|

시장보고서

상품코드

1956049

PFAS 여과 시장 : 오염물질 유형별, 최종 이용 산업별, 환경 매체별, 정화 기술별, 처리 장소별, 서비스 유형별, 기술 유형별, 지역별 - 세계 예측(-2031년)PFAS Filtration Market, By Technology (Water Treatment Systems, Water Treatment Chemicals), Place of Treatment, Remediation Technology, Environmental Medium, End-use Industry (Industrial, Municipal, Commercial), and Region - Global Forecast To 2031 |

||||||

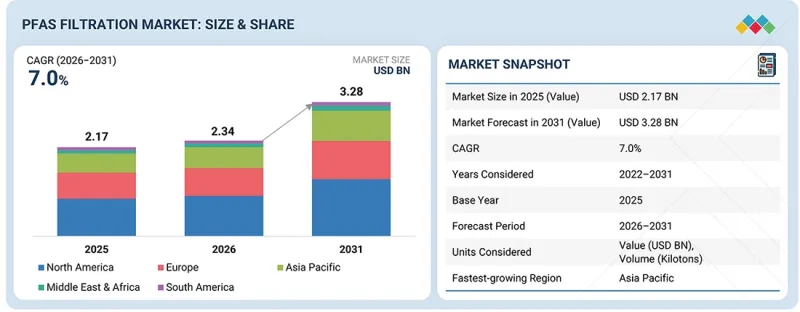

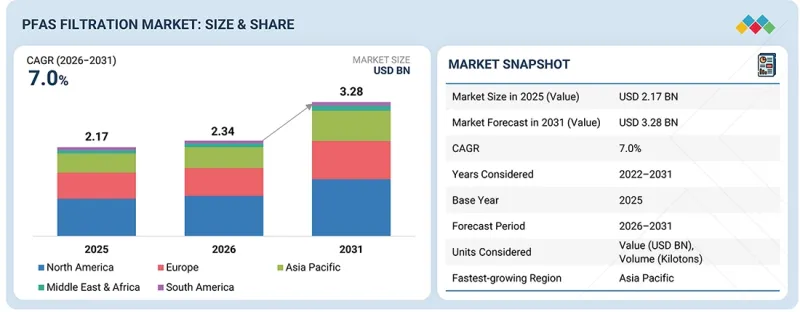

PFAS 여과 시장 규모는 예측 기간 동안 CAGR 7.0%로 성장하여 2026년 23억 4,000만 달러에서 2031년까지 32억 8,000만 달러에 달할 것으로 전망됩니다.

이온교환수지는 이온교환 능력을 이용하여 액체에서 용해된 오염물질을 분리하는 기능을 갖도록 설계된 고분자 비드입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 가치, 킬로톤 |

| 부문 | 오염물질 유형별, 최종 이용 산업별, 환경 매체별, 정화 기술별, 처리 장소별, 서비스 유형별, 기술 유형별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

이 기술은 무기이온, 중금속, 신종 오염물질인 PFAS 등 3가지 오염물질을 제거할 수 있어 물과 폐수처리에 효과적으로 작용합니다. 이온교환수지의 사용은 표준 흡착제에 비해 더 높은 선택성, 더 빠른 처리 속도, 더 긴 시스템 내구성을 보여주기 때문에 낮은 오염 수준에서도 우수한 성능을 발휘합니다. 이 수지는 도시 식수 시스템뿐만 아니라 산업 폐수처리 및 환경 정화 작업에도 활용되고 있습니다. 이온교환수지의 적용은 일회용 시스템 또는 재생 가능한 시스템 중 하나를 필요로 하며, 이를 통해 성능 효율과 수명 주기 비용의 최적화를 실현할 수 있습니다.

지자체 부문에서는 정부 기준을 충족하는 안전한 식수를 공급하는 동시에 변화하는 환경 규제에 따라 폐수를 처리해야 하기 때문에 수처리 기술이 요구됩니다. 지자체 사업자들은 PFAS, 중금속, 유기오염물질 등의 오염물질을 처리하기 위해 이온교환수지, 활성탄, 멤브레인 시스템 등 첨단 처리 솔루션을 점점 더 많이 채택하고 있습니다. 규제 요구의 증가, 노후화된 시설, 공중보건에 대한 지식의 향상 등의 요인이 결합되어 처리 시스템 강화를 추진하고 있습니다. 지자체는 PFAS 여과 시스템 및 첨단 수처리 기술에 대한 지속적인 시장을 제공하고 있으며, 이러한 기술은 향후 수년간 활용될 것으로 예상됩니다.

북미는 엄격한 정부 규제, 높아진 시민의식, 효과적인 집행 방식으로 인해 첨단 수처리 기술 및 PFAS 여과 기술의 주요 시장입니다. 지자체 수도사업체, 산업시설, 국방시설은 보다 엄격한 식수 및 폐수 기준을 충족하기 위해 이온교환수지, 활성탄, 신규 흡착제 기술에 많은 투자를 하고 있습니다.

북미 PFAS 여과 시장의 성장은 공공 자금, 소송으로 인한 정화 프로그램, 기술 발전(신기술의 출현)의 세 가지 요인에 기인합니다.

이 보고서는 기업 프로파일에 대한 종합적인 분석을 제공합니다.

주요 기업으로는 Veolia(프랑스), AECOM(미국), WSP(캐나다), Clean Earth(미국), Xylem(미국), Jacobs(미국), TRC Companies, Inc.(미국), Battelle Memorial Institute(미국), Cyclopure(미국), John Wood Group PLC(영국), Ion Exchange(인도), Ecolab Inc.(미국) 등이 있습니다.

조사 범위

본 보고서는 PFAS 여과 시장을 오염물질 유형별, 환경 매체별, 정화 기술별, 처리 장소별, 서비스 유형별, 기술 유형별, 최종 이용 산업별, 지역별로 분류하고 있습니다. 이 보고서의 조사 범위에는 PFAS 여과 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 진출 기업들에 대한 철저한 조사를 통해 각 기업의 사업 개요, 솔루션, 서비스, 주요 전략, 계약, 제휴, 합의에 대한 인사이트를 제공합니다. PFAS 여과 시장의 제품 출시, 인수합병, 최근 동향에 대해서도 다루고 있습니다. 본 보고서에는 PFAS 여과 시장 생태계의 신생 스타트업 기업의 경쟁에 대한 인사이트도 포함되어 있습니다.

본 보고서 구매의 장점:

이 보고서는 시장 리더와 신규 진입자에게 전체 PFAS 여과 시장 및 하위 부문의 수익 수치에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 사업 포지셔닝을 최적화하고 적절한 시장 진입 전략을 수립하는 데 도움이 되는 인사이트를 얻을 수 있습니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(오염자에 대한 소송 및 책임 비용 증가, PFAS 노출에 따른 건강 위험에 대한 대중의 인식 제고), 억제요인(고가의 복잡한 여과 공정, 숙련된 전문가 부족), 기회(전 세계 확대 가능성), 도전 과제(PFAS 처리 잔여물의 적절한 관리) 분석 분석.

- 제품 개발/혁신 : PFAS 여과 시장의 신기술, R&D 활동, 서비스 개발에 대한 상세한 분석.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 PFAS 여과 시장을 분석합니다.

- 시장 다각화 : PFAS 여과 시장의 서비스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보.

- 경쟁사 평가 : Veolia(프랑스), AECOM(미국), WSP(캐나다), Clean Earth(미국), Xylem(미국), Jacobs(미국), TRC Companies, Inc(미국), Battelle Memorial Institute(미국), Cyclopure(미국), John Wood Group plc(영국), Ion Exchange(인도), Ecolab Inc. Cyclopure(미국), John Wood Group plc(영국), Ion Exchange(인도), Ecolab Inc.(미국) 등 PFAS 여과 시장의 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보와 특허

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 PFAS 여과 시장(오염물질 유형별)

제10장 PFAS 여과 시장(최종 이용 산업별)

제11장 PFAS 여과 시장(환경 매체별)

제12장 PFAS 여과 시장(정화 기술별)

제13장 PFAS 여과 시장(처리 장소별)

제14장 PFAS 여과 시장(서비스 유형별)

제15장 PFAS 여과 시장(기술 유형별)

제16장 PFAS 여과 시장(지역별)

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSM 26.03.19The PFAS filtration market is projected to grow from USD 2.34 billion in 2026 to USD 3.28 billion by 2031, at a CAGR of 7.0% during the forecast period. Ion exchange resins are engineered polymer beads that function to separate dissolved contaminants from liquids by using their ion exchange capability.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2024 |

| Forecast Period | 2026-2031 |

| Units Considered | Value, Volume (Kilotons) |

| Segments | Remediation Technology, Technology, Contaminant Type, Environmental Medium, Place of Treatment, Service Type, End-use Industry, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

The technology functions effectively to treat water and wastewater because it can remove three types of pollutants: inorganic ions, heavy metals, and PFAS, which are emerging contaminants. The use of ion exchange resins enables superior performance at low contaminant levels because they exhibit greater selectivity, faster operation speeds, and longer system durability when compared to standard adsorbents. The resins find use in municipal drinking water systems as well as industrial wastewater treatment and environmental cleanup operations. The application of ion exchange resins requires either single-use or regenerable systems, which enable both performance efficiency and lifecycle cost optimization.

''By end-use industry, the municipal segment accounted for the largest share of the PFAS filtration market.''

The municipal sector requires water treatment technologies because it needs to deliver safe drinking water that meets government standards while treating wastewater according to changing environmental regulations. Municipal utilities increasingly adopt advanced treatment solutions such as ion exchange resins, activated carbon, and membrane systems to treat contaminants, which include PFAS, heavy metals, and organic pollutants. The combination of increasing regulatory demands, outdated facilities, and heightened public health knowledge drives treatment system enhancements. Municipalities provide an ongoing market for PFAS filtration systems and advanced water treatment technologies, which they will use for many years.

"North America is estimated to account for the largest market share during the forecast period."

North America is the key market for advanced water treatment and PFAS filtration technologies because of stringent government rules, growing public awareness, and effective enforcement methods. Municipal utilities, industrial facilities, and defense sites heavily invest in ion exchange resins, activated carbon, and new adsorbent technologies to comply with stricter drinking water and discharge requirements.

The growth of the PFAS filtration market in North America is attributed to three factors: public funding, remediation programs that result from litigation, and technological advancements (emergence of new technologies).

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

- By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

- By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies are Veolia (France), AECOM (US), WSP (Canada), Clean Earth (US), Xylem (US), Jacobs (US), TRC Companies, Inc. (US), Battelle Memorial Institute (US), Cyclopure (US), John Wood Group PLC (UK), Ion Exchange (India), and Ecolab Inc. (US).

Study Coverage

This research report categorizes the PFAS filtration market by Contaminant Type (PFOA & PFOS, Multiple PFAS Compounds), Environmental Medium (Groundwater Remediation, Soil Remediation, Surface Water & Sediment Remediation), Remediation Technology (Membranes, Chemicals), Place of Treatment (In-Situ, Ex-Situ), Service Type (On-Site, Off-Site), Technology Type (Water Treatment Systems, Water Treatment Chemicals), End-use Industry (Industrial, Municipal, Commercial), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the PFAS filtration market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the PFAS filtration market are all covered. This report includes a competitive analysis of upcoming startups in the PFAS filtration market ecosystem.

Reasons to Buy this Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall PFAS filtration market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising litigation and liability costs for polluters, growing public awareness of health risks associated with PFAS exposure), restraints (Expensive and complex filtration process, Limited availability of trained professionals), opportunities (Significant potential to expand globally), and challenges (Proper management of PFAS treatment residuals).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the PFAS filtration market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the PFAS filtration market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the PFAS filtration market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Veolia (France), AECOM (US), WSP (Canada), Clean Earth (US), Xylem (US), Jacobs (US), TRC Companies, Inc. (US), Battelle Memorial Institute (US), Cyclopure (US), John Wood Group plc (UK), Ion Exchange (India), and Ecolab Inc. (US), among others, in the PFAS filtration market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 STUDY SCOPE

- 1.4.1 MARKETS COVERED

- 1.4.2 YEARS CONSIDERED

- 1.4.3 CURRENCY CONSIDERED

- 1.4.4 UNIT CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PFAS FILTRATION MARKET

- 3.2 PFAS FILTRATION MARKET, BY REMEDIATION TECHNOLOGY

- 3.3 PFAS FILTRATION MARKET, BY END-USE INDUSTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing regulatory scrutiny and tightening environmental regulations regarding PFAS contamination

- 4.2.1.2 Growing awareness of health risks associated with PFAS exposure

- 4.2.1.3 Expansion of manufacturing, chemical processing, and semiconductor industries

- 4.2.1.4 Rising litigation and liability costs for polluters

- 4.2.2 RESTRAINTS

- 4.2.2.1 Expensive and complex filtration process

- 4.2.2.2 Limited availability of trained professionals

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Significant potential to expand globally

- 4.2.3.2 Substantial government funding and support for PFAS R&D

- 4.2.4 CHALLENGES

- 4.2.4.1 Management of residuals from PFAS treatment

- 4.2.4.2 Understanding potential risks and treatment requirements for emerging PFAS compounds

- 4.2.4.3 Retrofitting existing water treatment plants for PFAS filtration

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN PFAS FILTRATION MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.3 EMERGING BUSINESS MODELS

- 4.4.4 ECOSYSTEM SHIFTS

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 SEMICONDUCTOR MANUFACTURING PLANTS

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO FOR HS CODE 842121

- 5.6.2 EXPORT SCENARIO FOR HS CODE 842121

- 5.7 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 MUNICIPAL WASTEWATER TREATMENT PLANT (MICHIGAN) - CYCLOPURE

- 5.10.2 DRINKING WATER TREATMENT PLANT (ALASKA)-CYCLOPURE

- 5.10.3 NOSENZO POND DRINKING WATER TREATMENT PLANT (CYCLOPURE)

- 5.10.4 VEOLIA

- 5.10.5 CAPE FEAR PUBLIC UTILITY AUTHORITY (EVOQUA WATER TECHNOLOGIES)

- 5.10.6 NEW JERSEY AMERICAN WATER (CALGON CARBON CORPORATION)

- 5.10.7 REGENESIS

- 5.11 IMPACT OF 2025 US TARIFF - PFAS FILTRATION MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS AND PATENTS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 DEXSORB

- 6.1.1.1 Key features and benefits

- 6.1.1.2 Key advantages over other PFAS technologies

- 6.1.1.3 Key differentiators with competing technologies

- 6.1.2 COATED SAND

- 6.1.3 MODIFIED CLAY TECHNOLOGY

- 6.1.4 NANO FILTRATION (NF) AND REVERSE OSMOSIS (RO)

- 6.1.5 SORPTION TECHNOLOGY

- 6.1.6 ION EXCHANGE RESIN

- 6.1.7 IN SITU REMEDIATION WITH COLLOIDAL ACTIVATED CARBON

- 6.1.8 SOIL WASHING

- 6.1.9 ZEOLITE & CLAY MINERALS

- 6.1.1 DEXSORB

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 FOAM FRACTIONATION

- 6.3 PATENT ANALYSIS

- 6.3.1 INTRODUCTION

- 6.3.2 JURISDICTION ANALYSIS

7 REGULATORY LANDSCAPE

- 7.1 REGULATIONS

- 7.1.1 NORTH AMERICA

- 7.1.2 EUROPE

- 7.1.3 ASIA PACIFIC

- 7.1.4 MIDDLE EAST & AFRICA AND SOUTH AMERICA

- 7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

8 CUSTOMER LANDSCAPE AND BUYING BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.2.2.1 Quality

- 8.2.2.2 Service

9 PFAS FILTRATION MARKET, BY CONTAMINANT TYPE

- 9.1 INTRODUCTION

- 9.2 PFOA & PFOS

- 9.2.1 SIGNIFICANT PUBLIC HEALTH RISKS ASSOCIATED WITH PRESENCE IN ENVIRONMENT TO DRIVE MARKET

- 9.3 MULTIPLE PFAS COMPOUNDS

- 9.3.1 STRINGENT REGULATORY RESPONSE TO DRIVE MARKET

10 PFAS FILTRATION MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 INDUSTRIAL

- 10.2.1 OIL & GAS

- 10.2.1.1 Stringent environmental regulations to drive market

- 10.2.2 PHARMACEUTICAL

- 10.2.2.1 Growing awareness of health and environmental impacts of PFAS contamination to drive market

- 10.2.3 CHEMICAL MANUFACTURING

- 10.2.3.1 Expanding chemical manufacturing sector to drive market

- 10.2.4 MINING AND MINERAL PROCESSING

- 10.2.4.1 Growing mining industry and stringent discharge regulations to drive market

- 10.2.5 OTHER INDUSTRIAL SEGMENTS

- 10.2.1 OIL & GAS

- 10.3 COMMERCIAL

- 10.3.1 ACTIVATED CARBON, DEXSORB, AND ION EXCHANGE: EFFECTIVE PFAS FILTRATION METHODS IN COMMERCIAL SEGMENT

- 10.4 MUNICIPAL

- 10.4.1 DRINKING WATER TREATMENT

- 10.4.1.1 Stringent environmental regulations related to drinking water to drive market

- 10.4.2 WASTEWATER TREATMENT

- 10.4.2.1 Growing public concern to drive market

- 10.4.1 DRINKING WATER TREATMENT

11 PFAS FILTRATION MARKET, BY ENVIRONMENTAL MEDIUM

- 11.1 INTRODUCTION

- 11.2 GROUNDWATER REMEDIATION

- 11.2.1 STRINGENT FEDERAL AND STATE REGULATIONS TO DRIVE MARKET

- 11.3 SOIL REMEDIATION

- 11.3.1 EFFECTIVE ELIMINATION OR NEUTRALIZATION OF PFAS CONTAMINANTS TO DRIVE MARKET

- 11.4 SURFACE WATER AND SEDIMENT REMEDIATION

- 11.4.1 INCREASING AWARENESS OF PFAS CONTAMINATION TO BOOST MARKET

12 PFAS FILTRATION MARKET, BY REMEDIATION TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 MEMBRANES

- 12.2.1 ADOPTION OF MEMBRANE TECHNOLOGIES DRIVEN BY STRINGENT ENVIRONMENTAL REGULATIONS

- 12.2.2 RO MEMBRANES

- 12.3 CHEMICALS

- 12.3.1 COST-EFFECTIVE FOR LARGE-SCALE REMEDIATION

- 12.3.2 ACTIVATED CARBON ADSORPTION

- 12.3.3 CHEMICAL OXIDATION

- 12.3.4 ION EXCHANGE RESIN

- 12.3.5 BIOREMEDIATION

- 12.3.6 OTHER REMEDIATION TECHNOLOGIES

13 PFAS FILTRATION MARKET, BY PLACE OF TREATMENT

- 13.1 INTRODUCTION

- 13.2 IN-SITU

- 13.2.1 MINIMIZES SITE DISRUPTION AND REDUCES MATERIAL HANDLING COSTS

- 13.3 EX-SITU

- 13.3.1 ENABLES GREATER CONTROL OVER TREATMENT CONDITIONS

14 PFAS FILTRATION MARKET, BY SERVICE TYPE

- 14.1 INTRODUCTION

- 14.2 ON-SITE

- 14.2.1 IMMEDIACY AND CONVENIENCE TO DRIVE DEMAND

- 14.3 OFF-SITE

- 14.3.1 SUITABILITY FOR MUNICIPAL & INDUSTRIAL END-USE INDUSTRIES TO DRIVE DEMAND

15 PFAS FILTRATION MARKET, BY TECHNOLOGY TYPE

- 15.1 INTRODUCTION

- 15.2 WATER TREATMENT SYSTEMS

- 15.2.1 RISING CONCERNS ABOUT WIDESPREAD CONTAMINATION OF WATER SOURCES TO DRIVE MARKET

- 15.3 WATER TREATMENT CHEMICALS

- 15.3.1 TECHNOLOGICAL ADVANCEMENTS IN WATER TREATMENT CHEMICALS TO DRIVE MARKET

16 PFAS FILTRATION MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 Stringent regulations on PFAS contamination to drive market

- 16.2.2 CANADA

- 16.2.2.1 Rising government initiatives for PFAS removal to drive market

- 16.2.3 MEXICO

- 16.2.3.1 Increasing demand across industries to drive market

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 GERMANY

- 16.3.1.1 Rising demand from end-use industries to fuel market growth

- 16.3.2 FRANCE

- 16.3.2.1 Growing focus on adherence to EU drinking water regulations to drive demand

- 16.3.3 UK

- 16.3.3.1 Government and university funding in PFAS removal projects to drive market

- 16.3.4 REST OF EUROPE

- 16.3.1 GERMANY

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Stringent water treatment policies to drive demand

- 16.4.2 JAPAN

- 16.4.2.1 Growing pharmaceutical industry to drive market

- 16.4.3 AUSTRALIA

- 16.4.3.1 Stringent government regulations to drive market

- 16.4.4 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.5.1.1 Saudi Arabia

- 16.5.1.1.1 Government focus on water and wastewater treatment to drive market

- 16.5.1.2 UAE

- 16.5.1.2.1 Strong oil & gas sector to drive market

- 16.5.1.3 Other GCC countries

- 16.5.1.1 Saudi Arabia

- 16.5.2 SOUTH AFRICA

- 16.5.2.1 Growth in mining industry to drive market

- 16.5.3 REST OF MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.6 SOUTH AMERICA

- 16.6.1 BRAZIL

- 16.6.1.1 Government support and regulations to drive market

- 16.6.2 ARGENTINA

- 16.6.2.1 Stringent environmental regulations to drive market

- 16.6.3 REST OF SOUTH AMERICA

- 16.6.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2019-2025

- 17.3 REVENUE ANALYSIS, 2022-2024

- 17.4 MARKET SHARE ANALYSIS, 2025

- 17.5 BRAND/PRODUCT COMPARISON

- 17.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 17.6.1 STARS

- 17.6.2 EMERGING LEADERS

- 17.6.3 PERVASIVE PLAYERS

- 17.6.4 PARTICIPANTS

- 17.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.6.5.1 Company footprint

- 17.6.5.2 Region footprint

- 17.6.5.3 End-use industry footprint

- 17.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 17.7.1 PROGRESSIVE COMPANIES

- 17.7.2 RESPONSIVE COMPANIES

- 17.7.3 DYNAMIC COMPANIES

- 17.7.4 STARTING BLOCKS

- 17.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 17.7.5.1 Detailed list of key startups/SMEs

- 17.7.5.2 Competitive benchmarking of key startups/SMEs

- 17.8 COMPANY VALUATION AND FINANCIAL MATRIX

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 MAJOR PLAYERS

- 18.1.1 VEOLIA

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches

- 18.1.1.3.2 Deals

- 18.1.1.3.3 Expansions

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 AECOM

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Deals

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 WSP

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Deals

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 XYLEM

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Deals

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 JACOBS

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Deals

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 ION EXCHANGE

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 MnM view

- 18.1.7 ECOLAB INC.

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Deals

- 18.1.7.4 MnM view

- 18.1.8 CYCLOPURE

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches

- 18.1.8.3.2 Deals

- 18.1.8.4 MnM view

- 18.1.8.4.1 Key strengths

- 18.1.8.4.2 Strategic choices

- 18.1.8.4.3 Weaknesses and competitive threats

- 18.1.9 CLEAN EARTH

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches

- 18.1.9.3.2 Deals

- 18.1.9.3.3 Expansions

- 18.1.9.4 MnM view

- 18.1.10 JOHN WOOD GROUP PLC

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 MnM view

- 18.1.11 TRC COMPANIES, INC.

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions/Services offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Deals

- 18.1.11.4 MnM view

- 18.1.12 BATTELLE MEMORIAL INSTITUTE

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions/Services offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Product launches

- 18.1.12.4 MnM view

- 18.1.1 VEOLIA

- 18.2 OTHER PLAYERS

- 18.2.1 CALGON CARBON CORPORATION

- 18.2.2 REGENESIS

- 18.2.3 MINERAL TECHNOLOGIES, INC.

- 18.2.4 CDM SMITH, INC.

- 18.2.5 PENTAIR

- 18.2.6 AQUASANA INC.

- 18.2.7 NEWTERRA CORPORATION

- 18.2.8 LANXESS

- 18.2.9 EUROWATER

- 18.2.10 AQUA-AEROBIC SYSTEMS, INC.

- 18.2.11 HYDROVIV

- 18.2.12 SALTWORKS TECHNOLOGIES, INC.

- 18.2.13 AQUAGGA, INC.

- 18.2.14 ONVECTOR LLC.

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Key data from primary sources

- 19.1.2.2 Breakdown of primary interviews

- 19.1.2.3 Key industry insights

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 TOP-DOWN APPROACH

- 19.2.2 BOTTOM-UP APPROACH

- 19.3 DATA TRIANGULATION

- 19.4 RESEARCH ASSUMPTIONS

- 19.5 RESEARCH LIMITATIONS

20 APPENDIX

- 20.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.2 CUSTOMIZATION OPTIONS

- 20.3 RELATED REPORTS

- 20.4 AUTHOR DETAILS