|

시장보고서

상품코드

2034864

선박 엔진 시장 : 스트로크 유형별, 엔진 유형별, 출력 범위별, 연료 유형별, 선박 유형별, 지역별 - 예측(-2031년)Marine Engines Market by Engine (Propulsion, Auxiliary), Type (Two Stroke, Four Stroke), Power Range (<1,000 hp, 1,001-5,000 hp, 5,001-10,000 hp, 10,001-20,000 hp, >20,000 hp), Fuel, Vessel, and Region - Global Forecast to 2031 |

||||||

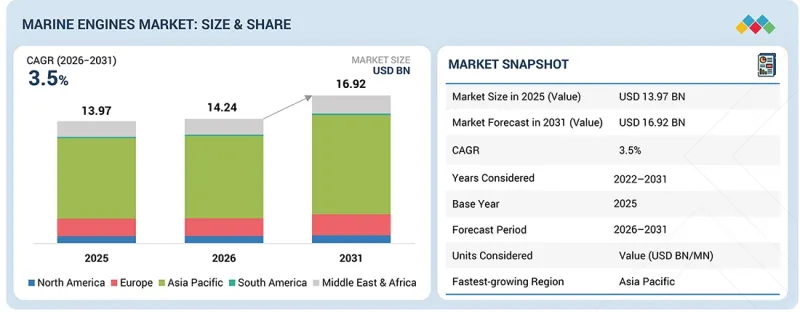

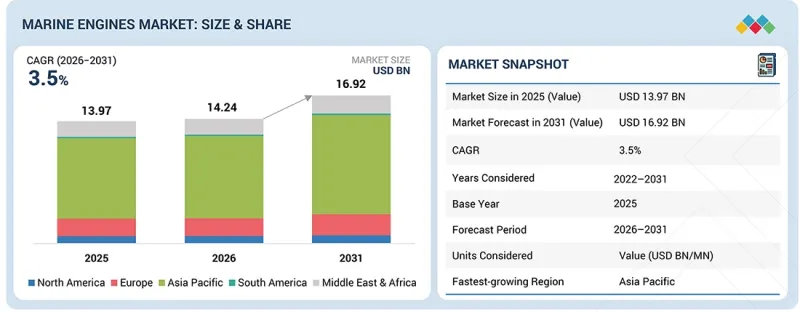

선박 엔진 시장 규모는 2026년 142억 4,000만 달러에서 2031년까지 169억 2,000만 달러에 이를 것으로 예측되며, CAGR은 3.5%를 나타낼 전망입니다.

이 시장 전망은 환경 규제 강화와 해운업계의 우선순위 변화에 따라 보다 깨끗하고 효율적이며 디지털로 통합된 추진 시스템으로의 명확한 전환을 통해 형성될 것으로 보입니다. 각국 정부와 국제 규제 기관은 탈탄소화 목표에 따라 점점 더 엄격한 배출 기준을 적용하고 있으며, 이로 인해 기존 중유 엔진에서 LNG, 메탄올, 암모니아, 하이브리드 전기 시스템과 같은 대체 연료 솔루션으로의 전환이 가속화되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억/1,000만 달러) |

| 부문 | 스트로크 유형별, 엔진 유형별, 출력 범위별, 연료 유형별, 선박 유형별, 지역별 |

| 대상 지역 | 유럽, 아시아태평양, 북미, 남미, 중동 및 아프리카 |

동시에 열효율 향상, 폐열 회수, 모듈식 구성 등 엔진 설계의 발전으로 전체 선박의 성능이 향상되고 운영 비용이 절감되고 있습니다. 또한, 스마트 센서의 통합, 예지보전, 실시간 성능 모니터링을 통해 엔진의 최적화된 운영과 다운타임 감소를 가능하게 하는 디지털화도 중요한 요소로 부상하고 있습니다.

"예측 기간 동안 유조선은 선박 부문에서 두 번째로 큰 점유율을 차지할 것으로 예측됩니다. "

이는 세계 에너지 무역에서 원유 및 정제된 제품의 운송이 여전히 중요하다는 것을 반영합니다. 정부 및 정부 간 기관의 데이터에 따르면, 재생에너지로의 전환이 점진적으로 진행되고 있음에도 불구하고, 중기적으로 석유는 세계 에너지 구성의 주요 요소로 남아 해상 석유 무역의 대량 수송이 유지될 것으로 예측됩니다. 이러한 지속적인 수요는 대용량과 내구성이 뛰어난 선박 엔진을 필요로 하는 대형 유조선 선단, 특히 초대형 원유운반선(VLCC)과 제품운반선에 대한 안정적인 수요를 뒷받침하고 있습니다. 또한, 노후화된 유조선 선단은 IMO의 엄격한 배기가스 규제에 대응하기 위해 갱신 및 개조가 진행되고 있으며, 이는 연료 효율이 높은 첨단 엔진에 대한 수요를 견인하고 있습니다. 특히 중동, 아프리카, 남미 지역의 해양 석유 생산에 대한 투자 확대는 유조선의 가동률을 뒷받침하고 있으며, 이는 선박 엔진 시장에서 이 부문의 확고한 입지를 더욱 공고히 하고 있습니다.

"보조 엔진은 예측 기간 동안 엔진 부문에서 2위를 차지할 것으로 예측됩니다. "

이는 주로 모든 선종에서 선내 전력 수요를 충족시키는 데 있어 보조 엔진이 중요한 역할을 하기 때문입니다. 보조 엔진은 항해 시스템, 하역 설비, 조명, 안전 시스템 및 생활 설비의 가동에 필수적이며, 선박의 규모와 용도에 관계없이 그 중요성은 변함없습니다. 전 세계 해운 활동의 꾸준한 성장과 선박의 복잡성 증가에 따라 신뢰할 수 있는 선내 전력 시스템에 대한 수요는 지속적으로 증가하고 있습니다. 또한, 환경 규제 및 에너지 효율 규제의 강화로 인해 배출가스 저감 및 연료 효율을 향상시킨 첨단 보조 엔진(하이브리드 및 이중 연료 구성 포함)의 도입이 촉진되고 있습니다. 규제 기준을 충족하기 위한 기존 선단의 개조와 기술적으로 진보된 선박에 대한 투자 증가로 인해 보조 엔진에 대한 수요가 더욱 증가하여 시장에서 큰 점유율을 차지하게 되었습니다.

"예측 기간 동안 유럽은 선박 엔진 시장에서 중요한 위치를 차지할 것으로 예측됩니다. "

유럽 선박 엔진 시장은 유로스타트(Eurostat), 유럽위원회(European Commission) 등 유럽 정부 기관의 일관된 데이터로 뒷받침되는 견고하고 확립된 해양 생태계에 의해 크게 견인되고 있습니다. 이 지역은 엄청난 양의 해상 무역을 처리하고 있으며, 2025년 한 분기 동안 EU 항구는 약 8억 4천만 톤의 화물을 처리했으며, 이는 해운 활동의 규모와 선박 및 엔진에 대한 지속적인 수요를 강조하고 있습니다. 또한, 유럽연합(EU) 대외 화물 무역의 약 90%가 해상 운송을 통해 이루어지고 있으며, 해운은 지역 경제의 중요한 기반이 되어 신규 엔진과 개조 솔루션 모두에 대한 안정적인 수요를 보장합니다. 또한, 유럽은 세계 최대 규모의 최첨단 선단을 유지하고 있으며, 세계 총톤수 및 LNG 운반선, 유조선 등 특수선박의 상당 부분을 차지하고 있으며, 이들 선박은 기술적으로 진보된 선박 엔진을 필요로 합니다. 또한, EU 전역에 약 150여 개의 주요 조선소가 고부가가치 및 기술적으로 복잡한 선박 건조에 집중하고 있어, 신조 및 개조 활동을 통해 엔진에 대한 지속적인 수요를 뒷받침하고 있습니다. 여기에 저배출 해운을 촉진하는 강력한 규제 프레임워크와 선대 현대화 및 지역 조선 역량 강화를 위한 정부 주도의 노력은 차세대 엔진 도입을 가속화하고 있습니다.

선박 엔진 시장은 주로 명성이 높은 세계 선도 기업들이 주도하고 있습니다. 주요 기업으로는 Caterpillar(미국), Wartsila(핀란드), AB Volvo Penta(스웨덴), Everllence(독일), Rolls-Royce Plc(영국), Mitsubishi Heavy Industries, Ltd.(일본), HD현대중공업(한국), Cummins Inc.(미국), DAIHATSU INFINEARTH MFG.(일본), Deutz AG(독일) 등을 들 수 있습니다.

조사 범위:

본 보고서에서는 엔진(추진용 및 보조용), 유형(4행정 및 2행정), 출력 범위(<1,000 hp, 1,001-5,000 hp, 5,001-10,000 hp, 10,001-20,000 hp, and> 1,000 hp, and> 2,000 hp)20,000마력), 연료(선박용 경유, 기타, 중유, 선박용 경유), 선박(벌크 화물선, 유조선, 해양 지원선, 일반 화물선, 기타, 컨테이너선, 예인선, 제품 탱커), 지역(아시아태평양, 북미, 유럽, 중동/아프리카, 남미) 등 다양한 매개변수에 따라 다양한 매개변수(아시아, 북미, 유럽, 중동, 아프리카, 남미)를 기반으로 선박 엔진 시장에 대한 종합적인 정의, 설명 및 예측을 제공합니다. 또한, 본 보고서는 선박 엔진 시장에 대한 철저한 정성적 및 정량적 분석을 제공하며, 주요 시장 성장 촉진요인 및 과제에 대한 종합적인 검토를 포함하고 있습니다. 또한, 경쟁 구도 평가, 시장 역학 분석, 가치 기반 시장 예측, 선박 엔진 시장 전망 동향 등 시장의 중요한 측면을 다루고 있습니다.

본 보고서 구매의 주요 이점

이 보고서는 선박 엔진 시장의 기존 업계 리더와 신규 시장 진출기업 모두에게 도움이 될 수 있도록 세심하게 설계되었습니다. 전체 시장 및 개별 하위 부문에 대해 신뢰할 수 있는 매출 예측을 제공합니다. 이 데이터는 이해관계자들이 경쟁 구도를 종합적으로 이해하고 비즈니스를 위한 효과적인 시장 전략을 수립할 수 있도록 도와주는 귀중한 자료가 될 것입니다. 또한, 이 보고서는 이해관계자들이 시장 현황을 파악할 수 있는 수단으로 작용하며, 시장 성장 촉진요인, 제약 조건, 과제 및 성장 기회에 대한 중요한 인사이트를 제공합니다. 이러한 인사이트를 통해 이해관계자들은 정보에 입각한 의사결정을 내릴 수 있고, 끊임없이 변화하는 선박 엔진 산업 동향에 대한 최신 정보를 얻을 수 있습니다.

- 시장 성장에 영향을 미치는 주요 촉진요인(해상무역 증가, 아시아 조선업 집중화 및 수주잔량 확대, 세계 선대 노후화에 따른 갱신 및 개조 수요 증가), 제약요인(선박 엔진의 긴 수명주기로 인한 갱신 수요 제한, 높은 자본비용), 기회요인(대체 연료로의 전환, 해양 산업에서의 디지털화 및 자동화), 과제(미래 연료 채택에 대한 불확실성으로 인한 투자 및 기술 리스크, 엄격하고 변화하는 배출가스 규제)를 분석하여 시장 성장에 영향을 미치는 요인을 파악할 수 있습니다.

- 제품 개발 및 혁신 : 선박 엔진 시장은 끊임없이 진화하고 있으며, 제품 개발 및 혁신이 주안점을 두고 있습니다. Caterpillar, Wartsila, Everllence, HDH현대중공업 등 업계 주요 기업들은 변화하는 수요와 환경에 대응하기 위해 제품 라인업 강화를 최전선에서 추진하고 있습니다.

- 시장 발전: 효율적이고 신뢰할 수 있는 추진 시스템에 대한 수요 증가에 힘입어 세계 해운, 에너지 운송 및 해군 활동이 지속적으로 확대됨에 따라 선박 엔진 시장은 꾸준히 발전하고 있습니다. 시장 발전을 형성하는 주요 동향 중 하나는 정부와 국제해사기구가 채택한 엄격한 환경 규제 및 배출 기준에 힘입어 더 깨끗하고 연비 효율적인 엔진으로의 강력한 전환입니다. 이에 따라 각 제조업체들은 하이브리드 및 전기 기술뿐만 아니라 LNG, 메탄올, 기타 저탄소 연료와 같은 대체 연료로 구동할 수 있는 엔진 개발에 집중하고 있습니다. 동시에 디지털 기술의 중요성이 높아지면서 선박 운영사들은 스마트 모니터링 시스템 및 예지보전을 활용하여 엔진 성능 향상과 다운타임 감소를 위해 노력하고 있습니다. 또한, 오래된 선박이 새로운 효율성 및 컴플라이언스 요건을 충족시키기 위해 개조되면서 선대의 현대화 및 개조 활동도 시장 성장을 가속하고 있습니다. 또한, 조선, 항만 인프라, 해양 에너지 프로젝트 및 해군 방위에 대한 투자 증가는 선박 엔진 시장의 확대를 더욱 뒷받침하고 있습니다. 전반적으로 시장은 보다 지속 가능하고 기술 주도적이며 효율성을 중시하는 미래로 향하고 있으며, 지속적인 혁신이 그 발전에 중요한 역할을 하고 있습니다.

- 시장 다각화 : 선박 엔진 시장은 규제 압력, 연료 선호도 변화, 세계 해운 및 해양 산업의 선박 요구사항 변화로 인해 크게 다각화되는 과정에 있습니다. 주요 촉진요인 중 하나는 각국 정부 및 국제해사기구의 배출 기준 강화이며, 이로 인해 제조업체와 선주들은 기존 디젤 엔진을 넘어 LNG, 메탄올, 암모니아 대응, 하이브리드 전기 추진 시스템 등 보다 광범위한 솔루션으로 전환해야 하는 상황에 직면해 있습니다. 동시에 컨테이너선, 유조선, 유조선, 크루즈선, 해양지원선 등 선종별로 운영상의 요구가 다르기 때문에 효율성, 출력, 연료의 유연성에 특화된 엔진 구성이 개발되고 있습니다. 미래 연료 표준에 대한 불확실성이 높아지면서 엔진 제조업체들이 이중 연료 및 다중 연료 엔진을 설계하고 있으며, 이를 통해 운항자는 연료의 가용성 및 비용에 따라 연료를 전환할 수 있습니다. 또한, 해군 방위, 해양 에너지, 내륙 수로에 대한 투자 확대로 선박 엔진의 적용 범위가 확대되어 시장 다변화에 더욱 기여하고 있습니다. 디지털 모니터링 시스템 및 모듈식 엔진 설계와 같은 기술적 진보도 보다 맞춤화된 적응형 솔루션을 가능하게 하고 있습니다. 전반적으로 이러한 다양화는 환경적 요건과 운영상의 요구사항이 모두 혁신을 형성하는 보다 유연하고 지속 가능하며 용도에 특화된 엔진 생태계로의 전환을 반영합니다.

- 경쟁 분석 : 선박 엔진 시장에서 주요 기업들 시장 입지, 성장 전략 및 서비스 제공 내용을 면밀히 조사하기 위해 종합적인 평가를 실시하였습니다. 주요 기업으로는 Caterpillar(미국), Wartsila(핀란드), Everllence(독일), Rolls-Royce Plc(영국), HD현대중공업(한국), AB Volvo Penta(스웨덴), Mitsubishi Heavy Industries, Ltd. Mitsubishi Heavy Industries, Ltd.(일본), Cummins Inc.(미국), 다이하츠 인피니어스 매뉴팩처링(일본),(일본), 도이치 AG(독일) 등을 들 수 있습니다. 이 보고서는 주요 업체들의 경쟁적 위치, 시장 성장을 가속하기 위한 노력, 선박 엔진 분야에서 제공하는 서비스 범위에 대한 상세한 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성 이니셔티브

제8장 고객 현황과 구매 행동

제9장 선박 엔진 시장(스트로크 유형별)

제10장 선박 엔진 시장(엔진 유형별)

제11장 선박 엔진 시장(출력 범위별)

제12장 선박 엔진 시장(연료 유형별)

제13장 선박 엔진 시장(선박 유형별)

제14장 선박 엔진 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSH 26.06.01The marine engines market is projected to reach USD 16.92 billion by 2031, from 14.24 billion in 2026, with a CAGR of 3.5%. The future of this market is poised to be shaped by a clear transition toward cleaner, more efficient, and digitally integrated propulsion systems, driven by tightening environmental regulations and evolving maritime industry priorities. Governments and international regulatory bodies are increasingly enforcing stricter emission norms aligned with decarbonization targets, which is accelerating the shift from conventional heavy fuel oil engines toward alternative fuel solutions such as LNG, methanol, ammonia, and hybrid-electric systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD BN/MN) |

| Segments | By Engine, Type, Power Range, Vessels, Fuel |

| Regions covered | Europe, Asia Pacific, North America, South America, Middle East & Africa |

At the same time, advancements in engine design, including higher thermal efficiency, waste heat recovery, and modular configurations, are improving overall vessel performance and reducing operating costs. Digitalization is also emerging as a critical factor, with the integration of smart sensors, predictive maintenance, and real-time performance monitoring enabling optimized engine operations and reduced downtime.

"Oil tankers are expected to hold the second-largest share in the vessel segment during the forecast period."

This reflects the continued importance of crude oil and refined product transportation in global energy trade. Despite the gradual shift toward renewable energy, government and intergovernmental data indicate that oil will remain a key component of the global energy mix in the medium term, sustaining high volumes of seaborne oil trade. This sustained demand supports consistent demand for large tanker fleets, particularly very large crude carriers (VLCCs) and product tankers, which require high-capacity, durable marine engines. Additionally, aging tanker fleets are being replaced and retrofitted to meet stricter emissions regulations aligned with IMO standards, driving demand for advanced, fuel-efficient engines. Increased investments in offshore oil production, especially in the Middle East, Africa, and South America, are also supporting tanker utilization, reinforcing the segment's strong position in the marine engines market.

"Auxiliary engines are expected to rank second in the engine segment during the forecast period."

This is primarily due to their critical role in meeting onboard power requirements across all vessel types. Auxiliary engines are essential for operating navigation systems, cargo-handling equipment, lighting, safety systems, and hotel loads, making them fundamental regardless of vessel size or application. With steady growth in global shipping activity and increasing vessel complexity, demand for reliable onboard power systems continues to rise. Stricter environmental and energy-efficiency regulations are also encouraging the adoption of advanced auxiliary engines with lower emissions and improved fuel efficiency, including hybrid and dual-fuel configurations. Retrofitting existing fleets to meet compliance standards, along with rising investments in technologically advanced vessels, is further strengthening demand for auxiliary engines and securing their significant share of the market.

"Europe is expected to hold a significant position in the marine engines market during the forecast period."

Europe's marine engines market is largely driven by its strong, well-established maritime ecosystem, supported by consistent data from European government sources such as Eurostat and the European Commission. The region handles high volumes of maritime trade, with EU ports managing around 840 million tonnes of goods in a single quarter of 2025, underscoring the scale of shipping activity and the continuous demand for vessels and engines. Additionally, nearly 90% of the European Union's external freight trade is transported by sea, making shipping a critical backbone of the regional economy and ensuring steady demand for both new engines and retrofitting solutions. Europe also maintains one of the world's largest and most advanced shipping fleets, accounting for a significant share of global tonnage and specialized vessels such as LNG carriers and tankers, which require technologically advanced marine engines. Furthermore, the presence of approximately 150 major shipyards across the EU, focusing on high-value and technologically complex vessels, supports continuous engine demand through both new shipbuilding and refurbishment activities. Alongside this, strong regulatory frameworks promoting low-emission shipping and government-backed initiatives to modernize fleets and strengthen regional shipbuilding capabilities are accelerating the adoption of next-generation engines.

Breakdown of Primaries:

In-depth interviews with key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, were conducted to obtain and verify critical qualitative and quantitative information, as well as to assess future market prospects. The primary interviews were distributed as follows:

By Company Type: Tier 1 - 30%, Tier 2 - 55%, and Tier 3 -15%

By Designation: C-level -30%, D-level -20%, and Others -50%

By Region: North America - 18%, Europe - 8%, Asia Pacific - 60%, South America - 4%, and

Middle East & Africa - 10%

The marine engines market is predominantly governed by well-established global leaders. Notable players include Caterpillar (US), Wartsila (Finland), AB Volvo Penta (Sweden), Everllence (Germany), Rolls-Royce Plc (UK), Mitsubishi Heavy Industries, Ltd. (Japan), HDHyundai Heavy Industries Co., Ltd. (South Korea), Cummins Inc. (US), DAIHATSU INFINEARTH MFG. CO., LTD (Japan), and Deutz AG (Germany).

Research Coverage:

The report provides a comprehensive definition, description, and forecast of the marine engines market based on various parameters, including Engine (Propulsion and Auxiliary), Type (Four Stroke and Two Stroke), Power Range (<1,000 hp, 1,001-5,000 hp, 5,001-10,000 hp, 10,001-20,000 hp, and >20,000 hp), Fuel (Marine Diesel Oil, Others, Heavy Fuel Oil, and Marine Gas Oil), Vessel (Bulk Carrier, Oil Tankers, Offshore Support Vessels, General Cargo, Others, Container Ships, Tugs, and Product Tankers), and Region (Asia Pacific, North America, Europe, Middle East and Africa, South America). The report also offers a thorough qualitative and quantitative analysis of the marine engines market, encompassing a comprehensive examination of the key market drivers, limitations, opportunities, and challenges. Additionally, it covers critical facets of the market, such as an assessment of the competitive landscape, an analysis of market dynamics, value-based market estimates, and future trends in the marine engines market.

Key Benefits of Buying this Report

The report is thoughtfully designed to benefit both established industry leaders and newcomers in the marine engines market. It provides reliable revenue forecasts for the entire market as well as its individual sub-segments. This data is a valuable resource for stakeholders, enabling them to gain a comprehensive understanding of the competitive landscape and formulate effective market strategies for their businesses. Furthermore, the report serves as a channel for stakeholders to grasp the current state of the market, providing essential insights into market drivers, limitations, challenges, and growth opportunities. By incorporating these insights, stakeholders can make well-informed decisions and stay informed about the constantly evolving dynamics of the marine engines industry.

- Analysis of key drivers (rising seaborne trade, shipbuilding concentration and orderbook expansion in Asia, aging global fleet propelling replacement and retrofit demand), restraints (long lifecycle of marine engines limiting replacement demand, high capital cost), opportunities (transition to alternative fuels, digitalization and automation in marine industry), and challenges (uncertainty in future fuel adoption creating investment and technology risk, stringent and evolving emission regulations) influencing the growth of the market.

- Product Development/Innovation: The marine engines market is in a constant state of evolution, with a primary focus on product development and innovation. Leading industry players like Caterpillar, Wartsila, Everllence, and HD Hyundai Heavy Industries are at the forefront of advancing their product offerings to address shifting demands and environmental considerations.

- Market Development: The marine engines market is developing steadily as global shipping, energy transport, and naval activities continue to expand, supported by increasing demand for efficient and reliable propulsion systems. One of the key trends shaping market development is the strong shift toward cleaner and more fuel-efficient engines, driven by stricter environmental regulations and emission standards adopted by governments and international maritime bodies. As a result, manufacturers are focusing on developing engines that can run on alternative fuels such as LNG, methanol, and other low-carbon options, along with hybrid and electric technologies. At the same time, digital technologies are becoming more important, with ship operators using smart monitoring systems and predictive maintenance to improve engine performance and reduce downtime. The market is also seeing growth from fleet modernization and retrofitting activities, as older vessels are upgraded to meet new efficiency and compliance requirements. In addition, rising investments in shipbuilding, port infrastructure, offshore energy projects, and naval defense are further supporting the expansion of the marine engines market. Overall, the market is moving toward a more sustainable, technology-driven, and efficiency-focused future, with continuous innovation playing a key role in its development.

- Market Diversification: The marine engines market is going through significant diversification, driven by a combination of regulatory pressure, evolving fuel preferences, and changing vessel requirements across global shipping and offshore industries. One of the primary drivers is the tightening of emission norms by governments and international maritime authorities, which is pushing manufacturers and shipowners to move beyond conventional diesel engines toward a wider mix of solutions such as LNG, methanol, ammonia-ready, and hybrid-electric propulsion systems. At the same time, different vessel types-such as container ships, oil tankers, cruise ships, and offshore support vessels-have varied operational needs, leading to the development of specialized engine configurations tailored for efficiency, power output, and fuel flexibility. Growing uncertainty around future fuel standards is also encouraging engine makers to design dual-fuel and multi-fuel engines, allowing operators to switch between fuels based on availability and cost. In addition, increasing investments in naval defense, offshore energy, and inland waterways are expanding the range of applications for marine engines, further contributing to market diversification. Technological advancements, including digital monitoring systems and modular engine designs, are also enabling more customized and adaptable solutions. Overall, this diversification reflects the industry's transition toward a more flexible, sustainable, and application-specific engine ecosystem, where both environmental requirements and operational demands are shaping innovation.

- Competitive Assessment: A comprehensive evaluation has been conducted to scrutinize the market presence, growth strategies, and service offerings of key players in the marine engines market. These prominent companies include Caterpillar (US), Wartsila (Finland), Everllence (Germany), Rolls-Royce Plc (UK), HD Hyundai Heavy Industries Co., Ltd. (South Korea), AB Volvo Penta (Sweden), Mitsubishi Heavy Industries, Ltd. (Japan), Cummins Inc. (US), DAIHATSU INFINEARTH MFG. CO., LTD. (Japan), Deutz AG (Germany), and others. This analysis provides in-depth insights into the competitive positions of these major players, their approaches to driving market growth, and the range of services they offer within the marine engines segment.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MARINE ENGINES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MARINE ENGINES MARKET

- 3.2 MARINE ENGINES MARKET, BY REGION

- 3.3 MARINE ENGINES MARKET IN ASIA PACIFIC, BY ENGINE TYPE AND STROKE TYPE

- 3.4 MARINE ENGINES MARKET, BY ENGINE TYPE

- 3.5 MARINE ENGINES MARKET, BY STROKE TYPE

- 3.6 MARINE ENGINES MARKET, BY POWER RANGE

- 3.7 MARINE ENGINES MARKET, BY VESSEL TYPE

- 3.8 MARINE ENGINES MARKET, BY FUEL TYPE

- 3.9 MARINE ENGINES MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising seaborne trade

- 4.2.1.2 Shipbuilding concentration and order book expansion in Asia

- 4.2.1.3 Aging global fleet

- 4.2.2 RESTRAINTS

- 4.2.2.1 Reduced replacement frequency due to long lifecycle of marine engines

- 4.2.2.2 High cost of marine engines

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Transition to alternative fuels with strong focus on decarbonization

- 4.2.3.2 Digitalization and automation in marine industry

- 4.2.4 CHALLENGES

- 4.2.4.1 Investment dilemma due to uncertainty regarding long-term adoption of marine fuels

- 4.2.4.2 Stringent and evolving emission regulations

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 THREATS OF SUBSTITUTES

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN OVERALL MARINE ENGINES MARKET

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF MARINE ENGINES, BY POWER RANGE, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF MARINE ENGINES, BY REGION, 2022-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 840810)

- 5.6.2 EXPORT SCENARIO (HS CODE 840810)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 BISSO DEPLOYS 3516E TIER 4-COMPLIANT DIESEL ENGINE-POWERED ASD TRACTOR TUG TO REDUCE EMISSIONS

- 5.9.2 EDDA WIND CHOOSES CAT 3512E MARINE ENGINES FOR ITS SERVICE VESSELS TO IMPROVE FUEL EFFICIENCY

- 5.9.3 FINNLINES DEPLOYS HYBRID SYSTEM IN FERRIES TO REDUCE ENVIRONMENTAL FOOTPRINT

- 5.9.4 SEASPAN FERRIES INTEGRATES 34DF GREENHOUSE-GAS-REDUCTION SYSTEMS TO ACHIEVE DEEP DECARBONIZATION

- 5.10 IMPACT OF US TARIFF - MARINE ENGINES MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON VESSEL TYPES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 DUAL-FUEL ENGINE TECHNOLOGY (LNG, METHANOL, AMMONIA-READY)

- 6.1.2 ADVANCED COMBUSTION AND FUEL INJECTION SYSTEMS

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 EXHAUST GAS TREATMENT SYSTEMS (SCRUBBERS, SCR)

- 6.2.2 MARINE ENERGY STORAGE SYSTEMS (BATTERY AND HYBRID SOLUTIONS)

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 DIGITAL MONITORING AND PREDICTIVE MAINTENANCE (IOT AND DATA ANALYTICS)

- 6.3.2 ALTERNATIVE FUEL INFRASTRUCTURE (LNG, METHANOL, AMMONIA SUPPLY SYSTEMS)

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | EMISSION COMPLIANCE AND FUEL EFFICIENCY OPTIMIZATION

- 6.4.2 MID-TERM (2027-2030) | ALTERNATIVE FUELS AND HYBRIDIZATION EXPANSION

- 6.4.3 LONG-TERM (2030-2035+) | ZERO-EMISSION PROPULSION AND AUTONOMOUS MARINE POWER SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON MARINE ENGINES MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY OEMS IN MARINE ENGINES MARKET

- 6.7.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN MARINE ENGINES MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GEN AI/AI-INTEGRATED MARINE ENGINES

- 6.8 SUCCESS STORIES AND REAL-WORD APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF MARINE ENGINES MARKET

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING FRAMEWORKS, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS VESSEL TYPES

- 8.5 MARKET PROFITABILITY

9 MARINE ENGINES MARKET, BY STROKE TYPE

- 9.1 INTRODUCTION

- 9.2 TWO-STROKE

- 9.2.1 HIGH EFFICIENCY IN CONTINUOUS LONG-HAUL OPERATIONS TO DRIVE MARKET

- 9.3 FOUR-STROKE

- 9.3.1 OPERATIONAL FLEXIBILITY AND VERSATILITY ACROSS MULTIPLE VESSEL TYPES TO BOOST DEMAND

10 MARINE ENGINES MARKET, BY ENGINE TYPE

- 10.1 INTRODUCTION

- 10.2 PROPULSION

- 10.2.1 INCREASING VESSEL DEMAND AND EXPANSION OF MARITIME TRADE TO FUEL MARKET GROWTH

- 10.3 AUXILIARY

- 10.3.1 RISING DEMAND FOR ELECTRIFIED VESSEL SYSTEMS TO FACILITATE MARKET GROWTH

11 MARINE ENGINES MARKET, BY POWER RANGE

- 11.1 INTRODUCTION

- 11.2 UP TO 1,000 HP

- 11.2.1 GROWTH IN SMALL VESSEL AND INLAND WATERWAY ACTIVITIES TO DRIVE MARKET

- 11.3 1,001-5,000 HP

- 11.3.1 FOCUS ON COST-EFFICIENT AND COMPLIANT MARINE TRANSPORT TO STIMULATE DEMAND

- 11.4 5,001-10,000 HP

- 11.4.1 ABILITY TO SUPPORT CONTINUOUS OPERATIONS OVER LONG DISTANCES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 11.5 10,001-20,000 HP

- 11.5.1 EXPANSION OF GLOBAL TRADE AND ENERGY TRANSPORT TO SUPPORT SEGMENTAL GROWTH

- 11.6 ABOVE 20,000 HP

- 11.6.1 POTENTIAL TO HANDLE IMMENSE CARGO LOADS AND NAVIGATE VAST DISTANCES EFFICIENTLY TO ACCELERATE DEMAND

12 MARINE ENGINES MARKET, BY FUEL TYPE

- 12.1 INTRODUCTION

- 12.2 HEAVY FUEL OIL

- 12.2.1 STRINGENT EMISSION REGULATIONS TO REDUCE ADOPTION OF HEAVY FUEL OIL

- 12.3 MARINE DIESEL OIL

- 12.3.1 COMPLIANCE WITH EMISSION STANDARDS AND OPERATIONAL FLEXIBILITY TO DRIVE DEMAND

- 12.4 MARINE GAS OIL

- 12.4.1 STRINGENT SULFUR REGULATIONS TO BOOST ADOPTION

- 12.5 OTHER FUEL TYPES

13 MARINE ENGINES MARKET, BY VESSEL TYPE

- 13.1 INTRODUCTION

- 13.2 OFFSHORE SUPPORT VESSELS

- 13.2.1 EXPANSION OF OFFSHORE OIL, GAS, AND WIND ACTIVITIES TO DRIVE MARKET

- 13.3 OIL TANKERS

- 13.3.1 LONG-HAUL CRUDE TRANSPORTATION AND REFINING IMBALANCES TO FACILITATE ADOPTION

- 13.4 BULK CARRIERS

- 13.4.1 LONG-HAUL MOVEMENT OF RAW MATERIALS FROM RESOURCE-RICH REGIONS TO MANUFACTURING HUBS TO SUPPORT MARKET GROWTH

- 13.5 GENERAL CARGO SHIPS

- 13.5.1 CONTINUED SHIFT TOWARD CONTAINERIZED SHIPPING TO REDUCE DEMAND FOR GENERAL CARGO SHIPS

- 13.6 CONTAINER SHIPS

- 13.6.1 EXPANSION OF CONTAINERIZED TRADE AND SUPPLY CHAIN INTEGRATION TO CREATE GROWTH OPPORTUNITIES

- 13.7 PRODUCT TANKERS

- 13.7.1 INCREASING SEABORNE TRADE OF REFINED PRODUCTS TO PROMOTE SEGMENTAL GROWTH

- 13.8 TUGS

- 13.8.1 GROWTH IN PORT ACTIVITY AND VESSEL SIZES TO DRIVE MARKET

- 13.9 OTHER VESSEL TYPES

14 MARINE ENGINES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 ASIA PACIFIC

- 14.2.1 CHINA

- 14.2.1.1 Export-oriented vessel production to accelerate market growth

- 14.2.2 JAPAN

- 14.2.2.1 Commitment to green shipping under government-backed programs to support market growth

- 14.2.3 SOUTH KOREA

- 14.2.3.1 Strong focus on high-value shipbuilding to create grow opportunities

- 14.2.4 PHILIPPINES

- 14.2.4.1 Government support for green shipping and digitalization to drive the market

- 14.2.5 VIETNAM

- 14.2.5.1 Strategic coastline, export-oriented economy, and growing role in regional logistics to support market growth

- 14.2.6 REST OF ASIA PACIFIC

- 14.2.1 CHINA

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Maritime decarbonization policies and green fuel transition to propel market

- 14.3.2 ITALY

- 14.3.2.1 Increasing investment in hydrogen-powered vessels to fuel market growth

- 14.3.3 RUSSIA

- 14.3.3.1 Increasing investment in port infrastructure and shipyard modernization to drive market

- 14.3.4 FINLAND

- 14.3.4.1 Emphasis on green shipping corridors to reduce emissions and promote eco-friendly transport to facilitate market growth

- 14.3.5 FRANCE

- 14.3.5.1 Strategic fleet modernization initiatives to elevate demand

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 NORTH AMERICA

- 14.4.1 US

- 14.4.1.1 High adoption of hybrid propulsion and battery-electric systems to accelerate market growth

- 14.4.2 CANADA

- 14.4.2.1 Green shipping corridors, clean fuel standards, and port sustainability initiatives to fuel market growth

- 14.4.3 MEXICO

- 14.4.3.1 Greater emphasis on improving sustainability and fleet efficiency to create growth opportunities

- 14.4.1 US

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.5.1.1 UAE

- 14.5.1.1.1 Heavy investment in smart ports, free trade zones, and maritime industrial clusters to support market growth

- 14.5.1.2 Rest of GCC

- 14.5.1.1 UAE

- 14.5.2 TURKEY

- 14.5.2.1 Heavy investments in defense shipbuilding to facilitate market growth

- 14.5.3 SOUTH AFRICA

- 14.5.3.1 Ongoing port modernization, dredging activities, and logistics upgrades to boost demand

- 14.5.4 EGYPT

- 14.5.4.1 Offshore energy projects and port development initiatives to contribute to market growth

- 14.5.5 REST OF MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.6 SOUTH AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 Significant focus on strengthening naval procurement and shipbuilding capacity to create market growth potential

- 14.6.2 ARGENTINA

- 14.6.2.1 Strategic Atlantic access and vast inland trade corridors to create potential for market expansion

- 14.6.3 REST OF SOUTH AMERICA

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 REVENUE ANALYSIS, 2021-2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Region footprint

- 15.5.5.2 Fuel type Footprint

- 15.5.5.3 Power range footprint

- 15.5.5.4 Engine type footprint

- 15.5.5.5 Stroke type footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of startups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 BRAND/PRODUCT COMPARISON

- 15.8.1 CATERPILLAR (US)

- 15.8.2 WARTSILA (FINLAND)

- 15.8.3 EVERLLENCE (GERMANY)

- 15.8.4 HD HYUNDAI HEAVY INDUSTRIES (SOUTH KOREA)

- 15.8.5 ROLLS-ROYCE PLC (UK)

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 CATERPILLAR

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 WARTSILA

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 EVERLLENCE

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 ROLLS-ROYCE PLC

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 HD HYUNDAI HEAVY INDUSTRIES

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.3.2 Deals

- 16.1.5.3.3 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 AB VOLVO PENTA

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches

- 16.1.6.3.2 Deals

- 16.1.6.3.3 Expansions

- 16.1.7 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Other developments

- 16.1.8 CUMMINS INC.

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.8.3.2 Deals

- 16.1.8.3.3 Other developments

- 16.1.9 DAIHATSU INFINEARTH MFG. CO., LTD.

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.9.3.2 Deals

- 16.1.10 DEUTZ AG

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.11 FAIRBANKS MORSE DEFENSE

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.11.3.2 Deals

- 16.1.11.3.3 Other developments

- 16.1.12 WABTEC CORPORATION

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Developments

- 16.1.13 YANMAR MARINE INTERNATIONAL

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Product launches

- 16.1.13.3.2 Deals

- 16.1.14 ISOTTA FRASCHINI MOTORI S.P.A.

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.15 SOCIETE INTERNATIONALE DES MOTEURS BAUDOUIN

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.1 CATERPILLAR

- 16.2 OTHER PLAYERS

- 16.2.1 CNPC JICHAI POWER COMPANY LIMITED

- 16.2.2 MAHINDRA POWEROL

- 16.2.3 IHI POWER SYSTEMS CO., LTD.

- 16.2.4 WEICHAI HOLDING GROUP CO., LTD.

- 16.2.5 AGCO POWER

- 16.2.6 KAWASAKI HEAVY INDUSTRIES, LTD.

- 16.2.7 SCANIA

- 16.2.8 COOPER CORP.

- 16.2.9 ANGLO BELGIAN CORPORATION NV

- 16.2.10 STX ENGINE

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of key secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 List of primary interview participants

- 17.1.2.3 Key industry insights

- 17.1.2.4 Breakdown of primary interviews

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 17.3.1 DEMAND-SIDE ANALYSIS

- 17.3.1.1 Demand-side assumptions

- 17.3.1.2 Demand-side calculations

- 17.3.2 SUPPLY-SIDE ANALYSIS

- 17.3.2.1 Supply-side assumptions

- 17.3.2.2 Supply-side calculations

- 17.3.1 DEMAND-SIDE ANALYSIS

- 17.4 MARKET FORECAST APPROACH

- 17.4.1 SUPPLY SIDE

- 17.4.2 DEMAND SIDE

- 17.5 DATA TRIANGULATION

- 17.6 FACTOR ANALYSIS

- 17.7 RESEARCH ASSUMPTIONS AND LIMITATIONS

- 17.8 RISK ANALYSIS

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS