|

시장보고서

상품코드

2029867

저속 차량 시장 : 차종(골프 카트, 상업용 잔디 관리차, 산업용 다목적차, 개인용), 출력(5kW 미만, 5-8 kW, 9-15 kW, 15kW 이상), 모터 유형 및 구성, 배터리, 추진, 카테고리, 용도, 전압별 - 세계 예측(-2035년)Low-speed Vehicle Market by Vehicle Type (Golf Cart, Commercial Turf Utility, Industrial Utility, Personal), Power Output (<5, 5-8, 9-15, >15 kW), Motor Type & Configuration, Battery, Propulsion, Category, Application, Voltage - Global Forecast to 2035 |

||||||

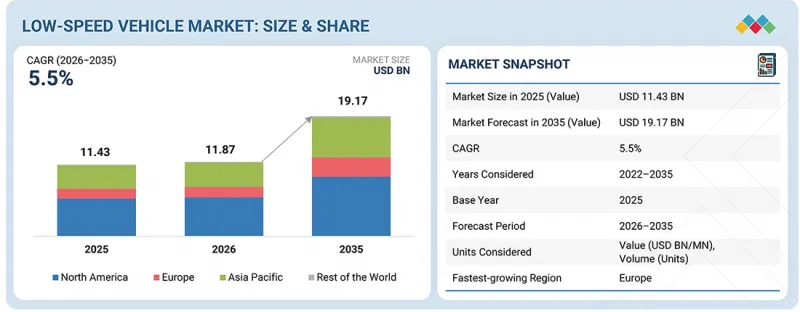

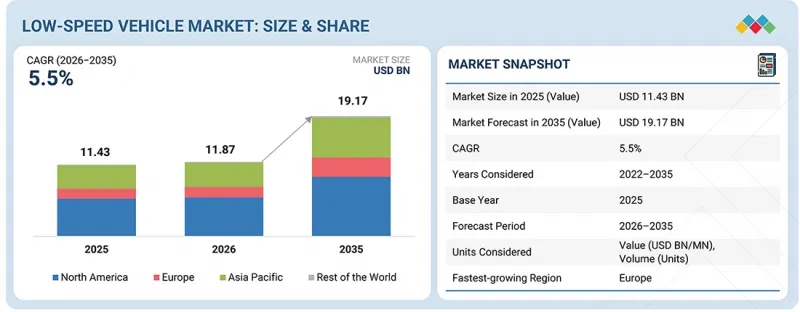

저속 차량 시장 규모는 2026년 118억 7,000만 달러에서 2035년까지 191억 7,000만 달러에 달할 것으로 예측되며, CAGR은 5.5%를 기록할 전망입니다.

저속 차량은 도로 주행 차량에 적용되는 완전한 형식승인 요건을 적용받지 않기 때문에 통제된 환경에서의 도입이 가속화되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2035년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 단위 | 달러 |

| 부문 | 차종, 출력, 모터 유형 및 구성, 추진 구분, 배터리, 용도, 카테고리, 전압별 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 세계 기타 지역 |

미국 교통부 도로교통안전국(NHTSA)과 같은 기관의 규제 프레임워크에서 저속 차량은 FMVSS 500에 따라 제한 속도 도로용 차량으로 분류됩니다. 이를 통해 저속 차량은 완전 규제 대상인 승용차와 명확히 구분되어 규제 준수 부담을 줄이고 신속한 차량 도입이 가능해졌습니다. 따라서 캠퍼스, 산업시설, 게이트형 커뮤니티 등에서의 도입이 확대되고 있습니다.

예측 기간 동안 퍼스널 모빌리티 차량이 가장 높은 성장률을 보일 것으로 예상됩니다.

도시 교통은 도심 및 저속 규제 구역에서 효율적으로 운영할 수 있는 소형, 저속 전기 모빌리티로 전환되고 있습니다. 인구 밀집 지역에서의 기존 차량에 대한 규제 강화와 저비용의 편리한 단거리 이동수단에 대한 수요 증가를 배경으로 일상적인 출퇴근 및 라스트 마일 연결에서 개인용 저속 차량의 채택이 가속화되고 있습니다. 또한, 일부 지역에서는 쿼드 재활용과 같은 경량 차량에 대한 면허 요건과 안전 기준이 완화되어 이 부문의 성장을 촉진하고 있습니다. 동시에 OEM은 운영 비용을 절감하고 아키텍처를 간소화한 전용 설계 차량 개발에 주력하고 있으며, 보다 광범위한 소비자층에 보급하고 도시 전기화 목표에 부합하도록 노력하고 있습니다. 2025년 10월 Club Car는 공도 주행이 가능한 저속 차량 'Onward'를 출시하여 근거리 이동 및 지역 내 이동을 위해 전개하고 있습니다.

예측 기간 동안 AC 모터가 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

AC 모터 시스템은 특히 캠퍼스 내 이동, 게이트가 있는 커뮤니티, 산업단지, 지자체 단거리 운송에서 넓은 운전 영역에서 높은 에너지 효율을 실현하고, 리튬이온 배터리 기반 플랫폼의 항속거리 연장 및 배터리 부하 감소에 기여합니다. DC 시스템에 비해 이 모터는 브러시 마모를 제거하여 유지보수 빈도를 줄이고 차량 가동률을 향상시킵니다. AC 시스템에서 회생제동 성능의 개선은 반복되는 제동 사이클 동안 에너지 회수를 더욱 향상시킵니다. 이는 저속으로 잦은 시동과 정지가 이루어지는 환경에서 중요합니다. 또한, 미국 연방 자동차 안전 표준 500(FMVSS 500)에 정의된 규제 대상 저속 차량 카테고리에서 OEM 업체들은 표준화된 전기 드라이브 트레인에 초점을 맞추고 있으며, 보다 효율적이고 전자적으로 제어 가능한 모터 아키텍처로의 전환을 촉진하고 있습니다. Yamaha Motor(자회사인 Yamaha Golf Car Company를 통해)는 'Drive2'와 'Umax' 시리즈 등의 AC 모터 모델을 전개하고 있습니다.

"유럽에서는 예측 기간 동안 괄목할 만한 성장이 예상됩니다."

경량 쿼드 재활용에 대한 규제 분류와 도시 모빌리티를 겨냥한 정책으로 인해 유럽 전역에서 저속 차량의 도입이 가속화되고 있습니다. 특히, EU가 정의한 L6e 및 L7e 카테고리에 따라 경량 전기자동차는 낮은 형식승인 요건, 최고 속도 제한, 간소화된 안전기준으로 운행할 수 있어 제조사와 사용자 모두 진입장벽을 낮출 수 있습니다. EU는 'Fit for 55' 패키지 등의 이니셔티브를 통해 지역 전체의 기후 및 교통 대책을 마련하고 있습니다. 여기에는 보다 엄격한 CO2 감축 목표가 포함되어 있으며, 무공해 모빌리티의 도입을 지원함으로써 도시에 적합한 소형 전기자동차에 대한 수요를 강화하고 있습니다. 영국, 프랑스, 독일 등 각 도시 당국은 저공해 구역과 출입 규제를 확대하고 있으며, 이를 통해 소형 전기자동차는 운영의 유연성을 높이고, 주차 용이성, 출입 제한 구역에 대한 접근성 등의 이점을 얻을 수 있습니다. 교통 체증 증가, 도시 밀집도 증가, 저비용 단거리 운송 및 라스트 마일 배송 솔루션에 대한 수요 증가는 저속 차량의 성능에 부합하는 소형 전기 모빌리티 형태로의 전환을 더욱 촉진하고 있습니다.

세계의 저속 차량 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 저속 차량 시장 : 차종별

제10장 저속 차량 시장 : 출력별

제11장 저속 차량 시장 : 배터리 유형별

제12장 저속 차량 시장 : 용도별

제13장 저속 차량 시장 : 추진 구분별

제14장 저속 차량 시장 : 카테고리별

제15장 저속 차량 시장 : 전압별

제16장 저속 차량 시장 : 모터 구성별

제17장 저속 차량 시장 : 모터 유형별

제18장 저속 차량 시장 : 지역별

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 부록

KSM 26.05.21The low-speed vehicle market is expected to reach USD 19.17 billion by 2035, from USD 11.87 billion in 2026, with a CAGR of 5.5%. The increasing adoption of low-speed vehicles in controlled environments is gaining momentum, as these vehicles operate outside the full homologation requirements applied to public road vehicles.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | USD Billion |

| Segments | By Vehicle Type, Power Output, Motor Type & Configuration, Propulsion, Battery Type, Application, Category, Voltage |

| Regions covered | Asia Pacific, Europe, North America, Rest of the World |

Regulatory frameworks from associations such as the National Highway Traffic Safety Administration, which classify low-speed vehicles under FMVSS 500 for limited-speed road use, have helped clearly separate low-speed vehicles from fully regulated passenger cars. This enables wider deployment across campuses, industrial sites, and gated communities with lower compliance burden and faster fleet integration.

Personal mobility vehicles are expected to grow at the fastest rate during the forecast period.

Urban transport patterns are shifting toward compact, low-speed electric solutions that can operate efficiently within city limits and in regulated low-speed zones. Increasing restrictions on conventional vehicles in dense urban areas, along with the need for affordable and convenient short-distance travel, are accelerating the adoption of personal low-speed vehicles for daily commuting and last-mile connectivity. Regulatory provisions in several regions that allow quadricycles and similar light vehicles to operate with relaxed licensing and safety requirements are further supporting this segment. At the same time, OEMs are focusing on purpose-built designs with lower operating costs and simplified architectures, making these vehicles more accessible to a wider consumer base while aligning with urban electrification goals. In October 2025, Club Car launched the Onward low-speed vehicle, built for street-legal driving, neighborhood travel, and short-distance journeys.

AC motors are expected to hold the largest market share during the forecast period.

AC motor systems deliver higher energy efficiency across operating ranges, especially for campus mobility, gated communities, industrial campuses, and municipal short-distance transport, helping extend the usable range and reduce battery stress in lithium-ion-based platforms. Compared with DC systems, these motors eliminate brush wear, reducing maintenance frequency and improving vehicle uptime. Improved regenerative braking performance in AC systems further enhances energy recovery during repetitive braking cycles, which is important in low-speed, high-stop-start environments. OEMs' focus on standardized electric drivetrains in regulated low-speed vehicle categories defined under US Federal Motor Vehicle Safety Standard 500 has also encouraged a shift toward more efficient, electronically controllable motor architectures. Yamaha Motor Co., Ltd. (through its subsidiary, Yamaha Golf Car Company) offers several AC motor models, including the Drive2 and Umax series.

"Europe is expected to grow at a significant rate during the forecast period."

Regulatory classification for light quadricycles and targeted urban mobility policies is accelerating low-speed vehicle adoption across Europe, particularly under the L6e and L7e categories defined by the European Union, which allow lightweight electric vehicles to operate with lower homologation requirements, capped speeds, and simplified safety norms, reducing entry barriers for both manufacturers and users. The European Commission has implemented region-wide climate and transport measures under initiatives such as the Fit for 55 package, which includes stricter CO2 reduction targets and supports the adoption of zero-emission mobility, thereby strengthening demand for compact electric vehicles suited for urban use. Authorities across cities such as the UK, France, and Germany have expanded low-emission zones and access control regulations that allow small electric vehicles greater operational flexibility, along with benefits such as easier parking and access to restricted areas. Increasing congestion, high urban density, and growing demand for low-cost, short-distance transport and last-mile delivery solutions are further driving the shift toward compact electric mobility formats that align with the capabilities of low-speed vehicles.

In-depth interviews were conducted with industry experts, including CXOs, vice presidents, and directors from business development, marketing, product development/innovation teams, and related executives from leading companies operating in this market.

- By Company Type: Low-speed Vehicle Manufacturers - 80% and Other Companies - 20%

- By Designation: Directors - 10%, Executives - 30%, and Others - 60%

- By Region: North America - 20%, Europe - 10%, Asia Pacific - 50%, and Others - 20%

The low-speed vehicle market is dominated by major players, including Textron Inc. (US), Yamaha Motor Co., Ltd. (Japan), Deere & Company (US), The Toro Company (US), and Kubota Corporation (Japan).

Research Coverage:

This research report categorizes the low-speed vehicle market by vehicle type (golf carts, commercial turf utility vehicles, industrial utility vehicles, personal mobility vehicles), power output (<5 kW, 5-8 kW, 9-15 kW, >15 kW), application, battery type, propulsion, category, voltage, motor configuration & type, and region. It covers the competitive landscape and profiles of the major players of the low-speed vehicle market. The study also includes an in-depth competitive analysis of the key market players, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall low-speed vehicle market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide insights into key drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (increasing adoption of low-speed vehicles in controlled-environment mobility where full homologation is not required, shift toward electric and lightweight platforms for short-range mobility, Growing popularity of golf), restraints (higher cost of low-speed vehicles compared to conventional utility vehicles, restricted road access due to speed limits and regulatory changes across regions), opportunities (growing use of low-speed vehicles in large-scale residential developments and private low-speed zones, integration of autonomous and connected technologies in low-speed vehicles), and challenges (substantial cost of batteries, competitive pressure from Chinese low-speed EV manufacturers)

- Product Development/Innovation: Detailed insights into upcoming technologies and R&D activities in the low-speed vehicle market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the low-speed vehicle market across varied regions)

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the low-speed vehicle market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players such as Textron Inc. (US), Yamaha Motor Co., Ltd. (Japan), Deere & Company (US), The Toro Company (US), and Kubota Corporation (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN LOW-SPEED VEHICLE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LOW-SPEED VEHICLE MARKET

- 3.2 LOW-SPEED VEHICLE MARKET, BY VEHICLE TYPE

- 3.3 LOW-SPEED VEHICLE MARKET, BY PROPULSION

- 3.4 LOW-SPEED VEHICLE MARKET, BY BATTERY TYPE

- 3.5 LOW-SPEED VEHICLE MARKET, BY APPLICATION

- 3.6 LOW-SPEED VEHICLE MARKET, BY POWER OUTPUT

- 3.7 LOW-SPEED VEHICLE MARKET, BY VOLTAGE

- 3.8 LOW-SPEED VEHICLE MARKET, BY CATEGORY

- 3.9 LOW-SPEED VEHICLE MARKET, BY MOTOR TYPE

- 3.10 LOW-SPEED VEHICLE MARKET, BY MOTOR CONFIGURATION

- 3.11 LOW-SPEED VEHICLE MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased adoption of low-speed vehicles in controlled environments

- 4.2.1.2 Shift toward electric and lightweight platforms for short-range mobility

- 4.2.2 RESTRAINTS

- 4.2.2.1 Higher cost of low-speed vehicles compared to conventional utility vehicles

- 4.2.2.2 Restricted road access due to speed limits and regulatory changes across regions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Extensive use of low-speed vehicles in large-scale residential developments and private low-speed zones

- 4.2.3.2 Integration of autonomous and connected technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Substantial cost of lithium-ion batteries

- 4.2.4.2 Competitive pressure from Chinese manufacturers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 SUPPLIERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN RECREATIONAL VEHICLE INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 LOW-SPEED VEHICLE MANUFACTURERS

- 5.2.2 DEALERS AND DISTRIBUTORS

- 5.2.3 PARTS AND COMPONENT MANUFACTURERS

- 5.2.4 CHARGING INFRASTRUCTURE PROVIDERS

- 5.2.5 FLEET OPERATORS

- 5.2.6 SOFTWARE AND FLEET MANAGEMENT PROVIDERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2026

- 5.4.2 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2026

- 5.4.3 AVERAGE SELLING PRICE, BY KEY PLAYER, 2026

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 870310)

- 5.8.2 EXPORT SCENARIO (HS CODE 870310)

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CLUB CAR ENHANCES FLEET ELECTRIFICATION

- 5.9.2 WAEV INC. EXPANDS STREET-LEGAL LOW-SPEED VEHICLE ADOPTION

- 5.9.3 TEXTRON INC. IMPROVES UTILITY VEHICLE EFFICIENCY

- 5.10 TOTAL COST OF OWNERSHIP

- 5.10.1 GASOLINE VS. ELECTRIC LOW-SPEED VEHICLES

- 5.10.2 COST-BENEFIT ANALYSIS

- 5.11 OEM ANALYSIS

- 5.11.1 VOLTAGE VS. SEATING OCCUPANCY OF LOW-SPEED VEHICLES

- 5.11.2 BATTERY CAPACITY VS. POWER OUTPUT OF QUADRICYCLES

- 5.11.3 BATTERY CAPACITY VS. POWER OUTPUT OF A00 VEHICLES

- 5.11.4 ENGINE CAPACITY VS. POWER OUTPUT OF KEI CARS

- 5.12 IMPACT OF EU-FTA TRADE DEAL ON RECREATIONAL VEHICLE INDUSTRY

- 5.13 IMPACT OF ISRAEL-IRAN WAR ON RECREATIONAL VEHICLE INDUSTRY

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 INTEGRATED MOTOR CONTROLLER UNITS

- 6.1.2 CAN/LIN-BASED VEHICLE ARCHITECTURE

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MODULAR EV PLATFORMS

- 6.2.2 DIGITAL INSTRUMENT CLUSTERS

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM ROADMAP

- 6.3.2 MID-TERM ROADMAP

- 6.3.3 LONG-TERM ROADMAP

- 6.4 IMPACT OF AI/GEN AI

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST PRACTICES

- 6.4.3 CASE STUDIES OF AI IMPLEMENTATION

- 6.4.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT AI/GEN AI

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES

9 LOW-SPEED VEHICLE MARKET, BY VEHICLE TYPE

- 9.1 INTRODUCTION

- 9.2 KEY LOW-SPEED VEHICLES, BY VEHICLE TYPE

- 9.3 GOLF CARTS

- 9.3.1 GROWING INTEREST IN GOLF TO DRIVE MARKET

- 9.4 COMMERCIAL TURF UTILITY VEHICLES

- 9.4.1 BOOMING TOURISM SECTOR TO DRIVE MARKET

- 9.5 INDUSTRIAL UTILITY VEHICLES

- 9.5.1 INCREASING CONSTRUCTION ACTIVITIES TO DRIVE MARKET

- 9.6 PERSONAL MOBILITY VEHICLES

- 9.6.1 RISING ACCEPTANCE OF STREET-LEGAL VEHICLES TO DRIVE MARKET

- 9.7 INDUSTRY INSIGHTS

10 LOW-SPEED VEHICLE MARKET, BY POWER OUTPUT

- 10.1 INTRODUCTION

- 10.2 <5 KW

- 10.2.1 HIGH DEMAND FOR LOW-POWER OUTPUT VEHICLES FROM NORTH AMERICA TO DRIVE MARKET

- 10.3 5-8 KW

- 10.3.1 FLEET STANDARDIZATION FOR LIGHT COMMERCIAL OPERATIONS TO DRIVE MARKET

- 10.4 9-15 KW

- 10.4.1 SHIFT TOWARD HIGHER PAYLOAD AND MULTI-PASSENGER UTILITY OPERATIONS TO DRIVE MARKET

- 10.5 >15 KW

- 10.5.1 LARGE-SCALE ADOPTION IN INDUSTRIAL FACILITIES TO DRIVE MARKET

- 10.6 INDUSTRY INSIGHTS

11 LOW-SPEED VEHICLE MARKET, BY BATTERY TYPE

- 11.1 INTRODUCTION

- 11.2 LITHIUM-ION BATTERIES

- 11.2.1 HIGHER RANGE AND EFFICIENCY TO DRIVE MARKET

- 11.3 LEAD-ACID BATTERIES

- 11.3.1 PERFORMANCE LIMITATIONS AND SHIFT TOWARD LITHIUM-ION ALTERNATIVES TO IMPEDE MARKET

- 11.4 INDUSTRY INSIGHTS

12 LOW-SPEED VEHICLE MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 GOLF COURSES

- 12.2.1 INCREASED PARTICIPATION IN GOLF TO DRIVE MARKET

- 12.3 HOTELS & RESORTS

- 12.3.1 SUBSTANTIAL INVESTMENTS IN HOSPITALITY INDUSTRY TO DRIVE MARKET

- 12.4 AIRPORTS

- 12.4.1 RISE IN PASSENGER AND CARGO TRAFFIC TO DRIVE MARKET

- 12.5 INDUSTRIAL FACILITIES

- 12.5.1 LOW MAINTENANCE COST OF LOW-SPEED VEHICLES TO DRIVE MARKET

- 12.6 OTHER APPLICATIONS

- 12.7 INDUSTRY INSIGHTS

13 LOW-SPEED VEHICLE MARKET, BY PROPULSION

- 13.1 INTRODUCTION

- 13.2 ELECTRIC

- 13.2.1 DEVELOPMENT OF ROBUST CHARGING INFRASTRUCTURE TO DRIVE MARKET

- 13.2.2 LOW SPEED VEHICLE MARKET, BY ELECTRIC VEHICLE TYPE

- 13.2.3 ELECTRIC GOLF CARTS

- 13.2.4 ELECTRIC COMMERCIAL TURF UTILITY VEHICLES

- 13.2.5 ELECTRIC INDUSTRIAL UTILITY VEHICLES

- 13.2.6 ELECTRIC PERSONAL MOBILITY VEHICLES

- 13.3 GASOLINE

- 13.3.1 HIGH POWER OUTPUT AND LOAD-CARRYING CAPACITY TO DRIVE MARKET

- 13.4 DIESEL

- 13.4.1 STRINGENT EMISSION NORMS TO IMPEDE MARKET

- 13.5 INDUSTRY INSIGHTS

14 LOW-SPEED VEHICLE MARKET, BY CATEGORY

- 14.1 INTRODUCTION

- 14.2 L7

- 14.2.1 INCREASING PREFERENCE FOR MICROCARS TO DRIVE MARKET

- 14.2.1.1 Asia Pacific

- 14.2.1.1.1 China

- 14.2.1.1.1.1 China: List of electric L7-e models

- 14.2.1.1.2 Japan

- 14.2.1.1.2.1 Japan: List of electric L7-e models

- 14.2.1.1.3 India

- 14.2.1.1.3.1 India: List of electric quadricycle models

- 14.2.1.1.4 South Korea

- 14.2.1.1.4.1 South Korea: List of electric L7-e models

- 14.2.1.1.1 China

- 14.2.1.2 Europe

- 14.2.1.2.1 Europe: List of electric L7-e models

- 14.2.1.3 North America

- 14.2.1.3.1 North America: List of electric L7-e models

- 14.2.1.1 Asia Pacific

- 14.2.1 INCREASING PREFERENCE FOR MICROCARS TO DRIVE MARKET

- 14.3 L6

- 14.3.1 INSTITUTIONAL AND RECREATIONAL USE CASES TO DRIVE MARKET

- 14.4 INDUSTRY INSIGHTS

15 LOW-SPEED VEHICLE MARKET, BY VOLTAGE

- 15.1 INTRODUCTION

- 15.2 <60V

- 15.2.1 ADEQUATE POWER AND COST ADVANTAGES TO DRIVE MARKET

- 15.3 61-100 V

- 15.3.1 WIDER RANGE AND HIGHER EFFICIENCY TO DRIVE MARKET

- 15.4 >100V

- 15.4.1 NEED FOR ROBUST PERFORMANCE IN RUGGED TERRAIN TO DRIVE MARKET

- 15.5 INDUSTRY INSIGHTS

16 LOW-SPEED VEHICLE MARKET, BY MOTOR CONFIGURATION

- 16.1 INTRODUCTION

- 16.2 HUB-MOUNTED

- 16.2.1 SURGE IN DEMAND FOR SUSTAINABLE TRANSPORTATION SOLUTIONS TO DRIVE MARKET

- 16.3 MID-MOUNTED

- 16.3.1 ONGOING ELECTRIFICATION TREND TO DRIVE MARKET

- 16.4 INDUSTRY INSIGHTS

17 LOW-SPEED VEHICLE MARKET, BY MOTOR TYPE

- 17.1 INTRODUCTION

- 17.2 AC MOTORS

- 17.2.1 HIGHER EFFICIENCY AND SIMPLER DESIGN TO DRIVE MARKET

- 17.3 DC MOTORS

- 17.3.1 LOWER LIFECYCLE COST AND REDUCED MAINTENANCE OF AC MOTORS TO IMPEDE MARKET

- 17.4 INDUSTRY INSIGHTS

18 LOW-SPEED VEHICLE MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 ASIA PACIFIC

- 18.2.1 CHINA

- 18.2.1.1 Increasing adoption of low-speed vehicles in industrial facilities to drive market

- 18.2.2 INDIA

- 18.2.2.1 Extensive use in industrial and tourism sectors to drive market

- 18.2.3 JAPAN

- 18.2.3.1 Rapid industrial development to drive market

- 18.2.4 SOUTH KOREA

- 18.2.4.1 Expanding tourism and increasing preference for golf to drive market

- 18.2.5 THAILAND

- 18.2.5.1 Availability of affordable golfing options to drive market

- 18.2.6 INDONESIA

- 18.2.6.1 Rising tourist activities to drive market

- 18.2.7 VIETNAM

- 18.2.7.1 Upcoming golf events to drive market

- 18.2.8 PHILIPPINES

- 18.2.8.1 Growing golfers community to drive market

- 18.2.1 CHINA

- 18.3 NORTH AMERICA

- 18.3.1 US

- 18.3.1.1 Stringent vehicle emission standards to drive market

- 18.3.2 MEXICO

- 18.3.2.1 High demand from hospitality industry to drive market

- 18.3.3 CANADA

- 18.3.3.1 Rising golfing activities to drive market

- 18.3.1 US

- 18.4 EUROPE

- 18.4.1 UK

- 18.4.1.1 High mobility needs amid escalating tourism activity to drive market

- 18.4.2 FRANCE

- 18.4.2.1 Growing popularity of golf to drive market

- 18.4.3 GERMANY

- 18.4.3.1 Increasing golf activities to drive market

- 18.4.4 NORDIC

- 18.4.4.1 Focus on green and zero-emission mobility to drive market

- 18.4.5 ITALY

- 18.4.5.1 High demand for commercial utility vehicles at hotels and resorts to drive market

- 18.4.6 SPAIN

- 18.4.6.1 Trend of golf holidays to drive market

- 18.4.1 UK

- 18.5 REST OF THE WORLD

- 18.5.1 SOUTH AFRICA

- 18.5.1.1 Surge in demand for personal mobility vehicles to drive market

- 18.5.2 BRAZIL

- 18.5.2.1 Presence of world-class golf courses to drive market

- 18.5.3 IRAN

- 18.5.3.1 Significant demand from tourism sector to drive market

- 18.5.1 SOUTH AFRICA

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 19.3 MARKET SHARE ANALYSIS, 2025

- 19.4 REVENUE ANALYSIS, 2021-2025

- 19.5 COMPANY VALUATION AND FINANCIAL METRICS

- 19.6 BRAND/PRODUCT COMPARISON

- 19.7 COMPANY EVALUATION MATRIX: LOW-SPEED VEHICLE SUPPLIERS, 2025

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT: LOW-SPEED VEHICLE SUPPLIERS, 2025

- 19.7.5.1 Company footprint

- 19.7.5.2 Region footprint

- 19.7.5.3 Application footprint

- 19.7.5.4 Propulsion footprint

- 19.7.5.5 Vehicle type footprint

- 19.8 COMPANY EVALUATION MATRIX: GOLF CART MANUFACTURERS, 2025

- 19.8.1 STARS

- 19.8.2 EMERGING LEADERS

- 19.8.3 PERVASIVE PLAYERS

- 19.8.4 PARTICIPANTS

- 19.8.5 COMPANY FOOTPRINT: GOLF CART MANUFACTURERS, 2025

- 19.8.5.1 Company footprint

- 19.8.5.2 Region footprint

- 19.8.5.3 Product type footprint

- 19.8.5.4 Application footprint

- 19.8.5.5 Vehicle type footprint

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 19.9.2 DEALS

- 19.9.3 EXPANSIONS

- 19.9.4 OTHERS

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- 20.1.1 TEXTRON INC.

- 20.1.1.1 Business overview

- 20.1.1.2 Products offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches/developments

- 20.1.1.3.2 Deals

- 20.1.1.3.3 Others

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses and competitive threats

- 20.1.2 DEERE & COMPANY

- 20.1.2.1 Business overview

- 20.1.2.2 Products offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Product launches/developments

- 20.1.2.3.2 Deals

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses and competitive threats

- 20.1.3 YAMAHA MOTOR CO., LTD.

- 20.1.3.1 Business overview

- 20.1.3.2 Products offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Product launches/developments

- 20.1.3.3.2 Deals

- 20.1.3.3.3 Others

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses and competitive threats

- 20.1.4 THE TORO COMPANY

- 20.1.4.1 Business overview

- 20.1.4.2 Products offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Product launches/developments

- 20.1.4.3.2 Deals

- 20.1.4.3.3 Others

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses and competitive threats

- 20.1.5 KUBOTA CORPORATION

- 20.1.5.1 Business overview

- 20.1.5.2 Products offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Product launches/developments

- 20.1.5.3.2 Deals

- 20.1.5.3.3 Expansions

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses and competitive threats

- 20.1.6 CLUB CAR

- 20.1.6.1 Business overview

- 20.1.6.2 Products offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 Product launches/developments

- 20.1.6.3.2 Deals

- 20.1.6.3.3 Expansions

- 20.1.6.3.4 Others

- 20.1.7 AMERICAN LANDMASTER

- 20.1.7.1 Business overview

- 20.1.7.2 Products offered

- 20.1.7.3 Recent developments

- 20.1.7.3.1 Product launches/developments

- 20.1.7.3.2 Deals

- 20.1.8 COLUMBIA VEHICLE GROUP INC.

- 20.1.8.1 Business overview

- 20.1.8.2 Products offered

- 20.1.8.3 Recent developments

- 20.1.8.3.1 Product launches/developments

- 20.1.8.3.2 Deals

- 20.1.9 WAEV INC.

- 20.1.9.1 Business overview

- 20.1.9.2 Products offered

- 20.1.9.3 Recent developments

- 20.1.9.3.1 Product launches/developments

- 20.1.9.3.2 Deals

- 20.1.9.3.3 Others

- 20.1.10 SUZHOU EAGLE ELECTRIC VEHICLE MANUFACTURING CO., LTD.

- 20.1.10.1 Business overview

- 20.1.10.2 Products offered

- 20.1.1 TEXTRON INC.

- 20.2 OTHER PLAYERS

- 20.2.1 AGT ELECTRIC CARS

- 20.2.2 BINTELLI ELECTRIC VEHICLES

- 20.2.3 MARSHELL GREEN POWER

- 20.2.4 ICON ELECTRIC VEHICLES

- 20.2.5 STAR EV CORPORATION

- 20.2.6 HDK ELECTRIC VEHICLE

- 20.2.7 TROPOS MOTORS, INC.

- 20.2.8 PILOTCAR

- 20.2.9 MOTO ELECTRIC VEHICLES

- 20.2.10 ACG INC.

- 20.2.11 CITECAR ELECTRIC VEHICLES

- 20.2.12 CRUISE CAR INC.

- 20.2.13 LIGIER GROUP

- 20.2.14 SPEEDWAYS ELECTRIC

- 20.2.15 DINIS

- 20.2.16 AUTOPOWER

- 20.2.17 DONGGUAN EXCAR ELECTRIC VEHICLE CO., LTD.

- 20.2.18 HAWK CARTS PTY LTD

- 20.2.19 AETRIC ELECTRIC VEHICLES

- 20.2.20 EV TITAN LLC

- 20.2.21 ENVY NEIGHBOURHOOD VEHICLE

- 20.2.22 VARLEY ELECTRIC VEHICLES PTY LIMITED

- 20.2.23 MAINI MATERIALS MOVEMENT PVT. LTD.

- 20.2.24 EVOLUTION ELECTRIC VEHICLES

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.1.1 Secondary sources

- 21.1.1.2 Key data from secondary sources

- 21.1.2 PRIMARY DATA

- 21.1.2.1 Primary interview participants

- 21.1.2.2 Breakdown of primary interviews

- 21.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 21.1.1 SECONDARY DATA

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.2 TOP-DOWN APPROACH

- 21.3 DATA TRIANGULATION

- 21.4 RESEARCH ASSUMPTIONS

- 21.5 RESEARCH LIMITATIONS

- 21.6 RISK ASSESSMENT

22 APPENDIX

- 22.1 INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.4.1 LOW-SPEED VEHICLE MARKET, BY MAX SPEED

- 22.4.1.1 Up to 10 mph

- 22.4.1.2 11-15 mph

- 22.4.1.3 16-20 mph

- 22.4.1.4 21-25 mph

- 22.4.2 LOW-SPEED VEHICLE MARKET, BY SEATING CAPACITY

- 22.4.2.1 2-seater

- 22.4.2.2 4-seater

- 22.4.2.3 6-seater

- 22.4.2.4 8-seater

- 22.4.1 LOW-SPEED VEHICLE MARKET, BY MAX SPEED

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS