|

시장보고서

상품코드

1961000

정맥내(IV) 장비 시장 예측(-2031년) : 유형별, 용도별, 최종사용자별, 지역별IV Equipment Market by Type (IV Catheter, IV Administration Set, Needle-free Connectors), Application (Medication Administration, Parenteral Nutrition, Diagnostic Testing, Blood & Blood Product Transfusion), End User (Hospital) - Global Forecast to 2031 |

||||||

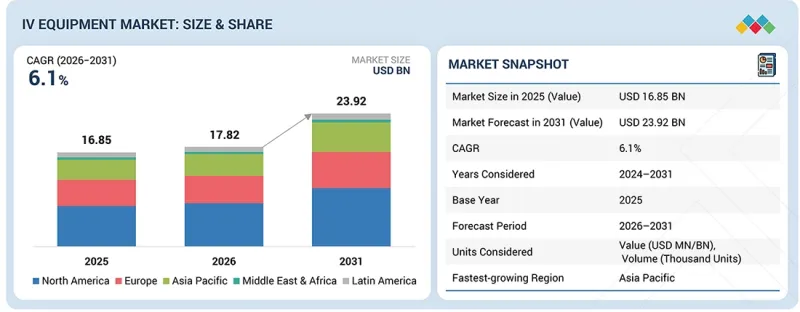

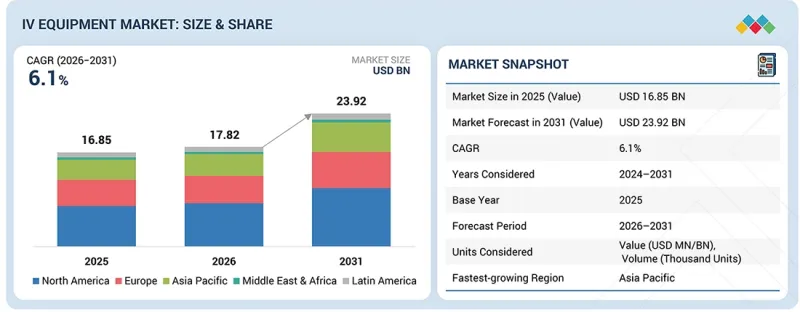

세계의 정맥내(IV) 장비 시장 규모는 2026년 178억 2,000만 달러에서 2031년까지 239억 2,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR 6.1%로 성장할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카. |

세계 만성질환 증가와 입원환자 증가를 배경으로 정맥주사(IV) 의료기기 수요는 꾸준히 확대되고 있습니다. 약물 투여, 수분 보충, 영양 보충을 위한 IV 요법의 보급 확대와 더불어 재택치료 및 외래 치료로의 전환이 진행됨에 따라 제품 이용이 촉진되고 있습니다. 병원 및 진료소에서는 정확한 약물 투여와 환자의 안전을 보장하기 위해 고품질의 안전하고 사용하기 쉬운 정맥 내(IV) 의료기기를 우선적으로 도입하고 있습니다. 바늘 없는 커넥터, 스마트 주입 펌프, 호환 가능한 다기능 IV 시스템과 같은 기술 혁신은 시장 보급을 더욱 촉진하고 있습니다. 또한 신흥 국가의 의료 인프라 확충과 현대적 의료행위를 촉진하기 위한 정부의 적극적인 정책은 향후 수년간 시장의 견고한 성장을 지속할 것으로 예측됩니다.

유형별로는 바늘 없는 커넥터 및 연장 세트가 정맥 내(IV) 의료기기 시장에서 가장 빠르게 성장하는 부문입니다. 그 배경에는 안전성 향상, 조작의 편리성, 감염 위험 및 침 찔림 사고의 현저한 감소 능력이 있습니다. 이 커넥터는 병원, 진료소, 재택치료 환경에서 약품 투여의 효율성, 오염 감소, 워크플로우의 효율화를 실현합니다. 또한 엄격한 감염 관리 규정과 의료 종사자들의 환자 안전에 대한 인식이 높아지면서 현대 의료시설에서 매우 선호되는 선택이 되고 있습니다.

용도별로는 약물 투여가 정맥내 투여 기기 시장에서 가장 큰 점유율을 차지하고 있습니다. 정맥내 요법은 약물을 혈류에 직접 주입하므로 약효 발현이 빠르고, 용량이 정확하며, 최적의 치료 효과를 기대할 수 있기 때문입니다. 이 용도는 특히 중환자실, 화학요법, 통증 관리, 중증 감염 치료에서 중요하며, 신속하고 정확한 약물 투여가 환자의 결과를 크게 개선합니다. 만성 및 급성 질환의 유병률 증가와 입원 환자 수 증가에 따라 정맥내 약물 투여에 대한 수요는 지속적으로 증가하고 있습니다.

정맥 투여 기기 시장은 북미, 유럽, 라틴아메리카, 아시아태평양, 중동 및 아프리카로 분류됩니다. 북미는 세계 정맥내 투여 기기 시장을 선도하고 있습니다. 이러한 우위는 높은 만성질환 유병률, 잘 구축된 의료 인프라, 첨단 의료기술의 빠른 도입에 기인합니다. 또한 주요 시장 진출기업의 강력한 존재감, 의료비 지출 증가, 병원 및 재택치료 환경에서의 첨단 주입 시스템에 대한 수요 증가는 이 지역 시장 선도적 지위를 더욱 지원하고 있습니다.

정맥 투여 기기 시장의 주요 업체는 다음과 같습니다. Becton, Dickinson and Company(미국), B. Braun SE(독일), Fresenius SE & Co. KGaA(독일), ICU Medical, Inc. Teleflex Incorporated(미국), Cardinal Health(미국), Shenzhen Mindray Bio-Medical Electronics(중국), Baxter(미국), Avanos Medical, Inc(미국), Nipro(일본), JMS(일본), Vitality, Inc. JMS(일본), Vygon(프랑스), Micrel Medical Devices SA(그리스) 등이 있습니다.

조사 범위

이 보고서는 정맥 내(IV) 의료기기 시장을 유형별, 용도별, 최종사용자별, 지역별로 분석합니다. 또한 시장 성장에 영향을 미치는 요인을 포괄하고, 시장의 다양한 기회와 과제를 분석하는 한편, 시장 리더경쟁 구도를 상세하게 제공합니다. 또한 마이크로마켓을 개별 성장 추세별로 분석하고, 5개 주요 지역(및 해당 지역내 국가) 시장 세분화에 대한 매출 예측을 제공합니다.

이 보고서 구매의 장점

이 보고서는 기존 기업 및 신규 진출기업/중소기업이 시장 동향을 파악하고 더 큰 시장 점유율을 확보하는 데 도움이 될 것입니다. 이 보고서를 구매하는 기업은 다음 전략 중 하나 또는 조합을 활용하여 시장에서의 입지를 강화할 수 있습니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

- 정맥주사(IV) 기기 시장의 성장에 영향을 미치는 주요 촉진요인(전 세계 질병 부담 증가와 이에 따른 고령 인구 급증, 재택 및 외래 환자 투약으로의 전환), 억제요인(제품 리콜 및 고장), 기회(신흥 시장의 미개발 성장 잠재력), 과제(벤더 간 제휴) 등을 분석합니다.

- 시장 침투: 정맥내 투여 기기 시장의 주요 기업이 제공하는 제품 포트폴리오에 대한 종합적인 정보.

- 제품 개발/혁신 : 정맥내 투여 기기 시장의 향후 동향, 연구개발 활동, 제품 개발에 대한 상세한 분석.

- 시장 개발: 수익성이 높은 신흥 지역에 대한 종합적인 정보.

- 시장 다각화 : 정맥 내(IV) 의료기기 시장의 신제품, 성장 지역, 최근 동향에 대한 종합적인 정보를 제공합니다.

- 경쟁 평가: 주요 시장 진출기업 시장 세분화, 성장 전략, 매출 분석, 제품에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 테크놀러지, 특허, 디지털·AI 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 정맥내(IV) 장비 시장(유형별)

제10장 정맥내(IV) 장비 시장(용도별)

제11장 정맥내(IV) 장비 시장(최종사용자별)

제12장 정맥내(IV) 장비 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSAThe global IV equipment market is projected to reach USD 23.92 billion by 2031 from USD 17.82 billion in 2026, growing at a CAGR of 6.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Application, End User, and Region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. |

The demand for IV equipment is growing steadily, driven by the rising prevalence of chronic diseases and increasing hospitalizations worldwide. The growing adoption of IV therapy for medication administration, hydration, and nutrition, along with the shift toward home-based and outpatient care, is boosting product utilization. Hospitals and clinics are prioritizing high-quality, safe, and user-friendly IV devices to ensure accurate drug delivery and patient safety. Technological innovations, such as needle-free connectors, smart infusion pumps, and compatible multi-parameter IV systems, are further enhancing market adoption. Moreover, expanding healthcare infrastructure in emerging economies and favorable government initiatives promoting modern healthcare practices are expected to sustain strong market growth in the coming years.

"By type, the needle-free connectors & extension sets segment is projected to grow significantly during the forecast period."

Based on type, needle-free connectors & extension sets are the fastest-growing segment in the IV equipment market, driven by their enhanced safety, ease of use, and ability to significantly reduce the risk of infections and needlestick injuries. These connectors streamline medication administration, reduce contamination, and improve workflow efficiency in hospitals, clinics, and home care settings. Their growing adoption is also supported by stringent infection control regulations and increasing awareness among healthcare providers about patient safety, making them a highly preferred choice in modern healthcare facilities.

"By application, the medication administration segment held the largest market share in 2025."

By application, medication administration holds the largest market share in the IV equipment market, as IV therapy allows drugs to be delivered directly into the bloodstream, ensuring rapid onset of action, precise dosing, and optimal therapeutic effectiveness. This application is particularly critical in intensive care units, chemotherapy treatments, pain management, and severe infection management, where timely and accurate drug delivery can significantly improve patient outcomes. The growing prevalence of chronic and acute diseases, along with increasing hospital admissions, continues to drive the demand for IV-based medication administration.

"By region, North America accounted for the largest market share in 2025."

The IV equipment market is segmented into North America, Europe, Latin America, the Asia Pacific, and the Middle East & Africa. North America leads the global IV equipment market. This dominance is attributed to the high prevalence of chronic diseases, well-established healthcare infrastructure, and rapid adoption of advanced medical technologies. Additionally, the strong presence of key market players, increased healthcare spending, and growing demand for advanced infusion systems in hospitals and home healthcare settings further contribute to the region's leading market position.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (35%), Tier 2 (40%), and Tier 3 (25%)

- By Designation: Directors (25%), Managers (50%), and Others (25%)

- By Region: North America (35%), Europe (30%), the Asia Pacific (15%), and the Rest of the World (20%)

The prominent players in the IV equipment market are Becton, Dickinson and Company (US), B. Braun SE (Germany), Fresenius SE & Co. KGaA (Germany), ICU Medical, Inc. (US), Terumo Corporation (Japan), Moog Inc. (US), Teleflex Incorporated (US), Cardinal Health (US), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), Baxter (US), Avanos Medical, Inc. (US), Nipro (Japan), JMS Co., Ltd. (Japan), Vygon (France), and Micrel Medical Devices SA (Greece), among others.

Research Coverage

This report analyzes the IV equipment market by type, application, end user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets by their individual growth trends and forecasts market segment revenues across five main regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

- Analysis of key drivers (rising disease burden and the subsequent surge in the geriatric population globally as well as the shift toward home and ambulatory infusion), restraints (product recalls and failures), opportunities (untapped growth potential in emerging markets), and challenges (vendor collaborations) influencing the growth of the IV equipment market.

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the IV equipment market.

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product developments in the IV equipment market.

- Market Development: Comprehensive information on lucrative emerging regions.

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the IV equipment market.

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS CONSIDERED & GEOGRAPHICAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN IV EQUIPMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 IV EQUIPMENT MARKET OVERVIEW

- 3.2 ASIA PACIFIC: IV EQUIPMENT MARKET, BY COUNTRY AND END USER

- 3.3 GEOGRAPHIC SNAPSHOT OF IV EQUIPMENT MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising disease burden and subsequent surge in geriatric population globally

- 4.2.1.2 Shift toward home and ambulatory infusion

- 4.2.1.3 Smart pumps, improved safety features, and precision infusion systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 Product recalls and failures

- 4.2.2.2 Infection and complication risk associated with IV therapy

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Untapped growth potential in emerging markets

- 4.2.3.2 Technological advancements and vendor collaborations

- 4.2.4 CHALLENGES

- 4.2.4.1 Device reliability, maintenance requirements, and user-related errors

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN IV EQUIPMENT MARKET

- 4.3.1.1 Interoperable & smart IV systems

- 4.3.1.2 Affordable, reliable equipment for emerging markets

- 4.3.1.3 Better infection-prevention designs

- 4.3.1.4 Home care & ambulatory-friendly IV devices

- 4.3.1.5 Streamlined regulatory pathways

- 4.3.1.6 Wider access & supply consistency

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Low-cost smart infusion pumps for emerging markets

- 4.3.2.2 Integrated IV ecosystem

- 4.3.2.3 Home infusion & ambulatory-first devices

- 4.3.2.4 Infection-prevention IV consumables

- 4.3.2.5 Disposable/Single-use smart components

- 4.3.1 UNMET NEEDS IN IV EQUIPMENT MARKET

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 MARKET ECOSYSTEM

- 5.5.1 ROLE IN ECOSYSTEM

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF IV EQUIPMENT, BY KEY PLAYER, 2023-2025 (USD)

- 5.6.2 AVERAGE SELLING PRICE TREND OF INFUSION PUMPS, BY REGION, 2023-2025 (USD)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA (HS CODE 901890)

- 5.7.2 EXPORT DATA (HS CODE 901890)

- 5.8 REIMBURSEMENT SCENARIO

- 5.9 KEY CONFERENCES & EVENTS, 2026-2027

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.11 INVESTMENT & FUNDING SCENARIO

- 5.12 CASE STUDY ANALYSIS

- 5.13 IMPACT OF 2025 US TARIFFS ON IV EQUIPMENT MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRY/REGION

- 5.13.5 IMPACT ON END-USE SEGMENTS

- 5.13.5.1 Hospitals

- 5.13.5.2 Outpatient infusion & specialty clinics

- 5.13.5.3 Ambulatory surgical centers (ASCs)

- 5.13.5.4 Home care settings

- 5.13.5.5 Other end users (long-term care facilities, emergency services, and specialty clinics)

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Smart infusion pumps

- 6.1.1.2 Closed-loop infusion control systems

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Dose-error reduction systems

- 6.1.2.2 Telemedicine & remote infusion monitoring

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Embedded software

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR TERM (2025-2027)

- 6.2.2 MID TERM (2028-2030)

- 6.2.3 LONG TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 REMOTE & HOME-BASED INFUSION THERAPY

- 6.4.2 CLOSED-LOOP IV THERAPY & AUTOMATED DOSING

- 6.4.3 AI-DRIVEN INFUSION SAFETY & PREDICTIVE QUALITY MANAGEMENT

- 6.5 IMPACT OF AI/GEN AI ON IV EQUIPMENT MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL OF AI IN IV EQUIPMENT

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.4 Latin America

- 7.1.1.5 Middle East & Africa

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RECYCLED AND ECO-FRIENDLY MATERIALS FOR IV EQUIPMENT

- 7.2.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 IV EQUIPMENT MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 IV CATHETERS

- 9.2.1 GROWING HOSPITAL ADMISSIONS AND VASCULAR ACCESS DEMAND TO DRIVE USE OF IV CATHETERS

- 9.3 INFUSION PUMPS

- 9.3.1 SHIFT TOWARD PRECISION MEDICINE AND DIGITAL SAFETY TO ACCELERATE SMART PUMP ADOPTION

- 9.4 IV ADMINISTRATION SETS & TUBING

- 9.4.1 HIGH-VOLUME THERAPY DEMAND AND SUPPLY CHAIN RESILIENCE TO DRIVE IV SET CONSUMPTION

- 9.5 SECUREMENT & STABILIZATION DEVICES

- 9.5.1 GROWING CLINICAL EMPHASIS ON LINE STABILITY AND INFECTION PREVENTION TO ELEVATE SECUREMENT DEMAND

- 9.6 NEEDLE-FREE CONNECTORS & EXTENSION SETS

- 9.6.1 NEEDLESTICK PREVENTION AND INFECTION CONTROL POLICIES TO EXPAND CONNECTOR ADOPTION

- 9.7 IV DRIP CHAMBERS

- 9.7.1 ESSENTIAL FLOW-CONTROL COMPONENTS TO SUPPORT HIGH-VOLUME GRAVITY INFUSIONS

- 9.8 OTHER IV EQUIPMENT

10 IV EQUIPMENT MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 MEDICATION ADMINISTRATION

- 10.2.1 ONCOLOGY (IV CHEMOTHERAPY)

- 10.2.1.1 Rising cancer burden to drive market growth

- 10.2.2 ANTIBIOTIC/ANTIMICROBIAL IV THERAPY

- 10.2.2.1 Prolonged antibiotic therapy to boost market growth

- 10.2.3 CRITICAL CARE & VASOACTIVE DRUG INFUSION

- 10.2.3.1 Demand for advanced IV pumps and compatible disposables to aid market growth

- 10.2.4 ANALGESIA/PAIN MANAGEMENT

- 10.2.4.1 Surge in chronic pain conditions to propel market growth

- 10.2.5 SEDATION & ANESTHESIA INFUSION

- 10.2.5.1 High procedural sedation demand to propel market growth

- 10.2.6 IMMUNOTHERAPY

- 10.2.6.1 Increasing use in immune-mediated conditions to support market growth

- 10.2.1 ONCOLOGY (IV CHEMOTHERAPY)

- 10.3 PARENTERAL NUTRITION (PN)

- 10.3.1 GASTROINTESTINAL DISORDERS

- 10.3.1.1 Rising GI disorders to support market growth

- 10.3.2 CRITICAL CARE NUTRITION

- 10.3.2.1 Increasing demand in ICU units to support market growth

- 10.3.3 NEONATAL & PEDIATRIC PARENTERAL NUTRITION

- 10.3.3.1 Increasing demand for neonatal lipid formulations to propel market growth

- 10.3.4 OTHER PARENTERAL NUTRITION APPLICATIONS

- 10.3.1 GASTROINTESTINAL DISORDERS

- 10.4 FLUID & ELECTROLYTE REPLACEMENT

- 10.4.1 GROWING DEMAND FOR FLUID AND REPLACEMENT THERAPY TO DRIVE MARKET GROWTH

- 10.5 BLOOD & BLOOD PRODUCTS TRANSFUSION

- 10.5.1 RED BLOOD CELL TRANSFUSION

- 10.5.1.1 Growing use in symptomatic anemia, acute blood loss, and perioperative blood replacement to support market growth

- 10.5.2 PLATELET TRANSFUSION

- 10.5.2.1 Growing use of standard blood administration sets to fuel growth

- 10.5.3 PLASMA TRANSFUSION

- 10.5.3.1 Wide usage in critical therapy for coagulation disorders to expand market

- 10.5.4 OTHER BLOOD & BLOOD PRODUCTS TRANSFUSION APPLICATIONS

- 10.5.1 RED BLOOD CELL TRANSFUSION

- 10.6 DIAGNOSTIC TESTING

- 10.6.1 INCREASING DEMAND FOR DIAGNOSTIC IMAGING PROCEDURES TO AID MARKET GROWTH

- 10.7 OTHER APPLICATIONS

11 IV EQUIPMENT MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HOSPITALS

- 11.2.1 HIGH DEMAND AND COMPLEX INFUSION WORKFLOWS TO SUSTAIN HOSPITAL DOMINANCE IN IV EQUIPMENT USE

- 11.3 AMBULATORY SURGICAL CENTERS

- 11.3.1 GROWING NUMBER OF SURGICAL PROCEDURES IN ASCS TO PROPEL MARKET GROWTH

- 11.4 OUTPATIENT INFUSION & SPECIALTY CLINICS

- 11.4.1 HIGH DEMAND FOR IV CONSUMABLES AND INFUSION PUMPS TO DRIVE MARKET GROWTH

- 11.5 HOME CARE SETTINGS

- 11.5.1 EXPANSION OF HOME INFUSION THERAPY TO CREATE NEW DEMAND FOR PORTABLE IV DEVICES AND CONSUMABLES

- 11.6 OTHER END USERS

12 IV EQUIPMENT MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 US to dominate North American IV equipment market

- 12.2.3 CANADA

- 12.2.3.1 Rising geriatric patient pool to drive market growth

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Increasing healthcare expenditure to drive market growth

- 12.3.3 UK

- 12.3.3.1 Rising adoption of advanced healthcare systems to support market growth

- 12.3.4 FRANCE

- 12.3.4.1 Rising digital expansion to propel market growth

- 12.3.5 ITALY

- 12.3.5.1 Rising elderly patient pool to drive market growth

- 12.3.6 SPAIN

- 12.3.6.1 Steady modernization of healthcare system in Spain to support market growth

- 12.3.7 NETHERLANDS

- 12.3.7.1 Strong healthcare infrastructure and aging population to drive market

- 12.3.8 DENMARK

- 12.3.8.1 Well-established healthcare infrastructure to boost market

- 12.3.9 SWEDEN

- 12.3.9.1 Rising healthcare expenditure to aid market growth

- 12.3.10 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 Government support and rising disease burden to drive market growth

- 12.4.3 JAPAN

- 12.4.3.1 High healthcare expenditure, favorable reimbursement, and insurance coverage to support market growth

- 12.4.4 INDIA

- 12.4.4.1 Government initiatives to propel market growth

- 12.4.5 SOUTH KOREA

- 12.4.5.1 Rising aging population to bolster market growth

- 12.4.6 AUSTRALIA

- 12.4.6.1 Rising hospitalization rates to aid market growth

- 12.4.7 PHILIPPINES

- 12.4.7.1 Government investment and public hospital modernization to fuel demand

- 12.4.8 MALAYSIA

- 12.4.8.1 Rising healthcare investment and technological advancements to drive market

- 12.4.9 VIETNAM

- 12.4.9.1 Growing aging population and healthcare infrastructure development to fuel market

- 12.4.10 SINGAPORE

- 12.4.10.1 Advanced healthcare infrastructure and technological integration to boost market

- 12.4.11 INDONESIA

- 12.4.11.1 Rising prevalence of chronic diseases to drive market

- 12.4.12 THAILAND

- 12.4.12.1 Rising geriatric population and chronic diseases to drive market

- 12.4.13 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Favorable government initiatives to propel market growth

- 12.5.3 MEXICO

- 12.5.3.1 Rising disease burden to aid market growth

- 12.5.4 ARGENTINA

- 12.5.4.1 Rapid aging population and subsequent rise in chronic diseases to boost market

- 12.5.5 COLOMBIA

- 12.5.5.1 Integration of technological advancements in hospitals & infusion therapy settings to propel market

- 12.5.6 CHILE

- 12.5.6.1 Growing focus on local infusion-therapy product manufacturers to fuel uptake

- 12.5.7 ECUADOR

- 12.5.7.1 Digital health initiatives to support market growth

- 12.5.8 PERU

- 12.5.8.1 Increasing focus on oncology therapeutics to boost market

- 12.5.9 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Kingdom of Saudi Arabia (KSA)

- 12.6.2.1.1 Favorable government initiatives to boost growth

- 12.6.2.2 United Arab Emirates (UAE)

- 12.6.2.2.1 Government strategies to drive market in UAE

- 12.6.2.3 Rest of GCC countries

- 12.6.2.1 Kingdom of Saudi Arabia (KSA)

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS

- 13.3 REVENUE ANALYSIS, 2023-2025

- 13.4 GLOBAL MARKET SHARE ANALYSIS, 2025

- 13.4.1 US MARKET SHARE ANALYSIS, 2025

- 13.4.2 EUROPE MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Type footprint

- 13.5.5.4 Application footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SME players

- 13.7 COMPANY VALUATION & FINANCIAL METRICS

- 13.7.1 FINANCIAL METRICS

- 13.7.2 COMPANY VALUATION

- 13.8 BRAND/PRODUCT COMPARISON

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BECTON, DICKINSON AND COMPANY

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product approvals

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.3.4 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 B. BRAUN SE

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches & approvals

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 BAXTER

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product approvals

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 FRESENIUS SE & CO. KGAA

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product approvals

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses & competitive threats

- 14.1.5 ICU MEDICAL, INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product approvals

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 TERUMO CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.3.2 Expansions

- 14.1.7 MOOG, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.2.1 Product approvals

- 14.1.8 TELEFLEX INCORPORATED

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.9 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches

- 14.1.9.3.2 Other developments

- 14.1.10 CARDINAL HEALTH

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Expansions

- 14.1.11 AVANOS MEDICAL, INC.

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.12 NIPRO

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Expansions

- 14.1.13 JMS CO., LTD.

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.14 VYGON

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Deals

- 14.1.15 MICREL MEDICAL DEVICES SA

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Deals

- 14.1.1 BECTON, DICKINSON AND COMPANY

- 14.2 OTHER PLAYERS

- 14.2.1 ARCOMED

- 14.2.2 HINDUSTAN SYRINGES & MEDICAL DEVICES LTD.

- 14.2.3 EITAN MEDICAL

- 14.2.4 ANGIPLAST PRIVATE LIMITED

- 14.2.5 PRIMEGUARD MEDICAL

- 14.2.6 IRADIMED CORPORATION

- 14.2.7 EPIC MEDICAL

- 14.2.8 ROMSONS

- 14.2.9 BEIJING KELLYMED CO., LTD.

- 14.2.10 INTUVIE HOLDINGS LLC

- 14.2.11 PROMED TECHNOLOGY CO., LIMITED

- 14.2.12 MEDCAPTAIN MEDICAL TECHNOLOGY CO., LTD.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH APPROACH

- 15.2 RESEARCH METHODOLOGY DESIGN

- 15.2.1 SECONDARY RESEARCH

- 15.2.1.1 Key data from secondary sources

- 15.2.2 PRIMARY DATA

- 15.2.2.1 Key industry insights

- 15.2.1 SECONDARY RESEARCH

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 BOTTOM-UP APPROACH

- 15.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 15.5 MARKET SHARE ESTIMATION

- 15.6 ASSUMPTIONS

- 15.6.1 GROWTH RATE ASSUMPTIONS

- 15.7 RISK ASSESSMENT

- 15.8 LIMITATIONS

- 15.8.1 METHODOLOGY-RELATED LIMITATIONS

- 15.8.2 SCOPE-RELATED LIMITATIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.3.1 COMPANY INFORMATION

- 16.3.2 GEOGRAPHIC ANALYSIS

- 16.3.3 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 16.3.4 COUNTRY-LEVEL VOLUME ANALYSIS

- 16.3.5 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS