|

시장보고서

상품코드

1928854

동물 정형외과 시장 : 제품별, 동물 유형별, 용도별, 재료별, 최종사용자별, 지역별 - 세계 예측(-2031년)Veterinary Orthopedics Market by Product (Orthopedic Implants, Instruments, Consumables), Animal Type (Dog, Cat, Horse, Livestock), Application (TPLO, TTA, Fracture Repair), Material (Metallic, Absorbable), End User, and Region - Global Forecast to 2031 |

||||||

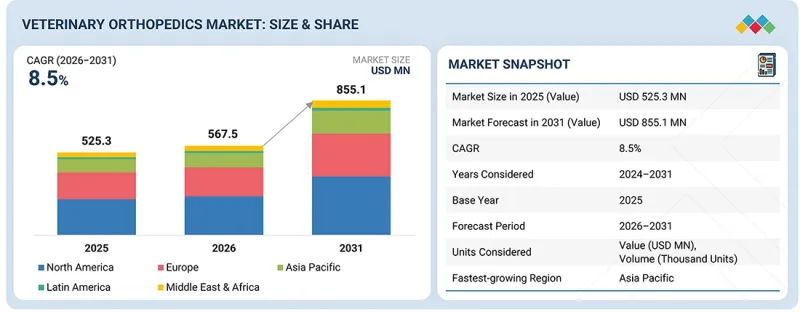

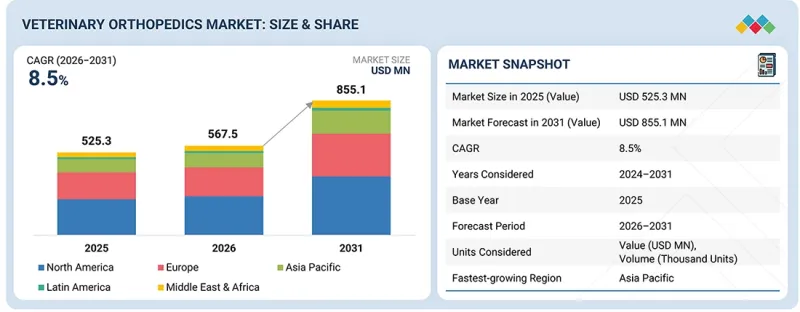

세계의 동물 정형외과 시장 규모는 2026년 5억 7,000만에서 2031년까지 8억 6,000만 달러에 달할 것으로 예측되며, CAGR로 8.5%의 성장이 전망됩니다.

이러한 성장은 동물 정형외과 치료, 외과적 개입, 동물의 운동 기능 회복의 미래를 형성하는 여러 요인에 의해 촉진되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 10억 달러 |

| 부문 | 제품, 용도, 재료, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카 |

반려동물과 가축의 근골격계 질환, 외상, 퇴행성 관절 질환의 발병률 증가, 반려동물 보호자들의 첨단 정형외과 수술에 대한 선호도 증가가 이 시장의 주요 촉진요인으로 작용할 것으로 보입니다. 수의학이 보다 전문화되고 결과 중심의 진료로 꾸준히 진화하면서 우수한 정형외과용 임플란트, 고정장치, 수술 지향적 수술 솔루션에 대한 수요가 증가하고 있습니다. 동물병원과 전문 진료소에서는 수술의 정확성, 회복 시간, 수술 후 이동성을 향상시킬 수 있는 혁신적인 솔루션이 요구되고 있습니다.

또한, 노화에 따른 정형외과적 질환, 비만 가축의 관절 질환, 외상 관련 사례의 증가로 인해 효과적이고 신뢰할 수 있는 표준화된 정형외과적 수술의 필요성이 증가하고 있습니다. 첨단 고정장치, 관절 안정화 제품, 재건 제품은 이러한 요구에 부응하는 데 중요한 역할을 합니다. 소개환자의 증가와 전문화된 정형외과 진료도 수술 건수 증가에 힘을 보태고 있습니다. 이미징의 발전, 디지털 수술 계획, 수술 후 재활 치료 등 동물 의료 부문의 현대화 추세는 정형외과 분야에서 첨단 솔루션의 채택 확대를 촉진하고 있습니다. 외과 의사의 교육 및 증거에 기반한 모범 사례에 대한 관심이 높아짐에 따라 채용률이 더욱 향상되고 있습니다.

강화된 생체 재료, 특정 환자 동물용 기기, 최소침습 수술, 3D 프린팅 수술 가이드 등의 기술 개발로 인해 동물 정형외과 시장이 발전하고 있습니다. 기기의 품질과 사용 편의성 향상은 예측 기간 동안 동물 정형외과 시장의 성장에 기여할 것으로 보입니다.

"동물 유형별로는 반려동물 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다."

개와 고양이는 노화와 비만으로 인해 인대파열, 골절, 관절질환 등 정형외과적 질환에 걸리기 쉽기 때문에 이러한 제품에 대한 수요는 항상 존재합니다. 또한, 전문 동물병원에 대한 접근성, 반려동물 보호자들 사이에서 이러한 수술의 결과에 대한 인식이 확산되고, 반려동물 보험 가입률이 점진적으로 증가하고 있는 것도 이러한 성장을 뒷받침하고 있습니다.

"최종사용자별로는 동물병원 및 진료소 부문이 2025년 가장 큰 시장 점유율을 차지했습니다."

2025년 동물병원 및 클리닉 부문이 동물 정형외과 시장을 주도했습니다. 이는 동물의 정형외과 질환의 진단, 수술, 수술 후 후속 치료의 주요 수행 장소이기 때문입니다. 동물병원 및 클리닉에서 치료하는 외상, 인대손상, 퇴행성 관절질환의 수는 여전히 많으며, 정교한 수술장비와 정형외과적 치료능력을 갖춘 시설이 증가하는 추세입니다. 또한, 여러 전문분야를 가진 동물병원의 발전과 소개가 아닌 병원 내 정형외과 진료에 대한 노력은 동물병원 및 동물병원의 이용 증가 요인으로 작용하고 있습니다.

"아시아태평양이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

아시아태평양은 동물 정형외과 시장에서 가장 높은 CAGR을 보일 가능성이 높습니다. 이는 중국, 인도, 일본, 호주 등의 국가에서 반려동물을 키우는 가구 수가 급증하고 동물 의료비가 지속적으로 증가하고 있기 때문입니다. 정형외과 전문병원과 진료 의뢰 센터의 발달로 수의학 인프라가 개선되면서 진단 검사 및 수술에 대한 접근성이 확대되고 있습니다. 또한, 삶의 질에 있어 운동 기능의 중요성에 대한 인식의 증가, 정형외과 의사의 가용성, 반려동물 보험의 이용 확대 등이 수술의 도입을 촉진하고 있습니다.

세계의 동물 정형외과 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

- 동물 정형외과 시장 개요

- 아시아태평양의 동물 정형외과 시장 : 제품별, 국가별(2025년)

- 동물 정형외과 시장 : 지역 구성

- 동물 정형외과 시장 : 지리적 성장 기회

- 동물 정형외과 시장 : 선진국 vs. 신흥국

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 수요와 화이트 스페이스

- 동물 정형외과 시장의 미충족 수요

- 화이트 스페이스 기회

- 상호 접속된 시장과 부문 횡단적인 기회

- 상호 접속된 시장

- 부문 횡단적인 기회

- Tier 1/2/3 기업의 전략적 활동

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 지표

- GDP 동향과 예측

- 세계의 의료 업계 동향

- 세계의 동물 의료 업계 동향

- 공급망 분석

- 밸류체인 분석

- 생태계 분석

- 가격 책정 분석

- 동물 정형외과 제품 평균판매가격 동향 : 주요 기업별(2023-2025년)

- 동물 정형외과 제품 평균판매가격 동향 : 재료별(2023-2025년)

- 동물 정형외과 제품 평균판매가격 동향 : 지역별(2023-2025년)

- 무역 분석

- HS 코드 9021의 무역 데이터

- HS 코드 9018의 무역 데이터

- 주요 회의와 이벤트(2026-2027년)

- 고객 비즈니스에 영향을 미치는 동향/디스럽션

- 투자와 자금 조달 시나리오

- 성공 사례와 실세계에 대한 응용

- 복잡한 개 사지 재건에 활용되는 특정 환축용 3D 프린팅 임플란트

- 최신 정형외과 임플란트 시스템을 이용한 소동물의 첨단 골절 고정

- 반려동물에서의 첨단 정형외과 수술 개입의 장기 임상 결과

- 동물 정형외과 시장에 대한 2025년 미국 관세의 영향

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종 이용 산업에 대한 영향

제6장 기술, 특허, 디지털과 AI 채용에 의한 전략적 파괴

- 기술 분석

- 주요 신기술

- 보완 기술

- 인접 기술

- 기술/제품 로드맵

- 단기(2025-2027년)

- 중기(2028-2030년)

- 장기(2030년 이후)

- 특허 분석

- 동물 정형외과의 특허 공보 동향

- 관할구역과 주요 신청자 분석

- 향후 용도

- 특정 환축용 정형외과 임플란트 및 수술 가이드

- 저침습·영상 유도 정형외과 수술

- 재생의료와 생물학적 제제를 활용한 정형외과 치료

- 디지털 수술 계획과 AI가 지원하는 의사 결정 지원

- 통합 재활, 모빌리티 트래킹, 장기적 성과 관리

- 동물 정형외과 시장에 대한 AI/생성형 AI의 영향

- 동물 정형외과 생태계의 시장 전망

- AI 이용 사례

- 동물 정형외과 시장에서 AI를 도입하고 있는 주요 기업

제7장 지속가능성과 규제 상황

- 지역 규제와 컴플라이언스

- 규제 분석

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 지속가능성에 대한 대처

- 동물 정형외과 제품용 재생 재료, 친환경 재료

- 지속가능성에 대한 영향과 규제 정책의 대처

- 인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

- 주요 이해관계자와 구입 기준

- 고객 상황과 구매 행동

- 의사결정 프로세스

- 채용 장벽과 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 수요

- 시장 수익성

제9장 동물 정형외과 시장 : 제품별

- 임플란트

- 기구

- 소모품

제10장 동물 정형외과 시장 : 재료별

- 금속

- 흡수성

제11장 동물 정형외과 시장 : 동물 유형별

- 반려동물

- 가축

제12장 동물 정형외과 시장 : 용도별

- 관절 치환술

- 상처 고정

- 특정 수술

제13장 동물 정형외과 시장 : 최종사용자별

- 동물병원·진료소

- 전문 정형외과 클리닉

- 구급 동물병원

- 학술연구기관

- 동물 재활 센터

제14장 동물 정형외과 시장 : 지역별

- 세계의 동물 정형외과 시장 수량 분석(2024-2031년)

- 북미

- 북미의 거시경제 전망

- 북미의 수량 분석 : 제품별(2024-2031년)

- 북미의 수량 분석 : 재료별(2024-2031년)

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 유럽의 수량 분석 : 제품별(2024-2031년)

- 유럽의 수량 분석 : 재료별(2024-2031년)

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타 유럽

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 아시아태평양의 수량 분석 : 제품별(2024-2031년)

- 아시아태평양의 수량 분석 : 재료별(2024-2031년)

- 중국

- 일본

- 인도

- 호주

- 한국

- 태국

- 뉴질랜드

- 기타 아시아태평양

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 라틴아메리카의 수량 분석 : 제품별(2024-2031년)

- 라틴아메리카의 수량 분석 : 재료별(2024-2031년)

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- 중동 및 아프리카의 수량 분석 : 제품별(2024-2031년)

- 중동 및 아프리카의 수량 분석 : 재료별(2024-2031년)

- GCC 국가

- 기타 중동 및 아프리카

제15장 경쟁 구도

- 개요

- 주요 진출 기업의 전략/강점

- 매출 분석(2021-2025년)

- 시장 점유율 분석(2025년)

- 미국의 시장 점유율 분석(2025년)

- 유럽의 시장 점유율 분석(2025년)

- 주요 시장 기업 순위

- 기업 평가 매트릭스 : 주요 기업(2025년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2025년)

- 브랜드/제품의 비교

- 주요 기업 연구개발비

- 기업 평가와 재무 지표

- 경쟁 시나리오

제16장 기업 개요

- 주요 기업

- MOVORA

- SECUROS SURGICAL(CENCORA, INC.)

- DEPUY SYNTHES(JOHNSON & JOHNSON)

- ARTHREX, INC.

- ORTHOMED(UK) LTD.

- B. BRAUN SE

- VETERINARY INSTRUMENTATION

- ANTECH DIAGNOSTICS, INC.

- RITA LEIBINGER GMBH & CO. KG

- BLUESAO

- INTEGRA LIFESCIENCES CORPORATION

- INTRAUMA S.P.A

- SURGICAL HOLDINGS VETERINARY

- PH ORTHCOM

- GERVETUSA

- 기타 기업

- NARANG MEDICAL LIMITED

- FUSION IMPLANTS

- BIO3DTECH

- ORTHOMAX MFG. CO. PVT. LTD.

- VET ORTHOPEDICS

- WELL TRUST(TIANJIN) TECH CO., LTD.

- VETERINARYIMPLANTS.COM(VETERINARY DIVISION OF GPC MEDICAL LTD.)

- INVICTOS

- SAFEX INC.

- GSOURCE(ARCH MEDICAL SOLUTIONS)

제17장 조사 방법

제18장 부록

KSM 26.02.24The veterinary orthopedics market is expected to grow from USD 0.57 billion in 2026 to USD 0.86 billion by 2031, at a CAGR of 8.5%. This growth is driven by several key factors shaping the future of veterinary orthopedic care, surgical intervention, and mobility restoration in animals.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Product, Application, Material, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and the Middle East & Africa |

The key factor driving this market is the rising incidence of musculoskeletal disorders, trauma, and degenerative joint diseases in companion and livestock animals, as well as the growing willingness of pet owners to opt for advanced orthopedic procedures. With the steady evolution of veterinary care toward greater specialization and results-oriented care, there is a growing demand for superior orthopedic implants, fixation devices, and procedure-oriented surgical solutions. Veterinary hospitals and specialty practices are seeking innovative solutions to improve surgical accuracy, recovery time, and post-surgical mobility.

In addition, the increasing prevalence of age-related orthopedic diseases, joint diseases in obese patients, and trauma-related cases is increasing the need for effective, reliable, and standardized orthopedic procedures. Advanced fixation devices, joint stabilizing, and reconstructive products are important in meeting this need. Increased referrals and specialized orthopedic practices are also fueling growth in procedures. Current modernization trends in the veterinary health sector, such as advancements in imaging, digital surgical planning, and post-operative rehabilitative care, are also driving increased adoption of advanced solutions in the orthopedic space. A growing emphasis on surgeon education and evidence-based best practices is further improving adoption rates.

Advances in the veterinary orthopedics market, driven by technological developments such as enhanced biomaterials and patient-specific devices, minimally invasive procedures, and 3D-printed surgical guides, are propelling the market forward. Enhancements in the quality and ease of usage of devices will contribute to the growth of the veterinary orthopedics market during the forecasted period.

"By animal type, the companion animals segment is projected to grow at the highest CAGR during the forecast period."

Dogs and cats are more prone to orthopedic disorders, such as ligament tears, fractures, and joint disorders, due to aging or obesity; hence, there is a constant demand for these products. Further, the easy accessibility of specialty animal hospitals, the growing awareness among owners of the outcomes of these procedures, and the gradually increasing adoption rate of pet insurance plans are also supporting this growth.

"By end user, the veterinary hospitals & clinics segment accounted for the largest market share in 2025."

In 2025, the veterinary hospitals & clinics segment dominated the veterinary orthopedics market as they are the primary locations for diagnosis and surgical and post-surgical follow-up treatments for orthopedic disorders in animals. The number of trauma cases, ligament injuries, and degenerative joint disorders treated by veterinary hospitals and clinics remains high, and they are increasingly set up with highly sophisticated surgical facilities and orthopedic capabilities. Moreover, the increased development of multi-specialty veterinary hospitals and the in-house approach to orthopedic care, rather than referral orthopedic care, are responsible for increased use within veterinary hospitals and clinics.

"The Asia Pacific region is expected to witness the highest growth rate during the forecast period."

The Asia Pacific region is likely to report the highest CAGR in the veterinary orthopedics market. This is due to the accelerated growth in the number of pet owners and continued increases in expenditure on animal care in countries such as China, India, Japan, and Australia. The improvement in veterinary infrastructure, with the development of orthopedic specialty hospitals and referral centers, is creating greater access to diagnostic work-ups and surgeries. Further, the growing recognition of the role of mobility in quality of life, along with the availability of orthopedic surgeons and the increased availability of pet insurance, is fueling the uptake of surgical procedures.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By End User: Veterinary Hospitals & Clinics (45%), Specialty Orthopedic Clinics (24%), Emergency Animal Hospitals (14%), Academic & Research Institutes (10%), and Animal Rehabilitation Centers (7%)

By Designation: Veterinarians (47%), Veterinary Hospital Directors & Managers (22%), Veterinary Critical Care Specialists (15%), and Others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the veterinary orthopedics market in various segments. It aims to estimate the market size and growth potential by product, material, animal type, application, end user, and region. The study also includes an in-depth competitive analysis of the market's key players, along with their company profiles, key observations on their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger share of the market. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (rising companion animal ownership & spending on pet healthcare, higher incidence of orthopedic conditions, and growth in specialty veterinary hospitals & referral networks with advanced surgical capabilities and technology improvements in implants and instruments), restraints (high cost of orthopedic implants, instruments, and advanced surgical procedures and limited availability of trained veterinary orthopedic surgeons), opportunities (geographic expansion into emerging markets and growing adoption of patient-specific implants and 3d-printed guides), and challenges (clinical outcome variability and complication risk and regulatory and quality compliance across regions) influencing the growth of the veterinary orthopedics market.

- Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the veterinary orthopedics market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of veterinary orthopedic products across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary orthopedics market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary orthopedics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 MARKET STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN VETERINARY ORTHOPEDICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 VETERINARY ORTHOPEDICS MARKET OVERVIEW

- 3.2 ASIA PACIFIC: VETERINARY ORTHOPEDICS MARKET, BY PRODUCT & COUNTRY (2025)

- 3.3 VETERINARY ORTHOPEDICS MARKET: REGIONAL MIX

- 3.4 VETERINARY ORTHOPEDICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.5 VETERINARY ORTHOPEDICS MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising companion animal ownership and spending on pet healthcare

- 4.2.1.2 Higher incidence of orthopedic conditions

- 4.2.1.3 Growth in specialty veterinary hospitals & referral networks with advanced surgical capabilities

- 4.2.1.4 Technology improvements in implants and instruments

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of orthopedic implants, instruments, and advanced surgical procedures

- 4.2.2.2 Limited availability of trained veterinary orthopedic surgeons

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Geographic expansion into emerging markets

- 4.2.3.2 Growing adoption of patient-specific implants and 3D-printed guides

- 4.2.4 CHALLENGES

- 4.2.4.1 Clinical outcome variability and complication risk

- 4.2.4.2 Regulatory and quality compliance across regions

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN VETERINARY ORTHOPEDICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ANIMAL HEALTH INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF VETERINARY ORTHOPEDIC PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.6.1.1 Average selling price trend of veterinary orthopedic plates, by key player, 2023-2025

- 5.6.1.2 Average selling price trend of veterinary orthopedic screws, by key player, 2023-2025

- 5.6.1.3 Average selling price trend of veterinary orthopedic instruments, by key player, 2023-2025

- 5.6.1.4 Average selling price trend of veterinary orthopedic consumables, by key player, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF VETERINARY ORTHOPEDIC PRODUCTS, BY MATERIAL TYPE, 2023-2025

- 5.6.2.1 Average selling price trend of metallic veterinary orthopedic products, by type, 2023-2025

- 5.6.2.2 Average selling price trend of absorbable veterinary orthopedic products, by type, 2023-2025

- 5.6.3 AVERAGE SELLING PRICE TREND OF VETERINARY ORTHOPEDIC PRODUCTS, BY REGION, 2023-2025

- 5.6.3.1 Average selling price trend of compression plates, by region, 2023-2025

- 5.6.3.2 Average selling price trend of locking plates, by region, 2023-2025

- 5.6.3.3 Average selling price trend of locking screws, by region, 2023-2025

- 5.6.3.4 Average selling price trend of drilling systems, by region, 2023-2025

- 5.6.3.5 Average selling price trend of cutting tools, by region, 2023-2025

- 5.6.1 AVERAGE SELLING PRICE TREND OF VETERINARY ORTHOPEDIC PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 TRADE DATA FOR HS CODE 9021

- 5.7.1.1 Import data for HS Code 9021

- 5.7.1.2 Export data for HS Code 9021

- 5.7.2 TRADE DATA FOR HS CODE 9018

- 5.7.2.1 Import data for HS Code 9018

- 5.7.2.2 Export data for HS Code 9018

- 5.7.1 TRADE DATA FOR HS CODE 9021

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 5.11.1 PATIENT-SPECIFIC 3D-PRINTED IMPLANTS FOR COMPLEX CANINE LIMB RECONSTRUCTION

- 5.11.2 ADVANCED FRACTURE FIXATION IN SMALL ANIMALS USING MODERN ORTHOPEDIC IMPLANT SYSTEMS

- 5.11.3 LONG-TERM CLINICAL OUTCOMES OF ADVANCED ORTHOPEDIC SURGICAL INTERVENTIONS IN COMPANION ANIMALS

- 5.12 IMPACT OF 2025 US TARIFFS ON VETERINARY ORTHOPEDICS MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRY/REGION

- 5.12.4.1 North America

- 5.12.4.2 Asia Pacific

- 5.12.4.3 Europe

- 5.12.4.4 Latin America

- 5.12.5 IMPACT ON END-USE INDUSTRIES

- 5.12.5.1 Veterinary hospitals & clinics

- 5.12.5.2 Specialty orthopedic clinics

- 5.12.5.3 Emergency animal hospitals

- 5.12.5.4 Academic & research institutes

- 5.12.5.5 Animal rehabilitation centers

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Patient-specific 3D printing

- 6.1.1.2 Minimally invasive orthopedic techniques

- 6.1.1.3 Bioresorbable/Biodegradable implants

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 C-arm/Fluoroscopy & cone-beam CT units

- 6.1.2.2 On-site bone printing/Bone glue-gun approaches

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Small animal prosthetics and orthoses

- 6.1.3.2 Implant surface engineering and coatings

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR TERM (2025-2027)

- 6.2.2 MID TERM (2028-2030)

- 6.2.3 LONG TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR VETERINARY ORTHOPEDICS

- 6.3.2 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 PATIENT-SPECIFIC ORTHOPEDIC IMPLANTS AND SURGICAL GUIDES

- 6.4.2 MINIMALLY INVASIVE AND IMAGE-GUIDED ORTHOPEDIC SURGERY

- 6.4.3 REGENERATIVE AND BIOLOGICS-ENHANCED ORTHOPEDIC THERAPIES

- 6.4.4 DIGITAL SURGICAL PLANNING AND AI-ASSISTED DECISION SUPPORT

- 6.4.5 INTEGRATED REHABILITATION, MOBILITY TRACKING, AND LONG-TERM OUTCOME MANAGEMENT

- 6.5 IMPACT OF AI/GENERATIVE AI ON VETERINARY ORTHOPEDICS MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL IN VETERINARY ORTHOPEDICS ECOSYSTEM

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI IN VETERINARY ORTHOPEDICS MARKET

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY ANALYSIS

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RECYCLED AND ECO-FRIENDLY MATERIALS FOR VETERINARY ORTHOPEDIC PRODUCTS

- 7.2.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 VETERINARY ORTHOPEDICS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 IMPLANTS

- 9.2.1 PLATES

- 9.2.1.1 Global volume analysis of plates, 2024-2031 (thousand units)

- 9.2.1.2 Compression plates

- 9.2.1.2.1 Continued preference for absolute stability in simple fractures to drive steady demand for compression plates

- 9.2.1.3 Locking plates

- 9.2.1.3.1 Growing cases of biologically challenged fractures and osteotomies to propel locking plate adoption

- 9.2.1.4 T-plates

- 9.2.1.4.1 Procedure-critical role of T-plates in distal limb fractures to maintain high adoption rates

- 9.2.1.5 L-plates

- 9.2.1.5.1 Growing need for stable corner and juxta-articular fixation to support L-plate adoption

- 9.2.1.6 Other plates

- 9.2.2 SCREWS

- 9.2.2.1 Global volume analysis of screws, 2024-2031 (thousand units)

- 9.2.2.2 Locking screws

- 9.2.2.2.1 Locking screws to gain structural preference as absolute stability becomes critical in complex fractures

- 9.2.2.3 Cortical screws

- 9.2.2.3.1 Broad clinical utility and low unit cost to boost market

- 9.2.3 PINS, WIRES, AND NAILS

- 9.2.3.1 Simple fracture prevalence and cost efficiency to anchor demand for pins, wires, and nails

- 9.2.3.2 Global volume analysis of pins, wires, and nails, 2024-2031 (thousand units)

- 9.2.4 EXTERNAL FIXATORS

- 9.2.4.1 Complex, high-risk fracture management to sustain demand for external fixators

- 9.2.4.2 Global volume analysis of external fixators, 2024-2031 (thousand units)

- 9.2.1 PLATES

- 9.3 INSTRUMENTS

- 9.3.1 DRILLING SYSTEMS

- 9.3.1.1 Complex, high-risk orthopedic procedures to sustain demand for advanced drilling systems

- 9.3.2 CUTTING TOOLS

- 9.3.2.1 Complex orthopedic reconstructions to drive demand for precision cutting instruments

- 9.3.3 SURGICAL POWER TOOLS

- 9.3.3.1 Rising demand for precision, efficiency, and high-throughput orthopedic procedures to drive adoption of surgical power tools

- 9.3.4 ARTHROSCOPY EQUIPMENT

- 9.3.4.1 Rising adoption of minimally invasive joint diagnosis and treatment to drive demand for arthroscopy equipment

- 9.3.1 DRILLING SYSTEMS

- 9.4 CONSUMABLES

- 9.4.1 SUTURES

- 9.4.1.1 Increasing orthopedic surgical volumes and demand for high-performance wound closure to drive growth of veterinary sutures

- 9.4.1.2 Global volume analysis of sutures, 2024-2031 (thousand units)

- 9.4.2 BONE GRAFT MATERIALS

- 9.4.2.1 Increasing need for bone regeneration and defect reconstruction to drive demand for veterinary bone graft materials

- 9.4.2.2 Global volume analysis of bone graft materials, 2024-2031 (thousand units)

- 9.4.3 ORTHOBIOLOGICS

- 9.4.3.1 Rising adoption of regenerative and minimally invasive therapies to drive demand for veterinary orthobiologics

- 9.4.3.2 Global volume analysis of orthobiologics, 2024-2031 (thousand units)

- 9.4.1 SUTURES

10 VETERINARY ORTHOPEDICS MARKET, BY MATERIAL

- 10.1 INTRODUCTION

- 10.2 METALLIC

- 10.2.1 GLOBAL VOLUME ANALYSIS OF METALLIC IMPLANTS, 2024-2031 (THOUSAND UNITS)

- 10.2.2 TITANIUM

- 10.2.2.1 Superior biocompatibility and load-bearing performance to drive adoption of titanium implants in veterinary orthopedics

- 10.2.3 STAINLESS STEEL

- 10.2.3.1 Cost-effective strength and structural reliability to sustain demand for stainless steel implants in veterinary orthopedics

- 10.3 ABSORBABLE

- 10.3.1 GLOBAL VOLUME ANALYSIS OF ABSORBABLE IMPLANTS, 2024-2031 (THOUSAND UNITS)

- 10.3.2 POLYMER

- 10.3.2.1 Preference for gradual load transfer and reduced need for secondary surgery supporting polymer-based implants

- 10.3.3 MAGNESIUM

- 10.3.3.1 Advancements in biodegradable magnesium alloys to support adoption in veterinary orthopedic fixation

- 10.3.4 COMPOSITE BIOABSORBABLE MATERIALS

- 10.3.4.1 Demand for enhanced mechanical strength with biological osteoconductivity to drive adoption of composite bioabsorbable materials

11 VETERINARY ORTHOPEDICS MARKET, BY ANIMAL TYPE

- 11.1 INTRODUCTION

- 11.2 COMPANION ANIMALS

- 11.2.1 DOGS

- 11.2.1.1 High incidence of stifle joint disorders and advanced surgical adoption to drive demand for canine orthopedic implants

- 11.2.2 CATS

- 11.2.2.1 Routine surgical fixation of feline fractures and miniaturized implant innovation to support market growth

- 11.2.3 HORSES

- 11.2.3.1 High lameness burden and arthroscopy-led precision surgery to drive demand for equine orthopedic systems

- 11.2.4 OTHER COMPANION ANIMALS

- 11.2.1 DOGS

- 11.3 LIVESTOCK ANIMALS

- 11.3.1 CATTLE

- 11.3.1.1 High lameness prevalence and field-based fracture management needs to drive demand for large-animal orthopedic fixation systems

- 11.3.2 PIGS

- 11.3.2.1 Lameness-driven productivity to support orthopedic intervention in swine

- 11.3.3 POULTRY

- 11.3.3.1 High prevalence of growth-related skeletal disorders and welfare-driven intervention in high-value birds to drive demand

- 11.3.4 OTHER LIVESTOCK ANIMALS

- 11.3.1 CATTLE

12 VETERINARY ORTHOPEDICS MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 JOINT REPLACEMENT

- 12.2.1 TOTAL HIP REPLACEMENT

- 12.2.1.1 Advancements in implant technology and surgical techniques to drive growth in total hip replacement

- 12.2.2 TOTAL KNEE REPLACEMENT

- 12.2.2.1 Enhanced functional outcomes and reduced recovery time to fuel demand for total knee replacement in veterinary orthopedics

- 12.2.3 TOTAL ELBOW REPLACEMENT

- 12.2.3.1 Innovative prosthetics and improved surgical approaches to drive growth

- 12.2.1 TOTAL HIP REPLACEMENT

- 12.3 TRAUMA FIXATION

- 12.3.1 FRACTURE REPAIR

- 12.3.1.1 Technological advancements in fracture repair materials and methods to enhance healing times and patient recovery

- 12.3.2 LIGAMENT RECONSTRUCTION

- 12.3.2.1 Minimally invasive techniques and advanced materials to accelerate ligament reconstruction procedures

- 12.3.3 BONE DEFORMITY CORRECTION

- 12.3.3.1 Emerging surgical techniques and advanced implants to favor market growth

- 12.3.1 FRACTURE REPAIR

- 12.4 SPECIFIC PROCEDURES

- 12.4.1 TIBIAL PLATEAU LEVELING OSTEOTOMY (TPLO)

- 12.4.1.1 Reduced recovery time and improved post-operative mobility to drive adoption

- 12.4.2 TIBIAL TUBEROSITY ADVANCEMENT (TTA)

- 12.4.2.1 Increased success rates and reduced complication rates to support market growth

- 12.4.3 EXTRACAPSULAR CCL REPAIR

- 12.4.3.1 Cost-effective solutions with reliable outcomes to fuel market growth

- 12.4.4 ARTHROSCOPY

- 12.4.4.1 Minimally invasive techniques and faster recovery times to drive growth of arthroscopy

- 12.4.1 TIBIAL PLATEAU LEVELING OSTEOTOMY (TPLO)

13 VETERINARY ORTHOPEDICS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 VETERINARY HOSPITALS & CLINICS

- 13.2.1 EXPANDING ORTHOPEDIC PROCEDURE VOLUMES IN VETERINARY HOSPITALS & CLINICS TO DRIVE IMPLANT ADOPTION

- 13.3 SPECIALTY ORTHOPEDIC CLINICS

- 13.3.1 RISING REFERRAL COMPLEXITY AT SPECIALTY ORTHOPEDIC CLINICS TO ACCELERATE USE OF ADVANCED FIXATION SYSTEMS

- 13.4 EMERGENCY ANIMAL HOSPITALS

- 13.4.1 INCREASING TRAUMA CASELOADS IN EMERGENCY ANIMAL HOSPITALS TO BOOST DEMAND FOR RAPID STABILIZATION SOLUTIONS

- 13.5 ACADEMIC & RESEARCH INSTITUTES

- 13.5.1 ACADEMIC & RESEARCH INSTITUTES TO ADVANCE ORTHOPEDIC INNOVATION THROUGH CLINICAL TRAINING AND VALIDATION

- 13.6 ANIMAL REHABILITATION CENTERS

- 13.6.1 GROWING INTEGRATION OF ANIMAL REHABILITATION CENTERS TO STRENGTHEN LONG-TERM ORTHOPEDIC CARE PATHWAYS

14 VETERINARY ORTHOPEDICS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 GLOBAL VOLUME ANALYSIS FOR VETERINARY ORTHOPEDICS MARKET, 2024-2031

- 14.3 NORTH AMERICA

- 14.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 14.3.2 NORTH AMERICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031 (THOUSAND UNITS)

- 14.3.3 NORTH AMERICA: VOLUME ANALYSIS, BY MATERIAL, 2024-2031 (THOUSAND UNITS)

- 14.3.4 US

- 14.3.4.1 Rising pet population to drive demand for veterinary orthopedic equipment

- 14.3.5 CANADA

- 14.3.5.1 Rising pet adoption rate to drive market

- 14.4 EUROPE

- 14.4.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 14.4.2 EUROPE: VOLUME ANALYSIS, BY PRODUCT, 2024-2031 (THOUSAND UNITS)

- 14.4.3 EUROPE: VOLUME ANALYSIS, BY MATERIAL, 2024-2031 (THOUSAND UNITS)

- 14.4.4 GERMANY

- 14.4.4.1 Germany to dominate European market

- 14.4.5 UK

- 14.4.5.1 Increasing pet ownership to drive market growth

- 14.4.6 FRANCE

- 14.4.6.1 Rising veterinary healthcare expenditure to drive market

- 14.4.7 ITALY

- 14.4.7.1 Growing livestock population and rising awareness to support market growth

- 14.4.8 SPAIN

- 14.4.8.1 Rising animal population to drive market growth

- 14.4.9 NETHERLANDS

- 14.4.9.1 Large pet population to fuel market growth

- 14.4.10 REST OF EUROPE

- 14.5 ASIA PACIFIC

- 14.5.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 14.5.2 ASIA PACIFIC: VOLUME ANALYSIS, BY PRODUCT, 2024-2031 (THOUSAND UNITS)

- 14.5.3 ASIA PACIFIC: VOLUME ANALYSIS, BY MATERIAL, 2024-2031 (THOUSAND UNITS)

- 14.5.4 CHINA

- 14.5.4.1 China to dominate APAC market

- 14.5.5 JAPAN

- 14.5.5.1 Rising demand for imported breeds to drive market

- 14.5.6 INDIA

- 14.5.6.1 Rising livestock population and growing awareness to boost market growth

- 14.5.7 AUSTRALIA

- 14.5.7.1 Rising livestock animal population and increasing pet ownership to support market growth

- 14.5.8 SOUTH KOREA

- 14.5.8.1 Increasing demand for preventive care and aging pet population to drive market

- 14.5.9 THAILAND

- 14.5.9.1 Increasing companion animal population to boost market growth

- 14.5.10 NEW ZEALAND

- 14.5.10.1 Large pet population to increase demand for orthopedic products

- 14.5.11 REST OF ASIA PACIFIC

- 14.6 LATIN AMERICA

- 14.6.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 14.6.2 LATIN AMERICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031 (THOUSAND UNITS)

- 14.6.3 LATIN AMERICA: VOLUME ANALYSIS, BY MATERIAL, 2024-2031 (THOUSAND UNITS)

- 14.6.4 BRAZIL

- 14.6.4.1 Brazil to dominate LATAM market due to large companion animal population

- 14.6.5 MEXICO

- 14.6.5.1 Rising demand for animal-derived food products to contribute to market growth

- 14.6.6 REST OF LATIN AMERICA

- 14.7 MIDDLE EAST & AFRICA

- 14.7.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 14.7.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031 (THOUSAND UNITS)

- 14.7.3 MIDDLE EAST & AFRICA: VOLUME ANALYSIS, BY MATERIAL, 2024-2031 (THOUSAND UNITS)

- 14.7.4 GCC COUNTRIES

- 14.7.4.1 Kingdom of Saudi Arabia (KSA)

- 14.7.4.1.1 Technology advancements in veterinary orthopedics to boost growth

- 14.7.4.2 United Arab Emirates (UAE)

- 14.7.4.2.1 Government support and high livestock population to fuel UAE's market growth

- 14.7.4.3 Rest of GCC Countries

- 14.7.4.1 Kingdom of Saudi Arabia (KSA)

- 14.7.5 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.4.1 US MARKET SHARE ANALYSIS, 2025

- 15.4.2 EUROPE MARKET SHARE ANALYSIS, 2025

- 15.4.3 RANKING OF KEY MARKET PLAYERS

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Product footprint

- 15.5.5.4 Application footprint

- 15.5.5.5 Animal type footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of key startups

- 15.7 BRAND/PRODUCT COMPARISON

- 15.8 R&D EXPENDITURE OF KEY PLAYERS

- 15.9 COMPANY VALUATION & FINANCIAL METRICS

- 15.9.1 FINANCIAL METRICS

- 15.9.2 COMPANY VALUATION

- 15.10 COMPETITIVE SCENARIO

- 15.10.1 PRODUCT LAUNCHES

- 15.10.2 DEALS

- 15.10.3 EXPANSIONS

- 15.10.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 MOVORA

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 SECUROS SURGICAL (CENCORA, INC.)

- 16.1.2.1 Business overview

- 16.1.2.2 Recent developments

- 16.1.2.2.1 Other developments

- 16.1.2.3 MnM view

- 16.1.2.3.1 Key strengths

- 16.1.2.3.2 Strategic choices

- 16.1.2.3.3 Weaknesses & competitive threats

- 16.1.3 DEPUY SYNTHES (JOHNSON & JOHNSON)

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses & competitive threats

- 16.1.4 ARTHREX, INC.

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses & competitive threats

- 16.1.5 ORTHOMED (UK) LTD.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.3.2 Deals

- 16.1.5.3.3 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses & competitive threats

- 16.1.6 B. BRAUN SE

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.7 VETERINARY INSTRUMENTATION

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.8 ANTECH DIAGNOSTICS, INC.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.9 RITA LEIBINGER GMBH & CO. KG

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.10 BLUESAO

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.11 INTEGRA LIFESCIENCES CORPORATION

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.12 INTRAUMA S.P.A

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.13 SURGICAL HOLDINGS VETERINARY

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.14 PH ORTHCOM

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.15 GERVETUSA

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.1 MOVORA

- 16.2 OTHER PLAYERS

- 16.2.1 NARANG MEDICAL LIMITED

- 16.2.2 FUSION IMPLANTS

- 16.2.3 BIO3DTECH

- 16.2.4 ORTHOMAX MFG. CO. PVT. LTD.

- 16.2.5 VET ORTHOPEDICS

- 16.2.6 WELL TRUST (TIANJIN) TECH CO., LTD.

- 16.2.7 VETERINARYIMPLANTS.COM (VETERINARY DIVISION OF GPC MEDICAL LTD.)

- 16.2.8 INVICTOS

- 16.2.9 SAFEX INC.

- 16.2.10 GSOURCE (ARCH MEDICAL SOLUTIONS)

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.2 RESEARCH METHODOLOGY DESIGN

- 17.2.1 SECONDARY DATA

- 17.2.1.1 Key data from secondary sources

- 17.2.2 PRIMARY DATA

- 17.2.2.1 Key data from primary sources

- 17.2.2.2 Key industry insights

- 17.2.1 SECONDARY DATA

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 17.3.2 APPROACH 2: COMPANY PRESENTATIONS AND PRIMARY INTERVIEWS

- 17.3.3 APPROACH 3: DEMAND-SIDE ANALYSIS

- 17.3.4 TOP-DOWN APPROACH

- 17.3.5 BOTTOM-UP APPROACH

- 17.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 17.5 MARKET SHARE ESTIMATION

- 17.5.1 RESEARCH ASSUMPTIONS

- 17.5.2 GROWTH RATE ASSUMPTIONS

- 17.6 RISK ASSESSMENT

- 17.7 RESEARCH LIMITATIONS

- 17.7.1 METHODOLOGY-RELATED LIMITATIONS

- 17.7.2 SCOPE-RELATED LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.3.1 PRODUCT ANALYSIS

- 18.3.2 COMPANY INFORMATION

- 18.3.3 GEOGRAPHIC ANALYSIS

- 18.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 18.3.5 COUNTRY-LEVEL VOLUME ANALYSIS, BY PRODUCT TYPE

- 18.3.6 MARKET SHARE ANALYSIS, BY PRODUCT (TOP 5 PLAYERS)

- 18.3.7 ANY CONSULT/CUSTOM REQUIREMENTS AS PER CLIENT REQUESTS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS