|

시장보고서

상품코드

1928856

농업용 칼슘 시장 : 유형별, 용도별, 형상별, 기능별, 지역별 - 세계 예측(-2030년)Agricultural Calcium Market by Type (Calcium Carbonate, Calcium Sulfate, Calcium Nitrate, Calcium Chloride, Calcium Oxide and Hydroxide, and Others), Application (Agriculture and Animal Feed), Form, Function, and Region - Global Forecast to 2030 |

||||||

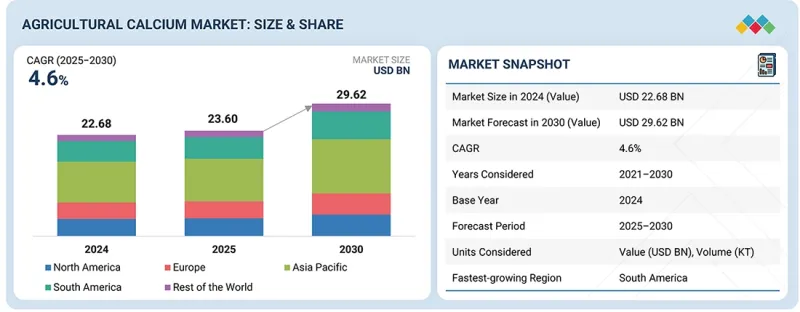

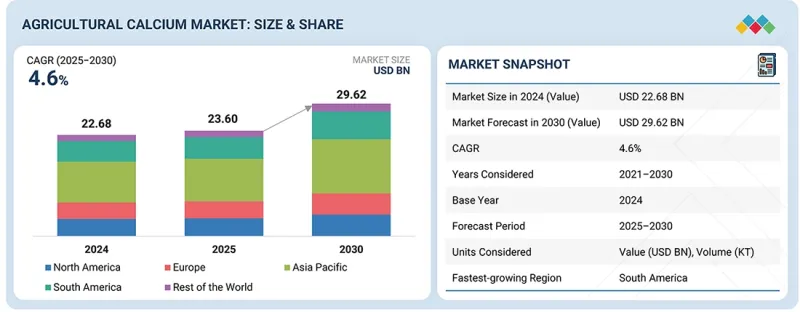

세계의 농업용 칼슘 시장 규모는 2025년에 추정 236억 달러이며, 2030년까지 296억 2,000만 달러에 달할 것으로 예측되며, CAGR로 4.6%의 성장이 전망됩니다.

시장은 지속가능한 정밀농업으로의 전환, 투입되는 광물에 대한 세계 지속가능성 요건 강화, 세계 토양 건강 관리의 새로운 우선순위, 동물의 건강과 생산성에 대한 관심, 계란 및 유제품 생산의 품질 기준 강화로 인해 큰 폭의 성장세를 보이고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러, 킬로톤 |

| 부문 | 종류, 용도, 형상, 기능(정성적), 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

또한, 광범위한 농학 연구에 따르면 칼슘의 적용은 토양의 pH 값, 양분 이용 효율, 구조적 건전성을 개선하고 산성 토양에서 알루미늄 독성을 감소시켜 작물의 성장과 장기적인 밭 생산성을 향상시키는 것으로 확인되었습니다. 칼슘은 또한 미네랄과 유기물의 상호 작용을 매개하여 탄소의 광물화 속도를 감소시킴으로써 토양의 탄소 안정화에 기여하는 것으로 나타났으며, 기후변화에 강한 재생 농업 시스템에서 그 중요성을 시사하고 있습니다.

그러나 미네랄에 의존하는 산업의 미래에 영향을 미치는 심각한 억제요인과 농가의 예산에서 질소 비료 및 복합 비료와의 경쟁은 농업용 칼슘 시장의 도전 과제가 될 것으로 예상됩니다. 또한, 채굴 활동과 관련된 환경 문제와 석회 가공의 높은 탄소 배출량도 기술적 과제로 남아있습니다.

전반적으로 특수작물 생산 확대, 고부가가치 작물 및 환경제어형 농업(CEA)의 보급, 정밀농업과 토양 진단의 향상으로 칼슘의 표적화된 시용이 촉진될 것으로 예측됩니다. 이는 칼슘 보충제 제조업체들이 시장에서 큰 점유율을 차지할 수 있는 상당한 성장 기회를 제공할 것으로 예상됩니다.

"유형별로는 탄산칼슘 부문이 예측 기간 동안 시장 점유율의 대부분을 차지할 것으로 예상됩니다."

탄산칼슘 부문은 풍부하고 저렴한 비용으로 동물 영양과 토양 개량에 사용되는 고순도 원소 칼슘을 제공하기 때문에 농업에서 가장 널리 사용되는 칼슘 공급원으로 시장을 독점할 것으로 추정됩니다. 또한, 가축 사료용 칼슘 보충제는 가금류, 젖소, 돼지, 양식업에서 뼈의 발달, 난각 형성, 대사 기능을 지원합니다. 탄산칼슘은 농업계와 가축 사료 산업에서 다양한 기능성으로 인해 탄산칼슘이 지배적인 시장 점유율을 차지할 것으로 예상됩니다.

"농업용 칼슘은 예측 기간 동안 밭작물 부문이 농업용 칼슘 시장을 주도할 것으로 예상됩니다."

곡물, 유지종자, 콩류의 대규모 재배는 토양의 비옥도와 구조적 건전성에 지속적인 부하를 가하기 때문에 농업용 칼슘의 핵심적인 하위 용도가 되었습니다. 따라서 석고, 탄산칼슘, 산화칼슘과 같은 칼슘계 미네랄은 집약적인 밭작물 시스템에서 채택이 확대되고 있으며, 영양 균형 개선, 생산성 향상, 농업용 칼슘 시장의 지속적인 수요에 기여하고 있습니다.

"남미는 예측 기간 동안 전 세계 농업용 칼슘 시장에서 큰 비중을 차지할 것으로 예상됩니다."

지역별로는 남미가 농업용 칼슘 시장에서 두 번째로 큰 규모를 차지하는 것으로 추정됩니다. 이 지역은 콩, 옥수수, 밀, 면화 등 수많은 작물의 주요 생산지이자 수출지입니다. 식물의 성장과 발달에 필수적인 역할을 하는 칼슘 보충제의 사용은 이 지역에서 점점 더 중요해지고 있습니다. 이 지역의 시장 성장은 상업용 밭작물과 수출 지향적 원예의 급속한 확대, 그리고 브라질과 아르헨티나의 적극적인 토양개량 방법의 채택이 그 요인으로 작용하고 있습니다.

세계의 농업용 칼슘 시장에 대해 조사 분석했으며, 주요 촉진요인 및 억제요인, 제품 개발 및 혁신, 경쟁 상황 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

- 농업용 칼슘 시장 기업에서 매력적인 기회

- 농업용 칼슘 시장 : 유형별, 지역별

- 농업용 칼슘 시장 : 상위 3개 유형별

- 농업용 칼슘 시장 : 용도별

- 농업용 칼슘 시장 : 형상별

- 농업용 칼슘 시장 : 국가별

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 수요와 화이트 스페이스

- 농업용 칼슘 시장의 미충족 수요

- 화이트 스페이스 기회

- 상호 접속된 시장과 부문 횡단적인 기회

- 상호 접속된 시장

- 부문 횡단적인 기회

- Tier 1/2/3 기업의 전략적 활동

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 세계의 식료 수요와 인구 증가 확대

- 성장하는 양계·수산양식 업계

- 밸류체인 분석

- 연구개발

- 조달

- 생산·가공

- 유통

- 마케팅·세일즈

- 최종사용자

- 생태계 분석

- 수요측

- 공급측

- 가격 책정 분석

- 시장 진입 기업 평균판매가격 : 유형별

- 농업용 칼슘 평균판매가격 동향 : 지역별

- 무역 분석

- HS 코드 283650 및 2510의 수입 시나리오

- HS 코드 283650 및 2510의 수출 시나리오

- 주요 회의와 이벤트(2026-2027년)

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 투자와 자금 조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세의 영향 - 농업용 칼슘 시장

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종 이용 산업에 대한 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- 향후 용도

- 작물 자외선 차단제로서의 미립화 탄산칼슘

- 차세대 칼슘 토양 개량제 : 염분을 관리하는 나노 석고

- 농업의 스마트 칼슘 공급에 이용되는 자극 응답성 셀룰로오스 하이드로겔

- 토양 강도 향상과 뿌리권 안정화를 위한 칼슘 이온의 전기화학적 주입

- 작물 품질과 생산성을 향상시키는 칼슘과 미생물 상승효과

- 농업용 칼슘 시장에 대한 AI/생성형 AI의 영향

- 주요 이용 사례와 시장 전망

- 농업용 칼슘 처리의 베스트 프랙티스

- 농업용 칼슘 시장의 AI 도입 사례 연구

- 상호 접속된 인접 생태계와 시장 기업에 대한 영향

- 농업용 칼슘의 생성형 AI 채용에 대한 고객 준비 상황

- 성공 사례와 실세계에 대한 응용

- AI를 활용한 정밀농업 : 밀수확고 성공 사례

- 정밀 영양 관리를 강화하는 AI를 활용한 가금 건강 관리

제7장 지속가능성과 규제 상황

- 지역 규제와 컴플라이언스

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 라벨표시 요건과 주장

- 향후 5-10년 동안 예측되는 규제 변경

- 지속가능성에 대한 대처

- 지속가능한 조달

- 탄소발자국 절감의 대처

- 순환경제 접근법

- 지속가능성의 대처에 대한 규제 정책의 영향

- 인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구매 프로세스에 관여하는 주요 이해관계자와 그 평가 기준

- 구매 프로세스의 주요 이해관계자

- 구입 기준

- 채용 장벽과 내부 과제

- 공급망 전반에 걸친 각 용도 업계의 미충족 수요

- 시장 수익성

- 잠재적 매출

- 비용 역학

- 마진 기회 : 주요 유형별

제9장 농업용 칼슘 시장 : 유형별

- 탄산칼슘

- 황산칼슘

- 질산칼슘

- 염화칼슘

- 산화칼슘·수산화칼슘(석회·소석회)

- 구연산칼슘

- 인산칼슘

- 천연 미네랄

제10장 농업용 칼슘 시장 : 용도별

- 농업

- 동물 사료

제11장 농업용 칼슘 시장 : 형상별

- 분말

- 과립

- 액체

- 펠릿

- 기타 형상

제12장 농업용 칼슘 시장 : 기능별

- 농업

- 동물 사료

제13장 농업용 칼슘 시장 : 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주·뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 기타 지역

- 중동

- 아프리카

제14장 경쟁 구도

- 개요

- 주요 기업 경쟁 전략/강점(2022-2025년)

- 매출 분석(2022-2024년)

- 시장 점유율 분석(2024년)

- 브랜드/제품의 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 기업 평가와 재무 지표

- 경쟁 시나리오

제15장 기업 개요

- 주요 기업

- YARA INTERNATIONAL ASA(YARA)

- OMYA INTERNATIONAL AG

- SIBELCO

- CARMEUSE

- COROMANDEL INTERNATIONAL LTD.

- IMERYS

- SAINT-GOBAIN FORMULA

- MINERALS TECHNOLOGIES INC.

- GRAYMONT

- KEMIN INDUSTRIES, INC.

- CALC GROUP

- EUROCHEM GROUP

- GLC MINERALS, LLC.

- LHOIST

- HUBER ENGINEERED MATERIALS

- 스타트업/중소기업

- MISSISSIPPI LIME COMPANY D/B/A MLC

- AZOMITE MINERAL PRODUCTS, INC.

- JILOCA INDUSTRIAL SA

- SIGMA MINERALS LTD.

- ASTRRA CHEMICALS

- CALCIUM PRODUCTS, INC.

- LONGCLIFFE QUARRIES LTD.

- BHAGVATI MINERALS

- ICL

- CULTIVACE & KWS DISTRIBUTING

제16장 조사 방법

제17장 인접 시장과 관련 시장

- 연구의 한계

- 비료 시장

- 시장 정의

- 시장 개요

- 사료 첨가제 시장

- 시장 정의

- 시장 개요

제18장 부록

KSM 26.02.24The agricultural calcium market is estimated to be USD 23.60 billion in 2025 and is projected to reach USD 29.62 billion by 2030, at a CAGR of 4.6%. The market is experiencing significant growth, driven by the shift toward sustainable & precision agriculture, strengthened by global sustainability mandates for mineral inputs, emerging priorities in global soil health management, focus on animal health and productivity, and quality standards in egg and milk production.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion), Volume (KT) |

| Segments | By Type, Application, Form, Functions (qualitative), and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Rest of the World (RoW) |

Additionally, extensive agronomic studies confirm that calcium application improves soil pH, nutrient availability, and structural integrity while reducing aluminum toxicity in acidic soils, thereby strengthening crop performance and long-term field productivity. Calcium has also been shown to contribute to soil carbon stabilization by mediating mineral-organic interactions and reducing carbon mineralization rates, indicating its relevance in climate-resilient and regenerative agriculture systems.

However, critical constraints affecting the future of mineral-dependent industries and competition with nitrogen & complex fertilizers in farmer budgeting are expected to pose challenges in the agricultural calcium market. Furthermore, environmental concerns related to mining activities and the high carbon footprint of lime processing also remain a technical challenge.

Overall, growth in specialty crop production, expansion of high-value crops & controlled environment agriculture (CEA), and the rise of precision agriculture & soil diagnostics are expected to boost targeted calcium application, presenting substantial growth opportunities for calcium supplement manufacturers to gain a significant share in the market.

"By type, the calcium carbonate segment is expected to hold a dominant market share during the forecast period"

The calcium carbonate segment is estimated to dominate the market as it is the most widely used calcium source in agriculture because it is abundant, low-cost, and provides high elemental calcium across both animal nutrition and soil conditioning applications. Additionally, in the animal feed application, calcium supplement supports bone development, eggshell formation, and metabolic function in poultry, dairy, swine, and aquaculture. Due to its various functionalities in the agriculture and animal feed industry, calcium carbonate is considered to have a dominant market share.

"In agriculture application, the field crops segment is expected to lead the agricultural calcium market during the forecast period"

The types of field crops considered in the study include cereals & grains, oilseeds & pulses, and other field crops. It represents a core sub-application for agricultural calcium, as large-scale cultivation of cereals, oilseeds, and pulses places sustained pressure on soil fertility and structural integrity. Thus, calcium-based minerals such as gypsum, calcium carbonate, calcium oxide, and others are increasingly adopted in intensive field crop systems, contributing to improved nutrient balance, higher productivity, and sustained demand within the agricultural calcium market.

"South America is expected to hold a significant share in the global agricultural calcium market during the forecast period"

By region, South America is estimated to be the second-largest market for agricultural calcium. It is a major agricultural producer and exporter of several crops, such as soybeans, corn, wheat, and cotton. The use of calcium supplements has gained importance in the region due to their essential role in plant growth and development. The market growth in this region is also attributed to the rapid expansion of commercial row crops and export-oriented horticulture, combined with strong adoption of soil correction practices in Brazil and Argentina.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the agricultural calcium market.

- By Company Type: Tier 1 - 30%, Tier 2 - 25%, and Tier 3 - 45%

- By Designation: CXOs - 25%, Managers - 35%, Others - 40%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 35%, South America - 10%, and Rest of the World -5%

Prominent companies in the market include Yara International (Norway), Omya International AG (Switzerland), Sibelco (US), Carmeuse (Belgium), Coromandel International Ltd. (India), Imerys (France), Saint-Gobain Formula (UK), Minerals Technologies Inc. (US), Graymont (Canada), Kemin Industries, Inc. (US), CALC Group (Poland), EuroChem Group (Switzerland), GLC Minerals, LLC. (US), Huber Engineered Materials (US), Mississippi Lime Company d/b/a MLC (US), AZOMITE Mineral Products, Inc. (US), Jiloca Industrial SA (Spain), Sigma Minerals Ltd. (India), Astrra Chemicals (India), Lhoist (Belgium), and others.

Research Coverage

This research report categorizes the agricultural calcium market by type (calcium carbonate [limestone], calcium sulfate [gypsum], calcium nitrate, calcium chloride, calcium oxide and hydroxide [lime & hydrated lime], calcium citrate, calcium phosphate, and natural mineral), application (agriculture and animal feed), form (powder, granules/grits, liquid, pellets, and other forms), function (qualitative) (agriculture [nutrient supplementation, soil structure improvement, disease prevention and plant health, fertilizer enhancement, and soil pH adjustment and liming] and animal feed [bone and muscle development, eggshell formation, milk production enhancement, and other functions]), and region (North America, Europe, Asia Pacific, South America, and Rest of the World).

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the agricultural calcium industry. A thorough analysis of the key industry players has been done to provide insights into their business, services, key strategies, contracts, partnerships, agreements, product launches, mergers & acquisitions, and recent developments associated with the agricultural calcium market. This report provides a competitive analysis of emerging startups in the agricultural calcium market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem & market mapping, and patent & regulatory landscape, among others.

Reasons to Buy This Report

The report provides market leaders/new entrants with information on the closest approximations of revenue numbers for the overall agricultural calcium and its subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (shift toward sustainable & precision agriculture strengthened by global sustainability mandates for mineral inputs), restraints (environmental concerns related to mining activities), opportunities (growth in specialty crop production & expansion of high-value crops & controlled environment agriculture (CEA)), and challenges (critical constraints affecting the future of mineral-dependent industries) influencing the growth of the agricultural calcium market

- Product Development/Innovation: Detailed insights into research & development activities and new product launches in the agricultural calcium market

- Market Development: Comprehensive information about lucrative markets-analysis of agricultural calcium across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the agricultural calcium market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as Yara International (Norway), Omya International AG (Switzerland), Sibelco (US), Carmeuse (Belgium), Coromandel International Ltd. (India), Imerys (France), Saint-Gobain Formula (UK), Minerals Technologies Inc. (US), Graymont (Canada), Kemin Industries, Inc. (US), CALC Group (Poland), EuroChem Group (Switzerland), GLC Minerals, LLC. (US), Huber Engineered Materials (US), Mississippi Lime Company d/b/a MLC (US), AZOMITE Mineral Products, Inc. (US), Jiloca Industrial SA (Spain), Sigma Minerals Ltd. (India), Astrra Chemicals (India), Lhoist (Belgium), and other players in the agricultural calcium market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AGRICULTURAL CALCIUM MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AGRICULTURAL CALCIUM MARKET

- 3.2 AGRICULTURAL CALCIUM MARKET, BY TYPE AND REGION

- 3.3 AGRICULTURAL CALCIUM MARKET, BY TOP 3 TYPES

- 3.4 AGRICULTURAL CALCIUM MARKET, BY APPLICATION

- 3.5 AGRICULTURAL CALCIUM MARKET, BY FORM

- 3.6 AGRICULTURAL CALCIUM MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Focus on animal health and productivity

- 4.2.1.2 Quality standards in egg and milk production

- 4.2.1.3 Shift toward sustainable and precision agriculture strengthened by global sustainability mandates for mineral inputs

- 4.2.1.3.1 Shift toward sustainable and precision agriculture

- 4.2.1.3.2 Sustainability mandates favoring mineral inputs

- 4.2.1.4 Emerging priorities in global soil health management

- 4.2.2 RESTRAINTS

- 4.2.2.1 Competition from alternative soil amendments

- 4.2.2.2 Environmental concerns related to mining activities

- 4.2.2.3 High carbon footprint of lime processing

- 4.2.2.4 Difficulty integrating calcium into liquid fertilizer systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Calcium as key input in climate-smart and regenerative farming systems

- 4.2.3.2 Rise of precision agriculture and soil diagnostics

- 4.2.3.3 Growth in specialty crop production and controlled environment agriculture (CEA)

- 4.2.3.4 Demand for functional feed additives and organic & non-GMO certified feed ingredients

- 4.2.3.5 Development of value-added co-products

- 4.2.4 CHALLENGES

- 4.2.4.1 Critical constraints affecting future of mineral-dependent industries

- 4.2.4.1.1 Environmental concerns related to mining activities

- 4.2.4.1.2 Dependence on mining regions creating supply imbalances

- 4.2.4.2 Competition with nitrogen and complex fertilizers in farmer budgeting

- 4.2.4.1 Critical constraints affecting future of mineral-dependent industries

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN AGRICULTURAL CALCIUM MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GROWING GLOBAL FOOD DEMAND AND POPULATION GROWTH

- 5.2.3 GROWING POULTRY AND AQUACULTURE INDUSTRIES

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 SOURCING

- 5.3.3 PRODUCTION & PROCESSING

- 5.3.4 DISTRIBUTION

- 5.3.5 MARKETING & SALES

- 5.3.6 END USERS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF MARKET PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND OF AGRICULTURAL CALCIUM, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO OF HS CODE 283650 & 2510

- 5.6.2 EXPORT SCENARIO OF HS CODE 283650 & 2510

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CALCIUM PRODUCTS, INC.: TRANSITION FROM CONVENTIONAL AGLIME TO PELLETIZED LIMESTONE FOR PREDICTABLE SOIL PH MANAGEMENT

- 5.10.2 YARA: SOLUBLE CALCIUM FERTIGATION TO IMPROVE CROP QUALITY IN HIGH-VALUE CROPS

- 5.10.3 OMYA AVICARB - IMPROVING EGGSHELL QUALITY THROUGH CONTROLLED CALCIUM RELEASE IN LAYING HENS

- 5.11 IMPACT OF 2025 US TARIFF - AGRICULTURAL CALCIUM MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Purification technologies

- 6.1.1.2 Pelletization systems

- 6.1.1.3 Nano-calcium technologies

- 6.1.1.4 Solubilization technology

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Precision agriculture

- 6.1.2.2 Farm management information systems

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 IoT and sensor technologies

- 6.1.3.2 Soil testing and mapping technologies

- 6.1.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.1.4.1 Short-term | Foundation & early commercialization

- 6.1.4.2 Mid-term | Expansion & standardization

- 6.1.4.3 Long-term | Precision nutrition & smart calcium solutions

- 6.1.1 KEY TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.2.1 LIST OF MAJOR PATENTS PERTAINING TO AGRICULTURAL CALCIUM MARKET, 2020-2025

- 6.3 FUTURE APPLICATIONS

- 6.3.1 MICRONIZED CALCIUM CARBONATE AS A CROP SUNSCREEN

- 6.3.2 NEXT-GENERATION CALCIUM AMENDMENTS: NANO-GYPSUM FOR SALINITY MANAGEMENT

- 6.3.3 STIMULUS-RESPONSIVE CELLULOSE HYDROGELS FOR SMART CALCIUM DELIVERY IN AGRICULTURE

- 6.3.4 ELECTROCHEMICAL INJECTION OF CALCIUM IONS FOR SOIL STRENGTH ENHANCEMENT AND ROOT-ZONE STABILITY

- 6.3.5 CALCIUM-MICROBIAL SYNERGIES FOR ENHANCED CROP QUALITY AND PRODUCTIVITY

- 6.4 IMPACT OF AI/GEN AI ON AGRICULTURAL CALCIUM MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST PRACTICES IN AGRICULTURAL CALCIUM PROCESSING

- 6.4.3 CASE STUDIES OF AI IMPLEMENTATION IN AGRICULTURAL CALCIUM MARKET

- 6.4.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN AGRICULTURAL CALCIUM

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.5.1 AI-ENABLED PRECISION AGRICULTURE: A WHEAT YIELD SUCCESS STORY

- 6.5.2 AI-DRIVEN POULTRY HEALTH MANAGEMENT ENHANCING PRECISION NUTRITION

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 LABELING REQUIREMENTS AND CLAIMS

- 7.1.4 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.4.1 Mandatory Validation of CFU Viability & Functional Claims

- 7.1.4.2 Global Harmonization of Calcium Fertilizer & Soil Amendment Classifications

- 7.1.4.3 Strengthened Safety, Environmental & Contaminant Control Regulations

- 7.1.4.4 Digital Labeling, Traceability & QR-based Compliance Tracking

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABLE SOURCING

- 7.2.2 CARBON FOOTPRINT REDUCTION INITIATIVES

- 7.2.3 CIRCULAR ECONOMY APPROACHES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS APPLICATION INDUSTRIES ACROSS SUPPLY CHAIN

- 8.5 MARKET PROFITABILITY

- 8.6 REVENUE POTENTIAL

- 8.6.1 COST DYNAMICS

- 8.6.2 MARGIN OPPORTUNITIES, BY KEY TYPES

9 AGRICULTURAL CALCIUM MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.1.1 CALCIUM CARBONATE

- 9.1.1.1 Correcting soil acidity and enhancing crop productivity

- 9.1.2 CALCIUM SULFATE

- 9.1.2.1 Driving soil conditioning and nutrient availability

- 9.1.3 CALCIUM NITRATE

- 9.1.3.1 Supporting rapid plant growth and animal nutrition efficiency

- 9.1.4 CALCIUM CHLORIDE

- 9.1.4.1 Driving calcium availability across crop nutrition and livestock feed systems

- 9.1.5 CALCIUM OXIDE AND CALCIUM HYDROXIDE (LIME & HYDRATED LIME)

- 9.1.5.1 Improving soil conditioning and animal health management through lime-based calcium

- 9.1.6 CALCIUM CITRATE

- 9.1.6.1 Improving plant growth response and animal mineral absorption

- 9.1.7 CALCIUM PHOSPHATE

- 9.1.7.1 Supporting root development and skeletal health with calcium phosphate

- 9.1.7.2 Dicalcium phosphate

- 9.1.7.3 Monocalcium phosphate

- 9.1.7.4 Mono-dicalcium phosphate

- 9.1.7.5 Tricalcium phosphate

- 9.1.8 NATURAL MINERAL

- 9.1.8.1 Restoring soil health and improving feed trace mineral availability using rock-derived calcium

- 9.1.8.2 AZOMITE

- 9.1.8.3 Kelzyme

- 9.1.8.4 Calcium with trace minerals

- 9.1.1 CALCIUM CARBONATE

10 AGRICULTURAL CALCIUM MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.1.1 AGRICULTURE

- 10.1.1.1 Agricultural calcium supports soil health and crop productivity across diverse farming systems

- 10.1.1.2 Field crops

- 10.1.1.2.1 Cereals & grains

- 10.1.1.2.2 Oilseeds & pulses

- 10.1.1.2.3 Other field crops

- 10.1.1.3 Horticulture crops

- 10.1.1.3.1 Fruits

- 10.1.1.3.2 Vegetables

- 10.1.1.3.3 Plantation crops

- 10.1.1.4 Controlled Environment Agriculture (CEA)

- 10.1.1.4.1 Greenhouse farming

- 10.1.1.4.2 Hydroponics

- 10.1.1.5 Land, forest, & mining regeneration

- 10.1.2 ANIMAL FEED

- 10.1.2.1 Essential mineral nutrition powering animal health, productivity, and performance

- 10.1.2.2 Poultry

- 10.1.2.2.1 Broilers

- 10.1.2.2.2 Layers

- 10.1.2.2.3 Breeders

- 10.1.2.3 Ruminants

- 10.1.2.3.1 Dairy

- 10.1.2.3.2 Beef

- 10.1.2.3.3 Calf

- 10.1.2.3.4 Other ruminants

- 10.1.2.4 Swine

- 10.1.2.5 Aquatic animals

- 10.1.2.6 Pets

- 10.1.1 AGRICULTURE

11 AGRICULTURAL CALCIUM MARKET, BY FORM

- 11.1 INTRODUCTION

- 11.2 POWDER

- 11.2.1 FEEDING HERDS, HEALING SOILS, AND FUELING FARM PRODUCTIVITY

- 11.3 GRANULES/GRITS

- 11.3.1 OFFERING PRACTICAL CALCIUM NUTRITION WITH PRECISION APPLICATION AND REDUCED LOSSES

- 11.4 LIQUID

- 11.4.1 SUPPORTING RAPID DEFICIENCY CORRECTION AND CONTROLLED NUTRIENT MANAGEMENT IN BOTH ANIMALS AND CROPS

- 11.5 PELLETS

- 11.5.1 ENSURING CLEAN HANDLING, PRECISE APPLICATION, AND SUSTAINED NUTRIENT AVAILABILITY FOR LONG-TERM PRODUCTIVITY

- 11.6 OTHER FORMS

12 AGRICULTURAL CALCIUM MARKET, BY FUNCTION

- 12.1 AGRICULTURE

- 12.1.1 NUTRIENT SUPPLEMENTATION

- 12.1.2 SOIL STRUCTURE IMPROVEMENT

- 12.1.3 DISEASE PREVENTION AND PLANT HEALTH

- 12.1.4 FERTILIZER ENHANCEMENT

- 12.1.5 SOIL PH ADJUSTMENT AND LIMING

- 12.2 ANIMAL FEED

- 12.2.1 BONE AND MUSCLE DEVELOPMENT

- 12.2.2 EGGSHELL FORMATION

- 12.2.3 MILK PRODUCTION ENHANCEMENT

- 12.2.4 OTHER FUNCTIONS

13 AGRICULTURAL CALCIUM MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 High-input farming and fertilizer-intensive agriculture to drive market

- 13.2.2 CANADA

- 13.2.2.1 Large-scale, export-driven farming and rising production intensity to drive market

- 13.2.3 MEXICO

- 13.2.3.1 Increasing agricultural production and diverse agro-climatic conditions to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Rising grain yields and increasingly intensive cereal cultivation to drive market

- 13.3.2 UK

- 13.3.2.1 Policy-driven soil sustainability targets and nutrient balancing needs to drive market

- 13.3.3 FRANCE

- 13.3.3.1 High-volume crop production and sustainability-led dairy farming to drive market

- 13.3.4 ITALY

- 13.3.4.1 Need for effective soil fertility management across both arable and perennial cropping systems to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Extensive cultivation of cereal and perennial crops and intensive livestock systems to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Public investment in food security and resource efficiency to support market growth

- 13.4.2 JAPAN

- 13.4.2.1 Continuous rice, wheat, and soybean cultivation under limited land availability to drive consistent adoption of calcium-based soil amendments

- 13.4.3 INDIA

- 13.4.3.1 Food security pressures and climate variability to strengthen demand for calcium in crop nutrition systems

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Soil restoration and nutrient efficiency goals to drive market

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Increasing production and export of agricultural products to drive market

- 13.5.2 ARGENTINA

- 13.5.2.1 Large-scale food exports and intensive cropping systems to drive market

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD

- 13.6.1 MIDDLE EAST

- 13.6.1.1 Agri-tech-led food security strategies to strengthen calcium use in high-efficiency farming systems

- 13.6.2 AFRICA

- 13.6.2.1 Yield improvement and soil restoration efforts to drive demand for agricultural calcium

- 13.6.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2025

- 14.3 REVENUE ANALYSIS, 2022-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Regional footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 Application footprint

- 14.6.5.5 Form footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.8.1 COMPANY VALUATION

- 14.8.2 FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 YARA INTERNATIONAL ASA (YARA)

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 OMYA INTERNATIONAL AG

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 SIBELCO

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 CARMEUSE

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 COROMANDEL INTERNATIONAL LTD.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 IMERYS

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.4 MnM view

- 15.1.7 SAINT-GOBAIN FORMULA

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.4 MnM view

- 15.1.8 MINERALS TECHNOLOGIES INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.4 MnM view

- 15.1.9 GRAYMONT

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.4 MnM view

- 15.1.10 KEMIN INDUSTRIES, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.4 MnM view

- 15.1.11 CALC GROUP

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.4 MnM view

- 15.1.12 EUROCHEM GROUP

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.4 MnM view

- 15.1.13 GLC MINERALS, LLC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.4 MnM view

- 15.1.14 LHOIST

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.4 MnM view

- 15.1.15 HUBER ENGINEERED MATERIALS

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.15.4 MnM view

- 15.1.1 YARA INTERNATIONAL ASA (YARA)

- 15.2 STARTUPS/SMES

- 15.2.1 MISSISSIPPI LIME COMPANY D/B/A MLC

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.4 MnM view

- 15.2.2 AZOMITE MINERAL PRODUCTS, INC.

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.4 MnM view

- 15.2.3 JILOCA INDUSTRIAL SA

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.4 MnM view

- 15.2.4 SIGMA MINERALS LTD.

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.4 MnM view

- 15.2.5 ASTRRA CHEMICALS

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.4 MnM view

- 15.2.6 CALCIUM PRODUCTS, INC.

- 15.2.7 LONGCLIFFE QUARRIES LTD.

- 15.2.8 BHAGVATI MINERALS

- 15.2.9 ICL

- 15.2.10 CULTIVACE & KWS DISTRIBUTING

- 15.2.1 MISSISSIPPI LIME COMPANY D/B/A MLC

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Breakdown of primary profiles

- 16.1.2.3 Key insights from industry experts

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.2.2 SUPPLY-SIDE ANALYSIS

- 16.2.3 BOTTOM-UP APPROACH (DEMAND SIDE)

- 16.3 DATA TRIANGULATION AND MARKET BREAKUP

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 ADJACENT & RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 STUDY LIMITATIONS

- 17.3 FERTILIZERS MARKET

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.4 FEED ADDITIVES MARKET

- 17.4.1 MARKET DEFINITION

- 17.4.2 MARKET OVERVIEW

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS