|

시장보고서

상품코드

1956048

위성 시장 : 위성 질량별, 서브시스템별, 용도별, 고객 유형별, 주파수별, 추진 기술별, 지역별 - 세계 예측(-2031년)Satellites Market by Mass (1-1200 kg, 1201-2000 kg, >2000 kg), Application (Communication, Earth Observation, Navigation), Subsystem (Satellite Bus, Solar Panels, Payloads, Satellite Antenna), Frequency, Propulsion, and Region -Global Forecast to 2031 |

||||||

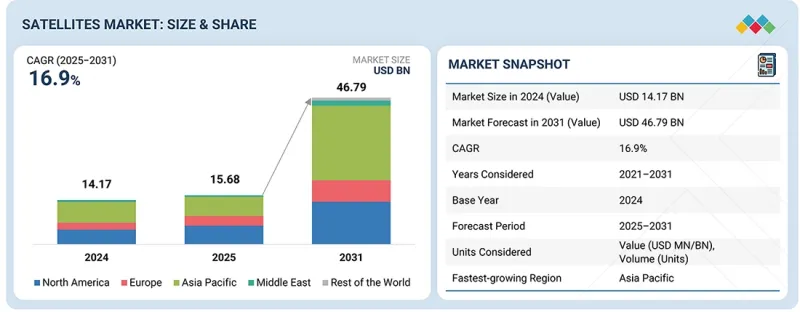

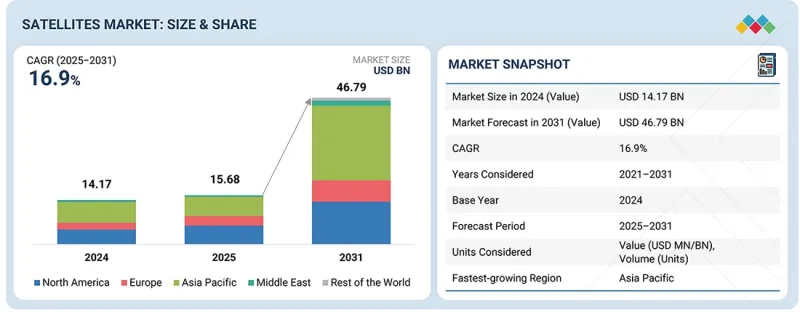

위성 시장 규모는 2025년 156억 8,000만 달러에서 2031년까지 467억 9,000만 달러에 달할 것으로 예측되며, CAGR은 16.9%로 전망됩니다.

수량 기준으로 시장 규모는 2025년 2,942대에서 2031년 5,110대로 증가할 것으로 예상됩니다. 위성 시장은 사업자들의 신규 발사, 위성 컨스텔레이션 확장, 노후 위성 교체를 통한 용량 증설이 지속되면서 확대되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 위성 질량별, 서브시스템별, 용도별, 고객 유형별, 주파수별, 추진 기술별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

통신, 지구 관측, 항법 분야의 수요가 증가하고 있으며, 이는 위성의 공급량 증가를 뒷받침하고 있습니다. 한편, 더 많은 민간 기업과 지역 우주 프로그램이 시장에 진입하여 전체 성장에 기여하고 있습니다.

Ku 밴드는 방송, 광대역 인터넷, 항공 및 해상 연결과 같은 모바일 애플리케이션에서 위성통신에 광범위하게 사용됨에 따라 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다. Ku밴드는 커버리지, 사용 가능한 대역폭, 성숙한 지상 인프라의 균형이 뛰어나며, 대규모 구축에 있어 비용 효율성이 높습니다. 기존 단말기 및 서비스 제공자 기반이 지속적인 보급과 꾸준한 성장을 뒷받침하고 있습니다.

전기 추진 부문은 예측 기간 동안 지배적인 위치를 차지할 것으로 예상됩니다. 이는 위성의 궤도 유지, 궤도 상승 및 별자리 임무에 보다 가볍고 효율적인 전기 추진이 점점 더 많이 채택되고 있기 때문입니다. 전기 추진 시스템을 통해 사업자는 발사 시마다 더 많은 페이로드를 탑재할 수 있어 전체 발사 비용을 절감할 수 있습니다. 또한, 위성의 수명 연장을 돕고 필요한 추진제가 적기 때문에 많은 상업 사업자들이 전기 추진으로 전환을 추진하고 있습니다.

북미는 강력한 상업용 위성 사업자와 국방 및 민간 우주 프로그램에 대한 지속적인 지출에 힘입어 2031년까지 위성 시장 점유율 2위를 유지할 것으로 예상됩니다. 이 지역은 광대역, 모빌리티, 데이터 서비스를 위한 통신위성 및 지구 관측위성 배치에 있어 선도적인 위치에 있습니다. 고처리량 플랫폼과 내결함성 우주 시스템과 같은 차세대 위성 시스템에 대한 지속적인 투자가 수요를 안정화시키고 있습니다. 성숙한 발사 생태계와 주요 위성 제조업체의 존재도 북미의 지위 유지에 기여하고 있습니다.

조사 범위:

이 시장 조사는 다양한 부문 및 하위 부문에 걸친 위성 시장을 대상으로 합니다. 각 지역별로 본 시장의 규모와 성장 가능성을 추정하는 것을 목표로 하고 있습니다. 또한 주요 기업의 상세한 경쟁 분석, 기업 개요, 제품 및 비즈니스 오퍼링에 대한 주요 관찰 사항, 최근 동향 및 주요 전략에 대한 주요 관찰 사항도 제공합니다.

본 보고서 구매의 장점:

이 보고서는 위성 시장 전체에 대한 대략적인 수익 규모를 제공함으로써 시장 리더와 신규 진입자를 지원할 수 있습니다. 또한, 이해관계자들이 경쟁 상황을 이해하고, 비즈니스를 더 잘 포지셔닝하고, 효과적인 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한, 주요 촉진요인, 제약, 과제, 기회 등 시장 동향에 대한 인사이트를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 시장 촉진요인(저궤도 위성 컨스텔레이션의 빠른 전개, 지구 관측 데이터 수요 증가, 발사 및 위성 제조 비용 감소), 제약요인(주파수 대역 할당 및 규제 당국의 승인, 우주 부품 공급 제한), 기회(서비스형 데이터(DaaS) 비즈니스 모델, 소프트웨어 정의형 및 재구축형 위성, 궤도 서비스 및 수명주기 솔루션), 도전 과제(궤도 혼잡 및 충돌 위험, 장기적인 경제성) 재구성이 가능한 위성, 궤도상 서비스 및 수명 종료 솔루션), 도전과제(궤도 혼잡 및 충돌 위험, 콘스텔레이션의 장기적 경제성)에 대한 자료입니다.

- 시장 침투 : 주요 기업이 제공하는 위성에 대한 종합 정보

- 제품 개발/혁신 : 위성 시장의 향후 기술 동향, 연구개발 활동, 제품 출시에 대한 상세 분석

- 시장 개발 : 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화 : 위성 시장의 신제품, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보를 제공합니다.

- 경쟁 평가 : 위성 시장 내 주요 기업의 시장 점유율, 성장 전략, 제품, 제조 능력에 대한 상세 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 고객 상황과 구매 행동

제8장 지속가능성과 규제 상황

제9장 위성 시장, 위성 질량별

제10장 위성 시장(서브시스템별)

제11장 위성 시장(용도별)

제12장 위성 시장(고객 유형별)

제13장 위성 시장(주파수별)

제14장 위성 시장(추진 기술별)

제15장 위성 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.03.19The satellites market is projected to reach USD 46.79 billion by 2031, from USD 15.68 billion in 2025, with a CAGR of 16.9%. In terms of volume, the market is expected to rise from 2,942 units in 2025 to 5,110 units by 2031. The satellites market is expanding as operators continue adding capacity through new launches, constellation expansion, and replacing older satellites.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Mass, Application, Subsystem and Region |

| Regions covered | North America, Europe, APAC, RoW |

Demand is increasing in communication, Earth observation, and navigation, which supports higher satellite volumes. Meanwhile, more commercial players and regional space programs are entering the market, contributing to overall growth.

"The Ku-band is expected to be the fastest-growing frequency segment during the forecast period."

The Ku-band is expected to record the highest CAGR during the forecast period because of its widespread use in satellite communication for broadcasting, broadband internet, and mobility applications such as aviation and maritime connectivity. Ku-band provides a good balance of coverage, available bandwidth, and mature ground infrastructure, making it cost-effective for large-scale deployments. The existing base of terminals and service providers supports continued strong adoption and steady growth.

"Electric is expected to be the largest propulsion technology segment during the forecast period."

The electric segment is expected to be dominant during the forecast period, as more satellites use electric propulsion for station keeping, orbit raising, and constellation missions because it is lighter and more efficient. Electric systems enable operators to carry more payloads per launch and reduce overall launch costs. They also support longer satellite lifespans and require less propellant, which is why many commercial operators are shifting toward electric propulsion.

"North America is expected to hold the second-largest position during the forecast period."

North America is expected to hold the second-largest share of the satellites market through 2031, driven by strong commercial satellite operators and consistent spending on defense and civil space programs. The region leads by deploying communication and Earth observation satellites for broadband, mobility, and data services. Continued investment in next-generation satellite systems like high-throughput platforms and resilient space setups keeps demand steady. A mature launch ecosystem and major satellite manufacturers also help sustain North America's position.

The breakdown of profiles for primary participants in the satellites market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: Directors - 20%, Managers - 10%, and Others - 70%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 20%, Middle East - 10%, and Rest of the World - 10%

Research Coverage:

This market study covers the satellites market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different regions. The study also provides an in-depth competitive analysis of the key players, their company profiles, important observations about their products and business offerings, recent developments, and the key strategies they have adopted.

Reasons to buy this report:

The report will assist market leaders and new entrants by providing approximations of the revenue figures for the overall satellites market. It will also help stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report will provide insights into the market pulse, including key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Rapid deployment of LEO constellations, Rising demand for Earth observation data, Declining launch and satellite production costs), Restraints (Spectrum allocation and regulatory approvals, Limited availability of space-qualified components), Opportunities (Data-as-a-service business models, Software-defined and reconfigurable satellites, On-orbit servicing and end-of-life solutions), Challenges (Orbital congestion and collision risk, Long-term constellation economics).

- Market Penetration: Comprehensive information on satellites offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product launches in the satellites market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the satellites market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the satellites market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SATELLITES MARKET

- 3.2 SATELLITES MARKET, BY SATELLITE MASS

- 3.3 SATELLITES MARKET, BY APPLICATION

- 3.4 SATELLITES MARKET, BY PROPULSION TECHNOLOGY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid deployment of low Earth orbit (LEO) constellations

- 4.2.1.2 Rising demand for Earth observation (EO) data

- 4.2.1.3 Declining launch and satellite production costs

- 4.2.2 RESTRAINTS

- 4.2.2.1 Spectrum allocation and regulatory approvals

- 4.2.2.2 Limited availability of space-qualified components

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Data-as-a-service business models

- 4.2.3.2 Software-defined and reconfigurable satellites

- 4.2.3.3 On-orbit servicing and end-of-life solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Orbital congestion and collision risk

- 4.2.4.2 Long-term constellation economics

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 INTEGRATED SPACE TRAFFIC MANAGEMENT AND COLLISION AVOIDANCE

- 4.3.2 AFFORDABLE LIFECYCLE MANAGEMENT FOR MID-VALUE SATELLITES

- 4.3.3 GROUND SEGMENT INTEGRATION AND DATA USABILITY GAPS

- 4.3.4 REGULATORY AND SUSTAINABILITY COMPLIANCE SUPPORT

- 4.4 INTERCONNECTED MARKET AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTEGRATION WITH TERRESTRIAL DIGITAL INFRASTRUCTURE

- 4.4.2 GOVERNMENT AND PUBLIC SECTOR DIGITALIZATION

- 4.4.3 ENERGY AND NATURAL RESOURCE MONITORING

- 4.4.4 FINANCIAL SERVICES AND INSURANCE APPLICATIONS

- 4.4.5 MOBILITY AND TRANSPORTATION ECOSYSTEMS

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6 SATELLITES MARKET: VOLUME DATA

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL SPACE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRIME CONTRACTORS & INTEGRATED SATELLITE PROVIDERS

- 5.4.2 SATELLITE PLATFORM & SUBSYSTEM MANUFACTURERS

- 5.4.3 END USERS

- 5.5 TOTAL COST OF OWNERSHIP

- 5.6 BILL OF MATERIALS

- 5.7 TRADE DATA

- 5.7.1 IMPORT SCENARIO (HS CODE 880260)

- 5.7.2 EXPORT SCENARIO (HS CODE 880260)

- 5.8 KEY CONFERENCES & EVENTS, 2026

- 5.9 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 PRICING ANALYSIS

- 5.11.1 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024 (USD MILLION)

- 5.11.2 INDICATIVE PRICING ANALYSIS, BY SATELLITE MASS, 2024 (USD MILLION)

- 5.12 CASE STUDIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED PROPULSION SYSTEMS

- 6.1.2 AUTONOMOUS OPERATIONS AND ONBOARD DECISION-MAKING

- 6.1.3 SPACE SITUATIONAL AWARENESS (SSA) AND THREAT MONITORING PAYLOADS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 COMMAND-AND-CONTROL SYSTEMS

- 6.2.2 GROUND SEGMENT VIRTUALIZATION AND CLOUD-BASED OPERATIONS

- 6.2.3 TECHNOLOGY ROADMAP

- 6.3 EMERGING TECHNOLOGY TRENDS

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/ GENERATIVE AI ON SATELLITES MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN THE SATELLITES MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN SATELLITES MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN SATELLITES MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 SPACEX - TRANSFORMING GLOBAL CONNECTIVITY THROUGH LARGE-SCALE LEO CONSTELLATIONS

- 6.7.2 AIRBUS DEFENCE AND SPACE - ENABLING MISSION-CRITICAL SATELLITE SYSTEMS ACROSS CIVIL AND DEFENSE DOMAINS

- 6.7.3 MAXAR TECHNOLOGIES - CONVERTING SATELLITE DATA INTO ACTIONABLE GEOSPATIAL INTELLIGENCE

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 TARIFF DATA

- 8.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.2 REGULATORY FRAMEWORK

- 8.2.1 NORTH AMERICA

- 8.2.2 EUROPE

- 8.2.3 ASIA PACIFIC

- 8.2.4 MIDDLE EAST

- 8.2.5 LATIN AMERICA AND AFRICA

- 8.2.6 INDUSTRY STANDARDS

- 8.3 SUSTAINABILITY INITIATIVES

- 8.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.5 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

9 SATELLITES MARKET, BY SATELLITE MASS

- 9.1 INTRODUCTION

- 9.2 ORBIT-LEVEL DEPLOYMENT OF SATELLITES BASED ON MASS CATEGORY

- 9.2.1 LOW EARTH ORBIT (LEO) (160-2,000 KM): TOP USE CASES

- 9.2.2 MEDIUM EARTH ORBIT (MEO) (2,000-35,786 KM): TOP USE CASES

- 9.2.3 GEOSTATIONARY ORBIT (GEO) (35,786 KM): TOP USE CASES

- 9.3 SMALL SATELLITES (1-1200 KG)

- 9.3.1 ADVANCEMENTS IN MINIATURIZATION OF ELECTRONICS TO DRIVE MARKET

- 9.3.2 NANOSATELLITE (1-10 KG)

- 9.3.3 MICROSATELLITE (11-100 KG)

- 9.3.4 MINISATELLITE (101-1200 KG)

- 9.4 MEDIUM SATELLITES (1201-2000 KG)

- 9.4.1 NEED FOR TECHNOLOGICAL ADVANCEMENTS TO DRIVE MARKET

- 9.5 LARGE SATELLITES (ABOVE 2000 KG)

- 9.5.1 DEMAND FOR HIGH-CAPACITY TELECOMMUNICATION AND BROADBAND SERVICES TO DRIVE MARKET

10 SATELLITES MARKET, BY SUBSYSTEM

- 10.1 INTRODUCTION

- 10.2 SATELLITE BUS CONFIGURATION OF LOW-COMPLEXITY AND HIGH-CAPABILITY PLATFORMS

- 10.2.1 LOW-COMPLEXITY BUS CONFIGURATIONS (NON-PROPULSION, BASIC ADCS, FIXED ANTENNAS): TOP USE CASES

- 10.2.2 HIGH-CAPABILITY BUS CONFIGURATIONS (PROPULSION-EQUIPPED, HIGH-POWER, PRECISE ADCS): TOP USE CASES

- 10.3 SATELLITE BUS

- 10.3.1 FOCUS ON ENHANCING SATELLITE PERFORMANCE TO DRIVE MARKET

- 10.3.2 ATTITUDE AND ORBITAL CONTROL SYSTEMS

- 10.3.2.1 Sensors

- 10.3.2.1.1 Sun sensors

- 10.3.2.1.2 Magnetometers

- 10.3.2.2 Reaction wheels

- 10.3.2.3 Actuators

- 10.3.2.4 Control electronics

- 10.3.2.1 Sensors

- 10.3.3 COMMAND AND DATA HANDLING SYSTEMS

- 10.3.3.1 Onboard computer

- 10.3.3.2 Processor

- 10.3.3.3 Microcontroller

- 10.3.3.4 Memory

- 10.3.3.5 Solid state recorder

- 10.3.3.6 Router

- 10.3.3.7 On-board charger (OBC) adaptor

- 10.3.4 ELECTRICAL POWER SYSTEMS

- 10.3.4.1 Power management device

- 10.3.4.2 Power converter

- 10.3.4.3 Battery

- 10.3.4.3.1 Primary battery

- 10.3.4.3.2 Secondary battery

- 10.3.5 PROPULSION SYSTEMS

- 10.3.5.1 Thrusters

- 10.3.5.2 Propellant tank

- 10.3.5.3 Propellant feed plumbing

- 10.3.6 TELEMETRY, TRACKING, AND COMMAND SYSTEMS

- 10.3.6.1 Transmitter

- 10.3.6.2 Receiver

- 10.3.6.3 Modem/Baseband unit

- 10.3.7 STRUCTURES

- 10.3.8 THERMAL SYSTEMS

- 10.3.8.1 Temperature sensors

- 10.3.8.2 Heaters

- 10.3.8.3 Thermostats

- 10.3.8.4 Insulation

- 10.4 PAYLOADS

- 10.4.1 PAYLOADS DRIVE SATELLITES' DESIGN AND SUBSYSTEMS

- 10.4.2 TRADITIONAL PAYLOADS

- 10.4.3 SOFTWARE-DEFINED PAYLOADS

- 10.5 SOLAR PANELS

- 10.5.1 NEED FOR ENHANCED EFFICIENCY WITH PHOTOVOLTAIC CELL MATERIALS TO DRIVE MARKET

- 10.6 SATELLITE ANTENNAS

- 10.6.1 ABILITY OF SATELLITE ANTENNAS TO OPERATE IN DIFFERENT FREQUENCIES TO DRIVE DEMAND

- 10.6.2 WIRE ANTENNAS

- 10.6.2.1 Monopole antenna

- 10.6.2.2 Dipole antenna

- 10.6.3 HORN ANTENNAS

- 10.6.4 ARRAY ANTENNAS

- 10.6.5 REFLECTOR ANTENNAS

- 10.6.5.1 Parabolic reflector

- 10.6.5.2 Double reflector

- 10.7 OTHER SYSTEMS

11 SATELLITES MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 PAYLOAD TECHNOLOGY USED ACROSS SATELLITE APPLICATIONS

- 11.2.1 SENSING AND IMAGING PAYLOADS (OPTICAL, IR, MULTISPECTRAL, HYPERSPECTRAL, SAR, LIDAR): TOP USE CASES

- 11.2.2 COMMUNICATION PAYLOADS (RF/OPTICAL TRANSPONDERS, IOT/M2M, DATA RELAY, AIS/ADS-B): TOP USE CASES

- 11.2.3 SCIENTIFIC AND MISSION-SUPPORT PAYLOADS (ATMOSPHERIC SENSORS, GNSS-R, PARTICLE DETECTORS, TECH-DEMO PAYLOADS): TOP USE CASES

- 11.3 COMMUNICATION SATELLITES

- 11.3.1 GROWING DEMAND FOR GLOBAL CONNECTIVITY AND RESILIENT COMMUNICATION INFRASTRUCTURE TO DRIVE MARKET

- 11.4 NAVIGATION SATELLITES

- 11.4.1 DEPENDENCE OF CRITICAL INFRASTRUCTURE AND MILITARY OPERATIONS ON PRECISE PNT SERVICES TO DRIVE MARKET

- 11.5 EARTH OBSERVATION SATELLITES

- 11.5.1 RISING NEED FOR REAL-TIME INTELLIGENCE AND DATA-DRIVEN ENVIRONMENTAL MONITORING TO DRIVE MARKET

- 11.6 OTHERS

12 SATELLITES MARKET, BY CUSTOMER TYPE

- 12.1 INTRODUCTION

- 12.2 REGION-WISE GOVERNMENT AND PRIVATE SATELLITE LAUNCH PROGRAMS

- 12.2.1 GOVERNMENT PROGRAMS: TOP USE CASES

- 12.2.2 PRIVATE PROGRAMS: TOP USE CASES

- 12.3 COMMERCIAL

- 12.3.1 SATELLITE OPERATORS/OWNERS

- 12.3.1.1 Rapid deployment of satellite constellations to drive market

- 12.3.2 MEDIA & ENTERTAINMENT COMPANIES

- 12.3.2.1 High demand for fast broadband connectivity from streaming platforms to drive market

- 12.3.3 ENERGY SERVICE PROVIDERS

- 12.3.3.1 Integration of satellite technology to enhance energy-related operations and services to drive market

- 12.3.4 SCIENTIFIC RESEARCH & DEVELOPMENT ORGANIZATIONS

- 12.3.4.1 Untapped potential in space research to drive market

- 12.3.5 OTHERS

- 12.3.1 SATELLITE OPERATORS/OWNERS

- 12.4 GOVERNMENT & CIVIL

- 12.4.1 NATIONAL SPACE AGENCIES

- 12.4.1.1 Need for cost-effective space exploration solutions to drive market

- 12.4.2 SEARCH & RESCUE ENTITIES

- 12.4.2.1 Need for swift and accurate data in emergencies to drive market

- 12.4.3 ACADEMIC & RESEARCH INSTITUTIONS

- 12.4.3.1 Active participation in satellite development to drive market

- 12.4.4 NATIONAL MAPPING & TOPOGRAPHIC AGENCIES

- 12.4.4.1 Emphasis on improving navigation and tracking capabilities to drive market

- 12.4.1 NATIONAL SPACE AGENCIES

- 12.5 DEFENSE

- 12.5.1 RESILIENT AND MISSION-CRITICAL SPACE ARCHITECTURES TO DRIVE MARKET

13 SATELLITES MARKET, BY FREQUENCY

- 13.1 INTRODUCTION

- 13.2 SATELLITE THROUGHPUT CATEGORIES ACROSS DIFFERENT FREQUENCY BANDS

- 13.2.1 LOW THROUGHPUT SATELLITES (1 KBPS-50 MBPS): TOP USE CASES

- 13.2.2 HIGH THROUGHPUT SATELLITES (50 MBPS-100+ GBPS): TOP USE CASES

- 13.3 L-BAND

- 13.3.1 NEED FOR EFFECTIVE SATELLITE COMMUNICATION AND GPS SERVICES TO BOOST GROWTH

- 13.4 S-BAND

- 13.4.1 INCREASING SCIENTIFIC MISSIONS TO DRIVE DEMAND FOR S-BAND SATELLITES

- 13.5 C-BAND

- 13.5.1 ESCALATING DEMAND FOR STEADY COMMUNICATIONS SERVICES FROM DEVELOPING REGIONS TO DRIVE MARKET

- 13.6 X-BAND

- 13.6.1 RISING GEOPOLITICAL TENSIONS TO DRIVE MARKET

- 13.7 KU-K BAND

- 13.7.1 GROWING INTERNET PENETRATION IN SATELLITES TO DRIVE MARKET

- 13.8 KA-BAND

- 13.8.1 NEED FOR BACKHAUL SOLUTIONS WITH EXPANSION OF 5G TO DRIVE MARKET

- 13.9 Q/V/E-BAND

- 13.9.1 ELEVATED DEMAND FOR ULTRA-HIGH-SPEED DATA SERVICES TO DRIVE MARKET

- 13.10 HF/VHF/UHF-BAND

- 13.10.1 NEED FOR WIDE-RANGE COVERAGE TO DRIVE MARKET

- 13.11 LASER/OPTICAL BAND

- 13.11.1 DEVELOPMENT OF LASER COMMUNICATION TECHNOLOGY BY PROMINENT COMPANIES TO DRIVE MARKET

14 SATELLITES MARKET, BY PROPULSION TECHNOLOGY

- 14.1 INTRODUCTION

- 14.2 HIGH-THRUST PROPULSION SYSTEMS (100-2,000 N): TOP USE CASES

- 14.2.1 LOW-THRUST PROPULSION SYSTEMS (MICRO-NEWTON TO < 100 N): TOP USE CASES

- 14.3 CHEMICAL

- 14.3.1 FOCUS ON FAST ORBIT INSERTION AND COLLISION AVOIDANCE TO DRIVE MARKET

- 14.3.1.1 Solid

- 14.3.1.2 Liquid

- 14.3.1.3 Hybrid

- 14.3.1 FOCUS ON FAST ORBIT INSERTION AND COLLISION AVOIDANCE TO DRIVE MARKET

- 14.4 ELECTRIC

- 14.4.1 EFFICIENCY OF ELECTRIC PROPULSION TO DRIVE CONSTELLATION-SCALE DEPLOYMENT OF SATELLITES

- 14.4.1.1 Electrostatic

- 14.4.1.2 Electrothermal

- 14.4.1.3 Electromagnetic

- 14.4.1 EFFICIENCY OF ELECTRIC PROPULSION TO DRIVE CONSTELLATION-SCALE DEPLOYMENT OF SATELLITES

- 14.5 OTHER TECHNOLOGIES

- 14.5.1 SOLAR SAIL

- 14.5.2 COLD GAS/WARM GAS

15 SATELLITES MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Integration of national security objectives with commercial space capabilities to drive market

- 15.2.2 CANADA

- 15.2.2.1 Sovereign Earth observation needs and climate-driven policy mandates to drive market

- 15.2.1 US

- 15.3 ASIA PACIFIC

- 15.3.1 CHINA

- 15.3.1.1 State-led expansion of satellite constellations to drive market

- 15.3.2 INDIA

- 15.3.2.1 Demand for digital connectivity, Earth observation, navigation augmentation, and defense surveillance to drive market

- 15.3.3 JAPAN

- 15.3.3.1 Emphasis on Earth observation, navigation augmentation, and defense-related satellite systems to drive market

- 15.3.4 SOUTH KOREA

- 15.3.4.1 Government funding for satellite development to drive market

- 15.3.5 AUSTRALIA

- 15.3.5.1 Government measures to develop domestic space industry to drive market

- 15.3.1 CHINA

- 15.4 EUROPE

- 15.4.1 RUSSIA

- 15.4.1.1 National security dependence on sovereign space infrastructure to drive market

- 15.4.2 UK

- 15.4.2.1 Commercial satellite services aligned with national resilience objectives to drive market

- 15.4.3 GERMANY

- 15.4.3.1 Emphasis on technological innovation and advanced engineering to drive market

- 15.4.4 FRANCE

- 15.4.4.1 Defense-led satellite modernization and sustained institutional funding to drive market

- 15.4.5 ITALY

- 15.4.5.1 Targeted investments in application-specific missions to drive market

- 15.4.1 RUSSIA

- 15.5 MIDDLE EAST

- 15.5.1 UAE

- 15.5.1.1 National technology leadership and sovereign space capability to drive market

- 15.5.2 SAUDI ARABIA

- 15.5.2.1 Growing investments in satellite infrastructure to drive market

- 15.5.3 REST OF MIDDLE EAST

- 15.5.1 UAE

- 15.6 REST OF THE WORLD (ROW)

- 15.6.1 LATIN AMERICA

- 15.6.1.1 Use of satellites for monitoring and management to drive market

- 15.6.2 AFRICA

- 15.6.2.1 Development-driven demand for data, connectivity, and capacity building to drive market

- 15.6.1 LATIN AMERICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.3 REVENUE ANALYSIS, 2021-2024

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.5.1 STARS

- 16.5.2 EMERGING LEADERS

- 16.5.3 PERVASIVE PLAYERS

- 16.5.4 PARTICIPANTS

- 16.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.6.1 PROGRESSIVE COMPANIES

- 16.6.2 RESPONSIVE COMPANIES

- 16.6.3 DYNAMIC COMPANIES

- 16.6.4 STARTING BLOCKS

- 16.6.5 COMPETITIVE BENCHMARKING

- 16.7 COMPANY VALUATION AND FINANCIAL METRICS

- 16.8 BRAND/PRODUCT COMPARISON

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 SPACEX

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.3.2 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 LOCKHEED MARTIN CORPORATION

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Deals

- 17.1.2.3.2 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 AIRBUS

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Other developments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 NORTHROP GRUMMAN

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.3.2 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 THALES ALENIA SPACE

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Deals

- 17.1.5.3.2 Other developments

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses & competitive threats

- 17.1.6 L3HARRIS TECHNOLOGIES, INC.

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.6.3.2 Other developments

- 17.1.7 MDA SPACE

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Other developments

- 17.1.8 PLANET LABS PBC

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.8.3.3 Other developments

- 17.1.9 SNC

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Other developments

- 17.1.10 LANTERIS SPACE SYSTEMS

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deals

- 17.1.10.3.2 Other developments

- 17.1.11 MITSUBISHI ELECTRIC CORPORATION

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.11.3.2 Other developments

- 17.1.12 RTX

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Other developments

- 17.1.13 OHB SE

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.13.3.2 Other developments

- 17.1.14 BOEING

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Solutions/Services offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Other developments

- 17.1.15 YORK SPACE SYSTEMS

- 17.1.15.1 Business overview

- 17.1.15.2 Products/Solutions/Services offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Other developments

- 17.1.16 SURREY SATELLITE TECHNOLOGY LTD.

- 17.1.16.1 Business overview

- 17.1.16.2 Products/Solutions/Services offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Deals

- 17.1.1 SPACEX

- 17.2 OTHER PLAYERS

- 17.2.1 AEROSPACELAB

- 17.2.2 ENDUROSAT

- 17.2.3 NANOAVIONICS

- 17.2.4 ASTRANIS

- 17.2.5 ICEYE

- 17.2.6 PIXXEL

- 17.2.7 FLEET SPACE TECHNOLOGIES PTY LTD

- 17.2.8 AMAZON LEO

- 17.2.9 ALEN SPACE

- 17.2.10 SKYKRAFT PTY LTD

- 17.2.11 ARGOTEC S.R.L.

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Primary sources

- 18.1.2.2 Key data from primary sources

- 18.1.2.3 Breakdown of primary interviews

- 18.1.1 SECONDARY DATA

- 18.2 FACTOR ANALYSIS

- 18.2.1 INTRODUCTION

- 18.2.2 DEMAND-SIDE INDICATORS

- 18.2.3 SUPPLY-SIDE INDICATORS

- 18.3 MARKET SIZE ESTIMATION

- 18.3.1 BOTTOM-UP APPROACH

- 18.3.1.1 Market size estimation methodology (demand side)

- 18.3.2 TOP-DOWN APPROACH

- 18.3.1 BOTTOM-UP APPROACH

- 18.4 DATA TRIANGULATION

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS