|

시장보고서

상품코드

2011931

디젤 발전기 시장 : 설계(고정형, 휴대형), 용도(스탠바이 전원, 피크 컷, 주전원 및 연속 전원), 최종사용자(산업용 및 상업용, 주거용), 정격출력, 지역별 - 세계 예측(-2031년)Diesel Generator Market by Design (Stationary, Portable), Application (Standby Power, Peak Shaving, Prime & Continuous Power), End User (Industrial, Commercial, Residential), Power Rating, Region - Global Forecast to 2031 |

||||||

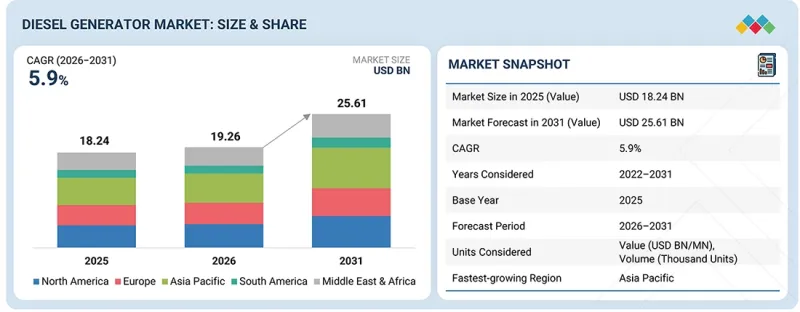

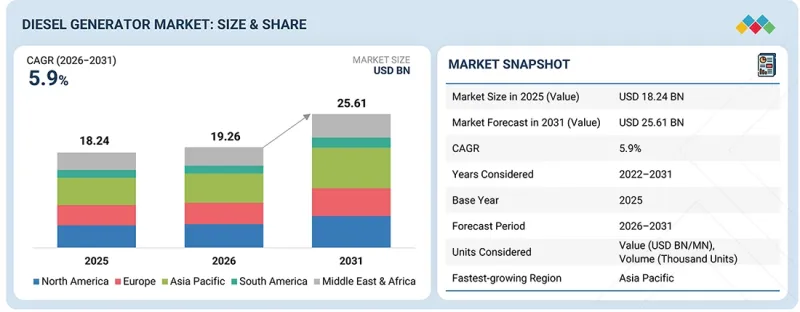

디젤 발전기 시장 규모는 2026년 192억 6,000만 달러에서 2031년까지 256억 1,000만 달러에 달할 것으로 예측되며, CAGR은 5.9%를 기록할 전망입니다.

주요 경제권에서 데이터센터, 의료 시설, 통신 인프라, 산업 프로젝트의 급속한 확장은 노후화된 전력망에 부담을 주고 있으며, 안정적인 대기 전력 및 주전원 공급을 보장하기 위한 첨단 디젤 발전기 솔루션에 대한 수요를 증가시키고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 설계, 용도, 정격출력, 최종사용자, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

인도, 중국 및 기타 신흥 시장에서는 제조 기지, 상업 시설, 원격지 광산, 인프라 프로젝트에서 대용량 디젤 발전기가 백업 전원으로 널리 사용되고 있습니다. 이러한 응용 분야에는 자동 부하 분산, 저배출 제어, 축전지 및 재생에너지와의 하이브리드 통합, 고급 모니터링 등 계통 지원 기능을 갖춘 스마트 디젤 발전기가 채택되고 있습니다. 디젤 발전기는 현재 현대의 전력 신뢰성 및 에너지 안보 시스템에서 핵심적인 역할을 하고 있습니다.

미국 및 기타 선진국에서는 전력망 복원력, 비상 대응, 국내 제조업에 대한 인센티브에 초점을 맞춘 지원 정책으로 인해 중요 인프라의 확장, 급속한 도시화, 안정적인 전력에 대한 수요가 가속화되고 있습니다. 이를 통해 전자식 엔진 관리, 디지털 모니터링, 예지보전, 배출가스 규제 대응(Tier 4/StageV) 및 하이브리드 기능을 갖춘 차세대 디젤 발전기의 보급을 촉진하고 있습니다. 이러한 추세는 운영 탄력성, 비즈니스 연속성, 에너지 안보를 향상시키고, 전 세계 인프라와 경제 성장을 지원하는 데 있어 디젤 발전기의 역할을 강화하고 있습니다.

"예측 기간 동안 대기 전력 공급이 가장 큰 응용 분야가 될 것으로 예상됩니다."

이는 주로 주택, 상업시설, 데이터센터, 의료시설, 통신 인프라, 산업용 백업 전원으로 광범위하게 사용되기 때문입니다. 이러한 용도의 디젤 발전기는 일반적으로 정전 시 신속하고 안정적인 비상 전력을 공급하여 비즈니스 연속성을 보장하고 중요한 업무를 보호하기 위해 사용됩니다. 디젤 발전기는 빠른 자동 시동, 높은 서지 전류 대응, 자동 전환 스위치(ATS)와의 원활한 연동이 가능하기 때문에 분산형 전원 시스템에 특히 적합합니다. 또한, 주택 및 중소형 상업 시설에서 하이브리드 디젤 발전 시스템의 인기가 높아짐에 따라 이 부문은 더욱 탄력을 받고 있습니다. 이러한 시스템은 축전지, 태양광발전, 스마트 에너지 관리 플랫폼과의 통합을 통해 연료 사용의 최적화와 배출가스 감소를 실현할 수 있습니다. 또한, 대기 전원공급장치 카테고리는 신흥국에서의 도입 증가의 혜택을 누리고 있습니다. 이들 국가에서는 불안정한 전력망 인프라, 잦은 정전, 증가하는 전력 수요 등이 도입을 부추기고 있습니다. 예비 디젤 발전기는 대규모 광업, 석유 및 가스 또는 유틸리티 프로젝트에서 일반적으로 사용되는 상시 가동 또는 주전원 장치에 비해 비용 효율적이고 설치가 용이하며 유지보수가 적습니다.

"예측 기간 동안 상업용 부문이 최종사용자 부문 중 가장 빠른 성장을 보일 것으로 예상됩니다."

데이터센터, 의료 시설, 숙박 산업, 복합 소매 시설, 오피스 빌딩, 교육 기관, 통신 인프라의 급속한 확장으로 인해 예측 기간 동안 상업용 부문은 디젤 발전기 시장에서 가장 높은 성장률을 기록할 것으로 예상됩니다. 비즈니스 연속성, 운영 탄력성 유지, 잦은 정전, 이상기후, 전압 변동으로부터 보호하기 위해 주요 경제권의 상업시설은 신뢰할 수 있는 백업 전원 솔루션을 적극적으로 요구하고 있습니다. 이 디젤 발전기는 고부하 수요에 대응하고 빠른 기동 및 자동 전환 기능을 제공하도록 설계되었으며, 부하 관리 시스템, 병렬 운전 제어, 저배출 기술, 배터리 및 재생에너지 원과의 원활한 하이브리드 통합과 같은 고급 기능을 갖추고 있습니다. 상업용 디젤 발전기는 점점 더 고도화되고 있으며, 간헐적인 재생에너지의 도입이 증가하는 상황에서도 안정적이고 신뢰할 수 있는 대기 전원 또는 주전원으로 공급할 수 있습니다. 모듈식 아키텍처, 원격 진단, 디지털 플랫폼을 통한 예지보전, SCADA 통합을 갖춘 최신 디젤 발전기는 효율적인 플랜트 모니터링과 시설 성능 최적화를 가능하게 합니다.

"예측 기간 동안 북미가 디젤 발전기 시장에서 두 번째로 큰 시장 규모가 될 것으로 예상됩니다."

예측 기간 동안 북미는 디젤 발전기 시장에서 두 번째로 큰 시장이 될 것으로 예상됩니다. 이러한 성장은 인프라 개발의 활성화, 데이터센터 및 상업 시설의 급속한 확장, 미국과 캐나다의 잦은 정전, 이상 기후, 노후화된 전력 인프라를 배경으로 신뢰할 수 있는 백업 전원공급장치에 대한 전반적인 수요에 의해 주도되고 있습니다. 이 지역에서는 유틸리티 및 산업 규모의 프로젝트가 지속적으로 크게 증가하고 있으며, 건설 활동, 의료 시설, 통신 타워, 석유 및 가스 사업도 빠르게 확대되고 있으며, 이 모든 분야에서 지속적인 전력 공급을 보장하기 위해 고급 디젤 발전기 기술이 필요합니다. 중요 인프라 복원력에 대한 인센티브, 국내 제조업 지원, 비상 대응에 대한 투자 등의 지원책도 디젤 발전기에 대한 수요를 촉진하고 있습니다. 또한, 북미의 전력회사와 최종사용자는 간헐적 재생에너지(IBR)의 고도의 통합으로 인해 발생하는 문제, 즉 시스템 관성 저하, 전압 변동, 신속한 백업 대응의 필요성 등을 해결하기 위해 보다 스마트하고 효율적인 디젤 발전기를 도입하고 있습니다.

세계의 디젤 발전기(Diesel Generator) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 디젤 발전기 시장 : 설계별

제10장 디젤 발전기 시장 : 용도별

제11장 디젤 발전기 시장 : 출력 정격별

제12장 디젤 발전기 시장 : 최종사용자별

제13장 디젤 발전기 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.04.30The diesel generator market is expected to reach USD 25.61 billion by 2031, from USD 19.26 billion in 2026, with a CAGR of 5.9%. The rapid growth of data centers, healthcare facilities, telecommunications infrastructure, and industrial projects in major economies is straining aging power grids and driving the demand for advanced diesel generator solutions to ensure reliable standby and primary power.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Design, Application, Power Rating, End User, & Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, South America |

In India, China, and other emerging markets, high-capacity diesel generators are being widely used for backup power in manufacturing hubs, commercial complexes, remote mining sites, and infrastructure projects. These applications involve smart diesel generators with grid-support features such as automatic load sharing, low-emission controls, hybrid integration with battery storage and renewables, and advanced monitoring. Diesel generators now play a central role in modern power reliability and energy security systems.

The growth of critical infrastructure, rapid urbanization, and the need for reliable power in the US and other developed nations is accelerating due to supportive policies focused on grid resilience, emergency preparedness, and incentives for domestic manufacturing. This encourages widespread use of next-generation diesel generators featuring electronic engine management, digital monitoring, predictive maintenance, reduced emissions compliance (Tier 4/Stage V), and hybrid capabilities. These trends are enabling greater operational resilience, business continuity, and energy security, reinforcing the role of diesel generators in supporting global infrastructure and economic growth.

"Standby power is expected to be the largest application segment during the forecast period."

The standby power segment is expected to hold the largest share in the diesel generator market during the forecast period, mainly due to its widespread use in residential buildings, commercial complexes, data centers, healthcare facilities, telecommunication infrastructure, and industrial backup power. Diesel generators in these applications are typically used to provide quick and reliable emergency power during grid outages, ensuring business continuity and protecting critical operations. They are particularly well-suited for distributed power setups because they can start automatically quickly, handle high surges, and seamlessly integrate with automatic transfer switches (ATS). Additionally, this segment is gaining strength because of the rising popularity of hybrid diesel generator systems in residential and small-to-medium commercial settings. These systems enable integration with battery storage, solar PV, and smart energy management platforms to optimize fuel use and cut emissions. The standby power category also benefits from increased installations in emerging economies, where unreliable grid infrastructure, frequent power outages, and growing electricity demand are boosting adoption. Standby diesel generators are cost-effective, easy to install, and require less maintenance compared to continuous or prime power units commonly used in large-scale mining, oil and gas, or utility projects.

"Commercial is expected to be the fastest-growing end user segment during the forecast period."

The commercial segment is expected to record the fastest growth in the diesel generator market during the forecast period due to rapid expansion in data centers, healthcare facilities, hospitality, retail complexes, office buildings, educational institutions, and telecommunications infrastructure. To maintain business continuity, operational resilience, and protection against frequent grid outages, extreme weather events, and voltage fluctuations, commercial establishments in large economies are actively seeking reliable backup power solutions. These diesel generators are designed to handle high load demands, provide quick start-up and automatic transfer capabilities, and include advanced features such as load management systems, paralleling controls, low-emission technologies, and seamless hybrid integration with batteries and renewable energy sources. Commercial-scale diesel generators are becoming more sophisticated, enabling stable and reliable standby or prime power even as the integration of intermittent renewable resources increases. The ability to monitor plants efficiently and optimize facility performance has been enhanced by modern diesel generators with modular architectures, remote diagnostics, predictive maintenance via digital platforms, and SCADA integration.

"North America is expected to be the second-largest market for diesel generators during the forecast period."

North America is expected to be the second-largest market for diesel generators during the forecast period. The growth is driven by high infrastructure development, rapid expansion of data centers and commercial facilities, and the overall need for reliable backup power amid frequent grid outages, extreme weather events, and aging power infrastructure in both the US and Canada. The region continues to see a significant influx of utility-scale and industrial projects, along with a rapid increase in construction activities, healthcare facilities, telecommunications towers, and oil & gas operations, all of which require advanced diesel generator technology to ensure a continuous power supply. Supportive policies, such as incentives for critical infrastructure resilience, backing for domestic manufacturing, and investments in emergency preparedness, are also fueling demand for diesel generators. Additionally, utilities and end users in North America are adopting smarter and more efficient diesel generators to address challenges posed by the high integration of intermittent renewable resources (IBRs), including reduced system inertia, voltage fluctuations, and the need for quick backup response.

In-depth interviews have been conducted with key industry participants, subject-matter experts, C-level executives of leading market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and to assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 45%, Tier 2 - 30%, and Tier 3 - 25%

By Designation: C-level Executives - 35%, Directors - 25%, and Others - 40%

By Region: Asia Pacific - 60%, Europe - 15%, North America - 10%, Middle East & Africa - 10%, and South America - 5%

Caterpillar (US), Cummins Inc. (US), Generac Power Systems, Inc. (US), Rolls-Royce plc (UK), and MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan) are the major players in the diesel generator market. The study includes an in-depth competitive analysis of these key players, including their company profiles, recent developments, and key market strategies.

Research Coverage:

The report defines, describes, and forecasts the global diesel generator market by design, power rating, application, end user, and region. It also provides a detailed qualitative and quantitative analysis of the market. The report thoroughly reviews the main market drivers, restraints, opportunities, and challenges. It further covers various key aspects of the market, including an analysis of the competitive landscape, market dynamics, market size estimates in value, and future trends in the diesel generator industry.

Key Benefits of Buying the Report

- It provides an analysis of key drivers (Increasing demand for reliable backup power, Growth of data centers and telecom infrastructure), restraints (Growing adoption of renewable energy, Volatility in diesel fuel prices), opportunities (Rapid urbanization and infrastructure development, Rising electrification in emerging regions), challenges (Adoption of stringent governmental regulations directed toward reaching net-zero emissions, High operational and maintenance costs) influencing the diesel generator market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the diesel generator market across varied regions.

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the diesel generator market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Caterpillar (US), Cummins Inc., (US), Generac Power Systems (US), Rolls-Royce PLC (UK), Mitsubishi Heavy Industries, Ltd (Japan), Rehlko (US), Atlas Copco (Sweden), Yamaha Motor Co., Ltd. (Japan), Hyundai Power Products (South Korea), Yanmar Holdings Co., Ltd. (Japan), Kirloskar (India), Denyo Co., Ltd (Japan), KUBOTA Corporation (Japan), Mahindra Powerol (India), Wartsila (Finland), Himalayan Power Machines Mfg Co (India), Aksa Jenerator Sanayi A.S. (Turkey), ASHOK LEYLAND (India), Greaves Cotton Limited (India), Weifang Haitai Power Machinery Co., Ltd (China), Anglo Belgian Corporation nv (Belgium), Doosan Bobcat (South Korea), JC Bamford Excavators (UK), Carrier (US), and EVERLLENCE (Germany), among others.

- Product Innovation/Development: Product introduction and upgrades in diesel generators are high in this market, particularly with the integration of advanced electronic engine control systems, smart digital monitoring, and predictive maintenance mechanisms. Sustainable developments, including Tier 4 Final/Stage V emission-compliant engines, selective catalytic reduction (SCR), diesel particulate filters (DPF), and exhaust gas recirculation (EGR) technologies, are increasingly gaining ground. Advanced fuel injection systems, variable speed engines, hybrid-ready designs, and compact modular configurations are finding more applications in backup power, prime power, renewable integration, data centers, healthcare, telecommunications, and remote/off-grid systems. The development of hybrid solutions is also advancing rapidly, with improved digital controls, artificial intelligence (AI)-based predictive maintenance and fuel optimization, remote monitoring platforms, and seamless integration with solar PV, battery storage, and microgrids. These innovations simplify deployment, reduce fuel consumption and emissions, enable easy scalability, lower operating costs, and offer better load response, frequency regulation, voltage stability, and overall system reliability for modern power needs.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTION SHAPING DIESEL GENERATOR MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DIESEL GENERATOR MARKET

- 3.2 DIESEL GENERATOR MARKET, BY DESIGN AND REGION

- 3.3 DIESEL GENERATOR MARKET, BY DESIGN

- 3.4 DIESEL GENERATOR MARKET, BY APPLICATION

- 3.5 DIESEL GENERATOR MARKET, BY POWER RATING

- 3.6 DIESEL GENERATOR MARKET, BY END USER

- 3.7 DIESEL GENERATOR MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for reliable backup power

- 4.2.1.2 Growth of data centers and telecom infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 Growing adoption of renewable energy

- 4.2.2.2 Volatility in diesel fuel prices

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing urbanization and infrastructure development

- 4.2.3.2 Rising electrification in developing regions

- 4.2.4 CHALLENGES

- 4.2.4.1 Adoption of stringent governmental regulations directed toward reaching net-zero emissions

- 4.2.4.2 High maintenance and operating costs

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL DIESEL GENERATOR INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF DIESEL GENERATORS, BY POWER RATING (2022-2025)

- 5.5.2 AVERAGE SELLING PRICE OF DIESEL GENERATORS, BY REGION (2022-2025)

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8502)

- 5.6.2 EXPORT SCENARIO (HS CODE 8502)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 NUCLEAR PLANT EDG REBUILD

- 5.10.2 MINING SITE PRIME POWER

- 5.11 IMPACT OF US TARIFFS-DIESEL GENERATOR MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.4 South America

- 5.11.4.5 Middle East and Africa

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 HYBRID DIESEL GENERATOR SYSTEMS

- 6.1.2 REMOTE MONITORING AND IOT

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 EMISSION-CONTROL RETROFIT DEVICES

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON DIESEL GENERATOR MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN DIESEL GENERATOR MARKET

- 6.6.3 CASE STUDIES OF AI/GEN AI IMPLEMENTATION IN DIESEL GENERATOR MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI/GEN AI IN DIESEL GENERATOR MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF DIESEL GENERATORS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

- 8.5 MARKET PROFITABILITY

9 DIESEL GENERATOR MARKET, BY DESIGN

- 9.1 INTRODUCTION

- 9.2 STATIONARY

- 9.2.1 RISING ELECTRICITY DEMAND AND INFRASTRUCTURE GROWTH TO BOOST THE MARKET

- 9.3 PORTABLE 106 9.3.1 RISING DEMAND FOR MOBILE AND TEMPORARY POWER SOLUTIONS TO BOOST MARKET

10 DIESEL GENERATOR MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 STANDBY POWER

- 10.2.1 INCREASING PARTNERSHIPS AMONG COMPANIES OFFERING STANDBY DIESEL GENERATORS TO DRIVE MARKET

- 10.3 PEAK SHAVING

- 10.3.1 IMPROVED POWER QUALITY, REDUCED CARBON EMISSIONS, INCREASED OPERATIONAL RELIABILITY, AND ENERGY EFFICIENCY TO DRIVE DEMAND

- 10.4 PRIME & CONTINUOUS POWER

- 10.4.1 RISING USE OF PRIME & CONTINUOUS GENERATORS IN REMOTE LOCATIONS OR HARD-TO-ACCESS AREAS TO DRIVE MARKET

11 DIESEL GENERATOR MARKET, BY POWER RATING

- 11.1 INTRODUCTION

- 11.2 UP TO 50 KW

- 11.2.1 INCREASING DEMAND FROM SMALL-SCALE BUSINESSES AND HOMEOWNERS TO BOOST MARKET GROWTH

- 11.3 51-280 KW

- 11.3.1 GROWING USE AT REMOTE CONSTRUCTION SITES AND IN TELECOM, MINING, AND SMALL OIL & GAS PROJECTS TO DRIVE MARKET

- 11.4 281-500 KW

- 11.4.1 RISING DEMAND IN OIL & GAS AND MINING INDUSTRIES TO FUEL MARKET GROWTH

- 11.5 501-2,000 KW

- 11.5.1 RISING DEPLOYMENT IN INDUSTRIES AND COMMERCIAL SECTOR TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- 11.6 ABOVE 2,000 KW

- 11.6.1 GROWING NEED FOR UNINTERRUPTED POWER SUPPLY IN MARINE INDUSTRY TO DRIVE DEMAND

12 DIESEL GENERATOR MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 INDUSTRIAL

- 12.2.1 UTILITIES/POWER GENERATION

- 12.2.1.1 Rising use of diesel generators by utilities in emergencies for generating electricity to drive market

- 12.2.2 OIL & GAS

- 12.2.2.1 Growing use of diesel generators during drilling and digging activities to drive market

- 12.2.3 CONSTRUCTION

- 12.2.3.1 Low maintenance and operational costs to drive demand

- 12.2.4 MANUFACTURING

- 12.2.4.1 Capability to deliver uninterrupted power to manufacturing units during grid failure and voltage fluctuations to fuel demand

- 12.2.5 MINING & METALS

- 12.2.5.1 Lack of access to power grids to fuel demand

- 12.2.6 MARINE

- 12.2.6.1 Low fuel consumption, high thermal efficiency, and adaptability to various conditions to drive demand

- 12.2.7 OTHER INDUSTRIAL END USERS

- 12.2.1 UTILITIES/POWER GENERATION

- 12.3 COMMERCIAL

- 12.3.1 TELECOM

- 12.3.1.1 Requirement for uninterrupted power supply to drive demand

- 12.3.2 HEALTHCARE

- 12.3.2.1 Stringent regulations for hospital backup generators to drive demand

- 12.3.3 DATA CENTERS

- 12.3.3.1 Explosive growth of hyperscale and AI-driven data centers to boost market

- 12.3.4 OTHER COMMERCIAL END USERS

- 12.3.1 TELECOM

- 12.4 RESIDENTIAL

- 12.4.1 INCREASING DEMAND FOR DIESEL GENERATORS IN BLACKOUT-PRONE AREAS TO DRIVE MARKET

13 DIESEL GENERATOR MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Massive data center expansion and rising grid reliability concerns to drive diesel generator market growth

- 13.2.2 CANADA

- 13.2.2.1 Surging data center investments and climate-driven resilience needs to fuel diesel generator demand

- 13.2.3 MEXICO

- 13.2.3.1 Industrial expansion, data center boom, and grid instability to accelerate growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Data center boom, grid constraints, and energy security needs to accelerate market growth

- 13.3.2 FRANCE

- 13.3.2.1 Nuclear-dominated grid, data center surge, and energy security priorities to propel market growth

- 13.3.3 GERMANY

- 13.3.3.1 Data center expansion, industrial resilience, and strict emission regulations to drive market growth

- 13.3.4 RUSSIA

- 13.3.4.1 Remote industrial operations, oil & gas expansion, and energy security needs to drive market growth

- 13.3.5 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Diesel generator demand fueled by industrialization, grid gaps, and data center expansion

- 13.4.2 INDIA

- 13.4.2.1 Power shortages and infrastructure boom propel market growth

- 13.4.3 JAPAN

- 13.4.3.1 Disaster resilience and critical infrastructure needs driving market growth

- 13.4.4 SOUTH AMERICA

- 13.4.4.1 Semiconductor dominance and industrial reliability needs driving market growth

- 13.4.5 AUSTRALIA

- 13.4.5.1 Grid gaps and infrastructure growth anchor diesel generator market

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Industrial expansion, mining revival, and persistent grid challenges to accelerate growth of the diesel generator market

- 13.5.2 ARGENTINA

- 13.5.2.1 Oil & gas development, mining growth, and economic volatility to accelerate growth

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Data center expansion to propel demand for diesel generators

- 13.6.1.2 Saudi Arabia

- 13.6.1.2.1 Oil & gas-led demand, industrial expansion, and grid-resilience driving market growth

- 13.6.1.3 UAE

- 13.6.1.3.1 Hydrocarbon-driven demand and diversification efforts to support market growth

- 13.6.1.4 Rest of GCC countries

- 13.6.2 ALGERIA

- 13.6.2.1 Grid instability and industry adoption drive strategic backup power deployment

- 13.6.3 NIGERIA

- 13.6.3.1 Increasing investments in telecommunications industry to drive demand

- 13.6.4 SOUTH AFRICA

- 13.6.4.1 Persistent load shedding drives diesel generator reliance

- 13.6.5 REST OF MIDDLE EAST

- 13.6.1 GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 14.3 MARKET SHARE ANALYSIS, 2025

- 14.4 REVENUE ANALYSIS, 2021-2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Design footprint

- 14.7.5.4 Application footprint

- 14.7.5.5 End-user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 CATERPILLAR

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses/Competitive threats

- 15.1.2 CUMMINS INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses/Competitive threats

- 15.1.3 GENERAC POWER SYSTEMS, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths/Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses/Competitive threats

- 15.1.4 ROLLS-ROYCE PLC

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Services/Solutions offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses/Competitive threats

- 15.1.5 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses/Competitive threats

- 15.1.6 WARTSILA

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Other developments

- 15.1.7 ATLAS COPCO AB

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Services/Solutions offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.8 YAMAHA MOTOR CO., LTD.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Services/Solutions offered

- 15.1.9 DOOSAN BOBCAT

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Expansions

- 15.1.10 CARRIER

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Other developments

- 15.1.11 ASHOK LEYLAND

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.11.3.2 Expansions

- 15.1.12 KIRLOSKAR

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches

- 15.1.13 GREAVES COTTON LIMITED

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.14 DENYO CO., LTD.

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.15 KUBOTA CORPORATION

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.1 CATERPILLAR

- 15.2 OTHER PLAYERS

- 15.2.1 REHLKO

- 15.2.2 HYUNDAI POWER PRODUCTS

- 15.2.3 MAHINDRA POWEROL

- 15.2.4 ANGLO BELGIAN CORPORATION NV

- 15.2.5 JC BAMFORD EXCAVATORS LTD.

- 15.2.6 AKSA POWER GENERATION

- 15.2.7 YANMAR HOLDINGS CO., LTD

- 15.2.8 EVERLLENCE

- 15.2.9 HIMALAYAN POWER MACHINES MFG CO.

- 15.2.10 WEIFANG HAITAI POWER MACHINERY CO., LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.2 SECONDARY AND PRIMARY RESEARCH

- 16.2.1 SECONDARY DATA

- 16.2.1.1 List of key secondary sources

- 16.2.1.2 Key data from secondary sources

- 16.2.2 PRIMARY DATA

- 16.2.2.1 List of primary interview participants

- 16.2.2.2 Key industry insights

- 16.2.2.3 Breakdown of primaries

- 16.2.2.4 Key data from primary sources

- 16.2.1 SECONDARY DATA

- 16.3 MARKET SIZE ESTIMATION METHODOLOGY

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.2 TOP-DOWN APPROACH

- 16.3.3 DEMAND-SIDE ANALYSIS

- 16.3.3.1 Demand-side assumptions

- 16.3.3.2 Demand-side calculations

- 16.3.4 SUPPLY-SIDE ANALYSIS

- 16.3.4.1 Supply-side assumptions

- 16.3.4.2 Supply-side calculations

- 16.4 GROWTH FORECAST

- 16.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 16.6 RESEARCH LIMITATIONS

- 16.7 SCOPE LIMITATIONS

- 16.8 RISK ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS