|

시장보고서

상품코드

2013047

부유식 해상 풍력발전 시장 : 터빈 출력(5MW 미만, 5-10MW, 11-15MW, 15MW 이상), 부유식 플랫폼(반잠수식, 스퍼부이식, 텐션 레그식, 바지선식 및 하이브리드식), 구성요소, 수심, 지역별 - 세계 예측(-2031년)Floating Offshore Wind Market by Turbine Rating (Up to 5 MW, 5-10 MW, 11-15 MW, Above 15 MW), Floating Platform (Semi-submersible, Spar-buoy, Tension-leg, Barge & Hybrid), Component, Depth, & Region - Global Forecast to 2031 |

||||||

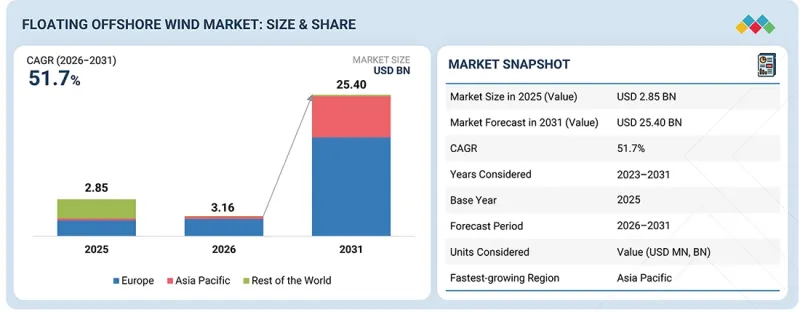

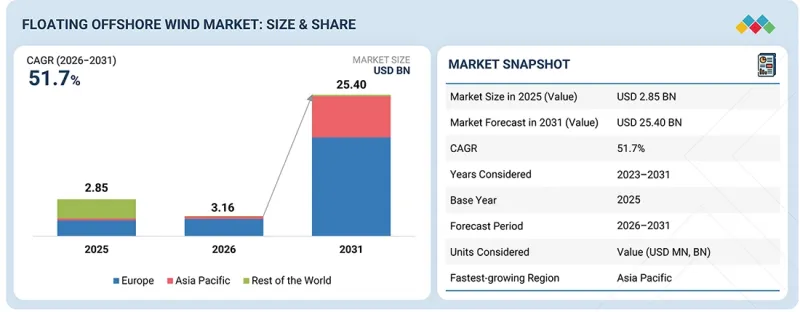

세계의 부유식 해상 풍력 시장 규모는 2026년 31억 6,000만 달러에서 2031년까지 254억 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR은 51.7%를 기록할 전망입니다.

이러한 급격한 성장은 청정에너지 시스템으로의 전환이 가속화되고 각국의 탈탄소화 전략에서 해상 풍력의 역할이 확대되고 있음을 반영합니다. 부유식 풍력발전 기술을 통해 에너지 개발 사업자들은 고정식 터빈으로는 접근할 수 없었던 더 깊고, 더 강력하고 안정적인 풍력 자원을 보유한 해역을 활용할 수 있게 됩니다. 이는 얕은 수역이 제한된 국가들에게 이 기술은 매우 중요한 솔루션이 될 수 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 터빈 출력, 부유식 플랫폼, 구성요소, 수심, 지역 |

| 대상 지역 | 유럽, 아시아태평양, 세계 기타 지역 |

유럽, 아시아태평양, 북미 각국 정부는 정책 인센티브, 입찰 제도, 장기 해상 풍력발전 목표를 잇달아 발표하며 대규모 투자 및 상업 프로젝트 파이프라인 확장을 주도하고 있습니다. 공급망이 성숙하고 플랫폼 설계가 표준화됨에 따라 부유식 해상 풍력발전의 비용 경쟁력이 지속적으로 향상되어 성장 궤도를 더욱 견고하게 하고 있습니다.

정책적 지원과 더불어 기술 발전과 업계 내 강력한 협력이 시장 준비 태세와 상업적 실현 가능성을 가속화하고 있습니다. 부유식 플랫폼, 계류 시스템, 해저 송전 인프라의 혁신은 프로젝트의 복잡성을 크게 줄이고, 개발업체가 파일럿 설치를 넘어 사업 규모를 확장할 수 있게 해줍니다. 동시에 대형 전력회사, 재생에너지 개발업체, 사업 전환을 추진하는 석유 및 가스 회사들이 해양 건설 전문성, 해양 엔지니어링 역량, 세계 물류 네트워크를 활용하기 위해 전략적 파트너십을 맺고 있습니다. 이러한 협력을 통해 새로운 도입 지역이 개척되고 있으며, 영국, 일본, 프랑스, 미국 등 주요 시장에서 수 기가 와트 규모의 프로젝트가 속속 발표되고 있습니다. 투자자들의 신뢰가 높아지고, LCOE가 낮아지고, 환경에 대한 관심이 높아지면서 부유식 해상 풍력은 주류 발전 기술로 발전해 2031년까지 세계 재생에너지의 판도를 뒤바꿀 것으로 예상됩니다.

예측 기간 동안 11-15MW 부문이 가장 높은 성장률을 보일 것으로 예상됩니다.

11-15MW급 터빈 부문은 기술적 성숙도와 경제성 간의 최적의 균형으로 인해 예측 기간 동안 가장 높은 성장을 기록할 것으로 예상됩니다. 이 범위의 터빈은 이미 상업적으로 확립되어 있으며, 프로젝트 파이프라인에서 널리 채택되고 있습니다. 단위당 에너지 출력이 월등히 높은 반면, 프로젝트 당 필요한 설치 대수를 줄일 수 있어 설치, 유지보수, 계통연계 비용을 절감할 수 있습니다. 아직 도입 초기 단계인 15MW 이상의 터빈과 달리, 11-15MW급은 검증된 설계, 확립된 공급망, 높은 자금조달 가능성 등의 장점을 가지고 있어 프로젝트를 빠르게 확장하고자 하는 개발사업자에게 최적의 선택이 될 수 있습니다. 또한, 이 터빈은 무게, 안정성, 통합의 제약으로 인해 크기와 운영 신뢰성의 균형이 요구되는 부유식 플랫폼에 매우 적합하며, 단기적인 발전 용량 증가에 있어 그 우위를 더욱 강화합니다.

부유식 플랫폼 부문은 2025년에 가장 큰 시장 점유율을 차지했습니다.

부유식 플랫폼 부문은 해저 고정식 기초가 실용적이지 않은 심해역에 해상 풍력발전을 배치할 수 있는 주요 기술이기 때문에 부유식 해상 풍력 시장에서 가장 큰 점유율을 차지하고 있습니다. 보다 강력하고 안정적인 풍력 자원을 이용하기 위해 전 세계 해상 풍력 개발 사업이 해상으로 진출함에 따라 반잠수식, 스파 부표, 텐션 레그 플랫폼과 같은 고급 부유식 하부 구조물에 대한 수요는 지속적으로 증가하고 있습니다. 이러한 플랫폼은 복잡한 설계, 재료, 계류 시스템 및 통합 요구 사항으로 인해 프로젝트 총 비용의 상당 부분을 차지합니다. 또한, 유럽과 아시아태평양 등에서 대규모 부유식 풍력발전 프로젝트의 상용화가 진행됨에 따라 플랫폼 설계, 표준화, 제조 능력에 대한 막대한 투자가 촉진되고 있습니다. 그 결과, 부유식 플랫폼은 밸류체인 내에서 가장 고부가가치 구성요소로 남아 있으며, 2025년에는 시장을 주도할 것으로 예상됩니다.

세계의 부유식 해상 풍력발전 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 부유식 해상 풍력발전 시장 : 터빈 출력별

제10장 부유식 해상 풍력발전 시장 : 부유식 플랫폼별

제11장 부유식 해상 풍력발전 시장 : 구성요소별

제12장 부유식 해상 풍력발전 시장 : 수심별

제13장 부유식 해상 풍력발전 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.04.30The global floating offshore market is projected to reach USD 25.40 billion by 2031 from USD 3.16 billion in 2026, at a CAGR of 51.7% during the forecast period. This sharp growth reflects the accelerating transition toward cleaner energy systems and the expanding role of offshore wind in national decarbonization strategies. Floating wind technology enables energy developers to tap into deeper waters with stronger and more consistent wind resources-areas previously inaccessible to fixed-bottom turbines-making it a critical solution for countries with limited shallow-water regions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million) |

| Segments | By Turbine Rating, By Floating Platform, By Component, Depth, & Region |

| Regions covered | Europe, Asia Pacific, Rest of the World |

Governments across Europe, Asia Pacific, and North America are increasingly unveiling policy incentives, auction mechanisms, and long-term offshore wind targets, which are collectively driving large-scale investment and the expansion of the commercial project pipeline. As supply chains mature and platform designs become more standardized, the cost competitiveness of floating offshore wind continues to improve, further reinforcing its growth trajectory.

Beyond policy support, technological advancements and strong industry collaboration are accelerating market readiness and commercial viability. Innovations in floating platforms, mooring systems, and subsea transmission infrastructure have significantly reduced project complexities, enabling developers to scale beyond pilot installations. Simultaneously, major utilities, renewable energy developers, and transitioning oil & gas companies are forming strategic partnerships to leverage offshore construction expertise, marine engineering capabilities, and global logistics networks. These collaborations are unlocking new deployment zones and catalyzing multi gigawatt project announcements across key markets such as the UK, Japan, France, and the US. With growing investor confidence, declining LCOE, and increasing environmental commitments, floating offshore wind is expected to evolve into a mainstream power generation technology, reshaping the global renewable energy landscape through 2031.

11-15 MW segment is expected to register the highest growth during the forecast period

The 11-15 MW turbine segment is expected to register the highest growth during the forecast period due to its optimal balance between technological maturity and economic efficiency. Turbines in this range are already commercially viable and widely adopted in project pipelines, offering significantly higher energy output per unit while reducing the number of installations required per project, thereby lowering installation, maintenance, and grid connection costs. Unlike >15 MW turbines, which are still in the early deployment phase, the 11-15 MW class benefits from proven designs, established supply chains, and greater bankability, making it the preferred choice for developers aiming to scale projects quickly. Additionally, these turbines are well-suited for floating platforms, where weight, stability, and integration constraints require a balance between size and operational reliability, further reinforcing their dominance in near-term capacity additions.

Floating platforms segment held the largest market share in 2025

The floating platforms segment holds the largest share of the floating offshore wind market because it is the key technology enabling offshore wind deployment in deep-water areas where seabed-fixed foundations are not practical. As global offshore wind development ventures move farther offshore to access stronger and more consistent wind resources, the demand for advanced floating substructures, such as semi-submersible, spar-buoy, and tension-leg platforms, continues to grow. These platforms account for a significant share of total project costs due to their complex engineering, materials, mooring systems, and integration requirements. Additionally, the increasing commercialization of large-scale floating wind projects in regions like Europe and the Asia Pacific is fueling substantial investment in platform design, standardization, and manufacturing capacity. Consequently, floating platforms remain the highest-value component within the supply chain and are expected to lead the market in 2025.

Breakdown of Primaries:

In-depth interviews with key industry participants, subject-matter experts, C-level executives at key market players, and industry consultants, among other experts, were conducted to obtain and verify critical qualitative and quantitative information and to assess future market prospects. The primary interviews were distributed as follows:

By Company Type: Tier 1 - 30%, Tier 2 - 55%, and Tier 3 - 15%

By Designation: C-Level - 30%, D-Level - 20%, and Others - 50%

By Region: Europe - 30%, Asia Pacific - 60%, and RoW - 10%

The floating offshore wind market is characterized by the strong presence of established global industry leaders driving innovation and large-scale project deployment. Notable players in the floating offshore wind market include GE Vernova (US), Siemens Gamesa Renewable Energy (Spain), Vestas Wind Systems A/S (Denmark), Mingyang Smart Energy Group Co., Ltd. (China), Goldwind (China), BW Ideol (France), Principle Power (US), SBM Offshore (Netherlands), Saipem SpA (Italy), Aker Solutions (Norway), X1 Wind (Spain), Hexicon AB (Sweden), Shanghai Electric (China), HD Hyundai Heavy Industries (South Korea), Japan Marine United Corporation (Japan), Saitec Offshore (Spain), Doosan Enerbility (South Korea), Stiesdal (Denmark), Dongfang Electric (China), Envision Group (China), CS Wind Corporation (South Korea), Seatrium (Singapore), Technip Energies (France), NOV (US), Gazelle Wind Power (Portugal), and GICON-GROBMANN INGENIEUR CONSULT GMBH (Germany)

Research Coverage:

The report provides a comprehensive definition, description, and forecast of the floating offshore wind market based on various parameters, including turbine rating (up to 5 MW, 5-10 MW, 11-15 MW, above 15 MW), floating platform (semi-submersible, spar-buoy, tension-leg platform, barge & hybrid concepts), component (turbines, floating platforms, moorings & anchors, electrical systems), depth (up to 30 M, 30-60 M, above 60 M), and region (Asia Pacific, North America, Europe, Rest of the World). The report also offers a thorough qualitative and quantitative analysis of the floating offshore wind market, encompassing a comprehensive examination of the key market drivers, limitations, opportunities, and challenges. Additionally, it covers critical facets of the market, such as an assessment of the competitive landscape, an analysis of market dynamics, value-based market estimates, and future trends in the floating offshore wind market. The report provides investment and funding information of key players in the floating offshore wind market.

Key Benefits of Buying the Report

The report is thoughtfully designed to benefit both established industry leaders and newcomers in the floating offshore wind market. It provides reliable revenue forecasts for the entire market and its subsegments. This data is a valuable resource for stakeholders, enabling them to gain a comprehensive understanding of the competitive landscape and formulate effective market strategies for their businesses. Furthermore, the report serves as a channel for stakeholders to grasp the current state of the market, providing essential insights into market drivers, limitations, challenges, and growth opportunities. By incorporating these insights, stakeholders can make well-informed decisions and stay informed about the constantly evolving dynamics of the floating offshore wind market.

- Analysis of key drivers (access to deep-water, high-quality wind resources, national energy security and decarbonization targets, rapid technological maturation of floating platforms), restraints (high capital expenditure compared to fixed-bottom offshore wind, high costs resulting from technical complexities), opportunities (large untapped markets in the Asia Pacific, first-mover advantage for developers and suppliers), and challenges (port readiness and logistical execution at scale, grid integration and offshore transmission coordination) influencing the growth of the floating offshore wind market.

- Product Development/Innovation: The floating offshore wind market is in a constant state of evolution, with a primary focus on product launches, expansions, contracts, agreements, and partnerships. Leading industry players like GE Vernova (US), Siemens Gamesa Renewable Energy (Spain), Vestas Wind Systems A/S (Denmark), Mingyang Smart Energy Group Co., Ltd. (China), Goldwind (China), BW Ideol (France), Principle Power (US), SBM Offshore (Netherlands), and Saipem SpA (Italy) are actively investing in advanced floating platform designs and larger turbine integration. This continuous innovation is accelerating cost reduction, improving structural stability in deep waters, and enabling large-scale commercial deployment of floating wind projects globally.

- Market Development: The floating offshore wind market is witnessing steady development driven by increasing government support, pilot-to-commercial-scale transitions, and growing project pipelines across key regions such as Europe and the Asia Pacific. Advancements in floating platform technologies, coupled with favorable regulatory frameworks and auction mechanisms, are accelerating deployment timelines. Additionally, rising investments from both energy majors and new entrants are strengthening project execution capabilities and enhancing overall market maturity.

- Market Diversification: The market is gradually diversifying across multiple dimensions, including platform technologies (semi-submersible, spar, and tension-leg platform) and water depths. Geographic expansion into markets such as Japan and the US is reducing dependency on early adopters like Europe. Furthermore, integration with hybrid energy systems, including offshore hydrogen production and energy storage, is broadening the scope of applications and creating new revenue streams for stakeholders.

- Competitive Assessment: A detailed review has been done to understand the market position, growth strategies, and services offered by key players in the floating offshore wind market. These prominent companies include GE Vernova (US), Siemens Gamesa Renewable Energy (Spain), Vestas Wind Systems A/S (Denmark), Mingyang Smart Energy Group Co., Ltd. (China), Goldwind (China), BW Ideol (France), Principle Power (US), SBM Offshore (Netherlands), Saipem SpA (Italy), Aker Solutions (Norway), X1 Wind (Spain), Hexicon AB (Sweden), Shanghai Electric (China), HD Hyundai Heavy Industries (South Korea), Japan Marine United Corporation (Japan), Saitec Offshore (Spain), Doosan Enerbility (South Korea), Stiesdal (Denmark), Dongfang Electric (China), Envision Group (China), CS Wind Corporation (South Korea), Seatrium (Singapore), Technip Energies (France), NOV (US), Gazelle Wind Power (Portugal), and GICON-GROBMANN INGENIEUR CONSULT GMBH (Germany). This analysis provides in-depth insights into the competitive positions of these major players, their approaches to driving market growth, and the range of products and services they offer within the floating offshore wind market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN FLOATING OFFSHORE WIND MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLOATING OFFSHORE WIND MARKET

- 3.2 FLOATING OFFSHORE WIND MARKET, BY REGION

- 3.3 ASIA PACIFIC: FLOATING OFFSHORE WIND MARKET, BY COMPONENT AND TURBINE RATING

- 3.4 FLOATING OFFSHORE WIND MARKET, BY TURBINE RATING

- 3.5 FLOATING OFFSHORE WIND MARKET, BY FLOATING PLATFORM

- 3.6 FLOATING OFFSHORE WIND MARKET, BY COMPONENT

- 3.7 FLOATING OFFSHORE WIND MARKET, BY DEPTH

- 3.8 FLOATING OFFSHORE WIND MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Access to deep-water, high-quality wind resources

- 4.2.1.2 National energy security and decarbonization targets

- 4.2.1.3 Rapid technological maturation of floating platforms

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital expenditure compared to fixed-bottom offshore wind

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Large untapped markets in Asia Pacific

- 4.2.3.2 First-mover advantage for developers and suppliers

- 4.2.4 CHALLENGES

- 4.2.4.1 Port readiness and logistical execution at scale

- 4.2.4.2 Grid integration and offshore transmission coordination

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN OVERALL FLOATING OFFSHORE WIND MARKET

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 850231)

- 5.6.2 EXPORT SCENARIO (HS CODE 850231)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 EQUINOR'S HYWIND SCOTLAND DEMONSTRATES COMMERCIAL VIABILITY OF FLOATING OFFSHORE WIND

- 5.9.2 WINDFLOAT ATLANTIC ENABLES SEMI-SUBMERSIBLE FLOATING WIND DEPLOYMENT

- 5.9.3 HYWIND TAMPEN POWERS OFFSHORE OIL & GAS PLATFORMS WITH FLOATING WIND

- 5.10 IMPACT OF 2025 US TARIFF - FLOATING OFFSHORE WIND MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 FLOATING SUBSTRUCTURE PLATFORM DESIGNS

- 6.1.2 DYNAMIC MOORING AND ANCHORING SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DYNAMIC SUBSEA CABLE SYSTEMS

- 6.2.2 FLOATING SUBSTATIONS AND HVDC TRANSMISSION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 GREEN HYDROGEN INTEGRATION

- 6.3.2 OFFSHORE ENERGY STORAGE AND HYBRID RENEWABLE SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | COST OPTIMIZATION & PRE-COMMERCIAL SCALING

- 6.4.2 MID-TERM (2027-2030) | GRID MODERNIZATION & SYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS, GRID-INTERACTIVE PROTECTION

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON FLOATING OFFSHORE WIND MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY OEMS IN FLOATING OFFSHORE WIND MARKET

- 6.7.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN FLOATING OFFSHORE WIND MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GEN AI/AI-INTEGRATED FLOATING OFFSHORE WIND TURBINES

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF FLOATING OFFSHORE WIND

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 MARKET PROFITABILITY

9 FLOATING OFFSHORE WIND MARKET, BY TURBINE RATING

- 9.1 INTRODUCTION

- 9.2 UP TO 5 MW

- 9.2.1 USED IN PILOT PROJECTS AND DEMONSTRATION FARMS TO TEST FLOATING WIND TECHNOLOGIES

- 9.3 5-10 MW

- 9.3.1 WELL-SUITED FOR COMMERCIAL FLOATING WIND FARMS

- 9.4 11-15 MW

- 9.4.1 USAGE IN MID- TO LARGE-SCALE FLOATING WIND PROJECTS TO DRIVE ADOPTION

- 9.5 ABOVE 15 MW

- 9.5.1 PLATFORM INNOVATION AND SUPPLY CHAIN MATURITY TO DRIVE MARKET

10 FLOATING OFFSHORE WIND MARKET, BY FLOATING PLATFORM

- 10.1 INTRODUCTION

- 10.2 SEMI-SUBMERSIBLE

- 10.2.1 PROVIDE SUPPORT FOR TURBINES IN DEEP-WATER OFFSHORE WIND PROJECTS

- 10.3 SPAR-BUOY

- 10.3.1 PROVIDES UNMATCHED STABILITY IN ULTRA-DEEP OFFSHORE WATERS

- 10.4 TENSION-LEG

- 10.4.1 TENSION-LEG PLATFORMS PROVIDE EXCEPTIONAL VERTICAL STABILITY FOR DEEP-WATER TURBINES

- 10.5 BARGE & HYBRID

- 10.5.1 ADVANCES IN MATERIALS AND HYDRODYNAMIC DESIGN IMPROVE STABILITY, EFFICIENCY, AND COST-EFFECTIVENESS

11 FLOATING OFFSHORE WIND MARKET, BY COMPONENT

- 11.1 INTRODUCTION

- 11.2 TURBINES

- 11.2.1 UP TO 5 MW TURBINES USED IN PILOT PROJECTS AND DEMONSTRATION FARMS TO TEST FLOATING WIND TECHNOLOGIES

- 11.3 FLOATING PLATFORMS

- 11.3.1 BACKBONE OF DEEP-WATER WIND ENERGY DEPLOYMENT

- 11.4 MOORINGS & ANCHORS

- 11.4.1 KEEP FLOATING PLATFORMS STABLE IN DEEP WATERS

- 11.5 ELECTRICAL SYSTEMS

- 11.5.1 ENABLE RELIABLE POWER TRANSMISSION FROM TURBINES TO SHORE

12 FLOATING OFFSHORE WIND MARKET, BY DEPTH

- 12.1 INTRODUCTION

- 12.2 UP TO 30 M

- 12.2.1 LOWER COST AND WELL-ESTABLISHED SUPPLY CHAIN TO DRIVE MARKET

- 12.3 30-60 M

- 12.3.1 MODERATE WATER DEPTHS ENABLE EARLY COMMERCIAL ADOPTION OF FLOATING WIND PROJECTS

- 12.4 ABOVE 60 M

- 12.4.1 HIGH ENERGY POTENTIAL AND LIMITED COMPETITION FOR NEARSHORE SITES TO PROPEL MARKET

13 FLOATING OFFSHORE WIND MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 BY TURBINE RATING

- 13.2.2 BY FLOATING PLATFORM

- 13.2.3 BY COMPONENT

- 13.2.4 BY DEPTH

- 13.2.5 BY COUNTRY

- 13.2.5.1 China

- 13.2.5.1.1 Deep-water expansion and large-scale targets to drive market

- 13.2.5.2 South Korea

- 13.2.5.2.1 Technological advancements to propel market

- 13.2.5.3 Taiwan

- 13.2.5.3.1 Shallow-water saturation and deep-water transition to drive market

- 13.2.5.4 Philippines

- 13.2.5.4.1 Deep-water resource potential and emerging project pipeline to drive market

- 13.2.5.5 Rest of Asia Pacific

- 13.2.5.1 China

- 13.3 EUROPE

- 13.3.1 BY TURBINE RATING

- 13.3.2 BY FLOATING PLATFORM

- 13.3.3 BY COMPONENT

- 13.3.4 BY DEPTH

- 13.3.5 BY COUNTRY

- 13.3.5.1 Norway

- 13.3.5.1.1 Strong offshore engineering expertise and maritime capabilities to support market growth

- 13.3.5.2 UK

- 13.3.5.2.1 Favorable government policies to propel market

- 13.3.5.3 France

- 13.3.5.3.1 Well-established offshore engineering and shipbuilding sector to support market growth

- 13.3.5.4 Sweden

- 13.3.5.4.1 Strong maritime engineering sector and offshore energy expertise to propel market

- 13.3.5.5 Italy

- 13.3.5.5.1 Government policies aligned with EU renewable energy targets to drive market

- 13.3.5.6 Rest of Europe

- 13.3.5.1 Norway

- 13.4 REST OF THE WORLD

- 13.4.1 BY TURBINE RATING

- 13.4.2 BY FLOATING PLATFORM

- 13.4.3 BY COMPONENT

- 13.4.4 BY DEPTH

- 13.4.5 BY REGION

- 13.4.5.1 North America

- 13.4.5.1.1 Government-backed leasing programs to drive market

- 13.4.5.2 South America

- 13.4.5.2.1 Excellent offshore wind resources and established offshore oil & gas expertise to propel market

- 13.4.5.3 Middle East & Africa

- 13.4.5.3.1 Underdeveloped market with strategic potential in energy diversification-key factor driving market growth

- 13.4.5.1 North America

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2026

- 14.3 MARKET RANKING

- 14.4 REVENUE ANALYSIS, 2021-2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Turbine rating footprint

- 14.5.5.3 Component footprint

- 14.5.5.4 Region footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.6.5.1 Detailed list of startups/SMEs

- 14.6.5.2 Competitive benchmarking of key startups/SMEs

- 14.7 COMPANY VALUATION AND FINANCIAL METRICS

- 14.8 BRAND/PRODUCT COMPARISON

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 GE VERNOVA

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 SIEMENS GAMESA RENEWABLE ENERGY

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 VESTAS WIND SYSTEMS A/S

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 MINGYANG SMART ENERGY GROUP CO., LTD

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.3.4 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 GOLDWIND

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 SBM OFFSHORE

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Expansions

- 15.1.6.3.4 Other developments

- 15.1.7 SAIPEM SPA

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.3.3 Other developments

- 15.1.8 AKER SOLUTIONS

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.3.3 Other developments

- 15.1.9 HEXICON AB

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Other developments

- 15.1.10 SHANGHAI ELECTRIC

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.11 HD HYUNDAI HEAVY INDUSTRIES

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Other developments

- 15.1.12 DOOSAN ENERBILITY

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.13 DOONGFANG ELECTRIC CORPORATION

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Expansions

- 15.1.14 ENVISION GROUP

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product launches

- 15.1.14.3.2 Deals

- 15.1.14.3.3 Expansions

- 15.1.14.3.4 Other developments

- 15.1.15 BW IDEOL

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches

- 15.1.15.3.2 Deals

- 15.1.15.3.3 Other developments

- 15.1.16 PRINCIPLE POWER

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Product launches

- 15.1.16.3.2 Deals

- 15.1.16.3.3 Other developments

- 15.1.17 X1 WIND

- 15.1.17.1 Business overview

- 15.1.17.2 Products/Solutions/Services offered

- 15.1.17.3 Recent developments

- 15.1.17.3.1 Deals

- 15.1.17.3.2 Expansions

- 15.1.18 JAPAN MARINE UNITED CORPORATION

- 15.1.18.1 Business overview

- 15.1.18.2 Products/Solutions/Services offered

- 15.1.18.3 Recent developments

- 15.1.18.3.1 Deals

- 15.1.19 SAITEC OFFSHORE

- 15.1.19.1 Business overview

- 15.1.19.2 Products/Solutions/Services offered

- 15.1.19.3 Recent developments

- 15.1.19.3.1 Deals

- 15.1.19.3.2 Other developments

- 15.1.20 STEISDAL

- 15.1.20.1 Business overview

- 15.1.20.2 Products/Solutions/Services offered

- 15.1.20.3 Recent developments

- 15.1.20.3.1 Deals

- 15.1.21 NOV

- 15.1.21.1 Business overview

- 15.1.21.2 Products/Solutions/Services offered

- 15.1.21.3 Recent developments

- 15.1.21.3.1 Product launches

- 15.1.21.3.2 Other developments

- 15.1.22 CS WIND CORPORATION

- 15.1.22.1 Business overview

- 15.1.22.2 Products/Solutions/Services offered

- 15.1.22.3 Recent developments

- 15.1.22.3.1 Deals

- 15.1.22.3.2 Other developments

- 15.1.23 SEATRIUM

- 15.1.23.1 Business overview

- 15.1.23.2 Products/Solutions/Services offered

- 15.1.23.3 Recent developments

- 15.1.23.3.1 Deals

- 15.1.23.3.2 Other developments

- 15.1.24 TECHNIP ENERGIES

- 15.1.24.1 Business overview

- 15.1.24.2 Products/Solutions/Services offered

- 15.1.24.3 Recent developments

- 15.1.24.3.1 Deals

- 15.1.1 GE VERNOVA

- 15.2 OTHER PLAYERS

- 15.2.1 GICON-GROBMANN INGENIEUR CONSULT GMBH

- 15.2.2 GAZELLE WIND POWER LTD

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 List of primary interview participants

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 16.3.1 DEMAND-SIDE ANALYSIS

- 16.3.1.1 Demand-side assumptions

- 16.3.1.2 Demand-side calculations

- 16.3.2 SUPPLY-SIDE ANALYSIS

- 16.3.2.1 Supply-side assumptions

- 16.3.2.2 Supply-side calculations

- 16.3.1 DEMAND-SIDE ANALYSIS

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS AND LIMITATIONS

- 16.8 RISK ANALYSIS

17 APPENDIX

- 17.1 INSIGHTS FROM INDUSTRY EXPERTS

- 17.2 DISCUSSION GUIDE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS