|

시장보고서

상품코드

2057476

헬스케어 IT 시장 : 솔루션별, 서비스별, 최종사용자별(병원, 외래 수술 센터, 약국, 보험 지불자) - 세계 예측(-2030년)Healthcare IT Market by Solution, Service, End User (Hospital, ASC, Pharmacy, Payer) - Global Forecast to 2030 |

||||||

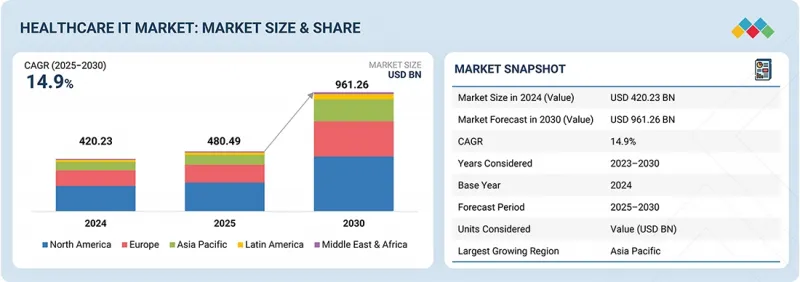

세계의 헬스케어 IT 시장 규모는 2025년 4,804억 9,000만 달러에서 2030년에는 9,612억 6,000만 달러에 달할 것으로 예측되며, 2025년부터 2030년까지 CAGR은 14.9%를 기록할 전망입니다.

기술 혁신 솔루션의 광범위한 도입이 헬스케어 IT 시장의 성장을 가속화하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 솔루션·서비스, 구성요소, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

2024년 8월 'Healthcare'지에 실린 기사에 따르면, AI를 활용한 임상의사결정지원시스템은 종양 전문의가 근거에 기반한 치료법을 선택할 때 이를 지원하고 있습니다. AI 도입으로 진단 정확도가 10-15% 향상된 것으로 밝혀졌습니다. 또한, 전자건강기록(EHR)의 도입 확대가 데이터 접근성을 향상시켜, 첨단 헬스케어 IT 솔루션에 대한 수요를 견인하고 있습니다.

"원격의료 솔루션 부문은 임상 헬스케어 IT 시장에서 가장 큰 부문이 될 것으로 전망됩니다."

임상 HCIT의 분석에 따르면, 원격의료 솔루션은 일시적이고 제한적인 의료 서비스에 그치지 않고, 현재는 주류 의료 제공 모델의 일부로 자리 잡아가고 있으며, 예측 기간 동안 주요 부문이 될 것으로 전망됩니다. 세계보건기구(WHO)가 제창한 'Global Strategy on Digital Health(2020-2025)'를 비롯해, "Slaintecare Action Plan', "HSE Corporate Plan', "Healthy Ireland Actions' 등 디지털 헬스 관련 정부 주도 정책들이, 특히 지역 의료, 만성 질환 관리, 케어 패스웨이 분야에서의 원격의료 솔루션 도입을 뒷받침하고 있습니다. 또한 고령화가 진행됨에 따라, 여러 가지 동반 질환을 앓기 쉬운 고령자에 대한 간병 부담이 커지고 있습니다. 이러한 환자들에게는 지속적인 관리가 필요하기 때문에 원격의료 솔루션의 도입이 전반적으로 확대되고 있으며, 의료 시스템이 인력 부족, 비용 증가, 의료 제공 능력 부족과 같은 과제에 직면한 가운데, 이 분야는 앞으로도 꾸준한 성장이 기대됩니다.

"최종사용자별로는 의료 제공자 부문이 2024년에 가장 큰 규모를 기록했습니다."

의료 제공자는 인력 확보라는 과제를 안고 있음에도 불구하고, 디지털화된 맞춤형 의료 서비스에 대한 높은 수요에 부응해야 합니다. 동시에 의료 시스템은 환자 유치, 적극적인 치료 참여, 지역 사회에 대한 기여를 촉진하기 위해 노력하고 있습니다. 또한, 재정적으로 지속가능한 가치 기반의 의료 서비스와 집단건강관리라는 장기적인 비전을 달성하기 위해서는, 환자와 직원의 경험을 개선하는 동시에 의료 제공자가 본연의 업무인 '의료 서비스'에 집중할 수 있도록 지원하는 의료 정보 기술 솔루션이 필요합니다. 이러한 이유로, 환자 치료를 개선하면서 업무 효율을 높이는 헬스케어 IT 솔루션에 대한 수요가 증가하고 있습니다.

"예측 기간 동안 아시아태평양이 가장 높은 성장률을 기록할 것으로 전망됩니다."

아시아태평양 시장의 성장은 주로 의료 인프라 개선, 기술 솔루션 도입, HCIT 솔루션 도입을 위한 정부의 노력과 같은 요인들에 의해 주도되고 있습니다. 예를 들어 인도에서는 병원 인증 기관인 National Accreditation Board for Hospitals(NABH)가 병원 정보 시스템(HIS) 및 전자 진료 기록(EMR)에 관한 기준과 지침을 마련함에 따라, 헬스케어 IT 솔루션에 대한 수요가 크게 증가하고 있습니다. 병원 정보 시스템(HIS) 및 전자 진료 기록(EMR)에 관한 기준과 지침을 수립하기 위한 국립병원인증위원회(NABH)의 최근 움직임이 헬스케어 기술 솔루션에 대한 수요를 크게 견인하고 있습니다. 2023년 9월에 도입된 이 디지털 헬스 기준에 대해 이미 275개 병원이 인증을 신청했으며, 그중 100개 병원이 인증을 획득했습니다. 이러한 규제 및 제도적 지원은 헬스케어 IT 시장의 성장을 촉진할 뿐만 아니라, 첨단 디지털 인프라를 활용한 의료 제공 체계를 구축함으로써 인도 의료 서비스 전반의 고도화에도 기여할 것으로 기대됩니다.

본 보고서에서는 전 세계 헬스케어 IT 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추정 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 종합적으로 다루고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 디스럽션

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 헬스케어 IT 시장 : 솔루션·서비스별

제10장 헬스케어 IT 시장 : 구성요소별

제11장 헬스케어 IT 시장 : 최종사용자별

제12장 헬스케어 IT 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.19The global Healthcare IT market is projected to reach 961.26 billion by 2030 from 480.49 billion in 2025, at a CAGR of 14.9% from 2025 to 2030. The widespread adoption of technology advancement solutions is accelerating the growth of the healthcare IT market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Solution & Service, Component, and End-user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East Africa. |

According to the Healthcare article published in August 2024, AI-powered clinical decision support systems assist oncologists by making evidence-based therapy recommendations. It was found that AI helped in improving the dignaostics accuracy by 10-15%. Moreover, increased adoptions of EHRs improve data accessibility and drive the demand for advanced healthcare IT solutions.

"The telehealth solutions segment is projected to be the largest segment in the clinical healthcare IT market"

On the basis of Clinical HCIT, Telehealth Solutions are poised to remain the leading segment over the forecast period, as these solutions become an integral part of mainstream care delivery models, apart from being confined to episodic care. Government-backed initiatives related to Digital Healthcare, including the Global Strategy on Digital Health (2020-2025) proposed by the World Health Organization, the "Slaintecare Action Plan, HSE Corporate Plan, and Healthy Ireland actions," are propelling the adoption of Telehealth Solutions, especially within Community Consultations, Chronic Care, and Care Pathways. The rising Geriatric Population, which puts more care intensity, as these people are often prone to multiple morbidities, increases the overall adoption of Telehealth Solutions, as these patients require continued care, placing this segment firmly on a growth path over the forecast period, as Healthcare Systems are challenged by capacity, costs, and talent deficits.

"Healthcare Providers was the largest segment by the end user of healthcare IT market in 2024"

Healthcare providers segment is projected to grow at the highest growth rate in the healthcare IT market in 2024. Providers face high demand for digitized, personalized service with staffing challenges. At the same time, health systems strive to advance patient acquisition, proactive care engagement and commitments to their communities. Achieving long-term visions for financially sustainable value-based care and population health management requires healthcare information technology solutions that can improve the patient and employee experience while allowing providers to focus on what they do best care. Thus, there is a rising demand for healthcare IT solutions to improve patient care while increasing operational efficiency.

"APAC to witness the highest growth rate during the forecast period."

In this report, the healthcare IT market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East and Africa. The healthcare IT market in APAC is projected to register the highest CAGR rate during the forecast period. The growth in the APAC market is mainly driven by factors such as the improving healthcare infrastructure, adoption of technology solutions and government initiatives for the adoption of HCIT solutions. For instance, the recent initiatives by the National Accreditation Board for Hospitals (NABH) to establish standards and guidelines for Hospital Information Systems (HIS) and Electronic Medical Records (EMR) are significantly driving the demand for healthcare technology solutions in India. Launched in September 2023, these digital health standards have already seen 275 hospitals apply for certification, with 100 achieving it. This regulatory push is not only fostering a robust market for healthcare IT solutions but also positioning India to enhance its healthcare delivery through advanced digital infrastructure.

The break-down of primary participants is as mentioned below:

- By Company Type - Tier 1: 45%, Tier 2: 35%, and Tier 3: 20%

- By Designation - C-level: 35%, Director-level: 25%, and Others: 40%

- By Region - North America: 45%, Europe: 30%, Asia Pacific: 20%, Latin America: 3%, and Middle East & Africa: 2%.

Optum, Inc.(US) & Oracle (US), are some of the key players in the healthcare IT market.

- The study includes an in-depth competitive analysis of these key players in the healthcare IT market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the healthcare IT market by solution & service (healthcare provider solutions, healthcare payer solutions, HCIT outsourcing services), by component (services, software, and hardware), by end-user (Payers, Providers, and Life Sciences Industry), and by region (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the healthcare IT market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; Contracts, partnerships, agreements. new product & service launches, mergers and acquisitions, and recent developments associated with the healthcare IT market. Competitive analysis of upcoming startups in the healthcare IT market ecosystem is covered in this report.

Reasons to buy this report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the healthcare IT market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Government mandates & support for HCIT solutions, rising use of big data, high returns on investments associated with HCIT solutions, need to crucial escalating healthcare costs, growing adoption of 2-prescribing, telehealth, mhealth, and other HCIT solutions) restraints (IT infrastructural constraints in developing countries, high cost of deploying HCIT solutions in small and medium-sized hospitals in emerging countries, resistance from traditional healthcare providers) opportunities (rising use of HCIT solutions in outpatient care facilities, cloud-based EHR solutions), shift towards patient-centric healthcare delivery challenges (security concerns, interoperability issues) influencing the growth of the healthcare IT market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the healthcare IT market

- Market Development: Comprehensive information about lucrative markets - the report analyses the healthcare IT market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the healthcare IT market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Optum, Inc. (US), Cognizant (US), Koninklijke Philips N.V. (Netherlands), Oracle (US), GE Healthcare (US), Dell Inc. (US), Wipro (India), eClinicalWorks (US), SAS Institute Inc. (US), Inovalon (US); among others in the healthcare IT market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 HEALTHCARE IT MARKET OVERVIEW

- 3.2 HEALTHCARE IT MARKET, BY SOLUTION & SERVICE AND REGION

- 3.3 HEALTHCARE IT MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Government mandates & support for HCIT solutions

- 4.2.1.2 Rising use of big data in healthcare

- 4.2.1.3 High returns on investment associated with HCIT solutions

- 4.2.1.4 Growing mhealth, telehealth, and remote patient monitoring markets

- 4.2.2 RESTRAINTS

- 4.2.2.1 IT infrastructure constraints in developing countries

- 4.2.2.2 High cost of deployment in small and medium-sized hospitals in emerging economies

- 4.2.2.3 Resistance from traditional healthcare providers

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising use of HCIT solutions in outpatient care facilities

- 4.2.3.2 Cloud-based EHR solutions

- 4.2.3.3 Shift toward patient-centric healthcare delivery

- 4.2.4 CHALLENGES

- 4.2.4.1 Rising data breach concerns

- 4.2.4.2 Interoperability issues

- 4.2.4.3 Limited availability of skilled personnel

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.3.2 TECHNOLOGY INPUTS AND INFRASTRUCTURE

- 5.3.3 PLATFORM DEVELOPMENT AND INTEGRATION

- 5.3.4 DISTRIBUTION

- 5.3.5 MARKETING AND SALES

- 5.3.6 POST-SALE SERVICES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR HEALTHCARE IT SOLUTIONS, BY TYPE (2025)

- 5.5.1.1 Indicative price of clinical decision support systems, by product

- 5.5.1.2 Indicative price of HCIT integration solutions, by type

- 5.5.1.3 Indicative price of laboratory information systems

- 5.5.1.4 Indicative price of patient registry software

- 5.5.1.5 Indicative price of population health management solutions

- 5.5.1.5.1 Initial fees

- 5.5.1.5.2 Annual maintenance fees

- 5.5.1.6 Indicative price of healthcare analytics solutions, by component

- 5.5.2 INDICATIVE PRICE FOR HEALTHCARE ANALYTICS SOLUTIONS, BY REGION (2025)

- 5.5.1 INDICATIVE PRICE FOR HEALTHCARE IT SOLUTIONS, BY TYPE (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF - HEALTHCARE IT MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END USERS

- 5.10.5.1 Healthcare providers

- 5.10.5.2 Payers

- 5.10.5.3 Life science industry

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.1.2 CLOUD COMPUTING

- 6.1.3 BIG DATA & ANALYTICS

- 6.1.4 INTEROPERABILITY & HEALTHCARE INFORMATION EXCHANGE PLATFORM

- 6.1.5 APP-ENABLED PATIENT PORTALS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INTERNET OF MEDICAL THINGS (IOMT)

- 6.2.2 BLOCKCHAIN

- 6.2.3 SMART HOSPITAL INFRASTRUCTURE

- 6.2.4 ROBOTIC PROCESS AUTOMATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 VIRTUAL REALITY (VR) & AUGMENTED REALITY (AR)

- 6.3.2 EDGE COMPUTING

- 6.3.3 MEDICAL ROBOTICS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR HEALTHCARE IT MARKET

- 6.5.2 HEALTHCARE IT PATENTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN CLINICAL DECISION SUPPORT

- 6.6.2 PRECISION MEDICINE & GENOMICS INTEGRATION

- 6.6.3 REMOTE PATIENT MONITORING & VIRTUAL CARE

- 6.7 IMPACT OF GEN AI IN HEALTHCARE IT MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN HEALTHCARE IT MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 AI-driven clinical summarization and interoperability intelligence at InterSystems HealthShare

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.4.1 Revenue cycle management market

- 6.7.4.2 Telehealth and telemedicine market

- 6.7.4.3 Healthcare fraud analytics market

- 6.7.5 USERS READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.2 Payers

- 6.7.5.3 Providers

- 6.7.5.4 Impact assessment

- 6.7.5.5 User A: Payers

- 6.7.5.5.1 Implementation

- 6.7.5.5.2 Impact

- 6.7.5.6 User B: Providers

- 6.7.5.6.1 Implementation

- 6.7.5.6.2 Impact

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 HEALTHCARE IT MARKET, BY SOLUTION & SERVICE

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE PROVIDER SOLUTIONS

- 9.2.1 CLINICAL HCIT SOLUTIONS

- 9.2.1.1 Electronic health records

- 9.2.1.1.1 Federal Interoperability Mandates and Cloud Migration Fueling Sustained EHR Modernization Demand

- 9.2.1.2 Population health management

- 9.2.1.2.1 Value-Based Care Transition and Chronic Disease Burden Driving PHM Platform Adoption

- 9.2.1.3 Specialty information management

- 9.2.1.3.1 Oncology information system

- 9.2.1.3.1.1 Rising cancer incidence and AI-driven precision oncology propelling comprehensive OIS adoption

- 9.2.1.3.2 Cardiology information system

- 9.2.1.3.2.1 Growing cardiac disease burden and cloud-native cardiology platforms reshaping cardiology IT

- 9.2.1.3.3 Other information system

- 9.2.1.3.3.1 Specialty information management systems expanding across high-complexity clinical service lines

- 9.2.1.3.1 Oncology information system

- 9.2.1.4 PACS & VNA

- 9.2.1.4.1 Enterprise imaging cloud migration and AI integration driving next-generation imaging archive adoption

- 9.2.1.5 Mhealth application

- 9.2.1.5.1 Chronic disease management demand and smartphone penetration accelerating mHealth platform adoption

- 9.2.1.6 HCIT integration

- 9.2.1.6.1 FHIR standardization and multi-system healthcare ecosystems driving integration platform investment

- 9.2.1.7 Telehealth solutions

- 9.2.1.7.1 Permanent reimbursement reforms and AI-powered virtual care scaling telehealth market globally

- 9.2.1.8 Medical image analysis

- 9.2.1.8.1 FDA-cleared AI radiology tools and workforce shortage driving medical imaging AI deployment

- 9.2.1.9 Laboratory information systems

- 9.2.1.9.1 Laboratory automation imperatives and FHIR-based result exchange elevating LIS platform investment

- 9.2.1.10 Practice management systems

- 9.2.1.10.1 Ambulatory care growth and revenue cycle automation driving practice management platform modernization

- 9.2.1.11 Clinical decision support system

- 9.2.1.11.1 AI-powered evidence integration and patient safety mandates accelerating CDSS platform adoption

- 9.2.1.12 ePrescribing solutions

- 9.2.1.12.1 Mandatory ePrescribing standards and controlled substance regulations driving adoption

- 9.2.1.13 Radiology information systems

- 9.2.1.13.1 Imaging volume growth and enterprise integration mandates propelling modernization

- 9.2.1.14 Computerized physician order entry

- 9.2.1.14.1 Patient safety imperatives and EHR integration sustaining CPOE adoption across clinical settings

- 9.2.1.15 Patient registry software

- 9.2.1.15.1 Precision medicine programs and regulatory quality reporting expanding patient registry deployment

- 9.2.1.16 Infection surveillance

- 9.2.1.16.1 Healthcare-associated infection reduction mandates and real-time analytics driving surveillance adoption

- 9.2.1.17 Radiation dose management

- 9.2.1.17.1 Regulatory dose reporting mandates and patient safety programs driving dosimetry platform adoption

- 9.2.1.1 Electronic health records

- 9.2.2 NON-CLINICAL HEALTHCARE IT SOLUTIONS

- 9.2.2.1 Healthcare asset management

- 9.2.2.1.1 Real-time location systems and IoT integration transforming hospital asset visibility and utilization

- 9.2.2.2 Revenue cycle management

- 9.2.2.2.1 Front end rcm solutions

- 9.2.2.2.1.1 AI-powered eligibility verification and digital patient access accelerating front-end RCM modernization

- 9.2.2.2.2 MID RCM solutions

- 9.2.2.2.2.1 Autonomous medical coding and AI-driven documentation intelligence transforming mid-RCM workflows

- 9.2.2.2.3 Back end RCM solutions

- 9.2.2.2.3.1 AI-driven denial management and patient payment automation advancing back-end RCM efficiency

- 9.2.2.2.1 Front end rcm solutions

- 9.2.2.3 Healthcare analytics

- 9.2.2.3.1 Clinical analytics

- 9.2.2.3.1.1 AI-enhanced decision support and real-time patient intelligence driving adoption

- 9.2.2.3.2 Financial analytics

- 9.2.2.3.2.1 Predictive revenue intelligence and value-based reimbursement pressures accelerating financial analytics adoption

- 9.2.2.3.3 Operational and administrative analytics

- 9.2.2.3.3.1 Predictive workforce management and real-time hospital operations intelligence driving operational analytics growth

- 9.2.2.3.1 Clinical analytics

- 9.2.2.4 Customer relationship management

- 9.2.2.4.1 Patient engagement mandates and consumer-centric care models driving healthcare CRM adoption

- 9.2.2.5 Pharmacy information systems

- 9.2.2.5.1 ePrescribing expansion and automated medication management driving pharmacy information system modernization

- 9.2.2.6 Healthcare interoperability

- 9.2.2.6.1 FHIR standardization and regulatory interoperability mandates accelerating healthcare data exchange infrastructure

- 9.2.2.7 Healthcare quality management

- 9.2.2.7.1 Regulatory compliance and value-based performance initiatives accelerating healthcare quality management adoption

- 9.2.2.8 Supply chain management

- 9.2.2.8.1 Procurement management

- 9.2.2.8.1.1 Predictive procurement intelligence and supplier optimization accelerating healthcare purchasing modernization

- 9.2.2.8.2 Inventory management

- 9.2.2.8.2.1 Real-time inventory visibility and intelligent replenishment driving healthcare inventory modernization

- 9.2.2.8.1 Procurement management

- 9.2.2.9 Medication management

- 9.2.2.9.1 Electronic medication administration

- 9.2.2.9.1.1 Closed-loop medication safety workflows and real-time documentation driving eMAR adoption

- 9.2.2.9.2 Barcode medication administration systems

- 9.2.2.9.2.1 Bedside barcode verification and closed-loop medication safety driving BCMA system adoption

- 9.2.2.9.3 Medication inventory management systems

- 9.2.2.9.3.1 Real-time pharmaceutical visibility and predictive replenishment driving medication inventory management adoption

- 9.2.2.9.4 Medication assurance systems

- 9.2.2.9.4.1 AI-enabled pharmacovigilance and real-time clinical surveillance advancing medication assurance systems

- 9.2.2.9.1 Electronic medication administration

- 9.2.2.10 Workforce management

- 9.2.2.10.1 Healthcare labor shortages and scheduling complexity driving AI-powered workforce optimization adoption

- 9.2.2.11 Healthcare information exchange

- 9.2.2.11.1 National interoperability frameworks and FHIR-based data exchange accelerating healthcare information exchange adoption

- 9.2.2.12 Medical document management

- 9.2.2.12.1 Paper elimination mandates and EHR integration requirements driving clinical document digitization

- 9.2.2.1 Healthcare asset management

- 9.2.1 CLINICAL HCIT SOLUTIONS

- 9.3 HEALTHCARE PAYER SOLUTIONS

- 9.3.1 CLAIMS MANAGEMENT

- 9.3.1.1 Administrative complexity and AI claims adjudication propelling payer claims platform modernization

- 9.3.2 POPULATION HEALTH MANAGEMENT

- 9.3.2.1 Medicare advantage expansion and value-based risk management accelerating payer population health investment

- 9.3.3 PHARMACY AUDIT & ANALYSIS

- 9.3.3.1 PBM transparency requirements and specialty drug cost pressures accelerating pharmacy analytics adoption

- 9.3.4 CUSTOMER RELATIONSHIP MANAGEMENT

- 9.3.4.1 AI-driven member engagement and digital experience modernization accelerating payer CRM adoption

- 9.3.5 FRAUD ANALYTICS SOLUTIONS

- 9.3.5.1 Escalating healthcare fraud costs and AI detection capabilities expanding fraud analytics deployment

- 9.3.6 PROVIDER NETWORK MANAGEMENT

- 9.3.6.1 Network adequacy compliance and value-based contracting driving provider network management modernization

- 9.3.1 CLAIMS MANAGEMENT

- 9.4 HCIT OUTSOURCING SERVICES

- 9.4.1 IT INFRASTRUCTURE MANAGEMENT

- 9.4.1.1 Cloud migration complexity and cybersecurity threats driving healthcare IT infrastructure outsourcing

- 9.4.2 PAYER HCIT OUTSOURCING SERVICES

- 9.4.2.1 Claims management

- 9.4.2.1.1 Rising claims complexity and denial management pressures accelerating claims outsourcing adoption

- 9.4.2.2 Provider network management

- 9.4.2.2.1 Automated credentialing and regulatory network oversight accelerating provider network outsourcing demand

- 9.4.2.3 Billing & accounts management

- 9.4.2.3.1 Billing automation and financial reconciliation complexity accelerating outsourcing adoption

- 9.4.2.4 Fraud analytics

- 9.4.2.4.1 AI-driven payment integrity and specialized investigation expertise fueling fraud analytics outsourcing growth

- 9.4.2.5 Other payer hcit outsourcing services

- 9.4.2.5.1 Digital member engagement and regulatory reporting complexity expanding payer HCIT outsourcing demand

- 9.4.2.1 Claims management

- 9.4.3 PROVIDER HCIT OUTSOURCING SERVICES

- 9.4.3.1 Revenue cycle management

- 9.4.3.1.1 Administrative burden and AI-driven automation accelerating revenue cycle outsourcing adoption

- 9.4.3.2 Medical documents management

- 9.4.3.2.1 Clinical document digitization and intelligent record processing driving segment growth

- 9.4.3.3 Laboratory information management

- 9.4.3.3.1 Molecular diagnostics expansion and digital pathology integration driving laboratory informatics outsourcing adoption

- 9.4.3.4 Other provider HCIT outsourcing services

- 9.4.3.4.1 Operational flexibility and specialized digital support driving demand for other provider HCIT outsourcing services

- 9.4.3.1 Revenue cycle management

- 9.4.4 OPERATIONAL HCIT OUTSOURCING SERVICES

- 9.4.4.1 Supply chain management

- 9.4.4.1.1 Supply chain resilience and data-driven procurement strategies accelerating healthcare supply chain outsourcing adoption

- 9.4.4.2 Business process management

- 9.4.4.2.1 Workforce constraints and hyper automation technologies reshaping healthcare BPM service delivery

- 9.4.4.3 Other operational HCIT outsourcing services

- 9.4.4.3.1 Cybersecurity resilience and enterprise operations modernization drive demand for operational IT outsourcing

- 9.4.4.1 Supply chain management

- 9.4.1 IT INFRASTRUCTURE MANAGEMENT

10 HEALTHCARE IT MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 SERVICES

- 10.2.1 REGULATORY COMPLEXITY AND CYBERSECURITY MANDATES ACCELERATING MANAGED IT SERVICES DEMAND

- 10.3 SOFTWARE

- 10.3.1 CLOUD-NATIVE SAAS MODELS AND AI INTEGRATION DRIVING FASTEST GROWTH ACROSS SOFTWARE PLATFORMS

- 10.4 HARDWARE

- 10.4.1 CONNECTED MEDICAL DEVICES AND SMART HOSPITAL INFRASTRUCTURE SUSTAINING HARDWARE INVESTMENT

11 HEALTHCARE IT MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HEALTHCARE PROVIDERS

- 11.2.1 HOSPITALS

- 11.2.1.1 Enterprise EHR consolidation and AI integration accelerating hospital IT transformation

- 11.2.2 AMBULATORY CARE CENTERS (OUTPATIENT SETTING)

- 11.2.2.1 Telehealth integration and practice management automation transforming outpatient IT Adoption

- 11.2.3 HOME HEALTHCARE AGENCIES & ASSISTED LIVING FACILITIES

- 11.2.3.1 Aging demographics and remote monitoring technologies expanding home care IT investment

- 11.2.4 DIAGNOSTIC & IMAGING CENTERS

- 11.2.4.1 Enterprise EHR consolidation and AI integration accelerating hospital IT transformation

- 11.2.5 PHARMACIES

- 11.2.5.1 Electronic prescribing expansion and specialty pharmacy growth driving pharmacy IT adoption

- 11.2.1 HOSPITALS

- 11.3 HEALTHCARE PAYERS

- 11.3.1 PUBLIC PAYERS

- 11.3.1.1 TEFCA expansion and CMS digital health ecosystem driving public payer IT modernization

- 11.3.2 PRIVATE PAYERS

- 11.3.2.1 AI-powered payment integrity and value-based care strategies accelerating private payer IT investments

- 11.3.1 PUBLIC PAYERS

- 11.4 LIFE SCIENCE INDUSTRY

12 HEALTHCARE IT MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 Vast healthcare infrastructure, reforms, and advancements in digital innovation to make US dominant global market

- 12.2.3 CANADA

- 12.2.3.1 Government investment in health infrastructure and prevalence of digital solutions such as EHRs to drive market

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Market expansion driven by government initiatives, digital upgrades, and record management innovation

- 12.3.3 UK

- 12.3.3.1 Government initiatives involving substantial public engagement and investments in recovery to boost market

- 12.3.4 FRANCE

- 12.3.4.1 Robust healthcare system-driving innovation and attracting foreign investments

- 12.3.5 ITALY

- 12.3.5.1 Need for integrated healthcare solutions and digitization of health records to enhance patient care

- 12.3.6 SPAIN

- 12.3.6.1 High potential for use of IT among GPs; innovations by large technology players - key drivers

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 JAPAN

- 12.4.2.1 Well-established technological sector and rapidly evolving mobile healthcare to boost market

- 12.4.3 CHINA

- 12.4.3.1 Strong government support through initiatives such as Healthy China 2030

- 12.4.4 INDIA

- 12.4.4.1 Rising FDI and government focus through initiatives such as Ayushman Bharat Digital Mission to boost growth

- 12.4.5 AUSTRALIA

- 12.4.5.1 Sharing by default legislation and FHIR modernization transforming national health record infrastructure

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Universal EMR adoption and national AI health data infrastructure driving next-generation clinical intelligence

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Brazil to dominate Latin American market with two major telehealth initiatives and significant investments

- 12.5.3 MEXICO

- 12.5.3.1 Government strategies and proximity to US with favorable cost differences to boost market

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Leveraging IT solutions through public-private partnerships and government initiatives to close demand-supply gaps

- 12.6.2.2 Saudi Arabia

- 12.6.2.2.1 Government-led digital transformation and strong investments in AI-driven healthcare to drive market

- 12.6.2.3 UAE

- 12.6.2.3.1 Advancing digital health innovation and strategic collaborations to drive healthcare IT solutions adoption

- 12.6.2.4 Rest of GCC

- 12.6.3 SOUTH AFRICA

- 12.6.3.1 Rising healthcare demand and need for cost-efficient, data-driven care delivery accelerate adoption

- 12.6.4 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN HEALTHCARE IT MARKET

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS

- 13.5 BRAND COMPARISON

- 13.6 VALUATION & FINANCIAL METRICS

- 13.6.1 FINANCIAL METRICS

- 13.6.2 COMPANY VALUATION

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Regional footprint

- 13.7.5.3 Solution & service footprint

- 13.7.5.4 Component footprint

- 13.7.5.5 End user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 OPTUM, INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products & services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 COGNIZANT

- 14.1.2.1 Business overview

- 14.1.2.2 Products & services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches & approvals

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 KONINKLIJKE PHILIPS N.V.

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches & approvals

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices made

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 DELL INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches & approvals

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 GE HEALTHCARE

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches & approvals

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 ORACLE

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches & approvals

- 14.1.6.3.2 Deals

- 14.1.7 EPIC SYSTEMS CORPORATION

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches & approvals

- 14.1.7.3.2 Deals

- 14.1.8 VERADIGM LLC

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches & approvals

- 14.1.8.3.2 Deals

- 14.1.9 SAS INSTITUTE INC.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches & approvals

- 14.1.9.3.2 Deals

- 14.1.10 NUANCE COMMUNICATIONS, INC.(MICROSOFT)

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches & approvals

- 14.1.10.3.2 Deals

- 14.1.11 WIPRO

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches & approvals

- 14.1.11.3.2 Deals

- 14.1.12 ECLINICALWORKS

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Product launches & approvals

- 14.1.12.3.2 Deals

- 14.1.13 INOVALON

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Product launches & approvals

- 14.1.13.3.2 Deals

- 14.1.14 INFOR (KOCH INDUSTRIES)

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches & approvals

- 14.1.14.3.2 Deals

- 14.1.15 CONIFER HEALTH SOLUTIONS, LLC.

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Deals

- 14.1.16 SOLVENTUM

- 14.1.16.1 Business overview

- 14.1.16.2 Products offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Product launches & approvals

- 14.1.16.3.2 Deals

- 14.1.17 MERATIVE

- 14.1.17.1 Business overview

- 14.1.17.2 Products offered

- 14.1.17.3 Recent developments

- 14.1.17.3.1 Product launches & approvals

- 14.1.17.3.2 Deals

- 14.1.18 INTERSYSTEMS CORPORATION

- 14.1.18.1 Business overview

- 14.1.18.2 Products offered

- 14.1.18.3 Recent developments

- 14.1.18.3.1 Product launches & approvals

- 14.1.18.3.2 Deals

- 14.1.19 SALESFORCE, INC.

- 14.1.19.1 Business overview

- 14.1.19.2 Products offered

- 14.1.19.3 Recent developments

- 14.1.19.3.1 Product launches & approvals

- 14.1.19.3.2 Deals

- 14.1.20 CITIUSTECH INC

- 14.1.20.1 Business overview

- 14.1.20.2 Products offered

- 14.1.20.3 Recent developments

- 14.1.20.3.1 Product launches & approvals

- 14.1.20.3.2 Deals

- 14.1.1 OPTUM, INC.

- 14.2 OTHER PLAYERS

- 14.2.1 CONDUENT, INC.

- 14.2.2 CARESTREAM HEALTH

- 14.2.3 PRACTICE FUSION, INC.

- 14.2.4 TATA CONSULTANCY SERVICES LIMITED

- 14.2.5 ELSEVIER

- 14.2.6 MEDEANALYTICS, INC.

- 14.2.7 MEDECISION

- 14.2.8 SURGICAL INFORMATION SYSTEMS

- 14.2.9 CHARTIS

- 14.2.10 CLEARWAVE CORPORATION

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH APPROACH

- 15.1.1 SECONDARY RESEARCH

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY RESEARCH

- 15.1.2.1 Primary sources

- 15.1.2.2 Key data from primary sources

- 15.1.2.3 Breakdown of primaries

- 15.1.2.4 Insights from primary experts

- 15.1.1 SECONDARY RESEARCH

- 15.2 RESEARCH METHODOLOGY DESIGN

- 15.3 MARKET SIZE ESTIMATION: HEALTHCARE IT MARKET

- 15.4 MARKET BREAKDOWN DATA TRIANGULATION

- 15.5 MARKET SHARE ESTIMATION

- 15.6 STUDY ASSUMPTIONS

- 15.7 RESEARCH LIMITATIONS

- 15.7.1 METHODOLOGY-RELATED LIMITATIONS

- 15.8 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS