEW ENTRANTS

- 6.1.2 THREAT OF SUBSTITUTES

- 6.1.3 BARGAINING POWER OF SUPPLIERS

- 6.1.4 BARGAINING POWER OF BUYERS

- 6.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.2 MACROECONOMICS INDICATORS

- 6.2.1 INTRODUCTION

- 6.2.2 GDP TRENDS AND FORECAST

- 6.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 6.3 SUPPLY CHAIN ANALYSIS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE OF VECTOR DATABASE SOLUTIONS, BY REGION, 2025

- 6.5.2 INDICATIVE PRICING ANALYSIS OF VECTOR DATABASE SOLUTIONS, BY KEY PLAYER, 2025

- 6.6 KEY CONFERENCES AND EVENTS, 2026

- 6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.8 INVESTMENT AND FUNDING SCENARIO

- 6.9 CASE STUDY ANALYSIS

- 6.9.1 PINECONE ENABLED VANGUARD TO BOOST CUSTOMER SUPPORT WITH FASTER CALLS AND 12% MORE ACCURATE RESPONSES

- 6.9.2 L'OREAL IMPROVED APP PERFORMANCE AND VELOCITY WITH MONGODB ATLAS

- 6.9.3 FILEVINE AND ZILLIZ CLOUD: TRANSFORMING LEGAL CASE MANAGEMENT WITH VECTOR SEARCH

- 6.9.4 SUPERLINKED REVOLUTIONIZED PERSONALIZATION WITH REDIS ENTERPRISE'S VECTOR DATABASE

- 6.9.5 ELASTIC HELPED GLOBAL E-COMMERCE RETAILER ENHANCE PRODUCT DISCOVERY AND RECOMMENDATIONS

- 6.9.6 ELASTIC ENABLED SEMANTIC AND HYBRID SEARCH FOR GLOBAL FINANCIAL SERVICES PROVIDER

- 6.9.7 ELASTIC HELPED MAJOR TELECOM AND MEDIA PROVIDER ENHANCE CONTENT DISCOVERY

- 6.10 IMPACT OF 2025 US TARIFF - VECTOR DATABASE MARKET

- 6.10.1 INTRODUCTION

- 6.10.2 KEY TARIFF RATES

- 6.10.3 PRICE IMPACT ANALYSIS

- 6.10.4 IMPACT ON COUNTRY/REGION

- 6.10.4.1 North America

- 6.10.4.1.1 US

- 6.10.4.1.2 Canada

- 6.10.4.1.3 Mexico

- 6.10.4.2 Europe

- 6.10.4.2.1 Germany

- 6.10.4.2.2 France

- 6.10.4.2.3 UK

- 6.10.4.3 Asia Pacific

- 6.10.4.3.1 China

- 6.10.4.3.2 India

- 6.10.4.1 North America

7 TECHNOLOGICAL ADVANCEMENTS: AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 EMBEDDING MODELS (TEXT, IMAGE, AUDIO, MULTIMODAL)

- 7.1.2 APPROXIMATE NEAREST NEIGHBOR (ANN) SEARCH ALGORITHMS

- 7.1.3 VECTOR INDEXING AND STORAGE ENGINES

- 7.1.4 GPU AND AI ACCELERATORS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 LARGE LANGUAGE MODELS (LLMS)

- 7.2.2 RETRIEVAL-AUGMENTED GENERATION (RAG) FRAMEWORKS

- 7.2.3 DATA ORCHESTRATION AND ETL PIPELINES

- 7.3 TECHNOLOGY/PRODUCT ROADMAP

- 7.3.1 SHORT-TERM (2025-2027) | FOUNDATION & AI ALIGNMENT

- 7.3.2 MID-TERM (2027-2030) | STANDARDIZATION & ECOSYSTEM EXPANSION

- 7.3.3 LONG-TERM (2030-2035+) | MASS ADOPTION & INTELLIGENT RETRIEVAL

- 7.4 PATENT ANALYSIS

- 7.4.1 LIST OF MAJOR PATENTS

- 7.5 IMPACT OF AI/GENERATIVE AI ON VECTOR DATABASE MARKET

- 7.5.1 CASE STUDY

- 7.5.1.1 Automating CSR generation through retrieval-augmented generation (RAG)

- 7.5.2 VENDOR INITIATIVES

- 7.5.2.1 Zilliz expands to Azure North Europe, accelerating AI-powered vector search for European enterprises

- 7.5.2.2 Redis redefines vector database intelligence with Vector Sets, LangCache, and Featureform integration

- 7.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.5.1 CASE STUDY

8 REGULATORY LANDSCAPE

- 8.1 INTRODUCTION

- 8.2 REGIONAL REGULATIONS AND COMPLIANCE

- 8.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.2.2 REGULATIONS, BY REGION

- 8.2.2.1 North America

- 8.2.2.2 Europe

- 8.2.2.3 Asia Pacific

- 8.2.2.4 Middle East & Africa

- 8.2.2.5 Latin America

- 8.2.3 INDUSTRY STANDARDS

- 8.2.3.1 General Data Protection Regulation

- 8.2.3.2 SEC Rule 17a-4

- 8.2.3.3 ISO/IEC 27001

- 8.2.3.4 COBIT (Control Objectives for Information and Related Technologies)

- 8.2.3.5 ISA (International Society of Automation)

- 8.2.3.6 System and Organization Controls 2 Type II

- 8.2.3.7 Financial Industry Regulatory Authority

- 8.2.3.8 Freedom of Information Act

- 8.2.3.9 Health Insurance Portability and Accountability Act

9 CUSTOMER LANDSCAPE AND BUYING BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 9.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 9.2.2 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 9.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

10 VECTOR DATABASE MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 NATIVE VECTOR DBS

- 10.2.1 OPTIMIZED SINGLE-MODALITY VECTOR MANAGEMENT FUELS GROWTH IN VECTOR DATABASE MARKET

- 10.3 MULTIMODAL VECTOR DBS

- 10.3.1 MULTIMODAL VECTOR INTEGRATION ENHANCES DATA DIVERSITY, DRIVING VECTOR DATABASE MARKET GROWTH

11 VECTOR DATABASE MARKET, BY OFFERING

- 11.1 INTRODUCTION

- 11.2 VECTOR DATABASE SOLUTIONS

- 11.2.1 VECTOR GENERATION & INDEXING

- 11.2.1.1 Vector Generation & Indexing Enhances Speed and Precision in Data Processing

- 11.2.1.2 Embedding Models

- 11.2.1.3 Index Structures

- 11.2.2 VECTOR SEARCH & QUERY PROCESSING

- 11.2.2.1 Vector Search & Query Processing Enables Real-time, High-accuracy Information Retrieval

- 11.2.2.2 Approximate Nearest Neighbor (ANN)

- 11.2.2.3 Multimodal Search

- 11.2.2.4 Query Ranking & Scoring Optimization

- 11.2.3 VECTOR STORAGE & RETRIEVAL

- 11.2.3.1 Scalable Vector Storage & Retrieval Solutions Improve Performance and Data Accessibility

- 11.2.3.2 In-memory

- 11.2.3.3 Disk-based

- 11.2.3.4 Hybrid Storage

- 11.2.1 VECTOR GENERATION & INDEXING

- 11.3 SERVICES

- 11.3.1 PROFESSIONAL SERVICES

- 11.3.1.1 Professional Services Drives Effective Deployment and Customization of Vector Databases

- 11.3.1.2 Implementation & Integration

- 11.3.1.3 Training & Consulting

- 11.3.1.4 Support & Maintenance

- 11.3.2 MANAGED SERVICES

- 11.3.2.1 Managed Services Delivering Consistent Operations and Optimized Vector Database Management

- 11.3.1 PROFESSIONAL SERVICES

12 VECTOR DATABASE MARKET, BY TECHNOLOGY/AI APPLICATION

- 12.1 INTRODUCTION

- 12.2 NATURAL LANGUAGE PROCESSING

- 12.2.1 NATURAL LANGUAGE PROCESSING ENABLES PRECISE TEXT ANALYSIS AND FASTER CUSTOMER INTERACTIONS

- 12.2.2 SEMANTIC SEARCH

- 12.2.3 TEXT EMBEDDING

- 12.2.4 SENTIMENT ANALYSIS

- 12.2.5 CHATBOTS & VIRTUAL ASSISTANTS

- 12.2.6 OTHERS

- 12.3 COMPUTER VISION

- 12.3.1 COMPUTER VISION AUTOMATES VISUAL INSPECTION AND IMPROVES DETECTION ACCURACY

- 12.3.2 IMAGE/VIDEO EMBEDDING

- 12.3.3 OBJECT DETECTION

- 12.3.4 OTHERS

- 12.4 RECOMMENDATION SYSTEMS

- 12.4.1 RECOMMENDATION SYSTEMS PERSONALIZE OFFERS TO BOOST SALES AND USER ENGAGEMENT

- 12.4.2 COLLABORATIVE FILTERING

- 12.4.3 CONTENT-BASED FILTERING

- 12.4.4 SESSION-BASED RECOMMENDATIONS

- 12.4.5 OTHERS

- 12.5 OTHERS (GRAPH-AUGMENTED RETRIEVAL AND AUDIO & SPEECH)

13 VECTOR DATABASE MARKET, BY DEPLOYMENT TYPE

- 13.1 INTRODUCTION

- 13.2 CLOUD

- 13.2.1 CLOUD DEPLOYMENT DRIVES SCALABILITY AND COST EFFICIENCY FOR GROWING DATA NEEDS

- 13.3 ON-PREMISES

- 13.3.1 ON-PREMISES DEPLOYMENT ENSURES DATA CONTROL AND COMPLIANCE FOR SENSITIVE WORKLOADS

14 VECTOR DATABASE MARKET, BY DATA TYPE

- 14.1 INTRODUCTION

- 14.2 SIMPLE TEXT DATA

- 14.2.1 SIMPLE TEXT DATA ENABLES EFFICIENT PROCESSING OF LARGE-SCALE UNSTRUCTURED INFORMATION

- 14.3 HYBRID & MULTIMODAL DATA

- 14.3.1 HYBRID & MULTIMODAL DATA INTEGRATES DIVERSE FORMATS TO IMPROVE CONTEXTUAL SEARCH ACCURACY

- 14.4 ADVANCED DATA

- 14.4.1 ADVANCED DATA SUPPORTS COMPLEX ANALYTICS THROUGH RICH, HIGH-DIMENSIONAL INFORMATION

15 VECTOR DATABASE MARKET, BY VERTICAL

- 15.1 INTRODUCTION

- 15.2 BFSI

- 15.2.1 BFSI IMPROVES DATA-DRIVEN DECISION-MAKING THROUGH EFFICIENT SIMILARITY SEARCHES

- 15.2.2 BFSI: USE CASES

- 15.2.2.1 Fraud Detection

- 15.2.2.2 Credit Risk Assessment

- 15.2.2.3 Customer Support Automation

- 15.3 RETAIL & E-COMMERCE

- 15.3.1 RETAIL & E-COMMERCE ENHANCE PRODUCT DISCOVERY WITH SCALABLE VECTOR SEARCH

- 15.3.2 RETAIL & E-COMMERCE: USE CASES

- 15.3.2.1 Visual Search

- 15.3.2.2 Personalized Recommendations

- 15.3.2.3 Dynamic Pricing

- 15.4 HEALTHCARE & LIFE SCIENCES

- 15.4.1 HEALTHCARE & LIFE SCIENCES ACCELERATE COMPLEX DATA MATCHING FOR RESEARCH AND DIAGNOSTICS

- 15.4.2 HEALTHCARE & LIFE SCIENCES: USE CASES

- 15.4.2.1 Medical Imaging Retrieval

- 15.4.2.2 Genomic Sequence Matching

- 15.4.2.3 Clinical Trial Matching

- 15.5 IT & ITES

- 15.5.1 IT & ITES ENABLE FAST SEMANTIC CODE AND LOG RETRIEVAL FOR BETTER DEVELOPMENT AND SECURITY

- 15.5.2 IT & ITES: USE CASES

- 15.5.2.1 Code Search & Reuse

- 15.5.2.2 Intelligent Ticket Routing

- 15.5.2.3 Cybersecurity Threat Detection

- 15.6 MEDIA & ENTERTAINMENT

- 15.6.1 MEDIA & ENTERTAINMENT FACILITATE MULTIMODAL CONTENT SEARCH AND METADATA MANAGEMENT

- 15.6.2 MEDIA & ENTERTAINMENT: USE CASES

- 15.6.2.1 Content-based Video Recommendation

- 15.6.2.2 Automated Metadata Tagging

- 15.6.2.3 Copyright Infringement Detection

- 15.7 MANUFACTURING & IIOT

- 15.7.1 MANUFACTURING & IIOT SUPPORT REAL-TIME SENSOR DATA ANALYSIS FOR OPERATIONAL INSIGHTS

- 15.7.2 MANUFACTURING & IIOT: USE CASES

- 15.7.2.1 Predictive Maintenance

- 15.7.2.2 Quality Control

- 15.7.2.3 Supply Chain Optimization

- 15.8 GOVERNMENT & DEFENSE

- 15.8.1 GOVERNMENT & DEFENSE STRENGTHEN MULTISOURCE DATA FUSION FOR INTELLIGENCE APPLICATIONS

- 15.8.2 GOVERNMENT & DEFENSE: USE CASES

- 15.8.2.1 Intelligence Analysis

- 15.8.2.2 Surveillance and Object Recognition

- 15.8.2.3 Cybersecurity Monitoring

- 15.9 AUTOMOTIVE & TRANSPORTATION

- 15.9.1 AUTOMOTIVE & TRANSPORTATION ENHANCING SENSOR DATA PROCESSING FOR ADVANCED ANALYTICS

- 15.9.2 AUTOMOTIVE & TRANSPORTATION: USE CASES

- 15.9.2.1 Autonomous Vehicle Perception

- 15.9.2.2 Route Optimization

- 15.9.2.3 Predictive Maintenance

- 15.10 OTHER VERTICALS (EDUCATION & RESEARCH, ENERGY & UTILITIES, ROBOTICS)

16 VECTOR DATABASE MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.1.1 NORTH AMERICA

- 16.1.2 US

- 16.1.2.1 Government AI Initiatives and Expanding Data Ecosystems Accelerate US Vector Database Market Growth

- 16.1.3 CANADA

- 16.1.3.1 AI Infrastructure Expansion and Startup Innovation Drive Canada's Vector Database Market

- 16.2 EUROPE

- 16.2.1 UK

- 16.2.1.1 AI-led Research Transformation and Data Modernization Fuel UK's Vector Database Growth

- 16.2.2 GERMANY

- 16.2.2.1 AI Infrastructure Expansion and Retail Intelligence Accelerate Germany's Vector Database Market

- 16.2.3 FRANCE

- 16.2.3.1 Advancing AI-driven Retail Infrastructure to Propel France's Vector Database Adoption

- 16.2.4 ITALY

- 16.2.4.1 AI Infrastructure Expansion and Smart City Initiatives Propel Italy's Vector Database Potential

- 16.2.5 REST OF EUROPE

- 16.2.1 UK

- 16.3 ASIA PACIFIC

- 16.3.1 CHINA

- 16.3.1.1 National AI Strategy and Robotics Innovation Power Vector Database Growth in China

- 16.3.2 JAPAN

- 16.3.2.1 Rising AI Adoption in Healthcare Demand for Advanced Data Management Frameworks in Japan

- 16.3.3 AUSTRALIA & NEW ZEALAND

- 16.3.3.1 Neocloud Growth, Sovereign AI Projects, and GPU Clouds Expand Vector Database Demand in Australia & New Zealand

- 16.3.4 REST OF ASIA PACIFIC

- 16.3.1 CHINA

- 16.4 MIDDLE EAST & AFRICA

- 16.4.1 GCC COUNTRIES

- 16.4.1.1 KSA

- 16.4.1.1.1 Saudi Arabia Accelerates AI and Gaming Infrastructure, Boosting Demand for Vector Databases

- 16.4.1.2 UAE

- 16.4.1.2.1 UAE Accelerates AI-led Economic Shift With Expanding Vector Infrastructure

- 16.4.1.3 Rest of GCC Countries

- 16.4.1.1 KSA

- 16.4.2 SOUTH AFRICA

- 16.4.2.1 AI-powered Public Services Push South Africa Toward Advanced Vector Data Platforms

- 16.4.3 REST OF MIDDLE EAST & AFRICA

- 16.4.1 GCC COUNTRIES

- 16.5 LATIN AMERICA

- 16.5.1 BRAZIL

- 16.5.1.1 Strengthening Brazil's AI and Gaming Infrastructure Through Vector-centric Technologies

- 16.5.2 MEXICO

- 16.5.2.1 AI-driven Cultural and Healthcare Advances Strengthen Mexico's Vector Database Needs

- 16.5.3 REST OF LATIN AMERICA

- 16.5.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 INTRODUCTION

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 17.3 REVENUE ANALYSIS, 2020-2024

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.5 PRODUCT COMPARISON

- 17.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 17.6.1 STARS

- 17.6.2 EMERGING LEADERS

- 17.6.3 PERVASIVE PLAYERS

- 17.6.4 PARTICIPANTS

- 17.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.6.5.1 Company footprint

- 17.6.5.2 Region footprint

- 17.6.5.3 Offering footprint

- 17.6.5.4 Vertical footprint

- 17.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 17.7.1 PROGRESSIVE COMPANIES

- 17.7.2 RESPONSIVE COMPANIES

- 17.7.3 DYNAMIC COMPANIES

- 17.7.4 STARTING BLOCKS

- 17.7.5 COMPETITIVE BENCHMARKING: STARTUP/SMES, 2024

- 17.7.5.1 Detailed list of key startups/SMEs

- 17.7.5.2 Competitive benchmarking of key startups/SMEs

- 17.8 COMPANY VALUATION AND FINANCIAL METRICS

- 17.8.1 COMPANY VALUATION OF KEY VENDORS

- 17.8.2 FINANCIAL METRICS OF KEY VENDORS

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

18 COMPANY PROFILES

- 18.1 INTRODUCTION

- 18.2 MAJOR PLAYERS

- 18.2.1 MICROSOFT

- 18.2.1.1 Business overview

- 18.2.1.2 Products/Solutions/Services offered

- 18.2.1.3 Recent developments

- 18.2.1.3.1 Product launches/enhancements

- 18.2.1.3.2 Deals

- 18.2.1.4 MnM view

- 18.2.1.4.1 Right to win

- 18.2.1.4.2 Strategic choices

- 18.2.1.4.3 Weaknesses and competitive threats

- 18.2.2 ELASTIC

- 18.2.2.1 Business overview

- 18.2.2.2 Products/Solutions/Services offered

- 18.2.2.3 Recent developments

- 18.2.2.3.1 Product launches/enhancements

- 18.2.2.3.2 Deals

- 18.2.2.4 MnM view

- 18.2.2.4.1 Right to win

- 18.2.2.4.2 Strategic choices

- 18.2.2.4.3 Weaknesses and competitive threats

- 18.2.3 MONGODB

- 18.2.3.1 Business overview

- 18.2.3.2 Products/Solutions/Services offered

- 18.2.3.3 Recent developments

- 18.2.3.3.1 Product launches/enhancements

- 18.2.3.3.2 Deals

- 18.2.3.4 MnM view

- 18.2.3.4.1 Right to win

- 18.2.3.4.2 Strategic choices

- 18.2.3.4.3 Weaknesses and competitive threats

- 18.2.4 GOOGLE

- 18.2.4.1 Business overview

- 18.2.4.2 Products/Solutions/Services offered

- 18.2.4.3 Recent developments

- 18.2.4.3.1 Product launches/enhancements

- 18.2.4.3.2 Deals

- 18.2.4.4 MnM view

- 18.2.4.4.1 Right to win

- 18.2.4.4.2 Strategic choices

- 18.2.4.4.3 Weaknesses and competitive threats

- 18.2.5 AWS

- 18.2.5.1 Business overview

- 18.2.5.2 Products/Solutions/Services offered

- 18.2.5.3 Recent developments

- 18.2.5.3.1 Product launches/enhancements

- 18.2.5.3.2 Deals

- 18.2.5.4 MnM view

- 18.2.5.4.1 Right to win

- 18.2.5.4.2 Strategic choices

- 18.2.5.4.3 Weaknesses and competitive threats

- 18.2.6 REDIS

- 18.2.6.1 Business overview

- 18.2.6.2 Products/Solutions/Services offered

- 18.2.6.3 Recent developments

- 18.2.6.3.1 Product launches/enhancements

- 18.2.6.3.2 Deals

- 18.2.7 ALIBABA CLOUD

- 18.2.7.1 Business overview

- 18.2.7.2 Products/Solutions/Services offered

- 18.2.7.3 Recent developments

- 18.2.7.3.1 Product launches/enhancements

- 18.2.7.3.2 Deals

- 18.2.8 DATASTAX

- 18.2.8.1 Business overview

- 18.2.8.2 Products/Solutions/Services offered

- 18.2.8.3 Recent developments

- 18.2.8.3.1 Product launches/enhancements

- 18.2.8.3.2 Deals

- 18.2.9 SINGLESTORE

- 18.2.9.1 Business overview

- 18.2.9.2 Products/Solutions/Services offered

- 18.2.9.3 Recent developments

- 18.2.9.3.1 Deals

- 18.2.10 PINECONE

- 18.2.10.1 Business overview

- 18.2.10.2 Products/Solutions/Services offered

- 18.2.10.3 Recent developments

- 18.2.10.3.1 Product launches/enhancements

- 18.2.10.3.2 Deals

- 18.2.1 MICROSOFT

- 18.3 OTHER PLAYERS

- 18.3.1 ZILLIZ

- 18.3.2 KX

- 18.3.3 MARQO.AI

- 18.3.4 ACTIVELOOP

- 18.3.5 SUPABASE

- 18.3.6 JINA AI

- 18.3.7 TYPESENSE

- 18.3.8 GSI TECHNOLOGY

- 18.3.9 KINETICA

- 18.3.10 QDRANT

- 18.3.11 WEAVIATE

- 18.3.12 CLICKHOUSE

- 18.3.13 OPENSEARCH

- 18.3.14 VESPA.AI

- 18.3.15 LANCEDB

19 ADJACENT/RELATED MARKETS

- 19.1 INTRODUCTION

- 19.1.1 RELATED MARKETS

- 19.1.2 LIMITATIONS

- 19.2 GENERATIVE AI MARKET

- 19.3 NATURAL LANGUAGE PROCESSING (NLP) MARKET

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS