|

시장보고서

상품코드

2050382

방사성동위원소 식별 장치 시장 : 기술별, 용도별, 최종사용자별 - 세계 예측(-2031년)Radioisotope Identification Devices Market by Technology, Application, End User - Global Forecast to 2031 |

||||||

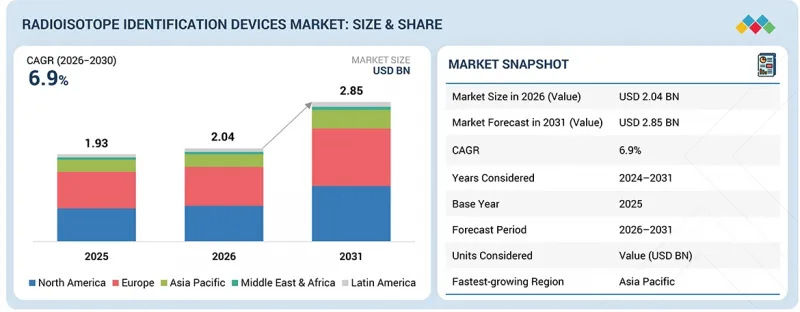

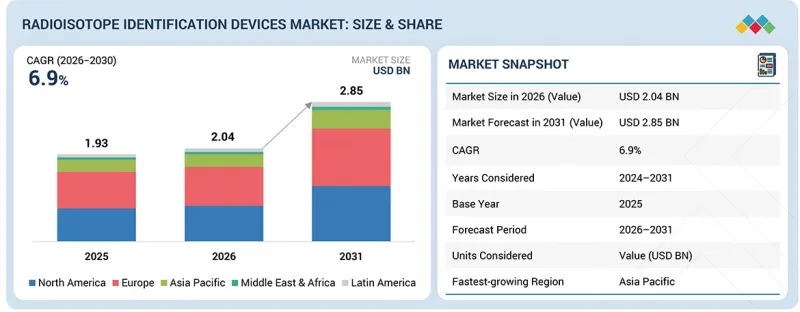

세계의 방사성동위원소 식별 장치 시장 규모는 2025년 19억 3,000만 달러에서 2031년에는 28억 5,000만 달러에 달할 것으로 예측되며, 2026년부터 2031년까지 CAGR은 6.9%를 기록할 전망입니다.

방사성동위원소 식별 장치 시장은 세계 핵안보 강화와 방사성 물질의 부정거래 증가를 배경으로 성장하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2025-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(달러) |

| 부문 | 제품 유형, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

각국 정부는 특히 국경 관리, 화물 검사, 테러 대응의 효율성을 높이기 위해 방사선 탐지에 도움이 되는 첨단 기술에 많은 투자를 하고 있습니다. RIID(방사성동위원소 식별 장치)는 방사성 물질을 신속하고 정확하게 식별하는 데 사용되기 때문에 가정과 법집행기관의 안전 확보, 방사성 물질 관련 사고에 대한 긴급 대응에 매우 중요한 역할을 하고 있습니다.

제품 유형별로는 분광형 개인용 방사선 검출기 부문이 예측 기간 동안 가장 높은 CAGR을 보일 것으로 예상됩니다.

제품 유형별로 살펴보면, SPRD(분광형 개인용 방사선 검출기)는 방사선을 감지할 뿐만 아니라 특정 동위원소를 정확하게 식별할 수 있는 고급 기능을 갖추고 있어 보안, 방위, 비상 대응 분야에서 그 중요성이 점점 더 커지고 있어 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. 기존의 개인용 방사선 검출기와 달리 SPRD는 고해상도 스펙트럼 분석을 제공하여 사용자가 안전한 방사성 물질과 위협적인 방사성 물질을 구분할 수 있도록 하여 오경보를 크게 줄입니다. 핵 테러, 불법 거래, CBRN(화학, 생물학, 방사성 물질, 핵) 위협에 대한 우려가 높아지면서 보다 정확하고 신뢰할 수 있는 식별 도구에 대한 수요가 증가하고 있습니다. 또한, 검출기 재료(CdZnTe, LaBr3 등)의 발전, 소형화, AI를 활용한 분석 기술로 인해 SPRD는 더욱 휴대성이 뛰어나고, 사용하기 쉽고, 현장 배치에 있어 효율적입니다. 국토안보 및 국방 기관의 규제 요건 강화와 현대화 프로그램의 진전은 이러한 고성능 장치의 빠른 보급을 더욱 촉진하고 있으며, 이에 따라 견조한 성장이 예상됩니다.

용도별로는 국토안보 및 국경 보안 부문이 예측 기간 동안 가장 높은 CAGR을 보일 것으로 예상됩니다.

핵물질 밀수, 방사선 테러, 방사성 물질의 불법 거래에 대한 우려가 높아지면서 각국 정부는 국경, 항만, 공항에서의 감시 및 탐지 능력을 강화해야 하며, 국토안보 및 국경 보안 부문이 가장 높은 CAGR을 기록할 것으로 예상됩니다. 지정학적 긴장의 고조와 다층적인 보안 인프라의 필요성으로 인해 RIID, 포털 모니터, 통합 스크리닝 시스템 등 첨단 방사선 탐지 기술에 대한 막대한 투자가 이루어지고 있습니다. 또한, 국제원자력기구(IAEA)와 같은 국제기구의 국제적인 의무와 가이드라인에 따라 각국은 방사선 모니터링 및 컴플라이언스 체계를 강화해야 합니다. 국경 보안 시스템의 지속적인 현대화와 더불어 AI를 활용한 네트워크 연결 감지 솔루션의 도입으로 수요가 더욱 가속화되고 있으며, 이로 인해 국토안보 및 국경 보안은 시장에서 가장 빠르게 성장하고 있는 분야로 부상하고 있습니다.

최종사용자별로는 정부 및 방위 기관 부문이 2025년 가장 큰 시장 점유율을 차지했습니다.

국방 및 국토안보 분야의 높은 수준과 지속적인 예산이 RIID의 광범위한 활용을 촉진하고 있습니다. 정부 및 국방 기관의 장기적인 RIID 조달을 통해 공항, 항만 및 국경 전역에 RIID의 견고한 기반이 구축되었습니다. 또한, 밀수를 통한 핵물질의 불법 운송에 대한 전 세계적인 우려와 방사성 대량살상무기의 위협이 증가함에 따라 국내 및 국제적으로 엄격한 법 집행이 요구되고 있습니다. 이는 이 부문의 견고하고 지속적인 수요를 지속적으로 견인할 것으로 보입니다.

예측 기간 동안 아시아태평양은 시장에서 가장 높은 성장률을 기록할 것으로 예상됩니다.

아시아태평양은 급속한 산업화, 원자력 에너지 계획의 확대, 국토안보 및 방사선 안전 인프라에 대한 투자 증가로 인해 시장에서 가장 높은 성장률을 보일 것으로 예상됩니다. 중국, 인도, 일본 등의 국가는 원자력 역량 및 규제 프레임워크 강화에 적극 나서고 있으며, 첨단 방사선 탐지 및 동위원소 식별 시스템의 필요성을 높이고 있습니다. 또한, 의료 분야에서의 핵의학 및 방사성의약품의 채택 확대도 시장 확대에 기여하고 있습니다. 방사선 위협에 대한 인식이 높아진 데다 국경 보안과 환경 모니터링을 강화하려는 정부의 노력으로 인해 아시아태평양은 세계에서 가장 빠르게 성장하는 시장으로 RIID의 도입이 가속화되고 있습니다.

세계의 방사성동위원소 식별 장치 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 방사성동위원소 식별 장치 시장 : 제품 유형별

제10장 방사성동위원소 식별 장치 시장 : 용도별

제11장 방사성동위원소 식별 장치 시장 : 최종사용자별

제12장 방사성동위원소 식별 장치 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.08The global radioisotope identification devices market is projected to reach USD 2.85 billion by 2031 from USD 1.93 billion in 2025, at a CAGR of 6.9% from 2026 to 2031. The radioisotope identification devices market is growing due to a global increase in nuclear security and the trafficking of radioactive materials.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product Type, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Governments in particular are investing significantly in advanced technologies that help with radiation detection to make border control, cargo screening, and countering terrorism more effective. As RIIDs are used to quickly and accurately identify radioactive materials, they are crucial for providing security for homes, law enforcement agencies, and for emergency response to incidents involving radiological materials.

By product type, the spectroscopic personal radiation detectors segment is expected to register the highest CAGR during the forecast period.

By product type, the radioisotope identification devices market is segmented into personal radiation detectors, handheld personal radiation detectors, radioisotope identification devices, fixed radiation monitoring systems, spectroscopic personal radiation detectors, and other products. Spectroscopic personal radiation detectors (SPRDs) are expected to register the highest CAGR in the market due to their advanced capability to not only detect radiation but also accurately identify specific isotopes, which is increasingly critical for security, defense, and emergency response applications. Unlike conventional personal radiation detectors, SPRDs provide high-resolution spectral analysis, enabling users to distinguish between benign and threatening radioactive sources, thereby significantly reducing false alarms. Growing concerns around nuclear terrorism, illicit trafficking, and CBRN threats are driving demand for more precise and reliable identification tools. Additionally, advancements in detector materials (such as CdZnTe and LaBr3), miniaturization, and AI-enabled analytics are making SPRDs more portable, user-friendly, and efficient for field deployment. Increasing regulatory requirements and modernization programs across homeland security and defense agencies further support the rapid adoption of these high-performance devices, resulting in their strong projected growth.

By application, the homeland security & border protection segment is projected to register the highest CAGR during the forecast period.

The homeland security & border protection segment is expected to witness the highest CAGR in the radioisotope identification devices (RIID) market due to escalating concerns over nuclear smuggling, radiological terrorism, and illicit trafficking of radioactive materials, which are driving governments to strengthen surveillance and detection capabilities at borders, ports, and airports. Increasing geopolitical tensions and the need for multi-layered security infrastructure are prompting significant investments in advanced radiation detection technologies, including RIIDs, portal monitors, and integrated screening systems. Additionally, international mandates and guidelines from organizations such as the International Atomic Energy Agency (IAEA) are pushing countries to enhance radiation monitoring and compliance frameworks. Continuous modernization of border security systems, coupled with the adoption of AI-enabled and networked detection solutions, is further accelerating demand, making homeland security and border protection the fastest-growing application segment in the market.

By end user, the government & defense agencies segment accounted for the highest market share in 2025.

The government & defense agencies segment accounted for the largest share in the radioisotope identification devices (RIIDs) market in 2025. High and sustained budgets for both defense and homeland security are driving the widespread use of RIIDs. Long-term procurement of RIIDs by government and defense agency customers has created a robust base of RIIDs throughout airports, seaports, and borders. Moreover, increasing global concerns about the illegal transport of nuclear material through smuggling and the increasing threat of radiological weapons of mass destruction have led to strict enforcement mandates (both domestically and internationally). This will continue to fuel strong and consistent demand from this segment.

Asia Pacific is expected to register the highest growth rate in the market during the forecast period.

Asia Pacific is expected to witness the highest growth rate in the radioisotope identification devices (RIIDs) market due to rapid industrialization, expanding nuclear energy programs, and increasing investments in homeland security and radiation safety infrastructure. Countries such as China, India, and Japan are actively strengthening their nuclear capabilities and regulatory frameworks, driving the need for advanced radiation detection and isotope identification systems. Additionally, the growing adoption of nuclear medicine and radiopharmaceuticals in the healthcare sector is further supporting market expansion. Rising awareness of radiological threats, coupled with government initiatives to enhance border security and environmental monitoring, is accelerating the deployment of RIIDs across the region, making Asia Pacific the fastest-growing market globally.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: C-level Executives (55%), Directors (27%), and Others (18%)

- By Region: North America (35%), Europe (32%), Asia Pacific (25%), Latin America (6%), and the Middle East & Africa (2%)

The prominent players in this market are AMETEK (US), ARKTIS Radiation Detectors (Switzerland), ATOMTEX (Belarus), Bertin Instruments (France), BNC (USA), Fortive (US), H3D (US), Hitachi (Japan), Kromek Group (UK), Landauer (US), Ludlum Measurements (USA), Mirion Technologies (US), Nucsafe (South Korea), Polimaster (Belarus), Radiation Detection Company (US), Rapiscan (US), RSI (US), Smiths Detection (UK), Symetrica (UK), Teledyne FLIR Defense (US), and Thermo Fisher Scientific (US), among others.

Research Coverage

The radioisotope identification devices market is segmented by product type, application, end user, and region. The report reviews the leading companies competing in the radioisotope identification devices market. A micro-level analysis can be conducted to examine trends, growth opportunities, and contributions to the market. Additionally, it highlights potential revenue growth opportunities across various market segments in five major regions.

Key Benefits of Buying the Report

The report is valuable for new entrants in the radioisotope identification devices market as it provides comprehensive information about the market. This information is essential for understanding various investment opportunities. The report provides insights into both key and smaller players in the market, which can help create a solid basis for risk analysis when making investment decisions. It accurately segments the market by end users and regions, providing focused insights into specific market segments. Additionally, the report highlights key trends, challenges, growth drivers, and opportunities to support strategic decision-making through a thorough analysis.

The report provides insights into the following points:

- Key drivers (Rising nuclear security threats and illicit trafficking of radioactive materials, Increasing government spending on homeland security and defense), restraints (High cost of advanced RIIDs and spectroscopic technologies, Stringent regulatory approvals and compliance requirements), opportunities (Expansion of nuclear energy programs in emerging economies, Growing adoption of nuclear medicine and radiopharmaceuticals), and challenges (Technical limitations in detecting mixed or low-intensity isotopes, Shortage of skilled professionals to operate advanced RIIDs)

- Product Development/Innovation: Emerging technologies in space, R&D, recent product launches & approvals in the radioisotope identification devices market

- Market Growth: In-depth insights into the radioisotope identification devices market across varied geographies

- Market Diversification: Detailed analysis of new products, unexplored geographies, latest trends, and investments in the radioisotope identification devices market

- Competitive Assessment: Detailed assessment of market share, service offerings, leading strategies of major players such as Mirion Technologies (US), Nucsafe (South Korea), Polimaster (Belarus), Radiation Detection Company (US), Rapiscan (US), RSI (US), Smiths Detection (UK), Symetrica (UK), Teledyne FLIR Defense (US), and Thermo Fisher Scientific (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STUDY LIMITATIONS

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN RADIOISOTOPE IDENTIFICATION DEVICES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN RADIOISOTOPE IDENTIFICATION DEVICES MARKET

- 3.2 RADIOISOTOPE IDENTIFICATION DEVICES MARKET IN NORTH AMERICA, BY COUNTRY AND PRODUCT TYPE, 2025

- 3.3 GEOGRAPHIC SNAPSHOT OF RADIOISOTOPE IDENTIFICATION DEVICES MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising nuclear security threats and illicit trafficking of radioactive materials

- 4.2.1.2 Increasing government spending on homeland security

- 4.2.1.3 Technological advancements in detection materials, embedded electronics, and spectroscopic algorithms

- 4.2.1.4 Increasing defense modernization programs globally

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of advanced RIIDs and spectroscopic technologies

- 4.2.2.2 Stringent regulatory approvals and compliance requirements

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing adoption of nuclear medicines and radiopharmaceuticals

- 4.2.3.2 Expansion of nuclear energy programs in emerging economies

- 4.2.3.3 Integration of RIIDs into AI and IoT connectivity frameworks and distributed sensor network architecture

- 4.2.4 CHALLENGES

- 4.2.4.1 Technical limitations in detecting mixed or low-intensity isotopes

- 4.2.4.2 Shortage of skilled professionals to operate advanced RIIDs

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF BUYERS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL RADIATION INDUSTRY

- 5.2.4 TRENDS IN GLOBAL RADIOISOTOPE IDENTIFICATION DEVICES INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 PRICING RANGE OF RADIOISOTOPE IDENTIFICATION PRODUCT TYPES, BY KEY PLAYER, 2025

- 5.6.2 PRICING TREND OF RADIOISOTOPE IDENTIFICATION PRODUCT TYPES, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 2844)

- 5.7.2 EXPORT SCENARIO (HS CODE 2844)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 STRENGTHENING DOMESTIC MEDICAL RADIONUCLIDE SUPPLY THROUGH COLLABORATIVE INNOVATION

- 5.11.2 ADVANCING PORTABLE RADIATION DETECTION FOR NUCLEAR SECURITY APPLICATIONS

- 5.11.3 ENABLING LARGE-SCALE MEDICAL RADIOISOTOPE PRODUCTION THROUGH ADVANCED SHIELDING INFRASTRUCTURE

- 5.12 IMPACT OF US TARIFF - RADIOISOTOPE IDENTIFICATION DEVICES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 KEY TARIFF RATES

- 5.12.4 PRICE IMPACT ANALYSIS

- 5.12.5 IMPACT ON COUNTRIES/REGIONS

- 5.12.5.1 US

- 5.12.5.2 Europe

- 5.12.5.3 Asia Pacific

- 5.12.6 IMPACT ON END USERS

- 5.13 KEY SALES OPPORTUNITY AREAS FOR TELEDYNE GLOBALLY (2025)

- 5.13.1 WHITE SPACE OPPORTUNITIES

- 5.13.2 REVENUE HOT SPOTS

- 5.13.3 HIGH-GROWTH SALES POCKETS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 CADMIUM ZINC TELLURIDE (CZT) DETECTOR

- 6.1.2 LANTHANUM BBROMIDE (LABR3) SCINTILLATION

- 6.1.3 HYBRID GAMMA-NEUTRON DETECTION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 RADIATION PORTAL MONITORS (RPMS)

- 6.2.2 RADIATION MAPPING AND DATA ANALYTICS PLATFORMS

- 6.3 PATENT ANALYSIS

- 6.4 IMPACT OF AI ON RADIOISOTOPE IDENTIFICATION DEVICES MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN RADIOISOTOPE IDENTIFICATION DEVICES MARKET

- 6.4.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN RADIOISOTOPE IDENTIFICATION DEVICES MARKET

- 6.4.4 INTERCONNECTED/ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED RADIOISOTOPE IDENTIFICATION DEVICES

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS END USERS

9 RADIOISOTOPE IDENTIFICATION DEVICES MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 PERSONAL RADIATION DETECTORS

- 9.2.1 INCREASING INVESTMENTS IN HOMELAND SECURITY INFRASTRUCTURE TO BOOST DEMAND

- 9.3 HANDHELD PERSONAL RADIATION DETECTORS

- 9.3.1 SHIFT FROM BELT-WORN MONITORS TO INTELLIGENT AND COST-EFFECTIVE HANDHELD RADIATION INTERDICTION TOOLS TO DRIVE SEGMENTAL GROWTH

- 9.4 RADIOISOTOPE IDENTIFICATION DEVICES

- 9.4.1 ABILITY TO ANALYZE FULL GAMMA-RAY ENERGY SPECTRUM FOR ISOTOPE IDENTIFICATION TO ACCELERATE ADOPTION

- 9.5 FIXED RADIATION MONITORING SYSTEMS

- 9.5.1 GROWING FOCUS ON NUCLEAR SAFETY, RADIOACTIVE WASTE MANAGEMENT, AND CRITICAL INFRASTRUCTURE PROTECTION TO STIMULATE DEMAND

- 9.6 SPECTROSCOPIC PERSONAL RADIATION DETECTORS

- 9.6.1 HIGH EMPHASIS ON HOMELAND SECURITY AND CRITICAL INFRASTRUCTURE PROTECTION TO SUPPORT SEGMENTAL GROWTH

- 9.7 OTHER PRODUCTS

10 RADIOISOTOPE IDENTIFICATION DEVICES MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 HOMELAND SECURITY & BORDER PROTECTION

- 10.2.1 CONTINUED INVESTMENTS IN RADIOLOGICAL SURVEILLANCE AND HOMELAND SECURITY MODERNIZATION INITIATIVES TO PROPEL MARKET

- 10.3 NUCLEAR POWER PLANTS & FUEL CYCLE FACILITIES

- 10.3.1 RAPID EXPANSION OF NUCLEAR ENERGY INFRASTRUCTURE TO FACILITATE MARKET GROWTH

- 10.4 MEDICAL & HEALTHCARE

- 10.4.1 GROWING ADOPTION OF ADVANCED DIAGNOSTIC IMAGING AND THERAPEUTIC RADIOPHARMACEUTICALS TO CONTRIBUTE TO MARKET GROWTH

- 10.5 ENVIRONMENTAL MONITORING & RADIATION SAFETY

- 10.5.1 RISING ENVIRONMENTAL RADIATION SURVEILLANCE AND NORM MONITORING ACTIVITIES TO SPUR DEMAND

- 10.6 INDUSTRIAL APPLICATIONS

- 10.6.1 ADVANCEMENTS IN CONNECTED RADIATION MONITORING INFRASTRUCTURE TO SPIKE DEMAND

- 10.7 CBRN MISSION USERS

- 10.7.1 STRINGENT MILITARY PERFORMANCE REQUIREMENTS AND RUGGEDIZED OPERATIONAL STANDARDS TO SUPPORT MARKET GROWTH

- 10.8 OTHER APPLICATIONS

11 RADIOISOTOPE IDENTIFICATION DEVICES MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 GOVERNMENT & DEFENSE AGENCIES

- 11.2.1 LARGE-SCALE RADIOLOGICAL PREPAREDNESS AND COUNTERTERRORISM PROGRAMS TO ELEVATE DEMAND

- 11.3 NUCLEAR FACILITIES

- 11.3.1 EXPANSION OF NUCLEAR POWER INFRASTRUCTURE TO CREATE GROWTH OPPORTUNITIES

- 11.4 HOSPITALS & DIAGNOSTIC CENTERS

- 11.4.1 INCREASING USE OF RADIOACTIVE ISOTOPES IN ONCOLOGY, CARDIOLOGY, NEUROLOGY, AND TARGETED ALPHA THERAPY TO FUEL MARKET GROWTH

- 11.5 RESEARCH INSTITUTES & UNIVERSITIES

- 11.5.1 SURGING USE OF RIID IN ENVIRONMENTAL MONITORING, ISOTOPE ANALYSIS, FACULTY-LED SCIENTIFIC STUDIES TO FOSTER MARKET GROWTH

- 11.6 INDUSTRIAL FACILITIES

- 11.6.1 TIGHTENING INTERNATIONAL RADIATION SAFETY REGULATIONS TO LEAD TO HIGH DEMAND FOR RIIDS

- 11.7 OTHER END USERS

12 RADIOISOTOPE IDENTIFICATION DEVICES MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Inclination toward advanced technology-driven alternatives in radiation management to drive demand

- 12.2.2 CANADA

- 12.2.2.1 Border security, environmental monitoring, and health physics applications to contribute to market growth

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Ongoing dismantling of multiple reactor sites to accelerate demand

- 12.3.2 UK

- 12.3.2.1 Major nuclear new-built projects and ongoing nuclear decommissioning activities to create lucrative opportunities

- 12.3.3 FRANCE

- 12.3.3.1 Expansion of nuclear ecosystem to fuel demand

- 12.3.4 ITALY

- 12.3.4.1 Nuclear policy shifts and port security initiatives to foster market growth

- 12.3.5 SPAIN

- 12.3.5.1 Strong focus on strengthening security posture through defense and technology modernization programs to propel market

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 JAPAN

- 12.4.1.1 World-leading nuclear medicine ecosystem to offer growth avenues

- 12.4.2 CHINA

- 12.4.2.1 Heavy investments by government agencies in radiation safety and security systems to accelerate market growth

- 12.4.3 INDIA

- 12.4.3.1 Long-term nuclear energy expansion roadmap to support market growth

- 12.4.4 AUSTRALIA

- 12.4.4.1 Pressing need to identify and intercept illicit trafficking of radioactive and nuclear materials to spur demand

- 12.4.5 SOUTH KOREA

- 12.4.5.1 Nuclear export leadership to strengthen market growth

- 12.4.6 REST OF ASIA PACIFIC

- 12.4.1 JAPAN

- 12.5 LATIN AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 Emphasis on innovation in nuclear medicine to expedite adoption

- 12.5.2 MEXICO

- 12.5.2.1 Cross-border security requirements to support market growth

- 12.5.3 REST OF LATIN AMERICA

- 12.5.1 BRAZIL

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GCC

- 12.6.1.1 Large-scale industrial radiation monitoring needs to facilitate adoption

- 12.6.2 REST OF MIDDLE EAST & AFRICA

- 12.6.1 GCC

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Product type footprint

- 13.5.5.4 Application footprint

- 13.5.5.5 End user footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of startups/SMEs

- 13.7 COMPANY VALUATION AND FINANCIAL METRICS

- 13.7.1 COMPANY VALUATION

- 13.7.2 FINANCIAL METRICS

- 13.8 BRAND COMPARISON

- 13.8.1 THERMO FISHER SCIENTIFIC INC. (US)

- 13.8.2 TELEDYNE FLIR (US)

- 13.8.3 AMETEK, INC. (US)

- 13.8.4 MIRION TECHNOLOGIES, INC. (US)

- 13.8.5 KROMEK GROUP PLC (UK)

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 MIRION TECHNOLOGIES INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths/Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 THERMO FISHER SCIENTIFIC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths/Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 TELEDYNE FLIR

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Key strengths/Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses and competitive threats

- 14.1.4 AMETEK, INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches & approvals

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 ARKTIS RADIATION DETECTORS LTD.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Developments

- 14.1.6 ATOMTEX SPE

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.7 BERTIN INSTRUMENTS (BERTIN TECHNOLOGIES GROUP)

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.7.3.2 Other developments

- 14.1.8 BERKELEY NUCLEONICS CORPORATION (BNC)

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Developments

- 14.1.9 H3D INC.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Developments

- 14.1.10 HITACHI, LTD.

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.11 KROMEK GROUP PLC

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches & approvals

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Other developments

- 14.1.11.4 MnM view

- 14.1.11.4.1 Key strengths/Right to win

- 14.1.11.4.2 Strategic choices

- 14.1.11.4.3 Weaknesses and competitive threats

- 14.1.12 LANDAUER (A FORTIVE COMPANY)

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Developments

- 14.1.13 LUDLUM MEASUREMENTS, INC.

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Deals

- 14.1.14 RAPISCAN

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Deals

- 14.1.14.3.2 Other developments

- 14.1.15 POLIMASTER

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Developments

- 14.1.16 RADIATION DETECTION COMPANY (RDC)

- 14.1.16.1 Business overview

- 14.1.16.2 Products offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Deals

- 14.1.16.3.2 Other developments

- 14.1.17 RADIATION SOLUTIONS INC.

- 14.1.17.1 Business overview

- 14.1.17.2 Products offered

- 14.1.17.3 Recent developments

- 14.1.17.3.1 Deals

- 14.1.1 MIRION TECHNOLOGIES INC.

- 14.2 OTHER PLAYERS

- 14.2.1 SMITHS DETECTION (SMITHS GROUP PLC)

- 14.2.2 SYMETRICA LIMITED

- 14.2.3 BUBBLE TECHNOLOGY INDUSTRIES

- 14.2.4 NUCTECH

- 14.2.5 PHDS CO.

- 14.2.6 BALTIC SCIENTIFIC INSTRUMENTS

- 14.2.7 ECOTEST GROUP

- 14.2.8 VNIIA ROSATOM INSTRUMENTS

- 14.2.9 LAURUS SYSTEMS

- 14.2.10 NUCLEONIX

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key sources of secondary data

- 15.1.1.2 Objectives of secondary research

- 15.1.1.3 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key primary sources

- 15.1.2.2 Key objectives of primary research

- 15.1.2.3 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH (REVENUE SHARE ANALYSIS)

- 15.2.1.1 Company revenue estimation approach

- 15.2.1.2 Customer-based market estimation

- 15.2.2 TOP-DOWN APPROACH

- 15.2.1 BOTTOM-UP APPROACH (REVENUE SHARE ANALYSIS)

- 15.3 DATA TRIANGULATION

- 15.4 MARKET SHARE ASSESSMENT

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.7 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS