|

시장보고서

상품코드

2007701

인물 식별 시장 예측(-2031년) : 제품(소모품, 기기, 소프트웨어), 기술, 용도, 최종사용자별Human Identification Market by Product (Consumables, Instruments, Software), Technology, Application, End User - Global Forecast to 2031 |

||||||

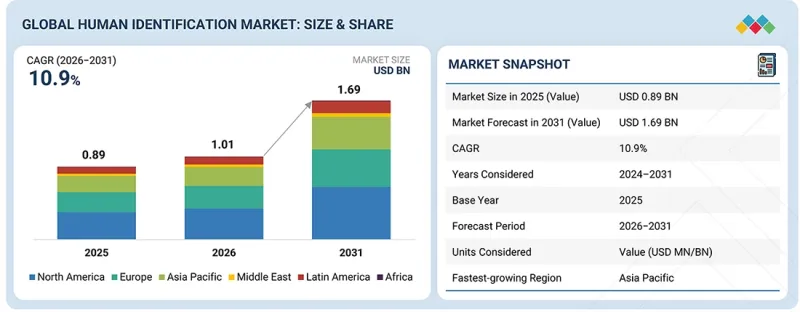

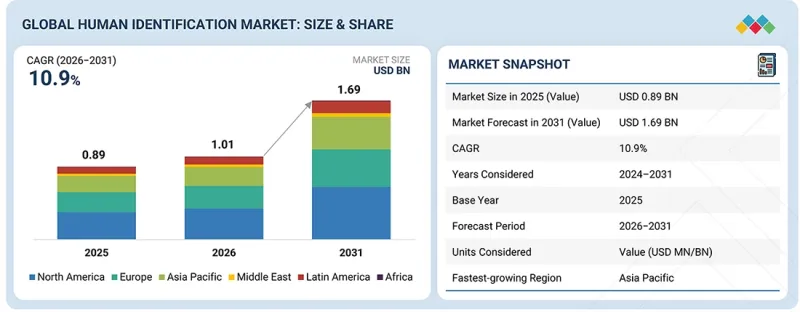

세계의 인물 식별 시장 규모는 2026년 10억 1,000만 달러에서 2031년까지 16억 9,000만 달러에 달할 것으로 예측되고 있으며, 2026-2031년 CAGR은 10.9%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 기술, 용도, 최종사용자별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

전 세계 신원 확인 시장은 법의학 미처리 건수 증가와 데이터베이스의 확충, 조사실에서의 신속한 DNA 검사 도입으로 인해 지속적으로 확대되고 있습니다.

"DNA 증폭 키트 및 시약 부문이 2025년 가장 큰 점유율을 차지했습니다. "

소모품 시장은 DNA 증폭 키트 및 시약, 신속 DNA 분석 키트 및 시약, DNA 정량 키트 및 시약, DNA 추출 키트 및 시약으로 분류됩니다. DNA 증폭 키트 및 시약 부문은 법의학 및 친자감정 분야에서 여전히 표준이 되고 있는 STR 기반 DNA 프로파일링 워크플로우에서 핵심적인 역할을 하고 있으므로 소모품 시장에서 가장 큰 점유율을 차지했습니다. 이 키트는 처리되는 모든 DNA 샘플에 필요하므로 실험실 전체에서 가장 많이 사용되는 소모품이 되었습니다. 또한 이러한 높은 점유율은 국가 DNA 데이터베이스(CODIS 등)에서 검증된 STR 키트의 광범위한 채택, 법의학적 사례의 증가, 다양한 시료 유형에 걸쳐 높은 처리량과 신뢰할 수 있는 DNA 증폭에 대한 요구가 지원하고 있습니다. 다른 소모품에 비해 증폭 키트는 1회당 검사 단가가 높고, 지속적인 수요가 있으며, 시장의 선도적 지위를 더욱 공고히 하고 있습니다.

"샘플 준비 및 추출 부문이 2025년 가장 큰 점유율을 차지할 것으로 예상됩니다. "

기기 부문은 시료 전처리 및 추출 시스템, DNA 증폭 시스템, DNA 분석 시스템, DNA 정량 시스템으로 분류됩니다. 2025년에는 시료 준비 및 추출 시스템이 가장 큰 점유율을 차지했습니다. 이 부문이 우위를 유지하는 주요 이유는 DNA 추출이 모든 DNA 분석 워크플로우에서 첫 번째이자 필수적인 단계로서 중요한 역할을 하고 있으며, 정확한 다운스트림 공정 결과를 얻기 위해서는 고품질의 불순물이 없는 DNA가 필요하기 때문입니다.

"아시아태평양이 2026-2031년 가장 높은 CAGR을 기록했습니다. "

이러한 급격한 성장은 중국, 인도, 일본의 의료 인프라의 급속한 확장, 범죄율의 증가, 법의학 연구소의 증가, 인물 식별 및 법의학에 대한 의식의 향상 캠페인 및 회의의 실시에 의해 주도되고 있습니다.

세계의 인물 식별(Person Identification) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 인물 식별 시장 : 제품별

제10장 인물 식별 시장 : 기술별

제11장 인물 식별 시장 : 용도별

제12장 인물 식별 시장 : 최종사용자별

제13장 인물 식별 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.04.29The global human identification market is projected to reach USD 1.69 billion by 2031 from USD 1.01 billion in 2026, at a CAGR of 10.9% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Product, Technology, Application, and End User |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa |

The expansion of the global human identification market has been fueled by rising forensic case backlogs and databank expansions, as well as the adoption of rapid DNA testing in booking stations.

In 2025, the DNA amplification kits & reagents segment held the largest share of the global human identification consumables market.

The consumables market is segmented into DNA amplification kits & reagents, rapid DNA analysis kits & reagents, DNA quantification kits & reagents, and DNA extraction kits & reagents. The DNA amplification kits & reagents segment held the largest share of the consumables market due to their central role in STR-based DNA profiling workflows, which remain the gold standard in forensic and paternity testing applications. These kits are required for every DNA sample processed, making them the most frequently used consumables across laboratories. Additionally, the large share is driven by the widespread adoption of validated STR kits in national DNA databases (such as CODIS), the increasing volume of forensic casework, and the need for high-throughput, reliable DNA amplification across various sample types. Compared to other consumables, amplification kits carry a higher per-test value and recurring demand, further contributing to their leading market position.

"The sample preparation & extraction segment accounted for the largest share of the global human identification instruments market in 2025."

Within the instruments segment, the global human identification market is divided into sample preparation & extraction systems, DNA amplification systems, DNA analysis systems, and DNA quantification systems. In 2025, sample preparation & extraction systems accounted for the largest share of the global human identification instruments market. The dominance of this segment is mainly due to the critical role of DNA extraction as the first and essential step in all DNA analysis workflows, where high-quality and contaminant-free DNA is required for accurate downstream results.

The APAC registered the highest CAGR from 2026 to 2031.

The human identification market is segmented into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. The APAC region is projected to grow at the highest CAGR during the forecast period. This surge is driven by the rapid expansion of healthcare infrastructure in China, India, and Japan, alongside rising crime rates, an increasing number of forensic laboratories, and the implementation of awareness campaigns and conferences on human identification and forensic sciences.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side (70%) and Demand Side (30%)

- By Designation: Managers (45%), CXOs & Directors (30%), and Executives (25%)

- By Region: North America (40%), Europe (25%), the Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

List of Key Companies Profiled in the Report:

Key players in the global human identification market include Thermo Fisher Scientific Inc. (US), QIAGEN N.V. (Netherlands), Promega Corporation (US), Hamilton Company (US), ANDE Corporation (US), FUJIFILM Wako Pure Chemical Corporation (Japan), AutoGen Inc. (US), InnoGenomics Technologies, LLC (US), Oxford Nanopore Technologies Plc (UK), Bode Cellmark Forensics Inc. (US), Bio-Rad Laboratories, Inc. (US), ZEISS (Germany), Cybergenetics, Inc. (US), MACHEREY-NAGEL GmbH & Co. KG (Germany), and BIOTYPE GmbH (Germany).

Research Coverage:

This research report categorizes the global human identification market by product (consumables, instruments, and software), technology (polymerase chain reaction, capillary electrophoresis, next-generation sequencing, microarrays, and rapid DNA analysis), application (forensic applications, paternity testing, and other applications), end user (forensic laboratories, research centers and academic & government institutes, and other end users), and region (North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the human identification market. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products, solutions, key strategies, collaborations, partnerships, and agreements.

Key Benefits of Buying the Report:

The report will help market leaders and new entrants by providing the closest approximations of revenue for the overall human identification market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their businesses and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide information on key drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers [rising forensic case backlog and expansion of DNA databases, adoption of rapid DNA technologies in booking stations, transition toward NGS in complex casework & DVI, and increased accreditation & quality standards (ISO 17025)], restraints (government budget constraints & forensic funding, slow replacement cycle of CE & PCR systems, price pressure on STR kits, and limited rapid DNA regulatory acceptance in some regions), opportunities (probabilistic genotyping adoption, automation of extraction workflows, NGS panel expansion for kinship & forensic genealogy, and emerging market forensic infrastructure build-out), and challenges (declining reagent usage due to direct-PCR kits, migration from CE to NGS reduces CE dominance, legal challenges/privacy concerns, and high cost of NGS validation & accreditation).

- Product Development/Innovation: Detailed insights on upcoming technologies and research & development activities in the global human identification market.

- Market Development: Comprehensive information about lucrative markets. The report analyzes the market across varied regions.

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the global human identification market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/approvals, acquisitions, partnerships, agreements, collaborations, other recent developments, investments & funding activities, brand/product comparative analysis, and vendor valuation & financial metrics of the global human identification market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.4 INCLUSIONS & EXCLUSIONS

- 1.4.1 YEARS CONSIDERED

- 1.4.2 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN HUMAN IDENTIFICATION MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 HUMAN IDENTIFICATION MARKET OVERVIEW

- 3.2 NORTH AMERICA: HUMAN IDENTIFICATION MARKET, BY PRODUCT

- 3.3 HUMAN IDENTIFICATION MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 HUMAN IDENTIFICATION MARKET SHARE, BY END USER, 2026 VS. 2031 (%)

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising forensic case backlog and expansion of DNA databases

- 4.2.1.2 Adoption of rapid DNA technologies in booking stations

- 4.2.1.3 Transition toward NGS in complex casework & DVI

- 4.2.1.4 Increased accreditation & quality standards (ISO 17025)

- 4.2.2 RESTRAINTS

- 4.2.2.1 Government budget constraints & forensic funding

- 4.2.2.2 Slow replacement cycle of CE & PCR systems

- 4.2.2.3 Price pressure on STR kits

- 4.2.2.4 Limited rapid DNA regulatory acceptance in some regions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Probabilistic genotyping adoption

- 4.2.3.2 Automation of extraction workflows

- 4.2.3.3 NGS panel expansion for kinship & forensic genealogy

- 4.2.3.4 Emerging market forensic infrastructure build-out

- 4.2.4 CHALLENGES

- 4.2.4.1 Declining reagent usage due to direct-PCR kits

- 4.2.4.2 Migration from CE to NGS reduces CE dominance

- 4.2.4.3 Legal challenges/privacy concerns

- 4.2.4.4 High cost of NGS validation & accreditation

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HUMAN IDENTIFICATION MARKET

- 5.2.4 TRENDS IN HEALTHCARE EXPENDITURE

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 EMERGING BUSINESS MODELS & ECOSYSTEM SHIFTS

- 5.7 PRICING ANALYSIS

- 5.7.1 INDICATIVE SELLING PRICE OF HUMAN IDENTIFICATION PRODUCTS, BY TYPE, 2025

- 5.7.2 INDICATIVE SELLING PRICE OF HUMAN IDENTIFICATION PRODUCTS, BY REGION, 2025

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT DATA FOR HS CODE 382200, 2021-2025

- 5.8.2 EXPORT DATA FOR HS CODE 382200, 2021-2025

- 5.8.3 IMPORT VOLUME FOR HS 382200, 2021-2025

- 5.8.4 EXPORT VOLUME FOR HS CODE 382200, 2021-2025

- 5.9 KEY CONFERENCES & EVENTS, 2026-2027

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.11 INVESTMENT & FUNDING ACTIVITY

- 5.12 CASE STUDY ANALYSIS

- 5.13 IMPACT OF 2025 US TARIFFS ON HUMAN IDENTIFICATION MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRY/REGION

- 5.13.4.1 US

- 5.13.4.2 Europe

- 5.13.4.3 Asia Pacific

- 5.13.5 IMPACT ON END-USE INDUSTRIES

- 5.13.5.1 Forensic laboratories

- 5.13.5.2 Research centers and academic & government institutes

- 5.13.5.3 Other end users

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Polymerase chain reaction (PCR)

- 6.1.1.2 Capillary electrophoresis (CE)

- 6.1.1.3 Next-generation sequencing

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Biometric identification technologies

- 6.1.2.2 Anti-spoofing & trust layers

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Digital identity & identity proofing (civil/enterprise)

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 TOP APPLICANTS/OWNERS (COMPANIES) FOR HUMAN IDENTIFICATION PRODUCT/TECHNOLOGY PATENTS, 2015-2025

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON HUMAN IDENTIFICATION MARKET

- 6.5.1 TOP USE CASES & MARKET POTENTIAL

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN HUMAN IDENTIFICATION MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEMS & IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN HUMAN IDENTIFICATION MARKET

- 6.6 SUCCESS STORIES & REAL-WORLD APPLICATIONS

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK/KEY REGULATIONS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 Japan

- 7.1.2.3.2 China

- 7.1.2.3.3 India

- 7.1.2.3.4 South Korea

- 7.1.2.4 Latin America

- 7.1.2.4.1 Brazil

- 7.1.2.5 Middle East

- 7.1.2.5.1 Saudi Arabia

- 7.1.2.1 North America

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 HUMAN IDENTIFICATION MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 DNA AMPLIFICATION KITS & REAGENTS

- 9.2.1.1 Increased demand for multiplex PCR assays to boost segmental growth

- 9.2.2 RAPID DNA ANALYSIS KITS & REAGENTS

- 9.2.2.1 Automated processing and reduced sample contamination to aid market growth

- 9.2.3 DNA QUANTIFICATION KITS & REAGENTS

- 9.2.3.1 Advancements in qPCR technology and growing need for faster human identification results to drive market growth

- 9.2.4 DNA EXTRACTION KITS & REAGENTS

- 9.2.4.1 Advancements in DNA extraction and purification technologies to propel market growth

- 9.2.1 DNA AMPLIFICATION KITS & REAGENTS

- 9.3 INSTRUMENTS

- 9.3.1 SAMPLE PREPARATION & EXTRACTION SYSTEMS

- 9.3.1.1 Complete sample traceability and high process safety to drive market growth

- 9.3.2 DNA AMPLIFICATION SYSTEMS

- 9.3.2.1 Easy replication of specific DNA regions in forensic sciences to propel segmental growth

- 9.3.3 DNA ANALYSIS SYSTEMS

- 9.3.3.1 Greater efficacy and lesser turnaround time to augment growth

- 9.3.4 DNA QUANTIFICATION SYSTEMS

- 9.3.4.1 Effective analysis of DNA integrity and detection of PCR inhibitors to boost market growth

- 9.3.1 SAMPLE PREPARATION & EXTRACTION SYSTEMS

- 9.4 SOFTWARE

- 9.4.1 RISING VOLUME OF PROCEDURES AND INCREASING COMPLEXITY OF GENETIC DATA TO DRIVE MARKET

10 HUMAN IDENTIFICATION MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 POLYMERASE CHAIN REACTION

- 10.2.1 HIGHER SENSITIVITY AND LOWER TURNAROUND TIME DURING FORENSIC INVESTIGATIONS TO PROPEL MARKET GROWTH

- 10.3 CAPILLARY ELECTROPHORESIS

- 10.3.1 ACCURATE EXAMINATION OF GENETIC MARKERS AND ESTABLISHMENT OF BIOLOGICAL LINKS TO SUPPORT GROWTH

- 10.4 NEXT-GENERATION SEQUENCING

- 10.4.1 EASY IDENTIFICATION OF MIXED DNA SAMPLES AND ANALYSIS OF COMPLEX PATERNITY CASES TO AID MARKET GROWTH

- 10.5 MICROARRAYS

- 10.5.1 RAPID AND ACCURATE ANALYSIS OF LARGE SAMPLE SETS AT LOW COSTS TO AUGMENT MARKET GROWTH

- 10.6 RAPID DNA ANALYSIS

- 10.6.1 EFFECTIVE REAL-TIME SAMPLE ANALYSIS FOR DNA PROFILE CREATION TO PROPEL MARKET GROWTH

11 HUMAN IDENTIFICATION MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 FORENSICS

- 11.2.1 INCREASING CRIME RATE TO PROPEL GROWTH

- 11.3 PATERNITY TESTING

- 11.3.1 RISING NEED TO RESOLVE LEGAL AND PERSONAL DISPUTES TO SUPPORT MARKET GROWTH

- 11.4 OTHER APPLICATIONS

12 HUMAN IDENTIFICATION MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 FORENSIC LABORATORIES

- 12.2.1 RISING CRIME RATE TO DRIVE DEMAND FOR HUMAN IDENTIFICATION SERVICES

- 12.3 RESEARCH CENTERS AND ACADEMIC & GOVERNMENT INSTITUTES

- 12.3.1 ADVANCEMENTS IN GENOMICS RESEARCH TO DRIVE MARKET

- 12.4 OTHER END USERS

13 HUMAN IDENTIFICATION MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Rising crime rates and increasing government-funded initiatives for forensic programs to boost demand

- 13.2.2 CANADA

- 13.2.2.1 Improvements in forensic laboratory infrastructure to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Stringent regulatory guidelines for forensic investigations to boost demand

- 13.3.2 UK

- 13.3.2.1 Growing availability of forensic equipment to propel market

- 13.3.3 FRANCE

- 13.3.3.1 Rising demand for tests to support market growth

- 13.3.4 ITALY

- 13.3.4.1 Advancements in DNA analysis to fuel market

- 13.3.5 SPAIN

- 13.3.5.1 Growing demand for gene expression analysis services to propel market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rising establishment of forensic databases to drive market

- 13.4.2 JAPAN

- 13.4.2.1 High demand for DNA analysis kits to drive market

- 13.4.3 INDIA

- 13.4.3.1 Rising crime rates to boost demand

- 13.4.4 AUSTRALIA

- 13.4.4.1 Increasing adoption of DNA profiling across forensic science

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Rapid modernization of national DNA infrastructure & advanced forensic technology adoption to support growth

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Scale-up of national DNA databasing to support market growth

- 13.5.2 MEXICO

- 13.5.2.1 Increasing missing-person crisis in country to boost market

- 13.5.3 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Saudi Arabia

- 13.6.1.1.1 Convergence of national genomics investment and forensic capability building to propel market

- 13.6.1.2 UAE

- 13.6.1.2.1 Move beyond routine forensic DNA testing toward higher-value model built on automation to support growth

- 13.6.1.3 Rest of GCC Countries

- 13.6.1.3.1 Steady investments in forensic infrastructure and regional standardization efforts to boost market

- 13.6.1.1 Saudi Arabia

- 13.6.2 REST OF MIDDLE EAST

- 13.6.1 GCC COUNTRIES

- 13.7 AFRICA

- 13.7.1 LARGE AND UNDERADDRESSED NEED FOR FORENSIC IDENTIFICATION OF MISSING PERSONS TO FUEL GROWTH

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 STRATEGIES ADOPTED BY KEY PLAYERS

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPETITIVE BENCHMARKING: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Product footprint

- 14.5.5.4 Technology footprint

- 14.5.5.5 Application footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.6.5.1 Detailed list of key startups/SMEs, 2025

- 14.6.5.2 Competitive benchmarking of key startups/SMEs, 2025

- 14.7 COMPANY VALUATION & FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.8 BRAND/PRODUCT COMPARISON

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 MnM view

- 15.1.1.3.1 Key strengths

- 15.1.1.3.2 Strategic choices

- 15.1.1.3.3 Weaknesses & competitive threats

- 15.1.2 QIAGEN N.V.

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches & approvals

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 PROMEGA CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches & approvals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 ANDE CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 MnM view

- 15.1.4.3.1 Key strengths

- 15.1.4.3.2 Strategic choices

- 15.1.4.3.3 Weaknesses & competitive threats

- 15.1.5 HAMILTON COMPANY

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 MnM view

- 15.1.5.3.1 Key strengths

- 15.1.5.3.2 Strategic choices

- 15.1.5.3.3 Weaknesses & competitive threats

- 15.1.6 FUJIFILM WAKO PURE CHEMICAL CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.7 AUTOGEN INC.

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.8 INNOGENOMICS TECHNOLOGIES, LLC

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.9 OXFORD NANOPORE TECHNOLOGIES PLC

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.10 BODE CELLMARK FORENSICS, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.11 BIO-RAD LABORATORIES, INC.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 ZEISS

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.13 CYBERGENETICS

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.14 MACHEREY-NAGEL GMBH & CO. KG

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.15 BIOTYPE

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.2 OTHER PLAYERS

- 15.2.1 OTHRAM INC.

- 15.2.2 GENETEK BIOPHARMA GMBH

- 15.2.3 CAROLINA BIOLOGICAL SUPPLY COMPANY

- 15.2.4 STRMIX LIMITED

- 15.2.5 NINGBO HEALTH GENE TECHNOLOGIES CO., LTD.

- 15.2.6 SOFTGENETICS

- 15.2.7 VERSATERM

- 15.2.8 GENO TECHNOLOGY INC.

- 15.2.9 COMPLETE GENOMICS INCORPORATED

- 15.2.10 BIONEER CORPORATION

- 15.2.11 ABNOVA CORPORATION

- 15.2.12 MGI TECH CO., LTD.

- 15.2.13 ULTIMA GENOMICS, INC.

- 15.2.14 ELEMENT BIOSCIENCES

- 15.2.15 SINGULAR GENOMICS SYSTEMS, INC.

- 15.2.16 WATCHMAKER GENOMICS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key primary participants

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 SEGMENTAL MARKET SIZE ESTIMATION

- 16.3 MARKET GROWTH RATE PROJECTIONS

- 16.4 FACTOR ANALYSIS

- 16.5 DATA TRIANGULATION

- 16.6 RESEARCH ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS & RISK ASSESSMENT

- 16.8 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS