|

시장보고서

상품코드

2029907

전기 보트 시장 : 보트 유형별, 동력원별, 보트 출력별, 선체 유형별, 운항 방식별, 보트 사이즈별, 지역별 - 세계 예측(-2031년)Electric Boats Market by Boat Type, Power Source, Boat Power, Hull Type, Mode of Operation, Boat Size, and Region - Global Forecast to 2031 |

||||||

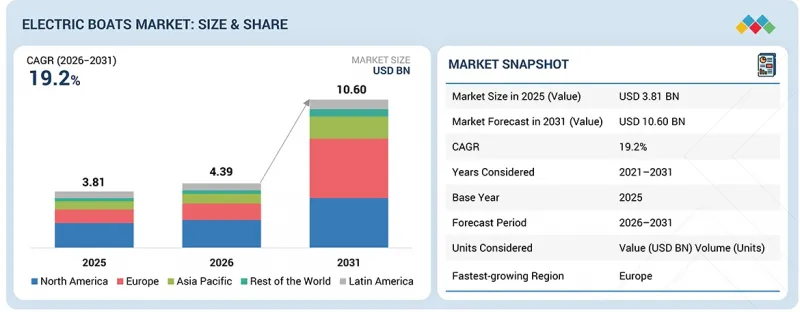

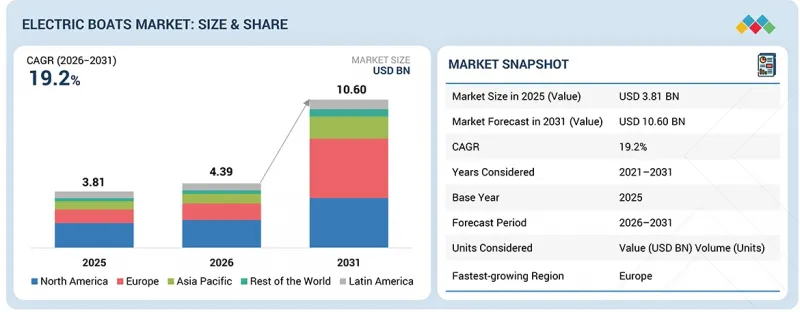

세계의 전기 보트 시장 규모는 2026년 43억 9,000만 달러에서 2031년에 106억 달러에 달할 것으로 예측되며, CAGR로 19.2%의 성장이 전망됩니다.

더 깨끗한 추진력에 대한 수요와 배터리 기술의 혁신으로 전기보트의 성능이 향상되고 항속거리와 신뢰성이 높아지면서 전기보트가 경제적으로도 실현 가능해졌습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 10억 달러 |

| 부문 | 보트 유형, 동력원, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

특히 레크리에이션 활동과 여행에서 지속가능하고 조용한 선박에 대한 소비자의 선호도 또한 그 보급을 촉진하고 있습니다. 항만이나 마리나에 충분한 충전소가 마련되면 운영이 쉬워지고, 항속거리 제한에 따른 영향도 줄일 수 있습니다. 또한, 여객 페리 서비스 및 단거리 수상 이동을 위한 전기 보트 이용의 확대도 업계를 주도하고 있습니다.

"보트 크기별로는 20피트 미만이 예측 기간 동안 가장 지배적인 부문이 될 것으로 예상됩니다."

20피트 미만 부문은 주로 소형 레크리에이션 보트, 텐더, 어선 등이 많이 포함되어 있으며, 전기 시스템을 쉽게 사용할 수 있기 때문에 계속해서 주요 부문이 될 것으로 예상됩니다. 이 보트는 주로 단거리에서 사용되기 때문에 소형 배터리가 필요하며, 전기 추진 시스템과 잘 어울립니다. 또한, 현재 더 작고 효율적인 모터를 사용할 수 있어 20피트 미만의 보트의 보급에 박차를 가하고 있습니다.

"보트 유형별로는 상업용 보트 부문이 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 보입니다."

상업용 보트 부문은 연료비 절감과 배출가스 규제 준수에 대한 운항 사업자의 노력으로 인해 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다. 더 많은 페리, 관광선, 내항선이 전기 추진으로 전환하고 있습니다. 배터리 수명 향상, 충전 시간 단축, 하이브리드 시스템의 보급도 상업용 보트의 일상 업무에서 실용성을 높이고 있습니다.

"유럽이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

내륙 및 연안 수로의 엄격한 배출 규제와 더불어 정부의 무공해 선박에 대한 자금 지원으로 인해 유럽이 전기 보트 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 상업 사업자의 조기 채택, 기존 충전 인프라 및 강력한 조선 능력으로 인해 다른 지역에 비해 빠른 배포 및 규모 확장이 가능합니다.

세계의 전기 보트 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 지속가능성과 규제 상황

제8장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제9장 전기 보트 시장 : 보트 유형별

제10장 전기 보트 시장 : 보트 출력별

제11장 전기 보트 시장 : 보트 사이즈별

제12장 전기 보트 시장 : 선체 유형별

제13장 전기 보트 시장 : 운항 방식별

제14장 전기 보트 시장 : 동력원별

제15장 전기 보트 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.05.21The electric boats market is projected to grow from USD 4.39 billion in 2026 to USD 10.60 billion in 2031, at a CAGR of 19.2%. The need for cleaner propulsion sources and innovations in battery technology has enhanced the performance of electric boats, increasing range and reliability and rendering them economically viable.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Boat Type, Power Source and Region |

| Regions covered | North America, Europe, APAC, RoW |

Consumer preference for sustainable, quiet marine vessels also boosts their adoption, especially for recreational activities and tours. The construction of sufficient charging stations at ports and marinas eases operation and reduces the effects of range limitations. Furthermore, the increasing use of electric boats for passenger ferry services and short trips across the water also drives the industry.

"By boat size, <20 feet to be most dominant segment during the forecast period."

The <20 feet segment is expected to remain the leading segment, mainly because it includes many small recreational boats, tenders, and fishing boats, for which electric systems are easier to use. These boats require smaller batteries and are mostly used over short distances, which aligns well with electric propulsion. Also, more compact and efficient motors are now available, supporting wider adoption of boats under 20 feet.

"By boat type, commercial boats segment to register highest CAGR during forecast period."

The commercial boats segment is expected to record the highest CAGR during the forecast period, primarily due to operators seeking to reduce fuel costs and comply with emission regulations. More ferries, tour boats, and inland vessels are moving toward electric options. Better battery life, faster charging, and hybrid systems are also making commercial boats more practical for daily operations.

"Europe to account for largest market share during forecast period."

Europe is projected to have the largest market share in the electric boats market due to strict emission regulations on inland and coastal waterways, which is supported by government funding for zero-emission vessels. Early adoption by commercial operators, established charging infrastructure, and strong shipbuilding capabilities enable faster deployment and scaling compared to other regions.

The breakdown of profiles for primary participants in the electric boats market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: Directors - 20%, C-level Executives - 10%, and Others (Managers and Other Non-C-level Executives) - 70%

- By Region: North America - 20%, Europe - 20%, Asia Pacific - 40%, Rest of the World (RoW) - 20%

Brunswick Corporation (US), Groupe Beneteau (France), AZIMUT | BENETTI GROUP (Italy), Candela Technology AB (Sweden), and Arc Boat Company (US) are some of the key players in the electric boats market.

Research Coverage:

This market study covers the electric boats market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of key players in the market, their company profiles, key observations on their products and business offerings, recent developments, and the key market strategies they have adopted.

Reasons to Buy This Report:

The report will help market leaders/new entrants with information on the closest approximations of revenue for the overall electric boats market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Rising focus of boat operators on reducing operating costs and fuel dependency, Improvements in battery capacity and hybrid/solar power systems), Restraints (Limited charging and shore power infrastructure, High upfront cost of high-power electric and hybrid boats), Opportunities (Emergence of autonomous and remotely operated electric boats, Development of high-power electric and hybrid systems for larger commercial boats), Challenges (Constant improvements in conventional diesel and hybrid engines, High dependence on battery supply chains and raw materials)

Market Penetration: Comprehensive information on electric boats offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the electric boats market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the electric boats market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the electric boats market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ELECTRIC BOATS MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRIC BOATS MARKET

- 3.2 ELECTRIC BOATS MARKET, BY BOAT TYPE

- 3.3 ELECTRIC BOATS MARKET, BY BOAT POWER

- 3.4 ELECTRIC BOATS MARKET, BY BOAT SIZE

- 3.5 ELECTRIC BOATS MARKET, BY MODE OF OPERATION

- 3.6 ELECTRIC BOATS MARKET, BY HULL TYPE

- 3.7 ELECTRIC BOATS MARKET, BY POWER SOURCE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Regulatory pressure on emissions and inland waterway decarbonization

- 4.2.1.2 Operating cost advantage in high-utilization and short-route applications

- 4.2.1.3 Advancements in battery systems improving range and performance

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited charging and shore power infrastructure for large vessels

- 4.2.2.2 High upfront capital cost and lifecycle uncertainty

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of electric ferries, workboats, and fleet-based applications

- 4.2.3.2 Development of autonomous and remotely operated electric vessels

- 4.2.4 CHALLENGES

- 4.2.4.1 Competition from improved hybrid and efficient ICE technologies

- 4.2.4.2 Dependence on battery supply chains and critical materials

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES IN ELECTRIC BOATS MARKET

- 4.4 INTER-CONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ELECTRIC BOAT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 89)

- 5.5.2 EXPORT SCENARIO (HS CODE 89)

- 5.6 KEY CONFERENCES & EVENTS, 2026-2027

- 5.7 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 PRICING ANALYSIS

- 5.9.1 AVERAGE SELLING PRICE OF ELECTRIC BOATS, BY BOAT TYPE

- 5.9.2 AVERAGE SELLING PRICE, BY REGION

- 5.10 OPERATIONAL DATA

- 5.11 CASE STUDIES

- 5.11.1 CASE STUDY 1: CURTIS MARITIME DEVELOPED HYBRID ELECTRIC TUGBOATS TO REDUCE EMISSIONS

- 5.11.2 CASE STUDY 2: STOCKHOLM DEPLOYED CANDELA P-12 USING BATTERY PROPULSION AND HYDROFOIL TECHNOLOGY

- 5.11.3 CASE STUDY 3: CANDYMAN BOATS INTRODUCED ELECTRIC HYDROFOIL FERRY FOR URBAN WATER TRANSPORT

- 5.12 IMPACT OF 2025 US TARIFFS

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRY/REGION

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.4.4 Rest of the World

- 5.12.5 IMPACT ON END-USER INDUSTRIES

- 5.13 TOTAL COST OF OWNERSHIP

- 5.13.1 INTEGRATION AND DEPLOYMENT COSTS

- 5.13.2 COST OF TRAINING AND SPARES

- 5.13.3 ANNUAL OPERATIONS & MAINTENANCE COSTS

- 5.13.4 MID-LIFE OVERHAUL COSTS

- 5.13.5 OTHER COSTS

- 5.14 VOLUME DATA

- 5.15 BILL OF MATERIALS (BOM ANALYSIS)

- 5.15.1 BUSINESS MODELS

- 5.15.2 SUBSCRIPTION-BASED MODEL

- 5.15.3 WHOLESALE/CAPACITY LEASING MODEL

- 5.15.4 REVENUE-SHARING PARTNERSHIPS MODEL

- 5.15.5 OWNERSHIP/DIRECT SALES MODEL

- 5.15.6 CHARGING-AS-A-SERVICE MODEL

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 TARIFF DATA

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 REGULATORY FRAMEWORK

- 7.3 INDUSTRY STANDARDS

- 7.4 SUSTAINABILITY INITIATIVES

- 7.4.1 CARBON IMPACT AND ECO-APPLICATIONS OF GRAPHENE

8 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 8.1 KEY EMERGING TECHNOLOGIES

- 8.1.1 LITHIUM-ION BATTERY SYSTEMS

- 8.1.2 ELECTRIC PROPULSION SYSTEMS

- 8.1.3 FAST CHARGING INFRASTRUCTURE

- 8.1.4 BATTERY MANAGEMENT SYSTEMS (BMS)

- 8.1.5 HYDROGEN FUEL CELLS

- 8.2 COMPLEMENTARY TECHNOLOGIES

- 8.2.1 SMART NAVIGATION AND CONTROL SYSTEMS

- 8.3 ADJACENT TECHNOLOGIES

- 8.3.1 LIGHTWEIGHT COMPOSITE MATERIALS

- 8.4 TECHNOLOGY ROADMAP

- 8.5 PATENT ANALYSIS

- 8.6 FUTURE APPLICATIONS

- 8.7 IMPACT OF AI/GENERATIVE AI ON ELECTRIC BOATS MARKET

- 8.7.1 TOP USE CASES AND MARKET POTENTIAL

- 8.7.2 BEST PRACTICES IN ELECTRIC BOATS MARKET

- 8.7.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 8.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ELECTRIC BOATS MARKET

9 ELECTRIC BOATS MARKET, BY BOAT TYPE

- 9.1 INTRODUCTION

- 9.2 RECREATIONAL ELECTRIC BOATS

- 9.2.1 CRUISING BOATS

- 9.2.1.1 Regulatory enforcement and alignment with predictable short-distance operating conditions to drive market

- 9.2.2 SPEEDBOATS

- 9.2.2.1 Need for high-power propulsion improvements and compliance with tightening emission and noise regulations to drive market

- 9.2.1 CRUISING BOATS

- 9.3 COMMERCIAL ELECTRIC BOATS

- 9.3.1 PASSENGER AND CREW FERRY BOATS

- 9.3.1.1 Focus on accelerating passenger and crew ferry electrification to drive market

- 9.3.2 FISHING BOATS

- 9.3.2.1 Focus on enabling fishing boat electrification through short-range operating patterns and fuel cost reduction pressures to boost growth

- 9.3.3 TUG & WORKBOATS

- 9.3.3.1 Need for driving tug and workboat electrification through port-level emission mandates t to spur demand

- 9.3.4 OTHER COMMERCIAL ELECTRIC BOATS

- 9.3.1 PASSENGER AND CREW FERRY BOATS

- 9.4 MILITARY & LAW ENFORCEMENT BOATS

- 9.4.1 PATROL BOATS

- 9.4.1.1 Need for advancing patrol boat electrification through low-signature mission requirements to drive market

- 9.4.2 ATTACK/COMBAT BOATS

- 9.4.2.1 Focus on integrating hybrid-electric systems in attack and combat boats to support growth

- 9.4.1 PATROL BOATS

10 ELECTRIC BOATS MARKET, BY BOAT POWER

- 10.1 INTRODUCTION

- 10.2 < 5 KW

- 10.2.1 NEED FOR ALIGNMENT WITH REGULATORY THRESHOLD, USAGE PATTERNS, AND INFRASTRUCTURE CONSTRAINTS TO DRIVE MARKET

- 10.3 5-30 KW

- 10.3.1 NEED FOR ALIGNING WITH OPERATIONAL REQUIREMENTS OF SMALL COMMERCIAL BOATS TO DRIVE MARKET

- 10.4 > 30 KW

- 10.4.1 FOCUS ON SUSTAINED PROPULSION TO SUPPORT HIGH SPEEDS, HEAVY PAYLOADS, AND LONG DUTY CYCLES TO DRIVE MARKET

11 ELECTRIC BOATS MARKET, BY BOAT SIZE

- 11.1 INTRODUCTION

- 11.2 < 20 FEET

- 11.2.1 NEED FOR ALIGNMENT BETWEEN BATTERY LIMITATIONS AND OPERATIONAL REQUIREMENTS TO DRIVE MARKET

- 11.3 20-50 FEET

- 11.3.1 EMPHASIS ON ADVANCEMENTS IN LITHIUM-ION BATTERY SYSTEMS TO SPUR DEMAND

- 11.4 > 50 FEET

- 11.4.1 NEED FOR DRIVING ELECTRIFICATION IN VESSEL CLASSES TO DRIVE MARKET

12 ELECTRIC BOATS MARKET, BY HULL TYPE

- 12.1 INTRODUCTION

- 12.2 CLASSIFICATION OF DIFFERENT HULL TYPES BASED ON DESIGN ATTRIBUTES

- 12.2.1 FOIL-BORNE BOATS

- 12.2.2 RIBS (NON-FOILING)

- 12.2.3 FULLY INFLATABLE BOATS (NON-FOILING)

- 12.2.4 CONVENTIONAL HARD-HULL BOATS (NON-FOILING, NON-INFLATABLE)

- 12.3 MONOHULL

- 12.3.1 MONOHULLS PROVIDE DIRECT PATHWAY FOR ELECTRIFICATION WITHOUT REQUIRING FUNDAMENTAL CHANGES TO VESSEL ARCHITECTURE

- 12.4 TWIN HULL (CATAMARAN)

- 12.4.1 STRUCTURAL ADVANTAGES OFFERED BY TWIN HULL DESIGNS TO DRIVE MARKET

- 12.5 TRI-HULL (TRIMARAN)

- 12.5.1 TRI-HULL CONFIGURATIONS OFFER STRUCTURAL BALANCE BETWEEN EFFICIENCY, STABILITY, AND DECK UTILIZATION

- 12.6 OTHERS

13 ELECTRIC BOATS MARKET, BY MODE OF OPERATION

- 13.1 INTRODUCTION

- 13.2 CREWED BOATS

- 13.2.1 STRINGENT REGULATORY DEMANDS AND OPERATIONAL CONSTRAINTS TO DRIVE MARKET

- 13.3 UNCREWED BOATS

- 13.3.1 REMOTELY OPERATED BOATS

- 13.3.1.1 Expanding remotely operated electric boat deployment through regulatory alignment to drive market

- 13.3.2 AUTONOMOUS BOATS

- 13.3.2.1 Advancing autonomous electric boat deployment through government-backed programs to boost market

- 13.3.1 REMOTELY OPERATED BOATS

14 ELECTRIC BOATS MARKET, BY POWER SOURCE

- 14.1 INTRODUCTION

- 14.2 BATTERY-POWERED BOATS

- 14.2.1 REGULATORY PRESSURE ON INLAND AND COASTAL WATERWAYS TO DRIVE MARKET

- 14.3 SOLAR-POWERED BOATS

- 14.3.1 ABILITY OF SOLAR-POWERED BOATS TO REDUCE RELIANCE ON SHORE-BASED CHARGING TO DRIVE GROWTH

- 14.4 HYBRID-POWERED BOATS

- 14.4.1 STRINGENT EMISSION REGULATIONS TO BOOST GROWTH

15 ELECTRIC BOATS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Regulatory enforcement and federally backed funding programs to drive deployment of electric boats

- 15.2.2 CANADA

- 15.2.2.1 Federal decarbonization programs and ferry electrification initiatives to drive electric boat adoption

- 15.2.1 US

- 15.3 ASIA PACIFIC

- 15.3.1 CHINA

- 15.3.1.1 Regulatory enforcement and domestic supply chain strength to drive market expansion

- 15.3.2 JAPAN

- 15.3.2.1 Government-backed pilot programs and propulsion innovation to drive market development

- 15.3.3 INDIA

- 15.3.3.1 Inland waterway modernization and localized electrification efforts to drive market penetration

- 15.3.4 SOUTH KOREA

- 15.3.4.1 National decarbonization targets and shipbuilding capabilities to drive growth

- 15.3.5 NEW ZEALAND

- 15.3.5.1 Policy-backed coastal decarbonization and pilot ferry electrification to drive growth

- 15.3.6 REST OF ASIA PACIFIC

- 15.3.1 CHINA

- 15.4 EUROPE

- 15.4.1 NORWAY

- 15.4.1.1 Government procurement mandates and zero-emission regulations to drive market

- 15.4.2 GREECE

- 15.4.2.1 EU-backed funding and island transport electrification initiatives for adoption

- 15.4.3 NETHERLANDS

- 15.4.3.1 Urban emission regulations and canal transport integration to drive market growth

- 15.4.4 FINLAND

- 15.4.4.1 Policy-backed pilot deployments and seasonal operating economics to drive growth

- 15.4.5 DENMARK

- 15.4.5.1 Port-level emission controls and national decarbonization pathways to drive market

- 15.4.6 GERMANY

- 15.4.6.1 Inland waterway regulations and subsidy-supported retrofits to drive market transition

- 15.4.7 REST OF EUROPE

- 15.4.1 NORWAY

- 15.5 REST OF THE WORLD

- 15.5.1 MIDDLE EAST & AFRICA

- 15.5.1.1 Government-led maritime electrification programs and fleet-based deployments to drive electric boats market expansion

- 15.5.2 LATIN AMERICA

- 15.5.2.1 Urban water transport modernization and fuel cost pressures to drive electric boats market adoption

- 15.5.1 MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 16.3 REVENUE ANALYSIS, 2021-2024

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.5 BRAND/PRODUCT COMPARISON

- 16.6 COMPANY VALUATION AND FINANCIAL METRICS

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Boat type footprint

- 16.7.5.4 Power source footprint

- 16.7.5.5 Boat size footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING

- 16.8.5.1 List of startups/SMEs

- 16.8.5.2 Competitive benchmarking of startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 BRUNSWICK CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 GROUPE BENETEAU

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 AZIMUT|BENETTI GROUP

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Other developments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 CANDELA TECHNOLOGY AB

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 GREENLINE YACHTS

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Other developments

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to Win

- 17.1.5.4.2 Strategic Choices

- 17.1.5.4.3 Weakness and competitive threats

- 17.1.6 ARC BOAT COMPANY

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.6.3.3 Other developments

- 17.1.7 BOOTE MARIAN GMBH

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Other developments

- 17.1.8 DUFFY ELECTRIC BOAT COMPANY

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.9 SAY CARBON YACHTS

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Deals

- 17.1.9.3.2 Other developments

- 17.1.10 RUBAN BLEU

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.10.3.3 Other developments

- 17.1.11 FRAUSCHER BOOTSWERFT

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches

- 17.1.11.3.2 Deals

- 17.1.11.3.3 Other developments

- 17.1.12 NAVALT

- 17.1.12.1 Business overview

- 17.1.12.2 Recent developments

- 17.1.12.2.1 Product launches

- 17.1.12.2.2 Deals

- 17.1.12.2.3 Other developments

- 17.1.13 INGENITY ELECTRIC

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product launches

- 17.1.13.3.2 Deals

- 17.1.13.3.3 Other developments

- 17.1.14 QUADROFOIL D.O.O

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.2.1 Other developments

- 17.1.15 VISION MARINE TECHNOLOGIES INC

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product launches

- 17.1.15.3.2 Deals

- 17.1.15.3.3 Other developments

- 17.1.16 SILENT YACHTS

- 17.1.16.1 Business overview

- 17.1.16.2 Products offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Product launches

- 17.1.16.3.2 Deals

- 17.1.16.3.3 Other developments

- 17.1.1 BRUNSWICK CORPORATION

- 17.2 OTHER PLAYERS

- 17.2.1 CALLBOATS

- 17.2.2 MAGONIS BOATS SL

- 17.2.3 OCEANVOLT

- 17.2.4 EVOY AS

- 17.2.5 COSMOPOLITAN YACHTS

- 17.2.6 SALONA YACHTS

- 17.2.7 RS ELECTRIC BOATS

- 17.2.8 ALFASTREET YACHTS

- 17.2.9 RAND

- 17.2.10 LASAI

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from secondary sources

- 18.1.2.2 Primary interview participants

- 18.1.2.3 Breakdown of primary interviews

- 18.1.1 SECONDARY DATA

- 18.2 FACTOR ANALYSIS

- 18.2.1 INTRODUCTION

- 18.2.2 DEMAND-SIDE INDICATORS

- 18.2.2.1 Growing interest in recreational activities

- 18.2.3 DEMAND-SIDE INDICATORS

- 18.2.3.1 Increasing technological advancements to enhance passenger experience

- 18.3 STUDY SCOPE

- 18.3.1 SEGMENTS AND SUBSEGMENTS

- 18.3.1.1 Electric boats market, by boat type

- 18.3.1.2 Electric boats market, by boat power

- 18.3.1.3 Electric boats market, by boat size

- 18.3.1 SEGMENTS AND SUBSEGMENTS

- 18.4 RESEARCH APPROACH AND METHODOLOGY

- 18.4.1 SEGMENTS AND SUBSEGMENTS

- 18.4.2 MARKET SIZE ESTIMATION

- 18.4.2.1 Bottom-up approach

- 18.4.2.2 Top-down approach

- 18.4.2.3 Bottom-up approach

- 18.5 DATA TRIANGULATION

- 18.6 RESEARCH ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS