|

시장보고서

상품코드

2007703

차세대 시퀀싱 시장 : 제공별, 유형별, 기술별, 워크플로우별, 최종사용자별, 용도별, 지역별 - 세계 예측(-2030년)Next-Generation Sequencing Market by Product Type (Consumables, Platforms, Bioinformatics), Technology (SBS, Nanopore), Workflow (Sequencing, Data Analysis), Services, Application (Drug Discovery, Diagnostic, Agriculture) - Global Forecast to 2030 |

||||||

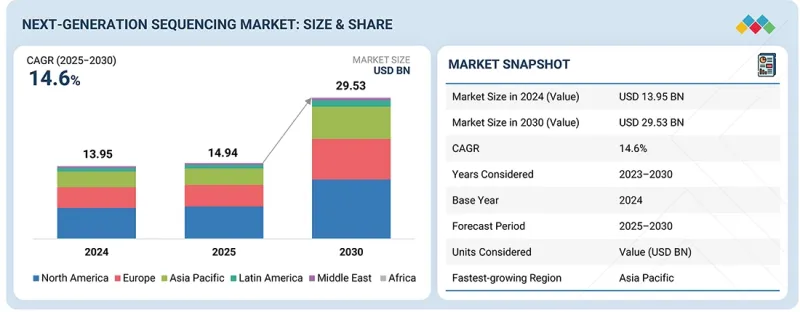

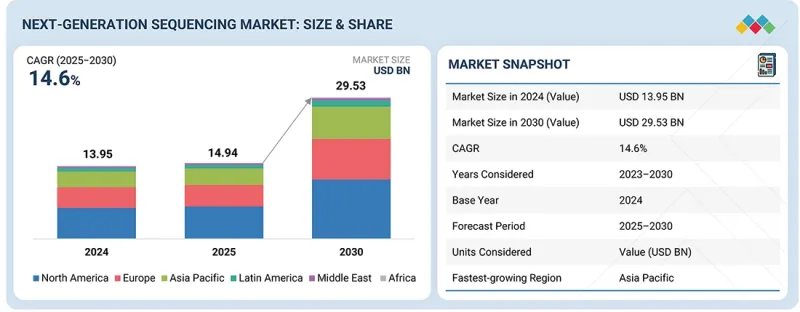

차세대 시퀀싱 시장 규모는 예측 기간 동안 CAGR 14.6%로 확대되어 2025년 149억 4,000만 달러에서 2030년에는 295억 3,000만 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제공별, 유형별, 기술별, 워크플로우별, 최종사용자별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

종양학, 감염성 질환, 생식의학, 군유전체학, 맞춤형 의료 분야에서 NGS의 적용 확대가 시장 확대의 주요 원동력이 되고 있습니다. 한편, 데이터 분석 및 해석을 위한 고급 생물정보학 도구는 NGS의 활용을 촉진하고 있으며, 이를 통해 더 많은 사용자층이 이 기술을 채택할 수 있도록 하고 있습니다.

NGS 제품 시장은 소모품, 플랫폼, 바이오인포매틱스 도구로 분류됩니다. 2024년에는 소모품이 가장 큰 비중을 차지했습니다. 이 부문에는 시약, 라이브러리 준비 키트, 시퀀싱 플로우셀, 샘플 조제 키트 등이 포함되며, 많은 응용 분야에서 대량으로 사용되고 있습니다. 장비는 일반적으로 일회성 투자인 반면, 소모품은 반복 구매가 가능하기 때문에 수요가 꾸준히 증가하고 있습니다. 타겟 시퀀스 및 커스텀 패널의 사용 확대도 특정 용도에 특화된 소모품에 대한 수요를 촉진하고 있습니다. 또한, 사용자층의 확대와 시퀀싱 화학의 지속적인 개선으로 더 많은 고객들이 워크플로우를 간소화하고 데이터 품질을 향상시키기 위해 소모품에 주목하고 있습니다.

차세대 시퀀싱 서비스 시장은 최종사용자별로 학계 및 연구기관, 제약 및 생명공학 기업, 병원 및 임상 실험실, 기타 사용자로 분류됩니다. 2024년에는 학계 및 연구기관이 가장 큰 점유율을 차지했습니다. 이러한 선도적 지위는 연구 프로그램에 대한 정부 및 민간의 강력한 자금 지원으로 뒷받침되고 있으며, 이로 인해 장비 및 소모품을 포함한 NGS 관련 수요에 대한 지출이 증가하고 있습니다. 제약 및 생명공학 기업은 시장에서 두 번째로 큰 최종사용자 부문을 차지했습니다.

아시아태평양은 대규모 인구 유전체 프로젝트와 정밀의료에 대한 수요 증가로 인해 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다. 또한, 일본, 중국 등의 국가에서 고령화에 따라 희귀질환 및 유전성 질환의 유병률이 증가하고 있습니다. 이러한 요인들은 의료 관리 및 치료에 있어 시퀀싱 기술의 도입을 촉진하고 시장 성장을 견인하고 있습니다.

본 보고서에서 다룬 기업 프로파일 목록:

- Illumina, Inc.(미국)

- Thermo Fisher Scientific Inc.(미국)

- F. Hoffmann-La Roche Ltd.(스위스)

- Danaher Corporation(미국)

- QIAGEN(네덜란드)

- Agilent Technologies, Inc.(미국)

- Revvity(미국)

- Eurofins Scientific(Luxembourg)

- PacBio(미국)

- Oxford Nanopore Technologies plc(영국)

- Takara Bio Inc. BGI Group(중국)

- Merck KGaA(독일)

- BD(미국)

- 10X Genomics(미국)

- New England Biolabs(미국)

- Promega Corporation(미국)

- Novogene(중국)

- LGC Limited(영국)

- WuXi Biologics(중국)

- MGI Tech(중국)

- Tecan Trading AG(스위스)

- Twist Biosciences(미국)

- Azenta US, Inc. GenScript(미국)

- SD Biosensor, Inc. Fulgent Genetics(미국)

- Hamilton Company(미국)

- Zymo Research Corporation(미국)

- NeoGenomics Laboratories(미국)

- Psomagen(미국)

조사 범위:

이 보고서의 조사 범위는 NGS 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 과제, 기회, 제약 등)에 대한 자세한 정보를 다룹니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 제품 및 서비스 포트폴리오, 제품 및 서비스 출시, 제휴, 파트너십, 사업 확장, 계약과 같은 주요 전략 및 NGS 시장과 관련된 최근 동향에 대한 인사이트를 제공합니다. 또한, 본 보고서는 NGS 시장 생태계의 주요 기업 및 신생 스타트업의 경쟁 분석도 다루고 있습니다.

본 보고서 구매의 주요 이점:

이 보고서는 전체 NGS 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 또한, 이해관계자들이 경쟁 상황을 더 깊이 이해하고, 자신의 비즈니스를 적절히 포지셔닝하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 본 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인 및 과제에 대한 정보를 제공합니다.

본 보고서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

시장 성장에 영향을 미치는 주요 촉진요인(시퀀싱 플랫폼의 발전, 시퀀싱의 임상 적용 확대, 정밀의학에 대한 수요 증가, 시퀀싱 비용 감소), 제약요인(복잡한 데이터 분석, 높은 초기 자본 투자), 기회요인(AI 및 ML 통합, 롱리드 시퀀싱 기술 채택, 멀티오믹스 통합에 집중), 도전요인(표준화 문제)에 대한 분석. 롱리드 시퀀싱 기술 채택, 멀티오믹스 통합에 집중), 도전과제(표준화 문제)에 대한 분석.

- 제품 개발/혁신 : 차세대 시퀀싱 시장에서 새롭게 출시되는 제품 및 서비스에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 시장을 분석합니다.

- 시장 다각화 : 차세대 시퀀싱 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보 제공

- 경쟁사 분석 : Illumina, Inc.(미국), Thermo Fisher Scientific Inc.(미국), F. Hoffmann-La Roche Ltd. Technologies, Inc.(미국), Revvity(미국), Eurofins Scientific(룩셈부르크), PacBio(미국), Oxford Nanopore Technologies plc(영국), Takara Bio Inc. Group(중국), Merck KGaA(독일), BD(미국), 10X Genomics(미국), New England Biolabs(미국), Promega Corporation(미국), Novogene(중국), LGC Limited(영국), WuXi Biologics(중국), MGI Tech(중국), Tecan Trading AG(스위스), Twist Biosciences(미국), Azenta US, Inc. Fulgent Genetics(미국), Hamilton Company(미국), Zymo Research Corporation(미국), NeoGenomics Laboratories(미국), Psomagen(미국), Psomagen(미국)

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 지속가능성과 규제 상황

제8장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제9장 차세대 시퀀싱 시장(제공별)

제10장 차세대 시퀀싱 제품 시장(유형별)

제11장 차세대 시퀀싱 플랫폼 시장(기술별)

제12장 차세대 시퀀싱 제품 시장(워크플로우별)

제13장 차세대 시퀀싱 제품 시장(최종사용자별)

제14장 차세대 시퀀싱 서비스 시장(유형별)

제15장 차세대 시퀀싱 서비스 시장(워크플로우별)

제16장 차세대 시퀀싱 서비스 시장(최종사용자별)

제17장 차세대 시퀀싱 시장(용도별)

제18장 차세대 시퀀싱 시장(지역별)

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 부록

KSM 26.04.28The next-generation sequencing market is expected to reach USD 29.53 billion in 2030, up from USD 14.94 billion in 2025, at a CAGR of 14.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product Type, Technology, Workflow, Service, Application |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

The growing application of NGS in oncology, infectious diseases, reproductive health, metagenomics, and personalized medicine is the primary driver of market expansion. Meanwhile, advanced bioinformatics tools for data analysis and interpretation are facilitating the use of NGS, thereby helping a wider user base adopt the technique.

"Consumables accounted for the largest share of the product segment in the NGS market in 2024."

The NGS products market is segmented into consumables, platforms, and bioinformatics tools. In 2024, consumables held the largest share. This segment includes reagents, library preparation kits, sequencing flow cells, and sample preparation kits, which are used in high volumes across many applications. Demand remains robust because consumables are purchased repeatedly, unlike instruments, which are generally one-time investments. The growing use of targeted sequencing and custom panels is also driving demand for specialized, application-specific consumables. Furthermore, an expanding user base and ongoing improvements in sequencing chemistries are drawing more customers toward consumables to simplify their workflows and improve data quality.

"The academic & research institutes segment accounted for the largest share by services end-user segment in the next-generation sequencing market in 2024."

The next-generation sequencing services market is segmented by end user into academic & research institutes, pharmaceutical & biotechnology companies, hospitals & clinical laboratories, and other users. In 2024, academic and research institutes held the largest share. This leadership is supported by strong government and private funding for research programs, enabling higher spending on NGS-related needs, including instruments and consumables. Pharmaceutical and biotechnology companies represented the second-largest end-user segment in the market.

"The Asia Pacific region will grow at the highest CAGR from 2025 to 2030."

The Asia Pacific region is estimated to be the fastest-growing segment of the market, owing to large-scale population genomics projects and rising demand for precision medicines. Additionally, the rising prevalence of rare and genetic diseases is attributed to the aging populations in countries such as Japan and China. These factors are supporting the adoption of sequencing technologies in healthcare management and treatment, driving market growth.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side- 70% and Demand Side 30%

- By Designation: Managers - 45% CXOs and Director-level - 30%, and Executives - 25%,

- By Region: North America -40%, Europe -25%, Asia-Pacific -25%, Latin America -5%, and Middle East -5%.

List of Companies Profiled in the Report:

- Illumina, Inc. (US)

- Thermo Fisher Scientific Inc. (US)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Danaher Corporation (US)

- QIAGEN (Netherlands)

- Agilent Technologies, Inc. (US)

- Revvity (US)

- Eurofins Scientific (Luxembourg)

- PacBio (US)

- Oxford Nanopore Technologies plc. (UK)

- Takara Bio Inc. (Japan)

- BGI Group (China)

- Merck KGaA (Germany)

- BD (US)

- 10X Genomics (US)

- New England Biolabs (US)

- Promega Corporation (US)

- Novogene Co., Ltd. (China)

- LGC Limited (UK)

- WuXi Biologics (China)

- MGI Tech Co. Ltd. (China)

- Tecan Trading AG (Switzerland)

- Twist Biosciences (US)

- Azenta US, Inc. (US)

- GenScript (US)

- SD Biosensor, Inc. (South Korea)

- Fulgent Genetics (US)

- Hamilton Company (US)

- Zymo Research Corporation (US)

- NeoGenomics Laboratories (US)

- Psomagen (US)

Research Coverage:

The scope of the report covers detailed information on the major factors, such as drivers, challenges, opportunities, and restraints, that influence the growth of the NGS market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, product and service portfolio, key strategies such as product and service launches, collaborations, partnerships, expansions, agreements, and recent developments associated with the NGS market. Competitive analysis of top players and upcoming startups in the NGS market ecosystem is also covered in this report.

Key Benefits of Buying the Report:

The report will help market leaders and new entrants by providing the closest approximations of revenue for the overall NGS market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain insights to better position their business and develop suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following points:

Analysis of key drivers (advancements in sequencing platforms, rising clinical applications of sequencing, growing demand for precision medicine, declining sequencing costs), restraints (complex data analysis, high initial capital investment), opportunities (integration of AI and ML, adoption of long-read sequencing technologies, emphasis on multiomics integration), and challenges (standardization issues) influencing the growth of the market.

- Product Development/Innovation: Detailed insights on newly launched products/services of the next-generation sequencing market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the next-generation sequencing market

- Competitive Assessment: Illumina, Inc. (US), Thermo Fisher Scientific Inc. (US), F. Hoffmann-La Roche Ltd. (Switzerland), Danaher Corporation (US), QIAGEN (Netherlands), Agilent Technologies, Inc. (US), Revvity (US), Eurofins Scientific (Luxembourg), PacBio (US), Oxford Nanopore Technologies plc. (UK), Takara Bio Inc. (Japan), BGI Group (China), Merck KGaA (Germany), BD (US), 10X Genomics (US), New England Biolabs (US), Promega Corporation (US), Novogene Co., Ltd. (China), LGC Limited (UK), WuXi Biologics (China), MGI Tech Co. Ltd. (China), Tecan Trading AG (Switzerland), Twist Biosciences (US), Azenta US, Inc. (US), GenScript (US), SD Biosensor, Inc. (South Korea), Fulgent Genetics (US), Hamilton Company (US), Zymo Research Corporation (US), NeoGenomics Laboratories (US), and Psomagen (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN NEXT-GENERATION SEQUENCING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 NEXT-GENERATION SEQUENCING MARKET OVERVIEW

- 3.2 NORTH AMERICA: NEXT-GENERATION SEQUENCING MARKET, BY OFFERING AND COUNTRY

- 3.3 NEXT-GENERATION SEQUENCING MARKET, BY COUNTRY

- 3.4 NEXT-GENERATION SEQUENCING MARKET, BY OFFERING, 2026 VS. 2031 (%)

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Advancements in sequencing platforms

- 4.2.1.2 Rising clinical applications of sequencing

- 4.2.1.3 Growing demand for precision medicine

- 4.2.1.4 Declining costs of sequencing

- 4.2.2 RESTRAINTS

- 4.2.2.1 Data analysis complexity

- 4.2.2.2 High capital investments and expenses

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of AI and ML

- 4.2.3.2 Adoption of long-read sequencing technologies

- 4.2.3.3 Emphasis on multiomics integration

- 4.2.4 CHALLENGES

- 4.2.4.1 Standardization issues

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVIES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT FROM SUBSTITUTES

- 5.1.5 THREAT FROM NEW ENTRANTS

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 R&D TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 R&D TRENDS IN GLOBAL BIOTECH INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 ROLE OF PLAYERS IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY KEY PLAYER

- 5.5.1.1 Average selling price trend of platforms, by key player

- 5.5.1.2 Average selling price trend of consumables, by key player

- 5.5.2 AVERAGE SELLING PRICE OF SERVICES, BY KEY PLAYER

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.1 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY KEY PLAYER

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 382200)

- 5.6.2 EXPORT SCENARIO (HS CODE 382200)

- 5.6.3 IMPORT SCENARIO (HS CODE 902700)

- 5.6.4 EXPORT SCENARIO (HS CODE 902700)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 COMPREHENSIVE GENOMIC PROFILING TEST EXPANDS PRECISION ONCOLOGY APPLICATIONS

- 5.10.2 ULTRA-SENSITIVE NGS PANEL ENABLES MEASURABLE RESIDUAL DISEASE MONITORING

- 5.10.3 NGS-BASED MYELOID FUSION PANEL ENHANCES HEMATOLOGIC MALIGNANCY RESEARCH

- 5.11 IMPACT OF 2025 US TARIFF ON NEXT-GENERATION SEQUENCING MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Pharmaceutical & biotechnology companies

- 5.11.5.2 CROs and academic & research institutes

- 5.11.5.3 Hospitals, diagnostic laboratories, and clinics

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOUR

- 6.1 DECISION-MAKING PROCESS

- 6.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 KEY BUYING CRITERIA FOR NGS PRODUCTS, BY END USER

- 6.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Rest of the world

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 8.1 TECHNOLOGY ANALYSIS

- 8.1.1 KEY TECHNOLOGIES

- 8.1.1.1 Sequencing by synthesis

- 8.1.1.2 Ion semiconductor sequencing

- 8.1.1.3 Nanopore sequencing

- 8.1.1.4 Single-molecule real-time sequencing (SMRT)

- 8.1.2 COMPLEMENTARY TECHNOLOGIES

- 8.1.2.1 Automated sample preparation systems

- 8.1.2.2 Bioinformatics and data analysis platforms

- 8.1.2.3 CRISPR-based targeted sequencing

- 8.1.2.4 Multiplex PCR

- 8.1.3 ADJACENT TECHNOLOGIES

- 8.1.3.1 Single-cell sequencing technology

- 8.1.3.2 Multiomics integration

- 8.1.3.3 Spatial genomics and transcriptomics

- 8.1.3.4 Gene editing technologies

- 8.1.1 KEY TECHNOLOGIES

- 8.2 TECHNOLOGY ROADMAP

- 8.3 PATENT ANALYSIS

- 8.3.1 METHODOLOGY

- 8.3.2 NUMBER OF PATENTS FILED, BY DOCUMENT TYPE

- 8.3.3 LIST OF KEY PATENTS

- 8.4 FUTURE APPLICATIONS

- 8.5 IMPACT OF AI/GEN AI ON NEXT-GENERATION SEQUENCING MARKET

- 8.5.1 TOP USE CASES AND MARKET POTENTIAL

- 8.5.2 BEST PRACTICES IN AI-ENABLED NGS WORKFLOWS

- 8.5.3 CASE STUDIES OF AI IMPLEMENTATION IN NEXT-GENERATION SEQUENCING MARKET

- 8.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 8.5.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED SEQUENCING SOLUTIONS IN NEXT-GENERATION SEQUENCING MARKET

9 NEXT-GENERATION SEQUENCING MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 PRODUCTS

- 9.2.1 DEMAND FOR CONSUMABLES AND TECHNOLOGICAL ADVANCEMENTS TO PROPEL MARKET

- 9.3 SERVICES

- 9.3.1 SHIFT TOWARD SERVICE-BASED MODELS TO DRIVE MARKET

10 NEXT-GENERATION SEQUENCING PRODUCTS MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 CONSUMABLES

- 10.2.1 LIBRARY PREPARATION KITS & REAGENTS

- 10.2.1.1 Strong demand and growing applications to ensure market growth

- 10.2.2 SEQUENCING KITS & REAGENTS

- 10.2.2.1 Focus on technological advancements to support market growth

- 10.2.3 OTHER CONSUMABLES

- 10.2.1 LIBRARY PREPARATION KITS & REAGENTS

- 10.3 PLATFORMS

- 10.3.1 SEQUENCING PLATFORMS

- 10.3.1.1 Need for advanced technologies to decode genetic information to drive market

- 10.3.1.2 Illumina

- 10.3.1.2.1 NovaSeq Series (X/X Plus)

- 10.3.1.2.1.1 Next-generation ultra-high throughput sequencing to enable large-scale genomics

- 10.3.1.2.2 MiSeq/MiSeq i100

- 10.3.1.2.2.1 Compact sequencing platforms to enable rapid and targeted genomic analysis

- 10.3.1.2.3 NextSeq 1k/2K and 550

- 10.3.1.2.3.1 Mid-throughput sequencing systems to support diverse research and clinical applications

- 10.3.1.2.4 NovaSeq 6000

- 10.3.1.2.4.1 High-throughput sequencing platform to enable large-scale genomic studies

- 10.3.1.2.1 NovaSeq Series (X/X Plus)

- 10.3.1.3 Thermo Fisher Scientific

- 10.3.1.4 PacBio

- 10.3.1.4.1 Revio

- 10.3.1.4.1.1 High-throughput long-read sequencing to support market growth

- 10.3.1.4.2 Sequel II/IIe

- 10.3.1.4.2.1 High-accuracy, long-read sequencing to support market growth

- 10.3.1.4.3 Vega Seq

- 10.3.1.4.3.1 Benchtop long-read sequencing platform to support market growth

- 10.3.1.4.1 Revio

- 10.3.1.5 Oxford Nanopore Technologies

- 10.3.1.6 Other sequencing platforms

- 10.3.2 LIBRARY PREPARATION PLATFORMS

- 10.3.2.1 Rising demand for sequencing in clinical applications to drive market

- 10.3.1 SEQUENCING PLATFORMS

- 10.4 BIOINFORMATICS TOOLS

- 10.4.1 DATA ANALYSIS SOFTWARE & WORKBENCHES

- 10.4.1.1 Demand for genome analysis in clinical diagnostics to support market growth

- 10.4.2 DATA VISUALIZATION TOOLS

- 10.4.2.1 Rising demand for sequencing-based research to support market growth

- 10.4.3 OTHER BIOINFORMATICS TOOLS

- 10.4.1 DATA ANALYSIS SOFTWARE & WORKBENCHES

11 NEXT-GENERATION SEQUENCING PLATFORMS MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 SEQUENCING BY SYNTHESIS

- 11.2.1 HIGH, RAPID PRODUCTION OF BASE PAIRS TO SUPPORT ADOPTION

- 11.3 ION SEMICONDUCTOR SEQUENCING

- 11.3.1 SIMPLER WORKFLOW AND COST-EFFECTIVENESS TO SUPPORT MARKET GROWTH

- 11.4 SMRT SEQUENCING

- 11.4.1 FOCUS ON RAPID RESULTS AND LOWER SEQUENCING COSTS TO DRIVE MARKET

- 11.5 NANOPORE SEQUENCING

- 11.5.1 EMPHASIS ON DIRECT RNA SEQUENCING CAPABILITIES TO PROPEL DEMAND

- 11.6 OTHER SEQUENCING TECHNOLOGIES

12 NEXT-GENERATION SEQUENCING PRODUCTS MARKET, BY WORKFLOW

- 12.1 INTRODUCTION

- 12.2 SEQUENCING

- 12.2.1 ABILITY TO ADDRESS COMPLEX GENOMIC REGIONS AND RESOLVE STRUCTURAL VARIATIONS TO DRIVE MARKET

- 12.3 PRESEQUENCING

- 12.3.1 INCREASED RESEARCH AND SUPPLY AGREEMENTS BETWEEN INDUSTRY PARTICIPANTS TO DRIVE MARKET

- 12.4 DATA ANALYSIS

- 12.4.1 RISE OF IN-HOUSE INSTALLATION OF BIOINFORMATICS INFRASTRUCTURE TO DRIVE MARKET

13 NEXT-GENERATION SEQUENCING PRODUCTS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 ACADEMIC & RESEARCH INSTITUTES

- 13.2.1 RISING RESEARCH INTENSITY FOR GENOME RESEARCH AMONG INSTITUTES TO SUPPORT MARKET GROWTH

- 13.3 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 13.3.1 RISING DEMAND FOR COMPREHENSIVE SEQUENCING DATA IN GENETIC RESEARCH TO DRIVE MARKET

- 13.4 CLINICAL & DIAGNOSTIC LABORATORIES

- 13.4.1 INCREASED APPLICATIONS IN DISEASE DIAGNOSTICS AND TREATMENT TO DRIVE MARKET GROWTH

- 13.5 OTHER END USERS

14 NEXT-GENERATION SEQUENCING SERVICES MARKET, BY TYPE

- 14.1 INTRODUCTION

- 14.2 SEQUENCING SERVICES

- 14.2.1 EXOME & TARGETED RESEQUENCING SERVICES AND CUSTOM PANELS

- 14.2.1.1 Advancements in target enrichment technologies to drive market

- 14.2.2 RNA SEQUENCING SERVICES

- 14.2.2.1 Launch of RNA services and availability of diverse RNA bioinformatics tools to drive market

- 14.2.3 DE NOVO SEQUENCING SERVICES

- 14.2.3.1 Need for more accurate and faster characterization than traditional methods to drive market

- 14.2.4 CHIP SEQUENCING SERVICES

- 14.2.4.1 Surge in demand from academic and research institutes to drive market

- 14.2.5 WHOLE-GENOME SEQUENCING SERVICES

- 14.2.5.1 Technological advancements in next-generation sequencing products to drive market

- 14.2.6 METHYL SEQUENCING SERVICES

- 14.2.6.1 Large-scale adoption in cancer research to drive market

- 14.2.7 OTHER SEQUENCING SERVICES

- 14.2.1 EXOME & TARGETED RESEQUENCING SERVICES AND CUSTOM PANELS

- 14.3 PRESEQUENCING SERVICES

- 14.3.1 LIBRARY PREPARATION & TARGET ENRICHMENT SERVICES

- 14.3.1.1 Development of advanced library preparation solutions to drive market

- 14.3.2 SAMPLE PREPARATION SERVICES

- 14.3.2.1 Applicability in oncology, infectious diseases, metagenomics, and epigenetics to drive market

- 14.3.3 QUALITY CONTROL SERVICES

- 14.3.3.1 Growing research activities using next-generation sequencing technology to drive market

- 14.3.1 LIBRARY PREPARATION & TARGET ENRICHMENT SERVICES

- 14.4 BIOINFORMATICS & DATA ANALYSIS SERVICES

- 14.4.1 DATA ANALYSIS SERVICES

- 14.4.1.1 Increasing demand for precision and speed in genomics for clinical diagnosis to drive market

- 14.4.2 DATA VISUALIZATION & INTERPRETATION SERVICES

- 14.4.2.1 Rising demand for sequencing-based research to drive market

- 14.4.3 DATA STORAGE & MANAGEMENT SERVICES

- 14.4.3.1 Need for effective data management to drive market

- 14.4.1 DATA ANALYSIS SERVICES

- 14.5 NGS PLATFORM SERVICES

- 14.5.1 COMPLIANCE WITH STRINGENT QUALITY AND OPERATIONAL REQUIREMENTS TO DRIVE MARKET

15 NEXT-GENERATION SEQUENCING SERVICES MARKET, BY WORKFLOW

- 15.1 INTRODUCTION

- 15.2 SEQUENCING

- 15.2.1 RISING DEMAND FOR SEQUENCING SERVICES AND APPLICATIONS IN CLINICAL DIAGNOSTICS TO SUPPORT MARKET GROWTH

- 15.3 PRESEQUENCING SERVICES

- 15.3.1 CUSTOM DEVELOPMENT OF SAMPLES FOR SEQUENCING TO BOOST MARKET GROWTH

- 15.4 DATA ANALYSIS SERVICES

- 15.4.1 RISING DEMAND FOR ADVANCED RESEARCH TO DRIVE MARKET

16 NEXT-GENERATION SEQUENCING SERVICES MARKET, BY END USER

- 16.1 INTRODUCTION

- 16.2 ACADEMIC & RESEARCH INSTITUTES

- 16.2.1 GROWING RESEARCH INTENSITY TO SUPPORT MARKET GROWTH

- 16.3 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 16.3.1 RISING DEMAND FOR COMPREHENSIVE GENETIC DATA TO DRIVE GROWTH

- 16.4 HOSPITALS & CLINICAL LABORATORIES

- 16.4.1 INCREASED APPLICATION IN NGS IN DISEASE DIAGNOSTICS AND TREATMENT TO DRIVE GROWTH

- 16.5 OTHER END USERS

17 NEXT-GENERATION SEQUENCING MARKET, BY APPLICATION

- 17.1 INTRODUCTION

- 17.2 DIAGNOSTICS

- 17.2.1 CANCER DIAGNOSTICS

- 17.2.1.1 Rising demand for targeted therapies to drive market

- 17.2.2 INFECTIOUS DISEASE DIAGNOSTICS

- 17.2.2.1 Rising demand for comprehensive genomic data in clinical diagnostics to propel growth

- 17.2.3 REPRODUCTIVE HEALTH DIAGNOSTICS

- 17.2.3.1 Focus on genetic disease diagnostics to drive growth

- 17.2.4 OTHER DIAGNOSTIC APPLICATIONS

- 17.2.1 CANCER DIAGNOSTICS

- 17.3 DRUG DISCOVERY & DEVELOPMENT

- 17.3.1 PHARMACOGENOMICS

- 17.3.1.1 Rising use of NGS for understanding genomic variants in humans to drive growth

- 17.3.2 OTHER DRUG DISCOVERY & DEVELOPMENT APPLICATIONS

- 17.3.1 PHARMACOGENOMICS

- 17.4 AGRICULTURE & ANIMAL RESEARCH

- 17.4.1 EMPHASIS ON IMPROVING CROP PRODUCTIVITY TO DRIVE ADOPTION OF NGS

- 17.5 OTHER APPLICATIONS

18 NEXT-GENERATION SEQUENCING MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 NORTH AMERICA

- 18.2.1 US

- 18.2.1.1 Rapid growth and advancements to lead market

- 18.2.2 CANADA

- 18.2.2.1 Increasing government initiatives in sequencing research to boost market growth

- 18.2.1 US

- 18.3 EUROPE

- 18.3.1 GERMANY

- 18.3.1.1 Adoption of advanced sequencing technologies to drive market

- 18.3.2 UK

- 18.3.2.1 Strategic initiatives and funding for genomics research to support market growth

- 18.3.3 FRANCE

- 18.3.3.1 Increasing government investment in genomics research to drive growth

- 18.3.4 ITALY

- 18.3.4.1 Favorable funding scenario to drive adoption of advanced sequencing technology

- 18.3.5 SPAIN

- 18.3.5.1 Growing focus on advancements in personalized medicine to support market growth

- 18.3.6 NETHERLANDS

- 18.3.6.1 Well-established research infrastructure to sustain demand for NGS

- 18.3.7 REST OF EUROPE

- 18.3.1 GERMANY

- 18.4 ASIA PACIFIC

- 18.4.1 CHINA

- 18.4.1.1 Favorable regulatory reforms to drive market

- 18.4.2 JAPAN

- 18.4.2.1 Rising number of collaborations in NGS to drive market

- 18.4.3 INDIA

- 18.4.3.1 Government and private initiatives for genomics projects to propel market

- 18.4.4 AUSTRALIA

- 18.4.4.1 Increased genetic research in Australia to support market growth

- 18.4.5 SOUTH KOREA

- 18.4.5.1 Demand for advanced sequencing technologies to support market

- 18.4.6 REST OF ASIA PACIFIC

- 18.4.1 CHINA

- 18.5 LATIN AMERICA

- 18.5.1 BRAZIL

- 18.5.1.1 Increased government investments in genomics advancements to drive market

- 18.5.2 MEXICO

- 18.5.2.1 Rising demand for chronic disease treatment to support growth

- 18.5.3 REST OF LATIN AMERICA

- 18.5.1 BRAZIL

- 18.6 MIDDLE EAST

- 18.6.1 GCC COUNTRIES

- 18.6.1.1 Saudi Arabia

- 18.6.1.1.1 Growing healthcare expenditure in Saudi Arabia to boost market growth

- 18.6.1.2 UAE

- 18.6.1.2.1 Collaborations to advance genome sequencing and market growth

- 18.6.1.3 Rest of GCC countries

- 18.6.1.1 Saudi Arabia

- 18.6.2 REST OF MIDDLE EAST

- 18.6.1 GCC COUNTRIES

- 18.7 AFRICA

- 18.7.1 GROWING FOCUS ON PRECISION MEDICINE TO PROPEL MARKET

19 COMPETITIVE LANDSCAPE

- 19.1 INTRODUCTION

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 19.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN NGS MARKET

- 19.3 REVENUE ANALYSIS, 2021-2025

- 19.4 MARKET SHARE ANALYSIS, 2025

- 19.5 BRAND/PRODUCT COMPARISON

- 19.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 19.6.1 STARS

- 19.6.2 EMERGING LEADERS

- 19.6.3 PERVASIVE PLAYERS

- 19.6.4 PARTICIPANTS

- 19.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 19.6.5.1 Company footprint

- 19.6.5.2 Region footprint

- 19.6.5.3 Offering footprint

- 19.6.5.4 Application footprint

- 19.6.5.5 Technology footprint

- 19.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 19.7.1 PROGRESSIVE COMPANIES

- 19.7.2 RESPONSIVE COMPANIES

- 19.7.3 DYNAMIC COMPANIES

- 19.7.4 STARTING BLOCKS

- 19.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 19.7.5.1 Detailed list of key startups/SMEs

- 19.7.5.2 Competitive benchmarking of startups/SMEs

- 19.8 COMPANY VALUATION & FINANCIAL METRICS

- 19.8.1 COMPANY VALUATION

- 19.8.2 FINANCIAL METRICS

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES

- 19.9.2 DEALS

- 19.9.3 EXPANSIONS

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- 20.1.1 ILLUMINA, INC.

- 20.1.1.1 Business overview

- 20.1.1.2 Products/Services offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches

- 20.1.1.3.2 Deals

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses and competitive threats

- 20.1.2 THERMO FISHER SCIENTIFIC INC.

- 20.1.2.1 Business overview

- 20.1.2.2 Products/Services offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Product launches

- 20.1.2.3.2 Deals

- 20.1.2.3.3 Expansions

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses and competitive threats

- 20.1.3 AGILENT TECHNOLOGIES, INC.

- 20.1.3.1 Business overview

- 20.1.3.2 Products/Services offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Deals

- 20.1.3.3.2 Expansions

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses and competitive threats

- 20.1.4 F. HOFFMANN-LA ROCHE LTD.

- 20.1.4.1 Business overview

- 20.1.4.2 Products/Services offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Product launches

- 20.1.4.3.2 Deals

- 20.1.4.3.3 Other developments

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses and competitive threats

- 20.1.5 QIAGEN

- 20.1.5.1 Business overview

- 20.1.5.2 Products/services offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Deals

- 20.1.5.3.2 Expansions

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses and competitive threats

- 20.1.6 DANAHER CORPORATION

- 20.1.6.1 Business overview

- 20.1.6.2 Products/services offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 Product launches

- 20.1.6.3.2 Deals

- 20.1.6.3.3 Expansions

- 20.1.7 REVVITY

- 20.1.7.1 Business overview

- 20.1.7.2 Products/Services offered

- 20.1.7.3 Recent developments

- 20.1.7.3.1 Product launches

- 20.1.7.3.2 Deals

- 20.1.7.3.3 Expansions

- 20.1.8 EUROFINS SCIENTIFIC

- 20.1.8.1 Business overview

- 20.1.8.2 Products/services offered

- 20.1.8.3 Recent developments

- 20.1.8.3.1 Deals

- 20.1.9 PACBIO

- 20.1.9.1 Business overview

- 20.1.9.2 Products/Services offered

- 20.1.9.3 Recent developments

- 20.1.9.3.1 Product launches

- 20.1.9.3.2 Deals

- 20.1.9.3.3 Expansions

- 20.1.10 OXFORD NANOPORE TECHNOLOGIES PLC

- 20.1.10.1 Business overview

- 20.1.10.2 Products/Services offered

- 20.1.10.3 Recent developments

- 20.1.10.3.1 Deals

- 20.1.10.3.2 Expansions

- 20.1.11 TAKARA BIO INC.

- 20.1.11.1 Business overview

- 20.1.11.2 Products/Services offered

- 20.1.11.3 Recent developments

- 20.1.11.3.1 Deals

- 20.1.12 BGI GROUP

- 20.1.12.1 Business overview

- 20.1.12.2 Products/Services offered

- 20.1.13 BD

- 20.1.13.1 Business overview

- 20.1.13.2 Products/Services offered

- 20.1.13.3 Recent developments

- 20.1.13.3.1 Product launches

- 20.1.14 10X GENOMICS

- 20.1.14.1 Business overview

- 20.1.14.2 Products/Services offered

- 20.1.15 PROMEGA CORPORATION

- 20.1.15.1 Business overview

- 20.1.15.2 Products/Services offered

- 20.1.16 LGC LIMITED

- 20.1.16.1 Business overview

- 20.1.16.2 Products/Services offered

- 20.1.16.3 Recent developments

- 20.1.16.3.1 Deals

- 20.1.17 WUXI BIOLOGICS

- 20.1.17.1 Business overview

- 20.1.17.2 Products/Services offered

- 20.1.18 TECAN TRADING AG

- 20.1.18.1 Business overview

- 20.1.18.2 Products/Services offered

- 20.1.18.3 Recent developments

- 20.1.18.3.1 Deals

- 20.1.19 TWIST BIOSCIENCE

- 20.1.19.1 Business overview

- 20.1.19.2 Products/Services offered

- 20.1.19.3 Recent developments

- 20.1.19.3.1 Product launches

- 20.1.19.3.2 Deals

- 20.1.20 AZENTA US INC.

- 20.1.20.1 Business overview

- 20.1.20.2 Products/Services offered

- 20.1.20.3 Recent developments

- 20.1.20.3.1 Deals

- 20.1.1 ILLUMINA, INC.

- 20.2 OTHER PLAYERS

- 20.2.1 MGI TECH CO. LTD.

- 20.2.2 NOVOGENE CO., LTD.

- 20.2.3 NEW ENGLAND BIOLABS

- 20.2.4 GENSCRIPT

- 20.2.5 PSOMAGEN

- 20.2.6 ZYMO RESEARCH CORPORATION

- 20.2.7 HAMILTON COMPANY

- 20.2.8 NEOGENOMICS LABORATORIES

- 20.2.9 FULGENT GENETICS

- 20.2.10 SD BIOSENSOR, INC.

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.1.1 Key data from secondary sources

- 21.1.2 PRIMARY DATA

- 21.1.2.1 Key data from primary sources

- 21.1.2.2 Key primary participants

- 21.1.2.3 Breakdown of primary interviews

- 21.1.2.4 Key industry insights

- 21.1.1 SECONDARY DATA

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 GLOBAL NEXT-GENERATION SEQUENCING MARKET ESTIMATION, 2025

- 21.2.2 SEGMENTAL MARKET SIZE ESTIMATION

- 21.3 MARKET GROWTH RATE PROJECTIONS

- 21.4 DATA TRIANGULATION

- 21.5 FACTOR ANALYSIS

- 21.6 RESEARCH ASSUMPTIONS

- 21.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

22 APPENDIX

- 22.1 DISCUSSION GUIDE

- 22.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.3 CUSTOMIZATION OPTIONS

- 22.4 RELATED REPORTS

- 22.5 AUTHOR DETAILS