|

시장보고서

상품코드

2007704

반도체 변압기(SST) 시장 예측(-2035년) : 반도체 디바이스 유형(SiC 기반, GaN 기반), 도입 형태(신규 설치, 개수 및 교환), 최종사용자(전력사업, 재생에너지 개발 사업자), 용도별Solid-state Transformer Market by Semiconductor Device Type (SiC-based, GaN-based), Deployment Type (New Installation, Retrofit/Replacement), and End User (Electric Utilities, Renewable Energy Developers), and Application - Global Forecast to 2035 |

||||||

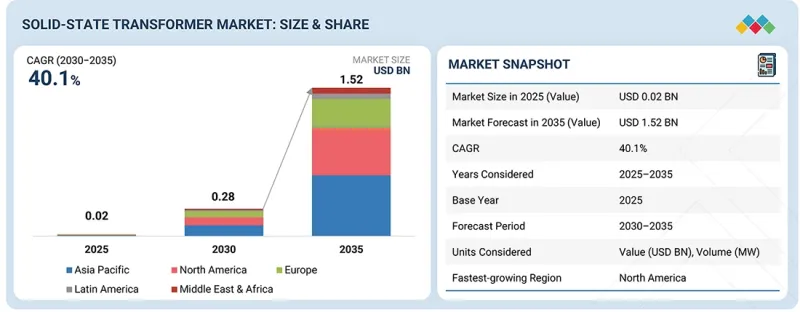

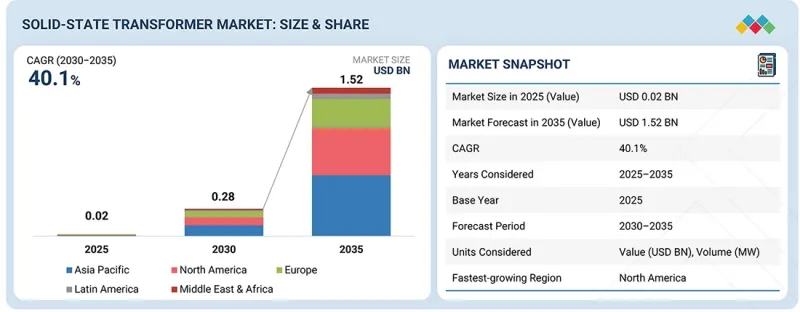

세계의 SST(반도체 변압기) 시장 규모는 2030년 2억 8,000만 달러에서 2035년까지 15억 1,000만 달러에 달할 것으로 예측됩니다.

CAGR은 40.1%에 달할 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2025-2035년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2030-2035년 |

| 단위 | 금액(달러) |

| 부문 | 도입 형태, 용도, 최종사용자, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

"정격 출력별로는 5-20MVA 초과 부문이 예측 기간 중 가장 높은 CAGR을 기록할 것으로 예상됩니다. "

5-20 MVA 이상 부문은 현대 전력망 인프라에서 중대형 전력 변환에 대한 수요가 증가함에 따라 가장 높은 CAGR을 기록할 것으로 예상됩니다. 이러한 변압기는 효율적이고 유연한 전력 관리가 필요한 스마트 그리드 네트워크, 재생에너지 통합 시스템, 대용량 전기자동차 충전 인프라에 점점 더 많이 도입되고 있습니다. 양방향 전력 흐름, 전압 조정 및 고급 그리드 제어를 지원할 수 있으며, 대규모 배전망 및 마이크로그리드 애플리케이션에 적합합니다. 또한 디지털 변전소, 철도 전기화 시스템, 산업용 배전에 대한 투자 증가로 인해 이 정격 출력 부문에서 SST의 도입이 가속화되고 있습니다.

"최종사용자별로는 예측 기간 중 교통 당국이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

교통 당국 부문은 SST 시장에서 가장 큰 점유율을 차지하고 있으며, 철도 전기화, 지하철 시스템, 전기 대중 교통 인프라에 대한 투자 증가에 힘입어 예측 기간 중도 비슷한 추세가 지속될 것으로 예상됩니다. 교통 기관은 에너지 효율 향상, 회생 브레이크 도입, 견인 시스템에서 양방향 전력 흐름을 지원하기 위해 SST를 채택하고 있습니다. 이러한 변압기는 현대 철도 네트워크에서 시스템의 소형화 및 제어성 향상에 기여하고 있습니다. 또한 고속철도의 도입 확대, 도시 교통망의 확장, 전기버스 네트워크의 보급으로 인해 전 세계 교통 인프라 전반에 걸쳐 SST의 채택이 더욱 강화되고 있습니다.

"예측 기간 중 아시아태평양이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

아시아태평양은 전력 인프라의 급속한 확장과 대규모 송전망 현대화 프로그램에 힘입어 가장 큰 점유율을 차지할 것으로 예상됩니다. 중국, 일본, 한국, 인도 등 국가들은 스마트그리드, 재생에너지 통합, 디지털 변전소에 많은 투자를 하고 있습니다. 태양광 및 풍력발전 프로젝트가 확대됨에 따라 변동하는 전력 흐름을 관리할 수 있는 첨단 전력 변환 기술에 대한 수요가 증가하고 있습니다. 또한 도시 및 산업 지역의 전기자동차 충전 인프라, 철도 전기화 프로젝트, 마이크로그리드 개발의 급속한 성장은 이 지역에서 SST의 채택을 가속화하고 있습니다.

세계의 SST(반도체 변압기) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 SST(반도체 변압기) 컴포넌트 상황 개요 분석

제10장 SST(반도체 변압기) 변환 단계

제11장 SST(반도체 변압기)의 열관리 기술

제12장 SST(반도체 변압기) 시장 : 전력정격별

제13장 SST(반도체 변압기) 시장 : 전압 레벨별

제14장 SST(반도체 변압기) 시장 : 반도체 디바이스 유형별

제15장 SST(반도체 변압기) 시장 : 도입 형태별

제16장 SST(반도체 변압기) 시장 : 용도별

제17장 SST(반도체 변압기) 시장 : 최종사용자별

제18장 SST(반도체 변압기) 시장 : 지역별

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 부록

KSA 26.04.29The global solid-state transformer market is estimated to be valued at USD 0.28 billion in 2030 and is projected to reach USD 1.51 billion by 2035, growing at a CAGR of 40.1%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2035 |

| Base Year | 2024 |

| Forecast Period | 2030-2035 |

| Units Considered | Value (USD Billion) |

| Segments | By Deployment Type, Application, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Based on power rating, >5-20 MVA segment to witness highest CAGR during forecast period"

The >5-20 MVA segment is expected to witness the highest CAGR in the solid-state transformer market due to growing demand for medium-to-high power conversion in modern grid infrastructure. These transformers are increasingly deployed in smart grid networks, renewable energy integration systems, and high-capacity electric vehicle charging infrastructure requiring efficient and flexible power management. Their ability to support bidirectional power flow, voltage regulation, and advanced grid control makes them suitable for large distribution networks and microgrid applications. Additionally, rising investments in digital substations, railway electrification systems, and industrial power distribution are accelerating the adoption of solid-state transformers within this power rating segment.

"Based on end user, transportation authorities to hold largest market share throughout forecast period"

The transportation authorities segment accounts for the largest share of the solid-state transformer market, and a similar trend is likely to continue during the forecast period, driven by increasing investments in railway electrification, metro systems, and electric public transport infrastructure. Transportation agencies are adopting solid-state transformers to improve energy efficiency, enable regenerative braking, and support bidirectional power flow in traction systems. These transformers also help reduce system size and enhance controllability in modern rail networks. Additionally, growing deployment of high-speed rail, urban transit expansion, and electrified bus networks is further strengthening the adoption of solid-state transformers across transportation infrastructure globally.

"Asia Pacific to capture largest market share during forecast period"

The Asia Pacific region is expected to hold the largest share of the solid-state transformer market, driven by the rapid expansion of electricity infrastructure and large-scale grid modernization programs. Countries such as China, Japan, South Korea, and India are investing heavily in smart grids, renewable energy integration, and digital substations. Increasing deployment of solar and wind energy projects is creating demand for advanced power conversion technologies capable of managing variable power flows. Additionally, rapid growth in electric vehicle charging infrastructure, railway electrification projects, and microgrid development across urban and industrial zones is accelerating the adoption of solid-state transformers in the region.

Extensive primary interviews were conducted with key industry experts in the solid-state transformer market to determine and verify the market size for various segments and subsegments, based on secondary research. The breakdown of primary participants for the report is shown below.

The study draws on insights from industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 30%, Tier 2 - 35%, and Tier 3 - 35%

- By Designation - C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region - North America - 35%, Europe - 25%, Asia Pacific - 30%, Latin America - 5%, and Middle East & Africa - 5%

The solid-state transformer market is characterized by the presence of several established technology providers and power electronics companies, such as Hitachi, Ltd. (Japan), ABB (Switzerland), Eaton (Ireland), Delta Electronics, Inc. (Taiwan), SolarEdge Technologies, Inc. (Israel), Ampereand PTE LTD (Singapore), RCT Systems (Switzerland), DG Matrix (US), GridBridge (US), and WattEV (US), among others.

The study includes an in-depth competitive analysis of these key players in the solid-state transformer market, covering their company profiles, recent developments, product innovations, and key market strategies.

Study Coverage:

The report segments the solid-state transformer market and forecasts its size by power rating (<1 MVA, 1-5 MVA, >5-20 MVA, >20 MVA), by voltage level (low voltage (<1 kV), medium voltage (1-35 kV), high voltage (>35 kV)), by semiconductor device type (silicon carbide (SiC)-based SST, gallium nitride (GaN)-based SST, hybrid SST (SiC+GaN)), by deployment type (new installation, retrofit/replacement), by application (smart grid & distribution networks, renewable energy integration, electric vehicle infrastructure, railway & traction systems, data centers, industrial & commercial applications), and by end user (electric utilities, renewable energy developers, transportation authorities, industrial enterprises, commercial & institutional operators, government & defense organizations). The report also analyzes key market drivers, restraints, opportunities, and challenges influencing industry growth. It provides a detailed regional assessment across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa, along with country-level insights for major markets. In addition, the study includes a value chain analysis and a competitive landscape assessment of leading players in the global solid-state transformer ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (increasing investments in grid modernization and smart grid infrastructure, rising integration of renewable energy sources into power systems, expanding electrification of transportation systems, accelerating demand for efficient power conversion in modern distribution networks, increasing adoption of distributed energy resources in power networks ), restraints (high initial development and deployment costs of solid-state transformers, limited large-scale commercial deployment and field validation, lack of standardized regulatory and grid integration frameworks, high cost of wide-bandgap semiconductor materials, shortage of large-scale facilities for manufacturing SST systems and specialized components), opportunities (growing deployment of digital substations and intelligent grid infrastructure, expansion of high-power electric vehicle fast-charging networks), increasing adoption of decentralized energy systems and microgrids, rising demand for compact and high-efficiency power distribution systems, accelerating R&D power electronics), challenges (thermal management challenges in high-power semiconductor modules, concerns about reliability during high-voltage and high-frequency operations, complexities associated with integrating SSTs into legacy grid infrastructure, managing power quality, harmonics, and stability in power electronics-based grids, and protection and fault management in converter-based transformer architectures.

- Product Development/Innovation: Detailed insights on emerging technologies, power semiconductor advancements such as silicon carbide (SiC) and gallium nitride (GaN), ongoing research and development activities, and product launches/developments in the solid-state transformer market

- Market Development: Comprehensive information about high-growth markets by analyzing the solid-state transformer market across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

- Market Diversification: Exhaustive information about new technological developments, untapped application areas, strategic investments, and expansion opportunities in the solid-state transformer market

- Competitive Assessment: In-depth assessment of market shares and growth strategies of leading players, such as Hitachi, Ltd. (Japan), ABB (Switzerland), Eaton (Ireland), Delta Electronics, Inc. (Taiwan), SolarEdge Technologies, Inc. (Israel), Ampereand PTE LTD (Singapore), RCT Systems (Switzerland), DG Matrix (US), GridBridge (US), and WattEV (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN SOLID-STATE TRANSFORMER MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SOLID-STATE TRANSFORMER MARKET

- 3.2 SOLID-STATE TRANSFORMER MARKET, BY POWER RATING

- 3.3 SOLID-STATE TRANSFORMER MARKET, BY VOLTAGE LEVEL

- 3.4 SOLID-STATE TRANSFORMER MARKET, BY SEMICONDUCTOR DEVICE TYPE

- 3.5 SOLID-STATE TRANSFORMER MARKET, BY DEPLOYMENT TYPE

- 3.6 SOLID-STATE TRANSFORMER MARKET, BY APPLICATION

- 3.7 SOLID-STATE TRANSFORMER MARKET, BY END USER

- 3.8 SOLID-STATE TRANSFORMER MARKET, BY REGION

- 3.9 SOLID-STATE TRANSFORMER MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing investments in grid modernization and smart grid infrastructure

- 4.2.1.2 Rising integration of renewable energy sources into power systems

- 4.2.1.3 Expanding electrification of transportation systems

- 4.2.1.4 Accelerating demand for efficient power conversion in modern distribution networks

- 4.2.1.5 Increasing adoption of distributed energy resources in power networks

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial development and deployment costs of solid-state transformers

- 4.2.2.2 Limited large-scale commercial deployment and field validation

- 4.2.2.3 Lack of standardized regulatory and grid integration frameworks

- 4.2.2.4 High cost of wide-bandgap semiconductor materials

- 4.2.2.5 Shortage of large-scale facilities for manufacturing SST systems and specialized components

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing deployment of digital substations and intelligent grid infrastructure

- 4.2.3.2 Expansion of high-power electric vehicle fast-charging networks

- 4.2.3.3 Increasing adoption of decentralized energy systems and microgrids

- 4.2.3.4 Rising demand for compact and high-efficiency power distribution systems

- 4.2.3.5 Accelerating R&D power electronics

- 4.2.4 CHALLENGES

- 4.2.4.1 Thermal management challenges in high-power semiconductor modules

- 4.2.4.2 Concerns about reliability during high-voltage and high-frequency operations

- 4.2.4.3 Complexities associated with integrating SSTs into legacy grid infrastructure

- 4.2.4.4 Managing power quality, harmonics, and stability in power electronics-based grids

- 4.2.4.5 Protection and fault management in converter-based transformer architectures

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.4.1 MARKET DYNAMICS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL POWER ELECTRONICS AND WIDE BANDGAP SEMICONDUCTOR INDUSTRY

- 5.3.4 TRENDS IN GLOBAL SOLID-STATE TRANSFORMER MARKET

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF SOLID-STATE TRANSFORMERS, BY DEPLOYMENT TYPE AND POWER RATING, 2022-2025

- 5.6.1.1 Average selling price trend of solid-state transformers in new installations, by power rating, 2022-2025

- 5.6.1.2 Average selling price trend of solid-state transformers in retrofit/replacement installations, by power rating, 2022-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF SOLID-STATE TRANSFORMERS, BY REGION, 2022-2025

- 5.6.2.1 Average selling price trend of solid-state transformers, by region, 2022-2025

- 5.6.1 AVERAGE SELLING PRICE TREND OF SOLID-STATE TRANSFORMERS, BY DEPLOYMENT TYPE AND POWER RATING, 2022-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8504)

- 5.7.2 EXPORT SCENARIO (HS CODE 8504)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 USE OF SOLID-STATE TRANSFORMERS IN SMART GRID APPLICATIONS TO ENHANCE GRID FLEXIBILITY AND POWER QUALITY

- 5.11.2 INTEGRATION OF SOLID-STATE TRANSFORMERS INTO RAILWAY ENERGY MANAGEMENT SYSTEMS TO IMPROVE ENERGY EFFICIENCY

- 5.11.3 ADOPTION OF SOLID-STATE TRANSFORMERS IN EV CHARGING INFRASTRUCTURE TO IMPROVE CHARGING EFFICIENCY

- 5.12 IMPACT OF US TARIFFS - SOLID-STATE TRANSFORMER MARKET

- 5.12.1 KEY TARIFF RATES

- 5.12.2 PRICE IMPACT ANALYSIS

- 5.12.3 IMPACT ON COUNTRIES/REGIONS

- 5.12.3.1 US

- 5.12.3.2 Europe

- 5.12.3.3 Asia Pacific

- 5.12.4 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 WIDE-BANDGAP SEMICONDUCTOR-BASED POWER CONVERSION

- 6.1.2 HIGH-FREQUENCY TRANSFORMER AND POWER CONVERTER ARCHITECTURES

- 6.1.3 MODULAR MULTILEVEL CONVERTER (MMC) ARCHITECTURES

- 6.1.4 DIGITAL CONTROL SYSTEMS AND SMART GRID INTEGRATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ENERGY STORAGE SYSTEM

- 6.2.2 POWER ELECTRONICS CONTROL AND MONITORING PLATFORMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ELECTRIC VEHICLE FAST-CHARGING INFRASTRUCTURE

- 6.3.2 RENEWABLE ENERGY POWER CONVERSION TECHNOLOGIES

- 6.4 TECHNOLOGY ROADMAP

- 6.4.1 SHORT-TERM (2025-2027): PERFORMANCE OPTIMIZATION AND PILOT DEPLOYMENTS

- 6.4.2 MID-TERM (2027-2030): GRID INTEGRATION AND SCALABLE DEPLOYMENT

- 6.4.3 LONG-TERM (2030-2035+): INTELLIGENT POWER NETWORKS AND WIDESPREAD SST DEPLOYMENT

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON SOLID-STATE TRANSFORMER MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN SOLID-STATE TRANSFORMER MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN SOLID-STATE TRANSFORMER MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED SOLID-STATE TRANSFORMERS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 INTRODUCTION

- 7.2 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.2 INDUSTRY STANDARDS

- 7.2.2.1 IEC power electronics and converter standards (IEC 61800 and IEC 61000 series)

- 7.2.2.2 IEEE power electronics and grid interconnection standards

- 7.2.2.3 IEC smart grid and substation automation standards (IEC 61850 series)

- 7.2.2.4 Grid code and interconnection standards

- 7.2.2.5 Safety and electrical equipment certification standards

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 USE OF SOLID-STATE TRANSFORMERS TO REDUCE ENVIRONMENTAL IMPACT

- 7.3.1.1 Deployment of solid-state transformers to reduce carbon impact

- 7.3.1.2 Adoption of solid-state transformers to ensure energy efficiency and grid optimization

- 7.3.2 IMPLEMENTATION OF SUSTAINABLE POWER ELECTRONICS TO REDUCE ENERGY CONSUMPTION

- 7.3.3 ESTABLISHMENT OF SUSTAINABLE GRID INFRASTRUCTURE TO ENHANCE POWER QUALITY AND RENEWABLE ENERGY INTEGRATION

- 7.3.1 USE OF SOLID-STATE TRANSFORMERS TO REDUCE ENVIRONMENTAL IMPACT

- 7.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4.1 IMPACT OF ENVIRONMENTAL REGULATIONS ON SOLID-STATE TRANSFORMER DESIGN

- 7.4.2 IMPACT OF RENEWABLE ENERGY POLICIES ON SOLID-STATE TRANSFORMER DEPLOYMENT

- 7.4.3 IMPACT OF ELECTRIFICATION AND GRID MODERNIZATION POLICIES ON SOLID-STATE TRANSFORMER DEMAND

- 7.5 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.5.1 PRODUCT SAFETY AND REGULATORY CERTIFICATION

- 7.5.2 ENVIRONMENTAL COMPLIANCE AND HAZARDOUS SUBSTANCE LABELING

- 7.5.3 ENERGY EFFICIENCY AND ENVIRONMENTAL LABELING PROGRAMS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS END USERS

- 8.6 MARKET PROFITABILITY

- 8.6.1 REVENUE POTENTIAL

- 8.6.2 COST DYNAMICS

- 8.6.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 SOLID-STATE TRANSFORMER COMPONENT LANDSCAPE ANALYSIS

- 9.1 INTRODUCTION

- 9.2 POWER CONVERTERS

- 9.3 SWITCHING DEVICES

- 9.4 CONTROL CIRCUITS

- 9.5 HIGH-FREQUENCY TRANSFORMERS

10 SOLID-STATE TRANSFORMER CONVERSION STAGES

- 10.1 INTRODUCTION

- 10.2 SINGLE-STAGE SST

- 10.3 TWO-STAGE SST

- 10.4 THREE-STAGE SST

11 THERMAL MANAGEMENT TECHNIQUES IN SOLID-STATE TRANSFORMERS

- 11.1 INTRODUCTION

- 11.2 AIR COOLING

- 11.3 LIQUID COOLING

- 11.4 HYBRID COOLING

12 SOLID-STATE TRANSFORMER MARKET, BY POWER RATING

- 12.1 INTRODUCTION

- 12.2 <1 MVA

- 12.2.1 ABILITY TO IMPROVE POWER QUALITY AND REDUCE CONVERSION LOSSES TO DRIVE DEMAND

- 12.3 1-5 MVA

- 12.3.1 INCREASING ELECTRIFICATION OF INDUSTRIAL PROCESSES TO BOOST DEMAND

- 12.4 >5-20 MVA

- 12.4.1 SMART GRID EXPANSION AND RENEWABLE ENERGY INTEGRATION PROGRAMS TO FUEL SEGMENTAL GROWTH

- 12.5 >20 MVA

- 12.5.1 MODERNIZATION OF TRANSMISSION AND DISTRIBUTION NETWORKS TO CREATE GROWTH OPPORTUNITIES

13 SOLID-STATE TRANSFORMER MARKET, BY VOLTAGE LEVEL

- 13.1 INTRODUCTION

- 13.2 LOW VOLTAGE (<1 KV)

- 13.2.1 STRONG FOCUS ON SUSTAINABLE INFRASTRUCTURE DEVELOPMENT TO BOOST DEMAND

- 13.3 MEDIUM VOLTAGE (1-35 KV)

- 13.3.1 HIGH ADOPTION OF SMART GRID TECHNOLOGY AND DIGITAL SUBSTATIONS TO STRENGTHEN SEGMENTAL GROWTH

- 13.4 HIGH VOLTAGE (>35 KV)

- 13.4.1 RAPID MODERNIZATION OF TRANSMISSION INFRASTRUCTURE AND RAIL ELECTRIFICATION TO CREATE GROWTH AVENUES

14 SOLID-STATE TRANSFORMER MARKET, BY SEMICONDUCTOR DEVICE TYPE

- 14.1 INTRODUCTION

- 14.2 SILICON CARBIDE (SIC)-BASED SST

- 14.2.1 HIGHER SWITCHING FREQUENCIES AND LOWER CONDUCTION LOSSES ATTRIBUTES TO SUPPORT SIC-BASED SST ADOPTION IN GRID INFRASTRUCTURE

- 14.3 GALLIUM NITRIDE (GAN)-BASED SST

- 14.3.1 SURGING USE OF COMPACT POWER CONVERSION SYSTEMS IN SMART BUILDINGS TO FACILITATE SEGMENTAL GROWTH

- 14.4 HYBRID SST (SIC + GAN)

- 14.4.1 POTENTIAL TO IMPROVE SYSTEM EFFICIENCY, REDUCE ENERGY LOSSES, AND ENHANCE THERMAL MANAGEMENT TO BOOST DEMAND

15 SOLID-STATE TRANSFORMER MARKET, BY DEPLOYMENT TYPE

- 15.1 INTRODUCTION

- 15.2 NEW INSTALLATION

- 15.2.1 RISING INVESTMENTS IN SMART GRID AND RENEWABLE ENERGY INFRASTRUCTURE TO FACILITATE SEGMENTAL GROWTH

- 15.3 RETROFIT/REPLACEMENT

- 15.3.1 PRESSING NEED TO MODERNIZE AGING GRID INFRASTRUCTURE TO PROMOTE SEGMENTAL GROWTH

16 SOLID-STATE TRANSFORMER MARKET, BY APPLICATION

- 16.1 INTRODUCTION

- 16.2 SMART GRID & DISTRIBUTION NETWORKS

- 16.2.1 REGULATORY MANDATES FOR DECARBONIZATION TO PROMOTE SST DEPLOYMENT

- 16.2.2 DISTRIBUTION-LEVEL TRANSFORMATION

- 16.2.3 MULTI-MICROGRID MANAGEMENT

- 16.2.4 GRID RESILIENCE ENHANCEMENT

- 16.3 RENEWABLE ENERGY INTEGRATION

- 16.3.1 ABILITY TO IMPROVE POWER QUALITY AND REDUCE CONVERSION LOSSES TO BOOST DEMAND

- 16.3.2 SOLAR PV INTERFACING

- 16.3.3 WIND FARM CONNECTIVITY

- 16.3.4 OFFSHORE WIND PLATFORMS

- 16.4 ELECTRIC VEHICLE INFRASTRUCTURE

- 16.4.1 RAPID EV ADOPTION AND HIGH DEMAND FOR FAST-CHARGING INFRASTRUCTURE TO EXPEDITE MARKET GROWTH

- 16.4.2 FAST-CHARGING STATIONS

- 16.4.3 VEHICLE-TO-GRID (V2G) APPLICATIONS

- 16.5 RAILWAY & TRACTION SYSTEMS

- 16.5.1 ELECTRIFICATION OF RAIL NETWORKS TO PROVIDE GROWTH AVENUES

- 16.5.2 MODERN ELECTRIC RAIL SYSTEMS

- 16.5.3 METRO AND LIGHT RAIL SYSTEMS

- 16.6 DATA CENTERS

- 16.6.1 TRANSITION TO MODULAR AND SCALABLE POWER ARCHITECTURES TO ACCELERATE DEMAND

- 16.6.2 AC-TO-DC CONVERSION EFFICIENCY ENHANCEMENT

- 16.6.3 POWER QUALITY IMPROVEMENT

- 16.7 INDUSTRIAL & COMMERCIAL APPLICATIONS

- 16.7.1 INCREASING FOCUS ON ENERGY OPTIMIZATION AND SUSTAINABILITY TO STIMULATE DEMAND

- 16.7.2 MANUFACTURING FACILITIES

- 16.7.3 URBAN SUBSTATIONS

- 16.7.4 CRITICAL INFRASTRUCTURE

17 SOLID-STATE TRANSFORMER MARKET, BY END USER

- 17.1 INTRODUCTION

- 17.2 ELECTRIC UTILITIES

- 17.2.1 ONGOING GRID MODERNIZATION PROGRAMS ACROSS DEVELOPED AND EMERGING MARKETS TO SUPPORT MARKET GROWTH

- 17.3 RENEWABLE ENERGY DEVELOPERS

- 17.3.1 RISING USE OF SOLID-STATE TRANSFORMERS IN INVERTER STATIONS AND HYBRID ENERGY HUBS TO DRIVE MARKET

- 17.4 TRANSPORTATION AUTHORITIES

- 17.4.1 SURGING DEMAND FOR HIGH-POWER CHARGING INFRASTRUCTURE AND ENERGY-EFFICIENT RAIL SYSTEMS TO FUEL MARKET GROWTH

- 17.5 INDUSTRIAL ENTERPRISES

- 17.5.1 INCREASING DEMAND FOR DIGITAL AND ENERGY-INTENSIVE INDUSTRIAL SYSTEMS TO FOSTER MARKET GROWTH

- 17.6 COMMERCIAL & INSTITUTIONAL OPERATORS

- 17.6.1 ELEVATING ADOPTION OF REAL-TIME ENERGY MONITORING PLATFORMS IN SMART BUILDINGS TO CONTRIBUTE TO MARKET GROWTH

- 17.7 GOVERNMENT & DEFENSE ORGANIZATIONS

- 17.7.1 ELECTRIFICATION OF DEFENSE INFRASTRUCTURE AND MOBILE POWER SYSTEMS TO OPEN UP OPPORTUNITIES

18 SOLID-STATE TRANSFORMER MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 NORTH AMERICA

- 18.2.1 US

- 18.2.1.1 Rapid expansion of EV charging infrastructure to drive market

- 18.2.2 CANADA

- 18.2.2.1 High reliance on hybrid renewable solutions to fuel market growth

- 18.2.1 US

- 18.3 EUROPE

- 18.3.1 GERMANY

- 18.3.1.1 Large-scale adoption of renewable energy through Energiewende strategy to accelerate market growth

- 18.3.2 FRANCE

- 18.3.2.1 Grid digitalization and transport electrification initiatives to support market growth

- 18.3.3 UK

- 18.3.3.1 Offshore wind expansion and grid decentralization efforts to boost demand

- 18.3.4 ITALY

- 18.3.4.1 Significant penetration of rooftop solar photovoltaic systems to facilitate market growth

- 18.3.5 SPAIN

- 18.3.5.1 Rapid shift toward solar-dominated energy mix to support market growth

- 18.3.6 REST OF EUROPE

- 18.3.1 GERMANY

- 18.4 ASIA PACIFIC

- 18.4.1 CHINA

- 18.4.1.1 Active investments in digital grid technologies and advanced power electronics to expedite market growth

- 18.4.2 JAPAN

- 18.4.2.1 Accelerated implementation of microgrid demonstration projects to promote market growth

- 18.4.3 SOUTH KOREA

- 18.4.3.1 Increasing investments in next-generation grid infrastructure to strengthen market growth

- 18.4.4 INDIA

- 18.4.4.1 Modernization of distribution infrastructure through smart metering, feeder automation, and digital substations to propel market

- 18.4.5 REST OF ASIA PACIFIC

- 18.4.1 CHINA

- 18.5 LATIN AMERICA

- 18.5.1 BRAZIL

- 18.5.1.1 Hydro-dominant system transition and distributed solar expansion to foster market growth

- 18.5.2 ARGENTINA

- 18.5.2.1 Need to upgrade aging and capacity-constrained grid infrastructure to spur demand

- 18.5.3 MEXICO

- 18.5.3.1 Expansion of private and industrial energy projects to spike demand

- 18.5.1 BRAZIL

- 18.6 MIDDLE EAST & AFRICA

- 18.6.1 GCC

- 18.6.1.1 Mega-scale energy projects and smart city initiatives to promote market growth

- 18.6.1.2 Saudi Arabia

- 18.6.1.3 UAE

- 18.6.1.4 Rest of GCC

- 18.6.2 SOUTH AFRICA

- 18.6.2.1 Government-led renewable energy programs to strengthen market growth

- 18.6.3 REST OF MIDDLE EAST & AFRICA

- 18.6.1 GCC

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2025

- 19.3 MARKET SHARE ANALYSIS, 2025

- 19.4 REVENUE ANALYSIS, 2020-2025

- 19.5 COMPANY VALUATION AND FINANCIAL METRICS

- 19.6 BRAND/PRODUCT COMPARISON

- 19.6.1 HITACHI, LTD. (JAPAN)

- 19.6.2 ABB (SWITZERLAND)

- 19.6.3 EATON (IRELAND)

- 19.6.4 DELTA ELECTRONICS (TAIWAN)

- 19.6.5 GRIDBRIDGE (US)

- 19.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 19.7.5.1 Company footprint

- 19.7.5.2 Region footprint

- 19.7.5.3 Semiconductor device type footprint

- 19.7.5.4 Application footprint

- 19.7.5.5 End user footprint

- 19.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 19.8.1 PROGRESSIVE COMPANIES

- 19.8.2 RESPONSIVE COMPANIES

- 19.8.3 DYNAMIC COMPANIES

- 19.8.4 STARTING BLOCKS

- 19.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 19.8.5.1 Detailed list of key startups/SMEs

- 19.8.5.2 Competitive benchmarking of key startups/SMEs

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES

- 19.9.2 DEALS

- 19.9.3 OTHER DEVELOPMENTS

20 COMPANY PROFILES

- 20.1 INTRODUCTION

- 20.2 KEY PLAYERS

- 20.2.1 HITACHI, LTD.

- 20.2.1.1 Business overview

- 20.2.1.2 Products offered

- 20.2.1.3 Recent developments

- 20.2.1.3.1 Product launches

- 20.2.1.3.2 Deals

- 20.2.1.4 MnM view

- 20.2.1.4.1 Key strengths/Right to win

- 20.2.1.4.2 Strategic choices

- 20.2.1.4.3 Weaknesses/Competitive threats

- 20.2.2 DELTA ELECTRONICS, INC.

- 20.2.2.1 Business overview

- 20.2.2.2 Products offered

- 20.2.2.3 Recent developments

- 20.2.2.3.1 Product launches

- 20.2.2.3.2 Deals

- 20.2.2.4 MnM view

- 20.2.2.4.1 Key strengths/Right to win

- 20.2.2.4.2 Strategic choices

- 20.2.2.4.3 Weaknesses/Competitive threats

- 20.2.3 EATON

- 20.2.3.1 Business overview

- 20.2.3.2 Products offered

- 20.2.3.3 Recent developments

- 20.2.3.3.1 Deals

- 20.2.3.3.2 Other developments

- 20.2.3.4 MnM view

- 20.2.3.4.1 Key strengths/Right to win

- 20.2.3.4.2 Strategic choices

- 20.2.3.4.3 Weaknesses/Competitive threats

- 20.2.4 ABB

- 20.2.4.1 Business overview

- 20.2.4.2 Products offered

- 20.2.4.3 Recent developments

- 20.2.4.3.1 Deals

- 20.2.4.4 MnM view

- 20.2.4.4.1 Key strengths/Right to win

- 20.2.4.4.2 Strategic choices

- 20.2.4.4.3 Weaknesses/Competitive threats

- 20.2.5 GRIDBRIDGE

- 20.2.5.1 Business overview

- 20.2.5.2 Products offered

- 20.2.5.3 MnM view

- 20.2.5.3.1 Key strengths/Right to win

- 20.2.5.3.2 Strategic choices

- 20.2.5.3.3 Weaknesses/Competitive threats

- 20.2.6 AMPERESAND PTE LTD

- 20.2.6.1 Business overview

- 20.2.6.2 Products offered

- 20.2.6.3 Recent developments

- 20.2.6.3.1 Product launches

- 20.2.6.3.2 Deals

- 20.2.6.3.3 Other developments

- 20.2.7 RCT SYSTEMS

- 20.2.7.1 Business overview

- 20.2.7.2 Products offered

- 20.2.8 DG MATRIX

- 20.2.8.1 Business overview

- 20.2.8.2 Products offered

- 20.2.8.3 Recent developments

- 20.2.8.3.1 Deals

- 20.2.8.3.2 Other developments

- 20.2.9 SOLAREDGE TECHNOLOGIES, INC.

- 20.2.9.1 Business overview

- 20.2.9.2 Products offered

- 20.2.9.3 Recent developments

- 20.2.9.3.1 Deals

- 20.2.10 WATTEV

- 20.2.10.1 Business overview

- 20.2.10.2 Products offered

- 20.2.10.3 Recent developments

- 20.2.10.3.1 Product launches

- 20.2.1 HITACHI, LTD.

- 20.3 OTHER PLAYERS

- 20.3.1 HERON POWER ELECTRONICS COMPANY

- 20.3.2 SIFANG

- 20.3.3 TRANSFORMA ENERGY

- 20.4 COMPONENT PROVIDERS

- 20.4.1 WOLFSPEED, INC.

- 20.4.2 STMICROELECTRONICS

- 20.4.3 SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC

- 20.4.4 ROHM CO., LTD.

- 20.4.5 TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION

- 20.4.6 MITSUBISHI ELECTRIC CORPORATION

- 20.4.7 FUJI ELECTRIC CO., LTD.

- 20.4.8 NAVITAS SEMICONDUCTOR

- 20.4.9 SEMIKRON DANFOSS

- 20.4.10 MICROCHIP TECHNOLOGY INC.

- 20.4.11 EFFICIENT POWER CONVERSION CORPORATION

- 20.4.12 INFINEON TECHNOLOGIES AG

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY AND PRIMARY RESEARCH

- 21.1.2 SECONDARY DATA

- 21.1.2.1 List of key secondary sources

- 21.1.2.2 Key data from secondary sources

- 21.1.3 PRIMARY DATA

- 21.1.3.1 List of primary interview participants

- 21.1.3.2 Breakdown of primaries

- 21.1.3.3 Key data from primary sources

- 21.1.3.4 Key industry insights

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 21.2.2 TOP-DOWN APPROACH

- 21.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 21.2.1 BOTTOM-UP APPROACH

- 21.3 DATA TRIANGULATION

- 21.4 RESEARCH ASSUMPTIONS

- 21.5 RESEARCH LIMITATIONS

- 21.6 RISK ASSESSMENT

22 APPENDIX

- 22.1 INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS