|

시장보고서

상품코드

1923692

건강기능식품 부형제 시장(-2030년) : 원료(유기화학제품 및 무기화학제품) 및 기능

|

||||||

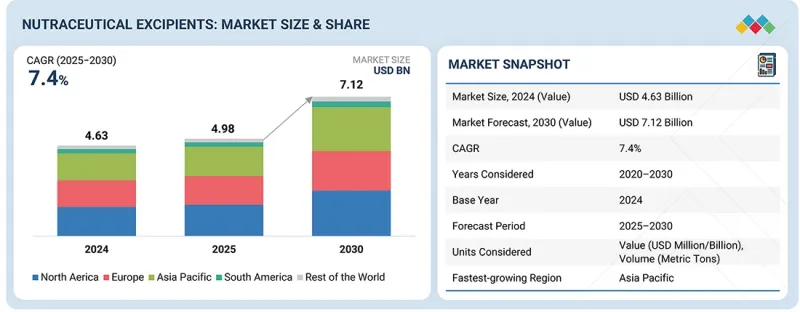

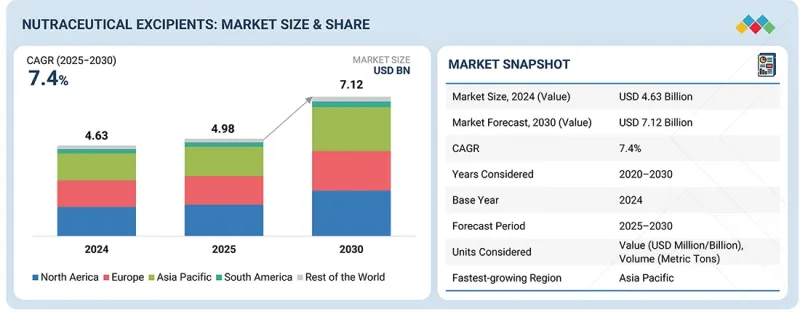

예측 기간 동안 CAGR은 7.4%를 나타낼 것으로 예상됩니다.

건강기능식품 부형제 시장은 전 세계 소비자 그룹을 대상으로 고품질, 클린 라벨, 과학적 근거를 갖춘 건강 보조 식품에 대한 수요가 급증함에 따라 2030년까지 꾸준한 성장을 보일 것으로 전망됩니다. 껌, 소프트젤, 서방형 정제, 기능성 음료 등 첨단 제형으로 혁신을 추구하는 브랜드가 증가함에 따라 안정성, 생체 이용률, 맛 및 전반적인 제품 성능을 향상시키는 부형제에 대한 수요가 커지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2025-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러), 수량(메트릭 톤) |

| 부문 | 원료, 최종 제품, 기능성, 기능성 용도, 제형, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미 및 기타 지역 |

건강에 대한 인식이 높아지고 식물성, 천연, 알레르기 유발 물질이 없는 원료로의 전환이 가속화되면서 식물성 및 지속 가능한 원료에서 추출한 새로운 부형제의 채택이 증가하고 있습니다. 식물성 캡슐 시스템, 다기능 부형제 혼합물, 개선된 용해성 증진제와 같은 기술적 진보와 유럽 및 북미와 같은 지역의 강력한 규제 프레임워크 지원이 시장 성장을 더욱 촉진하고 있습니다. 연구 개발, 제형 혁신 및 제조 현대화에 대한 투자 증가와 함께, 기능성 부형제 산업은 광범위한 건강 및 영양 환경 내에서 고성능 및 소비자 중심의 보충제 개발을 가능케 하는 핵심 요소로 부상하고 있습니다.

"건조 제형 부문이 예측 기간 동안 큰 점유율을 차지할 전망"

건강기능식품 부형제 부문은 제조사들이 안정성 향상, 유통기한 연장, 정제 및 캡슐 및 포장재 가공 용이성을 위해 분말 기반 원료를 점점 더 많이 채택함에 따라 시장을 계속 주도하고 있습니다. 미세결정셀룰로오스(MCC), 유당 일수화물, 말토덱스트린, 프리바이오틱 섬유, 이산화규소와 같은 건식 부형제는 우수한 유동성, 압축성, 부피 증가 특성으로 인해 여전히 널리 사용되고 있습니다. 클린 라벨 및 식물 유래 기능성 식품에 대한 수요 증가로 유기농 쌀가루, 아카시아검, 천연 전분 유도체 등 생물 기반 건식 부형제의 사용도 가속화되고 있습니다. 최근 업계 사례로는 로케트(Roquette)의 2024년 기능성 필름용 전분 부형제 ‘LYCOAT NG’ 출시, DFE 파마(DFE Pharma)의 식이 보충제용 건조 분말 부형제 포트폴리오 확장, 바스프(BASF)의 정제 성능 개선을 위한 건식 코팅 솔루션 도입 등이 있습니다. 이러한 혁신은 제형 효율성과 고품질 기능성 제품 개발을 지원하는 핵심 기능성 원료로서 건조 부형제의 역할을 강화하고 있습니다.

"맛 마스킹 기능의 부문이 견조한 성장을 유지하고 가장 빠른 성장 부문으로"

브랜드들이 쓴맛이 나는 식물 추출물, 미네랄, 아미노산 및 차세대 생리활성 물질을 소비자 친화적인 형태로 점점 더 많이 포함시키면서, 맛 가림 기능은 기능성 의약품 부형제 시장에서 가장 빠르게 성장하는 기능이 되었습니다. 구미, 츄어블, 발포성, 구강 분해성 분말에 대한 수요 증가로 제조업체들은 이제 쓴맛, 금속성 맛, 강한 허브 향을 효과적으로 감소시킬 수 있는 부형제에 의존하고 있습니다. 이러한 변화는 포함 복합체를 위한 사이클로덱스트린, 맛 수용체 상호작용을 차단하는 지질 기반 운반체, 마이크로캡슐화를 위한 변형 전분의 사용을 가속화했습니다. 이러한 추세는 인그레디온(Ingredion)의 2024년 청정 라벨 캡슐화 전분(풍미 조절용), 애슐랜드(Ashland)의 최근 출시된 맛 가림 츄어블용 최적화 클루셀 HPC 등급(Klucel HPC grades), 케리(Kerry)의 활성 성분 풍부 보충제용 엔마스크(Enmask™) 천연 풍미 조절 시스템 출시 등 새로운 개발로 더욱 강화되고 있습니다. 특히 소아용, 스포츠 영양제, 여성 건강 제품에서 소비자의 맛 좋은 기능성 식품에 대한 기대가 높아짐에 따라 맛 가림 기술은 핵심 성능 요인으로 급부상하며, 기능성 식품 부형제 분야에서 가장 빠르게 성장하는 용도로서 입지를 공고히 하고 있습니다.

본 보고서에서는 세계의 건강기능식품 부형제 시장을 조사했으며, 시장 개요, 시장 성장 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- 미충족 요구와 화이트 스페이스

- 관련 시장 및 이업종과의 분야 횡단적 기회

- Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제지표

- 공급망 분석

- 밸류체인 분석

- 에코시스템/시장지도

- 가격 분석

- 무역 분석

- 주요 회의 및 이벤트

- 고객의 비즈니스에 영향을 미치는 동향

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세의 영향(2025년) - 건강기능식품 시장

제6장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴

- 주요 신기술

- 보완적 기술

- 기술/제품 로드맵

- 특허 분석

- 미래의 응용

- AI/생성형 AI가 건강기능식품 시장에 미치는 영향

- 성공 사례와 실세계에의 응용

제7장 지속가능성과 규제상황

- 지역 규제 및 규정 준수

- 지속가능성에 대한 노력

- 지속가능성에 미치는 영향과 규제 정책의 노력

- 인증, 라벨, 환경 기준

제8장 고객 환경 및 구매행동

- 의사결정 공정

- 이해관계자와 구매평가기준

- 채택 장벽과 내부 과제

- 다양한 최종 사용자 산업의 미충족 요구

- 시장 수익성

제9장 건강기능식품 부형제 시장 : 최종 제품별

- 프로바이오틱스

- 프리바이오틱스

- 단백질과 아미노산

- 비타민

- 미네랄

- 오메가3 지방산

- 기타

제10장 건강기능식품 부형제 시장 : 원료별

- 유기화학제품

- 오레오케미컬즈

- 탄수화물

- 석유화학제품

- 단백질

- 기타

- 무기화학제품

- 인산칼슘

- 금속 산화물

- 암염

- 탄산칼슘

- 황산칼슘

- 기타

- 기타

제11장 건강기능식품 부형제 시장 : 기능성 용도별

- 맛 마스킹

- 안정제

- 수정 릴리스

- 용해성과 생체이용률 향상

- 기타

제12장 건강기능식품 부형제 시장 : 제형별

- 건조

- 정제

- 캡슐

- 액체

- 기타

제13장 건강기능식품 부형제 시장 : 기능성별

- 바인더

- 충전제 및 희석제

- 붕괴제

- 코팅제

- 향료 및 감미료

- 방부제

- 윤활제 및 윤활제

- 현탁제 및 점성제

- 착색료

- 유화제

- 기타

제14장 건강기능식품 부형제 시장 : 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

- 세계 기타 지역

- 중동

- 아프리카

제15장 경쟁 구도

- 개요

- 주요 기업의 경쟁 전략/유력 기업

- 수익 분석

- 시장 점유율 분석

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 기업

- 기업평가 매트릭스 : 스타트업, 중소기업

- 기업평가와 재무재표

- 경쟁 시나리오

제16장 기업 프로파일

- 주요 기업

- KERRY GROUP PLC

- INGREDION

- BASF SE

- ASSOCIATED BRITISH FOODS PLC

- SENSIENT TECHNOLOGIES CORPORATION

- CARGILL, INCORPORATED

- AZELIS

- ASHLAND

- MEGGLE HOLDING SE

- ROQUETTE FRERES

- COLORCON, INC.

- ALSIANO A/S

- JIGS CHEMICAL

- IMCD

- HILMAR CHEESE COMPANY, INC.

- OMYA

- BIOGRUND

- JRS PHARMA

- INNOPHOS

- NOVO EXCIPIENTS PVT. LTD.

- PANCHAMRUT CHEMICALS

- GATTEFOSSE

- FUJI CHEMICAL INDUSTRIES CO., LTD.

- SUDEEP PHARMA LIMITED

- SORSE TECHNOLOGIES

제17장 조사 방법

제18장 부록

HBR 26.02.19The nutraceutical excipients market is estimated to be valued at USD 4.98 billion in 2025 and is projected to reach USD 7.12 billion by 2030, growing at a CAGR of 7.4% during the forecast period. The nutraceutical excipients market is projected to witness steady expansion through 2030, driven by the surging demand for high-quality, clean-label, and science-backed dietary supplements across global consumer groups. As brands innovate with advanced dosage forms-including gummies, softgels, controlled-release tablets, and functional beverages-there is a growing need for excipients that enhance stability, bioavailability, taste, and overall product performance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD), Volume (Metric Tons) |

| Segments | Source, End Product, Functionality, Functionality Application, Formulation, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

Rising health consciousness, coupled with the shift toward plant-based, natural, and allergen-free ingredients, is accelerating the adoption of novel excipients sourced from botanical and sustainable materials. Technological advancements such as plant-based capsule systems, multifunctional excipient blends, and improved solubility enhancers, supported by strong regulatory frameworks in regions like Europe and North America, are further propelling market growth. With increasing investments in R&D, formulation innovation, and manufacturing modernization, the nutraceutical excipients industry is emerging as a key enabler of high-performance and consumer-centric supplement development within the broader health and nutrition landscape.

"The dry formulation segment is estimated to witness a significant share during the forecast period."

The dry nutraceutical excipients segment continues to dominate the market as manufacturers increasingly adopt powder-based ingredients for enhanced stability, extended shelf life, and ease of processing in tablets, capsules, and sachets. Dry excipients such as microcrystalline cellulose (MCC), lactose monohydrate, maltodextrin, prebiotic fibers, and silicon dioxide remain widely used for their superior flowability, compressibility, and bulking properties. Growing demand for clean-label and plant-derived nutraceuticals has also accelerated the use of bio-based dry excipients, including organic rice flour, acacia gum, and natural starch derivatives. Recent industry examples include Roquette's launch of LYCOAT NG starch excipient for nutraceutical films in 2024, DFE Pharma's expansion of its dry powder excipients portfolio for dietary supplements, and BASF's introduction of dry-coated solutions to improve tablet performance. These innovations are strengthening the role of dry excipients as essential functional ingredients supporting formulation efficiency and high-quality nutraceutical product development.

"The taste masking functionality segment is the fastest to maintain robust growth."

Taste masking has become the fastest-growing functionality in the nutraceutical excipients market as brands increasingly incorporate bitter plant extracts, minerals, amino acids, and next-generation bioactives into consumer-friendly formats. With rising demand for gummies, chewables, effervescent, and orally disintegrating powders, manufacturers now rely on excipients that can effectively reduce bitterness, metallic notes, and strong herbal flavors. This shift has accelerated the use of cyclodextrins for inclusion complexation, lipid-based carriers to block taste receptor interaction, and modified starches for microencapsulation. New developments are reinforcing this momentum, such as Ingredion's 2024 clean-label encapsulation starches for flavor modulation, Ashland's recent Klucel HPC grades optimized for taste-masked chewables, and Kerry's release of Enmask(TM) natural flavor-modulating systems for active-rich supplements. As consumer expectations for pleasant-tasting nutraceuticals rise-especially in pediatric, sports nutrition, and women's health products-taste masking is rapidly becoming a critical performance driver, solidifying its position as the fastest-expanding application area in nutraceutical excipients.

"Europe is estimated to account for a significant share of the nutraceutical excipients market."

Europe holds a significant share in the nutraceutical excipients market, driven by the strong presence of leading global players and a steady rise in innovative product launches across the region. Countries such as Germany, France, the UK, and Switzerland serve as key hubs for pharmaceutical and nutraceutical manufacturing, supported by advanced R&D capabilities and strict quality standards that encourage the development of next-generation excipients. Major companies like Roquette, BASF, Kerry, and IMCD continue to expand their portfolios, with recent launches such as Roquette's LYCAGEL(R) Flex softgel capsule shell system introduced at Vitafoods Europe 2024, reinforcing the region's leadership in plant-based and functional excipient solutions. These innovations cater to Europe's rapidly growing demand for vegan, clean-label, and high-performance nutraceutical formulations. The combination of well-established excipient manufacturers, continuous technological advancements, and a strong regulatory framework firmly positions Europe as a dominant and fast-evolving market for nutraceutical excipients.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the nutraceutical excipients market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) - 10%

Prominent companies in the market include International Flavors & Fragrances Inc. (US), Kerry Group plc (Ireland), Ingredion (US), Sensient Technologies Corporation (US), Associated British Foods plc (UK), BASF SE (Germany), Roquette Freres (France), MEGGLE GmbH & Co. KG (Germany), Cargill, Incorporated (US), Ashland (US), IMCD (Netherlands), Hilmar Cheese Company, Inc. (US), SEPPIC (US), and Azelis Group (Luxembourg).

Research Coverage

This research report categorizes the nutraceutical excipients market by source (organic chemicals, inorganic chemicals, others), functionality (disintegrants, colorants, lubricants & glidants, preservatives, emulsifying agents, other functionalities), end product (proteins & amino acids, omega-3 fatty acids, vitamins, minerals, prebiotics, probiotics, other end products), form (dry, liquid), functionality application (taste masking, stabilizers, modified release, solubility & bioavailability enhancers, other functionality applications), and region. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the nutraceutical excipients market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; Contracts, partnerships, and agreements. The study includes new product & service launches, mergers & acquisitions, and recent developments associated with the nutraceutical excipients market. This report also includes a competitive analysis of emerging startups in the nutraceutical excipients market ecosystem.

Reasons to Buy this Report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall nutraceutical excipients and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

1. In-depth Segmentation across Type, Source, and Application: This study presents a detailed breakdown of the nutraceutical excipients market, categorizing it source (organic chemicals, inorganic chemicals, others), functionality (Disintegrants, Colorants, Lubricants & Glidants, Preservatives, Emulsifying Agents, Other Functionalities), end product (Proteins & Amino Acids, Omega-3 Fatty Acids, Vitamins, Minerals, Prebiotics, Probiotics, Other End Products). The analysis also covers key functional roles such as taste masking agents, stabilizers, solubilizers, and release-modifying excipients. This holistic segmentation enables stakeholders to identify high-growth formulation areas, enhance product development strategies, and align offerings with evolving nutraceutical manufacturing needs.

2. Region-specific Insights with Focus on Emerging Markets: The report offers an in-depth regional and country-level assessment, highlighting expanding opportunities across high-growth regions such as the Asia Pacific, South America, and the Middle East. It examines regulatory frameworks, clean-label norms, and consumer shifts toward plant-based, vegan, and natural supplements, driving excipient adoption. Additionally, it outlines government support for nutraceutical manufacturing, investments in advanced processing technologies, and rising local production capabilities-providing valuable guidance for companies seeking to scale, partner locally, or strengthen regional presence.

3. Competitive Intelligence and Innovation Landscape: Detailed competitive profiles of leading players-including Roquette, Kerry Group, BASF, Ingredion, and DSM-are provided, covering their strategic initiatives, technological advancements, and expansion plans. The report tracks major market developments such as product launches, facility expansions, mergers and acquisitions, and R&D activities. These insights equip stakeholders to benchmark competition, understand innovation trajectories, and capitalize on emerging formulation technologies shaping the nutraceutical excipients market.

4. Demand Forecasts Backed by Data-driven Methodologies: Market size projections and growth estimates through 2030 are based on validated top-down and bottom-up analytical approaches, supplemented by industry expert inputs and verified trade data. The forecasts deliver reliable insights into demand patterns, excipient consumption trends across dosage forms, and long-term market opportunities, helping stakeholders strategize investments and strengthen future-ready portfolios.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 UNITS CONSIDERED

- 1.4.1 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN NUTRACEUTICAL EXCIPIENTS MARKET

- 3.2 NUTRACEUTICAL EXCIPIENTS MARKET, BY SOURCE AND REGION

- 3.3 NUTRACEUTICAL EXCIPIENTS MARKET, BY REGION

- 3.4 NUTRACEUTICAL EXCIPIENTS MARKET, BY FORMULATION

- 3.5 NUTRACEUTICAL EXCIPIENTS MARKET, BY SOURCE

- 3.6 NUTRACEUTICAL EXCIPIENTS MARKET, BY FUNCTIONALITY APPLICATION

- 3.7 NUTRACEUTICAL EXCIPIENTS MARKET, BY END PRODUCT

- 3.8 NUTRACEUTICAL EXCIPIENTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased focus on preventive care to encourage investments in products/solutions

- 4.2.1.2 Advancements in nanotechnology equipped with new features relating to nutraceutical excipients

- 4.2.1.3 Rising investments in clean-label and natural excipients driven by regulatory pressure and shifting consumer health preferences

- 4.2.1.4 Mandates on food fortification by government organizations

- 4.2.2 RESTRAINTS

- 4.2.2.1 Decrease in returns on R&D investments and high costs of clinical trials and registration

- 4.2.2.2 Stringent regulatory expectations for excipient safety, purity, and compliance, adding complexity to product approvals

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Multi-functionalities of excipients aiding in saving costs and processing time

- 4.2.3.2 Rising awareness of micronutrient deficiencies

- 4.2.3.3 Growing popularity of gummy supplements

- 4.2.4 CHALLENGES

- 4.2.4.1 Consumer skepticism associated with nutraceutical products due to rural and semi-urban consumers' perception of dietary supplements as pharmaceutical drugs

- 4.2.4.2 Ensuring compatibility with high-potency actives

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.2.2 BARGAINING POWER OF SUPPLIERS

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 THREAT OF NEW ENTRANTS

- 5.3 MACROECONOMIC INDICATORS

- 5.3.1 GLOBAL POPULATION WITNESSING HIGH PREVALENCE OF OBESITY

- 5.3.2 AGING POPULATION BECOMING MORE AWARE OF BENEFITS OF NUTRACEUTICALS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.5.1 SOURCING OF RAW MATERIALS

- 5.5.2 MANUFACTURING

- 5.5.3 DISTRIBUTION, MARKETING, AND SALES

- 5.6 ECOSYSTEM/MARKET MAP

- 5.6.1 UPSTREAM

- 5.6.1.1 Excipient manufacturers

- 5.6.1.2 Technology providers

- 5.6.2 DOWNSTREAM

- 5.6.2.1 Regulatory bodies

- 5.6.2.2 Nutraceutical manufacturers

- 5.6.1 UPSTREAM

- 5.7 PRICING ANALYSIS

- 5.7.1 INDICATIVE AVERAGE SELLING PRICE, BY SOURCE

- 5.7.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.8 TRADE ANALYSIS

- 5.8.1 TRADE ANALYSIS OF HS CODE 210690

- 5.8.1.1 Export trends of nutraceutical excipient under HS Code 210690

- 5.8.1.2 Import trends of nutraceutical excipients under HS Code 210690

- 5.8.2 TRADE ANALYSIS OF HS CODE 300490

- 5.8.2.1 Export trends of nutraceutical excipients under HS Code 300490

- 5.8.2.2 Import trends of nutraceutical excipients under HS Code 300490

- 5.8.3 TRADE ANALYSIS OF HS CODE 293090

- 5.8.3.1 Export trends of nutraceutical excipient under HS Code 293090

- 5.8.3.2 Import trends of nutraceutical excipients under HS Code 293090

- 5.8.4 TRADE ANALYSIS OF HS CODE 382200

- 5.8.4.1 Export trends of nutraceutical excipient under HS Code 382200

- 5.8.4.2 Import trends of nutraceutical excipient under HS Code 382200

- 5.8.1 TRADE ANALYSIS OF HS CODE 210690

- 5.9 KEY CONFERENCES & EVENTS

- 5.10 TRENDS IMPACTING CUSTOMERS' BUSINESSES

- 5.11 INVESTMENT AND FUNDING SCENARIO

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 BENEO'S GALENIQ(R) MULTIFUNCTIONAL FILLER-BINDER FOR CLEAN-LABEL TABLETS (CPHI 2025)

- 5.12.2 ROQUETTE READILYCOAT(R) LOW-TEMPERATURE COATING SYSTEM (2025)

- 5.12.3 EVONIK - LIPID-BASED CARRIER FOR OMEGA-3 CAPSULES (APRIL 2024)

- 5.13 IMPACT OF 2025 US TARIFF - NUTRACEUTICAL EXCIPIENTS MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRY/REGION

- 5.13.5 IMPACT ON END-USE INDUSTRY

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 INTRODUCTION

- 6.2 KEY EMERGING TECHNOLOGIES

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 LIST OF MAJOR PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON NUTRACEUTICAL EXCIPIENTS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN NUTRACEUTICAL EXCIPIENT PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN NUTRACEUTICAL EXCIPIENTS MARKET

- 6.7.3.1 AI-driven Ingredient Discovery & Formulation Optimization

- 6.7.3.2 AI-Enabled Evidence Review and Product Rationalization (2025)

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN NUTRACEUTICAL EXCIPIENTS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.2 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.2 INDUSTRY STANDARDS

- 7.2.2.1 Organizations/Regulations governing nutraceutical excipients market

- 7.2.2.2 North America

- 7.2.2.2.1 Canada

- 7.2.2.2.2 US

- 7.2.2.2.3 Mexico

- 7.2.2.3 European Union (EU)

- 7.2.2.4 Asia Pacific

- 7.2.2.4.1 Japan

- 7.2.2.4.2 China

- 7.2.2.4.3 India

- 7.2.2.4.4 Australia & New Zealand

- 7.2.2.5 Rest of the World (RoW)

- 7.2.2.5.1 Brazil

- 7.2.2.6 Probiotics

- 7.2.2.6.1 Introduction

- 7.2.2.6.2 National/International bodies for safety standards and regulations

- 7.2.2.6.3 Codex Alimentarius Commission (CAC)

- 7.2.2.6.4 North America: regulatory environment analysis

- 7.2.2.6.4.1 US

- 7.2.2.6.4.2 Canada

- 7.2.2.6.5 Asia Pacific: Regulatory environment analysis

- 7.2.2.6.5.1 Japan

- 7.2.2.6.5.2 India

- 7.2.2.6.6 South America: Regulatory Environment Analysis

- 7.2.2.6.6.1 Brazil

- 7.2.2.7 Prebiotics

- 7.2.2.7.1 Introduction

- 7.2.2.7.2 Asia Pacific

- 7.2.2.7.2.1 Japan

- 7.2.2.7.2.2 Australia & New Zealand

- 7.2.2.7.2.3 South Korea

- 7.2.2.7.2.4 India

- 7.2.2.7.3 North America

- 7.2.2.7.3.1 US

- 7.2.2.7.3.2 Canada

- 7.2.2.7.4 European Union

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 ADOPTION OF PLANT-BASED AND UPCYCLED RAW MATERIALS

- 7.3.2 IMPLEMENTATION OF ENERGY-EFFICIENT PROCESSING TECHNOLOGIES

- 7.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.5 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.6 MARKET PROFITABILITY

9 NUTRACEUTICAL EXCIPIENTS MARKET, BY END PRODUCT

- 9.1 INTRODUCTION

- 9.2 PROBIOTICS

- 9.2.1 GROWING STABILITY REQUIREMENTS OF PROBIOTIC INGREDIENTS TO DRIVE MARKET

- 9.3 PREBIOTICS

- 9.3.1 INCREASING FORMULATION NEEDS FOR STABLE PREBIOTIC INGREDIENTS TO DRIVE MARKET

- 9.4 PROTEINS & AMINO ACIDS

- 9.4.1 GROWING FORMULATION REQUIREMENTS FOR STABLE PROTEIN AND AMINO ACID INGREDIENTS TO DRIVE MARKET

- 9.5 VITAMINS

- 9.5.1 PREVALENCE OF VITAMIN DEFICIENCIES AMONG CONSUMERS TO DRIVE MARKET GROWTH FOR NUTRACEUTICAL EXCIPIENTS

- 9.6 MINERALS

- 9.6.1 BENEFITS OFFERED FOR OPTIMAL FUNCTIONING OF BRAIN AND HEART TO DRIVE GROWTH OF NUTRACEUTICAL EXCIPIENTS MARKET

- 9.7 OMEGA-3 FATTY ACIDS

- 9.7.1 INCREASE IN HEART DISEASES TO DRIVE DEMAND FOR OMEGA-3 FATTY ACID SUPPLEMENTS

- 9.8 OTHER END PRODUCTS

10 NUTRACEUTICAL EXCIPIENTS MARKET, BY SOURCE

- 10.1 INTRODUCTION

- 10.2 ORGANIC CHEMICALS

- 10.2.1 OLEOCHEMICALS

- 10.2.1.1 Fatty alcohols

- 10.2.1.1.1 Need for enhancing texture and creaminess likely to propel demand

- 10.2.1.2 Mineral stearates

- 10.2.1.2.1 Mineral stearates to reduce friction and avoid equipment clogging during manufacturing of nutraceuticals

- 10.2.1.3 Glycerin

- 10.2.1.3.1 Glycerin to help improve smoothness and lubrication process

- 10.2.1.4 Other oleochemicals

- 10.2.1.1 Fatty alcohols

- 10.2.2 CARBOHYDRATES

- 10.2.2.1 Sugars

- 10.2.2.1.1 Actual sugars

- 10.2.2.1.1.1 Rising diabetic population to fuel need for low-glycemic index alternatives like xylitol and isomaltulose

- 10.2.2.1.2 Sugar alcohols

- 10.2.2.1.2.1 Various advantageous and unique properties of sugar alcohols to make them an attractive option

- 10.2.2.1.3 Artificial sweeteners

- 10.2.2.1.3.1 Emerging trends in utilization of natural sweeteners in nutraceutical products to drive demand

- 10.2.2.1.1 Actual sugars

- 10.2.2.2 Cellulose

- 10.2.2.2.1 Microcrystalline cellulose

- 10.2.2.2.1.1 Rising nutraceutical trend to bolster microcrystalline cellulose demand for superior tablet integrity

- 10.2.2.2.2 Cellulose ethers

- 10.2.2.2.2.1 Cellulose ethers help streamline nutraceutical rheology

- 10.2.2.2.3 CMC & croscarmellose sodium

- 10.2.2.2.3.1 Enhanced mouthfeel and fast-acting properties to help propel market growth

- 10.2.2.2.4 Cellulose esters

- 10.2.2.2.4.1 Rising demand for cellulose esters to provide a technical edge in nutraceuticals

- 10.2.2.2.1 Microcrystalline cellulose

- 10.2.2.3 Starch

- 10.2.2.3.1 Modified starch

- 10.2.2.3.1.1 Technical advancements to fuel modified starch demand in nutraceutical excipient industry

- 10.2.2.3.2 Dried starch

- 10.2.2.3.2.1 Capabilities such as disintegration enhancement and bulking effects to drive market

- 10.2.2.3.3 Converted starch

- 10.2.2.3.3.1 Properties such as increased solubility to boost nutrient absorption

- 10.2.2.3.1 Modified starch

- 10.2.2.1 Sugars

- 10.2.3 PETROCHEMICALS

- 10.2.3.1 Glycols

- 10.2.3.1.1 Humectant & solvent properties to drive demand

- 10.2.3.2 Povidones

- 10.2.3.2.1 Film-forming function to provide controlled release of active ingredients

- 10.2.3.3 Mineral hydrocarbons

- 10.2.3.3.1 Properties such as antifoaming and lubrication to help in nutraceutical manufacturing

- 10.2.3.4 Acrylic polymers

- 10.2.3.4.1 Diverse functions of acrylic polymers in nutraceuticals to propel growth

- 10.2.3.5 Other petrochemical excipients

- 10.2.3.1 Glycols

- 10.2.4 PROTEINS

- 10.2.4.1 Expanding utilization of proteins as carriers for microparticles and nanoparticles to propel market growth

- 10.2.5 OTHER ORGANIC CHEMICALS

- 10.2.1 OLEOCHEMICALS

- 10.3 INORGANIC CHEMICALS

- 10.3.1 CALCIUM PHOSPHATE

- 10.3.1.1 Nutraceutical production to be optimized by utilizing GMO-free calcium phosphates as GRAS excipients

- 10.3.2 METAL OXIDES

- 10.3.2.1 Metal oxides to help meet rising demand for iron-enriched nutraceuticals

- 10.3.3 HALITES

- 10.3.3.1 Halites to ensure taste improvement and salting-out techniques

- 10.3.4 CALCIUM CARBONATE

- 10.3.4.1 Focus on R&D of calcium carbonate to help launch new products

- 10.3.5 CALCIUM SULFATE

- 10.3.5.1 Improved flowability to drive demand for calcium sulfate

- 10.3.6 OTHER INORGANIC CHEMICALS

- 10.3.1 CALCIUM PHOSPHATE

- 10.4 OTHER CHEMICALS

11 NUTRACEUTICAL EXCIPIENTS MARKET, BY FUNCTIONALITY APPLICATION

- 11.1 INTRODUCTION

- 11.2 TASTE MASKING

- 11.2.1 CREATING DIFFERENTIATION IS KEY IN THIS COMPETITIVE MARKET

- 11.3 STABILIZERS

- 11.3.1 MAINTAINING DESIRABLE PROPERTIES UNTIL CONSUMPTION TO DRIVE DEMAND FOR STABILIZERS

- 11.4 MODIFIED RELEASE

- 11.4.1 NEED FOR SLOWER AND STEADIER RELEASE OF COMPOUNDS TO PROPEL GROWTH OF MODIFIED-RELEASE APPLICATIONS IN NUTRACEUTICAL EXCIPIENTS MARKET

- 11.5 SOLUBILITY & BIOAVAILABILITY ENHANCEMENT

- 11.5.1 CHALLENGES RELATED TO POOR SOLUBILITY AND LIMITED ABSORPTION OF BIOACTIVE COMPOUNDS TO DRIVE DEMAND

- 11.6 OTHER FUNCTIONALITY APPLICATIONS

12 NUTRACEUTICAL EXCIPIENTS MARKET, BY FORMULATION

- 12.1 INTRODUCTION

- 12.2 DRY

- 12.2.1 TABLETS

- 12.2.1.1 Easy-to-carry and portable nature makes them attractive option

- 12.2.2 CAPSULES

- 12.2.2.1 Quick-dissolving capsule shells for targeted absorption are ideal for nutraceuticals designed to act in specific areas of digestive tract

- 12.2.1 TABLETS

- 12.3 LIQUID

- 12.3.1 POTENTIAL GROWTH OPPORTUNITIES FOR LIQUID NUTRACEUTICAL EXCIPIENTS DUE TO INNOVATIONS IN FORMULATIONS TO DRIVE GROWTH

- 12.4 OTHER FORMULATIONS

13 NUTRACEUTICAL EXCIPIENTS MARKET, BY FUNCTIONALITY

- 13.1 INTRODUCTION

- 13.2 BINDERS

- 13.2.1 INCREASED ACCEPTANCE AND USE OF BINDING AGENTS IN PRODUCTS TO DRIVE GROWTH OF NUTRACEUTICAL EXCIPIENTS MARKET

- 13.3 FILLERS & DILUENTS

- 13.3.1 USE OF ACTIVE INGREDIENTS IN NUTRACEUTICAL PRODUCTS TO ENCOURAGE USE OF FILLERS AND DILUENTS AS EXCIPIENTS

- 13.4 DISINTEGRANTS

- 13.4.1 HIGH CONSUMPTION OF DIETARY SUPPLEMENTS IN FORM OF ORAL DOSAGES OR TABLETS TO DRIVE GROWTH OF DISINTEGRANTS SEGMENT

- 13.5 COATING AGENTS

- 13.5.1 PROTECTION FROM MOISTURE AND BACTERIA TO DRIVE DEMAND

- 13.6 FLAVORING AGENTS & SWEETENERS

- 13.6.1 INCREASE IN NEED FOR MASKING STRONG AND UNAPPEALING FLAVORS TO DRIVE GROWTH OF SEGMENT

- 13.7 PRESERVATIVES

- 13.7.1 INHIBITION OF MICROBIAL GROWTH AND MAINTAINING PRODUCT QUALITY AND SAFETY TO DRIVE DEMAND FOR PRESERVATIVES

- 13.8 LUBRICANTS & GLIDANTS

- 13.8.1 INCREASE IN NEED FOR REDUCING FRICTION AND KEEPING FORMULATION INTACT DURING PRODUCTION PROCESS TO DRIVE GROWTH OF SEGMENT

- 13.9 SUSPENDING & VISCOSITY AGENTS

- 13.9.1 PREVENTING SETTLING TO HELP MAINTAIN HOMOGENEITY AND STABILITY OF PRODUCT

- 13.10 COLORANTS

- 13.10.1 NEED FOR VISUAL APPEAL AND PRODUCT DIFFERENTIATION TO FUEL DEMAND FOR COLORANTS

- 13.11 EMULSIFYING AGENTS

- 13.11.1 NEED FOR REDUCING SURFACE TENSION BETWEEN DIFFERENT COMPONENTS TO DRIVE DEMAND FOR EMULSIFYING AGENTS

- 13.12 OTHER FUNCTIONALITIES

14 NUTRACEUTICAL EXCIPIENTS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 High concentration of key players, various nutrition awareness programs, and increase in preventive healthcare trends in US

- 14.2.2 CANADA

- 14.2.2.1 Demand for quality and cost-competition: Two key factors for manufacturers to consider in Canada

- 14.2.3 MEXICO

- 14.2.3.1 Increase in foreign direct investments and rise in awareness regarding healthier lifestyles associated with dietary supplements

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Demand for nutraceutical excipients is likely to increase to serve health-conscious consumers

- 14.3.2 FRANCE

- 14.3.2.1 Innovations in product formulations to cater to increased consumer demands

- 14.3.3 UK

- 14.3.3.1 Growth of functional/fortified food & beverage industry in UK to drive demand for nutraceutical excipients

- 14.3.4 ITALY

- 14.3.4.1 Growing trend of online OTC and food supplement purchases in Italy

- 14.3.5 SPAIN

- 14.3.5.1 Excipient manufacturers expand Iberian operations to support tablets and capsules marketed across Spain

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Rise in preference for nutraceutical products and innovations in dietary supplement formulations and fortified food products

- 14.4.2 JAPAN

- 14.4.2.1 Manufacturers should think beyond pills & innovation to tap this growing market in Japan

- 14.4.3 INDIA

- 14.4.3.1 Government policies and importance of nutraceuticals in daily life

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Rapid growth of supplements industry in South Korea

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Growth in awareness regarding the benefits of functional foods and rise in aging population in Brazil

- 14.5.2 ARGENTINA

- 14.5.2.1 Country's focus on prevention healthcare system to be positive sign for nutraceutical excipients market

- 14.5.3 REST OF SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.6 REST OF THE WORLD (ROW)

- 14.6.1 MIDDLE EAST

- 14.6.1.1 Rise in obesity and other health-related concerns in Middle East

- 14.6.2 AFRICA

- 14.6.2.1 Intra-African trade policies and investments by global nutraceutical players

- 14.6.1 MIDDLE EAST

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2024

- 15.3 REVENUE ANALYSIS, 2022-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 BRAND/PRODUCT COMPARISON

- 15.5.1 KERRY GROUP PLC (IRELAND)

- 15.5.2 INGREDION (US)

- 15.5.3 BASF (GERMANY)

- 15.5.4 ASSOCIATED BRITISH FOODS PLC (UK)

- 15.5.5 SENSIENT TECHNOLOGIES CORPORATION (US)

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Source footprint

- 15.6.5.4 Functionality footprint

- 15.6.5.5 Functionality application footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8.1 COMPANY VALUATION

- 15.8.2 EV/EBITDA

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 KERRY GROUP PLC

- 16.1.1.1 Business overview

- 16.1.1.2 Product/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 INGREDION

- 16.1.2.1 Business overview

- 16.1.2.2 Product/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 BASF SE

- 16.1.3.1 Business overview

- 16.1.3.2 Product/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.3.2 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 ASSOCIATED BRITISH FOODS PLC

- 16.1.4.1 Business overview

- 16.1.4.2 Product/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 SENSIENT TECHNOLOGIES CORPORATION

- 16.1.5.1 Business overview

- 16.1.5.2 Product/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 CARGILL, INCORPORATED

- 16.1.6.1 Business overview

- 16.1.6.2 Product/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Expansions

- 16.1.6.4 MnM view

- 16.1.6.4.1 Right to win

- 16.1.6.4.2 Strategic choices

- 16.1.6.4.3 Weaknesses and competitive threats

- 16.1.7 AZELIS

- 16.1.7.1 Business overview

- 16.1.7.2 Product/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Expansions

- 16.1.7.4 MnM view

- 16.1.7.4.1 Right to win

- 16.1.7.4.2 Strategic choices

- 16.1.7.4.3 Weaknesses and competitive threats

- 16.1.8 ASHLAND

- 16.1.8.1 Business overview

- 16.1.8.2 Product/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.8.3.2 Other developments

- 16.1.8.4 MnM view

- 16.1.8.4.1 Right to win

- 16.1.8.4.2 Strategic choices

- 16.1.8.4.3 Weaknesses and competitive threats

- 16.1.9 MEGGLE HOLDING SE

- 16.1.9.1 Business overview

- 16.1.9.2 Product/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.9.4 MnM view

- 16.1.9.4.1 Right to win

- 16.1.9.4.2 Strategic choices

- 16.1.9.4.3 Weaknesses and competitive threats

- 16.1.10 ROQUETTE FRERES

- 16.1.10.1 Business overview

- 16.1.10.2 Product/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches

- 16.1.10.3.2 Deals

- 16.1.10.3.3 Expansions

- 16.1.10.4 MnM view

- 16.1.10.4.1 Right to win

- 16.1.10.4.2 Strategic choices

- 16.1.10.4.3 Weaknesses and competitive threats

- 16.1.11 COLORCON, INC.

- 16.1.11.1 Business overview

- 16.1.11.2 Product/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.11.3.2 Deals

- 16.1.11.3.3 Expansions

- 16.1.11.3.4 Other developments

- 16.1.11.4 MnM view

- 16.1.11.4.1 Right to win

- 16.1.11.4.2 Strategic choices

- 16.1.11.4.3 Weaknesses and competitive threats

- 16.1.12 ALSIANO A/S

- 16.1.12.1 Business overview

- 16.1.12.2 Product/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.4 MnM view

- 16.1.12.4.1 Right to win

- 16.1.12.4.2 Strategic choices

- 16.1.12.4.3 Weaknesses and competitive threats

- 16.1.13 JIGS CHEMICAL

- 16.1.13.1 Business overview

- 16.1.13.2 Product/Solutions/Services offered

- 16.1.13.3 MnM view

- 16.1.13.3.1 Right to win

- 16.1.13.3.2 Strategic choices

- 16.1.13.3.3 Weaknesses and competitive threats

- 16.1.14 IMCD

- 16.1.14.1 Business overview

- 16.1.14.2 Product/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Deals

- 16.1.14.3.2 Expansions

- 16.1.14.4 MnM view

- 16.1.14.4.1 Right to win

- 16.1.14.4.2 Strategic choices

- 16.1.14.4.3 Weaknesses and competitive threats

- 16.1.15 HILMAR CHEESE COMPANY, INC.

- 16.1.15.1 Business overview

- 16.1.15.2 Product/Solutions/Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Expansions

- 16.1.15.4 MnM view

- 16.1.15.4.1 Right to win

- 16.1.15.4.2 Strategic choices

- 16.1.15.4.3 Weaknesses and competitive threats

- 16.1.16 OMYA

- 16.1.16.1 Business overview

- 16.1.16.2 Product/Solutions/Services offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Deals

- 16.1.16.4 MnM view

- 16.1.17 BIOGRUND

- 16.1.17.1 Business overview

- 16.1.17.2 Product/Solutions/Services offered

- 16.1.17.3 Recent developments

- 16.1.17.3.1 Deals

- 16.1.17.3.2 Expansions

- 16.1.17.4 MnM view

- 16.1.18 JRS PHARMA

- 16.1.18.1 Business overview

- 16.1.18.2 Product/Solutions/Services offered

- 16.1.18.3 Recent developments

- 16.1.18.3.1 Product launches

- 16.1.18.3.2 Expansions

- 16.1.18.4 MnM view

- 16.1.19 INNOPHOS

- 16.1.19.1 Business overview

- 16.1.19.2 Product/Solutions/Services offered

- 16.1.19.3 Recent developments

- 16.1.19.3.1 Expansions

- 16.1.19.4 MnM view

- 16.1.20 NOVO EXCIPIENTS PVT. LTD.

- 16.1.20.1 Business overview

- 16.1.20.2 Products offered

- 16.1.20.3 MnM view

- 16.1.21 PANCHAMRUT CHEMICALS

- 16.1.22 GATTEFOSSE

- 16.1.23 FUJI CHEMICAL INDUSTRIES CO., LTD.

- 16.1.24 SUDEEP PHARMA LIMITED

- 16.1.25 SORSE TECHNOLOGIES

- 16.1.1 KERRY GROUP PLC

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key primary participants

- 17.1.2.2.1 Nutraceutical excipients companies

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 TOP-DOWN APPROACH

- 17.3 DATA TRIANGULATION

- 17.4 FACTOR ANALYSIS

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 RELATED REPORTS

- 18.4 AUTHOR DETAILS