|

시장보고서

상품코드

2013042

가상 의료 어시스턴트용 AI 시장 : 제공(앱, EHR/EMR, IoT), 모드(텍스트, 멀티모달, 아바타), 용도(워크플로우, 트리아지, RPM, 스케줄링, 청구), 최종사용자, 사용 사례(환자 액세스, 정신건강), 지역별 - 세계 예측(-2030년)AI in Virtual Medical Assistants Market by Offering (Apps, EHR/EMR, IoT), Mode (Text, Multimodal, Avatar), Application (Workflow, Triage, RPM, Scheduling, Billing), End User, Use Case (Patient Access, Mental Health) & Region - Global Forecast to 2030 |

||||||

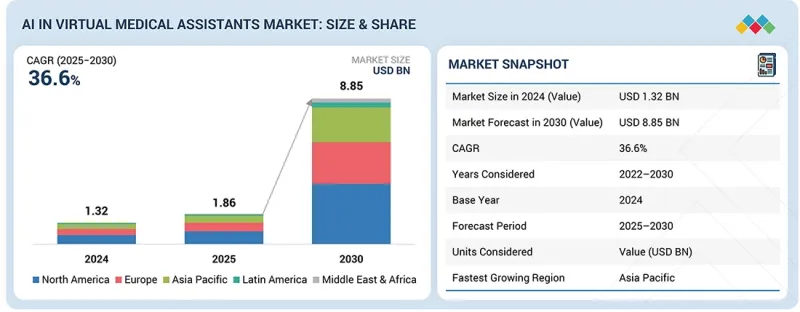

가상 의료 어시스턴트용 AI 시장 규모는 2025년에 18억 6,000만 달러로 평가되었으며, 2030년까지 88억 5,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR은 36.6%로 성장할 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 제공·인터랙션 모드·용도·최종사용자·지역별 |

| 대상 지역 | 북미·유럽·아시아태평양·라틴아메리카·중동 및 아프리카 |

시장 성장은 AI의 급속한 발전, 24시간 365일 의료 서비스에 대한 수요 증가, 의료 시스템에 대한 압력 증가, 스마트폰과 디지털 플랫폼의 보급, 맞춤형 의료 및 예방 의료로의 전환에 의해 주도되고 있습니다. 자연어 처리(NLP), 감정 인식, 전자건강기록(EHR)과의 통합과 같은 혁신이 기능을 향상시키는 한편, 전문 임상 지식 기반은 특히 종양학 및 당뇨병 관리에서 질병 및 전문 분야에 특화된 진료를 지원합니다.

최종사용자별로는 2024년 의료 서비스 제공자 부문이 가장 큰 점유율을 차지했습니다.

이는 주로 관리 업무의 부담을 줄이면서 임상적 효율성과 환자 참여도를 높여야 할 필요성이 높아졌기 때문입니다. 의료 서비스 제공자는 예약 관리, 의료 기록, 의료 기록, 선별 진료, 환자와의 소통을 효율화하기 위해 AI 기반 가상 비서를 점점 더 많이 도입하고 있습니다. 이를 통해 의사와 직원들은 직접적인 환자 치료에 더 집중하고, 워크플로우 관리를 개선하며, 비용을 절감하고, 더 나은 임상적 의사결정을 내릴 수 있습니다. 그 결과, 이 부문에서의 도입이 계속 확대되고 있습니다.

제공 부문별로는 EHR/EMR 통합 시스템이 예측 기간 동안 가장 빠르게 성장할 것으로 예상됩니다.

이 부문의 급속한 성장은 의료 네트워크 전반의 원활한 상호운용성과 환자 데이터에 대한 통합된 접근에 대한 요구가 증가함에 따라 이루어지고 있습니다. EHR/EMR 플랫폼에 AI 가상 의료 도우미를 통합함으로써 종합적인 건강 기록을 기반으로 한 자동화된 문서화, 실시간 임상 의사결정 지원, 개인화된 환자 참여가 가능해집니다. 이를 통해 진료 연계 및 워크플로우의 효율성을 향상시킬 뿐만 아니라, 규제 준수 및 가치 기반 진료에 대한 노력을 지원할 수 있기 때문에 EHR/EMR 통합 시스템에 대한 수요가 증가하고 있습니다.

2024년에는 북미 시장이 가장 큰 점유율을 차지했습니다.

북미에서는 증상 확인, 예약 조정, 복약 관리 등 편의성이 높은 디지털 의료 서비스에 대한 수요 증가를 배경으로 AI 기반 가상 의료 도우미(VHA)의 성장세가 두드러지고 있습니다. VHA는 워크플로우 효율화, 환자 분류 및 일상적인 대응을 지원하기 위해 의료 인력 부족으로 인해 도입이 더욱 가속화되고 있습니다. 자연어 처리(NLP), 머신러닝, 대화형 AI의 발전으로 정확성과 신뢰성이 향상되어 의료진과 환자 모두의 신뢰가 높아지고 있습니다. 웨어러블 기기 및 원격 모니터링과의 연계를 통해 실시간 건강 상태 파악 및 예방적 관리가 가능해지는 한편, 정신건강 및 행동의학에 대한 관심이 높아지면서 스트레스 관리 및 치료 순응도 지원에도 VHA의 활용 범위가 넓어지고 있습니다. 또한, 비용 절감에 대한 재정적 압박과 팬데믹 이후 원격의료의 지속적인 도입으로 인해 VHA는 진료 조정, 환자 참여, 디지털 헬스케어 제공에 있어 필수적인 도구로 자리매김하고 있습니다.

세계의 가상 의료 어시스턴트용 AI 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

제6장 가상 의료 어시스턴트용 AI 시장 : 제공별

제7장 가상 의료 어시스턴트용 AI 시장 : 인터랙션 모드별

제8장 가상 의료 어시스턴트용 AI 시장 : 용도별

제9장 가상 의료 어시스턴트용 AI 시장 : 최종사용자별

제10장 가상 의료 어시스턴트용 AI 시장 : 지역별

제11장 경쟁 구도

제12장 기업 개요

제13장 부록

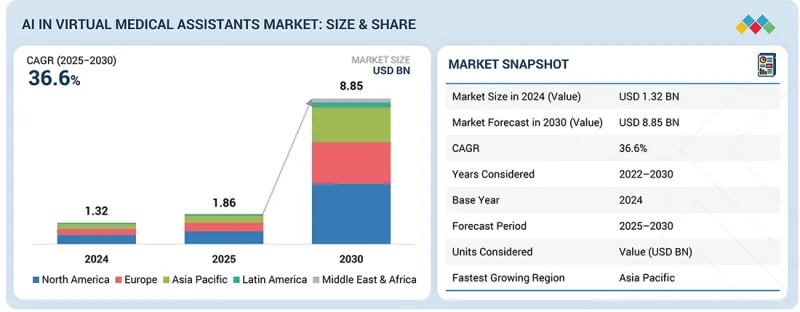

KSM 26.04.30The AI in virtual medical assistants market was valued at USD 1.86 billion in 2025 and is estimated to reach USD 8.85 billion by 2030, registering a CAGR of 36.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Offering, Mode of Interaction, Application, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

Market growth is fueled by rapid AI advances, the growing need for 24/7 healthcare access, mounting pressure on healthcare systems, the widespread adoption of smartphones and digital platforms, and a shift toward personalized and preventive care. Innovations like natural language processing (NLP), emotion recognition, and EHR integration are improving functionality, while specialized clinical knowledge bases support disease- and specialty-specific care, especially in oncology and diabetes management.

Based on end user, the healthcare provider segment dominated the AI in virtual medical assistants market in 2024

The healthcare provider segment had the largest share of the AI in virtual medical assistants market in 2024. This is mainly driven by the increasing need to improve clinical efficiency and patient engagement while reducing administrative workloads. Healthcare providers are more frequently adopting AI-powered virtual assistants to streamline appointment scheduling, medical documentation, triage, and patient communication. This allows physicians and staff to focus more on direct patient care, improve workflow management, lower costs, and support better clinical decision-making. As a result, adoption in this segment continues to grow.

By offering EHR/EMR integrated systems, it is expected to be the fastest growing segment during the study period.

The rapid growth of the EHR/EMR integrated systems segment is fueled by the rising need for seamless interoperability and unified access to patient data across healthcare networks. Incorporating AI-enabled virtual medical assistants into EHR/EMR platforms enables automated documentation, real-time clinical decision support, and personalized patient engagement based on comprehensive health records. This not only improves care coordination and workflow efficiency but also helps ensure regulatory compliance and supports value-based care initiatives, thereby increasing demand for EHR/EMR integrated systems in AI-powered virtual medical assistants market.

The North American market accounted for the largest share of the AI in virtual medical assistants market in 2024.

North America is experiencing significant growth in AI-enabled virtual medical assistants (VHAs), driven by increasing demand for convenient digital healthcare services such as symptom checking, appointment scheduling, and medication management. Healthcare professional shortages are further speeding up adoption, as VHAs help streamline workflows, triage patients, and handle routine interactions. Advances in NLP, machine learning, and conversational AI are enhancing their accuracy and reliability, increasing trust among providers and patients. Integration with wearables and remote monitoring offers real-time health insights and proactive care, while the growing focus on mental and behavioral health is broadening their use in stress management and therapy adherence. Additionally, financial pressures to cut costs and the continued adoption of telehealth after the pandemic are solidifying VHAs as essential tools for care coordination, patient engagement, and digital healthcare delivery.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the AI in virtual medical assistants market.

The breakdown of primary participants is as mentioned below:

- By Company Type - Tier 1 (41%), Tier 2 (31%), and Tier 3 (28%)

- By Designation - C-level (44%), Directors (31%), and Others (25%)

- By Region - North America (45%), Europe (28%), Asia Pacific (20%), Latin America (4%), Middle East & Africa (3%)

Key Players in the AI in Virtual Medical Assistants Market

Prominent players in the AI in virtual medical assistants market include Microsoft (US), Verint Systems (US), Amazon.com, Inc. (US), Infermendica (Poland), Salesforce, Inc. (US), Teckel Medical (Spain), eGain Corporation (US), Teladoc Health, Inc. (US), Fabric Labs (US), Teladoc Health, Inc. (US), Movate (US), Feebris (UK), Healthtap, Inc.(US), ADA health(Germany), Buoy Health(US), Woebot Health(US),, Wysa Ltd.(US), Well Health Technologies Corp (Canada), Healthily (UK), Orbita, Inc. (US), 5 Health holdings Inc (Singapore), Hyro AI Inc (US), Empower Health(US), Veradigm LLC (US), K Health (US).

Market players are focusing on both organic and inorganic growth strategies, such as product launches and improvements, investments, partnerships, collaborations, joint ventures, funding, acquisitions, expansions, agreements, contracts, and alliances, to broaden their offerings, meet unmet customer needs, increase profitability, and expand their presence in the global market.

The study includes an in-depth competitive analysis of these key players in the AI in virtual medical assistants market, with their company profiles, recent developments, and key market strategies.

Research Coverage

- The report studies the AI in virtual medical assistants market based on offerings, mode of interaction, application, end user, and region

- The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting market growth.

- The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

- The report studies micro-markets with respect to their growth trends, prospects, and contributions to the global AI in virtual medical assistants market.

- The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

The report can help established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the following five strategies.

This report provides insights into the following pointers:

- Analysis of key drivers (rising demand for 24/7 healthcare, growing pressure on healthcare system, advancements in AI technologies, increasing use of smartphones and digital platforms, shift towards personalized and preventive care), restraints (data privacy and security concerns, limited clinical validation and trust, Bias in inaccuracy in AI models), opportunities (AI integration with wearables and IOT devices, emerging markets and underserved populations,), and challenges (regulatory complexity and fragmentation, accountability and legal liability) influencing the industry macro dynamics of AI in virtual medical assistants market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the AI in virtual medical assistants market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the AI in virtual medical assistants across varied regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the AI in virtual medical assistants market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the AI in virtual medical assistants market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY RESEARCH

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY RESEARCH

- 2.1.2.1 Primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Breakdown of primaries

- 2.1.2.4 Insights from primary experts

- 2.1.1 SECONDARY RESEARCH

- 2.2 RESEARCH METHODOLOGY DESIGN

- 2.3 MARKET SIZE ESTIMATION

- 2.4 DATA TRIANGULATION

- 2.5 MARKET SHARE ESTIMATION

- 2.6 STUDY ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

- 2.7.1 METHODOLOGY-RELATED LIMITATIONS

- 2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 AI IN VIRTUAL HEALTH ASSISTANTS MARKET OVERVIEW

- 4.2 NORTH AMERICA: AI IN VIRTUAL HEALTH ASSISTANTS MARKET, BY APPLICATION & COUNTRY

- 4.3 AI IN VIRTUAL HEALTH ASSISTANTS MARKET: GEOGRAPHIC SNAPSHOT

- 4.4 AI IN VIRTUAL HEALTH ASSISTANTS MARKET: DEVELOPED VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising demand for 24/7 healthcare access

- 5.2.1.2 Growing pressure on healthcare systems

- 5.2.1.3 Increasing use of smartphones and digital platforms

- 5.2.1.4 Shift toward personalized & preventive care

- 5.2.1.5 Support for mental health & chronic care

- 5.2.2 RESTRAINTS

- 5.2.2.1 Data privacy and security concerns

- 5.2.2.2 Limited clinical validation and trust

- 5.2.2.3 Bias and inaccuracy in AI models

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 AI integration with wearables and IoT devices

- 5.2.3.2 Emerging markets and underserved populations

- 5.2.4 CHALLENGES

- 5.2.4.1 Regulatory complexity and fragmentation

- 5.2.4.2 User engagement and retention

- 5.2.4.3 Accountability and legal liability

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 INDUSTRY TRENDS

- 5.4.1 SHIFT TOWARD MULTIMODAL INTERACTION

- 5.4.2 USE OF GENERATIVE AI FOR HUMAN-LIKE CONVERSATIONS

- 5.4.3 RISE OF AI-POWERED VIRTUAL NURSES & AVATARS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Natural language processing (NLP)

- 5.7.1.2 Speech recognition and voice AI

- 5.7.1.3 Machine learning (ML) and deep learning

- 5.7.1.4 API and cloud integration

- 5.7.1.5 Generative AI and large language models (LLMS)

- 5.7.1.6 Avatars and embodied conversational agents (ECAS)

- 5.7.1.7 Conversational AI

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Electronic health record (EHR) systems

- 5.7.2.2 Wearable and Internet of Things (IOT) devices

- 5.7.2.3 Remote patient monitoring (RPM) tools

- 5.7.2.4 Speech emotion recognition (SER)

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Digital therapeutics (DTX)

- 5.7.3.2 Augmented reality (AR) and virtual reality (VR)

- 5.7.1 KEY TECHNOLOGIES

- 5.8 REGULATORY ANALYSIS

- 5.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8.2 REGULATORY ANALYSIS

- 5.9 PRICING ANALYSIS

- 5.9.1 INDICATIVE PRICE FOR AI IN VIRTUAL HEALTH ASSISTANTS, BY KEY PLAYER (2024)

- 5.9.2 INDICATIVE PRICE FOR AI IN VIRTUAL HEALTH ASSISTANTS, BY REGION (2024)

- 5.9.3 PRICING MODELS (QUALITATIVE)

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 THREAT OF NEW ENTRANTS

- 5.10.2 THREAT OF SUBSTITUTES

- 5.10.3 BARGAINING POWER OF BUYERS

- 5.10.4 BARGAINING POWER OF SUPPLIERS

- 5.10.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.11 PATENT ANALYSIS

- 5.11.1 PATENT PUBLICATION TRENDS FOR AI IN VIRTUAL HEALTH ASSISTANT SOLUTIONS

- 5.11.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 5.12 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 END-USER ANALYSIS

- 5.13.1 UNMET NEEDS

- 5.13.2 END-USER EXPECTATIONS

- 5.14 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14.1 AI IN VIRTUAL HEALTH ASSISTANTS MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2025-2026

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 TRANSFORMING PATIENT ACCESS WITH AI-DRIVEN VIRTUAL ASSISTANTS

- 5.15.1.1 Case 1: Reducing operational costs and improving access with Fabric's Clare at OSF HealthCare

- 5.15.2 ENHANCING PATIENT ACCESS AND EFFICIENCY THROUGH AI-DRIVEN CARE NAVIGATION

- 5.15.2.1 Case 2: Demonstrating threefold return on investment and enhanced care access through Fabric's AI-enabled virtual assistant at Endeavor Health

- 5.15.3 ADVANCING EQUITABLE CARE ACCESS THROUGH AI-POWERED PATIENT NAVIGATION

- 5.15.3.1 Case 3: Reducing access barriers and strengthening community health with Fabric's conversational AI at MLKCH

- 5.15.4 ENHANCING MENTAL HEALTH SUPPORT THROUGH AI-POWERED VIRTUAL ASSISTANTS

- 5.15.4.1 Case 4: Expanding access to mental health support via Wysa's AI-enabled virtual assistant in NHS talking therapies

- 5.15.1 TRANSFORMING PATIENT ACCESS WITH AI-DRIVEN VIRTUAL ASSISTANTS

- 5.16 INVESTMENT & FUNDING SCENARIO

- 5.17 BUSINESS MODEL ANALYSIS

- 5.17.1 LICENSE-BASED BUSINESS MODELS

- 5.17.2 SUBSCRIPTION-BASED BUSINESS MODELS

- 5.17.3 SOFTWARE-AS-A-SERVICE (SAAS) BUSINESS MODELS

- 5.17.4 PAY-PER-USE BUSINESS MODELS

- 5.17.5 FREEMIUM BUSINESS MODELS

- 5.17.6 INTEGRATED SERVICE AND SOFTWARE BUNDLE BUSINESS MODELS

- 5.17.7 OUTCOME-BASED OR VALUE-BASED BUSINESS MODELS

- 5.17.8 SOFTWARE AS A MEDICAL DEVICE (SAMD) BUSINESS MODELS

- 5.18 IMPACT OF AI/GEN AI ON AI IN VIRTUAL HEALTH ASSISTANTS MARKET

- 5.18.1 KEY USE CASES

- 5.18.2 CASE STUDIES

- 5.18.2.1 Case Study 1: Generative AI-powered conversational agent for appointment management at MLK Community Healthcare (MLKCH)

- 5.18.2.2 Case Study 2: Generative AI-driven multilingual VHA for chronic disease management at large Southeast Asian health system

- 5.18.3 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 5.18.3.1 AI in patient engagement & support platforms

- 5.18.3.2 AI in healthcare operations & management tools

- 5.18.3.3 AI in personalized health & wellness coaching

- 5.18.4 USER READINESS & IMPACT ASSESSMENT

- 5.18.4.1 User readiness

- 5.18.4.1.1 User A: Patients

- 5.18.4.1.2 User B: Healthcare providers

- 5.18.4.1.3 User C: Healthcare payers

- 5.18.4.2 Impact assessment

- 5.18.4.2.1 User A: Patients

- 5.18.4.2.1.1 Implementation

- 5.18.4.2.1.2 Impact

- 5.18.4.2.2 User B: Healthcare providers

- 5.18.4.2.2.1 Implementation

- 5.18.4.2.2.2 Impact

- 5.18.4.2.3 User C: Healthcare payers

- 5.18.4.2.3.1 Implementation

- 5.18.4.2.1 User A: Patients

- 5.18.4.1 User readiness

- 5.19 IMPACT OF 2025 US TARIFFS ON AI IN VIRTUAL HEALTH ASSISTANTS MARKET

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.4 IMPACT ON COUNTRY/REGION

- 5.19.4.1 US

- 5.19.4.2 Europe

- 5.19.4.3 Asia Pacific

- 5.19.5 IMPACT ON END-USE INDUSTRIES

6 AI IN VIRTUAL HEALTH ASSISTANTS MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.2 MOBILE APPLICATIONS

- 6.2.1 WIDESPREAD ADOPTION OF MOBILE APPLICATIONS TO SUPPORT MARKET GROWTH

- 6.3 SMART SPEAKERS & IOT/WEARABLE-CONNECTED DEVICES

- 6.3.1 GROWING USE OF WEARABLES FOR HEALTH AND FITNESS TRACKING TO DRIVE MARKET GROWTH

- 6.4 WEB-BASED PLATFORMS

- 6.4.1 ABILITY OF WEB PLATFORMS TO SERVE AS SCALABLE CHANNELS FOR VIRTUAL ASSISTANTS TO BOOST GROWTH

- 6.5 EHR/EMR-INTEGRATED SYSTEMS

- 6.5.1 ABILITY OF EHR/EMR TO EMBED AI VIRTUAL HEALTH ASSISTANTS DIRECTLY INTO EVERYDAY CLINICAL PRACTICE TO FUEL MARKET

7 AI IN VIRTUAL HEALTH ASSISTANTS MARKET, BY MODE OF INTERACTION

- 7.1 INTRODUCTION

- 7.2 TEXT-BASED INTERACTION

- 7.2.1 ACCESSIBLE, SCALABLE, AND USER-FRIENDLY VIRTUAL INTERACTIONS ASSOCIATED WITH TEXT-BASED AI ASSISTANTS TO BOOST GROWTH

- 7.3 VOICE-BASED INTERACTION

- 7.3.1 NEED FOR ACCESSIBLE, INTUITIVE, AND HANDS-FREE HEALTHCARE SOLUTIONS TO DRIVE DEMAND FOR VOICE-BASED INTERACTION

- 7.4 MULTIMODAL INTERACTION

- 7.4.1 INCREASING DIGITAL ADOPTION AMONG PATIENTS AND PROVIDERS TO DRIVE MULTIMODAL VHA DEPLOYMENT

- 7.5 AVATAR/EMOTION-AWARE AI

- 7.5.1 ADVANCING PATIENT ENGAGEMENT THROUGH AVATAR-BASED AND EMOTION-AWARE AI TO BOOST MARKET

8 AI IN VIRTUAL HEALTH ASSISTANTS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 CLINICAL APPLICATIONS

- 8.2.1 SYMPTOM ASSESSMENT & TRIAGE

- 8.2.1.1 Ability to strengthen digital front-door capabilities by streamlining patient flow to drive demand

- 8.2.2 PATIENT INTAKE & HISTORY COLLECTION

- 8.2.2.1 Advantages such as accurate, standardized data capture for effective diagnosis and treatment planning to boost market

- 8.2.3 MEDICATION MANAGEMENT & REMINDERS

- 8.2.3.1 Safe, accurate, and personalized treatment pathways to drive adoption

- 8.2.4 CLINICAL DECISION SUPPORT

- 8.2.4.1 Ability to leverage evidence-based insights to improve diagnostic accuracy and treatment outcomes to fuel growth

- 8.2.5 CLINICAL WORKFLOW ASSISTANCE

- 8.2.5.1 Advantages such as streamlined processes, optimized resources, and timely care delivery to drive demand

- 8.2.6 REHABILITATION & RECOVERY TRACKING

- 8.2.6.1 Improved post-treatment outcomes to propel market

- 8.2.7 REMOTE PATIENT MONITORING

- 8.2.7.1 Continuous tracking of vital signs and chronic conditions beyond hospital settings to support market growth

- 8.2.8 OPERATIVE CARE GUIDANCE

- 8.2.8.1 Real-time support, predictive insights, and standardized workflows to drive adoption

- 8.2.9 HEALTH EDUCATION & AWARENESS

- 8.2.9.1 Personalized insights, evidence-based guidance, and interactive support to strengthen engagement with patients

- 8.2.10 WELLNESS & LIFESTYLE COACHING

- 8.2.10.1 Personalized guidance, behavioral support, and continuous motivation to promote long-term health and well-being

- 8.2.1 SYMPTOM ASSESSMENT & TRIAGE

- 8.3 NON-CLINICAL APPLICATIONS

- 8.3.1 VIRTUAL FRONT DESK/SCHEDULING

- 8.3.1.1 Advantages such as streamlining patient access and reducing administrative inefficiencies to drive growth

- 8.3.2 PATIENT ONBOARDING & NAVIGATING

- 8.3.2.1 AI-powered onboarding and navigation to enhance engagement and retention

- 8.3.3 AI MEDICAL SCRIBING

- 8.3.3.1 Enhanced clinical documentation efficiency through AI-powered medical scribing to boost market

- 8.3.4 AI-DRIVEN BILLING & CLAIMS PROCESSING

- 8.3.4.1 Optimizing revenue cycle efficiency through AI-enabled billing and claims processing to fuel growth

- 8.3.5 WORKFORCE/STAFF ASSISTANCE

- 8.3.5.1 Enhanced workforce efficiency and staff support through AI-driven virtual assistance to support market

- 8.3.1 VIRTUAL FRONT DESK/SCHEDULING

9 AI IN VIRTUAL HEALTH ASSISTANTS MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS & CLINICS

- 9.2.1.1 Growing integration of AI-enabled virtual health assistants to enhance care delivery in hospitals & clinics

- 9.2.2 AMBULATORY CARE CENTERS

- 9.2.2.1 Ability of AI-enabled virtual assistants to drive efficiency and patient flow in ambulatory care services to boost market

- 9.2.3 LONG-TERM CARE & ASSISTED LIVING FACILITIES

- 9.2.3.1 Ability of intelligent virtual assistants to support proactive care and safety in long-term care settings to fuel growth

- 9.2.4 HOME HEALTHCARE

- 9.2.4.1 Ability of AI-based virtual health assistants to streamline monitoring of healthcare in home settings to propel growth

- 9.2.5 OTHER HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS & CLINICS

- 9.3 HEALTHCARE PAYERS

- 9.3.1 COST-EFFECTIVE, PREVENTIVE, AND PERSONALIZED CARE THROUGH AI-POWERED VIRTUAL HEALTH ASSISTANTS TO SUPPORT GROWTH

- 9.4 PATIENTS

- 9.4.1 ADVANTAGES OF AI-POWERED VIRTUAL HEALTH ASSISTANTS SUCH AS ACCESSIBLE AND PERSONALIZED CARE TO DRIVE ADOPTION

- 9.5 OTHER END USERS

10 AI IN VIRTUAL HEALTH ASSISTANTS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 Rising demand for personalized, accessible, and AI-driven healthcare to drive market growth

- 10.2.3 CANADA

- 10.2.3.1 Rising chronic disease burden and digital health transformation to drive market growth

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Leveraging digital health policy and DIGA reforms to accelerate AI virtual assistant adoption

- 10.3.3 FRANCE

- 10.3.3.1 Advancement in French-language NLP and institutional AI support to drive market growth

- 10.3.4 UK

- 10.3.4.1 National interoperability standards to drive system-wide integration

- 10.3.5 ITALY

- 10.3.5.1 Growing number of national AI research hubs focused on healthcare ethics and explainability to boost market

- 10.3.6 SPAIN

- 10.3.6.1 Strong emphasis on emotional AI and psychological wellbeing tools to advance virtual health assistant capabilities

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 Healthcare digitization and AI sovereignty to drive market growth

- 10.4.3 JAPAN

- 10.4.3.1 Technological sophistication and aging demographics to propel virtual health assistants market growth

- 10.4.4 INDIA

- 10.4.4.1 Rising population and healthcare burden to fuel demand for scalable AI virtual health assistant solutions

- 10.4.5 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Advancing AI-driven virtual care to contribute to market growth

- 10.5.3 MEXICO

- 10.5.3.1 Leveraging AI-powered virtual health assistants to address systemic healthcare gaps to drive growth

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 National AI agendas, workforce shortages, and multilingual needs to drive demand for AI-powered virtual health assistants

- 10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 STRATEGIES ADOPTED BY KEY PLAYERS

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN AI IN VIRTUAL HEALTH ASSISTANTS MARKET

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 BRAND/PRODUCT COMPARISON

- 11.6 COMPANY VALUATION & FINANCIAL METRICS

- 11.6.1 FINANCIAL METRICS

- 11.6.2 COMPANY VALUATION

- 11.7 MARKET RANKING ANALYSIS

- 11.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.8.1 STARS

- 11.8.2 EMERGING LEADERS

- 11.8.3 PERVASIVE PLAYERS

- 11.8.4 PARTICIPANTS

- 11.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.8.5.1 Company footprint

- 11.8.5.2 Region footprint

- 11.8.5.3 Offering footprint

- 11.8.5.4 Mode of interaction footprint

- 11.8.5.5 Application footprint

- 11.8.5.6 End-user footprint

- 11.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.9.1 PROGRESSIVE COMPANIES

- 11.9.2 RESPONSIVE COMPANIES

- 11.9.3 DYNAMIC COMPANIES

- 11.9.4 STARTING BLOCKS

- 11.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.9.5.1 Detailed list of key startups/SMEs

- 11.9.5.2 Competitive benchmarking of startups/SMEs

- 11.10 COMPETITIVE SCENARIO

- 11.10.1 PRODUCT LAUNCHES & APPROVALS

- 11.10.2 DEALS

- 11.10.3 EXPANSIONS

- 11.10.4 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 TELADOC HEALTH, INC.

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 MICROSOFT (NUANCE COMMUNICATIONS INC.)

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 AMAZON.COM INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 SALESFORCE, INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches & upgrades

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses & competitive threats

- 12.1.5 INFERMEDICA

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.3.3 Expansions

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses & competitive threats

- 12.1.6 EGAIN CORPORATION

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.4 MnM view

- 12.1.6.4.1 Right to win

- 12.1.6.4.2 Strategic choices

- 12.1.6.4.3 Weaknesses & competitive threats

- 12.1.7 VERINT SYSTEMS INC.

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.3.2 Deals

- 12.1.7.4 MnM view

- 12.1.7.4.1 Right to win

- 12.1.7.4.2 Strategic choices

- 12.1.7.4.3 Weaknesses & competitive threats

- 12.1.8 LIVEPERSON

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.8.3.2 Deals

- 12.1.8.4 MnM view

- 12.1.8.4.1 Right to win

- 12.1.8.4.2 Strategic choices

- 12.1.8.4.3 Weaknesses & competitive threats

- 12.1.9 NICE

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches & upgrades

- 12.1.9.3.2 Deals

- 12.1.9.4 MnM view

- 12.1.9.4.1 Right to win

- 12.1.9.4.2 Strategic choices

- 12.1.9.4.3 Weaknesses & competitive threats

- 12.1.10 TECKEL MEDICAL

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches

- 12.1.10.3.2 Deals

- 12.1.10.3.3 Other developments

- 12.1.10.4 MnM view

- 12.1.10.4.1 Right to win

- 12.1.10.4.2 Strategic choices

- 12.1.10.4.3 Weaknesses & competitive threats

- 12.1.11 MOVATE

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches

- 12.1.11.3.2 Deals

- 12.1.12 FEEBRIS LTD.

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Product launches

- 12.1.12.3.2 Deals

- 12.1.13 HEALTHTAP, INC.

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches

- 12.1.13.3.2 Deals

- 12.1.14 ADA HEALTH

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Product approvals

- 12.1.14.3.2 Deals

- 12.1.15 BUOY HEALTH, INC.

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Product launches

- 12.1.15.3.2 Deals

- 12.1.16 WOEBOT HEALTH

- 12.1.16.1 Business overview

- 12.1.16.2 Products offered

- 12.1.16.3 Recent developments

- 12.1.16.3.1 Deals

- 12.1.16.3.2 Other developments

- 12.1.17 FABRIC LABS, INC. (GYANT)

- 12.1.17.1 Business overview

- 12.1.17.2 Products offered

- 12.1.17.3 Recent developments

- 12.1.17.3.1 Product launches

- 12.1.17.3.2 Deals

- 12.1.17.3.3 Other developments

- 12.1.18 WYSA LTD.

- 12.1.18.1 Business overview

- 12.1.18.2 Products offered

- 12.1.18.3 Recent developments

- 12.1.18.3.1 Product launches

- 12.1.18.3.2 Deals

- 12.1.19 WELL HEALTH TECHNOLOGIES CORP

- 12.1.19.1 Business overview

- 12.1.19.2 Products offered

- 12.1.19.3 Recent developments

- 12.1.19.3.1 Product launches

- 12.1.19.3.2 Deals

- 12.1.20 HEALTHILY LTD

- 12.1.20.1 Business overview

- 12.1.20.2 Products offered

- 12.1.20.3 Recent developments

- 12.1.20.3.1 Product launches & upgrades

- 12.1.20.3.2 Deals

- 12.1.21 ORBITA, INC.

- 12.1.21.1 Business overview

- 12.1.21.2 Products offered

- 12.1.21.3 Recent developments

- 12.1.21.3.1 Product launches

- 12.1.21.3.2 Deals

- 12.1.22 5 HEALTH HOLDINGS INC

- 12.1.22.1 Business overview

- 12.1.22.2 Products offered

- 12.1.22.3 Recent developments

- 12.1.22.3.1 Deals

- 12.1.23 HYRO AI INC.

- 12.1.23.1 Business overview

- 12.1.23.2 Products offered

- 12.1.23.3 Recent developments

- 12.1.23.3.1 Product launches

- 12.1.23.3.2 Deals

- 12.1.24 EMPOWER HEALTH

- 12.1.24.1 Business overview

- 12.1.24.2 Products offered

- 12.1.24.3 Recent developments

- 12.1.24.3.1 Product launches

- 12.1.24.3.2 Deals

- 12.1.25 VERADIGM LLC

- 12.1.25.1 Business overview

- 12.1.25.2 Products offered

- 12.1.25.3 Recent developments

- 12.1.25.3.1 Product launches

- 12.1.25.3.2 Deals

- 12.1.26 K HEALTH

- 12.1.26.1 Business overview

- 12.1.26.2 Products offered

- 12.1.26.3 Recent developments

- 12.1.26.3.1 Deals

- 12.1.1 TELADOC HEALTH, INC.

- 12.2 OTHER PLAYERS

- 12.2.1 SULLY AI

- 12.2.2 MEDVA

- 12.2.3 HEIDI

- 12.2.4 DOCTRONIC INC.

- 12.2.5 EMPARA

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS