|

시장보고서

상품코드

2007702

프리필드 시린지 시장 예측(-2031년) : 유형(기존형, 안전형), 소재(유리, 플라스틱), 설계(단실형, 이중실형), 용도(당뇨병, 암, 류마티스 관절염), 지역별Prefilled Syringes Market by Type (Conventional, Safety), Material (Glass Prefilled Syringe, Plastic), Design (Single-Chamber Prefilled Syringe, Dual-Chamber), Application (Diabetes, Cancer, and Rheumatoid Arthritis), & Region - Global Forecast to 2031 |

||||||

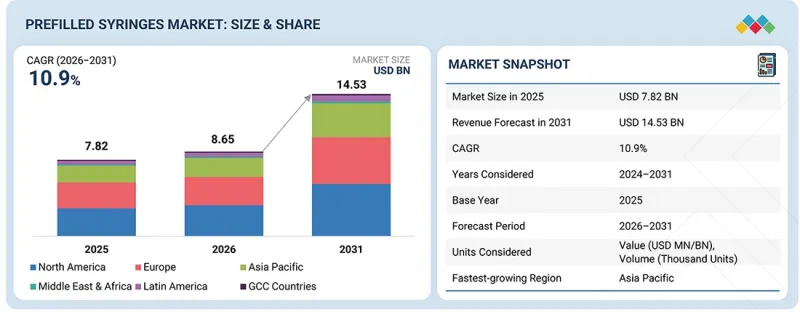

세계의 프리필드 시린지 시장 규모는 2026년 86억 5,000만 달러에서 2031년까지 145억 3,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 10.9%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 금액(달러) |

| 부문 | 유형, 소재, 디자인, 용도, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

"만성질환의 유병률 증가, 바이오의약품 및 바이오시밀러의 채택 확대, 자가 투여에 대한 수요 증가, 생명 공학 및 제약 분야의 발전이 프리필드 시린지 시장의 성장에 크게 기여하고 있습니다. "

프리필드 시린지 시장은 당뇨병, 류마티스 관절염, 심혈관 질환 등 만성질환의 유병률 증가 등 여러 요인으로 인해 강력한 성장세를 보이고 있습니다. 또한 프리필드 시린지는 즉시 사용 가능한 용량을 공급함으로써 만성질환 환자에게 정확하고 일관된 투약을 용이하게 하고, 환자의 복약 순응도를 향상시키며, 투약 오류의 가능성을 줄여줍니다. 또한 자가 투약의 증가 추세도 시장 성장에 큰 역할을 하고 있습니다. 프리필드 시린지는 복용량 측정이 필요 없어 편리함과 사용 편의성 때문에 환자들이 선호하고 있습니다. 이를 통해 안전성이 향상되고 오염의 위험도 감소합니다.

"유형별로는 기존 프리필드 시린지 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

유형별로 보면 기존 프리필드 시린지 부문은 몇 가지 요인으로 인해 시장을 독점할 것으로 예상됩니다. 즉시 사용 가능한 특성과 미리 측정된 용량은 준비 시간을 단축하고 투약 오류를 줄여 편의성과 안전성을 높입니다. 또한 첨단 안전 기능을 통해 오염 위험과 바늘에 찔리는 사고를 줄일 수 있습니다. 프리필드 시린지는 사용 편의성이 뛰어나며, 특히 만성질환에서 환자의 치료 계획 준수를 촉진하여 환자의 순응도를 향상시킵니다. 특히 생물제제 및 만성질환 치료에 대한 적응증과 함께 이러한 질환의 유병률 증가와 함께 치료 용도의 범용성은 시장 지배력을 더욱 강화하고 있습니다.

"소재별로는 유리 프리필드 시린지 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

소재별로는 유리 프리필드 시린지 부문이 프리필드 시린지 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 우수한 화학적 불활성 특성으로 약물의 안정성을 보장하고 약물과 용기의 상호 작용 위험을 감소시켜 다양한 의약품 용도에 적합합니다. 또한 유리 주사기는 투명도가 높아 약액내 이물질이나 변색을 쉽게 확인할 수 있으며, 품질관리 및 환자 안전 확보에 매우 중요합니다. 그 결과, 제약회사와 의료진들은 약액 투여의 신뢰성, 안전성, 효율성이 높아 유리 프리필드 주사기를 선호하고 있습니다.

"디자인별로 보면 단일 챔버형 프리필드 시린지 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

디자인별로는 단일 챔버 프리필드 주사기 부문이 약물 투여의 편의성, 안전성, 효율성으로 인해 가장 큰 시장 점유율을 차지했습니다. 1회 분량의 약물이 미리 채워져 있는 이 주사기는 투약 실수나 오염의 위험을 최소화하여 환자의 안전성을 높입니다. 또한 주사 과정의 효율화를 통해 의료진과 환자가 보다 빠르고 쉽게 주사할 수 있으며, 복약 순응도 및 치료 결과를 개선할 수 있습니다. 또한 다양한 치료 분야, 특히 만성질환 관리 및 응급의료 분야에서 이러한 주사기가 광범위하게 채택되면서 시장 성장을 더욱 촉진하고 있습니다.

"용도별로는 암 분야가 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

용도별로는 전 세계에서 암 유병률이 증가하고 있고, 첨단 약물전달 시스템에 대한 수요가 증가함에 따라 암 분야가 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 프리필드 시린지는 정확한 투약, 오염 위험 감소, 환자 안전 및 복약 순응도 강화 등 암 치료에 큰 이점을 제공합니다. 암 치료는 정기적이고 정확한 투약이 필요한 복잡한 투약 계획이 수반되는 경우가 많기 때문에 프리필드 시린지의 편리성과 신뢰성이 매우 중요합니다. 또한 종양 분야에서 자주 사용되는 바이오의약품과 표적 치료의 발전은 프리필드 주사기의 수요를 더욱 촉진하고 있으며, 암 분야가 이 시장의 주요 응용 분야가 되고 있습니다.

"지역별로는 북미가 가장 큰 시장 점유율을 차지할 것으로 전망"

예측 기간 중 북미는 몇 가지 요인으로 인해 프리필드 시린지 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 여기에는 잘 구축된 의료 인프라, 첨단 의료기술의 높은 보급률, 환자의 안전과 편의성에 대한 강한 관심 등이 포함됩니다. 또한 이 지역은 엄격한 품질 기준과 안전 조치를 보장함으로써 프리필드 시린지 채택을 촉진하는 강력한 규제 프레임워크의 혜택을 누리고 있습니다. 또한 정기적인 주사를 필요로 하는 만성질환의 증가와 의료비 증가도 북미 지역의 프리필드 시린지 수요 확대에 기여하고 있습니다. 대형 제약사 및 생명공학 기업의 존재는 약물전달 시스템을 개선하기 위한 광범위한 연구개발 활동을 통해 시장의 성장을 더욱 촉진하고 있습니다.

세계의 프리필드 시린지(Prefilled Syringe) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 프리필드 시린지 시장 : 유형별

제10장 프리필드 시린지 시장 : 설계별

제11장 프리필드 시린지 시장 : 소재별

제12장 프리필드 시린지 시장 : 용도별

제13장 프리필드 시린지 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

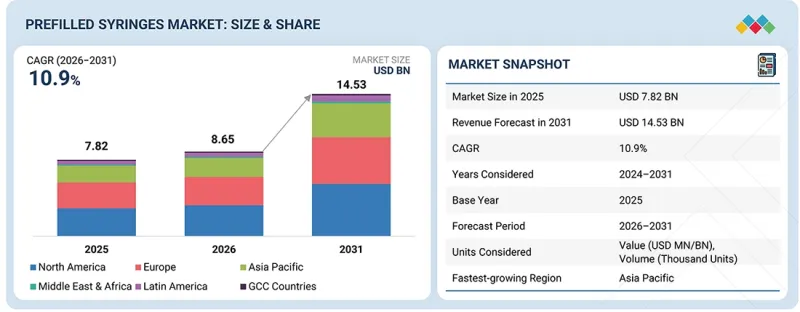

KSA 26.04.29The global prefilled syringes market is projected to reach USD 14.53 billion by 2031 from USD 8.65 billion in 2026, at a CAGR of 10.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Type, Material, Design, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and the GCC Countries |

"The increasing prevalence of chronic diseases, growing adoption of biologics and biosimilars, rising demand for self-administration, and advancements in biotechnology and pharmaceuticals contribute significantly to the growth of the prefilled syringes market."

The prefilled syringes market has had strong growth due to a number of factors such as the rising incidence of chronic diseases like diabetes, rheumatoid arthritis, and cardiovascular disorders. Moreover, prefilled syringes make it easier to administer medications precisely and consistently to patients with chronic conditions, by providing ready-to-use doses that improve patient compliance and lower the possibility of dosage errors. Additionally, the growing trend of self-administration has also played a major role in the market's growth. Prefilled syringes are preferred by patients due to their comfort and ease of use, as they eliminate the need for dose measurement, hence improving safety and lowering the danger of contamination.

"By type, the conventional prefilled syringes segment is expected to hold the largest market share in the prefilled syringes market."

Based on type, the conventional prefilled syringes segment is expected to dominate the prefilled syringes market due to several factors. Their ready-to-use nature and pre-measured doses enhance convenience and safety by reducing preparation time and dosing errors. They lower contamination risks and needlestick injuries through advanced safety features. Prefilled syringes improve patient compliance, particularly for chronic conditions, by being user-friendly and encouraging adherence to treatment regimens. Their versatility in therapeutic applications, especially for biologics and chronic disease treatments, coupled with the growing prevalence of such conditions, further drive their market dominance.

"By material, the glass prefilled syringes segment is expected to hold the largest market share in the prefilled syringes market."

Based on material, the glass prefilled syringes segment is expected to hold the largest market share in the prefilled syringes market. Their superior chemical inertness ensures drug stability and reduces the risk of interactions between the drug and the container, making them ideal for a wide range of pharmaceutical applications. Additionally, glass syringes offer high visibility, allowing for easy inspection of the drug for particulates and discoloration, which is critical for quality control and patient safety. As a result, pharmaceutical companies and healthcare providers prefer glass prefilled syringes for their reliability, safety, and efficiency in drug delivery.

"By design, the single-chamber prefilled syringes segment is expected to hold the largest market share in the prefilled syringes market."

Based on design, the single-chamber prefilled syringes segment accounted for the largest market share of the prefilled syringes market due to their convenience, safety, and efficiency in drug administration. These syringes, which come pre-loaded with a single dose of medication, minimize the risk of dosing errors and contamination, enhancing patient safety. They streamline the injection process, making it quicker and easier for healthcare providers and patients, thereby improving compliance and treatment outcomes. Moreover, their widespread adoption in various therapeutic areas, particularly in chronic disease management and emergency care, further drives growth in the market.

"By application, the cancer segment is expected to hold the largest market share in the prefilled syringes market."

By application, the cancer segment is expected to hold the largest market share due to the increasing prevalence of cancer globally and the rising need for advanced drug delivery systems. Prefilled syringes offer significant advantages for cancer treatment, including precise dosing, reduced risk of contamination, and enhanced patient safety and compliance. As cancer treatments often involve complex medication regimens requiring regular and accurate administration, the convenience and reliability of prefilled syringes become critical. Additionally, advancements in biologics and targeted therapies, which are frequently used in oncology, further drive the demand for prefilled syringes, making the cancer segment the dominant application area in this market.

"By region, North America is expected to hold the largest market share in the prefilled syringes market."

North America is expected to hold the largest share of the prefilled syringes market during the forecast period due to several factors. These include a well-established healthcare infrastructure, high adoption rates of advanced medical technologies, and a significant focus on patient safety and convenience. Moreover, the region benefits from robust regulatory frameworks that encourage the adoption of prefilled syringes by ensuring stringent quality standards and safety measures. Additionally, the increasing incidence of chronic diseases requiring regular injections, coupled with rising healthcare expenditures, contribute to the growing demand for prefilled syringes in North America. The presence of major pharmaceutical companies and biotechnology firms further enhances market growth through extensive research and development activities aimed at improving drug delivery systems.

A breakdown of the primary participants (supply side) for the prefilled syringes market referred to for this report is provided below:

- By Company Type: Tier 1 (30%), Tier 2 (35%), and Tier 3 (35%)

- By Designation: C-level Executives (20%), Directors (35%), and Others (45%)

- By Region: North America (37%), Europe (34%), Asia Pacific (22%), Latin America (5%), Middle East & Africa (2%)

Prominent players in the prefilled syringes market are BD (US), Gerresheimer AG (Germany), SCHOTT (Germany), West Pharmaceutical Services, Inc. (US), AptarGroup Inc. (US), Nipro (Japan), Baxter (US), Owen Mumford Ltd. (UK), Weigao Medical International Co., Ltd. (China), Credence MedSystems, Inc. (US), Novartis AG (Switzerland), Stevanato Group (Italy), Polymed (India), MedXL (Canada), Sharps Technology, Inc. (US), Fresenius Kabi (US), DBM S.R.L. (Italy), Taisei Kako Co., Ltd. (Japan), Shandong Province Medicinal Glass Co., Ltd. (China), SHIN YAN SHENO PRECISION INDUSTRIAL CO., LTD. (Japan), J.O. PHARMA CO., LTD. (Japan), BMIKOREA (Korea), B. Braun SE ( Germany), and Al Shifa Medical Products Co. (Saudi Arabia).

Research Coverage:

The report analyzes the prefilled syringes market and aims at estimating the market size and future growth potential of this market based on various segments such as type, material, design, application, and region. The report also includes a competitive analysis of the key players in this market along with their company profiles, service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall prefilled syringes market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (increasing chronic diseases, increasing biologics and biosimilars, and technological advancements), restraints (product recalls and stringent government regulations), opportunities (increasing preference for self-administration of injectables and increasing regulatory support), and challenges (presence of alternative drug delivery methods and infections associated with needlestick injuries)

- Market Penetration: It includes extensive information on products offered by the major players in the global prefilled syringes market. The report includes various segments in type, material, design, application, and region.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global prefilled syringes market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by type, material, design, application, and region.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global the prefilled syringes market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products, and capacities of the major competitors in the global prefilled syringes market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING PREFILLED SYRINGES MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PREFILLED SYRINGES MARKET OVERVIEW

- 3.2 PREFILLED SYRINGES MARKET, BY REGION, 2025 VS. 2030

- 3.3 ASIA PACIFIC: PREFILLED SYRINGES MARKET, BY TYPE AND COUNTRY

- 3.4 PREFILLED SYRINGES MARKET: GEOGRAPHICAL GROWTH OPPORTUNITIES

- 3.5 PREFILLED SYRINGES MARKET: DEVELOPED VS. EMERGING MARKETS

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing prevalence of chronic diseases

- 4.2.1.2 Growing adoption of self-injection devices

- 4.2.1.3 Increasing adoption of prefilled syringes in parenteral dosage forms

- 4.2.1.4 Increased use of biologics and vaccines

- 4.2.1.5 Technological advancements in prefilled syringes

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent government regulations

- 4.2.2.2 Impact of product recalls

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing preference for unit-dose medication using prefilled syringes

- 4.2.3.2 Emerging markets with growing healthcare infrastructure

- 4.2.4 CHALLENGES

- 4.2.4.1 Alternative drug delivery methods

- 4.2.4.2 Infections associated with needlestick injuries

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER- 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN PREFILLED SYRINGES MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF PREFILLED SYRINGES, BY TYPE, 2022-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF CONVENTIONAL PREFILLED SYRINGES, BY REGION, 2022-2025

- 5.6.3 AVERAGE SELLING PRICE TREND OF SAFETY PREFILLED SYRINGES, BY REGION, 2022-2025

- 5.6.4 AVERAGE SELLING PRICE TREND OF PREFILLED SYRINGES, BY KEY PLAYER, 2022-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 901831

- 5.7.2 EXPORT DATA FOR HS CODE 901831

- 5.8 KEY CONFERENCES & EVENTS, 2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ENVIRONMENTAL BENEFITS OF USING PREFILLED 'EMERGENCY' DRUGS

- 5.11.2 DEVELOPMENT OF NOVEL PHARMACEUTICAL DRUG MODALITIES REQUIRING FROZEN STORAGE AND TRANSPORTATION

- 5.12 IMPACT OF 2025 US TARIFF ON PREFILLED SYRINGES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.3.1 Impact on country/region

- 5.12.3.1.1 US

- 5.12.3.1.2 Europe

- 5.12.3.1.3 Asia Pacific

- 5.12.3.1 Impact on country/region

- 5.12.4 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Integration Disinfection Unit (IDU)

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Cyclic Olefin Polymers (COP) and Cyclic Olefin Copolymers (COC)

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Integration with autoinjectors

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM |RECENT TECHNOLOGIES| FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.2.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR PREFILLED SYRINGES

- 6.3.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.3.3 LIST OF PATENTS

- 6.4 IMPACT OF AI/GEN AI ON PREFILLED SYRINGES MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN PREFILLED SYRINGES MARKET

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.5.1 STEVANATO GROUP: AI-DRIVEN VISUAL INSPECTION FOR PREFILLED SYRINGES

- 6.5.2 SCHOTT PHARMA: AI-ENABLED SMART GLASS & DEFECT PREDICTION

- 6.5.3 GERRESHEIMER: PREDICTIVE QUALITY CONTROL IN FILL-FINISH OPERATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 PREFILLED SYRINGES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 CONVENTIONAL PREFILLED SYRINGES

- 9.2.1 DISPOSABLE PREFILLED SYRINGES

- 9.2.1.1 Increasing focus on patient safety to drive market

- 9.2.2 REUSABLE PREFILLED SYRINGES

- 9.2.2.1 Cost-effectiveness and technological advancements to drive market

- 9.2.1 DISPOSABLE PREFILLED SYRINGES

- 9.3 SAFETY PREFILLED SYRINGES

- 9.3.1 INTEGRATED SAFETY FEATURES TO BOOST ADOPTION

10 PREFILLED SYRINGES MARKET, BY DESIGN

- 10.1 INTRODUCTION

- 10.2 SINGLE-CHAMBER PREFILLED SYRINGES

- 10.2.1 CONVENIENCE, SAFETY, AND EFFICIENCY OF SINGLE-CHAMBER SYRINGES TO SUPPORT MARKET GROWTH

- 10.3 DUAL-CHAMBER PREFILLED SYRINGES

- 10.3.1 ABILITY TO MAINTAIN STABILITY, MINIMIZE DOSING ERRORS, AND MEET REGULATORY STANDARDS TO PROPEL MARKET GROWTH

- 10.4 CUSTOMIZED PREFILLED SYRINGES

- 10.4.1 EASY-TO-READ DOSAGE INDICATORS AND SAFETY MECHANISMS TO BOOST ADOPTION

11 PREFILLED SYRINGES MARKET, BY MATERIAL

- 11.1 INTRODUCTION

- 11.2 GLASS PREFILLED SYRINGES

- 11.2.1 ABILITY OF GLASS PREFILLED SYRINGES TO OFFER SUPERIOR BARRIER PROPERTIES TO BOOST MARKET GROWTH

- 11.3 PLASTIC PREFILLED SYRINGES

- 11.3.1 IMPROVED SAFETY, COST-EFFECTIVENESS, VERSATILITY, AND CONVENIENCE TO SUPPORT ADOPTION

12 PREFILLED SYRINGES MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 DIABETES

- 12.2.1 INCREASING PREVALENCE OF DIABETES TO FAVOR MARKET GROWTH

- 12.3 RHEUMATOID ARTHRITIS

- 12.3.1 RISING DEMAND FOR EFFECTIVE AND CONVENIENT TREATMENT OPTIONS TO AID MARKET GROWTH

- 12.4 ANAPHYLAXIS

- 12.4.1 CONVENIENCE OF PREFILLED SYRINGES TO ADMINISTER MEDICATION QUICKLY TO BOOST ADOPTION

- 12.5 CANCER

- 12.5.1 RISING GLOBAL CANCER RATES TO SPUR MARKET GROWTH

- 12.6 THROMBOSIS

- 12.6.1 MINIMIZED RISK OF CONTAMINATION AND INFECTION ASSOCIATED WITH PREFILLED SYRINGES TO AUGMENT MARKET DEMAND

- 12.7 OPHTHALMOLOGY

- 12.7.1 FEWER SIDE EFFECTS ASSOCIATED WITH PREFILLED SYRINGES COMPARED TO TOPICAL MEDICATIONS TO SUPPORT GROWTH

- 12.8 OTHER APPLICATIONS

13 PREFILLED SYRINGES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 US to dominate North American prefilled syringes market during forecast period

- 13.2.2 CANADA

- 13.2.2.1 Rising incidence of chronic diseases to propel market growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 High investment in healthcare R&D to foster innovation in drug delivery technologies

- 13.3.2 UK

- 13.3.2.1 Rising number of patients with cardiovascular diseases and diabetes patients to fuel market growth

- 13.3.3 FRANCE

- 13.3.3.1 Increasing incidence of needlestick injuries and growing trend of self-administration to drive market growth

- 13.3.4 SPAIN

- 13.3.4.1 Increase in biologics production to support market growth

- 13.3.5 ITALY

- 13.3.5.1 Growing focus of pharmaceutical and medical device companies on high-quality manufacturing standards to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 JAPAN

- 13.4.1.1 Increase in geriatric population to augment market growth

- 13.4.2 CHINA

- 13.4.2.1 Large diabetic population to attract pharmaceutical and drug delivery device manufacturers to Chinese market

- 13.4.3 INDIA

- 13.4.3.1 High number of cancer and diabetes cases to fuel market growth

- 13.4.4 AUSTRALIA

- 13.4.4.1 Growing healthcare expenditure and rising focus on chronic disease management to aid market growth

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Well-developed healthcare sector and presence of major pharmaceutical manufacturers to drive market

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 JAPAN

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Increasing prevalence of obesity and rising use of generic medicines to aid market growth

- 13.5.2 MEXICO

- 13.5.2.1 Rising Healthcare Investment and Pharmaceutical Expansion to propel market growth

- 13.5.3 ARGENTINA

- 13.5.3.1 Increasing geriatric population with chronic diseases to fuel demand for prefilled syringes

- 13.5.4 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 RISING CHRONIC DISEASE BURDEN AND HEALTHCARE INVESTMENTS TO BOOST MARKET

- 13.7 GCC COUNTRIES

- 13.7.1 INCREASING HEALTHCARE EXPENDITURE TO DRIVE MARKET

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY MAJOR PLAYERS IN PREFILLED SYRINGES MARKET

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Type footprint

- 14.5.5.4 Material footprint

- 14.5.5.5 Design footprint

- 14.5.5.6 Application footprint

- 14.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.6.5.1 Detailed list of key Startups/SMEs

- 14.6.5.2 Competitive benchmarking of Startups/SMEs

- 14.7 BRAND/PRODUCT COMPARISON

- 14.8 COMPANY VALUATION & FINANCIAL METRICS

- 14.8.1 FINANCIAL METRICS

- 14.8.2 COMPANY VALUATION

- 14.9 R&D EXPENDITURE

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES AND APPROVALS

- 14.10.2 DEALS

- 14.10.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 BECTON, DICKINSON AND COMPANY (BD)

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 GERRESHEIMER AG

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 SCHOTT

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 WEST PHARMACEUTICAL SERVICES, INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 APTARGROUP, INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 NIPRO

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Expansions

- 15.1.7 BAXTER (SIMTRA BIOPHARMA SOLUTIONS)

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.3.3 Expansions

- 15.1.8 OWEN MUMFORD LTD.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.9 WEIGAO MEDICAL INTERNATIONAL CO., LTD.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.10 CREDENCE MEDSYSTEMS, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.11 NOVARTIS AG

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 STEVANATO GROUP

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches

- 15.1.12.3.2 Deals

- 15.1.12.3.3 Expansions

- 15.1.13 POLYMEDICURE

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.14 AMSINO INTERNATIONAL, INC.

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 SHARPS TECHNOLOGY, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.1 BECTON, DICKINSON AND COMPANY (BD)

- 15.2 OTHER PLAYERS

- 15.2.1 FRESENIUS KABI USA

- 15.2.2 MEDEFIL, INC.

- 15.2.3 D.B.M. S.R.L.

- 15.2.4 TAISEI KAKO CO., LTD.

- 15.2.5 SHANDONG PROVINCE MEDICINAL GLASS CO., LTD.

- 15.2.6 SHIN YAN SHENO PRECISION INDUSTRIAL CO., LTD.

- 15.2.7 J.O. PHARMA CO., LTD. (OTSUKA HOLDINGS CO., LTD.)

- 15.2.8 BMI KOREA

- 15.2.9 B. BRAUN SE

- 15.2.10 AL SHIFA MEDICAL PRODUCTS CO.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key primary sources

- 16.1.2.2 Key objectives of primary research

- 16.1.2.3 Key data from primary sources

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 16.2.2 COMPANY PRESENTATIONS AND PRIMARY INTERVIEWS

- 16.2.3 TOP-DOWN APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 MARKET SHARE ESTIMATION

- 16.5 STUDY ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.6.1 METHODOLOGY-RELATED LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 RELATED REPORTS

- 17.4 AUTHOR DETAILS