|

시장보고서

상품코드

1961005

우주 상황 인식 시장 예측(-2030년) : 솔루션별, 물체 유형별, 궤도 유형별, 능력별, 최종사용자별, 지역별Space Situational Awareness Market by Capability (Observation & Detection, Orbit Determination, Object Data Management, Event Detection, Re-entry Assessment, Risk Prediction), Solution, Object Type, End User, and Region - Global Forecast to 2030 |

||||||

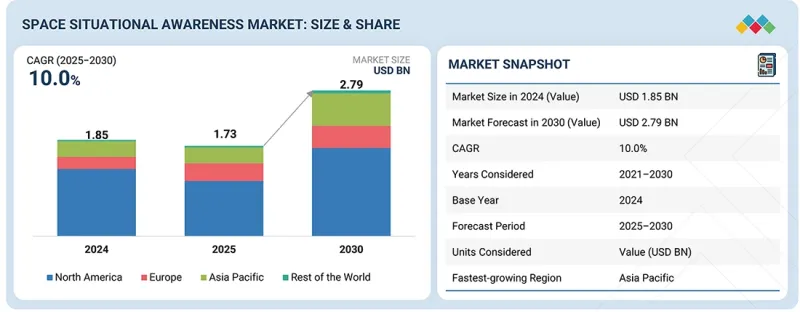

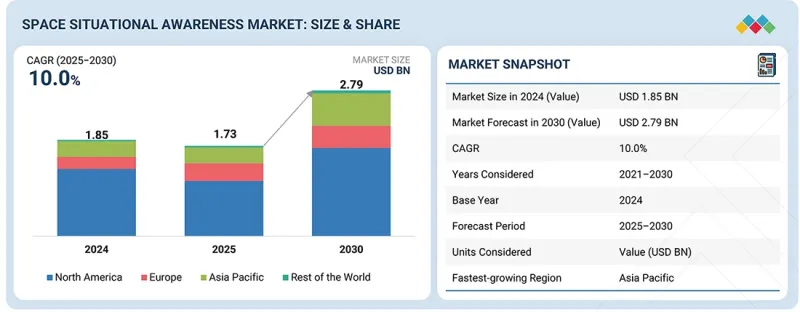

우주 상황 인식 시장 규모는 2025년 17억 3,000만 달러에서 2031년까지 27억 9,000만 달러로, CAGR 10.0%로 성장할 것으로 예측되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 솔루션별, 물체 유형별, 궤도 유형별, 능력별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

우주 상황 인식 시장은 위성 운영 사업자들이 혼잡한 궤도에서 계획되지 않은 궤도 변경, 신호 간섭, 자산 손실로 인한 재정적 및 서비스 위험 증가에 직면하면서 성장하고 있습니다. 미션 가동 시간을 보호하고 고가의 위성 교체를 피하는 것이 핵심 운영 우선순위가 되고 있습니다.

우주가 중요한 작전 영역으로 인식되고 있는 가운데, 정부 및 방위 부문은 예측 기간 중 가장 두드러진 성장을 보일 것으로 예측됩니다. 군사 조직은 감시, 조기경보, 항법, 보안 통신에 필수적인 전략 위성을 보호하기 위해 우주 상황 인식(SSA)에 의존하고 있습니다. 대우주 능력, 적대적 작전, 우주 기반 위협에 대한 우려가 높아지면서 SSA에 대한 지속적인 국방 투자가 촉진되고 있습니다.

페이로드 시스템 부문은 가장 높은 CAGR로 성장하고 그 우위를 유지할 것으로 예측됩니다. 이는 SSA 기능이 인공위성이나 우주선에 직접 통합되기 때문입니다. 운영자들은 이제 지상 데이터에만 의존하지 않고, 탑재형 센싱, 추적, 자율 기동 지원을 선호하고 있습니다. 이러한 변화를 통해 충돌 위험과 신호 간섭에 대한 신속한 대응이 가능해집니다.

북미는 2030년까지 우주 상황 인식 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이는 이 지역에 방위기관, 상업용 위성 사업자, 우주 상황 인식(SSA) 기술 프로바이더가 다수 존재하기 때문입니다. 북미는 우주 감시를 위한 최첨단 레이더 및 광학 센서 네트워크를 보유하고 있습니다. 대규모 위성 별자리 관측에 대한 강력한 공공 자금과 민간 투자의 조합은 SSA에 대한 높은 수요를 지속적으로 견인하고 있습니다.

조사 범위:

이 시장 조사는 다양한 부문 및 하위 부문에 걸친 우주 상황 인식 시장을 대상으로 합니다. 이 보고서는 다양한 지역과 분야에서 시장 규모와 성장 가능성을 추정하는 것을 목표로 하고 있습니다. 또한 시장내 주요 업체들의 상세한 경쟁 분석, 기업 개요, 제품 및 비즈니스 제공 제품에 대한 주요 관찰 사항, 최근 동향, 주요 시장 전략에 대한 분석도 포함되어 있습니다.

이 보고서 구매 이유:

이 보고서는 시장 리더와 신규 진출기업에게 우주 상황 인식 시장 전체 매출에 대한 가장 정확한 예측치를 제공합니다. 또한 이해관계자들이 경쟁 구도를 이해하고, 사업 포지셔닝을 강화하거나 적절한 시장 진출 전략을 수립하는 데 도움이 되는 심층 인사이트을 얻을 수 있도록 지원합니다. 또한 시장 동향을 파악하고 주요 시장 성장 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

- 시장 성장 촉진요인(위성 별자리 급성장 및 궤도 혼잡), 제약 요인(위성 별자리 급성장 및 궤도 혼잡, 세계 표준화 및 데이터 상호운용성 부족), 기회(상용 SSA-as-a-service 모델 확대, 궤도상 서비스, 근접 운용, 우주 쓰레기 제거 임무의 성장), 과제(궤도 환경의 복잡성, 오경보 관리 및 의사결정의 불확실성) 성장), 과제(궤도 환경의 복잡성, 오경보 관리 및 의사결정의 불확실성)

- 시장 침투: 시장을 선도하는 주요 기업별 우주 상황 인식(SSA)에 대한 종합 정보

- 제품 개발/혁신 : 우주 상황 인식 시장의 향후 기술 동향, 연구개발 활동, 제품 출시에 대한 심층 분석

- 시장 개발: 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화 : 우주 상황 인식 시장의 신제품, 미개발 지역, 최근 동향, 투자에 관한 종합적인 정보

- 경쟁사 평가: 우주 상황 인식 시장내 주요 기업의 시장 점유율, 성장 전략, 제품, 제조 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성에 관한 구상

제8장 고객 상황과 구매 행동

제9장 우주 상황 인식 시장(솔루션별)

제10장 우주 상황 인식 시장(물체 유형별)

제11장 우주 상황 인식 시장(궤도 유형별)

제12장 우주 상황 인식 시장(능력별)

제13장 우주 상황 인식 시장(최종사용자별)

제14장 우주 상황 인식 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.03.20The space situational awareness market is projected to grow from USD 1.73 billion in 2025 to USD 2.79 billion by 2031, at a CAGR of 10.0%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Capability, Solution, Object Type, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

The space situational awareness market is growing as satellite operators face rising financial and service risks from unplanned maneuvers, signal interference, and asset loss in congested orbits. Protecting mission uptime and avoiding costly satellite replacements is becoming a core operational priority.

"By end-user, the government & defense segment is projected to account for the largest market share during the forecast period."

The government & defense segment is expected to be the most prominent during the forecast period, as space is increasingly recognized as a critical operational domain. Military organizations depend on space situational awareness (SSA) to safeguard strategic satellites essential for surveillance, early warning, navigation, and secure communications. Growing concerns about counter-space capabilities, hostile maneuvers, and space-based threats are driving sustained defense investments in SSA.

"By solution, the payload systems segment is expected to grow at the highest CAGR during the forecast period."

The payload systems segment is projected to grow at the highest CAGR and maintain its dominance. This is due to the integration of SSA capabilities directly into satellites and spacecraft. Operators now prefer onboard sensing, tracking, and autonomous maneuver support instead of relying solely on ground-based data. This shift allows for a quicker response to collision risks and signal interference.

"North America is projected to account for the largest market share during the forecast period."

North America is projected to account for the largest share of the space situational awareness market through 2030. This is due to the significant presence of defense agencies, commercial satellite operators, and space situational awareness (SSA) technology providers in the region. North America boasts some of the most advanced radar and optical sensor networks for space monitoring. The combination of strong public funding and private investment in large satellite constellations continues to drive high demand for SSA.

The breakdown of profiles for primary participants in the space situational awareness market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: Directors - 20%, Managers - 10%, and Others - 70%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 20%, Middle East - 10%, and the Rest of the World (RoW) - 10%

Research Coverage:

This market study covers the space situational awareness market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations on their products and business offerings, recent developments, and the key market strategies they have adopted.

Reasons to buy this report:

The report will help market leaders/new entrants with information on the closest approximations of revenue for the overall space situational awareness market. It will also help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (rapid growth of satellite constellations and orbital congestion, rapid growth of satellite constellations and orbital congestion), restraints (rapid growth of satellite constellations and orbital congestion, limited global standardization and data interoperability), opportunities (expansion of commercial SSA-as-a-service models, growth of in-orbit servicing, proximity operations, and debris removal missions), challenges (increasing complexity of the orbital environment, managing false alerts and decision uncertainty)

- Market Penetration: Comprehensive information on space situational awareness offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the space situational awareness market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the space situational awareness market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the space situational awareness market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

- 2.5 BUSINESS MODELS

- 2.5.1 SUBSCRIPTION MODEL

- 2.5.2 DATA LICENSING MODEL

- 2.5.3 ANALYTICS AND SOFTWARE LICENSING MODEL

- 2.5.4 MANAGED SERVICES MODEL

- 2.5.5 CONSTELLATION-BASED SENSOR NETWORK MODEL

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SPACE SITUATIONAL AWARENESS MARKET

- 3.2 SPACE SITUATIONAL AWARENESS MARKET, BY SOLUTION

- 3.3 SPACE SITUATIONAL AWARENESS MARKET, BY OBJECT TYPE

- 3.4 SPACE SITUATIONAL AWARENESS MARKET, BY END USER

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid expansion of satellite constellations

- 4.2.1.2 Regulatory focus on space safety and debris mitigation

- 4.2.1.3 Advancements in sensor technology and analytics for improving space situational awareness accuracy and commercial viability

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital intensity of space situational awareness infrastructure

- 4.2.2.2 Lack of global standardization and data interoperability

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Shift toward commercial space situational awareness-as-a-service models

- 4.2.3.2 Emergence of in-orbit servicing, proximity operations, and debris removal missions

- 4.2.4 CHALLENGES

- 4.2.4.1 Increasing complexity of orbital environment

- 4.2.4.2 Managing false alerts and decision uncertainty

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL SPACE SECTOR

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 SYSTEM INTEGRATORS AND PRIME SPACE SITUATIONAL AWARENESS SOLUTION PROVIDERS

- 5.4.2 SENSOR, HARDWARE, AND SPACE DOMAIN DATA PROVIDERS

- 5.4.3 ANALYTICS, SOFTWARE, AND SPACE SITUATIONAL AWARENESS SERVICE SPECIALISTS

- 5.5 TRADE DATA

- 5.5.1 IMPORT SCENARIO (HS CODE 880260)

- 5.5.2 EXPORT SCENARIO (HS CODE 880260)

- 5.6 KEY CONFERENCES AND EVENTS

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 PRICING ANALYSIS

- 5.9.1 INDICATIVE PRICING ANALYSIS, BY SOLUTION

- 5.9.2 INDICATIVE PRICING ANALYSIS, BY REGION

- 5.10 USE CASE ANALYSIS

- 5.10.1 COLLISION AVOIDANCE AND CONJUNCTION ASSESSMENT FOR OPERATIONAL SATELLITES

- 5.10.2 SPACE DEBRIS MONITORING AND ORBITAL ENVIRONMENT ASSESSMENT

- 5.10.3 COMMERCIAL SPACE SITUATIONAL AWARENESS SERVICES FOR LARGE SATELLITE CONSTELLATIONS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SPACE-BASED SITUATIONAL AWARENESS SENSORS AND HYBRID SENSING ARCHITECTURE

- 6.1.2 HIGH-PRECISION LASER RANGING AND NEXT-GENERATION OPTICAL TRACKING TECHNOLOGIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 GROUND-BASED RADAR AND OPTICAL SENSOR TECHNOLOGIES

- 6.2.2 CLOUD COMPUTING AND SECURE DATA INFRASTRUCTURE

- 6.3 TECHNOLOGY ROADMAP

- 6.4 EMERGING TECHNOLOGY TRENDS

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GEN AI

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 LEOLABS: SCALING COMMERCIAL SPACE SITUATIONAL AWARENESS THROUGH PROPRIETARY GLOBAL RADAR INFRASTRUCTURE

- 6.8.2 COMSPOC CORPORATION: ENABLING OPERATIONAL SPACE SITUATIONAL AWARENESS THROUGH ADVANCED ANALYTICS AND DECISION SUPPORT PLATFORMS

- 6.8.3 LOCKHEED MARTIN CORPORATION: INTEGRATING SPACE SITUATIONAL AWARENESS INTO NATIONAL SPACE SECURITY AND SPACE DOMAIN AWARENESS ARCHITECTURES

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

9 SPACE SITUATIONAL AWARENESS MARKET, BY SOLUTION

- 9.1 INTRODUCTION

- 9.2 CLASSIFICATION OF SPACE SITUATIONAL AWARENESS SOLUTIONS BY DEPLOYMENT

- 9.2.1 CLOUD-BASED

- 9.2.2 ON-PREMISES

- 9.2.3 HYBRID

- 9.3 PAYLOAD SYSTEMS

- 9.3.1 DEMAND FOR HIGH-ACCURACY SENSING INFRASTRUCTURE TO MONITOR CONGESTED ORBITAL ENVIRONMENT

- 9.3.2 GROUND-BASED SYSTEMS

- 9.3.2.1 Radars

- 9.3.2.2 Electro-optic sensors

- 9.3.3 SPACE-BASED SENSORS

- 9.3.4 DATALINKS & NETWORK INFRASTRUCTURE

- 9.3.4.1 Ground-to-space datalinks

- 9.3.4.2 Space-to-ground datalinks

- 9.3.4.3 Inter-satellite datalinks

- 9.4 SOFTWARE

- 9.4.1 NEED FOR REAL-TIME ANALYTICS AND AUTOMATED DECISION SUPPORT TO MANAGE OPERATIONAL COMPLEXITY

- 9.4.2 ORBIT DETERMINATION, PROPAGATION, & CATALOG MANAGEMENT SOFTWARE

- 9.4.3 CONJUNCTION ASSESSMENT & COLLISION AVOIDANCE SOFTWARE

- 9.4.4 RE-ENTRY PREDICTION & RISK MODELING SOFTWARE

- 9.4.5 FRAGMENTATION/BREAKUP EVENT ANALYTICS SOFTWARE

- 9.4.6 SPACE OBJECT CHARACTERIZATION & IDENTIFICATION SOFTWARE

- 9.4.7 VISUALIZATION, WORKFLOW AUTOMATION, & INTEGRATION PLATFORMS

- 9.5 SERVICES

- 9.5.1 GROWING RELIANCE ON CONTINUOUS, SUBSCRIPTION-BASED SPACE SITUATIONAL AWARENESS

- 9.5.2 SPACE WEATHER SERVICES

- 9.5.2.1 Space weather forecasts & warnings

- 9.5.2.2 Space weather impact advisory

- 9.5.3 SPACE SURVEILLANCE & TRACKING

- 9.5.3.1 Launch & early orbit phase

- 9.5.3.2 Conjunction assessment

- 9.5.3.3 Fragmentation & breakup analysis

- 9.5.3.4 Deorbit

- 9.5.3.5 Collision avoidance & mitigation

- 9.5.3.6 Precision tracking

- 9.5.4 NEAR-EARTH OBJECT DETECTION

- 9.5.4.1 Survey & detection

- 9.5.4.2 Orbit determination & impact probability

- 9.5.4.3 Orbit & observation data

10 SPACE SITUATIONAL AWARENESS MARKET, BY OBJECT TYPE

- 10.1 INTRODUCTION

- 10.2 PAYLOADS

- 10.2.1 EXPANSION OF OPERATIONAL SATELLITE FLEETS

- 10.2.2 ACTIVE PAYLOADS

- 10.2.3 INACTIVE PAYLOADS

- 10.3 UNCATEGORIZED OBJECTS

- 10.3.1 NEED FOR RAPID IDENTIFICATION OF NEWLY DETECTED OR AMBIGUOUS SPACE OBJECTS

- 10.4 ROCKET BODIES

- 10.4.1 DEMAND FOR CONJUNCTION ASSESSMENT AND FRAGMENTATION MONITORING

- 10.5 DEBRIS

- 10.5.1 ACCELERATING DEBRIS ACCUMULATION THREATENING SUSTAINABLE SPACE OPERATIONS

11 SPACE SITUATIONAL AWARENESS MARKET, BY ORBIT TYPE

- 11.1 INTRODUCTION

- 11.2 NEAR-EARTH ORBIT

- 11.2.1 INCLINATION TOWARD REAL-TIME TRACKING AMID GROWING SATELLITE DEPLOYMENTS

- 11.2.2 LOW EARTH ORBIT

- 11.2.3 MEDIUM EARTH ORBIT

- 11.2.4 GEOSTATIONARY EARTH ORBIT

- 11.3 DEEP SPACE/BEYOND GEOSTATIONARY EARTH ORBIT

- 11.3.1 EMERGING NEED FOR ADVANCED DEEP SPACE TRACKING AND ANOMALY DETECTION CAPABILITIES

12 SPACE SITUATIONAL AWARENESS MARKET, BY CAPABILITY

- 12.1 INTRODUCTION

- 12.2 OBSERVATION & DETECTION

- 12.2.1 HIGH DEMAND FOR EARLY DETECTION DUE TO EXPANDING DEBRIS POPULATIONS

- 12.3 TRACKING, ORBIT DETERMINATION, & CUSTODY

- 12.3.1 EMPHASIS ON PREVENTING COLLISION RISKS ARISING FROM CONGESTED ORBITS

- 12.4 CATALOG & OBJECT DATA MANAGEMENT

- 12.4.1 SHARP RISE IN TRACKED OBJECTS AND CONSUMER PREFERENCE FOR DATA TRACEABILITY

- 12.5 EVENT DETECTION & CHARACTERIZATION

- 12.5.1 NEED FOR QUICK RESPONSES TO HIGH-IMPACT EVENTS

- 12.6 RE-ENTRY ASSESSMENT

- 12.6.1 SURGE IN RE-ENTRY RISK EVALUATION DUE TO INCREASING SATELLITE RETIREMENTS

- 12.7 RISK PREDICTION & THREAT ASSESSMENT

- 12.7.1 OPERATIONAL AND SECURITY CONCERNS ELEVATING PREDICTIVE SPACE SITUATIONAL AWARENESS CAPABILITIES

13 SPACE SITUATIONAL AWARENESS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 COMMERCIAL

- 13.2.1 RAPID EXPANSION OF SATELLITE CONSTELLATIONS DUE TO INCREASED COLLISION RISK

- 13.2.2 SATELLITE OPERATORS/OWNERS

- 13.2.3 LAUNCH SERVICE PROVIDERS

- 13.2.4 SPACE INSURANCE COMPANIES

- 13.2.5 OTHER COMMERCIAL END USERS

- 13.3 GOVERNMENT & DEFENSE

- 13.3.1 FOCUS ON STRENGTHENING SOVEREIGN SPACE MONITORING AND INTEGRATED THREAT RESPONSE CAPABILITIES IN CONTESTED ORBITS

- 13.3.2 DEPARTMENTS OF DEFENSE

- 13.3.3 INTELLIGENCE/NATIONAL SECURITY AGENCIES

- 13.3.4 SPACE AGENCIES

- 13.3.5 CIVIL MINISTRIES/PUBLIC SAFETY AUTHORITIES

- 13.3.6 ACADEMIC & RESEARCH INSTITUTIONS

14 SPACE SITUATIONAL AWARENESS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 National security-driven scaling of operational space situational awareness to drive market

- 14.2.2 CANADA

- 14.2.2.1 Government initiatives for space technology development to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Defense operationalization of space and sovereign capability development to drive market

- 14.3.2 GERMANY

- 14.3.2.1 Rise of security programs and resilience-oriented space policy to drive market

- 14.3.3 FRANCE

- 14.3.3.1 Sovereign surveillance and geostationary asset protection to drive market

- 14.3.4 ITALY

- 14.3.4.1 Secure government missions and operational continuity need to drive market

- 14.3.5 RUSSIA

- 14.3.5.1 Defense and national security considerations to drive market

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Expanding government and commercial space activity to drive market

- 14.4.2 INDIA

- 14.4.2.1 Rapid commercialization of space to drive market

- 14.4.3 JAPAN

- 14.4.3.1 Defense-led space domain awareness and proximity operations to drive market

- 14.4.4 AUSTRALIA

- 14.4.4.1 Geographic advantage for space surveillance to drive market

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Growth in satellite activity and high security concerns to drive market

- 14.4.1 CHINA

- 14.5 REST OF THE WORLD

- 14.5.1 MIDDLE EAST

- 14.5.1.1 Emphasis on mission assurance, space security, and international cooperation to drive market

- 14.5.2 LATIN AMERICA & AFRICA

- 14.5.2.1 Rise of national space programs and reliance on international space situational awareness services to drive market

- 14.5.1 MIDDLE EAST

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 15.3 REVENUE ANALYSIS, 2021-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Solution footprint

- 15.5.5.4 Capability footprint

- 15.5.5.5 End user footprint

- 15.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING

- 15.6.5.1 List of start-ups/SMEs

- 15.6.5.2 Competitive benchmarking of start-ups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 15.9.2 DEALS

- 15.9.3 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 LOCKHEED MARTIN CORPORATION

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches/developments

- 16.1.1.3.2 Other developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 L3HARRIS TECHNOLOGIES, INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/developments

- 16.1.2.3.2 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 PARSONS CORPORATION

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 AIRBUS

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 RTX

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 PERATON

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Other developments

- 16.1.7 KRATOS DEFENSE & SECURITY SOLUTIONS, INC.

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Expansions

- 16.1.7.3.3 Other developments

- 16.1.8 GMV INNOVATING SOLUTIONS S.L.

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Other developments

- 16.1.9 QINETIQ

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Other developments

- 16.1.10 HENSOLDT AG

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.11 LEOLABS

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.11.3.2 Other developments

- 16.1.12 EXOANALYTIC SOLUTIONS

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches/developments

- 16.1.12.3.2 Deals

- 16.1.13 SLINGSHOT AEROSPACE

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Product launches/developments

- 16.1.13.3.2 Deals

- 16.1.13.3.3 Other developments

- 16.1.14 COMSPOC CORPORATION

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.15 AGI

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.1 LOCKHEED MARTIN CORPORATION

- 16.2 OTHER PLAYERS

- 16.2.1 VISION ENGINEERING SOLUTIONS, LLC

- 16.2.2 TELESPAZIO S.P.A.

- 16.2.3 GLOBVISION

- 16.2.4 SPACENAV, LLC

- 16.2.5 KAYHAN SPACE CORP

- 16.2.6 NORTHSTAR EARTH & SPACE INC.

- 16.2.7 ANDURIL INDUSTRIES

- 16.2.8 PRIVATEER SPACE

- 16.2.9 ELECNOR DEIMOS

- 16.2.10 ASTROSCALE

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Primary sources

- 17.1.2.2 Key data from primary sources

- 17.1.2.3 Breakdown of primary interviews

- 17.1.1 SECONDARY DATA

- 17.2 FACTOR ANALYSIS

- 17.2.1 DEMAND-SIDE INDICATORS

- 17.2.2 SUPPLY-SIDE INDICATORS

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.1.1 Market size estimation methodology (demand side)

- 17.3.2 TOP-DOWN APPROACH

- 17.3.1 BOTTOM-UP APPROACH

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS