|

시장보고서

상품코드

2029868

디지털 바이오마커 시장 예측(-2031년) : 유형별, 치료 분야별, 용도별, 최종사용자별, 지역별Digital Biomarkers Market by Type (Physiological, Vocal, Idiosyncratic), Therapy, Application, End User (Pharma & Biotech Companies, CROs) - Global Forecast to 2031 |

||||||

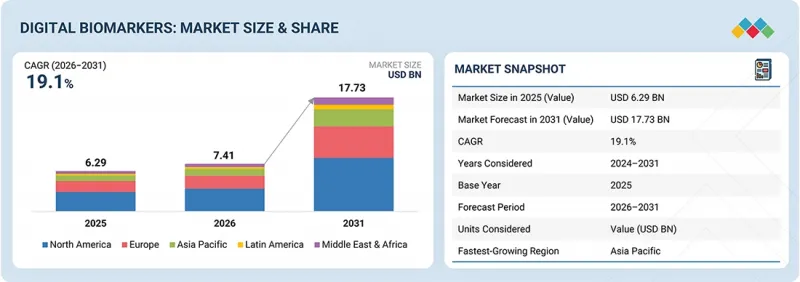

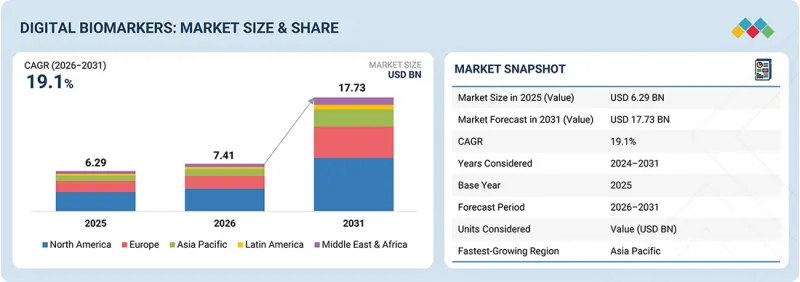

세계의 디지털 바이오마커 시장 규모는 2026년 74억 1,000만 달러에서 CAGR 19.1%로 확대하며, 2031년까지 177억 3,000만 달러에 달할 것으로 예측됩니다.

디지털 바이오마커 시장은 데이터베이스 임상시험의 급속한 발전과 디지털 헬스 기술을 임상시험에 통합하는 추세에 힘입어 성장하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 치료 분야별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

제약회사와 생명공학 기업은 임상 시험의 다양한 단계에서 디지털 바이오마커를 점점 더 많이 활용하고 있으며, 이를 통해 지속적이고 객관적인 환자 모니터링을 가능하게 함으로써 데이터의 품질과 엔드포인트의 정확성을 향상시키고 있습니다. 이는 보다 효율적이고 환자 중심의 임상시험을 지향하는 큰 흐름의 일부이며, 이 과정에서 실제 데이터는 약물의 효능을 판단하는 데 있으며, 매우 중요한 역할을 하고 있습니다. 동시에 웨어러블 기기, 센서 기술 등 원격 데이터 수집 기술을 활용하여 보다 빈번하게 데이터를 수집하는 분산형 임상시험으로 전환하는 추세도 증가하고 있습니다. 이는 임상 시험에서 디지털 바이오마커 소프트웨어 기술의 보급이라는 더 큰 흐름의 일부입니다.

"유형별로는 예측 기간 중 생리적 바이오마커 부문이 디지털 바이오마커 시장에서 가장 큰 시장점유율을 차지할 것으로 예상됩니다. "

유형별로는 예측 기간 중 생리적 바이오마커 부문이 디지털 바이오마커 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이는 주로 심박수, 심전도(ECG), 호흡수, 활동량 등 지속적인 생리적 측정값이 다양한 임상 조사 및 환자 치료 현장에서 널리 활용되고 있기 때문입니다. 생리적 바이오마커는 확장성이 높고 충분히 검증되어 원격 환자 모니터링 및 만성질환 관리에 적합합니다. 또한 웨어러블 기기 관련 소프트웨어 플랫폼과 AI 기반 툴을 활용하는 경향이 높아지면서 웨어러블 기기 도입이 더욱 활발해지고 있습니다. 특히 임상적 판단에 있으며, 지속적인 모니터링이 필수적인 심혈관계 질환이나 대사성 질환 분야에서 두드러집니다. 이는 심박수 및 활동 수준과 같은 생리적 데이터 스트림이 임상 시험에서 가장 일반적으로 사용되는 디지털 엔드포인트 중 하나이며, 이는 주로 객관성과 고빈도 및 실제 데이터를 제공할 수 있는 능력으로 인해 임상 시험에서 가장 일반적으로 사용되는 디지털 엔드포인트 중 하나라는 발표된 연구 결과에서도 알 수 있습니다. 또한 분산형 임상 시험 및 RWE(Real World Data) 생성으로의 전환은 기존 임상 환경 밖에서 환자 모니터링을 가능하게 함으로써 디지털 바이오마커 분야에서의 입지를 더욱 공고히 하고 있습니다.

2025년 6월, AliveCor, Inc.(미국)는 영국 심장 재단(UK)과 제휴하여 자사의 KardiaMobile 6L 장치 판매의 일부를 기부하여 심혈관 연구를 지원하고 디지털 심박수 모니터링 기술의 보급을 촉진했습니다. 이러한 사례는 심장 의료 및 연구 발전에서 생리적 디지털 바이오마커의 역할이 확대되고 있음을 시사합니다.

"최종사용자별로 보면 예측 기간 중 병원 및 전문 클리닉 부문이 가장 빠른 성장세를 보일 것으로 예상됩니다. "

최종사용자별로는 예측 기간 중 병원 및 전문 클리닉 부문이 디지털 바이오마커 시장에서 가장 높은 성장률을 기록할 것으로 예상됩니다. 이 부문의 성장은 실시간 환자 모니터링을 위한 병원 및 전문 클리닉의 디지털 바이오마커 채택 확대에 기인합니다. 디지털 바이오마커는 데이터베이스 의사결정을 위해 병원과 전문 클리닉의 워크플로우에 점점 더 많이 통합되고 있습니다. 병원 및 전문 클리닉에서는 환자의 생리적, 인지적, 행동적 변화를 지속적으로 모니터링하기 위해 웨어러블 지원 플랫폼과 인공지능(AI) 기반 분석 솔루션을 도입하고 있습니다. 디지털 바이오마커는 병원이나 전문 클리닉이 환자 데이터를 실시간으로 지속적으로 모니터링하여 환자의 건강 상태 변화를 조기에 감지할 수 있도록 돕습니다. 또한 가치 기반 의료(Value-Based Care)의 확산 추세는 병원 및 전문 클리닉의 원격 모니터링 솔루션 도입을 촉진하고 있습니다. 심혈관질환, 신경질환, 당뇨병 등 만성질환의 유병률 증가도 병원 및 전문 클리닉의 디지털 바이오마커 시장 성장에 기여하고 있습니다. 디지털 바이오마커 솔루션을 전자건강기록(EHR)에 원활하게 통합할 수 있는 헬스케어 정보기술의 보급 추세도 병원 및 전문 클리닉의 디지털 바이오마커 시장 성장을 촉진하고 있습니다.

"아시아태평양은 예측 기간 중 가장 높은 성장률을 기록할 것으로 보입니다. "

아시아태평양의 디지털 바이오마커 시장은 빠르게 성장하고 있으며, 아시아태평양의 임상 연구 활동의 확대가 두드러진 성장세를 보이고 있습니다. 이 지역에서는 의료 인프라에 디지털 기술 도입이 진행되고 있습니다. 인도, 한국, 일본, 호주 등의 국가들은 임상연구 활동의 거점으로서 그 중요성이 커지고 있습니다. 규제 환경의 개선과 비용적 이점으로 인해 제약 및 생명공학 산업은 아시아태평양을 임상 연구 활동의 거점으로 점점 더 많이 활용하고 있습니다. 제약 및 생명공학 산업이 임상 연구 활동을 수행함에 있으며, 디지털 기술에 대한 의존도가 높아짐에 따라 디지털 바이오마커 시장은 빠르게 성장하고 있습니다.

아시아태평양에서는 의료 인프라에 디지털 기술이 도입되고 있습니다. 이 지역에서는 임상 연구 활동이 확대되고 있습니다. 2025년 11월, 한국에 본사를 둔 Lunit Inc.는 Labcorp와의 제휴를 발표했습니다. 이는 인공지능을 활용한 디지털 병리 기술을 활용한 연구를 수행하고, 임상 및 중개 종양학 연구에서 이미지 기반 바이오마커에 대한 접근성을 전 세계에서 확대하는 것을 목표로 하고 있습니다. 이러한 추세는 이 지역이 디지털 바이오마커의 유망한 시장이 될 수 있음을 보여줍니다.

IXICO PLC(영국), Ametris, LLC(미국), Empatica, Inc.(미국)는 디지털 바이오마커 시장의 주요 기업 중 일부입니다. 이 보고서에서는 이들 주요 기업에 대한 상세한 경쟁 분석, 기업 개요, 최근 동향, 주요 시장 전략에 대해 조사했습니다.

조사 범위:

디지털 바이오마커 시장을 유형별(생리적 바이오마커, 특이적 바이오마커, 인지 바이오마커, 음성 바이오마커, 기타 바이오마커), 치료 분야별(심혈관계[죽상동맥경화성 심혈관질환(ASCVD)/이차 예방, 심부전(심부전, 심근경색, 심방세동, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심근경색, 심부전 HFrEF 및 HFpEF), 고혈압, 심방세동(AF)/뇌졸중 예방, 폐고혈압, 구조적 심장질환/중재적 심장학], 종양학(고형종양, 혈액암), 당뇨병, 정신건강 및 행동건강, 호흡기 질환, 생활습관 및 웰빙 개선, 신경학, 근골격계 신경학, 근골격계 질환/통증 관리, 여성 건강 및 생식 건강, 기타 질환), 용도, [임상연구용(임상 II상, 임상 III상, 임상 IV상) 및 임상 치료용], 최종사용자[제약 및 생명공학 기업, CRO, 병원 및 전문 클리닉, 기타(연구기관 등)] 및 지역 사회 기관 등)], 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)으로 나뉜다.

이 보고서의 범위에는 디지털 바이오마커 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 솔루션 및 서비스, 계약, 파트너십, 합의, 제품 및 서비스 출시, 인수합병, 디지털 바이오마커 시장과 관련된 최근 동향에 대한 인사이트를 제공합니다. 이 보고서에서는 디지털 바이오마커 시장 생태계의 신흥 스타트업 기업의 경쟁 분석도 함께 다루고 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 디지털 바이오마커 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 도전 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(스마트폰, 웨어러블 기기, 커넥티드 헬스 생태계 확대, 분산형 및 원격 임상시험 확대, 지속적인 모니터링이 필요한 만성질환 유병률 증가, AI 및 디지털 헬스 분석의 발전) 억제요인(건강 데이터 관련 데이터 프라이버시 및 보안 문제, 환자의 디지털 리터러시 및 기술 접근성 제한, 디지털 바이오마커 활용 확대, 정밀 의료 및 신약 개발 엔드포인트의 한계) 데이터 프라이버시 및 보안 문제, 환자의 디지털 리터러시 및 기술 접근성 제한), 기회 요인(신약 개발 및 임상 시험의 엔드포인트에서 디지털 바이오마커 활용 확대, 정밀의료 및 개인 맞춤형 헬스케어의 성장, 신경 및 정신건강 신경학 및 정신건강 모니터링의 새로운 응용), 과제(디지털 바이오마커에 대한 표준화된 검증 프레임워크 부족, 디지털 엔드포인트 및 바이오마커 검증에 대한 규제 불확실성)가 디지털 바이오마커 시장의 성장에 영향을 미치고 있습니다. 영향을 미치고 있습니다.

- 제품 개발 및 혁신: 디지털 바이오마커 시장의 미래 기술, R&D 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발: 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화: 디지털 바이오마커 시장의 신제품 및 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보 제공

- 경쟁사 분석: IXICO PLC(영국), Ametris, LLC(미국), Empatica, Inc. Lunit, Inc.(한국) 등 디지털 바이오마커 시장 주요 기업의 시장점유율, 성장전략, 서비스 제공내용에 대한 상세 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 규제 상황

제8장 기술, 특허, AI 도입에 의한 전략적 파괴

제9장 디지털 바이오마커 시장(유형별)

제10장 디지털 바이오마커 시장(치료 분야별)

제11장 디지털 바이오마커 시장(용도별)

제12장 디지털 바이오마커 시장(최종사용자별)

제13장 디지털 바이오마커 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.05.21The global digital biomarkers market is projected to reach USD 17.73 billion by 2031, growing from USD 7.41 billion in 2026 at a CAGR of 19.1%. The digital biomarkers market is being driven by the rapid evolution of data-driven clinical trials and the growing trend of integrating digital health technology into clinical trials.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Therapeutic Area, Application, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Pharmaceutical and biotech companies are increasingly using digital biomarkers in various stages of clinical trials to enable continuous and objective patient monitoring, thus improving data quality and endpoint accuracy. This is a part of a larger trend towards more efficient and patient-centric clinical trials, in which data from real-world sources plays a crucial role in determining the effectiveness of a drug. At the same time, there is a growing trend toward more decentralized clinical trials, in which data is collected more frequently by using remote data collection technology such as wearable devices and sensor technology. This is a part of a larger trend towards more digital biomarker software technology in clinical trials.

"By type, the physiological biomarkers segment is expected to account for the largest market share of the digital biomarkers market during the forecast period."

By type, the physiological biomarkers segment is expected to hold the largest share of the digital biomarkers market during the forecast period. This is mainly due to the widespread use of continuous physiological measures like heart rate, ECG, respiratory rate, and activity levels in various clinical research and patient care settings. Physiological biomarkers are scalable and are well validated, making them more suitable for remote patient monitoring and chronic disease management. In addition, the growing trend of using software platforms and AI-based tools associated with wearable devices is further propelling their adoption, particularly in cardiovascular and metabolic conditions where continuous monitoring is critical in making clinical decisions. This is also evident from published research that states that physiological data streams like heart rate and activity levels are some of the most commonly used digital endpoints in clinical trials, mainly due to their objectivity and ability to provide high-frequency and real-world data. In addition, the move towards decentralized trials and RWE generation is also further solidifying their position in the field of digital biomarkers, as they allow for patient monitoring outside traditional clinical environments.

In June 2025, AliveCor, Inc. (US) partnered with the British Heart Foundation (UK), donating proceeds from its KardiaMobile 6L device to support cardiovascular research and promote the adoption of digital heart rhythm monitoring technologies. These examples further hint at the growing role of physiological digital biomarkers in advancing cardiac care and research.

"By end user, the hospitals & specialty clinics segment is expected to achieve the fastest growth during the forecast period."

By end user, the hospitals & specialty clinics segment is expected to witness the highest growth in the digital biomarkers market over the forecast period. The growth in this segment can be attributed to the rising adoption of digital biomarkers in hospitals and specialty clinics for real-time patient monitoring. Digital biomarkers are being increasingly integrated into the workflows of hospitals and specialty clinics for data-driven decision-making. Hospitals and specialty clinics are adopting wearable-enabled platforms and artificial intelligence-based analytics solutions for continuously monitoring physiological, cognitive, and behavioral changes in patients. Digital biomarkers help hospitals and specialty clinics in continuously monitoring patient data in real-time, thus helping in the early detection of changes in patient health. Moreover, the rising trend of value-based care is fueling the adoption of remote monitoring solutions in hospitals and specialty clinics. The rising prevalence of chronic diseases such as cardiovascular diseases, neurological disorders, and diabetes is also contributing to the growth of the digital biomarkers market in hospitals and specialty clinics. The rising trend of health information technology, which allows for seamless integration of digital biomarker solutions into electronic health records, is also fueling the growth of the digital biomarkers market in hospitals and specialty clinics.

"Asia Pacific to witness the highest growth rate during the forecast period."

The digital biomarkers market in Asia Pacific is growing rapidly, with the region witnessing high growth in the expansion of clinical research activities. The region is witnessing the incorporation of digital technologies into the healthcare infrastructure. Countries such as India, South Korea, Japan, and Australia are gaining importance as hubs for clinical research activities. Due to the improvement in the regulatory environment and the cost advantage, the pharmaceutical and biotech industries are increasingly using the Asia Pacific as a hub for conducting clinical research activities. As the pharmaceutical and biotech industries increasingly rely on digital technologies to conduct clinical research activities, the digital biomarkers market is growing rapidly.

Asia Pacific is witnessing the incorporation of digital technologies into the healthcare infrastructure. The region is witnessing the expansion of clinical research activities. In November 2025, Lunit Inc., a South Korean-based company, announced its collaboration with Labcorp to conduct research using digital pathology technology powered by artificial intelligence and expand access to imaging-based biomarkers for clinical and translational oncology research globally. Such developments indicate the potential of the region as a lucrative market for digital biomarkers.

The breakdown of primary participants is as follows:

- By Company Type - Tier 1 Companies: 60%, Tier 2 Companies: 30%, and Tier 3 Companies: 10%

- By Designation - C-level Executives: 30%, Director-level Personnel: 50%, and Other Designations: 20%

- By Region - North America: 45%, Europe: 20%, Asia Pacific: 25%, Rest of the world: 10%

IXICO PLC (UK), Ametris, LLC (US), and Empatica, Inc. (US) are some of the key players in the digital biomarkers market. The study includes an in-depth competitive analysis of these key players, their company profiles, recent developments, and key market strategies.

Research Coverage:

This research report categorizes the digital biomarkers market by type (physiological biomarkers, idiosyncratic biomarkers, cognitive biomarkers, vocal biomarkers, and other biomarkers), therapeutic area {cardiovascular [atherosclerotic cardiovascular disease (ASCVD)/secondary prevention, heart failure (HFrEF and HFpEF), hypertension, atrial fibrillation (AF)/stroke prevention, pulmonary hypertension, and structural heart disease/interventional cardiology], oncology (solid tumors, hematologic malignancies), diabetes, mental health & behavioral health, respiratory disorders, lifestyle & wellness improvement, neurology, musculoskeletal disorders/pain management, women's health & reproductive health, and other diseases}, application, [clinical research applications (phase II, phase III, phase IV) and clinical care applications], end user [pharmaceutical and biotechnology companies, contract research organizations (CROs), hospitals and specialty clinics, and others (including research institutes, etc.)] and region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the digital biomarkers market. A detailed analysis of the key industry players has been done to provide insights into their business overview; solutions and services; contracts, partnerships, agreements, product & service launches, mergers & acquisitions; and recent developments associated with the digital biomarkers market. Competitive analysis of upcoming startups in the digital biomarkers market ecosystem is covered in this report.

Reasons to Buy this Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the digital biomarkers market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Expansion of smartphones, wearables, and connected health ecosystems; expansion of decentralized and remote clinical trials; rising prevalence of chronic diseases requiring continuous monitoring; advancements in AI and digital health analytics) restraints (Data privacy and security concerns related to health data, limited digital literacy and technology access among patients) opportunities (Increasing use of digital biomarkers in drug development and clinical trial endpoints, growth of precision medicine and personalized healthcare, emerging applications in neurological and mental health monitoring), challenges (Lack of standardized validation frameworks for digital biomarkers, regulatory uncertainty around digital endpoints and biomarker validation) influencing the growth of the digital biomarkers market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the digital biomarkers market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the digital biomarkers market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players, namely IXICO PLC (UK), Ametris, LLC (US), Empatica, Inc. (US), AliveCor, Inc. (US), CONNEQT Health (US), VivoSense (US), BioSensics (US), Lunit, Inc. (South Korea), among others, in the digital biomarkers market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DIGITAL BIOMARKERS MARKET OVERVIEW

- 3.2 DIGITAL BIOMARKERS MARKET, BY APPLICATION & REGION

- 3.3 DIGITAL BIOMARKERS MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Expansion of smartphones, wearables, and connected health ecosystems

- 4.2.1.2 Expansion of decentralized and remote clinical trials

- 4.2.1.3 Rising prevalence of chronic diseases that require continuous monitoring

- 4.2.1.4 Advancements in AI and digital health analytics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Data privacy and cybersecurity concerns

- 4.2.2.2 Limited digital literacy and technology access among patients

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing use in drug development and clinical trial endpoints

- 4.2.3.2 Growth of precision medicine and personalized healthcare

- 4.2.3.3 Emerging applications in neurological and mental health monitoring

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of standardized validation frameworks for digital biomarkers

- 4.2.4.2 Regulatory uncertainty around digital endpoints and biomarker validation

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS (MODERATE)

- 5.1.2 BARGAINING POWER OF BUYERS (HIGH)

- 5.1.3 THREAT OF SUBSTITUTES (MODERATE TO HIGH)

- 5.1.4 THREAT OF NEW ENTRANTS (MODERATE)

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY (HIGH)

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR DIGITAL BIOMARKERS, BY KEY PLAYER (2025)

- 5.5.2 INDICATIVE PRICE FOR DIGITAL BIOMARKERS, BY REGION (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF ON DIGITAL BIOMARKERS MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END USERS

- 5.10.5.1 Pharmaceutical and biotechnology companies

- 5.10.5.2 Contract research organizations

- 5.10.5.3 Hospitals and specialty clinics

- 5.10.5.4 Others (research institutes, etc.)

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 INTRODUCTION

- 6.2 DECISION-MAKING PROCESS

- 6.3 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.3.2 BUYING CRITERIA

- 6.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 6.5.1 UNMET NEEDS

- 6.5.2 END USER EXPECTATIONS

- 6.6 MARKET PROFITABILITY

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, & OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, AND AI ADOPTION

- 8.1 KEY EMERGING TECHNOLOGIES

- 8.1.1 WEARABLE SENSOR TECHNOLOGIES

- 8.1.2 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING ANALYTICS

- 8.1.3 MOBILE HEALTH (MHEALTH) PLATFORMS AND SMARTPHONE SENSORS

- 8.2 COMPLEMENTARY TECHNOLOGIES

- 8.2.1 INTERNET OF MEDICAL THINGS (IOMT)

- 8.2.2 TELEHEALTH AND REMOTE PATIENT MONITORING

- 8.3 ADJACENT TECHNOLOGIES

- 8.3.1 DIGITAL THERAPEUTICS

- 8.3.2 DIGITAL PATHOLOGY AND IMAGING AI

- 8.4 TECHNOLOGY/PRODUCT ROADMAP

- 8.5 PATENT ANALYSIS

- 8.5.1 PATENT PUBLICATION TRENDS IN DIGITAL BIOMARKERS MARKET

- 8.5.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 8.6 FUTURE APPLICATIONS

- 8.6.1 AI-ENABLED INTELLIGENT SCREENING AND INTERPRETATION

- 8.6.2 CONTINUOUS AND PREDICTIVE HEALTH MONITORING APPLICATIONS

- 8.6.3 DECENTRALIZED, REMOTE, AND REAL-WORLD DATA ECOSYSTEMS

- 8.7 IMPACT OF AI/GEN AI ON DIGITAL BIOMARKERS MARKET

- 8.7.1 INTRODUCTION

- 8.7.2 MARKET POTENTIAL OF AI/GEN AI IN DIGITAL BIOMARKERS MARKET

- 8.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 8.7.3.1 Early Alzheimer's detection using mobile-based cognitive assessment platforms

- 8.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 8.7.4.1 Digital health market

- 8.7.4.2 Remote patient monitoring market

- 8.7.4.3 Telehealth & telemedicine market

- 8.7.5 USER READINESS AND IMPACT ASSESSMENT

- 8.7.5.1 User readiness

- 8.7.5.1.1 User A: Pharmaceutical & biotechnology companies

- 8.7.5.1.2 User B: Contract research organizations (CROs)

- 8.7.5.2 Impact assessment

- 8.7.5.2.1 User A: Pharmaceutical & biotechnology companies

- 8.7.5.2.1.1 Implementation

- 8.7.5.2.1.2 Impact

- 8.7.5.2.2 User B: Contract research organizations

- 8.7.5.2.2.1 Implementation

- 8.7.5.2.2.2 Impact

- 8.7.5.2.1 User A: Pharmaceutical & biotechnology companies

- 8.7.5.1 User readiness

9 DIGITAL BIOMARKERS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 PHYSIOLOGICAL BIOMARKERS

- 9.2.1 SEGMENT LEADS MARKET ADOPTION THROUGH CLINICAL VALIDATION AND AI-DRIVEN ANALYTICS

- 9.3 IDIOSYNCRATIC BIOMARKERS

- 9.3.1 PRECISION MEDICINE DRIVEN THROUGH PERSONALIZED, INDIVIDUAL-LEVEL DATA INSIGHTS

- 9.4 COGNITIVE BIOMARKERS

- 9.4.1 ENABLE SCALABLE AND OBJECTIVE MEASUREMENT OF NEUROLOGICAL FUNCTION THROUGH ADVANCED ANALYTICS

- 9.5 VOCAL BIOMARKERS

- 9.5.1 AI-POWERED VOICE ANALYSIS ENABLES SCALABLE MENTAL HEALTH MONITORING

- 9.6 OTHER BIOMARKERS

10 DIGITAL BIOMARKERS MARKET, BY THERAPEUTIC AREA

- 10.1 INTRODUCTION

- 10.2 CARDIOVASCULAR

- 10.2.1 ATHEROSCLEROTIC CARDIOVASCULAR DISEASE/SECONDARY PREVENTION

- 10.2.1.1 Continuous risk monitoring and predictive insights in cardiovascular disease management - key driver

- 10.2.2 HEART FAILURE (HFREF & HFPEF)

- 10.2.2.1 Demand driven by advanced early detection and remote monitoring in heart failure management

- 10.2.3 HYPERTENSION

- 10.2.3.1 Transforming blood pressure assessment from episodic to continuous monitoring

- 10.2.4 ATRIAL FIBRILLATION/STROKE PREVENTION

- 10.2.4.1 Unlocking subclinical AF identification via long-duration rhythm analytics

- 10.2.5 PULMONARY HYPERTENSION

- 10.2.5.1 Advancement of functional endpoint measurement beyond traditional walk tests to boost growth

- 10.2.6 STRUCTURAL HEART DISEASE/INTERVENTIONAL CARDIOLOGY

- 10.2.6.1 Remote post-procedural surveillance in structural heart interventions to drive segment

- 10.2.1 ATHEROSCLEROTIC CARDIOVASCULAR DISEASE/SECONDARY PREVENTION

- 10.3 ONCOLOGY

- 10.3.1 SOLID TUMORS

- 10.3.1.1 BREAST CANCER

- 10.3.1.1.1 Segment driven by enhanced tumor characterization through AI-driven imaging and pathology analytics

- 10.3.1.2 LUNG CANCER

- 10.3.1.2.1 Enhanced immunotherapy response prediction using imaging biomarkers to boost growth

- 10.3.1.3 Prostate cancer

- 10.3.1.3.1 Segment growth propelled by reduced variability in cancer grading with quantitative digital pathology

- 10.3.1.4 COLORECTAL CANCER

- 10.3.1.4.1 Enhanced gastrointestinal oncology trials with decentralized functional endpoints - major driver

- 10.3.1.5 BRAIN TUMOR

- 10.3.1.5.1 Enhanced tumor monitoring with advanced MRI and volumetric analytics

- 10.3.1.6 OTHER SOLID TUMORS

- 10.3.1.6.1 Extension of digital biomarker utility across rare and heterogeneous tumor types to drive segment

- 10.3.1.1 BREAST CANCER

- 10.3.2 HEMATOLOGIC MALIGNANCIES

- 10.3.2.1 LEUKEMIA

- 10.3.2.1.1 Enhanced MRD detection and quantification through AI-driven analytics to boost market

- 10.3.2.2 LYMPHOMA

- 10.3.2.2.1 Capturing immune response dynamics with continuous digital monitoring - key benefit

- 10.3.2.3 MULTIPLE MYELOMA

- 10.3.2.3.1 Segment growth driven by enhanced disease burden assessment with integrated imaging and pathology analytics

- 10.3.2.4 OTHER HEMATOLOGIC MALIGNANCIES

- 10.3.2.4.1 High-sensitivity endpoint generation in small patient populations to boost market

- 10.3.2.1 LEUKEMIA

- 10.3.1 SOLID TUMORS

- 10.4 DIABETES

- 10.4.1 CONTINUOUS MONITORING PLATFORMS EXPANDING INTO HOLISTIC CARDIOMETABOLIC RISK PREDICTION

- 10.5 MENTAL HEALTH & BEHAVIORAL HEALTH

- 10.5.1 PASSIVE BEHAVIORAL AND VOICE DATA ENABLE SCALABLE OBJECTIVE CONDITION MONITORING

- 10.6 RESPIRATORY DISORDERS

- 10.6.1 EARLY EXACERBATION DETECTION THROUGH CONTINUOUS MONITORING REDUCES HOSPITALIZATIONS AND COSTS

- 10.7 LIFESTYLE & WELLNESS IMPROVEMENT

- 10.7.1 EXPANDING PREVENTIVE HEALTH THROUGH CONTINUOUS BEHAVIORAL DATA INSIGHTS

- 10.8 NEUROLOGY

- 10.8.1 REGULATORY VALIDATION OF DIGITAL ENDPOINTS TO ACCELERATE EARLY DETECTION AND TRIAL ADOPTION

- 10.9 MUSCULOSKELETAL DISORDERS/PAIN MANAGEMENT

- 10.9.1 EMPLOYER-BACKED DIGITAL CARE AND MOTION TRACKING TO DRIVE SCALABLE REHABILITATION SOLUTIONS

- 10.10 WOMEN'S HEALTH & REPRODUCTIVE HEALTH

- 10.10.1 ADDRESSING UNMET NEEDS THROUGH DATA-DRIVEN WOMEN'S HEALTH INSIGHTS

- 10.11 OTHER DISEASES

- 10.11.1 EXPANDING USE CASES TO DRIVE ADOPTION ACROSS CHRONIC AND UNDERSERVED CONDITIONS

11 DIGITAL BIOMARKERS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 CLINICAL RESEARCH

- 11.2.1 PHASE II

- 11.2.1.1 Critical role in early-stage validation and risk reduction in clinical development

- 11.2.2 PHASE III

- 11.2.2.1 Regulatory-grade endpoint validation drives high-stakes clinical trial adoption

- 11.2.3 PHASE IV

- 11.2.3.1 Real-world evidence demand drives scalable continuous monitoring and reimbursement adoption

- 11.2.1 PHASE II

- 11.3 CLINICAL CARE

- 11.3.1 RISING CHRONIC DISEASE BURDEN DRIVING SHIFT TO CONTINUOUS PROACTIVE CARE

12 DIGITAL BIOMARKER MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 12.2.1 CLINICAL TRIAL DRIVEN EFFICIENCY THROUGH HIGH-IMPACT DIGITAL ENDPOINTS

- 12.3 CONTRACT RESEARCH ORGANIZATIONS

- 12.3.1 END-TO-END DIGITAL TRIAL EXECUTION ENABLED THROUGH ADVANCED ANALYTICS

- 12.4 HOSPITALS & SPECIALTY CLINICS

- 12.4.1 ENHANCED CLINICAL OUTCOMES WITH REAL-TIME, DATA-DRIVEN CARE DELIVERY

- 12.5 OTHER END USERS

- 12.5.1 PUBLIC FUNDING AND REAL-WORLD DATA INITIATIVES ACCELERATE ECOSYSTEM-WIDE ADOPTION

13 DIGITAL BIOMARKERS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Regulatory advancements and pharma-tech convergence drive market growth

- 13.2.3 CANADA

- 13.2.3.1 Increasing integration of AI-driven screening and remote monitoring to drive market

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Strong clinical trial ecosystem and progressive digital health regulation to drive market

- 13.3.3 FRANCE

- 13.3.3.1 Strong clinical trial base and evidence-driven regulatory pathways to drive market

- 13.3.4 UK

- 13.3.4.1 Strong NHS data infrastructure and push for data-enabled clinical trials to drive market

- 13.3.5 ITALY

- 13.3.5.1 Strong clinical research activity and oncology-driven demand to shape market growth

- 13.3.6 SPAIN

- 13.3.6.1 Strong clinical trial leadership and high domestic research concentration to drive market

- 13.3.7 REST OF EUROPE

- 13.4 LATIN AMERICA

- 13.4.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.4.2 BRAZIL

- 13.4.2.1 Expanding digital health ecosystem and regulatory reforms to drive digital biomarkers adoption

- 13.4.3 MEXICO

- 13.4.3.1 Growing clinical trial participation and digital transformation to drive digital biomarkers adoption

- 13.4.4 REST OF LATIN AMERICA

- 13.5 ASIA PACIFIC

- 13.5.1 ASIA PACIFIC: CLINICAL TRIAL INITIATIONS IN 2014 AND 2024

- 13.5.2 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.5.3 CHINA

- 13.5.3.1 Expanding clinical trial leadership and advancing digital health ecosystem to drive market

- 13.5.4 JAPAN

- 13.5.4.1 Declining clinical trial activity despite strong legacy position to impact market

- 13.5.5 INDIA

- 13.5.5.1 Rapid clinical trial growth, cost advantages, and regulatory reforms to drive market

- 13.5.6 AUSTRALIA

- 13.5.6.1 Strong early-phase trial capabilities and advanced research infrastructure to drive market

- 13.5.7 SOUTH KOREA

- 13.5.7.1 Steady clinical trial growth and strong innovation ecosystem to drive market

- 13.5.8 REST OF ASIA PACIFIC

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 GCC COUNTRIES

- 13.6.2.1 Strong digital health transformation and growing clinical research activity to drive adoption

- 13.6.3 SAUDI ARABIA

- 13.6.3.1 Expanding clinical research activity and government-led initiatives to drive market

- 13.6.4 UAE

- 13.6.4.1 Advancing digital health innovation and strategic collaborations - key growth drivers

- 13.6.5 OTHER GCC COUNTRIES

- 13.6.5.1 Regulatory initiatives, national health visions, and digital health infrastructure boost market growth

- 13.6.6 SOUTH AFRICA

- 13.6.6.1 Leading clinical research hub in Africa with strong infrastructure

- 13.6.7 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL BIOMARKERS MARKET

- 14.3 REVENUE SHARE ANALYSIS OF THE TOP MARKET PLAYERS

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND COMPARISON

- 14.6 COMPANY VALUATION & FINANCIAL METRICS

- 14.6.1 FINANCIAL METRICS

- 14.6.2 COMPANY VALUATION

- 14.7 COMPANY EVALUATION MATRIX

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Therapeutic area footprint

- 14.7.5.5 Application footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT/SERVICE LAUNCHES & APPROVALS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 IXICO PLC

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches/approvals

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 AMETRIS, LLC

- 15.1.2.1 Business overview

- 15.1.2.2 Products Offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches/enhancements

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 EMPATICA INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches/approvals

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 ALIVECOR, INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches/approvals

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 CONNEQT HEALTH

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product enhancements/approvals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 VIVOSENSE

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.2.1 Other developments

- 15.1.7 BIOSENSICS

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches/approvals

- 15.1.7.3.2 Deals

- 15.1.8 LUNIT INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches/approvals

- 15.1.8.3.2 Deals

- 15.1.9 AKILI, INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.10 QUIBIM

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches/approvals/enhancements

- 15.1.10.3.2 Deals

- 15.1.11 CLARIO

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 PROSCIA INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches/approvals

- 15.1.12.3.2 Deals

- 15.1.13 KONEKSA HEALTH

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Deals

- 15.1.14 LINUS HEALTH

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product launches/approvals

- 15.1.14.3.2 Deals

- 15.1.1 IXICO PLC

- 15.2 OTHER PLAYERS

- 15.2.1 SONDE HEALTH, INC.

- 15.2.2 ALTOIDA

- 15.2.3 IMVARIA INC.

- 15.2.4 CUMULUS NEUROSCIENCE LIMITED

- 15.2.5 DELVE HEALTH

- 15.2.6 FEEL THERAPEUTICS

- 15.2.7 NANOWEAR INC.

- 15.2.8 EXOSYSTEMS

- 15.2.9 CARDIOSIGNAL

- 15.2.10 IMAGENE AI LTD.

- 15.2.11 NEUROTRACK TECHNOLOGIES, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH APPROACH

- 16.1.1 SECONDARY RESEARCH

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY RESEARCH

- 16.1.2.1 Primary sources

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of primaries

- 16.1.2.4 Insights from primary experts

- 16.1.1 SECONDARY RESEARCH

- 16.2 RESEARCH METHODOLOGY DESIGN

- 16.3 MARKET SIZE ESTIMATION

- 16.4 MARKET BREAKDOWN DATA TRIANGULATION

- 16.5 MARKET SHARE ESTIMATION

- 16.6 STUDY ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS

- 16.7.1 METHODOLOGY-RELATED LIMITATIONS

- 16.8 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS