|

시장보고서

상품코드

1986225

동물 의료 수탁 제조 및 연구 시장 예측(-2031년) : 서비스(디스커버리, API 개발, 규제 대응, 컨설팅, 포장 및 라벨링), 제품(API, Fill-Finish, 의료기기), 동물 유형별(반려동물, 가축)Veterinary Contract Manufacturing & Research Market by Service (Discovery, API Development, Regulatory Affairs, Consulting, Packaging & Labeling), Product (API, Fill-Finish, Medical Devices), Animal Type (Companion, Livestock) - Global Forecast to 2031 |

||||||

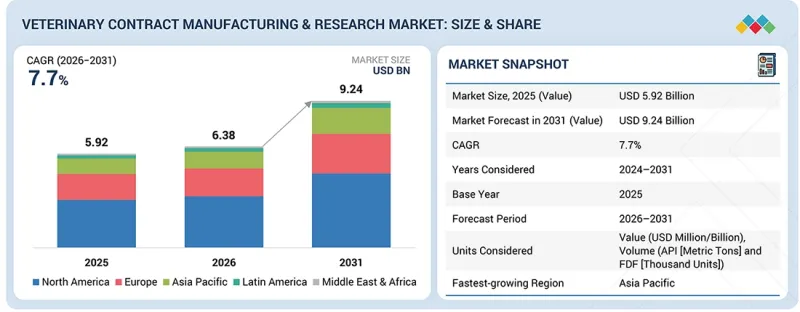

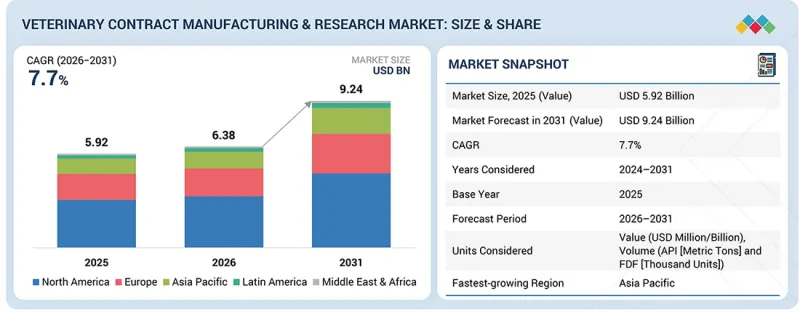

동물 의료 수탁 제조·연구 시장 규모는 2026년 63억 8,000만 달러에서 2031년에는 92억 4,000만 달러에 CAGR 7.7%로 확대할 것으로 예측됩니다.

이 시장의 성장은 동물용 의약품 개발, 바이오의약품 제조, 정밀 동물 의료의 미래를 형성하는 몇 가지 주요 요인에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 서비스별, 제품 유형별, 동물 유형별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

이러한 성장의 주요 요인은 동물용 의약품 기업이 제품 파이프라인의 가속화, 내부 비용 절감, 바이오의약품, 백신, 첨단 제제 등 복잡한 치료제에 대한 전문적 지식에 대한 접근을 원하면서 개발 및 제조 서비스 아웃소싱에 대한 수요가 증가하고 있기 때문입니다. 동물 의료 산업이 보다 타겟팅된 데이터베이스 치료 접근 방식으로 전환함에 따라 고품질 연구, 분석 테스트 및 GMP 준수 생산에 대한 요구가 빠르게 증가하고 있습니다. 또한 반려동물과 가축의 만성질환, 전염병, 인수공통전염병에 대한 부담이 증가함에 따라 보다 신속하고 효율적인 연구개발(R&D) 프로세스에 대한 요구가 증가하고 있습니다. CDMO와 CRO는 확장 가능한 제조, 높은 처리량 스크리닝, 첨단 연구 역량을 제공함으로써 이러한 요구에 부응하는 데 있으며, 매우 중요한 역할을 하고 있습니다. 실시간 모니터링 툴의 도입, 디지털 워크플로우, 임상시험 관리 개선 등 동물 의료의 지속적인 현대화 추세는 전문 아웃소싱 파트너에 대한 의존도를 더욱 높이고 있습니다.

예측 모델링을 위한 AI 통합, 바이오프로세스 자동화, 고급 분석 플랫폼 개발 등의 기술 발전도 시장 성장을 촉진하고 있습니다. 이러한 혁신은 정확도를 높이고, 개발 기간을 단축하며, 전임상, 임상, 상업화 단계의 아웃소싱 서비스 적용 범위를 확대할 수 있습니다. 전반적으로 업계 수요 증가, 기술 발전, 전문적이고 아웃소싱된 전문 지식으로의 전환이 동물 의료 분야의 수탁제조 및 위탁 연구 시장의 강력하고 지속적인 성장을 주도하고 있습니다.

"동물 유형별로는 반려동물 부문이 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예측됩니다. "

반려동물 사육두수 증가, 고급 치료에 대한 지출 확대, 개와 고양이를 위한 혁신적인 치료제에 대한 수요증가로 인해 이 부문은 가장 높은 성장세를 보일 것으로 예측됩니다. 암, 비만, 알레르기, 만성질환 등의 질병이 반려동물에게 더욱 흔해지면서 신약, 바이오의약품, 특수 제제에 대한 수요가 증가하고 있습니다. 반려동물 보호자들의 고품질 케어에 대한 투자 의지와 더불어 반려동물의 '인간화'와 보험 적용 범위의 확대가 맞물리면서 동물 의료 기업은 보다 복잡한 제품 개발을 추진하고 있으며, 그 결과 연구개발, 제조, 임상시험을 CDMO 및 CRO에 아웃소싱하는 사례가 증가하고 있습니다.

"최종사용자별로는 2024년 다국적 동물의료기업이 가장 큰 시장 점유율을 보일 것"

다국적 동물의료 기업 부문은 광범위한 제품 파이프라인을 관리하고, 세계 규제에 대응하는 공급망을 운영하며, 첨단 치료제, 백신, 진단약 개발에 지속적으로 투자하고 있으며, 2024년 시장을 주도할 것으로 예측되었습니다. 광범위한 포트폴리오와 높은 생산량은 제형 개발, 스케일업, 분석 시험, 임상 연구를 지원하는 전문 아웃소싱 파트너에 대한 강력한 수요를 창출하고 있습니다. 또한 이들 기업은 시장 출시 기간 단축, 제조 능력 확대, 첨단 기술 접근을 위해 CDMO 및 CRO에 대한 의존도를 높이고 있으며, 이는 전체 시장 수요를 견인하는 주요 요인으로 작용하고 있습니다.

"아시아태평양이 예측 기간 중 가장 높은 성장률을 보일 것으로 예상"

아시아태평양은 중국, 인도, 동남아시아 등의 국가에서 가축 생산 증가, 반려동물 사육두수 증가, 동물 보건 인프라에 대한 투자 확대에 힘입어 가장 높은 성장이 예상됩니다. 이 지역에서는 동물용 의약품 생산이 빠르게 확대되고, 첨단 생물제제와 진단약의 채택이 증가하고 있으며, 질병 대책과 백신 접종 프로그램에 대한 정부 지원도 강화되고 있습니다. 또한 운영 비용 절감, 규제 프레임워크의 개선, 현지 CDMO 및 CRO의 부상으로 인해 전 세계 동물용의약품 기업이 연구 및 제조 아웃소싱을 아시아태평양으로 더 많이 이전하고 있으며, 이는 이 지역의 성장을 가속화하고 있습니다.

세계의 동물용 의약품 수탁제조 및 위탁연구 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다. 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴적 혁신

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 동물 의료 수탁 제조·연구 시장 : 서비스별

제10장 동물 의료 수탁 제조·연구 시장 : 제품 유형별

제11장 동물 의료 수탁 제조·연구 시장 : 동물 유형별

제12장 동물 의료 수탁 제조·연구 시장 : 최종사용자별

제13장 동물 의료 수탁 제조·연구 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.04.10The veterinary contract manufacturing & research market is expected to grow from USD 6.38 billion in 2026 to USD 9.24 billion by 2031, at a CAGR of 7.7%. The market growth is driven by several key factors shaping the future of veterinary drug development, biologics manufacturing, and precision animal health.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Service, Product Type, Animal Type, End User, Region |

| Regions covered | North America, Europe,Asia Pacific, Latin America, Middle East & Africa |

A major driver of this growth is the increasing demand for outsourced development and manufacturing services as animal health companies seek to accelerate product pipelines, reduce internal costs, and access specialized expertise for complex therapeutics such as biologics, vaccines, and advanced formulations. As the veterinary industry shifts toward more targeted, data-driven treatment approaches, the need for high-quality research, analytical testing, and GMP-compliant production is rapidly rising. Additionally, the growing burden of chronic, infectious, and zoonotic diseases in both companion and livestock animals is driving demand for faster and more efficient research and development (R&D) processes. CDMOs and CROs play a critical role in meeting this need by providing scalable manufacturing, high-throughput screening, and advanced study capabilities. The ongoing trend toward modernization in veterinary healthcare, including the adoption of real-time monitoring tools, digital workflows, and improved clinical trial management, further strengthens reliance on specialized outsourcing partners.

Technological advancements, including the integration of AI for predictive modeling, automation in bioprocessing, and the development of enhanced analytical platforms, also drive market growth. These innovations enhance accuracy, shorten development timelines, and expand the applications of outsourced services across preclinical, clinical, and commercial phases. Overall, rising industry demands, advancements in technology, and the growing shift toward specialized and outsourced expertise are driving strong and sustained growth in the veterinary contract manufacturing & research market.

"By animal type, the companion animals segment is projected to grow at the highest CAGR during the forecast period."

The software & services segment is expected to see the highest growth in the veterinary contract manufacturing & research market, due to rising pet ownership, increasing spending on advanced treatments, and growing demand for innovative therapeutics for dogs and cats. Conditions such as cancer, obesity, allergies, and chronic diseases are becoming more prevalent in pets, driving the need for new drugs, biologics, and specialty formulations. Pet owners' willingness to invest in premium care, coupled with the humanization of pets and expanding insurance coverage, is encouraging animal health companies to develop more complex products-leading to greater outsourcing of R&D, manufacturing, and clinical studies to CDMOs and CROs.

"By end user, the multinational animal-health companies segment accounted for the largest market share in 2024."

In 2024, the veterinary clinics segment dominated the veterinary contract manufacturing & research market because they manage extensive product pipelines, operate globally regulated supply chains, and consistently invest in developing advanced therapeutics, vaccines, and diagnostics. Their broad portfolios and high production volumes create a strong need for specialized outsourcing partners to support formulation, scale-up, analytical testing, and clinical research. Additionally, these companies increasingly rely on CDMOs and CROs to accelerate time-to-market, expand manufacturing capacity, and access cutting-edge technologies, making them the primary contributors to overall market demand.

"The Asia Pacific region is projected to witness the highest growth rate during the forecast period."

The Asia Pacific is expected to experience the highest growth in the veterinary contract manufacturing & research market, driven by rising livestock production, increasing pet ownership, and growing investment in animal health infrastructure across countries such as China, India, and Southeast Asia. The region is witnessing rapid expansion of veterinary pharmaceutical manufacturing, greater adoption of advanced biologics and diagnostics, and stronger government support for disease control and vaccination programs. Additionally, lower operational costs, improving regulatory frameworks, and the emergence of local CDMOs and CROs are attracting global animal health companies to outsource more research and manufacturing to APAC, driving its accelerated growth.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By End User: Multinational animal-health companies (59%), mid-sized / specialty animal-health firms (26%), and start-ups & veterinary biotech firms (15%)

- By Designation: R&D directors/heads of research (47%), product development & innovation managers (22%), regulatory affairs managers/directors (15%), and others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the veterinary contract manufacturing & research market in various segments. It aims to estimate the market size and growth potential of this market by service, product type, animal type, end user, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can help established companies and newer or smaller firms understand market trends, enabling them to capture a larger market share. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (growth in animal health spending, increasing complexity of veterinary biologics and the increasing regulatory burden for GMP, biosecurity & environmental compliance.), restraints (limited specialized infrastructure and long approval timelines & regulatory diversity globally), opportunities (geographic expansion into emerging markets, digital CRO services), and challenges (difficulty in clinical trial recruitment and difficulty in scaling sterile/biologics capacity quickly) influencing the growth of the veterinary contract manufacturing & research market

- Product Development/Innovation: Detailed insights on upcoming technologies and service launches in the veterinary contract manufacturing & research market

- Market Development: Comprehensive information about lucrative emerging markets; the report analyzes the markets for various types of veterinary CDMO & CRO services across regions

- Market Diversification: Exhaustive information about services, untapped regions, recent developments, and investments in the veterinary contract manufacturing & research market

- Competitive Assessment: In-depth assessment of market shares, strategies, services, distribution networks, and manufacturing capabilities of the leading players in the veterinary contract manufacturing & research market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 LIMITATIONS

2 EXECUTIVE SUMMARY

3 PREMIUM INSIGHTS

- 3.1 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET OVERVIEW

- 3.2 ASIA PACIFIC: VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET, BY SERVICE & COUNTRY (2025)

- 3.3 VETERINARY CROS MARKET: REGIONAL MIX

- 3.4 VETERINARY CDMOS MARKET: REGIONAL MIX

- 3.5 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.6 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in animal health spending

- 4.2.1.2 Increasing complexity of veterinary biologics

- 4.2.1.3 Rising regulatory requirements for GMP, biosecurity, and environmental compliance

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited specialized infrastructure

- 4.2.2.2 Long approval timelines & regulatory diversity globally

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Geographic expansion into emerging markets

- 4.2.3.2 Digital CRO services

- 4.2.4 CHALLENGES

- 4.2.4.1 Challenges in clinical trial recruitment

- 4.2.4.2 Difficulty in scaling sterile/biologics capacity quickly

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 UNMET NEEDS IN VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF API & FILL-FINISH PHARMACEUTICALS & BIOLOGICS, BY KEY PLAYER, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF API & FILL-FINISH PHARMACEUTICALS & BIOLOGICS, BY REGION, 2023-2025

- 5.6.2.1 Average selling price trend of small-molecule pharmaceuticals for API/drug substance manufacturing, by region, 2023-2025

- 5.6.2.2 Average selling price trend of small-molecule pharmaceuticals for fill-finish/drug product manufacturing, by region, 2023-2025

- 5.6.2.3 Average selling price trend of animal health biologics & vaccines for API/drug substance manufacturing, by region, 2023-2025

- 5.6.2.4 Average selling price trend of animal health biologics & vaccines for fill-finish/drug product manufacturing, by region, 2023-2025

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 5.10.1 END-TO-END CDMO SUPPORT FOR ANIMAL HEALTH LATERAL FLOW DIAGNOSTICS

- 5.10.2 END-TO-END CDMO SUPPORT FOR FIRST-IN-CLASS VETERINARY MONOCLONAL ANTIBODY (MAB)

- 5.10.3 END-TO-END BIOLOGICS OPTIMIZATION FOR CANINE ANTIBODY PROGRAMS

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 High-throughput in vitro & in vivo screening platforms

- 6.1.1.2 AI/ML platforms for drug discovery

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Laboratory automation, robotics, and smart QC systems

- 6.1.2.2 Stability, cold chain, and packaging optimization technologies

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Digital therapeutics & software-as-a-medical-device (SaMD)

- 6.1.3.2 Precision livestock technologies

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR TERM (2025-2027)

- 6.2.2 MID TERM (2028-2030)

- 6.2.3 LONG TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR VETERINARY PHARMACEUTICALS

- 6.3.2 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 ADVANCED BIOLOGICS & VACCINE MANUFACTURING PLATFORMS

- 6.4.2 DIGITALIZED, DATA-RICH CLINICAL DEVELOPMENT USING AI, REMOTE MONITORING, AND REAL-WORLD DATA

- 6.4.3 GLOBALIZED, REGULATORY-READY DEVELOPMENT WITH HARMONIZED QUALITY & MANUFACTURING SYSTEMS

- 6.4.4 INNOVATIVE FORMULATION TECHNOLOGIES FOR LONG-ACTING, SPECIES-TAILORED, AND DIFFICULT-TO-DELIVER PRODUCTS

- 6.5 IMPACT OF AI/GENERATIVE AI ON VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL IN VETERINARY CONTRACT MANUFACTURING & RESEARCH ECOSYSTEM

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI IN VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY ANALYSIS

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RECYCLED AND ECO-FRIENDLY MATERIALS FOR VETERINARY PRODUCTS

- 7.2.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET, BY SERVICE

- 9.1 INTRODUCTION

- 9.2 CRO SERVICES

- 9.2.1 DISCOVERY & PRE-CLINICAL STUDIES

- 9.2.1.1 Growing use of discovery & pre-clinical studies to accelerate veterinary drug pipeline initiation

- 9.2.2 VETERINARY CLINICAL TRIALS

- 9.2.2.1 Growing dependence on veterinary clinical trials to validate safety and efficacy for regulatory approvals to boost market

- 9.2.3 ANALYTICAL & BIOANALYTICAL SERVICES AND QUALITY ASSURANCE

- 9.2.3.1 Rising adoption of analytical & bioanalytical services to ensure high-quality, compliant veterinary products to fuel growth

- 9.2.4 REGULATORY AFFAIRS & CONSULTING

- 9.2.4.1 Increasing need for regulatory affairs & consulting to navigate complex global veterinary approval pathways to support growth

- 9.2.1 DISCOVERY & PRE-CLINICAL STUDIES

- 9.3 CDMO SERVICES

- 9.3.1 PROCESS API & FORMULATION DEVELOPMENT

- 9.3.1.1 Growing focus on process API & formulation development to optimize veterinary product performance to drive growth

- 9.3.2 MANUFACTURING

- 9.3.2.1 Increasing outsourcing of manufacturing to scale production of veterinary drugs and biologics

- 9.3.3 PACKAGING & LABELING

- 9.3.3.1 Rising dependence on packaging & labeling services to ensure regulatory-compliant product delivery to propel market

- 9.3.4 QUALITY/STABILITY & POST-MARKET SUPPORT

- 9.3.4.1 Expanding use of quality, stability, and post-market support to maintain lifecycle product compliance to boost market

- 9.3.1 PROCESS API & FORMULATION DEVELOPMENT

10 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET, BY PRODUCT TYPE

- 10.1 INTRODUCTION

- 10.2 MEDICINES

- 10.2.1 SMALL-MOLECULE PHARMACEUTICALS

- 10.2.1.1 API/Drug substance manufacturing

- 10.2.1.1.1 Growing focus on API manufacturing to support market growth

- 10.2.1.1.2 Global volume analysis of small-molecule pharmaceuticals market for API/drug substance manufacturing, by type, 2024-2031 (metric tons)

- 10.2.1.2 Fill-finish/drug product manufacturing

- 10.2.1.2.1 Increasing demand for fill-finish operations to fuel market growth

- 10.2.1.2.2 Global volume analysis of small-molecule pharmaceuticals market for fill-finish/drug product manufacturing, by type, 2024-2031 (ten thousand units)

- 10.2.1.1 API/Drug substance manufacturing

- 10.2.2 ANIMAL HEALTH BIOLOGICS & VACCINES

- 10.2.2.1 API/Drug substance manufacturing

- 10.2.2.1.1 Rising demand for API/drug substance manufacturing to drive growth

- 10.2.2.1.2 Global volume analysis of animal health biologics & vaccines for API/drug substance manufacturing, by type, 2024-2031 (metric tons)

- 10.2.2.2 Fill-finish/drug product manufacturing

- 10.2.2.2.1 Rising dependence on fill-finish capabilities to fuel growth

- 10.2.2.2.2 Global volume analysis of animal health biologics & vaccines market for fill-finish/drug product manufacturing, by type, 2024-2031 (thousand units)

- 10.2.2.1 API/Drug substance manufacturing

- 10.2.3 MEDICATED FEED & SUPPLEMENTS

- 10.2.3.1 Rising use of medicated feed & supplements to enhance livestock health and productivity

- 10.2.1 SMALL-MOLECULE PHARMACEUTICALS

- 10.3 MEDICAL DEVICES

- 10.3.1 DIAGNOSTICS

- 10.3.1.1 Growing adoption of veterinary diagnostics to drive market growth

- 10.3.2 MONITORING SYSTEMS

- 10.3.2.1 Expanding utilization of monitoring systems to improve real-time animal health management to fuel growth

- 10.3.3 IMPLANTS

- 10.3.3.1 Increasing use of veterinary implants to support long-term treatment and orthopedic care to drive growth

- 10.3.1 DIAGNOSTICS

11 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET, BY ANIMAL TYPE

- 11.1 INTRODUCTION

- 11.2 COMPANION ANIMALS

- 11.2.1 DOGS

- 11.2.1.1 High adoption rates of dogs to drive market growth

- 11.2.2 CATS

- 11.2.2.1 Rising disease prevalence among cats to drive market

- 11.2.3 HORSES

- 11.2.3.1 Growing equine population to support market growth

- 11.2.4 OTHER COMPANION ANIMALS

- 11.2.1 DOGS

- 11.3 LIVESTOCK ANIMALS

- 11.3.1 CATTLE

- 11.3.1.1 Growing consumption of meat to drive market

- 11.3.2 SWINE

- 11.3.2.1 Growing incidence of infectious diseases to drive market

- 11.3.3 POULTRY

- 11.3.3.1 Increasing demand for poultry meat to contribute to market growth

- 11.3.4 SHEEP & GOATS

- 11.3.4.1 Growing global demand for wool to drive market

- 11.3.5 OTHER LIVESTOCK ANIMALS

- 11.3.1 CATTLE

12 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 MULTINATIONAL ANIMAL HEALTH COMPANIES

- 12.2.1 INCREASED OUTSOURCING BY MULTINATIONAL ANIMAL HEALTH COMPANIES TO EXPAND GLOBAL PRODUCT DEVELOPMENT

- 12.3 MID-SIZED/SPECIALTY ANIMAL HEALTH FIRMS

- 12.3.1 RISING RELIANCE OF MID-SIZED & SPECIALTY ANIMAL HEALTH FIRMS ON CDMO/CRO PARTNERS TO BOOST PIPELINES

- 12.4 START-UPS & VETERINARY BIOTECH FIRMS

- 12.4.1 GROWING ENGAGEMENT OF START-UPS & VETERINARY BIOTECH FIRMS TO ACCESS ADVANCED DEVELOPMENT CAPABILITIES

13 VETERINARY CONTRACT MANUFACTURING & RESEARCH MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 NORTH AMERICA: VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031

- 13.2.3 NORTH AMERICA: VALUE ANALYSIS, 2024-2031

- 13.2.4 US

- 13.2.4.1 Rising pet population to drive demand

- 13.2.5 CANADA

- 13.2.5.1 Rising pet adoption rate to drive market

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 EUROPE: VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031

- 13.3.3 EUROPE: VALUE ANALYSIS, 2024-2031

- 13.3.4 GERMANY

- 13.3.4.1 Germany to dominate European market during forecast period

- 13.3.5 UK

- 13.3.5.1 Increasing pet ownership to drive market growth

- 13.3.6 FRANCE

- 13.3.6.1 Rising cases of zoonotic diseases to drive market growth

- 13.3.7 ITALY

- 13.3.7.1 Growing livestock population to support market growth

- 13.3.8 SPAIN

- 13.3.8.1 Increasing animal healthcare expenditure to drive market growth

- 13.3.9 NETHERLANDS

- 13.3.9.1 Increasing companion animal population to drive market growth

- 13.3.10 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 ASIA PACIFIC: VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031

- 13.4.3 ASIA PACIFIC: VALUE ANALYSIS, 2024-2031

- 13.4.4 CHINA

- 13.4.4.1 China to dominate APAC market during forecast period

- 13.4.5 JAPAN

- 13.4.5.1 Aging pet population to drive market

- 13.4.6 INDIA

- 13.4.6.1 Rising livestock population to boost market growth

- 13.4.7 AUSTRALIA

- 13.4.7.1 Rising livestock animal population and increasing pet ownership to support market growth

- 13.4.8 SOUTH KOREA

- 13.4.8.1 Increasing demand for preventive care and aging pet population to drive market

- 13.4.9 THAILAND

- 13.4.9.1 Increasing demand for preventive care and aging pet population to drive market

- 13.4.10 NEW ZEALAND

- 13.4.10.1 High biosecurity standards to drive market

- 13.4.11 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 LATIN AMERICA: VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031

- 13.5.3 LATIN AMERICA: VALUE ANALYSIS, 2024-2031

- 13.5.4 BRAZIL

- 13.5.4.1 Brazil to dominate LATAM market due to rapidly increasing livestock population

- 13.5.5 MEXICO

- 13.5.5.1 Rising demand for animal-derived food products to contribute to market growth

- 13.5.6 ARGENTINA

- 13.5.6.1 Rising livestock population to fuel market growth

- 13.5.7 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS, BY PRODUCT TYPE, 2024-2031

- 13.6.3 MIDDLE EAST & AFRICA: VALUE ANALYSIS, 2024-2031

- 13.6.4 GCC COUNTRIES

- 13.6.4.1 Kingdom of Saudi Arabia (KSA)

- 13.6.4.1.1 Technological advancements & government initiatives to boost growth

- 13.6.4.2 United Arab Emirates (UAE)

- 13.6.4.2.1 Government support and high livestock population to fuel UAE's market growth

- 13.6.4.3 Rest of GCC Countries

- 13.6.4.1 Kingdom of Saudi Arabia (KSA)

- 13.6.5 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.3.1 KEY VETERINARY CONTRACT RESEARCH ORGANIZATIONS

- 14.3.2 KEY VETERINARY CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS

- 14.4 VETERINARY CRO MARKET SHARE ANALYSIS, 2025

- 14.4.1 GLOBAL MARKET SHARE ANALYSIS OF VETERINARY CONTRACT RESEARCH ORGANIZATIONS, 2025

- 14.4.2 RANKING OF KEY MARKET PLAYERS

- 14.4.3 US MARKET SHARE ANALYSIS OF VETERINARY CONTRACT RESEARCH ORGANIZATIONS, 2025

- 14.4.4 EUROPE MARKET SHARE ANALYSIS OF VETERINARY CONTRACT RESEARCH ORGANIZATIONS, 2025

- 14.5 VETERINARY CDMO MARKET SHARE ANALYSIS, 2025

- 14.5.1 GLOBAL MARKET SHARE ANALYSIS OF VETERINARY CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS, 2025

- 14.5.2 RANKING OF KEY MARKET PLAYERS

- 14.5.3 US MARKET SHARE ANALYSIS OF VETERINARY CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS, 2025

- 14.5.4 EUROPE MARKET SHARE ANALYSIS OF VETERINARY CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS, 2025

- 14.6 COMPANY EVALUATION MATRIX: KEY VETERINARY CROS, 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY VETERINARY CROS, 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Service footprint

- 14.6.5.4 Product type footprint

- 14.6.5.5 Animal type footprint

- 14.7 COMPANY EVALUATION MATRIX: VETERINARY CRO STARTUPS/SMES, 2025

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: VETERINARY CRO STARTUPS/SMES, 2025

- 14.7.5.1 Detailed list of key veterinary CRO startups/SMEs

- 14.7.5.2 Competitive benchmarking of key veterinary CRO startups/SMEs

- 14.8 COMPANY EVALUATION MATRIX: VETERINARY CDMOS, 2025

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 PERVASIVE PLAYERS

- 14.8.4 PARTICIPANTS

- 14.8.5 COMPANY FOOTPRINT: KEY VETERINARY CDMOS, 2025

- 14.8.5.1 Company footprint

- 14.8.5.2 Region footprint

- 14.8.5.3 Service footprint

- 14.8.5.4 Product type footprint

- 14.8.5.5 Animal type footprint

- 14.9 COMPANY EVALUATION MATRIX: VETERINARY CDMO STARTUPS/SMES, 2025

- 14.9.1 PROGRESSIVE COMPANIES

- 14.9.2 RESPONSIVE COMPANIES

- 14.9.3 DYNAMIC COMPANIES

- 14.9.4 STARTING BLOCKS

- 14.9.5 COMPETITIVE BENCHMARKING: VETERINARY CDMO STARTUPS/SMES, 2025

- 14.9.5.1 Detailed list of key veterinary CDMO startups/SMEs

- 14.9.5.2 Competitive benchmarking of key veterinary CDMO startups/SMEs

- 14.10 SERVICE COMPARATIVE ANALYSIS

- 14.11 COMPANY VALUATION & FINANCIAL METRICS

- 14.11.1 FINANCIAL METRICS

- 14.11.2 COMPANY VALUATION

- 14.12 COMPETITIVE SCENARIO

- 14.12.1 SERVICE LAUNCHES & APPROVALS

- 14.12.2 DEALS

- 14.12.3 EXPANSIONS

- 14.12.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS

- 15.1.1 KEY PLAYERS

- 15.1.1.1 Argenta Holdco Limited

- 15.1.1.1.1 Business overview

- 15.1.1.1.2 Services offered

- 15.1.1.1.3 Recent developments

- 15.1.1.1.3.1 Service launches & upgrades

- 15.1.1.1.3.2 Deals

- 15.1.1.1.3.3 Expansions

- 15.1.1.1.4 MnM view

- 15.1.1.1.4.1 Key strengths

- 15.1.1.1.4.2 Strategic choices

- 15.1.1.1.4.3 Weaknesses & competitive threats

- 15.1.1.2 Aenova Group

- 15.1.1.2.1 Business overview

- 15.1.1.2.2 Services offered

- 15.1.1.2.3 Recent developments

- 15.1.1.2.3.1 Expansions

- 15.1.1.2.3.2 Other developments

- 15.1.1.2.4 MnM view

- 15.1.1.2.4.1 Key strengths

- 15.1.1.2.4.2 Strategic choices

- 15.1.1.2.4.3 Weaknesses & competitive threats

- 15.1.1.3 FAREVA SA

- 15.1.1.3.1 Business overview

- 15.1.1.3.2 Services offered

- 15.1.1.3.3 MnM view

- 15.1.1.3.3.1 Key strengths

- 15.1.1.3.3.2 Strategic choices

- 15.1.1.3.3.3 Weaknesses & competitive threats

- 15.1.1.4 Vetio

- 15.1.1.4.1 Business overview

- 15.1.1.4.2 Services offered

- 15.1.1.4.3 MnM view

- 15.1.1.4.3.1 Key strengths

- 15.1.1.4.3.2 Strategic choices

- 15.1.1.4.3.3 Weaknesses & competitive threats

- 15.1.1.5 TriRx Pharmaceutical Services

- 15.1.1.5.1 Business overview

- 15.1.1.5.2 Services offered

- 15.1.1.5.3 MnM view

- 15.1.1.5.3.1 Key strengths

- 15.1.1.5.3.2 Strategic choices

- 15.1.1.5.3.3 Weaknesses & competitive threats

- 15.1.1.6 Indian Immunologicals Ltd.

- 15.1.1.6.1 Business overview

- 15.1.1.6.2 Services offered

- 15.1.1.7 Recipharm AB

- 15.1.1.7.1 Business overview

- 15.1.1.7.2 Services offered

- 15.1.1.7.3 Recent developments

- 15.1.1.7.3.1 Technology launches

- 15.1.1.7.3.2 Deals

- 15.1.1.7.3.3 Expansions

- 15.1.1.7.3.4 Other developments

- 15.1.1.8 LABIANA

- 15.1.1.8.1 Business overview

- 15.1.1.8.2 Services offered

- 15.1.1.8.3 Recent developments

- 15.1.1.8.3.1 Other developments

- 15.1.1.9 Syngene International Limited

- 15.1.1.9.1 Business overview

- 15.1.1.9.2 Services offered

- 15.1.1.9.3 Recent developments

- 15.1.1.9.3.1 Deals

- 15.1.1.9.3.2 Other developments

- 15.1.1.10 CZ Vaccines

- 15.1.1.10.1 Business overview

- 15.1.1.10.2 Services offered

- 15.1.1.1 Argenta Holdco Limited

- 15.1.2 OTHER PLAYERS

- 15.1.2.1 AB7 Group

- 15.1.2.2 Kela Health

- 15.1.2.3 Eirgen Pharma

- 15.1.2.4 Bioingenium

- 15.1.2.5 Elise Biopharma

- 15.1.1 KEY PLAYERS

- 15.2 CONTRACT RESEARCH ORGANIZATIONS

- 15.2.1 KEY PLAYERS

- 15.2.1.1 Labcorp

- 15.2.1.1.1 Business overview

- 15.2.1.1.2 Services offered

- 15.2.1.1.3 Recent developments

- 15.2.1.1.3.1 Technology launches

- 15.2.1.1.3.2 Expansions

- 15.2.1.1.4 MnM view

- 15.2.1.1.4.1 Key strengths

- 15.2.1.1.4.2 Strategic choices

- 15.2.1.1.4.3 Weaknesses & competitive threats

- 15.2.1.2 Eurofins Scientific

- 15.2.1.2.1 Business overview

- 15.2.1.2.2 Services offered

- 15.2.1.2.3 Recent developments

- 15.2.1.2.3.1 Deals

- 15.2.1.2.4 MnM view

- 15.2.1.2.4.1 Key strengths

- 15.2.1.2.4.2 Strategic choices

- 15.2.1.2.4.3 Weaknesses & competitive threats

- 15.2.1.3 Charles River Laboratories

- 15.2.1.3.1 Business overview

- 15.2.1.3.2 Services offered

- 15.2.1.3.3 MnM view

- 15.2.1.3.3.1 Key strengths

- 15.2.1.3.3.2 Strategic choices

- 15.2.1.3.3.3 Weaknesses & competitive threats

- 15.2.1.4 Knoell Germany GmbH

- 15.2.1.4.1 Business overview

- 15.2.1.4.2 Services offered

- 15.2.1.4.3 Recent developments

- 15.2.1.4.3.1 Deals

- 15.2.1.4.4 Other developments

- 15.2.1.4.5 MnM view

- 15.2.1.4.5.1 Key strengths

- 15.2.1.4.5.2 Strategic choices

- 15.2.1.4.5.3 Weaknesses & competitive threats

- 15.2.1.5 Evotec

- 15.2.1.5.1 Business overview

- 15.2.1.5.2 Services offered

- 15.2.1.5.2.1 Deals

- 15.2.1.5.3 MnM view

- 15.2.1.5.3.1 Key strengths

- 15.2.1.5.3.2 Strategic choices

- 15.2.1.5.3.3 Weaknesses & competitive threats

- 15.2.1.6 KLIFOVET GmbH

- 15.2.1.6.1 Business overview

- 15.2.1.6.2 Services offered

- 15.2.1.7 Clinglobal

- 15.2.1.7.1 Business overview

- 15.2.1.7.2 Services offered

- 15.2.1.7.3 Recent developments

- 15.2.1.7.3.1 Service launches

- 15.2.1.7.3.2 Deals

- 15.2.1.7.3.3 Other developments

- 15.2.1.8 BioAgile Therapeutics Private Limited

- 15.2.1.8.1 Business overview

- 15.2.1.8.2 Services offered

- 15.2.1.9 Vetspin SRL

- 15.2.1.9.1 Business overview

- 15.2.1.9.2 Services offered

- 15.2.1.10 Veterinary Research Management

- 15.2.1.10.1 Business overview

- 15.2.1.10.2 Services offered

- 15.2.1.1 Labcorp

- 15.2.2 OTHER PLAYERS

- 15.2.2.1 Ridgeway Research Ltd.

- 15.2.2.2 Lohlein and Wolf Vet Research

- 15.2.2.3 Cebiphar

- 15.2.2.4 OCRvet

- 15.2.2.5 East Tennessee Clinical Research, Inc.

- 15.2.1 KEY PLAYERS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.2 RESEARCH METHODOLOGY DESIGN

- 16.2.1 SECONDARY DATA

- 16.2.1.1 Key data from secondary sources

- 16.2.2 PRIMARY DATA

- 16.2.2.1 Key data from primary sources

- 16.2.2.2 Key industry insights

- 16.2.1 SECONDARY DATA

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 BOTTOM-UP APPROACH

- 16.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 16.5 MARKET SHARE ESTIMATION

- 16.5.1 RESEARCH ASSUMPTIONS

- 16.5.2 GROWTH RATE ASSUMPTIONS

- 16.6 RISK ASSESSMENT

- 16.7 RESEARCH LIMITATIONS

- 16.7.1 METHODOLOGY-RELATED LIMITATIONS

- 16.7.2 SCOPE-RELATED LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.3.1 SERVICE ANALYSIS

- 17.3.2 COMPANY INFORMATION

- 17.3.3 GEOGRAPHIC ANALYSIS

- 17.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 17.3.5 COUNTRY-LEVEL VOLUME ANALYSIS, BY PRODUCT TYPE

- 17.3.6 MARKET SHARE ANALYSIS, BY SERVICE (TOP 5 PLAYERS)

- 17.3.7 ANY CONSULT/CUSTOM REQUIREMENTS AS PER CLIENT REQUESTS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS