|

시장보고서

상품코드

2013046

보행자 보호 시스템 시장 : 기술별, 구성부품별, 차종별, EV 유형별, 지역별 - 세계 예측(-2033년)Pedestrian Protection System Market by Technology (Passive, Active), Component (Camera, Radar, LiDAR, Ultrasonic, ECU, Actuator, Sensor), Vehicle Type (Passenger, Commercial), EV Type (BEV, HEV, PHEV), and Region - Global Forecast to 2033 |

||||||

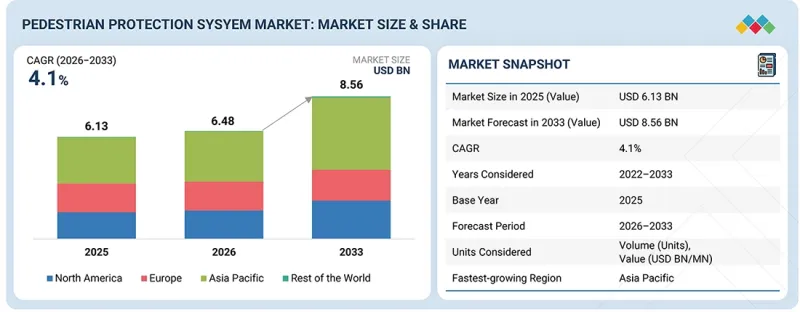

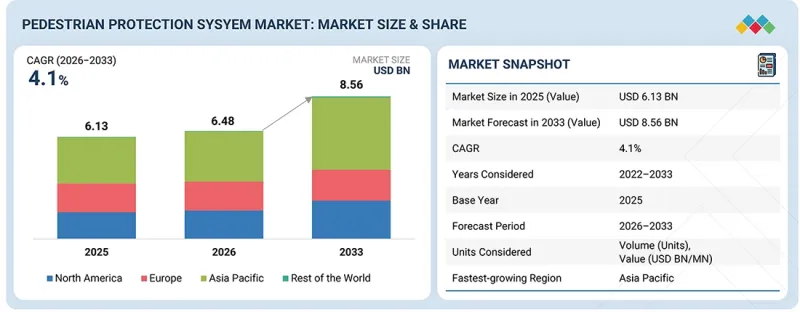

보행자 보호 시스템 시장 규모는 2026년 64억 8,000만 달러에서 2033년까지 85억 6,000만 달러에 달할 것으로 예측되며, CAGR은 4.1%가 됩니다.

자동차 제조업체(OEM)가 보행자 안전을 개선하고 변화하는 규제 기준을 준수하기 위해 첨단 안전 기술을 점점 더 많이 채택함에 따라 이 시장은 꾸준히 성장하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2035년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 대상 단위 | 10억 달러 |

| 부문 | 기술별, 구성부품별, 차종별, EV 유형별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 기타 지역 |

자동 긴급 제동, 보행자 감지 등 ADAS 기능의 채택으로 다양한 차종 부문에서 시스템 도입이 확대되고 있습니다. 77 GHz 레이더 센서, 전방 카메라 모듈, 이미징 레이더, 센서 융합 플랫폼 등의 기술을 통해 감지 정확도와 응답 시간을 향상시켰습니다. 승용차 및 상용차 생산량 증가는 신뢰할 수 있고 확장 가능한 안전 솔루션에 대한 수요를 주도하고 있습니다. 센서, 액추에이터, 제어 유닛의 지속적인 발전은 시스템 성능 향상에 기여하고 있습니다.

초음파 센서는 보행자 보호 시스템 시장에서 가장 큰 점유율을 차지하고 있으며, 일반적으로 전체 센서 수요의 35% 이상을 차지합니다. 이는 주로 단거리 감지에서의 역할에 기인합니다. 이 센서는 음파 펄스를 발사하여 주변 물체를 식별하고 거리를 측정하여 도심 주행이나 주차 등 저속 및 근거리 상황에서 안정적인 성능을 보장합니다. 사각지대나 차량 가장자리 부근에 있는 보행자를 감지하는 능력으로 주차 지원, 장애물 감지, 저속 자동 제동 등의 기능을 지원합니다. 전 세계 신차 승용차의 70% 이상에 주차 보조 기능이 탑재되어 있어 초음파 센서에 대한 수요는 꾸준히 증가하고 있습니다. Bosch, Denso, Valeo와 같은 업계 선도 기업들은 신호 처리의 고도화 및 설계의 소형화를 통해 성능을 향상시키고 있습니다.

승용차는 전 세계적으로 많은 생산량과 광범위한 안전 기술 채택으로 보행자 보호 시스템 시장을 독점하고 있습니다. 보행자 감지, 자동 비상 브레이크, 레이더, 카메라, 초음파 센서를 이용한 센서 기반 시스템의 광범위한 도입이 시장 성장을 견인하고 있습니다. 도시 교통량의 증가와 보행자 노출의 증가로 인해, 높은 정확도의 감지 및 충돌 완화 솔루션에 대한 요구가 증가하고 있습니다. Euro NCAP, UNECE GTR No. 9, Regulation No. 127, China NCAP, Japan NCAP 등의 규제 기준에 따라 Toyota, Volkswagen, Hyundai, Honda, Ford 등의 OEM 업체들은 첨단 보행자 안전 기능을 첨단 보행자 안전기능을 탑재하도록 촉구하고 있습니다. ADAS, 센서 융합, AI를 활용한 물체 인식 기술의 지속적인 발전이 도입을 더욱 촉진하고 있습니다.

유럽에서는 엄격한 규제와 안전 기준의 지속적인 강화로 인해 보행자 보호 시스템 시장이 크게 성장하고 있습니다. Euro NCAP, UNECE R127 및 일반 안전 규정은 보행자 충돌 보호 및 능동 안전 시스템에 대해 더 높은 성능을 요구하고 있습니다. 폭스바겐, BMW, 메르세데스-벤츠, 스텔란티스 등 자동차 제조사들은 폭스바겐 ID.7, BMW의 'Neue Klasse' 플랫폼, 메르세데스-벤츠 E클래스, 푸조 e-3008 등 신형 모델에 자동 긴급제동, 보행자 감지 등 첨단 기능을 탑재하고 있습니다. 보행자 감지 등의 첨단 기능을 탑재하고 있습니다. 또한, 이 지역에서는 AI 기반 물체 감지 기술을 향상시켜 보다 정확한 보행자 인식을 가능하게 하는 등 ADAS 분야에서도 진전을 보이고 있습니다. 지속적인 규제 압력과 급속한 기술 개발로 인해 OEM은 완전히 통합된 안전 아키텍처를 채택해야 합니다.

보행자 보호 시스템 시장의 주요 기업으로는 Robert Bosch GmbH(독일), Aumovio, Denso(일본), ZF Group(독일), Aptiv(아일랜드) 등이 있습니다.

조사 범위:

보행자 보호 시스템 시장을 기술별[화공식(패시브), 메카트로닉스식(액티브)], 구성부품별[액티브(카메라, 레이더, LiDAR, 초음파, ECU, 패시브/액티브 후드리프터, 후드리프트 액추에이터, ACU, 센서(압력 튜브, 가속도), 차량 유형(승용차, 소형 상용차, 대형 상용차), EV 유형(BEV, HEV, EV, 대형 상용차), 차량 유형(승용차, 소형 상용차, 대형 상용차) 센서(압력 튜브, 가속도)], 차량 유형(승용차, 소형 상용차, 대형 상용차), EV 유형(BEV, HEV, PHEV), 그리고 지역(아시아태평양, 유럽, 북미, 기타 지역)을 기준으로 분류하고 있습니다. 이 보고서의 조사 범위에는 시장 성장에 영향을 미치는 주요 요인(촉진요인, 억제요인, 도전 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 또한 주요 업계 플레이어에 대한 종합적인 분석을 통해 각 회사의 사업 개요, 솔루션 및 시장과 관련된 최근 동향에 대한 인사이트를 제공합니다.

본 보고서 구매의 주요 이점:

이 보고서는 보행자 보호 시스템 시장 생태계와 그 하위 부문의 수익 추정치를 제공함으로써 시장 리더와 신규 진입자를 지원합니다. 이해관계자들이 경쟁 상황을 이해하고, 비즈니스를 더 나은 위치에 놓고 효과적인 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한, 이 보고서는 주요 시장 촉진요인 및 과제, 시장 억제요인, 도전 과제 및 기회를 강조함으로써 시장 동향을 파악하는 데 도움이 될 것입니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(보행자 사망사고 증가와 교통안전에 대한 우려, 보행자 감지 기능을 갖춘 ADAS의 급속한 보급), 제약요인(EV의 구조적 강성으로 인한 수동적 보행자 보호 제한, 액티브 후드 및 외부 에어백 시스템의 통합 및 검증의 높은 복잡성), 기회(차량 부문 전반에 걸친 보행자 자동 긴급 제동 확대, AI 기반 보행자 의도 예측 기술), 도전과제 분석(보행자 행동 및 갑작스러운 도로 횡단 이벤트 예측, 보행자 보호 테스트의 규제 불일치별 비용 및 복잡성 증가)

- 제품 개발/혁신 : 보행자 보호 시스템 시장의 미래 기술, 연구 개발 활동 및 제품 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보. 이 보고서는 다양한 지역의 보행자 보호 시스템 시장을 분석합니다.

- 시장 다각화 : 보행자 보호 시스템 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보

- 경쟁사 분석 : Robert Bosch GmbH(독일), Aumovio(독일), Denso(일본), ZF Group(독일), Aptiv(아일랜드) 등 주요 기업의 시장 순위, 성장 전략, 서비스 제공에 대한 상세 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 보행자 보호 시스템 시장(기술별)

제10장 보행자 보호 시스템 시장(구성부품별)

제11장 보행자 보호 시스템 시장(차종별)

제12장 보행자 보호 시스템 시장(EV 유형별)

제13장 보행자 보호 시스템 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.04.30The pedestrian protection system market is projected to reach USD 8.56 billion by 2033, from USD 6.48 billion in 2026, with a CAGR of 4.1%. The market is experiencing steady growth as OEMs increasingly incorporate advanced safety technologies to improve pedestrian safety and comply with evolving regulatory standards.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | USD Billion |

| Segments | Technology, Component, Vehicle Type, EV Type, and Region |

| Regions covered | Asia Pacific, North America, Europe, Rest of the World |

The adoption of ADAS features like automatic emergency braking and pedestrian detection is expanding system deployment across various vehicle segments. Technologies such as 77 GHz radar sensors, forward-facing camera modules, imaging radar, and sensor fusion platforms are enhancing detection accuracy and response times. Growing production of passenger and commercial vehicles is driving the demand for reliable and scalable safety solutions. Ongoing advances in sensors, actuators, and control units are boosting system performance.

"Ultrasonic sensors are the largest segment by component."

Ultrasonic sensors hold the largest share in the pedestrian protection system market, usually making up over 35% of total sensor demand, primarily due to their role in short-range detection. These sensors emit sound wave pulses to identify nearby objects and measure distance, ensuring reliable performance in low-speed and close-proximity situations like urban driving and parking. Their ability to detect pedestrians in blind spots and near the vehicle's edges supports features such as parking assistance, obstacle detection, and low-speed automatic braking. With over 70% of new passenger cars worldwide incorporating parking assist features, the demand for ultrasonic sensors remains strong. Industry leaders like Bosch, Denso, and Valeo are enhancing capabilities through better signal processing and more compact designs.

"Passenger cars lead the market by vehicle type."

Passenger cars dominate the pedestrian protection system market due to high global production and widespread safety technology adoption. Growth is fueled by the broad deployment of pedestrian detection, automatic emergency braking, and sensor-based systems that use radar, cameras, and ultrasonic sensors. Increasing urban traffic and greater pedestrian exposure are driving the need for precise detection and impact mitigation solutions. Regulatory standards like Euro NCAP, UNECE GTR No. 9, Regulation No. 127, China NCAP, and Japan NCAP are encouraging OEMs such as Toyota, Volkswagen, Hyundai, Honda, and Ford to incorporate advanced pedestrian safety features. Ongoing advances in ADAS, sensor fusion, and AI-powered object recognition are further enhancing adoption.

"Stringent safety regulations and NCAP standards propel the market for pedestrian protection systems in Europe."

Europe is experiencing significant growth in the pedestrian protection system market, driven by strict regulations and ongoing enhancements in safety standards. Euro NCAP, UNECE R127, and the General Safety Regulation require higher performance for pedestrian impact protection and active safety systems. Automakers such as Volkswagen, BMW, Mercedes-Benz, and Stellantis are incorporating advanced features like automatic emergency braking and pedestrian detection across new models like the Volkswagen ID.7, BMW Neue Klasse platforms, Mercedes-Benz E-Class, and Peugeot e-3008. The region is also making progress in ADAS by improving AI-based object detection, which allows for more precise pedestrian recognition. Continuous regulatory pressure and rapid technological development are compelling OEMs to adopt fully integrated safety architectures.

Key players in the pedestrian protection system market include Robert Bosch GmbH (Germany), Aumovio, Denso Corporation (Japan), ZF Group (Germany), and Aptiv (Ireland).

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: ADAS and Active Safety System Providers - 50%, Automotive OEMs - 40%, Others - 10%

- By Designation: CXOs - 30%, Directors - 40%, Others - 30%

- By Country: Asia Pacific - 50%, Europe - 20%, North America - 20%, Rest of the World - 10%

Research Coverage:

This research report categorizes the pedestrian protection system market, in terms of technology [pyrotechnic (passive), mechatronic (active)], component [Active (camera, radar, LiDAR, ultrasonic, ECU), passive active hood lifter, hood lift actuator, ACU, sensor (pressure tube, acceleration)], vehicle type (passenger car, light commercial vehicle, heavy commercial vehicle), EV type (BEV, HEV, PHEV), and region (Asia Pacific, Europe, North America, Rest of the World). The scope of the report includes detailed information on major factors such as drivers, restraints, challenges, and opportunities that influence the market's growth. It also features a comprehensive analysis of key industry players to provide insights into their business overview, solutions, and recent developments related to the market.

Key Benefits of Buying the Report:

This report will assist market leaders and new entrants in this market by providing estimates of revenue figures for the pedestrian protection system market ecosystem and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report offers an understanding of the market's pulse by highlighting key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (Rising pedestrian fatalities and road safety concerns, Rapid integration of ADAS with pedestrian detection capability), restraints (EV structural rigidity limits passive pedestrian protection, High complexity in integrating and validating active hood and external airbag systems), opportunities (Expansion of Pedestrian Automatic Emergency Braking across vehicle segments, AI based pedestrian intent prediction technologies) and challenges (Predicting pedestrian behaviour and sudden road crossing events, Lack of Regulatory Harmonization in Pedestrian Protection Testing Increasing Cost and Complexity)

- Product Development/Innovation: Detailed insights into upcoming technologies, R&D activities, and product launches in the pedestrian protection system market

- Market Development: Comprehensive information about lucrative markets; the report analyzes the pedestrian protection system market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the pedestrian protection system market

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like Robert Bosch GmbH (Germany), Aumovio (Germany), Denso Corporation (Japan), ZF Group (Germany), and Aptiv (Ireland)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PEDESTRIAN PROTECTION SYSTEM MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PEDESTRIAN PROTECTION SYSTEM MARKET

- 3.2 PEDESTRIAN PROTECTION SYSTEM MARKET, BY COMPONENT

- 3.3 PEDESTRIAN PROTECTION SYSTEM MARKET, BY VEHICLE TYPE

- 3.4 PEDESTRIAN PROTECTION SYSTEM MARKET, BY EV TYPE

- 3.5 PEDESTRIAN PROTECTION SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising pedestrian fatalities and road safety concerns

- 4.2.1.2 Rapid integration of ADAS with pedestrian detection capabilities

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited adoption of passive pedestrian protection systems due to packaging constraints in EVs

- 4.2.2.2 Complexity in integrating and validating active hood and external airbag systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of pedestrian automatic emergency braking across vehicle segments

- 4.2.3.2 Rise of AI-based pedestrian intent prediction technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Unpredictable pedestrian behavior

- 4.2.4.2 High development cost and engineering complexity due to lack of regulatory harmonization

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL ADAS INDUSTRY

- 5.1.3 TRENDS IN GLOBAL AUTOMOTIVE SAFETY SYSTEM INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 RAW MATERIAL SUPPLIERS

- 5.2.2 SENSOR AND SEMICONDUCTOR SUPPLIERS

- 5.2.3 ADAS TECHNOLOGY PROVIDERS

- 5.2.4 SAFETY SYSTEM MANUFACTURERS

- 5.2.5 AUTOMOTIVE OEMS

- 5.2.6 SOFTWARE AND CONNECTIVITY PROVIDERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2025

- 5.4.2 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2025

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 900211)

- 5.7.2 EXPORT SCENARIO (HS CODE 900211)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 BOSCH DEVELOPS CAMERA- AND RADAR-BASED PEDESTRIAN AUTOMATIC EMERGENCY BRAKING

- 5.9.2 CONTINENTAL IMPLEMENTS SENSOR FUSION PLATFORM FOR PEDESTRIAN DETECTION

- 5.9.3 MOBILEYE DEVELOPS AI-BASED VISION SYSTEM FOR PEDESTRIAN COLLISION AVOIDANCE

- 5.9.4 AUTOLIV CREATES PEDESTRIAN AIRBAG SYSTEM FOR PASSIVE PEDESTRIAN PROTECTION

- 5.9.5 ZF INTRODUCES ADVANCED DRIVER ASSISTANCE PLATFORM WITH PEDESTRIAN DETECTION

- 5.9.6 VALEO IMPLEMENTS ADVANCED SENSING TECHNOLOGIES FOR PEDESTRIAN DETECTION

- 5.10 TECHNICAL IMPLEMENTATION ANALYSIS

- 5.10.1 PEDESTRIAN PROTECTION SYSTEM ARCHITECTURE

- 5.10.2 DETECTION TECHNOLOGY

- 5.10.3 ACTUATION MECHANISM

- 5.10.4 ELECTRONIC CONTROL ARCHITECTURE

- 5.10.5 INTEGRATION WITH ADAS ECOSYSTEM

- 5.10.6 FUNCTIONAL SAFETY FRAMEWORK

- 5.10.7 TESTING AND VALIDATION

- 5.10.8 FAILURE MODE AND RISK ANALYSIS

- 5.11 INSIGHTS ON SUPPLIER STRATEGIES FOR PEDESTRIAN PROTECTION SYSTEMS

- 5.12 INSIGHTS ON OEM STRATEGIES FOR PEDESTRIAN PROTECTION SYSTEMS

- 5.13 EU-INDIA FTA ANALYSIS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 AI-BASED PEDESTRIAN DETECTION

- 6.1.2 VISION-BASED PEDESTRIAN RECOGNITION

- 6.1.3 PEDESTRIAN AUTOMATIC EMERGENCY BRAKING

- 6.1.4 ZONAL AND DOMAIN ECU ARCHITECTURE

- 6.1.5 DIGITAL TWIN AND CRASH SIMULATION

- 6.1.6 V2X COMMUNICATION

- 6.1.7 ACTIVE HOOD LIFT

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DRIVE-BY-WIRE AND BRAKE-BY-WIRE

- 6.2.2 ACTIVE SUSPENSION AND RIDE HEIGHT CONTROL

- 6.2.3 LIGHTWEIGHT FRONT-END MATERIAL

- 6.2.4 EXTERNAL PEDESTRIAN PROTECTION AIRBAG

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027): FOUNDATION AND EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030): EXPANSION AND STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2033+): MASS COMMERCIALIZATION AND DISRUPTION

- 6.4 PATENT ANALYSIS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

9 PEDESTRIAN PROTECTION SYSTEM MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 PYROTECHNIC (PASSIVE)

- 9.3 MECHATRONIC (ACTIVE)

10 PEDESTRIAN PROTECTION SYSTEM MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 ACTIVE

- 10.2.1 CAMERA

- 10.2.1.1 Expansion of vision-led ADAS architectures to drive market

- 10.2.2 RADAR

- 10.2.2.1 Safety standards emphasizing consistent all-weather performance to drive market

- 10.2.3 LIDAR

- 10.2.3.1 Declining sensor costs and increasing integration with sensor fusion systems to drive market

- 10.2.4 ULTRASONIC

- 10.2.4.1 Cost efficiency and suitability for short-range detection to drive market

- 10.2.5 ECU

- 10.2.5.1 Transition toward centralized and software-defined architectures to drive market

- 10.2.1 CAMERA

- 10.3 PASSIVE

- 10.3.1 ACTIVE HOOD LIFTER

- 10.3.2 HOOD LIFT ACTUATOR

- 10.3.3 ACU

- 10.3.4 SENSOR

11 PEDESTRIAN PROTECTION SYSTEM MARKET, BY VEHICLE TYPE

- 11.1 INTRODUCTION

- 11.2 PASSENGER CAR

- 11.2.1 INCREASING INTEGRATION OF ADAS AND SOFTWARE-DRIVEN SAFETY ARCHITECTURES TO DRIVE MARKET

- 11.3 LIGHT COMMERCIAL VEHICLE

- 11.3.1 GROWING RELIANCE ON ELECTRONIC CONTROL UNITS AND TELEMATICS FOR URBAN MOBILITY TO DRIVE MARKET

- 11.4 HEAVY COMMERCIAL VEHICLE

- 11.4.1 RISING REGULATORY FOCUS ON URBAN SAFETY TO DRIVE MARKET

12 PEDESTRIAN PROTECTION SYSTEM MARKET, EV TYPE

- 12.1 INTRODUCTION

- 12.2 BEV

- 12.2.1 RAPID ELECTRIFICATION AND NEED FOR LIGHTWEIGHT, ENERGY-EFFICIENT SAFETY SYSTEMS TO DRIVE MARKET

- 12.3 HEV

- 12.3.1 SURGE IN DEMAND FOR FLEXIBLE SAFETY SOLUTIONS TO DRIVE MARKET

- 12.4 PHEV

- 12.4.1 FOCUS ON OPTIMIZING SYSTEM COORDINATION AND CALIBRATION FOR RELIABLE PEDESTRIAN DETECTION TO DRIVE MARKET

13 PEDESTRIAN PROTECTION SYSTEM MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Strict regulatory enforcement and rapid technology deployment to drive market

- 13.2.2 JAPAN

- 13.2.2.1 Technology-led innovation and OEM-driven development to drive market

- 13.2.3 INDIA

- 13.2.3.1 Increasing localization of safety technologies to drive market

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Robust vehicle safety standards to drive market

- 13.2.5 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Advanced engineering and premium vehicle positioning to drive market

- 13.3.2 FRANCE

- 13.3.2.1 EU regulation alignment and sensor innovation to drive market

- 13.3.3 SPAIN

- 13.3.3.1 Increasing OEM focus on cost-efficient product development to drive market

- 13.3.4 UK

- 13.3.4.1 Software-led ADAS development to drive market

- 13.3.5 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 NORTH AMERICA

- 13.4.1 US

- 13.4.1.1 Continuous OEM-led innovations to drive market

- 13.4.2 MEXICO

- 13.4.2.1 Platform standardization and alignment with North American safety expectations to drive market

- 13.4.3 CANADA

- 13.4.3.1 Focus on environment-specific safety innovation to drive market

- 13.4.1 US

- 13.5 REST OF THE WORLD

- 13.5.1 BRAZIL

- 13.5.1.1 High volume ADAS integration across compact and mid-segment vehicles to drive market

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Prevalence of informal transport systems and unstructured pedestrian movement to drive market

- 13.5.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 14.3 MARKET SHARE ANALYSIS, 2025

- 14.4 REVENUE ANALYSIS, 2021-2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Technology footprint

- 14.7.5.4 Vehicle type footprint

- 14.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.8.5.1 List of start-ups/SMEs

- 14.8.5.2 Competitive benchmarking of start-ups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 DEALS

- 14.9.2 EXPANSIONS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 ROBERT BOSCH GMBH

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 AUMOVIO SE

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 DENSO CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Expansions

- 15.1.3.3.3 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 ZF FRIEDRICHSHAFEN AG

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.3.2 Expansions

- 15.1.4.3.3 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 APTIV

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 VALEO

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Expansions

- 15.1.6.3.3 Other developments

- 15.1.7 MOBILEYE

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.3.2 Other developments

- 15.1.8 HYUNDAI MOBIS

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.3.2 Expansions

- 15.1.8.3.3 Other developments

- 15.1.9 MAGNA INTERNATIONAL INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Other developments

- 15.1.10 HITACHI ASTEMO

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.11 AUTOLIV

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Expansions

- 15.1.11.3.3 Other developments

- 15.1.12 JOYSON SAFTEY SYSTEMS

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.12.3.2 Other developments

- 15.1.1 ROBERT BOSCH GMBH

- 15.2 OTHER PLAYERS

- 15.2.1 NXP SEMICONDUCTORS

- 15.2.2 TEXAS INSTRUMENTS

- 15.2.3 ONSEMI

- 15.2.4 INFINEON TECHNOLOGIES AG

- 15.2.5 HELLA GMBH & CO. KGAA

- 15.2.6 ITERIS, INC.

- 15.2.7 ARBE ROBOTICS LTD.

- 15.2.8 INNOVIZ TECHNOLOGIES LTD.

- 15.2.9 LUMINAR TECHNOLOGIES, INC.

- 15.2.10 TRIEYE

- 15.2.11 CEPTON

- 15.2.12 STRADVISION

- 15.2.13 AMBARELLA, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Breakdown of primary interviews

- 16.1.2.2 Primary participants

- 16.1.2.3 Insights from industry experts

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 FACTOR ANALYSIS

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 INSIGHTS FROM INDUSTRY EXPERTS

- 17.2 DISCUSSION GUIDE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.4.1 PEDESTRIAN PROTECTION SYSTEM MARKET, BY LEVEL OF AUTONOMY, AT REGIONAL LEVEL

- 17.4.2 COMPANY INFORMATION

- 17.4.2.1 Profiling of five additional market players

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS