|

시장보고서

상품코드

2008703

PFAS 폐기물 관리 시장 예측(-2031년) : 처리 기술별, 서비스 유형별, 최종 용도 산업별, 지역별PFAS Waste Management Market by Treatment Technology (Destruction, Recycling & Recovery, Others), Service Type (On-site, Off-site), End-use Industry (Industrial, Commercial, Municipal), and Region - Global forecast to 2031 |

||||||

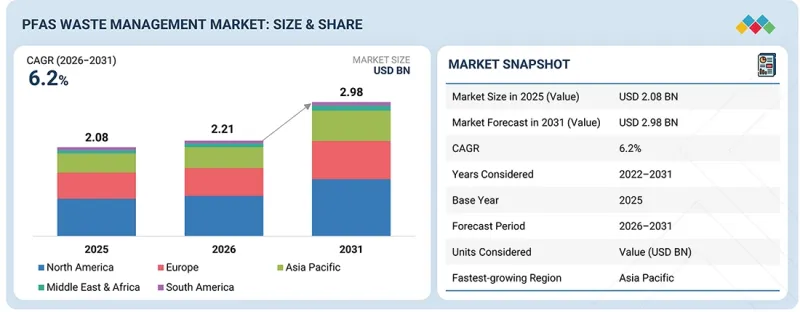

세계의 PFAS 폐기물 관리 시장 규모는 2026년 22억 1,000만 달러에서 2031년까지 29억 8,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 6.2%의 확대가 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 100만 달러 |

| 부문 | 기술, 서비스 유형, 최종 용도 산업, 지역 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

PFAS 폐기물 관리의 오프사이트 서비스 부문은 특수 외부 시설에서 PFAS 오염물질의 수집, 운송, 처리를 포함합니다. 이 방법은 오염된 토양, 슬러지, 사용 후 활성탄, 현장에서 효과적으로 처리하기 어려운 산업폐기물 등 고농도 또는 유해한 폐기물 흐름에 일반적으로 사용됩니다. 오프사이트 시설은 통제된 조건에서 복잡한 폐기물을 처리할 수 있는 첨단 대규모 처리 및 파괴 기술을 갖추고 있으며, 높은 효율성과 규제 준수를 보장합니다.

"금액 기준으로는 지자체 부문이 전체 PFAS 폐기물 관리 시장에서 가장 큰 점유율을 차지했습니다. "

지자체 부문에서는 정부의 기준을 충족하는 안전한 식수를 공급하는 수처리 기술이 요구되고 있습니다. 지방 상수도 사업자는 PFAS, 중금속, 유기오염물질 등 오염물질을 처리하기 위해 전기화학 산화, 초임계 수산화, 소각 등 첨단 분해 솔루션을 점점 더 많이 채택하고 있습니다. 강화된 규제 요건, 노후화된 시설의 존재, 공중보건에 대한 지식의 증가가 결합되어 처리 시스템의 개선이 가속화되고 있습니다. 지자체는 PFAS 폐기물 관리 시스템과 첨단 수처리 기술에 지속적인 시장을 제공하고 있습니다.

"북미 지역이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

북미는 첨단 수처리 기술과 PFAS 처리 기술의 가장 큰 시장입니다. 이 지역의 시장은 엄격한 정부 규제, PFAS 처리에서 처리 잔여물의 적절한 관리에 대한 요구, 그리고 사회적 인식의 증가에 의해 주도되고 있습니다. 지자체 수도사업자, 산업시설, 국방 관련 시설은 엄격한 식수 및 폐수 요건을 준수하기 위해 분해 기술 및 응고 처리에 많은 투자를 하고 있습니다.

또한 북미 PFAS 폐기물 관리 시장은 공공 자금, 소송으로 인한 복원 프로그램, 신기술의 발전에 힘입어 성장하고 있습니다.

세계의 PFAS 폐기물 관리 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 PFAS 폐기물 관리 시장 : 처리 기술별

제6장 PFAS 폐기물 관리 시장 : 서비스 유형별

제7장 PFAS 폐기물 관리 시장 : 최종 용도 산업별

제8장 PFAS 폐기물 관리 시장 : 지역별

제9장 경쟁 구도

제10장 기업 개요

제11장 조사 방법

제12장 부록

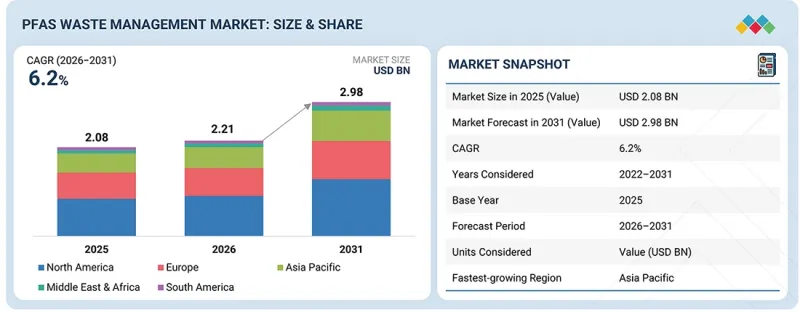

KSA 26.04.29The PFAS waste management market is projected to grow from USD 2.21 billion in 2026 to USD 2.98 billion by 2031, at a CAGR of 6.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million) |

| Segments | By Technology, Service Type, End-Use Industry, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

The off-site service segment in PFAS waste management involves the collection, transportation, and treatment of PFAS-contaminated materials at specialized external facilities. This approach is commonly used for highly concentrated or hazardous waste streams such as contaminated soil, sludge, spent activated carbon, and industrial residues that cannot be effectively treated on-site. Off-site facilities are equipped with advanced, large-scale treatment and destruction technologies capable of handling complex waste under controlled conditions, ensuring high efficiency and regulatory compliance.

''In terms of value, the municipal segment accounted for the largest share of the overall PFAS waste management market.''

The municipal sector requires water treatment technologies to deliver safe drinking water that meets government standards. Municipal utilities increasingly adopt advanced destruction solutions such as electrochemical oxidation, supercritical water oxidation, incineration, and others to treat contaminants, which include PFAS, heavy metals, and organic pollutants. The combination of increasing regulatory demands, the presence of outdated facilities, and heightened public health knowledge drives faster development of treatment system enhancements. Municipalities provide an ongoing market for PFAS waste management systems and advanced water treatment technologies.

"North America is projected to account for the largest market share during the forecast period.

North America is the largest market for advanced water treatment and PFAS treatment technologies. The market in the region is driven by stringent government regulations, the need for proper management of treatment residuals during PFAS treatment, and growing public awareness. Municipal utilities, industrial facilities, and defense sites heavily invest in destruction technologies and solidification to comply with stricter drinking water and discharge requirements.

The North America PFAS waste management market is also fueled by public funding, remediation programs that result from litigation, and the advancement of new technologies.

The primary sources used for this study have been divided based on the following three categories:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: Director Level - 70%, Managers - 20%, and Others - 10%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 30%, Middle East & Africa - 10%, and Latin America - 10%

The report provides a comprehensive analysis of company profiles:

The prominent companies in the market are Veolia (France), AECOM (US), WSP (Canada), Clean Earth (US), Indaver (Belgium), Jacobs (US), Aquatech (US), Battelle Memorial Institute (US), Ovivo Water Inc. (Canada), and Gradient (US)

Study Coverage

This research report categorizes the PFAS waste management market by technology (Destruction, Recycling & Recovery, and others), service type (On-Site, Off-Site), end-use industry (Industrial, Municipal, Commercial), and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the PFAS waste management market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers & acquisitions, and recent developments in the PFAS waste management market are covered. This report includes a competitive analysis of upcoming startups in the PFAS waste management market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall PFAS waste management market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising litigation and liability cost for polluters, growing public awareness of health risks associated with PFAS exposure), restraints (Limited availability of trained professionals), opportunities (Significant potential to expand globally), and challenges (Transportation and liability risks)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the PFAS waste management market

- Market Development: Comprehensive information about lucrative markets - the report analyses the PFAS waste management market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the PFAS waste management market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Veolia (France), AECOM (US), WSP (Canada), Clean Earth (US), Indaver (Belgium), Jacobs (US), Aquatech (US), Battelle Memorial Institute (US), Ovivo Water Inc. (Canada), and Gradient (US), among others, in the PFAS waste management market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PFAS WASTE MANAGEMENT MARKET

- 3.2 PFAS WASTE MANAGEMENT MARKET, BY TREATMENT TECHNOLOGY

- 3.3 PFAS WASTE MANAGEMENT MARKET, BY END-USE INDUSTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing regulatory scrutiny and tightening environmental regulations regarding PFAS contamination

- 4.2.1.2 Growing public awareness of health risks associated with PFAS exposure

- 4.2.1.3 Expansion of manufacturing, chemical processing, and semiconductor industries

- 4.2.1.4 Rising litigation and liability costs for polluters

- 4.2.2 RESTRAINTS

- 4.2.2.1 Expensive and complex process

- 4.2.2.2 Limited availability of trained professionals

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Implementation of stringent regulations

- 4.2.3.2 Significant government funding and support for PFAS research, development, and treatment efforts

- 4.2.4 CHALLENGES

- 4.2.4.1 Addressing emerging PFAS compounds and understanding their potential risks and treatment requirements

- 4.2.4.2 Development of practical and scalable technologies for semiconductor industry

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN PFAS WASTE MANAGEMENT MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

- 4.7 VALUE CHAIN ANALYSIS

- 4.7.1 RAW MATERIAL SUPPLIERS

- 4.7.2 PFAS FILTRATION TECHNOLOGY PROVIDERS

- 4.7.3 PFAS WATER TREATMENT TECHNOLOGY SUPPLIERS

- 4.7.4 PFAS DESTRUCTION AND HAZARDOUS WASTE MANAGEMENT SUPPLIERS

- 4.7.5 END USERS

- 4.8 PORTER'S FIVE FORCES ANALYSIS

- 4.8.1 THREAT OF NEW ENTRANTS

- 4.8.2 THREAT OF SUBSTITUTES

- 4.8.3 BARGAINING POWER OF SUPPLIERS

- 4.8.4 BARGAINING POWER OF BUYERS

- 4.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.9 PATENT ANALYSIS

- 4.9.1 METHODOLOGY

- 4.9.2 DOCUMENT TYPE

- 4.9.3 PUBLICATION TRENDS, 2016-2025

- 4.9.4 INSIGHTS

- 4.9.5 JURISDICTION ANALYSIS

- 4.9.6 TOP 10 PATENT OWNERS IN LAST 10 YEARS

- 4.10 ECOSYSTEM ANALYSIS

- 4.11 TRADE ANALYSIS

- 4.11.1 IMPORT SCENARIO FOR HS CODE 842121

- 4.11.2 EXPORT SCENARIO FOR HS CODE 842121

- 4.12 MACROECONOMIC OUTLOOK

- 4.12.1 SEMICONDUCTOR MANUFACTURING PLANTS

- 4.12.2 GDP TRENDS AND FORECASTS

- 4.13 TECHNOLOGY ANALYSIS

- 4.13.1 KEY EMERGING TECHNOLOGIES

- 4.13.1.1 DE-FLUORO

- 4.13.1.2 PFAS Annihilator

- 4.13.1.3 Obreak

- 4.13.2 COMPLEMENTARY TECHNOLOGIES

- 4.13.2.1 Foam fractionation

- 4.13.2.2 Sorption technology

- 4.13.2.3 Ion exchange resin

- 4.13.2.4 In situ remediation with colloidal activated carbon

- 4.13.2.5 Soil washing

- 4.13.2.6 Zeolite & clay minerals

- 4.13.1 KEY EMERGING TECHNOLOGIES

- 4.14 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 4.14.1 REGIONAL REGULATIONS AND COMPLIANCE

- 4.14.1.1 North America

- 4.14.1.2 Europe

- 4.14.1.3 Asia Pacific

- 4.14.1.4 Middle East & Africa and South America

- 4.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 4.14.1 REGIONAL REGULATIONS AND COMPLIANCE

- 4.15 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.16 KEY CONFERENCES & EVENTS IN 2026-2027

- 4.17 DECISION-MAKING PROCESS

- 4.18 KEY STAKEHOLDERS & BUYING CRITERIA

- 4.18.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 4.18.2 BUYING CRITERIA

- 4.18.2.1 Quality

- 4.18.2.2 Service

- 4.19 CASE STUDY ANALYSIS

- 4.19.1 MICHIGAN-BASED CENTRALIZED WASTE TREATMENT FACILITY

- 4.19.2 MIDWEST AIRPORT

- 4.19.3 THE PASSAIC VALLEY SEWERAGE COMMISSION

- 4.20 IMPACT OF 2025 US TARIFF - OVERVIEW

- 4.20.1 INTRODUCTION

- 4.20.2 KEY TARIFF RATES

- 4.20.3 PRICE IMPACT ANALYSIS

- 4.20.4 IMPACT ON COUNTRIES/REGIONS

- 4.20.4.1 US

- 4.20.4.2 Europe

- 4.20.4.3 Asia Pacific

- 4.20.5 IMPACT ON END-USE INDUSTRIES

- 4.21 INVESTMENT AND FUNDING SCENARIO

5 PFAS WASTE MANAGEMENT MARKET, BY TREATMENT TECHNOLOGY

- 5.1 INTRODUCTION

- 5.2 THERMAL DESTRUCTION

- 5.2.1 INCINERATION

- 5.2.2 THERMAL CARBON REACTIVATION

- 5.2.3 OTHER THERMAL DESTRUCTION TECHNOLOGIES

- 5.3 RECYCLING & RECOVERY

- 5.4 LANDFILLING

- 5.5 STABILISATION & SOLIDIFICATION

- 5.6 OTHER TECHNOLOGIES

6 PFAS WASTE MANAGEMENT MARKET, BY SERVICE TYPE

- 6.1 INTRODUCTION

- 6.2 ON-SITE

- 6.2.1 NEED FOR IMMEDIATE MITIGATION AND CONVENIENCE TO DRIVE DEMAND

- 6.3 OFF-SITE

- 6.3.1 SUITABILITY FOR ADOPTION IN MUNICIPAL & INDUSTRIAL SECTORS TO DRIVE MARKET

7 PFAS WASTE MANAGEMENT MARKET, BY END-USE INDUSTRY

- 7.1 INTRODUCTION

- 7.2 INDUSTRIAL

- 7.2.1 OIL & GAS

- 7.2.1.1 Stringent environmental regulations to drive market growth

- 7.2.2 PHARMACEUTICAL

- 7.2.2.1 Growing awareness of health and environmental impacts to drive demand

- 7.2.3 CHEMICAL MANUFACTURING

- 7.2.3.1 Stringent regulatory compliance and hazardous effluent management driving adoption

- 7.2.4 ELECTRONICS & SEMICONDUCTOR

- 7.2.4.1 Rising semiconductor waste complexity driving adoption of advanced PFAS destruction technologies

- 7.2.5 TEXTILE

- 7.2.5.1 Stringent discharge norms and sustainability mandates accelerating PFAS treatment in textile effluents

- 7.2.6 MILITARY

- 7.2.6.1 Legacy AFFF contamination driving large-scale PFAS remediation across defense sites

- 7.2.7 OTHER INDUSTRIAL SEGMENTS

- 7.2.1 OIL & GAS

- 7.3 COMMERCIAL

- 7.3.1 BALL MILLING AND ELECTROCHEMICAL OXIDATION ADOPTED AS EFFECTIVE METHODS IN COMMERCIAL SEGMENT

- 7.4 MUNICIPAL

- 7.4.1 DRINKING WATER TREATMENT

- 7.4.1.1 Stringent environmental regulations related to drinking water to drive market

- 7.4.2 WASTEWATER TREATMENT

- 7.4.2.1 Growing public concern to increase adoption

- 7.4.1 DRINKING WATER TREATMENT

8 PFAS WASTE MANAGEMENT MARKET, BY REGION

- 8.1 INTRODUCTION

- 8.2 NORTH AMERICA

- 8.2.1 US

- 8.2.1.1 Stringent regulations on PFAS contamination to drive market

- 8.2.2 CANADA

- 8.2.2.1 Rising government initiatives for PFAS removal to drive market

- 8.2.3 MEXICO

- 8.2.3.1 Increasing demand across industries to drive market

- 8.2.1 US

- 8.3 EUROPE

- 8.3.1 GERMANY

- 8.3.1.1 Upgradation of water treatment infrastructure to support adoption of advanced PFAS waste management solution

- 8.3.2 FRANCE

- 8.3.2.1 Growing focus on adherence to EU drinking water regulations to drive demand

- 8.3.3 UK

- 8.3.3.1 Universities and government funding PFAS removal projects to drive market

- 8.3.4 REST OF EUROPE

- 8.3.1 GERMANY

- 8.4 ASIA PACIFIC

- 8.4.1 CHINA

- 8.4.1.1 Stringent water treatment policies to support market growth

- 8.4.2 JAPAN

- 8.4.2.1 Growing pharmaceutical industry to drive market

- 8.4.3 AUSTRALIA

- 8.4.3.1 Stringent government regulations to increase adoption

- 8.4.4 REST OF ASIA PACIFIC

- 8.4.1 CHINA

- 8.5 MIDDLE EAST & AFRICA

- 8.5.1 GCC

- 8.5.1.1 Government focus on water and wastewater treatment to drive market

- 8.5.2 SOUTH AFRICA

- 8.5.2.1 Growth in mining industry to support market growth

- 8.5.3 REST OF MIDDLE EAST & AFRICA

- 8.5.1 GCC

- 8.6 SOUTH AMERICA

- 8.6.1 BRAZIL

- 8.6.1.1 Government support and regulations to drive market

- 8.6.2 ARGENTINA

- 8.6.2.1 Favorable locations for manufacturing and stringent water regulations to increase demand

- 8.6.3 REST OF SOUTH AMERICA

- 8.6.1 BRAZIL

9 COMPETITIVE LANDSCAPE

- 9.1 OVERVIEW

- 9.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 9.3 REVENUE ANALYSIS

- 9.4 MARKET SHARE ANALYSIS, 2025

- 9.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 9.5.1 STARS

- 9.5.2 EMERGING LEADERS

- 9.5.3 PERVASIVE PLAYERS

- 9.5.4 PARTICIPANTS

- 9.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 9.5.5.1 Company footprint

- 9.5.5.2 Region footprint

- 9.5.5.3 End-use industry footprint

- 9.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 9.6.1 PROGRESSIVE COMPANIES

- 9.6.2 RESPONSIVE COMPANIES

- 9.6.3 DYNAMIC COMPANIES

- 9.6.4 STARTING BLOCKS

- 9.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 9.6.5.1 Detailed list of key startups/SMEs

- 9.6.5.2 Competitive benchmarking of key startups/SMEs

- 9.7 COMPANY VALUATION AND FINANCIAL MATRIX

- 9.8 BRAND/PRODUCT COMPARISON

- 9.9 COMPETITIVE SCENARIO

- 9.9.1 PRODUCT LAUNCHES

- 9.9.2 DEALS

- 9.9.3 EXPANSIONS

10 COMPANY PROFILES

- 10.1 MAJOR PLAYERS

- 10.1.1 VEOLIA

- 10.1.1.1 Business overview

- 10.1.1.2 Products/Solutions/Services offered

- 10.1.1.3 Recent developments

- 10.1.1.3.1 Product launches

- 10.1.1.3.2 Deals

- 10.1.1.3.3 Expansions

- 10.1.1.4 MnM view

- 10.1.1.4.1 Key strengths

- 10.1.1.4.2 Strategic choices

- 10.1.1.4.3 Weaknesses and competitive threats

- 10.1.2 AECOM

- 10.1.2.1 Business overview

- 10.1.2.2 Products/Solutions/Services offered

- 10.1.2.3 Recent developments

- 10.1.2.3.1 Product launches

- 10.1.2.3.2 Deals

- 10.1.2.4 MnM view

- 10.1.2.4.1 Key strengths

- 10.1.2.4.2 Strategic choices

- 10.1.2.4.3 Weaknesses and competitive threats

- 10.1.3 WSP

- 10.1.3.1 Business overview

- 10.1.3.2 Products/Solutions/Services offered

- 10.1.3.3 Recent developments

- 10.1.3.3.1 Deals

- 10.1.3.4 MnM view

- 10.1.3.4.1 Key strengths

- 10.1.3.4.2 Strategic choices

- 10.1.3.4.3 Weaknesses and competitive threats

- 10.1.4 CLEAN EARTH

- 10.1.4.1 Business overview

- 10.1.4.2 Products/Solutions/Services offered

- 10.1.4.3 Recent developments

- 10.1.4.3.1 Product launches

- 10.1.4.3.2 Deals

- 10.1.4.3.3 Expansions

- 10.1.4.4 MnM view

- 10.1.5 BATTELLE MEMORIAL INSTITUTE

- 10.1.5.1 Business overview

- 10.1.5.2 Products/Solutions/Services offered

- 10.1.5.3 Recent developments

- 10.1.5.3.1 Product launches

- 10.1.5.3.2 Deals

- 10.1.5.4 MnM view

- 10.1.6 JACOBS

- 10.1.6.1 Business overview

- 10.1.6.2 Products/Solutions/Services offered

- 10.1.6.3 Recent developments

- 10.1.6.3.1 Deals

- 10.1.6.4 MnM view

- 10.1.6.4.1 Key strengths

- 10.1.6.4.2 Strategic choices

- 10.1.6.4.3 Weaknesses and competitive threats

- 10.1.7 INDAVER

- 10.1.7.1 Business overview

- 10.1.7.2 Products/Solutions/Services offered

- 10.1.7.3 MnM view

- 10.1.8 AQUATECH

- 10.1.8.1 Business overview

- 10.1.8.2 Products/Solutions/Services offered

- 10.1.8.2.1 Deals

- 10.1.8.3 MnM view

- 10.1.9 OVIVO WATER INC.

- 10.1.9.1 Business overview

- 10.1.9.2 Products/Solutions/Services offered

- 10.1.9.2.1 Deals

- 10.1.9.3 MnM view

- 10.1.10 GRADIANT

- 10.1.10.1 Business overview

- 10.1.10.2 Products/Solutions/Services offered

- 10.1.10.2.1 Product launches

- 10.1.10.2.2 Deals

- 10.1.10.2.3 Expansions

- 10.1.10.3 MnM view

- 10.1.1 VEOLIA

- 10.2 OTHER PLAYERS

- 10.2.1 ENVIROPACIFIC SERVICES LIMITED

- 10.2.2 CLAROS TECHNOLOGIES, INC.

- 10.2.3 AQUAGGA

- 10.2.4 ACLARITY, INC.

- 10.2.5 ENSPIRED SOLUTION

- 10.2.6 E2METRIX

- 10.2.7 374WATER

- 10.2.8 CALGON CARBON CORPORATION

- 10.2.9 AXINE WATER TECHNOLOGIES

- 10.2.10 SYNERGEN MET LIMITED

- 10.2.11 ONVECTOR LLC

- 10.2.12 AQUAGREEN

- 10.2.13 ARVIA

- 10.2.14 GENERAL ATOMICS

- 10.2.15 CLEAN HARBORS

11 RESEARCH METHODOLOGY

- 11.1 RESEARCH DATA

- 11.1.1 SECONDARY DATA

- 11.1.1.1 Key data from secondary sources

- 11.1.2 PRIMARY DATA

- 11.1.2.1 Key data from primary sources

- 11.1.2.2 Breakdown of interviews with experts

- 11.1.2.3 Key industry insights

- 11.1.1 SECONDARY DATA

- 11.2 MARKET SIZE ESTIMATION

- 11.2.1 TOP-DOWN APPROACH

- 11.2.2 BOTTOM-UP APPROACH

- 11.3 DATA TRIANGULATION

- 11.4 RESEARCH ASSUMPTIONS

- 11.5 RESEARCH LIMITATIONS

12 APPENDIX

- 12.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.2 CUSTOMIZATION OPTIONS

- 12.3 RELATED REPORTS

- 12.4 AUTHOR DETAILS