|

시장보고서

상품코드

2024208

자동차용 카메라 시장 : 기술별, ICE/EV 용도별, 차종별, 시야별, EV 유형별, 자율주행 레벨별, 지역별 - 세계 예측(-2033년)Automotive Camera Market by Technology (Digital, Infrared, Thermal), ICE and EV Application (ACC, BSD, AFL, IPA, OMS, NVS, & PA), Vehicle Type (PC, LCV, HCV), View (Front, Rear, Surround), EV Type, Level of Autonomy, Region - Global Forecast to 2033 |

||||||

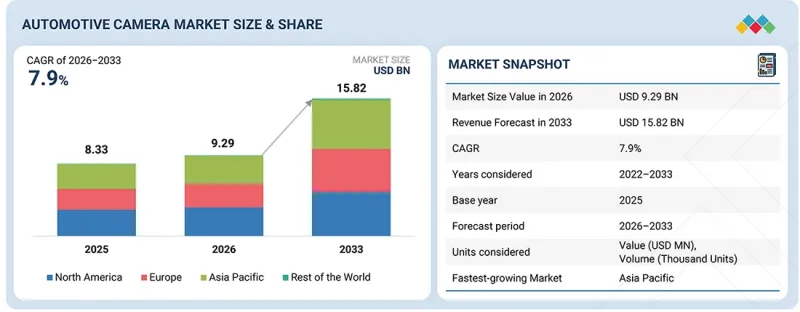

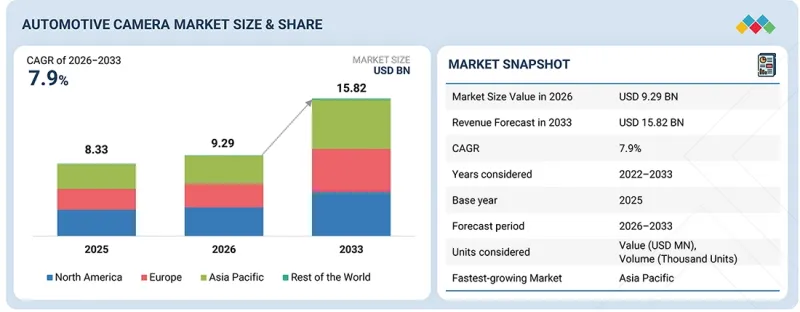

세계의 자동차용 카메라 시장 규모는 2026년 92억 9,000만 달러에서 2033년까지 158억 2,000만 달러에 달할 것으로 예측되며, CAGR로 7.9%의 확대가 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 10억 달러 |

| 부문 | 기술, ICE/EV 용도, 차종, 시야, EV 유형, 자율주행 레벨, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 기타 지역 |

프리미엄 자동차에 대한 수요 증가, 더 안전하고 스마트한 모빌리티 솔루션에 대한 소비자 선호, 자율주행차의 급속한 발전으로 인해 전 세계적으로 시장이 확대되고 있습니다. 이러한 추세는 안전과 운전 경험을 향상시키는 어댑티브 크루즈 컨트롤, 나이트 비전 시스템, 차선 유지 보조 등 운전 보조 기능에 첨단 카메라 시스템이 활용되고 있음을 보여줍니다. 또한, 자동차 카메라 시스템에 AI/ML 통합과 같은 첨단 기술의 통합이 시장 성장을 가속화하고 있습니다.

"시야 유형별로는 서라운드 뷰 카메라가 차량용 카메라 시장에서 가장 빠르게 성장할 것으로 예상됩니다."

서라운드 뷰 카메라는 차량 주변의 360도 시야를 제공하고 안전과 주차 편의성을 향상시키는 장점으로 인해 모든 차량 유형 부문에서 점점 더 널리 보급되고 있습니다. 초기에는 프리미엄 및 고급 차량에 한정되어 있었지만, 현재는 비용 최적화 및 안전 기능에 대한 소비자 수요 증가로 인해 많은 OEM들이 해치백 및 소형 SUV를 포함한 미들 부문 차량에 서라운드 뷰 시스템을 확대 적용하고 있습니다. 이 시스템은 전방, 후방, 사이드 미러에 설치된 여러 대의 고해상도 카메라를 통합하여 차량 주변의 실시간 연결된 오버뷰 시야를 생성합니다. 자동차 OEM들은 안전성을 높이고, 규제 요건에 대응하며, 특히 저속 주행과 밀집된 도시 환경에서의 주차 편의성을 높이기 위해 새로운 차량 플랫폼에 멀티 카메라 시스템 탑재를 확대하고 있습니다. Robert Bosch, Continental, Valeo, Magna와 같은 주요 Tier 1 공급업체들은 360° 통합 인식 시스템을 제공함으로써 이러한 추세를 주도하고 있으며, 이를 통해 자동 주차 및 물체 감지 등의 첨단 기능을 가능하게 하고 있습니다. 이러한 트렌드를 주도하고 있습니다. 따라서 이러한 시스템은 현대 ADAS 스택의 핵심 요소로 자리 잡았습니다. 따라서, OEM의 통합이 진행되고 기술이 발전함에 따라 서라운드 뷰 카메라 시스템이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다.

"사각지대감지가 자동차 카메라의 가장 큰 용도가 될 것으로 예상됩니다."

사각지대감지(BSD) 시스템은 정숙한 주행의 안전성 향상을 위해 ICE 승용차 및 전기 승용차에서 채택이 확대되고 있습니다. BSD는 중급차부터 고급차에서 가장 보편적인 ADAS 기능 중 하나입니다. 이 시스템은 여러 대의 카메라와 센서(보통 2대, 고급차에서는 1대당 최대 3-4대)를 이용하여 카메라의 탑재 대수를 직접적으로 증가시키기 때문에 현재 시장에서 압도적인 점유율을 차지하고 있습니다. 도시화가 진행되고 대도시권의 교통 혼잡이 증가함에 따라 시야 제한 및 차선 변경 조작에 따른 위험이 증가하고 있으며, 이에 따라 BSD 시스템에 대한 수요가 가속화되고 있습니다. 카메라 기반의 ADAS 기능은 주로 사이드 미러나 리어 범퍼에 장착된 광각 후방 카메라로 사용되기 때문에 인접 차선이나 차량의 사각지대를 커버할 수 있습니다. 또한, 전 세계 OEM들은 센서 융합, 즉 자동차 카메라와 레이더, 360° 서라운드 뷰 시스템의 조합으로 전환하고 있으며, 레인 어시스트, 자동 주차 등의 기능과의 통합이 진행되고 있습니다. 이로써 BSD의 유용성은 단일 기능에 그치지 않고 ADAS의 핵심인 인지 레이어로 확장되고 있습니다. 부문 전반에 걸친 보급, 차량 당 카메라 탑재 대수 증가, 규제 당국의 강력한 추진력, OEM의 표준화 진행, 광범위한 ADAS 아키텍처에서 필수적인 역할로 인해 사각지대감지는 예측 기간 동안 자동차 카메라의 가장 큰 응용 분야로 남을 것으로 예상됩니다.

세계의 자동차용 카메라 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 그리고 혁신

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 자동차용 카메라 시장(OE-ICE) : 용도별

제10장 자동차용 카메라 시장(OE-ICE) : 차종별

제11장 자동차용 카메라 시장(OE-ICE) : 기술별

제12장 자동차용 카메라 시장(OE-ICE) : 시야 유형별

제13장 전기자동차·하이브리드 자동차(OE)용 카메라 시장 : 용도별

제14장 전기자동차·하이브리드 자동차(OE)용 카메라 시장 : EV 유형별

제15장 자동차용 카메라 시장(ICE) : 자율주행 레벨별

제16장 자동차용 카메라 애프터마켓 수요

제17장 자동차용 카메라(OE-ICE) 시장 : 지역별

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

KSM 26.05.19The global automotive camera market size is projected to grow from USD 9.29 billion in 2026 to USD 15.82 billion by 2033, at a CAGR of 7.9%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | Automotive Camera Market by Technology, ICE and EV Application, Vehicle Type, View, EV Type, Level of Autonomy, Region - Global Forecast to 2033 |

| Regions covered | Asia Pacific, Europe, North America, and the Rest of the World |

The market is expanding globally due to the growing demand for premium vehicles, consumer preference for safer and smarter mobility solutions, and rapid advancements in autonomous vehicles. This trend highlights the use of advanced camera systems for driver assistance features such as adaptive cruise control, night vision system, and lane keep assist to enhance safety and driving experience. Additionally, the integration of cutting-edge technologies, such as AI/ML integration in automotive camera systems, accelerates market growth.

"Surround-view camera to be fastest-growing segment in automotive camera market, by view type"

Surround-view cameras offer a 360-degree view around the vehicle, which is increasingly gaining traction across vehicle segments due to their enhanced safety and parking convenience benefits. Initially limited to premium and luxury vehicles, currently many OEMs have expanded the availability of surround-view systems to mid-segment vehicles, including hatchbacks and compact SUVs, driven by cost optimization and rising consumer demand for safety features. These systems integrate multiple high-resolution cameras mounted at the front, rear, and side mirrors, generating a real-time stitched top-down view of the vehicle's surroundings. Automotive OEMs are increasingly installing multi-camera systems into new vehicle platforms to enhance safety, meet regulatory requirements, and improve user convenience, particularly for low-speed maneuvers and parking in dense urban environments. Major Tier 1 suppliers such as Robert Bosch, Continental, Valeo, and Magna are supporting this trend by delivering fully integrated 360° perception systems that provide a stitched top-down view and enable advanced functions like automated parking and object detection, making them a core part of modern ADAS stacks. Hence, with increasing OEM integration and technological advancements, surround-view camera systems are projected to grow at the fastest rate during the forecast period.

"Blind spot detection to be largest application of automotive cameras"

Blind spot detection (BSD) systems are witnessing increasing adoption in ICE and electric passenger vehicles, driven by the need for enhanced safety in silent vehicle operation. BSD is one of the most common ADAS features in mid- to premium-range cars. It utilizes multiple sets of cameras and sensors (usually 2 and can go up to 3-4 units per vehicle in higher-end cars), directly increasing the camera count, leading to its dominant share in the current scenario. With rising urbanization and increasing traffic congestion in metropolitan areas, the risk associated with limited visibility and lane-changing maneuvers is growing, thereby accelerating the demand for BSD systems. The integration of camera-based ADAS features, as they are primarily used in wide-angle rear-facing cameras mounted on side mirrors or rear bumpers, enables coverage of adjacent lanes and vehicle blind zones. Further, global OEMs are shifting toward sensor fusion, i.e., a combination of automotive cameras along with radars plus a 360° surround-view system, and integration with functions like lane assist and automated parking. This is expanding the BSD's utility beyond a single feature into a core perception ADAS layer. With its cross-segment penetration, higher camera-per-vehicle requirement, strong regulatory push, increasing OEM standardization, and integral role in broader ADAS architectures, blind spot detection is expected to remain the largest automotive camera application throughout the forecast period.

"Asia Pacific to be second-largest automotive camera market"

The Asia Pacific is the second-largest automotive camera market, driven by high vehicle production, rapid ADAS adoption in some economy-to-mid-level vehicles, and evolving safety regulations. China leads the market in the region due to its massive production base and increasing penetration of camera-based ADAS across both mass (A-C segment) and premium vehicles, where features such as rear-view cameras, lane departure warning, and 360-degree surround view are becoming standard. India is emerging as a high-growth market, supported by rising safety awareness, regulatory push, and increasing demand for affordable ADAS features in passenger vehicles. Meanwhile, Japan and South Korea are witnessing strong demand due to advanced safety standards and higher adoption of Level 2 and Level 2+ autonomous features, particularly in premium and electric vehicles. Growth is also notable in the commercial vehicle segment, where fleet operators are adopting cameras for blind spot detection, driver monitoring, and rear visibility to improve safety and efficiency.

The growth in the region is primarily driven by increasing safety regulations, electrification, and OEM-led technology integration. Automakers such as Hyundai Motor Company, Kia Corporation, Toyota Motor Corporation, and Honda Motor Co., Ltd. are aggressively integrating multi-camera systems across vehicle segments, focusing on applications such as ADAS, driver monitoring systems, and parking assistance. In addition, the shift toward EVs, especially in China, Japan, and South Korea, is accelerating camera adoption due to advanced electronic architectures. With strong policy support and rising investments in cost-effective camera modules, the demand for automotive cameras in the Asia Pacific is expected to remain high, with India and China acting as key growth engines due to volume expansion and increasing feature penetration.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in the automotive camera market. The break-up of the primaries is as follows:

- By Respondent Type: OEMs - 25%, Tier I -55%, and Tier II - 20%,

- By Designation: C-Level Director - 30%, Director-Level- 60%, and Others - 10%

- By Region: North America - 30%, Europe - 30%, and Asia Pacific - 40%,

The automotive camera market comprises major players such as Robert Bosch GmbH (Germany), Continental AG (Germany), Valeo (France), ZF Friedrichshafen AG (Germany), Denso Corporation (Japan), and Ficosa Internacional SA (Spain).

Research Coverage:

This research report categorizes the automotive camera market by technology (digital, infrared, thermal), EV application (adaptive cruise control, forward collision warning, traffic sign recognition, blind spot detection, lane keep assist, adaptive lighting system, intelligent park assist, driver monitoring system, night vision system, parking assist), vehicle type (passenger car, light commercial vehicle, heavy commercial vehicle), view type (front view, surround view, rear view), EV type (battery electric vehicle, plug-in hybrid electric vehicle, fuel cell electric vehicle), level of autonomy (Level 0/1, Level 2, Level 3), and region (Asia Pacific, Europe, North America, Rest of the World).

The report provides detailed information regarding key factors influencing market growth, including drivers, restraints, opportunities, and challenges. It also includes an in-depth competitive analysis of major industry players, covering their company profiles, product and service offerings, key strategies, partnerships, agreements, product launches, mergers & acquisitions, and recent developments. Additionally, the report covers analysis of SMEs/startups, the supplier ecosystem, and key developments across the automotive camera market.

Key Benefits of Buying the Report:

- The report will help market leaders and new entrants with information on the closest approximations of revenue numbers for the overall automotive camera market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain insights to position their businesses effectively and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market dynamics and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (shift toward camera-based perception systems replacing traditional sensors in entry- and mid-level vehicles, along with strong regulatory push for automotive safety features such as ADAS and rear-view cameras), restraints (high validation and calibration complexity of multi-camera systems and performance sensitivity under adverse environmental conditions such as low light and weather), opportunities (rapid adoption of camera-only or camera-dominant perception architectures in ADAS and growing demand for in-cabin sensing applications such as driver monitoring systems), and challenges (increasing bandwidth and data processing limitations with rising camera count and ensuring real-world performance reliability across diverse driving conditions)

- Product Development/Innovation: Insights into upcoming technologies, R&D activities, and advancements in camera systems, including AI-based image processing, high-resolution imaging, thermal sensing, and sensor fusion technologies

- Market Development: Comprehensive information about key markets, with analysis across major regions such as the Asia Pacific, Europe, North America, and the Rest of the World

- Market Diversification: Detailed insights into untapped markets, emerging applications, and recent investments in the automotive camera ecosystem

- Competitive Assessment: In-depth analysis of market share, growth strategies, and product offerings of leading players such as Robert Bosch GmbH, Continental AG, Valeo, ZF Friedrichshafen AG, and Denso Corporation

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AUTOMOTIVE CAMERA MARKET

- 2.4 HIGH-GROWTH SEGMENTS IN AUTOMOTIVE CAMERA MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE CAMERA MARKET

- 3.2 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY ICE APPLICATION

- 3.3 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VEHICLE TYPE

- 3.4 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY

- 3.5 ELECTRIC VEHICLE CAMERA MARKET (OE), BY EV TYPE

- 3.6 AUTOMOTIVE CAMERA MARKET, BY VIEW TYPE

- 3.7 ELECTRIC VEHICLE CAMERA MARKET (OE), BY EV APPLICATION

- 3.8 AUTOMOTIVE CAMERA MARKET (OE), BY LEVEL OF AUTONOMY

- 3.9 AUTOMOTIVE CAMERA MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Shift toward camera-based perception systems in entry and mid-level vehicles

- 4.2.1.2 Regulation-led "camera-per- vehicle inflation"

- 4.2.2 RESTRAINTS

- 4.2.2.1 Validation and calibration complexity for multi-camera systems

- 4.2.2.2 Susceptibility to environmental conditions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid adoption of camera-only or camera-dominant perception architectures in ADAS

- 4.2.3.2 Rise of in-cabin sensing applications

- 4.2.4 CHALLENGES

- 4.2.4.1 Bandwidth and data processing limitations with increasing camera count

- 4.2.4.2 Ensuring performance reliability in real-world environments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 CROSS-INDUSTRY STRATEGIC THEMES

- 4.5.1.1 Shift from camera module -> perception system

- 4.5.1.2 Multi-camera architecture expansion

- 4.5.1.3 OEM co-development & platform lock-ins

- 4.5.1.4 Regional manufacturing & China /Emerging market focus

- 4.5.1.5 Transition to software-defined vehicles (SDVs)

- 4.5.1 CROSS-INDUSTRY STRATEGIC THEMES

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.2.1 RAW MATERIAL SUPPLIERS

- 5.2.2 COMPONENT MANUFACTURERS/TECHNOLOGY PROVIDERS

- 5.2.3 CLOUD SERVICE PROVIDERS

- 5.2.4 OEMS

- 5.2.5 END USERS

- 5.3 SUPPLIER LIST OF AUTOMOTIVE CAMERA COMPONENTS

- 5.3.1 LIST OF IMAGE SENSOR SUPPLIERS

- 5.3.2 LIST OF CAMERA MODULE SUPPLIERS

- 5.3.3 LIST OF TIER 1 ADAS SUPPLIERS

- 5.3.4 LIST OF SOFTWARE SUPPLIERS

- 5.3.5 LIST OF SEMICONDUCTOR SUPPLIERS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2023-2025

- 5.4.2 AVERAGE SELLING PRICE, BY REGION, 2025

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 900211)

- 5.5.2 EXPORT SCENARIO (HS CODE 900211)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 DRIVER STATUS MONITOR BY DENSO

- 5.9.2 MPILOT AUTONOMOUS PARKING AND HIGHWAY DRIVING SYSTEM BY MOMENTA

- 5.9.3 R-CAR SOFTWARE DEVELOPMENT KIT BY RENESAS

- 5.9.4 EVASIVE MANEUVER ASSIST SYSTEM BY UNIVERSITY OF TOKYO

- 5.10 SENSOR FUSION SYSTEM BY NIDEC ELESYS

- 5.11 ECOSYSTEM ANALYSIS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 VEHICLE PLATFORM AND E/E ARCHITECTURE

- 6.1.2 CENTRALIZED COMPUTE PLATFORM

- 6.1.3 ZONAL ARCHITECTURE

- 6.1.4 SOFTWARE-DEFINED VEHICLE

- 6.1.5 HIGH-SPEED NETWORK

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 RADAR, LIDAR, AND ULTRASONIC SENSOR

- 6.2.2 ADAS ECU

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2027): FOUNDATION AND EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2030): SCALING AND PERFORMANCE OPTIMIZATION

- 6.3.3 LONG-TERM (2030-2033): FULL AUTONOMY AND INTELLIGENT ECOSYSTEMS

- 6.4 IMPACT OF AI/GENERATIVE AI

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF EU-FTA TRADE DEAL ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 6.7 IMPACT OF ISRAEL-IRAN WAR ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS

- 7.2.2 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.2.2.1 European Union

- 7.2.2.2 US

- 7.2.2.3 China

- 7.2.2.4 India

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.2.3.1 Type I ecolabels

- 7.2.3.2 Product carbon footprint

- 7.2.3.3 Ecodesign and material standards

- 7.2.3.4 Hazardous substance restrictions

- 7.2.3.5 Circular economy and recycling certification

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.1.1 KEY BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 ADAPTIVE CRUISE CONTROL

- 9.2.1 ENHANCES OBJECT CLASSIFICATION, LANE CONTEXT, AND PERFORMANCE IN COMPLEX SCENARIOS

- 9.3 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING

- 9.3.1 INTEGRATION OF ADAPTIVE CRUISE CONTROL AND FORWARD COLLISION WARNING IN MID-RANGE VEHICLES TO DRIVE MARKET

- 9.4 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION

- 9.4.1 RELIANT ON FRONT-VIEW CAMERAS AND ON-BOARD IMAGE PROCESSING

- 9.5 BLIND SPOT DETECTION

- 9.5.1 STANDARDIZATION OF ADAS ACROSS MID AND HIGH SEGMENTS IN EMERGING MARKETS TO DRIVE GROWTH

- 9.6 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING

- 9.6.1 EFFECTIVE FOR HIGHWAY AND LONG-DISTANCE DRIVING

- 9.7 ADAPTIVE LIGHTING SYSTEM

- 9.7.1 EVOLVING TOWARD CAMERA-INTEGRATED MATRIX LED AND PIXEL LIGHTING

- 9.8 INTELLIGENT PARKING ASSIST

- 9.8.1 EMERGING AS PREMIUM CONVENIENCE FEATURE

- 9.9 DRIVER MONITORING SYSTEM

- 9.9.1 RISING CONCERNS ABOUT DRIVER FATIGUE AND DISTRACTION TO DRIVE GROWTH

- 9.10 NIGHT VISION SYSTEM

- 9.10.1 IMPROVED INFRARED AND THERMAL IMAGING TECHNOLOGIES TO DRIVE GROWTH

- 9.11 PARKING ASSIST

- 9.11.1 TRANSITION FROM COMPLIANCE-DRIVEN FEATURE TO MULTI-CAMERA, SOFTWARE-LED SYSTEM TO DRIVE GROWTH

- 9.12 KEY PRIMARY INSIGHTS

10 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 PASSENGER CAR

- 10.2.1 GOVERNMENT REGULATIONS FOR MAKING ADAS MANDATORY IN PASSENGER CARS TO DRIVE GROWTH

- 10.3 LIGHT COMMERCIAL VEHICLE

- 10.3.1 INCREASING EMPHASIS ON LOGISTICS EFFICIENCY AND SAFETY TO DRIVE MARKET

- 10.4 HEAVY COMMERCIAL VEHICLE

- 10.4.1 GROWING NEED FOR IMPROVED DRIVER VISIBILITY TO DRIVE GROWTH

- 10.5 KEY PRIMARY INSIGHTS

11 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 DIGITAL

- 11.2.1 INCREASING ADOPTION OF ADAS TO DRIVE GROWTH

- 11.3 INFRARED

- 11.3.1 TRANSITION FROM OPTIONAL SAFETY FEATURE TO REGULATORY-MANDATED STANDARD TO DRIVE GROWTH

- 11.4 THERMAL

- 11.4.1 ADVANCEMENTS IN THERMAL IMAGING TECHNOLOGY FOR OBJECT DETECTION CAPABILITY ENHANCEMENT TO DRIVE GROWTH

12 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE

- 12.1 INTRODUCTION

- 12.2 FRONT VIEW

- 12.2.1 NEED FOR COMPLIANCE WITH NCAP STANDARDS TO DRIVE GROWTH

- 12.3 REAR VIEW

- 12.3.1 SHIFT TOWARD HIGHER DYNAMIC RANGE TO DRIVE GROWTH

- 12.4 SURROUND VIEW

- 12.4.1 DEMAND FOR ENHANCED PARKING AND MANEUVERING ASSISTANCE IN CONGESTED URBAN AREAS TO DRIVE GROWTH

- 12.5 KEY PRIMARY INSIGHTS

13 ELECTRIC AND HYBRID VEHICLE (OE) CAMERA MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 ADAPTIVE CRUISE CONTROL (ACC)

- 13.2.1 SURGING ADOPTION OF ADAS IN MID-SEGMENT VEHICLES TO DRIVE GROWTH

- 13.3 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING

- 13.3.1 ENABLES AUTOMATIC SPEED, DISTANCE MANAGEMENT, AND TIMELY ALERTS IN CRITICAL SITUATIONS

- 13.4 ADAPTIVE CRUISE CONTROL (ACC) + FORWARD COLLISION WARNING (FCW) + TRAFFIC SIGN RECOGNITION (TSR)

- 13.4.1 REGULATORY BODIES PUSHING FOR ENHANCED ROAD SAFETY STANDARDS TO DRIVE GROWTH

- 13.5 BLIND SPOT DETECTION

- 13.5.1 GROWING COMPLEXITY OF URBAN DRIVING ENVIRONMENTS AND EV-SPECIFIC SAFETY CHALLENGES TO DRIVE GROWTH

- 13.6 BLIND SPOT DETECTION (BSD) + LANE KEEP ASSIST (LKA) + LANE DEPARTURE WARNING (LDW)

- 13.6.1 GROWING DEMAND FOR BUNDLED SAFETY FEATURES IN ASIA PACIFIC AND EUROPE TO DRIVE GROWTH

- 13.7 ADAPTIVE LIGHTING SYSTEM (ALS)

- 13.7.1 SHIFT FROM PREMIUM TO CRITICAL SAFETY FEATURE TO DRIVE GROWTH

- 13.8 INTELLIGENT PARKING ASSIST (IPA)

- 13.8.1 RISING ADOPTION IN PREMIUM ELECTRIC AND PLUG-IN HYBRID VEHICLES TO DRIVE GROWTH

- 13.9 DRIVER MONITORING SYSTEM (DMS)

- 13.9.1 GROWING ADOPTION IN DEVELOPED ECONOMIES TO DRIVE GROWTH

- 13.10 NIGHT VISION SYSTEM (NVS)

- 13.10.1 DEVELOPMENT OF SEMI AND FULLY AUTONOMOUS CARS NECESSITATING ADVANCED NIGHT VISION CAPABILITIES TO DRIVE MARKET

- 13.11 PARKING ASSIST

- 13.11.1 GROWING DEMAND FOR SAFETY FEATURES DURING VEHICLE REVERSALS TO PREVENT COLLISIONS TO DRIVE GROWTH

- 13.12 KEY PRIMARY INSIGHTS

14 ELECTRIC AND HYBRID VEHICLE (OE) CAMERA MARKET, BY EV TYPE

- 14.1 INTRODUCTION

- 14.2 BATTERY ELECTRIC VEHICLE (BEV)

- 14.2.1 DEPLOYMENT OF PEDESTRIAN AND CYCLIST DETECTION SYSTEMS TO DRIVE GROWTH

- 14.3 PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

- 14.3.1 CONSUMER PREFERENCE FOR ADVANCED SAFETY TECHNOLOGIES TO DRIVE GROWTH

- 14.4 FUEL CELL ELECTRIC VEHICLE (FCEV)

- 14.4.1 INTEGRATION OF ADAPTIVE CRUISE CONTROL AND LANE KEEP ASSISTANCE TO DRIVE GROWTH

- 14.5 KEY PRIMARY INSIGHTS

15 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY

- 15.1 INTRODUCTION

- 15.2 LEVEL 0/LEVEL 1 (L0/L1)

- 15.2.1 WIDELY DEPLOYED ACROSS ENTRY AND MID-SEGMENT VEHICLES

- 15.3 LEVEL 2 (L2)

- 15.3.1 HIGH DEMAND FOR ADVANCED DRIVER ASSISTANCE IN PREMIUM VEHICLE SEGMENT TO DRIVE MARKET

- 15.4 LEVEL 3 (L3)

- 15.4.1 OEM PUSH FOR HIGHER LEVELS OF AUTONOMOUS VEHICLES TO DRIVE MARKET

- 15.5 KEY PRIMARY INSIGHTS

16 AUTOMOTIVE CAMERA AFTERMARKET DEMAND

- 16.1 INTRODUCTION

- 16.2 AUTOMOTIVE CAMERA AFTERMARKET FOR ORGANIZED PLAYERS

- 16.3 AUTOMOTIVE CAMERA AFTERMARKET FOR UNORGANIZED PLAYERS

- 16.4 REGIONAL TRENDS FOR AUTOMOTIVE CAMERA AFTERMARKET DEMAND

- 16.5 AFTERMARKET PRICING ANALYSIS FOR DIFFERENT TYPES OF CAMERAS AT REGIONAL LEVEL

17 AUTOMOTIVE CAMERA (OE-ICE) MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 ASIA PACIFIC

- 17.2.1 CHINA

- 17.2.1.1 Push toward commercialization of autonomous vehicles to drive market

- 17.2.2 INDIA

- 17.2.2.1 Rising safety awareness and regulatory push to drive market

- 17.2.3 JAPAN

- 17.2.3.1 Mandated safety features and innovation to drive market

- 17.2.4 SOUTH KOREA

- 17.2.4.1 Rising investment in autonomous driving solutions to drive market

- 17.2.5 THAILAND

- 17.2.5.1 Increasing vehicle manufacturing and exports to drive market

- 17.2.6 REST OF ASIA PACIFIC

- 17.2.1 CHINA

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Advancements in automotive camera technology to drive market

- 17.3.2 FRANCE

- 17.3.2.1 Stringent government policies aimed at enhancing road safety to drive market

- 17.3.3 SPAIN

- 17.3.3.1 Initiatives for advanced automotive systems to drive market

- 17.3.4 RUSSIA

- 17.3.4.1 Government regulations mandating advanced safety systems to drive market

- 17.3.5 UK

- 17.3.5.1 Government's commitment to autonomy and safety to drive market

- 17.3.6 TURKEY

- 17.3.6.1 Surging adoption of driver assistance functions to drive market

- 17.3.7 REST OF EUROPE

- 17.3.1 GERMANY

- 17.4 NORTH AMERICA

- 17.4.1 US

- 17.4.1.1 Major automakers equipping premium vehicles with automotive cameras to drive market

- 17.4.2 CANADA

- 17.4.2.1 Growth of connected and autonomous vehicles to drive market

- 17.4.3 MEXICO

- 17.4.3.1 Emergence as key manufacturing hub for automakers and vehicle parts to drive market

- 17.4.1 US

- 17.5 REST OF THE WORLD (ROW)

- 17.5.1 BRAZIL

- 17.5.1.1 Government encouraging adoption of camera-enabled ADAS to drive market

- 17.5.2 IRAN

- 17.5.2.1 Consumer demand for safety features in vehicles to drive market

- 17.5.3 OTHERS

- 17.5.1 BRAZIL

18 COMPETITIVE LANDSCAPE

- 18.1 INTRODUCTION

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 18.3 MARKET SHARE ANALYSIS, 2025

- 18.4 REVENUE ANALYSIS, 2021-2025

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.6 BRAND/PRODUCT COMPARISON

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 View type footprint

- 18.7.5.4 Level of autonomy footprint

- 18.7.5.5 Technology footprint

- 18.7.5.6 Vehicle type footprint

- 18.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPETITIVE BENCHMARKING

- 18.8.5.1 List of start-ups/SMEs

- 18.8.5.2 Competitive benchmarking of start-ups/SMEs

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

- 18.9.4 OTHERS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 ROBERT BOSCH GMBH

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches/developments

- 19.1.1.3.2 Deals

- 19.1.1.3.3 Others

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 MAGNA INTERNATIONAL INC.

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches/developments

- 19.1.2.3.2 Deals

- 19.1.2.3.3 Expansions

- 19.1.2.3.4 Others

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 VALEO

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches/developments

- 19.1.3.3.2 Deals

- 19.1.3.3.3 Expansions

- 19.1.3.3.4 Others

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 ZF FRIEDRICHSHAFEN AG

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches/developments

- 19.1.4.3.2 Deals

- 19.1.4.3.3 Expansions

- 19.1.4.3.4 Others

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses and competitive threats

- 19.1.5 DENSO CORPORATION

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches/developments

- 19.1.5.3.2 Deals

- 19.1.5.3.3 Expansions

- 19.1.5.3.4 Others

- 19.1.5.4 MnM view

- 19.1.5.4.1 Key strengths

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses and competitive threats

- 19.1.6 FICOSA INTERNACIONAL SA

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches/developments

- 19.1.6.3.2 Deals

- 19.1.6.3.3 Expansions

- 19.1.6.3.4 Others

- 19.1.7 APTIV

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches/developments

- 19.1.7.3.2 Deals

- 19.1.7.3.3 Expansions

- 19.1.7.3.4 Others

- 19.1.8 AUMOVIO SE

- 19.1.8.1 Business overview

- 19.1.8.2 Products offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Product launches/developments

- 19.1.8.3.2 Deals

- 19.1.8.3.3 Expansions

- 19.1.9 FORVIA

- 19.1.9.1 Business overview

- 19.1.9.2 Products offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Product launches/developments

- 19.1.9.3.2 Deals

- 19.1.9.3.3 Expansions

- 19.1.9.3.4 Others

- 19.1.10 RICOH

- 19.1.10.1 Business overview

- 19.1.10.2 Products offered

- 19.1.11 KYOCERA CORPORATION

- 19.1.11.1 Business overview

- 19.1.11.2 Products offered

- 19.1.11.3 Recent developments

- 19.1.11.3.1 Product launches/developments

- 19.1.11.3.2 Expansions

- 19.1.11.3.3 Others

- 19.1.1 ROBERT BOSCH GMBH

- 19.2 OTHER PLAYERS

- 19.2.1 MOTHERSON

- 19.2.2 AMBARELLA INTERNATIONAL LP

- 19.2.3 OMNIVISION

- 19.2.4 HITACHI ASTEMO, LTD.

- 19.2.5 GENTEX CORPORATION

- 19.2.6 SAMSUNG ELECTRO-MECHANICS

- 19.2.7 TELEDYNE FLIR LLC

- 19.2.8 HYUNDAI MOBIS

- 19.2.9 MCNEX CO., LTD.

- 19.2.10 STONKAM CO., LTD.

- 19.2.11 BRIGADE ELECTRONICS GROUP PLC

- 19.2.12 H.P.B. OPTOELECTRONICS CO., LTD.

- 19.2.13 SONY SEMICONDUCTOR SOLUTIONS CORPORATION

- 19.2.14 LG ELECTRONICS

- 19.2.15 GARMIN LTD.

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 List of secondary sources

- 20.1.1.2 Key data from secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 Breakdown of primaries

- 20.1.2.2 Primary participants

- 20.1.2.3 Objectives of primary research

- 20.1.2.4 Sampling techniques and data collection methods

- 20.1.1 SECONDARY DATA

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 BOTTOM-UP APPROACH

- 20.2.2 TOP-DOWN APPROACH

- 20.3 DATA TRIANGULATION

- 20.4 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

- 20.5 RESEARCH LIMITATIONS

21 APPENDIX

- 21.1 INSIGHTS FROM INDUSTRY EXPERTS

- 21.2 DISCUSSION GUIDE

- 21.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.4 CUSTOMIZATION OPTIONS

- 21.4.1 GLOBAL AUTOMOTIVE CAMERA MARKET, BY APPLICATION AND VEHICLE TYPE (ICE)

- 21.4.2 ELECTRIC & HYBRID VEHICLE CAMERA MARKET, BY APPLICATION AND ELECTRIC VEHICLE TYPE

- 21.4.3 COMPANY INFORMATION:

- 21.4.3.1 Profiling of additional market players (up to 5)

- 21.5 RELATED REPORTS

- 21.6 AUTHOR DETAILS