|

시장보고서

상품코드

2013045

생성형 AI 서버 시장 : 프로세서 유형별, 기능별, 폼팩터별, 전개별, 냉각 기술별, 최종사용자별 - 세계 예측(-2030년)Generative AI Server Market by Processor Type (GPU, FPGA, ASIC), Function (Training, Inference), Form Factor (Rack-mounted Server, Blade Server, Tower Server), Deployment (On-premises, Cloud), Cooling Technology, End User - Global Forecast to 2030 |

||||||

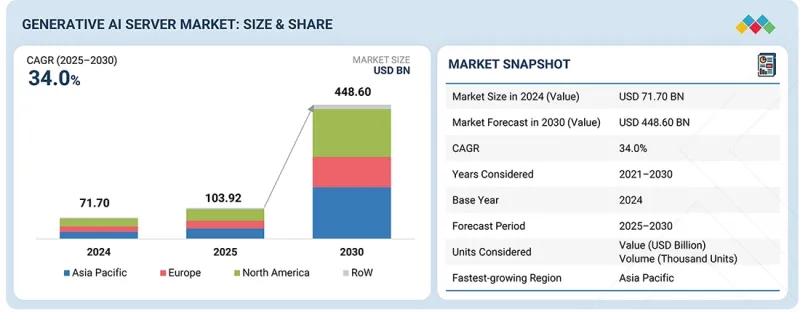

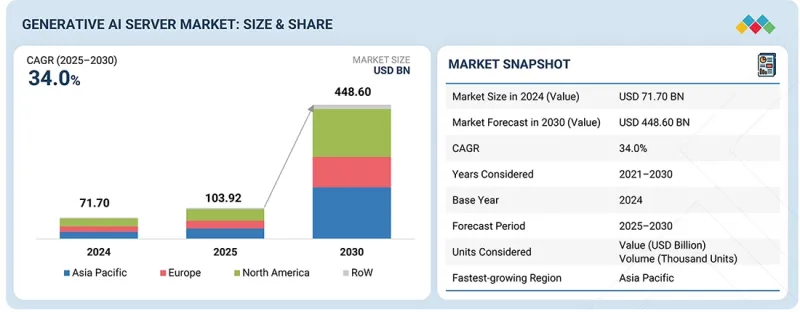

세계의 생성형 AI 서버 시장 규모는 2025년 1,039억 2,000만 달러에서 2030년까지 4,486억 달러로 성장할 것으로 예측되며, 2025-2030년에 CAGR로 34.0%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 프로세서 유형, 기능, 전개, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

기업들은 컨텐츠 제작, 고객 서비스 자동화, 신약 개발, 개인화 마케팅 등을 위해 생성형 AI를 점점 더 많이 도입하고 있습니다. 이러한 광범위한 채택으로 인해 고부하 워크로드를 처리할 수 있는 고성능 AI 서버에 대한 수요가 크게 증가하고 있습니다.

"클라우드 구축이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

클라우드 구축은 탁월한 확장성, 유연성, 비용 효율성으로 인해 2030년까지 생성형 AI 서버 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 대규모 언어 모델, 이미지 생성, 실시간 추론 등의 생성형 AI 워크로드에는 방대한 연산 능력이 필요하지만, 기업이 온프레미스에서 이를 유지하는 것은 현실적이지 않을 수 있습니다. 클라우드 플랫폼을 통해 조직은 주문형 고성능 GPU 및 ASIC 기반 서버에 대한 액세스를 온디맨드 방식으로 제공받을 수 있으며, 초기 투자비용을 절감할 수 있습니다. 또한, Amazon Web Services, Microsoft Azure, Google Cloud 등 주요 클라우드 서비스 제공업체들은 전용 AI 칩, 고속 네트워크, 수랭식 데이터센터 등 첨단 AI 인프라에 지속적으로 투자하고 있습니다. 이를 통해 기업은 복잡한 하드웨어를 관리하지 않고도 최첨단 기능을 활용할 수 있습니다. 또한, 클라우드 배포는 원활한 업데이트, 신속한 모델 배포, AI 개발 툴과의 통합을 지원하여 시장 출시 시간을 단축할 수 있습니다. 데이터 양이 증가하고 각 산업 분야에서 AI 도입이 확대되는 가운데, 탄력적이고 고성능 인프라를 제공하는 클라우드의 능력은 2030년까지 생성형 AI 서버 시장에서 클라우드의 지배적 지위를 확고히 할 것입니다.

"기업 부문이 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 추정됩니다."

기업 부문은 비즈니스 운영 전반에 걸쳐 AI 도입이 빠르게 가속화됨에 따라 생성형 AI 서버 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. 기업들은 고객 지원, 소프트웨어 개발, 마케팅 자동화, 의사결정 등의 기능에 생성형 AI를 통합하려는 움직임을 강화하고 있으며, 이는 고성능 서버 인프라에 대한 강력한 수요를 창출하고 있습니다. 하이퍼스케일러 주도의 초기 도입과 달리, 기업들은 현재 파일럿 프로젝트에서 대규모 언어 모델과 도메인 특화 AI 시스템을 포함한 AI 모델의 본격적인 배포로 전환하고 있습니다. 이러한 전환으로 인해 확장 가능한 연산, 스토리지, 네트워크 기능에 대한 요구가 크게 증가하고 있습니다. 또한, 기업들은 맞춤형 보안 환경을 필요로 하는 경우가 많으며, 이는 전용 또는 하이브리드 AI 서버 구축에 대한 투자를 촉진하고 있습니다. 데이터 프라이버시 및 규제 준수에 대한 관심이 높아진 것도 주요 원인 중 하나이며, 기업들은 기밀 데이터 처리에 있어 통제된 환경을 선호하는 경향이 있습니다. 이에 따라 퍼블릭 클라우드 이용과 더불어 프라이빗 클라우드 및 온프레미스 AI 서버의 도입이 활발히 이루어지고 있습니다. 또한, BFSI, 의료, 제조, 소매 등의 산업은 경쟁 우위를 확보하기 위해 생성형 AI를 활용하고 있으며, 이는 인프라 수요를 증가시키고 있습니다. 디지털 전환이 가속화되고 AI가 기업 전략의 중심이 되는 가운데, 생성형 AI 서버 시장에서 기업 부문이 가장 높은 성장률을 보일 것으로 예상됩니다.

"아시아태평양이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다."

아시아태평양은 디지털화 확대, 정부 지원, 기업 내 AI 도입 증가라는 강력한 조합으로 인해 생성형 AI 서버 시장에서 가장 높은 CAGR을 기록할 것으로 예측됩니다. 중국, 인도, 일본, 한국 등의 국가에서 데이터 생성, 클라우드 도입, AI 기반 애플리케이션이 빠르게 성장하면서 고성능 AI 서버에 대한 수요가 급증하고 있습니다.

세계의 생성형 AI 서버 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

제5장 시장 개요

제6장 생성형 AI 서버 시장 : 프로세서 유형별

제7장 생성형 AI 서버 시장 : 기능별

제8장 냉각 생성형 AI 서버 시장 : 기술별

제9장 생성형 AI 서버 시장 : 폼팩터별

제10장 생성형 AI 서버 시장 : 전개별

제11장 생성형 AI 서버 시장 : 최종사용자별

제12장 생성형 AI 서버 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 부록

KSM 26.04.30The generative AI server market is anticipated to grow from USD 103.92 billion in 2025 to USD 448.60 billion by 2030, at a CAGR of 34.0% between 2025 and 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Processor Type, Function, Deployment and Region |

| Regions covered | North America, Europe, APAC, RoW |

Enterprises are increasingly deploying generative AI for applications such as content creation, customer service automation, drug discovery, and personalized marketing. This widespread adoption is significantly increasing demand for high-performance AI servers capable of handling intensive workloads.

"Cloud deployment will hold the largest market share."

Cloud deployment is expected to hold the largest market share in the generative AI server market by 2030 due to its unmatched scalability, flexibility, and cost efficiency. Generative AI workloads-such as large language models, image generation, and real-time inference-require massive computational power that is often impractical for enterprises to maintain on-premises. Cloud platforms enable organizations to access high-performance GPU- and ASIC-based servers on demand, eliminating heavy upfront capital investments. Additionally, leading cloud service providers like Amazon Web Services, Microsoft Azure, and Google Cloud continuously invest in advanced AI infrastructure, including specialized AI chips, high-speed networking, and liquid-cooled data centers. This ensures enterprises can leverage cutting-edge capabilities without managing complex hardware. Cloud deployment also supports seamless updates, rapid model deployment, and integration with AI development tools, accelerating time-to-market. As data volumes grow and AI adoption expands across industries, the cloud's ability to deliver elastic, high-performance infrastructure will solidify its dominant position in the generative AI server market by 2030.

"Enterprises are estimated to record the highest CAGR during the forecast period."

The enterprises segment is projected to register the highest CAGR in the generative AI server market due to the rapid acceleration of AI adoption across business operations. Enterprises are increasingly integrating generative AI into functions such as customer support, software development, marketing automation, and decision-making, creating strong demand for high-performance server infrastructure. Unlike early adoption led by hyperscalers, enterprises are now moving from pilot projects to full-scale deployment of AI models, including large language models and domain-specific AI systems. This transition significantly increases the need for scalable compute, storage, and networking capabilities. Additionally, enterprises often require customized and secure environments, driving investments in dedicated or hybrid AI server deployments. The growing focus on data privacy and regulatory compliance is another key factor, as enterprises prefer controlled environments for sensitive data processing. This is encouraging the adoption of private cloud and on-premise AI servers alongside public cloud usage. Furthermore, industries such as BFSI, healthcare, manufacturing, and retail are leveraging generative AI for competitive advantage, boosting infrastructure demand. As digital transformation intensifies and AI becomes central to enterprise strategy, the enterprise segment is expected to witness the fastest growth rate in the generative AI server market.

"Asia Pacific is expected to grow at the highest CAGR during the forecast period."

Asia Pacific is expected to register the highest CAGR in the generative AI server market due to a strong combination of digital expansion, government support, and rising enterprise AI adoption. Countries such as China, India, Japan, and South Korea are witnessing rapid growth in data generation, cloud adoption, and AI-driven applications, creating significant demand for high-performance AI servers. Governments across the region are actively promoting AI development through national strategies, funding programs, and digital infrastructure investments. For instance, China's AI development plans and India's digital initiatives are accelerating the deployment of AI workloads across sectors. This policy support is encouraging both domestic innovation and foreign investments in AI infrastructure. Additionally, the expansion of hyperscale data centers and the increasing presence of global cloud providers such as Amazon Web Services, Microsoft Azure, and Google Cloud are boosting regional capacity for generative AI workloads. Moreover, a large developer base, growing startup ecosystem, and increasing enterprise digitalization are driving widespread adoption of generative AI solutions. As businesses scale AI deployments across industries, the demand for advanced server infrastructure in the Asia Pacific is expected to grow at the fastest pace globally.

Extensive primary interviews were conducted with key industry experts in the generative AI server to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is provided below:

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1-50%, Tier 2-20%, and Tier 3-30%

- By Designation: C-level-20%, Directors-30%, and Others-50%

- By Region: North America-40%, Europe-20%, Asia Pacific-30%, and RoW-10%

The report profiles key players in the generative AI server market with their respective market ranking analysis. Prominent players profiled in this report are Dell Inc. (US), Hewlett Packard Enterprise Development LP (US), Lenovo (China), Huawei Technologies Co., Ltd. (China), IBM (US), Super Micro Computer, Inc. (US), INSPUR Co., Ltd. (China), H3C Technologies Co., Ltd. (China), Cisco Systems, Inc. (US), Fujitsu (Japan), among others.

Research Coverage:

This research report categorizes the generative AI server market based on processor type, function, cooling technology, form factor, deployment, end user, and region. The report describes the major drivers, restraints, challenges, and opportunities pertaining to the generative AI server market and forecasts the same till 2030. Apart from these, the report also consists of leadership mapping and analysis of all the companies included in the generative AI server market ecosystem.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the numbers for the overall generative AI server market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Rising Adoption of Generative AI Applications), restraints (High Infrastructure Costs), opportunities (Emerging Demand in Enterprises), and challenges (Data Privacy, Sovereignty & Regulatory Hurdles)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the generative AI server market

- Market Development: Comprehensive information about lucrative markets-the report analyzes the generative AI server market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the generative AI server market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Dell Inc. (US), Hewlett Packard Enterprise Development LP (US), Lenovo (China), Huawei Technologies Co., Ltd. (China), and IBM (US), in the generative AI server market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary interview participants

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GENERATIVE AI SERVER MARKET

- 4.2 AI SERVER MARKET, BY PROCESSOR TYPE

- 4.3 AI SERVER MARKET, BY FUNCTION

- 4.4 AI SERVER MARKET, BY COOLING TECHNOLOGY

- 4.5 AI SERVER MARKET, BY FORM FACTOR

- 4.6 AI SERVER MARKET, BY DEPLOYMENT

- 4.7 AI SERVER MARKET, BY END-USER

- 4.8 AI SERVER MARKET, BY COUNTRY

- 4.9 AI SERVER MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising adoption of generative AI applications

- 5.2.1.2 Demand for high-performance computing (HPC) infrastructure

- 5.2.1.3 Aggressive investments by cloud providers

- 5.2.2 RESTRAINTS

- 5.2.2.1 High infrastructure costs

- 5.2.2.2 Power consumption and sustainability concerns

- 5.2.2.3 Vendor lock-in and limited hardware availability

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Emerging markets

- 5.2.3.2 AI chip innovation and open hardware initiatives

- 5.2.4 CHALLENGES

- 5.2.4.1 Data privacy, sovereignty, and regulatory hurdles

- 5.2.4.2 Talent shortage in AI infrastructure design

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESSES

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICE TREND OF GENERATIVE AI SERVERS, BY REGION (USD)

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 High-performance computing (HPC)

- 5.7.1.2 High bandwidth memory (HBM)

- 5.7.1.3 GenAI workload

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Data center power management and cooling system

- 5.7.2.2 High-speed interconnects

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 AI development frameworks

- 5.7.3.2 Quantum AI

- 5.7.1 KEY TECHNOLOGIES

- 5.8 UPCOMING DEPLOYMENTS OF DATA CENTERS BY CLOUD SERVICE PROVIDERS

- 5.9 CAPEX OF CLOUD SERVICE PROVIDERS

- 5.10 PROCESSOR BENCHMARKING

- 5.10.1 GPU BENCHMARKING

- 5.10.2 CPU BENCHMARKING

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 THREAT OF NEW ENTRANTS

- 5.11.2 THREAT OF SUBSTITUTES

- 5.11.3 BARGAINING POWER OF SUPPLIERS

- 5.11.4 BARGAINING POWER OF BUYERS

- 5.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 AIVRES' HIGH-PERFORMANCE COMPUTING SERVER ACCELERATES AI SOLUTION DEVELOPMENT

- 5.13.2 SEEWEB COLLABORATES WITH LENOVO AND NVIDIA TO LAUNCH GPU-COMPUTING-AS-A-SERVICE MODEL AND EXPAND AI ACCESSIBILITY

- 5.13.3 SHARONAI EXPANDS AI INFRASTRUCTURE WITH LENOVO TRUSCALE, DEPLOYING HUNDREDS OF GPU-DENSE SERVERS

- 5.13.4 SERVING INFERENCE FOR LLMS: A CASE STUDY WITH NVIDIA TRITON INFERENCE SERVER AND ELEUTHER AI

- 5.13.5 APPLIED DIGITAL CORPORATION EXPANDS AI CAPABILITIES WITH SUPERMICRO SERVERS

- 5.14 INVESTMENT AND FUNDING SCENARIO

- 5.15 TRADE ANALYSIS

- 5.15.1 IMPORT SCENARIO (HS CODE 847150)

- 5.15.2 EXPORT SCENARIO (HS CODE 847150)

- 5.16 PATENT ANALYSIS

- 5.17 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.18 REGULATORY LANDSCAPE

- 5.18.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.18.2 STANDARDS

6 GENERATIVE AI SERVER MARKET, BY PROCESSOR TYPE

- 6.1 INTRODUCTION

- 6.2 GPU-BASED SERVERS

- 6.2.1 SCALABILITY AND PARALLEL PROCESSING CAPABILITIES TO DRIVE ADOPTION

- 6.3 FPGA-BASED SERVERS

- 6.3.1 CUSTOMIZATION AND ENERGY EFFICIENCY TO SUPPORT NICHE AI APPLICATIONS

- 6.4 ASIC-BASED SERVERS

- 6.4.1 HIGH-PERFORMANCE AND TASK-SPECIFIC DESIGN TO ACCELERATE GENERATIVE AI DEPLOYMENTS

7 GENERATIVE AI SERVER MARKET, BY FUNCTION

- 7.1 INTRODUCTION

- 7.2 TRAINING

- 7.2.1 HIGH COMPUTATIONAL DEMANDS OF TRAINING GENERATIVE AI MODELS TO DRIVE SERVER DEPLOYMENT

- 7.3 INFERENCE

- 7.3.1 LOW LATENCY AND REAL-TIME PROCESSING NEEDS TO FUEL DEMAND FOR INFERENCE-OPTIMIZED SERVERS

8 GENERATIVE AI SERVER MARKET, BY COOLING TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 AIR COOLING

- 8.2.1 COST-EFFECTIVE AND EASY-TO-DEPLOY SOLUTIONS CONTINUE TO SUPPORT AI INFRASTRUCTURE EXPANSION

- 8.3 LIQUID COOLING

- 8.3.1 HIGH-THERMAL-EFFICIENCY SOLUTIONS TO MEET DEMANDS OF DENSE, PERFORMANCE-INTENSIVE AI INFRASTRUCTURE

- 8.4 HYBRID COOLING

- 8.4.1 COMBINATION OF AIR AND LIQUID COOLING SOLUTIONS TO OPTIMIZE PERFORMANCE AND EFFICIENCY IN AI INFRASTRUCTURE

9 GENERATIVE AI SERVER MARKET, BY FORM FACTOR

- 9.1 INTRODUCTION

- 9.2 RACK-MOUNTED SERVER

- 9.2.1 HIGH-DENSITY COMPUTE CAPABILITIES AND MODULAR DESIGN OF RACK-BASED SERVERS TO SUPPORT GEN AI WORKLOADS

- 9.3 BLADE SERVERS

- 9.3.1 COMPACT DESIGN AND EFFICIENT RESOURCE UTILIZATION MAKE BLADE SERVERS IDEAL FOR AI-INTENSIVE DATA CENTERS

- 9.4 TOWER SERVERS

- 9.4.1 COST-EFFECTIVE AND EASILY DEPLOYABLE TOWER SERVERS CATER TO ENTRY-LEVEL GENERATIVE AI APPLICATIONS

10 GENERATIVE AI SERVER MARKET, BY DEPLOYMENT

- 10.1 INTRODUCTION

- 10.2 ON-PREMISES

- 10.2.1 DATA SECURITY AND CUSTOMIZATION NEEDS FUEL ON-PREMISES ADOPTION IN GENERATIVE AI SERVER DEPLOYMENTS

- 10.3 CLOUD

- 10.3.1 FLEXIBILITY AND SCALABILITY OF CLOUD DEPLOYMENT DRIVE GROWTH IN GENERATIVE AI SERVER MARKET

11 GENERATIVE AI SERVER MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 CLOUD SERVICE PROVIDERS

- 11.2.1 SCALABILITY, COST EFFICIENCY, AND INFRASTRUCTURE FLEXIBILITY TO DRIVE CSP ADOPTION OF GENERATIVE AI SERVERS

- 11.3 ENTERPRISES

- 11.3.1 HEALTHCARE

- 11.3.1.1 Adoption of generative AI for drug discovery fuels market expansion

- 11.3.2 BFSI

- 11.3.2.1 Rising need for enhanced fraud detection in finance drives demand

- 11.3.3 AUTOMOTIVE

- 11.3.3.1 Increasing focus on safety, efficiency, and better driving experiences fuels growth

- 11.3.4 RETAIL & E-COMMERCE

- 11.3.4.1 Personalized shopping experiences and enhanced customer service to generate significant growth opportunities

- 11.3.5 MEDIA & ENTERTAINMENT

- 11.3.5.1 Real-time analysis of viewer preferences, engagement patterns, and demographic information to augment market growth

- 11.3.6 OTHERS

- 11.3.6.1 Proliferation of visual data through smart devices, security cameras, and self-driving cars to drive demand

- 11.3.1 HEALTHCARE

- 11.4 GOVERNMENT ORGANIZATIONS

- 11.4.1 INCREASING USE OF GENERATIVE AI IN NATIONAL SECURITY AND DEFENSE TO DRIVE MARKET GROWTH

12 GENERATIVE AI SERVER MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 Government-led initiatives to boost semiconductor manufacturing to drive market

- 12.2.3 CANADA

- 12.2.3.1 Growing emphasis on commercializing AI to spur demand

- 12.2.4 MEXICO

- 12.2.4.1 Increasing shift toward digital platforms and cloud-based solutions to accelerate demand

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 UK

- 12.3.2.1 Strategic data center investments drive generative AI server demand

- 12.3.3 GERMANY

- 12.3.3.1 Industrial strength and strategic partnerships fuel market

- 12.3.4 FRANCE

- 12.3.4.1 Expanding startup ecosystem and government support to drive growth of market

- 12.3.5 ITALY

- 12.3.5.1 Government strategy and industry digitalization boost market

- 12.3.6 SPAIN

- 12.3.6.1 Strategic cloud investments and language model development - key drivers

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 Strategic investments and AI infrastructure expansion accelerate growth

- 12.4.3 JAPAN

- 12.4.3.1 Strategic investments and sovereign AI initiatives to drive market expansion

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Market driven by semiconductor leadership and government initiatives

- 12.4.5 INDIA

- 12.4.5.1 Government initiatives and infrastructure investments drive market growth

- 12.4.6 REST OF ASIA PACIFIC

- 12.5 ROW

- 12.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 12.5.2 MIDDLE EAST

- 12.5.2.1 Growing emphasis on digital transformation and technological innovation to drive market growth

- 12.5.2.2 GCC countries

- 12.5.2.3 Rest of Middle East

- 12.5.3 AFRICA

- 12.5.3.1 Rising internet penetration and mobile subscriptions to offer lucrative growth opportunities

- 12.5.4 SOUTH AMERICA

- 12.5.4.1 Growing need to store vast amounts of data to boost demand

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS, 2022-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS, 2024

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Processor type footprint

- 13.7.5.4 Function footprint

- 13.7.5.5 Cooling technology footprint

- 13.7.5.6 Form factor footprint

- 13.7.5.7 Deployment footprint

- 13.7.5.8 Application footprint

- 13.7.5.9 End user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO AND TRENDS

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 DELL INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 HEWLETT PACKARD ENTERPRISE DEVELOPMENT LP

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 LENOVO

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 HUAWEI TECHNOLOGIES CO., LTD.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 IBM

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 H3C TECHNOLOGIES CO., LTD.

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Deals

- 14.1.7 CISCO SYSTEMS, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.3.2 Deals

- 14.1.8 SUPER MICRO COMPUTER, INC.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.3.2 Deals

- 14.1.9 FUJITSU

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.10 INSPUR CO., LTD.

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches

- 14.1.10.3.2 Deals

- 14.1.1 DELL INC.

- 14.2 OTHER PLAYERS

- 14.2.1 NVIDIA CORPORATION

- 14.2.2 ADLINK TECHNOLOGY INC.

- 14.2.3 ADVANCED MICRO DEVICES, INC.

- 14.2.4 QUANTA COMPUTERS

- 14.2.5 WISTRON CORPORATION

- 14.2.6 GIGABIT TECHNOLOGIES PVT LTD.

- 14.2.7 ASUSTEK COMPUTER INC.

- 14.2.8 AIVRES

- 14.2.9 AIME

- 14.2.10 WIWYNN CORPORATION

- 14.2.11 MITAC COMPUTING TECHNOLOGY CORPORATION

- 14.2.12 NEC CORPORATION INDIA PRIVATE LIMITED

- 14.2.13 XENON SYSTEMS PTY LTD.

- 14.2.14 GRAPHCORE

- 14.2.15 2CRSI GROUP

15 APPENDIX

- 15.1 INSIGHTS FROM INDUSTRY EXPERTS

- 15.2 DISCUSSION GUIDE

- 15.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.4 CUSTOMIZATION OPTIONS

- 15.5 RELATED REPORTS

- 15.6 AUTHOR DETAILS