|

시장보고서

상품코드

2048956

실리콘 엘라스토머 시장 : 유형별, 프로세스별, 최종 이용 산업별, 지역별 - 세계 예측(-2031년)Silicone Elastomers Market By Type, By Process, By End-use Industry, and Region - Global Forecast to 2031 |

||||||

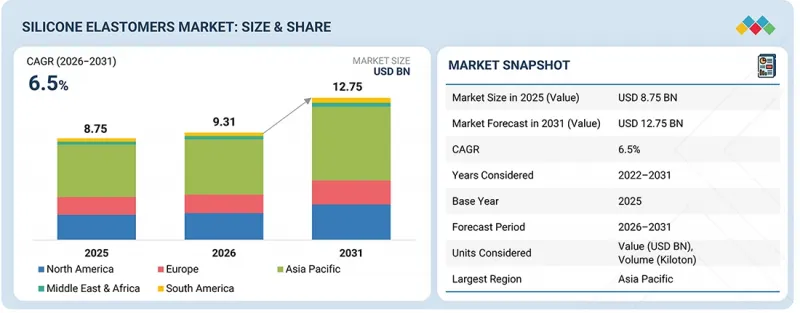

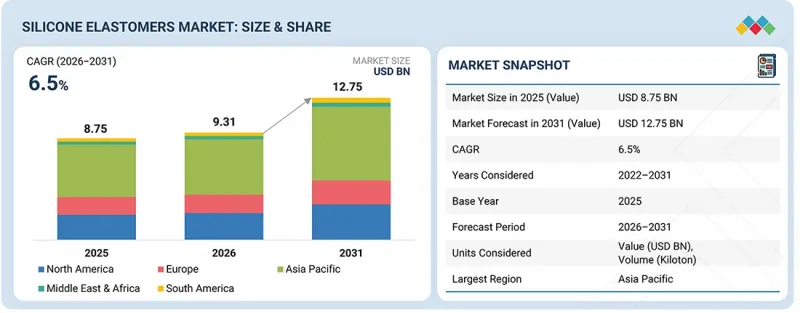

실리콘 엘라스토머 시장 규모는 2026년 93억 1,000만 달러에서 2031년까지 127억 5,000만 달러로 성장하여 이 기간 CAGR은 6.5%에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(10억 달러)/수량(1,000톤) |

| 부문 | 유형별, 프로세스별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미 |

실리콘 엘라스토머 시장은 자동차 및 운송 부문의 수요 증가에 의해 주도되고 있습니다. 이 부문에서는 개스킷, 씰, 진동 흡수 부품에서 높은 열 안정성, 유연성, 내구성이 필수적인 요소로 여겨지고 있습니다.

"상온가황(RTV) 부문은 예측 기간 동안 두 번째로 큰 시장 규모가 될 것으로 예상됩니다."

유형별로는 실온 가황(RTV) 부문이 낮은 경화 온도(경화 시)와 시공의 용이성으로 인해 예측 기간 동안 실리콘 엘라스토머 시장에서 두 번째 점유율을 차지할 것으로 예상됩니다. 상온 가황 실리콘 엘라스토머는 우수한 접착력, 탄력성 및 우수한 밀봉성으로 인해 건설, 전자, 자동차 및 일반 산업 분야의 수많은 응용 분야에서 일반적으로 사용되고 있습니다. 이들은 실란트, 접착제, 코팅제, 포팅 컴파운드 등의 용도에 매우 효과적인 재료이며, 현장에서 경화 및 가공이 용이하다는 장점이 있습니다. 또한, 이러한 실리콘 엘라스토머는 습기, 내후성, 내후성 및 많은 화학제품에 대한 높은 내성을 가지고 있어 실내 및 실외 환경 모두에서 사용할 수 있습니다. 또한, 다른 종류의 실리콘 엘라스토머에 비해 상온 가황형 실리콘 엘라스토머의 취급 및 사용이 용이하기 때문에 전체 실리콘 엘라스토머 시장은 앞으로도 강력하고 건전한 성장 추세를 이어갈 것으로 예상됩니다.

"예측 기간 동안 액체 사출 성형 부문이 가장 큰 부문이 될 것으로 예상됩니다."

공정별로 보면 실리콘 엘라스토머 시장에서 액체 사출 성형 부문이 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예상됩니다. 이 공정은 높은 효율성과 정밀도를 제공할 뿐만 아니라 복잡한 형상의 부품을 높은 생산량 수준에서 일관성과 품질을 유지하면서 생산할 수 있는 능력을 갖추고 있습니다. 액체 사출 성형은 빠른 가공 속도, 재료 손실 감소, 자동화에 대한 적응성 등의 장점으로 인해 의료, 자동차, 전기 및 전자 등 많은 산업 분야에서 채택되고 있습니다. 제조업체는 매우 엄격한 공차를 충족하는 복잡한 실리콘 엘라스토머 부품을 생산할 수 있어 의료기기(예 : 의료기기용 씰 및 커넥터) 및 전자 제품에서 유용하게 사용할 수 있습니다. 또한, 이 공정을 통해 제조업체는 높은 재현성(제품의 균일성)을 유지하면서 대량 생산을 할 수 있습니다. 액체 사출 성형이 고성능 액체 실리콘 고무 재료를 가공할 수 있는 능력은 그 응용 범위를 확장하고 있습니다.

"예측 기간 동안 소비재 최종 사용 산업은 두 번째 부문이 될 것으로 예상됩니다."

용도별로는 예측 기간 동안 소비재 부문이 두 번째로 큰 점유율을 차지할 것으로 예상됩니다. 실리콘 엘라스토머는 무독성, 고온에 대한 내성, 장기적으로 안정적인 성능으로 인해 모든 소비자 응용 분야에서 선호되고 있습니다. 대표적인 용도로는 베이비 케어 제품, 주방 용품, 전자기기 액세서리, 웨어러블 기기 등이 있으며, 이 분야에서는 장기간의 편안함과 신뢰성이 중요한 고려 사항입니다. 고품질, 내구성, 안전성을 갖춘 소비재에 대한 수요 증가가 이 부문의 성장에 기여하고 있습니다. 또한 도시화, 라이프스타일의 변화, 고급 소비재에 대한 지출 증가도 시장 규모 확대에 기여하고 있습니다. 혁신적인 제품 설계를 가능하게 하고 사용자 경험을 향상시키는 실리콘 엘라스토머의 다재다능함은 세계 실리콘 엘라스토머 시장에서 이 부문의 2위 자리를 굳건히 지켜나갈 것입니다.

"예측 기간 동안 유럽은 두 번째로 큰 시장 규모가 될 것으로 예상됩니다."

지역별로 보면 유럽은 자동차, 헬스케어, 전자제품 제조 산업이 발달한 유럽은 예측 기간 동안 실리콘 엘라스토머 시장에서 두 번째로 큰 점유율을 차지할 것으로 예상됩니다. 독일, 프랑스, 이탈리아가 주요 기여국이며, 자동차, 의료, 산업용 고성능 소재에 대한 수요가 성장을 주도하고 있습니다. EU의 엄격한 제품 안전, 에너지 효율 및 환경 지속가능성에 대한 요구 사항도 우수한 실리콘 엘라스토머의 사용을 촉진하는 원동력이 되고 있습니다. 의료기술에 대한 투자 확대와 헬스케어 분야에서의 생체적합성 소재 활용 확대도 수요 증가에 기여하고 있습니다. 지속적인 혁신과 연구 개발 노력, 그리고 지속가능한 소재 개발로 유럽은 세계 2위의 실리콘 엘라스토머 시장으로서의 입지를 더욱 공고히 하고 있습니다.

대상 기업 : Dow Inc.(미국), Wacker Chemie AG(독일), KCC Corporation(한국), Shin-Etsu Chemical(일본), China National Bluestar(Group)(중국), Rogers Corporation(미국), Cabot Corporation(미국), Reiss Manufacturing Inc. 미국), Cabot Corporation(미국), Reiss Manufacturing Inc.(미국), Mesgo S.p.A.(이탈리아), CHT Germany GmbH(독일) 등이 본 보고서의 대상입니다.

실리콘 엘라스토머 시장의 주요 기업들에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시하였습니다.

조사 범위

실리콘 엘라스토머 시장을 유형별(고온 가황, 상온 가황, 액상 실리콘 고무), 제조 공정별(압출 성형, 액상 사출 성형, 사출 성형, 압축 성형, 기타 공정), 최종 이용 산업별(자동차-운송, 전기 및 전자, 헬스케어, 소비재, 건축 및 건설, 발포체, 기타 최종 이용 산업), 지역별(아시아, 아메리카, 유럽, 중동 및 아프리카) 등으로 분류하여 조사했습니다. 성형체, 기타 최종 이용 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류하고 있습니다. 이 보고서의 범위에는 실리콘 엘라스토머 시장의 성장에 영향을 미치는 촉진요인, 제약 조건, 과제 및 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 제품 및 실리콘 엘라스토머 시장과 관련된 파트너십, 제휴, 제품 출시, 사업 확장, 인수 등의 주요 전략에 대한 인사이트를 제공합니다. 본 보고서는 실리콘 엘라스토머 시장 생태계의 신생 스타트업 기업의 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 실리콘 엘라스토머 시장 전체 및 각 하위 부문의 매출에 대한 가장 정확한 추정치를 시장 리더와 신규 진입 기업에게 제공합니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 위한 인사이트를 강화하며, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

주요 촉진요인(고령화로 인한 의료 산업 수요 증가, 전기 및 전자산업에서 실리콘 엘라스토머의 높은 수요, 실리콘 엘라스토머의 우수한 특성), 제약요인(환경문제 및 지속가능성 문제, 선진국의 성장 둔화), 기회요인(의료 산업용 항균성 실리콘 엘라스토머, 자동차 수요 증가), 도전과제(원자재 가격의 변동) 분석

- 제품 개발/혁신 : 실리콘 엘라스토머 시장의 미래 기술, R&D 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 실리콘 엘라스토머 시장을 분석합니다.

시장 다각화 : 실리콘 엘라스토머 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : Dow Inc.(미국), Wacker Chemie AG(독일), KCC Corporation(한국), Shin-Etsu Chemical(일본), China National Bluestar(Group)(중국), Rogers Corporation(미국), Cabot Corporation(미국), Reiss Manufacturing Inc. 미국), Cabot Corporation(미국), Reiss Manufacturing Inc.(미국), Mesgo S.p.A.(이탈리아), CHT Germany GmbH(독일) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 실리콘 엘라스토머 시장(유형별)

제10장 실리콘 엘라스토머 시장(프로세스별)

제11장 실리콘 엘라스토머 시장(용도별)

제12장 실리콘 엘라스토머 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.08The silicone elastomers market is projected to grow from USD 9.31 billion in 2026 to USD 12.75 billion by 2031, registering a CAGR of 6.5% during this period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) / Volume (Kiloton) |

| Segments | Type, Process, End-Use Industry and Region |

| Regions covered | Type, Process, End-Use Industry and Region |

The silicone elastomers market is driven by rising demand from the automotive and transportation sector, where their high thermal stability, flexibility, and durability are essential for gaskets, seals, and vibration-dampening components.

"The room temperature vulcanized segment is projected to be the second-largest segment during the forecast period."

By type, the room temperature vulcanized segment is expected to account for the second-largest share during the forecast period in the silicone elastomers market due to their low curing temperature (for curing) and simplicity when applied. Room temperature vulcanized silicone elastomers are typically used in numerous applications within the construction, electronics, automotive, and general industrial fields because of their superior adhesive properties, elasticity, and ability to provide good sealing. They are very effective materials for applications such as sealants, adhesives, coatings, and potting compounds, all of which benefit from their ability to cure on-site and be easily processed. These silicone elastomers are also highly resistant to moisture, weathering, and many chemicals, allowing for their use in both indoor and outdoor environments. Additionally, the simplicity of working with and using room temperature vulcanized silicone elastomers as compared to the other categories of silicone elastomers will continue to create a strong and healthy growth trend in the overall silicone elastomers market.

"The liquid injection molding segment is projected to be the largest segment during the forecast period."

By process, the liquid injection molding segment is expected to account for the largest share during the forecast period in the silicone elastomers market. This process provides greater efficiency and precision, along with the capabilities to create complex geometric parts with consistency and quality at high volume levels. Liquid injection molding is used by many industries, including healthcare, automotive, and electrical/electronics, as it offers advantages like speed of processing, lower material waste, and suitability for automation. Manufacturers can produce intricate silicone elastomer components with very tight tolerances, making them useful in medical devices (e.g., seals/connectors for medical devices) and electronic products. In addition, this process offers manufacturers the ability to produce in large volumes with high repeatability (consistency of product). The ability of liquid injection molding to process high-performance liquid silicone rubber materials expands the range of applications. The

"The consumer goods end-use industry is projected to be the second-largest segment during the forecast period."

By end-use industry, the consumer goods segment is expected to account for the second-largest share during the forecast period. Silicone elastomers are desirable for all consumer applications since they are non-toxic, can withstand high temperatures, and offer performance consistency over time. Typical applications include baby care, kitchen utensils, electronic accessories, and wearable devices, where comfort over long periods of time and reliability are significant considerations. The increase in demand for high-quality, durable and safe consumer products is contributing to the growth of this segment. Additionally, urbanization, shifting lifestyles and increased spending on premium consumer products are all contributing to an increase in market size. The versatility of silicone elastomers to enable innovative product designs and enhance the user experience will continue to solidify this segment's second-largest position as a contributor to the global silicone elastomer market.

"Europe is projected to be the second-largest market during the forecast period."

By region, Europe is expected to account for the second-largest share during the forecast period in the silicone elastomers market due to the presence of strong automotive, healthcare, and electronic manufacturing industries. Germany, France, and Italy are the main contributors, where growth is being driven by the demand for high-performing materials in automotive, medical, and industrial applications. The strict product safety, energy efficiency and environmental sustainability requirements imposed by the EU have also been a driving force in promoting the use of superior silicone elastomers. The growing investment in medical technologies and the greater use of biocompatible materials in healthcare are also contributing to an increase in demand. Ongoing innovation and research and development initiatives, as well as the continued development of sustainable materials, are further strengthening Europe's position as the second-largest regional silicone elastomer market in the world.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Dow Inc. (US), Wacker Chemie AG (Germany), KCC Corporation (South Korea), Shin-Etsu Chemical Co., Ltd. (Japan), China National Bluestar (Group) Co., Ltd. (China), Rogers Corporation (US), Cabot Corporation (US), Reiss Manufacturing Inc. (US), Mesgo S.p.A. (Italy), and CHT Germany GmbH (Germany), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the silicone elastomers market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the silicone elastomers market by type (High-temperature vulcanized, room temperature vulcanized, liquid silicone rubber), by process (Extrusion, liquid injection molding, injection molding, compression molding, other processes), by end-use industry (Automotive & Transportation, electrical & electronics, healthcare, consumer goods, building & construction, foams, other end-use industries), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the silicone elastomers market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the silicone elastomers market. This report covers a competitive analysis of upcoming startups in the silicone elastomers market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall silicone elastomers market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (Aging population fueling demand from healthcare industry, High demand for silicone elastomers in electrical & electronics industry, Superior properties of silicone elastomers), restraints (Environmental concerns and sustainability challenges, Stagnant growth in developed countries), opportunities (Antimicrobial silicone elastomers for healthcare industry, Increasing demand for automobiles), and challenges (Fluctuating raw material prices)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the silicone elastomers market

- Market Development: Comprehensive information about profitable markets - the report analyzes the silicone elastomers market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the silicone elastomers market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Dow Inc. (US), Wacker Chemie AG (Germany), KCC Corporation (South Korea), Shin-Etsu Chemical Co., Ltd. (Japan), China National Bluestar (Group) Co., Ltd. (China), Rogers Corporation (US), Cabot Corporation (US), Reiss Manufacturing Inc. (US), Mesgo S.p.A. (Italy), and CHT Germany GmbH (Germany).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 MARKET DEFINITION AND INCLUSIONS, BY PROCESS

- 1.3.4 MARKET DEFINITION AND INCLUSIONS, BY END-USE INDUSTRY

- 1.3.5 YEARS CONSIDERED

- 1.3.6 CURRENCY CONSIDERED

- 1.3.7 UNIT CONSIDERED

- 1.3.8 STAKEHOLDERS

- 1.4 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SILICONE ELASTOMERS MARKET

- 3.2 SILICONE ELASTOMERS MARKET, BY TYPE AND END-USE INDUSTRY

- 3.3 SILICONE ELASTOMERS MARKET, BY END-USE INDUSTRY

- 3.4 SILICONE ELASTOMERS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Aging population fueling demand from healthcare industry

- 4.2.1.2 High demand for silicone elastomers in electrical & electronics industry

- 4.2.1.3 Superior properties of silicone elastomers

- 4.2.2 RESTRAINTS

- 4.2.2.1 Environmental concerns and sustainability challenges

- 4.2.2.2 Stagnant growth in developed countries

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Antimicrobial silicone elastomers for healthcare industry

- 4.2.3.2 Increasing demand for automobiles

- 4.2.4 CHALLENGES

- 4.2.4.1 Fluctuating raw material prices

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN SILICONE ELASTOMERS MARKET

- 4.3.1.1 COST-EFFECTIVE RECYCLABLE AND LOW-CARBON SILICONE ELASTOMERS WITHOUT PERFORMANCE LOSS

- 4.3.1.2 High-purity silicone elastomers for long-term implantable medical devices

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Ultra-high thermally conductive silicone elastomers for EVS and AI data centers

- 4.3.2.2 Silicone elastomers with self-healing and smart-sensing capabilities

- 4.3.1 UNMET NEEDS IN SILICONE ELASTOMERS MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.3 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.4.4 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES' ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA RELATED TO HS CODE 3910, BY COUNTRY, 2021-2025 (USD THOUSAND)

- 5.6.2 EXPORT DATA RELATED TO HS CODE 3910, BY COUNTRY, 2021-2025 (USD THOUSAND)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY OF DOW, INC.

- 5.10.2 CASE STUDY OF WACKER CHEMIE AG

- 5.11 IMPACT OF 2025 US TARIFFS ON SILICONE ELASTOMERS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 KEY IMPACT ON VARIOUS REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SILICONE ELASTOMER NANOCOMPOSITES TECHNOLOGY

- 6.1.2 ADJACENT TECHNOLOGIES

- 6.1.2.1 Liquid silicone rubber 3D printing technology

- 6.1.2.2 Silicone in flexible medical dressing technology

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2025-2027) | PERFORMANCE OPTIMIZATION & APPLICATION ENGINEERING PHASE

- 6.2.2 MID-TERM (2027-2030) | MULTIFUNCTIONAL MATERIAL INTEGRATION PHASE

- 6.2.3 LONG-TERM (2030-2035+) | INTELLIGENT & CIRCULAR SILICONE SYSTEMS PHASE

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 ADAPTIVE THERMAL SILICONE NETWORKS FOR AI DATA CENTERS

- 6.4.2 BIOELECTRONIC SILICONE INTERFACES FOR NEURAL COMMUNICATION

- 6.4.3 SELF-HEALING SILICONE ELASTOMERS FOR AUTONOMOUS MOBILITY SYSTEMS

- 6.5 IMPACT OF AI/GENERATIVE AI ON SILICONE ELASTOMERS MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN SILICONE ELASTOMERS

- 6.5.3 CASE STUDIES OF AI IMPLEMENTATION IN SILICONE ELASTOMERS MARKET

- 6.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN SILICONE ELASTOMERS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF SILICONE ELASTOMERS

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF SILICONE ELASTOMERS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 SILICONE ELASTOMERS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 HIGH-TEMPERATURE VULCANIZED/HIGH-CONSISTENCY RUBBER

- 9.2.1 FLAME RETARDANCE, OIL RESISTANCE, AND EXTREME TEMPERATURE RESISTANCE PROPERTIES TO DRIVE MARKET

- 9.3 ROOM-TEMPERATURE VULCANIZED

- 9.3.1 FLEXIBILITY IN MOLDING, EASY WORKABILITY, AND STABILITY TO DRIVE MARKET

- 9.4 LIQUID SILICONE RUBBER

- 9.4.1 BIOCOMPATIBILITY, EASY PROCESSING, AND FLEXIBILITY TO DRIVE MARKET

- 9.4.2 INDUSTRIAL-GRADE LIQUID SILICONE RUBBER

- 9.4.2.1 Growing population and purchasing power to drive market

- 9.4.3 MEDICAL-GRADE LIQUID SILICONE RUBBER

- 9.4.3.1 Stringent regulations regarding health & safety to drive market

- 9.4.4 FOOD-GRADE LIQUID SILICONE RUBBER

- 9.4.4.1 Growing industrial base for food and rapid urbanization to drive market

10 SILICONE ELASTOMERS MARKET, BY PROCESS

- 10.1 INTRODUCTION

- 10.2 EXTRUSION

- 10.2.1 CONTINUOUS SILICONE EXTRUSION SUPPORTS HIGH PRECISION MANUFACTURING ACROSS ADVANCED INDUSTRIAL APPLICATIONS

- 10.3 LIQUID INJECTION MOLDING

- 10.3.1 LIQUID INJECTION MOLDING ACCELERATES HIGH-PRECISION SILICONE COMPONENT MANUFACTURING ACROSS CRITICAL INDUSTRIES

- 10.4 INJECTION MOLDING

- 10.4.1 HIGH-PRESSURE SILICONE INJECTION MOLDING ENHANCES COMPLEX COMPONENT MANUFACTURING CAPABILITIES

- 10.5 COMPRESSION MOLDING

- 10.5.1 COMPRESSION MOLDING MAINTAINS STRATEGIC IMPORTANCE FOR LARGE DURABLE SILICONE INDUSTRIAL COMPONENTS

- 10.6 OTHER PROCESSES

11 SILICONE ELASTOMERS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 AUTOMOTIVE & TRANSPORTATION

- 11.2.1 BATTERY CENTRIC THERMAL SEALING ARCHITECTURE IS RESHAPING SILICONE DEMAND IN AUTOMOTIVE SYSTEMS

- 11.3 ELECTRICAL & ELECTRONICS

- 11.3.1 ADVANCED ELECTRONICS EXPANSION IS DRIVING SILICONE ELASTOMERS INTO SEMICONDUCTOR GRADE PROTECTION SYSTEMS

- 11.4 HEALTHCARE

- 11.4.1 MEDICAL-GRADE SILICONE SYSTEMS ARE REDEFINING DEVICE SAFETY AND BIOCOMPATIBILITY STANDARDS IN HEALTHCARE

- 11.5 CONSUMER GOODS

- 11.5.1 RISING HYGIENE AND LIFESTYLE PRODUCT DEMAND ACCELERATING ADOPTION IN CONSUMER GOODS

- 11.6 BUILDING & CONSTRUCTION

- 11.6.1 FIRE SAFETY AND INFRASTRUCTURE DURABILITY REQUIREMENTS ACCELERATING ADOPTION IN BUILDING SYSTEMS

- 11.7 FOAM

- 11.7.1 SILICONE FOAM TECHNOLOGIES ENABLE ADVANCED THERMAL AND FIRE PROTECTION IN CRITICAL INDUSTRIAL ENVIRONMENTS

- 11.8 OTHER END-USE INDUSTRIES

12 SILICONE ELASTOMERS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Growing automotive healthcare and construction activities accelerating silicone elastomer demand

- 12.2.2 CANADA

- 12.2.2.1 Growing automotive digital infrastructure and healthcare investments driving demand

- 12.2.3 MEXICO

- 12.2.3.1 Expanding automotive exports and infrastructure investments increasing demand

- 12.2.1 US

- 12.3 ASIA PACIFIC

- 12.3.1 CHINA

- 12.3.1.1 Expanding automotive and high technology industries accelerating demand

- 12.3.2 INDIA

- 12.3.2.1 Expanding automotive electronics and industrial investments accelerating demand

- 12.3.3 JAPAN

- 12.3.3.1 Advanced automotive semiconductor and infrastructure investments strengthening demand

- 12.3.4 SOUTH KOREA

- 12.3.4.1 Expanding automotive exports and semiconductor dominance strengthening demand

- 12.3.5 INDONESIA

- 12.3.5.1 Export-led mobility growth and domestic consumption reinforcing demand

- 12.3.6 REST OF ASIA PACIFIC

- 12.3.1 CHINA

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Electric mobility expansion and precision manufacturing accelerating demand

- 12.4.2 FRANCE

- 12.4.2.1 Electric vehicle localization and medical technology expansion driving demand

- 12.4.3 UK

- 12.4.3.1 Electric mobility expansion and infrastructure modernization strengthening demand

- 12.4.4 ITALY

- 12.4.4.1 Automotive component exports and medical technology demand supporting growth

- 12.4.5 SPAIN

- 12.4.5.1 Rising electric vehicle production and industrial modernization increasing demand

- 12.4.6 TURKEY

- 12.4.6.1 Electric vehicle adoption and industrial export growth accelerating demand

- 12.4.7 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.2 SAUDI ARABIA

- 12.5.2.1 Accelerating infrastructure and industrial diversification strengthening demand

- 12.5.3 UAE

- 12.5.3.1 Liquidity strength and urban infrastructure scaling, accelerating demand

- 12.5.4 REST OF GCC COUNTRIES

- 12.5.5 SOUTH AFRICA

- 12.5.5.1 Expanding automotive and infrastructure growth increases demand

- 12.5.6 REST OF MIDDLE EAST & AFRICA

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Industrial expansion and electronics growth accelerate demand

- 12.6.2 ARGENTINA

- 12.6.2.1 Expanding industrial recovery and infrastructure revival strengthen silicone elastomers demand

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 BRAND COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Type footprint

- 13.6.5.4 Process footprint

- 13.6.5.5 End-use industry footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2026

- 13.7.5.1 List of key startups/SMEs

- 13.7.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.8.1 COMPANY VALUATION

- 13.9 FINANCIAL METRICS

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES

- 13.10.2 DEALS

- 13.10.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 DOW, INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weakness and competitive threats

- 14.1.2 WACKER CHEMIE AG

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 KCC CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weakness and competitive threats

- 14.1.4 SHIN-ETSU CHEMICAL CO., LTD.

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weakness and competitive threats

- 14.1.5 CHINA NATIONAL BLUESTAR (GROUP) CO., LTD.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weakness and competitive threats

- 14.1.6 ROGERS CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.3.2 Expansions

- 14.1.6.4 MnM view

- 14.1.7 CABOT CORPORATION

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 MnM view

- 14.1.8 REISS MANUFACTURING INC.

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 MnM view

- 14.1.9 MESGO S.P.A.

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 MnM view

- 14.1.10 CHT GERMANY GMBH

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 MnM view

- 14.1.11 BELLOFRAM ELASTOMERS

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 MnM view

- 14.1.12 AB SPECIALTY SILICONES LLC

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.12.3 MnM view

- 14.1.13 SPECIALTY SILICONE PRODUCTS INC.

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.13.3 MnM view

- 14.1.14 STOCKWELL ELASTOMERICS, INC.

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.14.3 MnM view

- 14.1.1 DOW, INC.

- 14.2 OTHER PLAYERS

- 14.2.1 AVANTOR, INC.

- 14.2.2 SILICONE SOLUTIONS, INC.

- 14.2.3 ZHEJIANG XINAN CHEMICAL INDUSTRIAL GROUP CO., LTD. (CHINA)

- 14.2.4 RAVAGO PETROKIMYA URETIM A.S.

- 14.2.5 SHENZHEN HONG JIE YI TECHNOLOGY CO., LTD.

- 14.2.6 JIANGSHAN SUNOIT PERFORMANCE MATERIAL SCIENCE CO.,

- 14.2.7 POLYSIL SILICONE MATERIAL CO., LTD.

- 14.2.8 SHANGHAI RICH CHEMICAL NEW MATERIAL CO., LTD.

- 14.2.9 NANO TECH CHEMICAL BROTHERS CO., LTD.

- 14.2.10 SHENZHEN YIJIASAN SILICONE CO., LTD.

- 14.2.11 SHENZHEN GENVAN SILICONE MATERIALS CO., LTD.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 DEMAND-SIDE APPROACH

- 15.3.2 SUPPLY-SIDE APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS