|

시장보고서

상품코드

1901400

회로차단기 시장 : 절연 유형별, 전압별, 설치 방법별, 용도별, 지역별 - 예측(-2030년)Circuit Breaker Market By Insulation Type, Voltage, Installation, End User, Region - Global Forecast to 2030 |

||||||

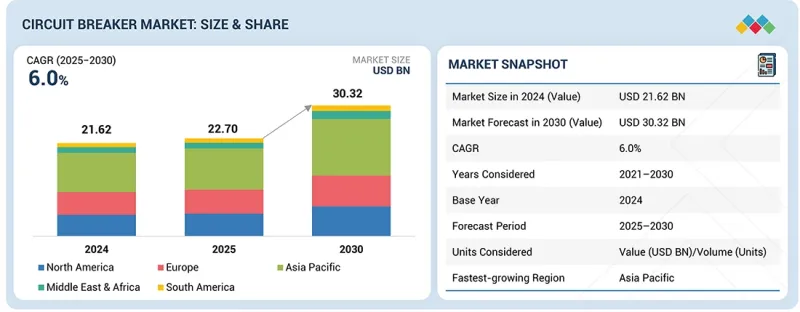

세계의 회로차단기 시장 규모는 2025년에 227억 달러로 평가되었고 2030년까지 303억 2,000만 달러에 이를 것으로 예측되며, 2025-2030 CAGR은 6.0%를 보일 전망입니다. 이 성장은 전력 신뢰성에 수요 증가, 주택 및 산업용도 전력 소비량 증가, 송전망 현대화 구상 확대에 의해서 촉진되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 가치(100만 달러)/수량(unit) |

| 부문 | 절연 유형별, 전압별, 설치 방법별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미 |

고전압 송전망의 개발이 급증하고 있으며, 스마트 변전소 및 재생에너지 인프라에 대한 투자가 세계 시장 수요를 가속화하고 있습니다. 또한, 노후화된 설비의 교체와 디지털 모니터링 및 지속가능성 목표를 지원하는 첨단 보호 시스템 도입에 대한 규제 압력도 시장 성장에 영향을 미치고 있습니다.

절연 유형별로는 공기 절연 부문이 예측 기간 동안 회로 차단기 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이러한 성장은 특히 상업용 건물, 가정용 전력 연결 및 산업용 제어반의 저압 배전 시스템에 대한 광범위한 도입에 기인합니다. 도시 개발 증가, 상업 건설 프로젝트, 시설 내 안전한 전력 분배에 대한 강한 강조는 공기 회로 차단기에 대한 수요를 촉진하고 있습니다. 또한, 공압식 시스템은 높은 유지보수성 및 비용 측면에서 우위를 가지고 있어 계약자 및 최종 사용자에게 더 선호되는 선택이 되고 있습니다. 스마트 빌딩 인프라의 보급이 확산되는 가운데, 모니터링 기능과 아크 보호 기술을 탑재한 저전압 공압식 차단기가 시장 확대를 견인할 것으로 예측됩니다.

송배전 사업자는 전력망의 급속한 현대화와 재생에너지 통합을 지원하는 변전소의 대규모 증설을 배경으로 회로 차단기 시장에서 가장 큰 비중을 차지하고 있습니다. 각국 정부는 풍력, 태양광, 에너지 저장 시설로 인한 변동 부하를 관리하기 위해 신뢰성이 높은 대용량 네트워크에 대한 투자를 우선시하고 있으며, 이는 중전압 및 고전압 회로 차단기 설치 증가로 이어지고 있습니다. 또한, 개발도상국의 전기화율 증가와 미국, 유럽 연합과 같은 성숙한 시장에서의 노후화된 송전망의 갱신도 채택을 촉진하고 있습니다. 전력망 사업자들은 또한 고장 대응 시간을 개선하기 위해 스마트하고 자동화된 개폐 시스템으로 전환하고 있으며, 디지털화 및 예지보전 기능을 갖춘 회로 차단기 솔루션에 대한 수요가 증가하고 있습니다.

아시아태평양에서는 중국, 인도, 한국, 일본 등 국가의 대규모 산업화, 도시 지역의 높은 에너지 수요, 지속적인 전기화 추진 정책의 결과로 회로 차단기 시장이 빠르게 성장하고 있으며, 유럽, 북미가 그 뒤를 잇고 있습니다. 재생 에너지에 대한 대규모 투자와 전력망 용량 증설로 인해 고압 및 중압 회로 차단기 수요가 증가하고 있습니다. 상업용 빌딩, 지하철 프로젝트, EV 인프라, 제조 시설의 확장은 시장 가속화에 더욱 기여하고 있습니다. 유럽에서는 SF6 프리 기술을 촉진하는 지속가능성 규제에 힘입어 진전을 보이고 있습니다. 북미에서는 특히 미국의 데이터센터 지원과 청정 에너지 통합을 촉진하기 위한 전력망 현대화 노력이 성장에 영향을 미치고 있습니다.

조사 방법에 대한 자세한 내용:

주요 업계 관계자, 전문 지식을 보유한 전문가, 주요 시장 진출기업의 경영진, 업계 컨설턴트, 기타 관련 전문가 등 다양한 대상에 대한 1차 인터뷰를 실시하였습니다. 이 인터뷰는 중요한 정성적, 정량적 정보를 수집 및 검증하고 시장 전망을 평가하기 위해 실시되었습니다.

조사 범위:

이 보고서는 여러 지역을 포괄하는 회로 차단기 시장에 대한 종합적인 개요를 제공합니다. 그 목적은 절연 유형별, 전압별, 설치 방법별, 용도별, 지역별 등 다양한 부문 시장 규모를 추정하고 향후 성장 가능성을 평가하는 데 있습니다. 또한, 주요 시장 진입업체에 대한 상세한 경쟁 분석과 함께 각 업체의 기업 프로파일, 최근 동향, 주요 시장 전략에 대한 내용을 담고 있습니다. 시장은 절연 유형, 전압, 설치 방법, 용도, 지역별로 세분화되어 있으며, 업계 동향 분석에 중점을 두고 있습니다. 이 보고서는 주요 기업의 시장 점유율 분석, 공급망 분석, 기업 프로파일을 제공하며, 이를 종합적으로 분석하여 회로 차단기 시장 경쟁 구도와 신흥 고성장 부문에 대한 통찰력을 제공합니다.

본 보고서 구매의 주요 이점

이 보고서는 회로 차단기 시장의 리더와 신규 시장 진출기업을 지원하기 위해 전체 시장 및 하위 부문에 대한 신뢰할 수 있는 수익 예측을 제공하는 것을 목표로 하고 있습니다. 이 정보를 통해 이해관계자들은 경쟁 구도를 이해하고, 자사의 포지셔닝과 효과적인 시장 진출 전략을 수립하는 데 도움이 되는 귀중한 통찰력을 얻을 수 있습니다. 또한, 이 보고서는 이해관계자들이 시장 현황을 파악하는 데 도움이 되며, 시장 성장 촉진요인, 시장 성장 억제요인, 과제 및 기회에 대한 중요한 정보를 제공합니다. 이러한 요소들을 이해함으로써 이해관계자들은 정보에 입각한 의사결정을 내릴 수 있고, 회로 차단기 산업 시장 역학에 민감하게 대응할 수 있습니다.

- 주요 촉진요인(송전망 투자 증가 및 전력 수요 증가, 데이터센터의 급속한 성장, 교통 부문의 전기화), 억제요인(SF6 차단기에 대한 엄격한 환경 및 안전 기준, 비조직 부문의 현지 제조업체별 저가 제품 존재), 기회(전력 보호 및 제어를 위한 스마트 그리드 기술 도입 확대, 기존 송배전 인프라의 업데이트 필요), 과제(현대식 차단기와 관련된 사이버 보안) 등을 분석했습니다. 전력 보호 및 제어를 위한 스마트 그리드 기술 도입 확대, 기존 송배전 인프라 업데이트 필요), 과제(현대식 회로 차단기 관련 사이버 보안 위험)

- 제품 개발 및 혁신 : 회로 차단기 시장의 향후 기술 동향, 연구개발 활동, 신제품 및 서비스 출시에 대한 상세한 분석.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 -이 보고서는 다양한 지역의 회로 차단기 시장을 분석합니다.

- 시장 다각화 : 신제품 및 서비스, 미개척 지역, 최근 동향 및 회로 차단기 시장 투자에 관한 종합적인 정보

- 경쟁사 평가 : Eaton(아일랜드), ABB(스위스), Schneider Electric(프랑스), Siemens(독일), Mitsubishi Electric Corporation(일본) 등 회로차단기 시장 내 주요 기업의 시장 점유율, 성장성, 전략, 서비스를 종합적으로 평가 전략, 서비스 제공 내용에 대한 종합적인 평가를 실시했습니다. 이 평가는 이들 주요 기업들 시장에서의 위치, 성장 촉진 전략, 회로 차단기 분야에서 제공하는 서비스 범위에 대한 심층적인 통찰력을 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

- 시장 역학

- 미충족 요구와 공백

- 연결된 시장과 분야간 기회

- 새로운 비즈니스 모델과 에코시스템 변화

- Tier1/2/3 참여 기업의 전략적 움직임

제5장 업계 동향

- Porter의 Five Forces 분석

- 거시경제 전망

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 2025년-2026년 주요 컨퍼런스 및 이벤트

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향-회로차단기 시장

제6장 기술 진보, AI 별 영향, 특허, 혁신, 그리고 향후 응용

- 주요 신기술

- 보완적 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- 향후 응용

- AI/생성형 AI가 회로차단기 시장에 미치는 영향

- 성공 사례와 실세계에의 응용

제7장 규제 상황과 지속가능성에 관한 대처

- 지역 규제와 컴플라이언스

- 지속가능성 이니셔티브

- 규제 정책이 지속가능성 구상에 미치는 영향

- 인증, 라벨 및 환경기준

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구매 프로세스와 평가 기준에 관련되는 주요 이해관계자

- 채택 장벽과 내부 과제

- 다양한 용도의 미충족 요구

- 시장 수익성

제9장 회로차단기 시장(절연 유형별)

- 진공

- 공기

- 가스

- 석유

제10장 회로차단기 시장(전압별)

- 저

- 중

- 고

제11장 회로차단기 시장(설치 방법별)

- 실내

- 야외

제12장 회로차단기 시장(용도별)

- T&D 유틸리티

- 산업용

- 공장 자동화

- 상업시설 및 주택

- 재생에너지

- 철도

- EV 충전

- 데이터센터

- 기타

제13장 회로차단기 시장(지역별)

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제14장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점, 2022년-2025년

- 매출 분석, 2020년-2024년

- 시장 점유율 분석

- 기업 평가와 재무 지표

- 브랜드 비교

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제15장 기업 개요

- 주요 시장 진출기업

- SIEMENS

- EATON

- SCHNEIDER ELECTRIC

- ABB

- MITSUBISHI ELECTRIC CORPORATION

- EMERSON ELECTRIC CO.

- FUJI ELECTRIC CO., LTD.

- ROCKWELL AUTOMATION

- LS ELECTRIC CO., LTD.

- TOSHIBA CORPORATION

- WEG

- CG POWER & INDUSTRIAL SOLUTIONS LTD.

- GE VERNOVA

- HD HYUNDAI ELECTRIC CO., LTD.

- TE CONNECTIVITY

- POWELL INDUSTRIES

- LEGRAND

- 기타 기업

- CHINT

- TAVRIDA ELECTRIC

- SECHERON

- EFACEC

- KIRLOSKAR ELECTRIC COMPANY

- AISO ELECTRIC

- SRIWINELECTRIC

- ORECCO

- PHOENIX CONTACT

- MANGAL ELECTRICAL INDUSTRIES LIMITED

- BRUSH

제16장 조사 방법

제17장 부록

LSH 26.01.15The global circuit breaker market is valued at USD 22.70 billion in 2025 and is expected to reach USD 30.32 billion by 2030, registering a CAGR of 6.0% during 2025-2030. This rise is driven by the growing need for power reliability, increasing electricity consumption in residential and industrial applications, and expanding grid modernization initiatives.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million)/Volume (Units) |

| Segments | Insulation Type, Voltage, Installation, End User |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and South America |

A surge in high-voltage transmission development, along with investments in smart substations and renewable energy infrastructure, is accelerating global market demand. The market growth is also influenced by regulatory pressure to replace aging equipment and adopt advanced protective systems that support digital monitoring and sustainability goals.

"The air segment is expected to hold the largest share of the circuit breaker market, by insulation type, during the forecast period."

The air segment is expected to hold the largest share of the circuit breaker market, by insulation type, during the forecast period. This growth is attributed to its extensive deployment in low-voltage distribution systems, especially in commercial buildings, household power connections, and industrial control panels. Increasing urban development, commercial construction projects, and a strong emphasis on safe distribution inside premises are reinforcing the demand for air circuit breakers. Additionally, air-based systems offer easier maintenance and a cost advantage, making them more preferable for contractors and end-users. As smart building infrastructure gains momentum, low-voltage air circuit breakers equipped with monitoring and arc protection technology are expected to drive market expansion further.

"T&D utilities, by end user, is the largest segment of the circuit breaker market."

T&D utilities represent the largest segment of the circuit breaker market, driven by the rapid modernization of electric grids and the large-scale addition of substations to support the integration of renewable power. Governments are prioritizing investment in reliable, high-capacity networks to manage fluctuating loads from wind, solar, and energy storage facilities, leading to higher installation of medium- and high-voltage breakers. Additionally, the rising electrification in developing economies and the refurbishment of old grids in mature markets, such as the US and the European Union, are driving adoption. Grid operators are also moving toward smart, automated switching systems to improve fault response time, increasing the demand for digital and predictive maintenance-enabled breaker solutions.

"Asia Pacific is expected to be the fastest-growing market for circuit breakers."

The Asia Pacific region is experiencing rapid growth in the circuit breaker market, followed by Europe and North America. This growth is a result of large-scale industrialization, high urban energy demand, and continuing electrification initiatives in countries such as China, India, South Korea, and Japan. Massive investments in renewable energy and utility grid capacity enhancement are pushing demand for high-voltage and medium-voltage circuit breakers. Expansion of commercial buildings, metro projects, EV infrastructure, and manufacturing facilities further contribute to market acceleration. Europe is advancing, driven by sustainability regulations that promote SF6-free technologies. In North America, growth is influenced by grid modernization efforts, particularly in the US, which aim to support data centers and facilitate the integration of clean energy.

Breakdown of Primaries:

Primary interviews were conducted with a diverse range of key industry participants, subject-matter experts, C-level executives from key market players, industry consultants, and other relevant experts. These interviews were conducted to gather and verify crucial qualitative and quantitative information, as well as to assess the market's prospects. The distribution of these primary interviews is as follows:

By Company Type: Tier 1 - 57%, Tier 2 - 29%, Tier 3 - 14%

By Designation: C-Level - 35%, Directors - 20%, Others- 45%

By Region: North America - 20%, Europe- 15%, Asia Pacific - 30%, Middle East & Africa - 25%, and South America - 10%

Note: The tier of the companies has been defined based on their total revenue as of 2024: Tier 1 = >USD 5 billion, Tier 2 = USD 1 billion to USD 5 billion, and Tier 3 = <USD 1 billion.

The key players in the circuit breaker market include companies such as ABB (Switzerland), Schneider Electric (France), Siemens (Germany), Mitsubishi Electric Corporation (Japan), and Eaton (Ireland).

Research Coverage:

The report provides a comprehensive overview of the circuit breaker market, encompassing multiple regions. Its objective is to estimate the market size and assess the potential for future growth across various segments, including insulation type, voltage, installation type, end-user, and region. Additionally, the report includes a detailed competitive analysis of key market players, featuring their company profiles, recent developments, and key market strategies. The market has been segmented by insulation type, voltage, installation, end user, and region, with a focus on analyzing industry trends. The report also provides market share analysis of the top players, supply chain analysis, and company profiles, collectively providing insights into the competitive landscape and emerging high-growth segments within the circuit breaker market.

Key Benefits of Buying the Report

The report is designed to assist leaders and new entrants in the circuit breaker market by providing them with reliable revenue estimates for the overall market as well as its subsegments. This information will enable stakeholders to understand the competitive landscape and gain valuable insights to position their businesses and develop suitable go-to-market strategies effectively. Furthermore, the report helps stakeholders comprehend the current state of the market and provides key information on market drivers, restraints, challenges, and opportunities. By understanding these factors, stakeholders can make informed decisions and stay attuned to market dynamics in the circuit breaker industry.

- Analysis of key drivers (Increasing investment in the grid and rising electricity demand, rapid expansion of data centers, electrification of transportation sector) restraints (strict environmental and safety standards for SF6 circuit breakers, presence of low-cost products offered by local players in the unorganized sector), opportunities (growing adoption of smart grid technologies for power protection and control and need to upgrade existing T&D infrastructure), and challenges (cybersecurity risks associated with modern circuit breakers)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the circuit breaker market.

- Market Development: Comprehensive information about lucrative markets--the report analyses the circuit breaker market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the circuit breaker market

- Competitive Assessment: A comprehensive evaluation has been conducted to analyze the market shares, growth strategies, and service offerings of prominent players in the circuit breaker market, including Eaton (Ireland), ABB (Switzerland), Schneider Electric (France), Siemens (Germany), and Mitsubishi Electric Corporation (Japan), among others. The assessment provides in-depth insights into the market position of these key players, their strategies for driving growth, and the range of services they offer in the circuit breaker segment

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN CIRCUIT BREAKER MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CIRCUIT BREAKER MARKET

- 3.2 CIRCUIT BREAKER MARKET, BY REGION

- 3.3 CIRCUIT BREAKER MARKET, BY INSULATION TYPE

- 3.4 CIRCUIT BREAKER MARKET, BY INSTALLATION

- 3.5 CIRCUIT BREAKER MARKET, BY VOLTAGE

- 3.6 CIRCUIT BREAKER MARKET, BY APPLICATION

- 3.7 CIRCUIT BREAKER MARKET IN ASIA PACIFIC, BY APPLICATION AND COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Surging industrial activity and electrification

- 4.2.1.2 Increasing investment in data centers amid rise in cloud computing

- 4.2.1.3 Expansion of electric vehicle charging infrastructure

- 4.2.1.4 Growing emphasis on upgrading T&D infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 Strict environmental and safety standards for SF6 circuit breakers

- 4.2.2.2 Availability of low-cost products in gray markets

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Mounting adoption of smart grid technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Cybersecurity risks associated with modern circuit breakers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 THREATS OF SUBSTITUTES

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ENERGY TRANSITION INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ELECTRIFICATION INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF CIRCUIT BREAKERS, BY VOLTAGE, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF CIRCUIT BREAKERS, BY REGION, 2021-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 853521)

- 5.6.2 EXPORT SCENARIO (HS CODE 853521)

- 5.6.3 IMPORT SCENARIO (HS CODE 853529)

- 5.6.4 EXPORT SCENARIO (HS CODE 853529)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 KCY CLOUD DATA CENTER USES ABB'S CIRCUIT BREAKERS AND SWITCHGEAR TO ENABLE RELIABLE POWER DISTRIBUTION FOR HIGH-DENSITY IT LOADS

- 5.10.2 ECODATACENTER ADOPTS SCHNEIDER ELECTRIC'S CONNECTED CIRCUIT BREAKERS TO SUPPORT LOW-CARBON DATA CENTER

- 5.10.3 EATON EXPERIENCE CENTER LEVERAGES SMART CIRCUIT BREAKER TO DEMONSTRATE VEHICLE-TO-GRID AND HOME ENERGY MANAGEMENT SCENARIOS

- 5.11 IMPACT OF 2025 US TARIFF - CIRCUIT BREAKER MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON APPLICATIONS

6 TECHNOLOGICAL ADVANCES, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 VACUUM INTERRUPTERS

- 6.1.2 SOLID-STATE CIRCUIT BREAKERS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SWITCHGEAR AND INTEGRATED DISTRIBUTION PANELS

- 6.2.2 CURRENT/VOLTAGE SENSING AND CT/VT INSTRUMENTATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 POWER TRANSFORMERS AND SUBSTATION EQUIPMENT

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | DIGITAL & ECO-DESIGN FOUNDATION

- 6.4.2 MID-TERM (2027-2030) | GRID MODERNIZATION & SYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS, GRID-INTERACTIVE PROTECTION

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON CIRCUIT BREAKER MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY OEMS IN CIRCUIT BREAKER PROCESSING

- 6.7.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN CIRCUIT BREAKER MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT AI/GEN AI-INTEGRATED CIRCUIT BREAKERS

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

9 CIRCUIT BREAKER MARKET, BY INSULATION TYPE

- 9.1 INTRODUCTION

- 9.2 VACUUM

- 9.2.1 HIGH EMPHASIS ON GRID MODERNIZATION AND INDUSTRIAL RETROFITS TO FOSTER SEGMENTAL GROWTH

- 9.3 AIR

- 9.3.1 PROLIFERATION OF DISTRIBUTED ENERGY RESOURCES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 9.4 GAS

- 9.4.1 GLOBAL DECARBONIZATION POLICIES AND ESG-LINKED INVESTMENT FRAMEWORKS TO FUEL SEGMENTAL GROWTH

- 9.5 OIL

- 9.5.1 RISE IN REFURBISHMENT, SPARE PART SUPPLY, AND DROP-IN REPLACEMENT FOR AGING SUBSTATIONS TO DRIVE MARKET

10 CIRCUIT BREAKER MARKET, BY VOLTAGE

- 10.1 INTRODUCTION

- 10.2 LOW

- 10.2.1 ELECTRIFICATION AND DIGITALIZATION TRENDS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 10.3 MEDIUM

- 10.3.1 RISING DEVELOPMENT OF COMMERCIAL AND RESIDENTIAL INFRASTRUCTURE TO BOLSTER SEGMENTAL GROWTH

- 10.4 HIGH

- 10.4.1 INCREASING RELIANCE ON RENEWABLE ENERGY SOURCES TO FOSTER SEGMENTAL GROWTH

11 CIRCUIT BREAKER MARKET, BY INSTALLATION

- 11.1 INTRODUCTION

- 11.2 INDOOR

- 11.2.1 RISE IN DATA CENTERS AND AUTOMATION TO ACCELERATE SEGMENTAL GROWTH

- 11.3 OUTDOOR

- 11.3.1 EXPANSION OF RENEWABLE ENERGY CAPACITY TO BOOST SEGMENTAL GROWTH

12 CIRCUIT BREAKER MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 T&D UTILITIES

- 12.2.1 RENEWABLE CAPACITY EXPANSION AND GRID MODERNIZATION TO BOOST SEGMENTAL GROWTH

- 12.3 INDUSTRIAL

- 12.3.1 IMPLEMENTATION OF NET-ZERO AND ENERGY-EFFICIENCY TARGETS TO FUEL SEGMENTAL GROWTH

- 12.4 FACTORY AUTOMATION

- 12.4.1 PRESENCE OF ELECTRO-INTENSIVE MANUFACTURING SECTORS TO AUGMENT SEGMENTAL GROWTH

- 12.5 COMMERCIAL & RESIDENTIAL

- 12.5.1 STRONG FOCUS ON ELECTRIFICATION AND ENERGY EFFICIENCY TO ACCELERATE SEGMENTAL GROWTH

- 12.6 RENEWABLES

- 12.6.1 HIGH EMPHASIS ON UPDATING GRID CODES AND ACCELERATING INTERCONNECTION TO EXPEDITE SEGMENTAL GROWTH

- 12.7 RAILWAYS

- 12.7.1 FOCUS ON HIGH TRANSPORT WORK PER UNIT OF ENERGY TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.8 EV CHARGING

- 12.8.1 EXPANSION OF CHARGING PLAZAS, DEPOT INSTALLATIONS, AND HIGHER PER-SITE CAPACITY TO DRIVE MARKET

- 12.9 DATA CENTERS

- 12.9.1 GROWING ENERGY FOOTPRINT AND INVESTMENT TO ACCELERATE SEGMENTAL GROWTH

- 12.10 OTHERS

13 CIRCUIT BREAKER MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Rising consumption of renewable energy and electricity demand to foster market growth

- 13.2.2 JAPAN

- 13.2.2.1 Increasing need for stable and reliable power to accelerate market growth

- 13.2.3 INDIA

- 13.2.3.1 Thriving manufacturing and data center sectors to bolster market growth

- 13.2.4 AUSTRALIA

- 13.2.4.1 Rising installation of renewable energy systems to fuel market growth

- 13.2.5 SOUTH KOREA

- 13.2.5.1 Substantial increase in solar and wind capacity to expedite market growth

- 13.2.6 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Increasing manufacturing activities and renewable power generation to drive market

- 13.3.2 UK

- 13.3.2.1 Rapid digitalization, grid modernization, and data center expansion to foster market growth

- 13.3.3 FRANCE

- 13.3.3.1 Robust manufacturing base and rapidly digitalizing infrastructure to boost market growth

- 13.3.4 SPAIN

- 13.3.4.1 Expansion of electric vehicle charging infrastructure to accelerate market growth

- 13.3.5 ITALY

- 13.3.5.1 Increase in solar and wind energy additions to expedite market growth

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 NORTH AMERICA

- 13.4.1 US

- 13.4.1.1 High emphasis on addressing large-scale digital loads and electrification to bolster market growth

- 13.4.2 CANADA

- 13.4.2.1 Mounting electricity generation to contribute to market growth

- 13.4.3 MEXICO

- 13.4.3.1 Rapid renewable expansion and grid upgrades to augment market growth

- 13.4.1 US

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Rising implementation of renewable and grid programs to drive market

- 13.5.1.2 UAE

- 13.5.1.2.1 Growing focus on clean energy and grid modernization programs to augment market growth

- 13.5.1.3 Kuwait

- 13.5.1.3.1 High emphasis on energy diversification and grid upgrades to bolster market growth

- 13.5.1.4 Rest of GCC

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Strong focus on strengthening power transmission networks to bolster market growth

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Ongoing expansion in renewables and high electricity demand to accelerate market growth

- 13.6.2 ARGENTINA

- 13.6.2.1 Industrial modernization, grid upgrades, and renewable energy diversification to expedite market growth

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND COMPARISON

- 14.6.1 EATON

- 14.6.2 SCHNEIDER ELECTRIC

- 14.6.3 ABB

- 14.6.4 SIEMENS

- 14.6.5 MITSUBISHI ELECTRIC CORPORATION

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Installation footprint

- 14.7.5.4 Voltage footprint

- 14.7.5.5 Insulation type footprint

- 14.7.5.6 Application footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 SIEMENS

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses/Competitive threats

- 15.1.2 EATON

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses/Competitive threats

- 15.1.3 SCHNEIDER ELECTRIC

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths/Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses/Competitive threats

- 15.1.4 ABB

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.3.4 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses/Competitive threats

- 15.1.5 MITSUBISHI ELECTRIC CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses/Competitive threats

- 15.1.6 EMERSON ELECTRIC CO.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.7 FUJI ELECTRIC CO., LTD.

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Expansions

- 15.1.8 ROCKWELL AUTOMATION

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.9 LS ELECTRIC CO., LTD.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Other developments

- 15.1.10 TOSHIBA CORPORATION

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.11 WEG

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Expansions

- 15.1.11.3.2 Other developments

- 15.1.12 CG POWER & INDUSTRIAL SOLUTIONS LTD.

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Expansions

- 15.1.13 GE VERNOVA

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Other developments

- 15.1.14 HD HYUNDAI ELECTRIC CO., LTD.

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.14.3.2 Expansions

- 15.1.14.3.3 Other developments

- 15.1.15 TE CONNECTIVITY

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.16 POWELL INDUSTRIES

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.17 LEGRAND

- 15.1.17.1 Business overview

- 15.1.17.2 Products/Solutions/Services offered

- 15.1.1 SIEMENS

- 15.2 OTHER PLAYERS

- 15.2.1 CHINT

- 15.2.2 TAVRIDA ELECTRIC

- 15.2.3 SECHERON

- 15.2.4 EFACEC

- 15.2.5 KIRLOSKAR ELECTRIC COMPANY

- 15.2.6 AISO ELECTRIC

- 15.2.7 SRIWINELECTRIC

- 15.2.8 ORECCO

- 15.2.9 PHOENIX CONTACT

- 15.2.10 MANGAL ELECTRICAL INDUSTRIES LIMITED

- 15.2.11 BRUSH

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 List of primary interview participants

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of primaries

- 16.1.1 SECONDARY DATA

- 16.2 SCOPE

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.2 TOP-DOWN APPROACH

- 16.3.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.1.1 Supply-side assumptions

- 16.4.1.2 Supply-side calculations

- 16.4.2 DEMAND SIDE

- 16.4.2.1 Demand-side assumptions

- 16.4.2.2 Demand-side calculations

- 16.4.1 SUPPLY SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 FORECAST

- 16.8 RESEARCH ASSUMPTIONS

- 16.9 RISK ANALYSIS

17 APPENDIX

- 17.1 INSIGHTS FROM INDUSTRY EXPERTS

- 17.2 DISCUSSION GUIDE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS