|

시장보고서

상품코드

1979421

화학 발광 면역분석법 시장(-2031년) : 제품 유형(장비, 소모품), 기술(CLEIA, ECLI, 미립자 CLIA), 검체(혈액, 타액), 용도(종양, 심장병), 최종사용자(병원, 임상실험실)Chemiluminescence Immunoassay Market by Product (Instruments, Consumables), Technology (CLEIA, ECLI, Microparticle CLIA), Sample Type (Blood, Saliva), Application (Oncology, Cardiology), End User (Hospital, Clinical Laboratory) - Global Forecast to 2031 |

||||||

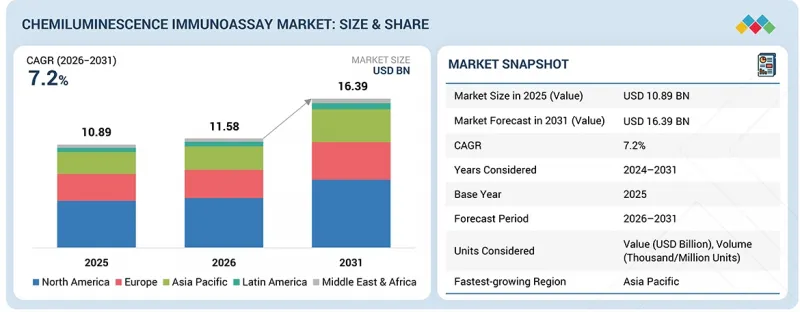

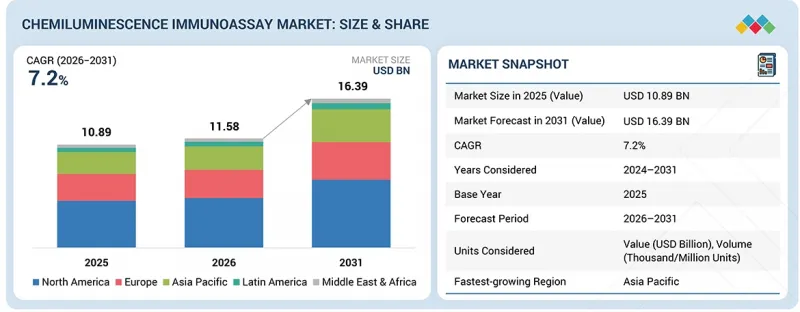

화학 발광 면역분석법 시장 규모는 2026년 115억 8,000만 달러에서 2031년에는 163억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.2%로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품 유형, 기술, 샘플 유형, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중남미, 중동 및 아프리카 |

CLIA 검사 시스템 세계 시장은 암, 심혈관 질환, 갑상선 질환, 바이러스 감염 등 만성질환 및 감염성 질환을 확인하기 위한 정확한 진단 검사에 대한 수요가 증가함에 따라 지속적으로 성장하고 있습니다. 질병의 조기발견에 대한 요구가 높아지고 예방의학적 접근이 확산됨에 따라, 우수한 민감도와 넓은 검사 범위, 미량의 바이오마커까지 검출할 수 있는 CLIA 검사의 활용이 확대되고 있습니다. 자동화된 고처리량 검사 시스템 개발, 보다 안정적인 검사 재료, 여러 검사를 동시에 수행할 수 있는 능력으로 검사 시간을 단축하고 검사실의 생산성을 향상시켰습니다. 시장 성장은 신흥 시장의 의료시설 개선, 검사실 시스템 확충, 의료비 증가에 의해 촉진되고 있습니다. 또한, 개인 맞춤형 의료, 의약품 개발, 임상연구에서 바이오마커 검사의 중요성이 높아지고 있으며, 엄격한 혈액검사 규제와 건강검진에 대한 인식이 높아짐에 따라 전 세계 병원 및 검사기관에서 CLIA 시스템에 대한 수요가 증가하고 있습니다.

"제품별로는 소모품 부문이 가장 높은 CAGR로 성장할 것으로 예측됩니다."

소모품 부문의 성장 배경에는 진단검사에서 검사실이 하루 업무 중 시약, 교정기, 대조군, 반응용기를 여러 번 사용해야 한다는 점이 있습니다. 감염 검사, 종양 마커 검사, 심장 바이오마커 검사, 내분비 장애 검사, 치료제물 모니터링 검사의 실시 빈도가 증가함에 따라 병원 및 기준 검사실에서 일상적으로 사용하는 분석 키트 및 시약 팩에 대한 수요가 증가하고 있습니다. 소모품은 분석 장비와 달리 지속적인 교체가 필요하기 때문에 지속적인 수익을 창출하며 시장 성장을 견인합니다. 시약의 안정성을 높이는 신기술 도입, 즉시 사용 가능한 제품 개발, 유통기한 연장 기술은 검사실 워크플로우의 업무 효율성 향상과 재료 폐기물의 감소로 이어집니다. 자동화된 고처리량 CLIA 시스템의 확대와 더불어 예방적 건강검진 프로그램 증가, 혈액 안전 검사 강화, 검사 메뉴의 확대가 소모품 소비를 증가시키고 있으며, 이 분야가 전체 CLIA 시장 확대를 주도하는 주요 요인으로 작용하고 있습니다.

"용도별로는 종양 부문이 가장 높은 CAGR로 성장할 것으로 예측됩니다."

종양 부문의 성장은 전 세계적으로 암 환자가 증가하고 있으며, 조기 진단, 예후 평가, 치료 효과 평가에 대한 수요가 증가하고 있는 것이 주요 요인으로 작용하고 있습니다. CLIA 기술은 PSA, CA-125, CEA, AFP, HER2 등의 종양표지자를 고감도, 고특이적으로 검출할 수 있어 환자의 초기 평가 및 병상 경과 관찰을 위한 진단 도구로 활용되고 있습니다. 바이오마커 기반 검사 및 정밀 종양학 실습이 증가함에 따라 표적 치료 및 개인 맞춤형 치료 옵션 결정을 지원하는 신뢰할 수 있는 면역 측정법의 필요성이 대두되고 있습니다. CLIA 검사의 임상적 활용이 확대되고 있는 배경에는 의사가 환자의 치료 반응을 모니터링하고, 암 재발을 확인하며, 암 발생 위험이 높은 환자를 평가하는 데 유용하다는 점이 있습니다. 자동화 프로세스 및 다중 검사 기능을 통해 검사 민감도를 향상시키는 우수한 분석 시스템의 도입은 암 진단 프로세스에서 CLIA 시스템의 채택을 더욱 촉진할 것입니다.

"최종 사용자별로는 병원 부문이 가장 높은 CAGR로 성장할 것으로 예측됩니다."

병원에서는 심근표지자, 패혈증 지표, 암 바이오마커, 호르몬 수치, 감염성 병원체 등 다양한 병태에 대한 정확한 검사를 시행해야 합니다. CLIA 시스템은 높은 민감도, 광범위한 검사 능력, 신속한 결과 제공으로 응급실, 중환자실, 입원 서비스가 지체 없이 치료를 시작할 수 있도록 지원합니다. 중앙 집중식 진단 시스템으로의 전환과 자동 진단 장비의 도입은 표준화된 프로세스를 통해 업무 효율성을 향상시키는 동시에 병원의 수작업을 줄이는 데 도움이 됩니다. 병원 시설의 확장, 예방 의료 검진 프로그램의 보급, 인증 기준 및 품질 기준의 강화, 종합적인 검사 정보 시스템의 필요성이 증가함에 따라 병원 시스템에서 CLIA 분석기 및 검사 키트의 세계 도입이 가속화되고 있습니다.

"아시아태평양이 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다."

아시아태평양의 CLIA 시장은 의료 확대, 의료비 증가, 중국, 인도, 동남아시아 국가들의 진단 서비스 보급 확대라는 세 가지 요인에 의해 성장하고 있습니다. 만성질환, 감염성 질환, 생활습관병이 증가함에 따라 정밀한 조기 진단 검사의 필요성이 높아지고 있습니다. 병원 현대화, 검사실 자동화, 국가 검진 프로그램 구축 등 정부 주도의 현대화 프로젝트가 고처리량 CLIA 시스템 도입을 가속화하고 있습니다. 예방의료에 대한 국민 인식 개선, 민간 진단검사 네트워크 확대, 의료관광 증가 등 세 가지 요인으로 인해 첨단 면역측정기술에 대한 수요가 증가하고 있습니다. 또한, 대규모 환자 기반, 보험 접근성 개선, 고부하 검사를 관리하는 자동화 검사 시스템으로 시장 전환이 이 시장의 지역적 성장을 가속하고 있습니다. 또한, 아시아태평양 전체에서 CLIA 플랫폼의 광범위한 도입은 국제적인 진단 기업의 지속적인 확장과 저렴한 가격의 국내 제조업체의 부상으로 인해 촉진되고 있습니다.

세계의 화학발광 면역분석(Chemiluminescent Immunoassay) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 화학 발광 면역분석법 시장 : 제품 유형별

제10장 화학 발광 면역분석법 시장 : 기술별

제11장 화학 발광 면역분석법 시장 : 검체별

제12장 화학 발광 면역분석법 시장 : 용도별

제13장 화학 발광 면역분석법 시장 : 최종사용자별

제14장 화학 발광 면역분석법 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSH 26.04.08The chemiluminescence immunoassay market is projected to reach USD 16.39 billion by 2031 from USD 11.58 billion in 2026, at a CAGR of 7.2% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product type, technology, sample type, application, end user, and region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The global market for CLIA testing systems is growing as people need accurate diagnostic tests to identify chronic and infectious diseases, including cancer, cardiovascular disorders, thyroid diseases, and viral infections. The increasing need for early disease detection, together with preventive healthcare approaches, leads to greater use of CLIA testing because it provides excellent sensitivity and a wide testing range and can identify trace amounts of biomarkers. The development of automated high-throughput testing systems, together with more stable testing materials and the ability to conduct multiple tests simultaneously, has improved laboratory productivity while decreasing testing duration. The market growth benefits from improved healthcare facilities, expanded testing laboratory systems, and increased medical expenditures that emerging markets are experiencing. The rising importance of biomarker testing for personalized medicine, drug development, and clinical research, together with strict blood screening regulations and health checkup awareness, boosts the need for CLIA systems in hospitals and reference laboratories throughout the world.

"Based on the product, the consumables segment is expected to grow at the highest CAGR in the CLIA market."

The consumables segment of the CLIA market is growing because diagnostic testing requires laboratories to use reagents, calibrators, controls, and reaction vessels multiple times throughout their workday. Assay kits and reagent packs that hospitals and reference laboratories use daily see increased demand because infectious disease tests, oncology marker tests, cardiac biomarker tests, endocrine disorder tests, and therapeutic drug monitoring tests are being performed more frequently. Consumables require continuous replacement, which generates ongoing revenue while driving market growth, in contrast to analyzers. The adoption of new technologies that enhance reagent stability and ready-to-use product development and extended shelf-life capabilities leads to higher operational efficiency and lower material waste in laboratory workflows. The expansion of automated high-throughput CLIA systems, together with increased preventive health screening programs, higher blood safety testing, and expanded test menu options, is driving up consumables consumption, which makes this segment a key driver of overall CLIA market expansion.

"Based on application, the oncology segment is expected to grow with the highest CAGR in the CLIA market."

The CLIA market in oncology applications shows growth because cancer cases are increasing worldwide, and there is greater demand for early diagnosis, prognosis evaluation, and treatment assessment. CLIA technology enables the detection of tumor markers through highly sensitive and specific methods, which include PSA, CA-125, CEA, AFP, and HER2 as diagnostic tools for initial patient evaluation and progress assessment of their medical condition. The rise in biomarker-based testing and precision oncology practices has created a need for dependable immunoassays, which assist in determining targeted therapies and individualized treatment options. The clinical use of CLIA tests has grown because these tests now help doctors monitor patient treatment response, identify cancer recurrences, and assess patients who have a high risk of developing cancer. The introduction of better assay systems, which enhance test sensitivity through automated processes and multiplex testing features, will continue to drive businesses toward adopting CLIA systems in their cancer diagnostic processes.

"Based on the end user, the hospitals segment is expected to grow by the highest CAGR in the CLIA market."

Hospitals need to conduct accurate tests for various medical conditions, including cardiac markers, sepsis indicators, cancer biomarkers, hormone levels, and infectious pathogens. The CLIA systems enable emergency departments, intensive care units, and inpatient services to start treatment without delay through their advanced sensitivity, extensive testing capabilities, and quick result delivery. The move to centralized diagnostic systems, together with automated diagnostic machines, helps hospitals to cut down on manual tasks while achieving better operational results through standardized processes. The worldwide implementation of CLIA analyzers and assays in hospital systems accelerates because hospitals expand their facilities, and preventive health screening programs become more popular, accreditation and quality standards increase, and hospitals need complete laboratory information systems.

"APAC is estimated to register the highest CAGR during the forecast period."

The CLIA market in the Asia Pacific region is growing due to three factors: expanding healthcare, rising healthcare spending, and improved distribution of diagnostic services in countries such as China, India, and Southeast Asia. The rising need for precise early diagnostic tests results from the increasing incidence of chronic illnesses, infectious diseases, and conditions linked to lifestyle choices. The government modernization projects, which include hospital upgrades, laboratory automation, and the development of a national screening program, accelerate the implementation of high-throughput CLIA systems. The demand for advanced immunoassay technologies grows due to three factors, which include increasing public knowledge about preventive healthcare, expanding private diagnostic laboratory networks, and rising medical tourism. The regional growth of the market benefits from three factors, which include a large patient base, better insurance access, and the market's shift toward automated laboratory systems that manage high testing loads. The widespread implementation of CLIA platforms throughout APAC results from two factors, which include ongoing international diagnostic company expansion and the rise of affordable domestic manufacturers.

Key players in the CLIA market

The key players in the market include F. Hoffmann-La Roche Ltd. (Switzerland), Abbott Laboratories (US), Siemens Healthineers (Germany), Danaher Corporation (US), DiaSorin S.p.A. (Italy), QuidelOrtho Corporation (US), Sysmex Corporation (Japan), Shenzhen New Industry Biomedical Engineering Co., Ltd. (SNIBE Diagnostics) (China), Tosoh Corporation (Japan), Werfen (Spain), Bio-Rad Laboratories, Inc. (US), Shenzhen Mindray Biomedical Electronics Co., Ltd. (China), Fujirebio (Japan), HUMAN Gesellschaft fur Biochemica und Diagnostica mbH. (Germany), EUROIMMUN Medizinische Labordiagnostika AG (Germany), Agappe Diagnostics Ltd (India), Zecen Biotech Co., Ltd (China), Maccura Biotechnology Co., Ltd (China), Autobio Diagnostics Co., Ltd. (China), Artron Laboratories Inc.(Canada), Abnova Corporation (Taiwan), Beijing Hotgen Biotech Co., Ltd (China), and Shanghai Kehua Bio-Engineering Co., Ltd. (China).

Research Coverage:

The report analyzes the CLIA market and aims at estimating the market size and future growth potential of this market based on various segments such as product type, sample type, technology, application, and end user. The report also includes a product portfolio matrix of various CLIA available in the market. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall CLIA market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (increasing incidences of chronic and infectious diseases globally, advancements in improving CLIA technologies in recent years, rapid increase in geriatric population globally, growth of biotechnology and biopharmaceutical industries), restraints (high cost associated with placement and maintenance of CLIA, product recalls and failures), challenges (shortage of skilled professionals, risks associated with CLIAs), and opportunities (growth potential in emerging economies)

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global CLIA market

- Product Development/Innovation: Detailed insights on upcoming trends, research & development activities, and new product launches in the global CLIA market

- Market Development: Comprehensive information on the lucrative emerging markets by product type, technology, sample type, application, and end user

- Market Diversification: Exhaustive information about new products and services or product and service enhancements, growing geographies, recent developments, and investments in the global CLIA market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global CLIA market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN CHEMILUMINESCENCE IMMUNOASSAY (CLIA) MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 CHEMILUMINESCENCE IMMUNOASSAY OVERVIEW

- 3.2 ASIA PACIFIC CHEMILUMINESCENCE IMMUNOASSAY, BY PRODUCT AND COUNTRY

- 3.3 CHEMILUMINESCENCE IMMUNOASSAY: DEVELOPED MARKETS VS. EMERGING ECONOMIES

- 3.4 CHEMILUMINESCENCE IMMUNOASSAY: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.5 CHEMILUMINESCENCE IMMUNOASSAY: REGIONAL MIX

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing incidence of chronic and infectious diseases globally

- 4.2.1.2 Advancements in chemiluminescence immunoassay technologies in recent years

- 4.2.1.3 Rapid increase in geriatric population globally

- 4.2.1.4 Growth of biotechnology and biopharmaceutical industries

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of chemiluminescence systems and reagents

- 4.2.2.2 Lack of regular quality control procedures for monitoring and detecting cross-reactivity and interference

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 High growth prospects for players in emerging economies

- 4.2.3.2 Increasing number of collaborations and partnerships

- 4.2.4 CHALLENGES

- 4.2.4.1 Unfavorable reimbursement scenario and budgetary constraints in healthcare systems

- 4.2.4.2 Lack of skilled professionals and aging workforce

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF CHEMILUMINESCENCE IMMUNOASSAY ANALYZERS, BY KEY PLAYER, 2023-2025 (USD)

- 5.6.2 AVERAGE SELLING PRICE TREND OF CHEMILUMINESCENCE IMMUNOASSAY ANALYZERS, BY REGION, 2023-2025 (USD)

- 5.6.3 AVERAGE SELLING PRICE TREND OF CHEMILUMINESCENCE IMMUNOASSAY ANALYZERS, BY TECHNOLOGY, 2023-2025 (USD)

- 5.6.4 AVERAGE SELLING PRICE TREND OF CHEMILUMINESCENCE IMMUNOASSAY CONSUMABLES (KITS, REAGENTS, AND OTHERS), BY SAMPLE TYPE, 2023-2025 (USD)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 9027.89, 2021-2025

- 5.7.2 EXPORT DATA FOR HS CODE 9027.89, 2021-2025

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 CASE STUDY 1: ROCHE COBAS CLIA DRIVES HIGH-VOLUME TESTING PERFORMANCE

- 5.11.2 CASE STUDY 2: ABBOTT ARCHITECT DRIVES REGIONAL MULTI-CENTER LAB EXPANSION

- 5.11.3 CASE STUDY 3: SIEMENS ADVIA CENTAUR XP BOOSTS GOVERNMENT LAB TESTING EFFICIENCY

- 5.12 IMPACT OF 2025 US TARIFFS ON CHEMILUMINESCENCE IMMUNOASSAY MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

- 5.12.5.1 Hospitals

- 5.12.5.2 Clinical laboratories

- 5.12.5.3 Pharmaceutical & biotechnology companies and contract research organizations

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Nano-engineered chemiluminescent labels

- 6.1.1.2 Digital immunoassay platforms

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Bead-based & microarray chemiluminescence

- 6.1.2.2 Integration with microfluidic platforms

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Enzyme-linked immunosorbent assay (ELISA)

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS, AND JURISDICTION FOR CHEMILUMINESCENCE IMMUNOASSAY MARKET, JANUARY 2015-SEPTEMBER 2025

- 6.3.2 LIST OF MAJOR PATENTS, 2022-2025

- 6.4 FUTURE APPLICATIONS

- 6.4.1 PERSONALIZED & PRECISION MEDICINE

- 6.4.2 REMOTE MONITORING & DECENTRALIZED TESTING

- 6.4.3 PREDICTIVE DIAGNOSTICS & CLINICAL DECISION SUPPORT

- 6.4.4 INTEGRATION WITH DIGITAL HEALTH ECOSYSTEMS

- 6.4.5 NEXT-GENERATION BIOMARKER DISCOVERY & MULTIPLEX TESTING

- 6.5 IMPACT OF GEN AI ON CHEMILUMINESCENCE IMMUNOASSAY MARKET

- 6.5.1 IMPACT OF AI/GEN AI ON INTERCONNECTED & ADJACENT ECOSYSTEMS

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 IMPROVED OUTCOMES IN CRITICAL CARE & EMERGENCY DIAGNOSTICS

- 6.6.2 PUBLIC HEALTH SCREENING & INFECTIOUS DISEASE CONTROL

- 6.6.3 ENDOCRINOLOGY & CHRONIC DISEASE MANAGEMENT

- 6.6.4 ONCOLOGY DIAGNOSTICS & THERAPY MONITORING

- 6.6.5 MATERNAL & NEONATAL SCREENING PROGRAMS

- 6.6.6 DECENTRALIZED & MID-VOLUME LABORATORY ADOPTION

- 6.6.7 REAL-WORLD IMPACT

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 ISO 15189 - Quality & competence requirements for medical laboratories

- 7.1.2.2 CLSI Guidelines (Clinical & Laboratory Standards Institute) - Immunoassay performance & validation

- 7.1.2.3 ISO 13485 - Quality management systems for IVD manufacturers

- 7.1.2.4 ISO 17511 - Metrological traceability of calibrators & control materials

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 REAGENT PACKAGING REDUCTION & RECYCLABLE MATERIALS (INDUSTRY INITIATIVES)

- 7.2.2 ENERGY-EFFICIENT & LOW-WASTE ANALYZER OPERATIONS

- 7.2.3 LABORATORY WASTE MANAGEMENT & GREEN LAB PROGRAMS

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.3.1 CERTIFICATIONS & LABELING STANDARDS

- 7.3.2 ECO-STANDARDS & SUSTAINABILITY CONSIDERATIONS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.1.1 Influence of stakeholders on buying process for product types

- 8.2.2 BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE SETTINGS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 CHEMILUMINESCENCE IMMUNOASSAY MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 CONSUMABLES TO ACCOUNT FOR LARGEST MARKET SHARE DURING STUDY PERIOD

- 9.3 INSTRUMENTS

- 9.3.1 INCREASING ADVANCES WITH HIGH-THROUGHPUT CAPACITIES AND GROWING AUTOMATION TRENDS TO DRIVE MARKET

10 CHEMILUMINESCENCE IMMUNOASSAY MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 CHEMILUMINESCENCE ENZYME IMMUNOASSAYS

- 10.2.1 HIGH RELIABILITY OF BLOOD TESTS IN CLINICAL DIAGNOSTICS AND PHARMACEUTICAL RESEARCH TO DRIVE MARKET

- 10.3 ELECTROCHEMILUMINESCENCE IMMUNOASSAYS

- 10.3.1 RISING DEMAND FOR HIGH-SENSITIVITY CARDIAC AND ONCOLOGY BIOMARKERS TO DRIVE MARKET

- 10.4 MICROPARTICLE CHEMILUMINESCENCE IMMUNOASSAYS

- 10.4.1 SUPERIOR SENSITIVITY AND EARLY DISEASE DETECTION TO DRIVE MARKET GROWTH

11 CHEMILUMINESCENCE IMMUNOASSAY MARKET, BY SAMPLE TYPE

- 11.1 INTRODUCTION

- 11.2 BLOOD

- 11.2.1 RELIABILITY OF BLOOD TESTS FOR IMMUNOASSAY DIAGNOSTIC PROCEDURES AND HEALTH SCREENING TO DRIVE MARKET

- 11.3 URINE

- 11.3.1 INCREASING USE IN LAW ENFORCEMENT AND DRUG TESTING CENTERS TO DRIVE MARKET

- 11.4 SALIVA

- 11.4.1 CONVENIENCE AND EASY TESTING OF BIOLOGICALLY ACTIVE PARTS OF HORMONES TO DRIVE MARKET

- 11.5 OTHER SAMPLE TYPES

12 CHEMILUMINESCENCE IMMUNOASSAY MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 INFECTIOUS DISEASES

- 12.2.1 RISING PREVALENCE OF INFECTIOUS DISEASES TO DRIVE MARKET

- 12.3 ENDOCRINOLOGY

- 12.3.1 RISING INCIDENCES OF DIABETES TO PROPEL DEMAND FOR DIAGNOSTICS

- 12.4 ONCOLOGY

- 12.4.1 RISING BURDEN OF CANCER AND EMPHASIS ON EARLY DISEASE DIAGNOSIS TO DRIVE MARKET

- 12.5 CARDIOLOGY

- 12.5.1 HIGH BURDEN OF CARDIOVASCULAR DISEASES AMONG ALL AGE GROUPS TO DRIVE MARKET

- 12.6 ALLERGY DIAGNOSTICS

- 12.6.1 GROWING PREVALENCE OF ALLERGIES TO INCREASE DEMAND FOR CHEMILUMINESCENCE IMMUNOASSAYS

- 12.7 BLOOD SCREENING

- 12.7.1 RISING VOLUME OF BLOOD DONATIONS AND INCREASING INCIDENCES OF BLOOD-RELATED DISORDERS TO DRIVE MARKET

- 12.8 AUTOIMMUNE DISORDERS

- 12.8.1 GROWING PREVALENCE OF AUTOIMMUNE DISORDERS AND RISING ECONOMIC BURDEN OF DISEASE MANAGEMENT TO DRIVE MARKET

- 12.9 BONE & MINERAL DISORDERS

- 12.9.1 HIGH DISORDER PREVALENCE TO OFFER STRONG GROWTH OPPORTUNITIES FOR IMMUNOASSAYS

- 12.10 TOXICOLOGY

- 12.10.1 INCREASED DRUG-OF-ABUSE TESTING AND HIGHER ILLICIT DRUG CONSUMPTION TO DRIVE MARKET

- 12.11 NEWBORN SCREENING

- 12.11.1 ROUTINE USE IN FIRST-TIER NEWBORN SCREENING PROTOCOL TO SUSTAIN DEMAND

- 12.12 THERAPEUTIC DRUG MONITORING

- 12.12.1 RAPID DETECTION TIME AND GOOD SPECIFICITY TO DRIVE MARKET

- 12.13 METABOLIC DISORDERS

- 12.13.1 RISING PREVALENCE OF METABOLIC DISORDERS TO DRIVE MARKET

- 12.14 GASTROENTEROLOGY

- 12.14.1 INCREASING INCIDENCE OF GASTROINTESTINAL TRACT INFECTIONS AND SERIOUS GASTRIC DISEASES TO DRIVE MARKET

- 12.15 NEUROLOGY

- 12.15.1 EFFECTIVE DETECTION, MONITORING, AND MANAGEMENT OF NEUROLOGICAL DISORDERS TO DRIVE SEGMENT

- 12.16 RESPIRATORY DISEASES

- 12.16.1 EASY DETECTION AND DIAGNOSIS OF RESPIRATORY DISEASES TO DRIVE MARKET

- 12.17 OTHER APPLICATIONS

13 CHEMILUMINESCENCE IMMUNOASSAY MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 HOSPITALS

- 13.2.1 GROWING PATIENT POPULATION AND TESTING VOLUMES ENSURE LEADERSHIP OF HOSPITALS

- 13.3 CLINICAL LABORATORIES

- 13.3.1 RISING CLINICAL TEST VOLUMES AND REQUIREMENTS TO DRIVE SEGMENT

- 13.4 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES AND CROS

- 13.4.1 RISING DRUG DISCOVERY ACTIVITY AND CLINICAL STUDIES TO DRIVE MARKET

- 13.5 OTHER END USERS

14 CHEMILUMINESCENCE IMMUNOASSAY MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.1.1 GLOBAL: VOLUME ANALYSIS OF CHEMILUMINESCENCE IMMUNOASSAY INSTRUMENTS, 2024-2031 (HUNDRED UNITS)

- 14.2 NORTH AMERICA

- 14.2.1 MACROECONOMIC OUTLOOK

- 14.2.2 NORTH AMERICA: VOLUME ANALYSIS OF CHEMILUMINESCENCE IMMUNOASSAY INSTRUMENTS, 2024-2031 (HUNDRED UNITS)

- 14.2.3 US

- 14.2.3.1 US to hold largest share of North American market during forecast period

- 14.2.4 CANADA

- 14.2.4.1 Rising government initiatives and funding for early disease diagnosis to drive market

- 14.3 EUROPE

- 14.3.1 MACROECONOMIC OUTLOOK

- 14.3.2 EUROPE: VOLUME ANALYSIS OF CHEMILUMINESCENCE IMMUNOASSAY INSTRUMENTS, 2024-2031 (HUNDRED UNITS)

- 14.3.3 GERMANY

- 14.3.3.1 Growing investments in clinical diagnostics research and increasing government spending on healthcare to drive market

- 14.3.4 FRANCE

- 14.3.4.1 Favorable reimbursement policies and increased investments in diagnostics to drive market

- 14.3.5 UK

- 14.3.5.1 Increasing number of accredited clinical laboratories and growing accessibility to IVD tests to drive market

- 14.3.6 ITALY

- 14.3.6.1 Growing geriatric population and increasing support for research to drive market

- 14.3.7 SPAIN

- 14.3.7.1 Rising adoption of technologically advanced immunoassay systems to drive market

- 14.3.8 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 MACROECONOMIC OUTLOOK

- 14.4.2 ASIA PACIFIC: VOLUME ANALYSIS OF CHEMILUMINESCENCE IMMUNOASSAY INSTRUMENTS, 2024-2031 (HUNDRED UNITS)

- 14.4.3 JAPAN

- 14.4.3.1 Growing investments in clinical diagnostics research to drive market

- 14.4.4 CHINA

- 14.4.4.1 China to register highest growth rate in Asia Pacific market during study period

- 14.4.5 INDIA

- 14.4.5.1 Growing medical tourism and healthcare infrastructure to drive market

- 14.4.6 SOUTH KOREA

- 14.4.6.1 Rising healthcare spending for innovative IVD technologies to drive market

- 14.4.7 AUSTRALIA

- 14.4.7.1 Rising healthcare spending for innovative IVD technologies to drive market

- 14.4.8 REST OF ASIA PACIFIC

- 14.5 LATIN AMERICA

- 14.5.1 MACROECONOMIC OUTLOOK

- 14.5.2 LATIN AMERICA: VOLUME ANALYSIS OF CHEMILUMINESCENCE IMMUNOASSAY INSTRUMENTS, 2024-2031 (HUNDRED UNITS)

- 14.5.3 BRAZIL

- 14.5.3.1 Improving healthcare facilities to drive market

- 14.5.4 MEXICO

- 14.5.4.1 Robust healthcare system to drive market growth in Mexico

- 14.5.5 REST OF LATIN AMERICA

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MACROECONOMIC OUTLOOK

- 14.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS OF CHEMILUMINESCENCE IMMUNOASSAY INSTRUMENTS, 2024-2031 (HUNDRED UNITS)

- 14.6.3 GCC COUNTRIES

- 14.6.4 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Product type footprint

- 15.5.5.4 Technology footprint

- 15.5.5.5 Sample type footprint

- 15.5.5.6 Application footprint

- 15.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2025

- 15.6.5.1 Detailed list of key start-ups/SMEs

- 15.6.5.2 Competitive benchmarking of key start-ups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 PRODUCT COMPARISON

- 15.8.1 F. HOFFMANN-LA ROCHE LTD

- 15.8.2 DANAHER CORPORATION

- 15.8.3 ABBOTT

- 15.8.4 SIEMENS HEALTHINEERS AG

- 15.8.5 DIASORIN S.P.A

- 15.9 COMPETITIVE SCENARIO

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 F. HOFFMANN-LA ROCHE LTD

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses/Competitive threats

- 16.1.2 ABBOTT

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses/Competitive threats

- 16.1.3 SIEMENS HEALTHINEERS AG

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses/Competitive threats

- 16.1.4 DANAHER CORPORATION

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses/Competitive threats

- 16.1.5 DIASORIN S.P.A.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product approvals

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses/Competitive threats

- 16.1.6 QUIDELORTHO CORPORATION

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.7 SYSMEX CORPORATION

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches

- 16.1.7.3.2 Deals

- 16.1.8 SHENZHEN NEW INDUSTRIES BIOMEDICAL ENGINEERING CO., LTD.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product approvals

- 16.1.9 TOSOH CORPORATION

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.10 WERFEN

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.11 BIO-RAD LABORATORIES, INC.

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.12 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.13 FUJIREBIO

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.14 EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches & approvals

- 16.1.14.3.2 Deals

- 16.1.15 AGAPPE DIAGNOSTICS LTD.

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.1 F. HOFFMANN-LA ROCHE LTD

- 16.2 OTHER PLAYERS

- 16.2.1 ZECEN BIOTECH CO., LTD

- 16.2.2 MACCURA BIOTECHNOLOGY CO., LTD.

- 16.2.3 AUTOBIO DIAGNOSTICS

- 16.2.4 ARTRON LABORATORIES INC.

- 16.2.5 HUMAN GESELLSCHAFT FUR BIOCHEMICA UND DIAGNOSTICA MBH

- 16.2.6 ABNOVA CORPORATION

- 16.2.7 BEIJING HOTGEN BIOTECH CO., LTD.

- 16.2.8 ELABSCIENCE

- 16.2.9 GETEIN BIOTECH, INC.

- 16.2.10 SHANGHAI KEHUA BIO-ENGINEERING CO., LTD.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.1.2 Primary sources

- 17.1.1.3 Key data from primary sources

- 17.1.1.4 Breakdown of primaries

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.3 GROWTH FORECAST

- 17.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.3.1 GEOGRAPHIC ANALYSIS

- 18.3.2 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 18.3.3 COMPANY INFORMATION

- 18.3.4 PRODUCT TYPE ANALYSIS

- 18.3.4.1 By Analyzer (Semi and fully automated system)

- 18.3.4.2 By Technology (Breakdown by subcategories)

- 18.3.5 BY END USER (BREAKDOWN BY SUBCATEGORIES)

- 18.3.6 BY MODE OF PURCHASE/BUSINESS MODEL

- 18.3.7 COUNTRY-LEVEL VOLUME ANALYSIS

- 18.3.8 BY PRODUCT TYPE MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 18.3.9 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS