|

시장보고서

상품코드

1993559

화재 차단재 시장 : 유형별, 용도별, 최종 이용 산업별, 지역별 - 세계 예측(-2030년)Fire Stopping Materials Market by Type, Application, End-use Industry, and Region - Global Forecast to 2030 |

||||||

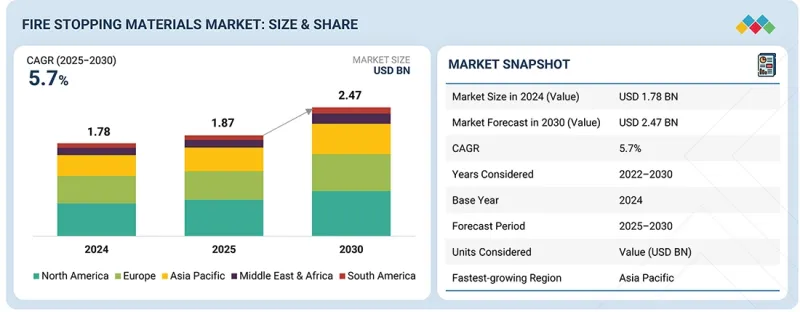

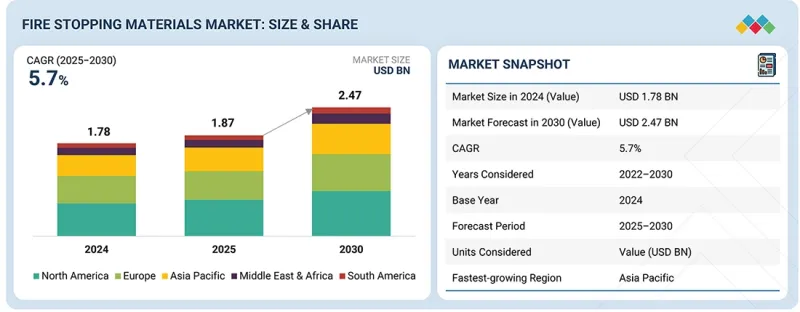

세계의 화재 차단재 시장 규모는 2025년에 추정 18억 7,000만 달러이며, 2030년까지 24억 7,000만 달러에 달할 것으로 예측되며, 2025-2030년에 CAGR로 5.7%의 성장이 전망됩니다.

화재 차단재 시장의 성장에 기여하는 요인 중 하나는 주거용, 상업용, 산업용 건축물 등 다양한 건물에서 엄격한 방화기준을 채택하고 있다는 점입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만 달러 |

| 부문 | 유형, 용도, 최종 이용 산업 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

전 세계 정부 및 각종 규제기관은 화재 위험을 최소화하기 위해 엄격한 건축 기준과 방화 규정을 시행하고 있습니다. 이러한 방화규정에서는 화재나 연기, 유독가스의 연소를 방지하기 위해 건물에 수동적 방화시스템을 설치하도록 요구하고 있습니다. 각 도시의 건설 활동이 활발해지고 고층 건물이 증가함에 따라, 현재는 건물 건설에 있어 방화 기준과 규정을 준수하도록 의무화되어 있습니다.

"금액 기준으로는 배관 부문이 예측 기간 동안 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다."

배관 부문은 신축 주택, 상업용 및 산업용 건물에서 복잡한 배관 시스템에 대한 수요 증가로 인해 화재 차단재 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 건축물의 벽이나 바닥의 배관 관통은 일반적으로 화재 연소 및 연기의 위험을 초래하기 때문에 내화성을 유지하고 건물의 안전을 보장하기 위해 방염 방수 솔루션이 필요합니다. 고층 건물과 화재 안전 기준 준수 또한 이 시장을 촉진하는 요인으로 작용하고 있습니다.

"금액 기준으로는 산업 부문이 예측 기간 동안 두 번째로 높은 CAGR을 기록할 것으로 보입니다."

이는 제조공장, 발전소, 석유 및 가스 플랜트, 창고 등 산업시설에서 화재 안전에 대한 중요성이 높아지고 있기 때문입니다. 이러한 시설에는 화재나 연기의 연소 경로가 될 수 있는 복잡한 케이블 트레이, 배관, 기계설비 관통부가 존재합니다. 산업시설의 수가 증가하고 규모가 확대되는 한편, 방화규제가 강화됨에 따라 이러한 시설에 화재 차단재 채택이 증가하고 있습니다.

"금액 기준으로는 중동 및 아프리카가 예측 기간 동안 두 번째로 높은 CAGR을 기록할 것으로 보입니다."

중동 및 아프리카는 화재 차단재 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 이는 주로 높은 도시화율과 인프라 개발의 진행과 더불어 상업시설과 주택 건설 및 개발에 대한 투자가 증가하고 있기 때문입니다. 사우디아라비아, 아랍에미리트, 카타르 등의 국가에서는 스마트 시티, 고층빌딩, 공항, 산업시설이 빠르게 개발되고 있으며, 이는 소방안전 분야의 최적의 솔루션에 대한 수요 증가로 이어질 것으로 예상됩니다. 또한, 화재 안전 기준의 제정과 준수 필요성에 대한 인식이 높아지면서 화재 차단재 사용을 촉진하고 있습니다.

세계의 화재 차단재 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 채용에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 화재 차단재 시장 : 유형별

제10장 화재 차단재 시장 : 용도별

제11장 화재 차단재 시장 : 최종 이용 산업별

제12장 화재 차단재 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.04.15The fire stopping materials market is estimated at USD 1.87 billion in 2025 and is projected to reach USD 2.47 billion by 2030, at a CAGR of 5.7% from 2025 to 2030. One of the key factors contributing to the growth of the fire stopping materials market is the increasing adoption of stringent fire safety norms in various buildings, such as residential, commercial, and industrial structures.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) |

| Segments | Type, Application, End-use Industry |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

Governments and various regulatory bodies across the world are enforcing strict building codes and fire safety regulations to ensure that fire safety risks are reduced to a minimum. Such fire safety regulations require passive fire protection systems to be installed in buildings to prevent the spread of fire, smoke, and toxic gases. With an increase in construction activities in various cities and a rise in the number of high-rise buildings, it is now mandatory to adhere to fire safety norms and regulations while constructing buildings.

"In terms of value, plumbing is expected to register the second-highest CAGR during the forecast period."

The plumbing segment is expected to witness the second-highest CAGR in the fire stopping materials market, driven by the rising demand for complex piping systems in new residential, commercial, and industrial structures. Pipe penetrations in walls and floors of structures are common, creating fire spread and smoke hazards, thereby necessitating fire stopping solutions to maintain fire resistance and ensure safe structures. High-rise structures and fire safety compliance are other factors driving this market.

"In terms of value, the industrial segment is expected to register the second-highest CAGR during the forecast period."

The industrial segment is expected to record the second-highest CAGR in the market for fire stopping materials. This is due to growing emphasis on fire safety in industrial facilities such as manufacturing plants, power plants, oil and gas plants, and warehouses. Such facilities have complex cable trays, pipes, and mechanical penetrations that are potential pathways for fire and smoke spread. As industrial facilities are growing in number and becoming larger in scale, along with increasing regulations for fire protection, there is a growing adoption of fire stopping materials in such facilities.

"In terms of value, the Middle East & Africa is expected to register the second-highest CAGR during the forecast period."

The Middle East & African region is expected to record the second-highest CAGR in the fire stopping materials market, mainly because of the high rate of urbanization and the development of infrastructure, along with the growing investments in building and constructing commercial and residential properties. Countries such as Saudi Arabia, the UAE, and Qatar are rapidly developing smart cities, high-rise buildings, airports, and industrial facilities, which will lead to the growing demand for the best solutions in the field of fire safety. Moreover, the rising awareness of the need for building and adhering to the standards of fire safety has resulted in the use of fire stopping materials.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

- By Designation: C-level - 33%, Director-level - 33%, and Managers - 34%

- By Region: North America - 15%, Europe - 25%, Asia Pacific - 30%, the Middle East & Africa - 20%, and South America - 10%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market include Hilti Corporation (Liechtenstein), 3M (US), Sika AG (Switzerland), Etex Group (Belgium), RPM International Inc. (US), Armacell (Luxembourg), Specified Technologies Inc. (US), Quelfire (UK), Fischer Group (Germany), ROCKWOOL Group (Denmark), Owens Corning (Finland), ZAPP-ZIMMERMANN GmbH (Germany), TGroup (Australia), BOSS Passive Fire (Australia), Saverto Holding GmbH (Germany), and Tenmat Ltd (UK).

Research Coverage

This research report categorizes the fire stopping materials market by type (mortar, sealants, cast-in devices, boards, putty and putty pads, collars, wraps/strips, other types), application (electrical, mechanical, plumbing, other applications), end-use industry (commercial, industrial, residential), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the fire stopping materials market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions and services, key strategies, and recent developments in the fire stopping materials market. This report includes a competitive analysis of upcoming startups in the fire stopping materials market ecosystem.

Reasons to buy this report

The report will help leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall fire stopping materials market and the subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Increasing fire safety regulations, Growth in MEP installations), restraints (Frequent cable re-penetration and airflow management), opportunities (Stringent fire regulations in Middle East to boost demand for fire stopping materials), and challenges (Non-compliance with regulations in emerging markets) influencing the growth of the fire stopping materials market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the fire stopping materials market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the fire stopping materials market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the fire stopping materials market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like Hilti Corporation (Liechtenstein), 3M (US), Sika AG (Switzerland), Etex Group (Belgium), RPM International Inc. (US), Armacell (Luxembourg), Specified Technologies Inc. (US), Quelfire (UK), Fischer Group (Germany), ROCKWOOL Group (Denmark), Owens Corning (Finland), ZAPP-ZIMMERMANN GmbH (Germany), TGroup (Australia), BOSS Passive Fire (Australia), Saverto Holding GmbH (Germany), and Tenmat Ltd (UK).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FIRE STOPPING MATERIALS MARKET

- 3.2 FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY AND REGION

- 3.3 FIRE STOPPING MATERIALS MARKET, BY TYPE

- 3.4 FIRE STOPPING MATERIALS MARKET, BY APPLICATION

- 3.5 FIRE STOPPING MATERIALS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing fire safety regulations

- 4.2.1.2 Rising fire incidents and property loss driving demand for fire stopping materials

- 4.2.1.3 Growth in MEP installations to drive market

- 4.2.1.4 Industrial expansion in Asia Pacific and Middle East

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost sensitivity and budget constraints in construction projects

- 4.2.2.2 Frequent cable re-penetration and airflow management challenges in data centers

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of innovative fire stopping systems

- 4.2.3.2 Stringent fire regulations in Middle East to boost fire stopping materials demand

- 4.2.3.3 Growing retrofit & renovation activities of existing buildings

- 4.2.3.4 Growth of data centers & mission-critical facilities

- 4.2.3.5 Increasing demand for passive fire protection systems

- 4.2.4 CHALLENGES

- 4.2.4.1 Non-compliance with regulations in emerging markets

- 4.2.4.2 Technical complexity in installing fire stopping systems

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN FIRE STOPPING MATERIALS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN CONSTRUCTION INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 321410)

- 5.6.2 EXPORT SCENARIO (HS CODE 321410)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 HILTI: ADVANCING FIRE STOPPING SOLUTIONS THROUGH PRODUCT INNOVATION AND PARTNERSHIPS

- 5.10.2 SPECIFIED TECHNOLOGIES' SPECSEAL FIRESTOP BLOCK PRODUCT LAUNCH

- 5.10.3 FSI PROMAT'S PARAFLAM ULTRA SLAB EDGE FIRE STOP SYSTEM LAUNCH

- 5.11 IMPACT OF 2025 US TARIFF ON FIRE STOPPING MATERIALS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INTUMESCENT TECHNOLOGY

- 6.1.2 ENDOTHERMIC TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CHEMICAL SUPPRESSION

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPE

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS OF PATENTS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 LIST OF PATENTS BY HILTI AG

- 6.5 FUTURE APPLICATIONS

- 6.5.1 NEXT-GENERATION INTUMESCENT SEALANTS: HIGH-RISE AND MEGA INFRASTRUCTURE

- 6.5.2 LOW-VOC AND SUSTAINABLE FIRESTOP SOLUTION: GREEN BUILDINGS APPLICATIONS

- 6.5.3 CAST-IN AND PREFAB FIRESTOP SYSTEMS FOR MODULAR CONSTRUCTION

- 6.5.4 FIRESTOP BARRIERS FOR FACADE AND BUILDING ENVELOPE PROTECTION

- 6.5.5 SMART AND DIGITALLY INTEGRATED FIRESTOP ECOSYSTEMS

- 6.6 IMPACT OF AI/GEN AI ON FIRE STOPPING MATERIALS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN FIRE STOPPING MATERIALS PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN FIRE STOPPING MATERIALS MARKET

- 6.6.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN FIRE STOPPING MATERIALS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 HILTI GROUP: AI-ENABLED R&D, FORMULATION, AND PROCESS OPTIMIZATION

- 6.7.2 ATKINSREALIS: AI-DRIVEN DESIGN ASSISTANCE AND FIELD EXECUTION

- 6.7.3 EQUINIX: LIFECYCLE FIRESTOP MANAGEMENT AND COMPLIANCE

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF STAINLESS STEEL METAL POWDER

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF STAINLESS STEEL METAL POWDER

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 FIRE STOPPING MATERIALS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 MORTAR

- 9.2.1 LOW COST SIGNIFICANTLY DRIVING CONSUMPTION OF MORTARS

- 9.3 SEALANTS

- 9.3.1 HIGH VERSATILITY AND COMPATIBILITY WITH VARIOUS BASE MATERIALS BOOSTING DEMAND FOR SEALANTS

- 9.4 CAST-IN DEVICES

- 9.4.1 EASY INSTALLATION SPURRING DEMAND FOR CAST-IN DEVICES

- 9.5 BOARDS

- 9.5.1 GROWTH OF HVAC INDUSTRY AND NEED FOR EFFICIENT VENTILATION POSITIVELY INFLUENCING BOARDS DEMAND

- 9.6 PUTTY AND PUTTY PADS

- 9.6.1 RISING ELECTRICAL BOX INSTALLATIONS IN HIGH-DENSITY BUILDINGS

- 9.7 COLLARS

- 9.7.1 STRINGENT CODE COMPLIANCE FOR SERVICE PENETRATIONS

- 9.8 WRAPS/STRIPS

- 9.8.1 PROPERTY OF BLOCKING HEAT AND TOXIC BY-PRODUCTS DRIVING DEMAND FOR WRAPS/STRIPS

- 9.9 OTHER TYPES

- 9.9.1 PILLOWS

- 9.9.2 SLEEVES

- 9.9.3 DISCS

- 9.9.4 COMPOSITE SHEETS

10 FIRE STOPPING MATERIALS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 ELECTRICAL

- 10.2.1 RAPID EXPANSION OF ELECTRICAL INFRASTRUCTURE AND DIGITALIZATION

- 10.3 MECHANICAL

- 10.3.1 GROWTH IN HVAC INSTALLATIONS TO DRIVE DEMAND

- 10.4 PLUMBING

- 10.4.1 RISING HIGH-RISE AND MULTI-SERVICE BUILDING CONSTRUCTION ACTIVITIES

- 10.5 OTHER APPLICATIONS

11 FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 COMMERCIAL

- 11.2.1 RAPID EXPANSION OF COMMERCIAL BUILDING CONSTRUCTION

- 11.3 INDUSTRIAL

- 11.3.1 INCREASING INVESTMENTS IN HIGH-RISK INDUSTRIAL INFRASTRUCTURE

- 11.4 RESIDENTIAL

- 11.4.1 GROWING GDP AND RISE IN RESIDUAL INCOME DRIVING RESIDENTIAL END-USE INDUSTRY

12 FIRE STOPPING MATERIALS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: FIRE STOPPING MATERIALS MARKET, BY TYPE

- 12.2.2 NORTH AMERICA: FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY

- 12.2.3 NORTH AMERICA: FIRE STOPPING MATERIALS MARKET, BY COUNTRY

- 12.2.3.1 US

- 12.2.3.1.1 Stringent fire safety standards and construction growth in US

- 12.2.3.2 Canada

- 12.2.3.2.1 Surge in major energy and mining infrastructure investments

- 12.2.3.3 Mexico

- 12.2.3.3.1 Expansion of data centers and energy infrastructure

- 12.2.3.1 US

- 12.3 EUROPE

- 12.3.1 EUROPE: FIRE STOPPING MATERIALS MARKET, BY TYPE

- 12.3.2 EUROPE: FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY

- 12.3.3 EUROPE: FIRE STOPPING MATERIALS MARKET, BY COUNTRY

- 12.3.3.1 Germany

- 12.3.3.1.1 Presence of global fire protection leaders and strict building regulations

- 12.3.3.2 UK

- 12.3.3.2.1 Stringent building fire safety regulations driving UK fire stopping materials market

- 12.3.3.3 France

- 12.3.3.3.1 Rapid industrialization driving fire stopping materials market

- 12.3.3.4 Italy

- 12.3.3.4.1 Growth in tourism and commercial construction supporting fire stopping materials demand

- 12.3.3.5 Russia

- 12.3.3.5.1 Nationwide growth in infrastructure driving market in Russia

- 12.3.3.6 Spain

- 12.3.3.6.1 Growing residential construction driving market in Spain

- 12.3.3.7 Benelux

- 12.3.3.7.1 Renovation of aging infrastructure driving fire stopping materials market

- 12.3.3.8 Rest of Europe

- 12.3.3.1 Germany

- 12.4 ASIA PACIFIC

- 12.4.1 ASIA PACIFIC: FIRE STOPPING MATERIALS MARKET, BY TYPE

- 12.4.2 ASIA PACIFIC: FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY

- 12.4.3 ASIA PACIFIC: FIRE STOPPING MATERIALS MARKET, BY COUNTRY

- 12.4.3.1 China

- 12.4.3.1.1 Expansion of green and energy-efficient buildings driving demand for fire stopping materials in China

- 12.4.3.2 Japan

- 12.4.3.2.1 Stringent fire safety regulations driving demand for fire stopping materials in Japan

- 12.4.3.3 India

- 12.4.3.3.1 Increasing urban fire risk to drive demand

- 12.4.3.4 South Korea

- 12.4.3.4.1 Stringent building safety regulations and growth of high-rise construction

- 12.4.3.5 Indonesia

- 12.4.3.5.1 Rapid urbanization and infrastructure development

- 12.4.3.6 Australia & New Zealand

- 12.4.3.6.1 Rising infrastructure and public facility development

- 12.4.3.7 Rest of Asia Pacific

- 12.4.3.1 China

- 12.5 SOUTH AMERICA

- 12.5.1 SOUTH AMERICA: FIRE STOPPING MATERIALS MARKET, BY TYPE

- 12.5.2 SOUTH AMERICA: FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY

- 12.5.3 SOUTH AMERICA: FIRE STOPPING MATERIALS MARKET, BY COUNTRY

- 12.5.3.1 Brazil

- 12.5.3.1.1 Increasing government spending on infrastructure to drive demand

- 12.5.3.2 Argentina

- 12.5.3.2.1 Growth in commercial and infrastructure construction driving demand

- 12.5.3.3 Rest of South America

- 12.5.3.1 Brazil

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MIDDLE EAST & AFRICA: FIRE STOPPING MATERIALS MARKET, BY TYPE

- 12.6.2 MIDDLE EAST & AFRICA: FIRE STOPPING MATERIALS MARKET, BY END-USE INDUSTRY

- 12.6.3 MIDDLE EAST & AFRICA: FIRE STOPPING MATERIALS MARKET, BY COUNTRY

- 12.6.3.1 GCC countries

- 12.6.3.1.1 UAE

- 12.6.3.1.1.1 Rapid high-rise construction and smart city projects

- 12.6.3.1.2 Saudi Arabia

- 12.6.3.1.2.1 Mega construction projects under Vision 2030 driving demand

- 12.6.3.1.3 Rest of GCC Countries

- 12.6.3.1.1 UAE

- 12.6.3.2 South Africa

- 12.6.3.2.1 Economic growth after decades of political turmoil largely boosting market growth

- 12.6.3.3 Rest of Middle East & Africa

- 12.6.3.1 GCC countries

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS

- 13.5 BRAND/PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Type footprint

- 13.6.5.4 Application footprint

- 13.6.5.5 End-use industry footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.7.5.1 Competitive benchmarking of key startups/SMEs

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 DEALS

- 13.9.2 EXPANSIONS

- 13.9.3 PRODUCT LAUNCHES

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 HILTI CORPORATION

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 MnM view

- 14.1.1.3.1 Right to win

- 14.1.1.3.2 Strategic choices

- 14.1.1.3.3 Weaknesses and competitive threats

- 14.1.2 3M

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 MnM view

- 14.1.2.3.1 Right to win

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses and competitive threats

- 14.1.3 SIKA AG

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.3.2 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 ETEX GROUP

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 RPM INTERNATIONAL INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 ARMACELL

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Expansions

- 14.1.7 SPECIFIED TECHNOLOGIES INC

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.8 QUELFIRE

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.9 FISCHER GROUP

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.10 ROCKWOOL GROUP

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.11 OWENS CORNING (PAROC)

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.12 ZAPP-ZIMMERMANN GMBH

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.13 TGROUP

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.14 BOSS PASSIVE FIRE

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.15 SAVERTO HOLDING GMBH

- 14.1.15.1 Business overview

- 14.1.15.2 Products/Solutions/Services offered

- 14.1.16 TENMAT LTD

- 14.1.16.1 Business overview

- 14.1.16.2 Products/Solutions/Services offered

- 14.1.1 HILTI CORPORATION

- 14.2 OTHER PLAYERS

- 14.2.1 WALRAVEN

- 14.2.2 EVERKEM DIVERSIFIED PRODUCTS

- 14.2.3 ABESCO LIMITED

- 14.2.4 RWC (HOLDRITE)

- 14.2.5 UNIQUE FIRE STOP PRODUCTS INC.

- 14.2.6 INTERNATIONAL CARBIDE TECHNOLOGY CO., LTD

- 14.2.7 RECTORSEAL

- 14.2.8 AL MUQARRAM INDUSTRY LLC

- 14.2.9 ASHARAM ENGINEERING & FIRESTOP SYSTEM (P) LTD.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key primary interview participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 15.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS