|

시장보고서

상품코드

2059327

소화기계 스텐트 시장 : 제품별, 유형별, 용도별, 최종사용자별, 지역별 - 예측(-2031년)Gastrointestinal Stent Market By Product (Duodenal, Pancreatic, Colonic, Biliary), Type [Metal (SEMS, Balloon-expandable, Nitinol, Stainless Steel), Plastic, Biodegradable], Application (Colorectal & Stomach Cancer), End User - Global Forecast to 2031 |

||||||

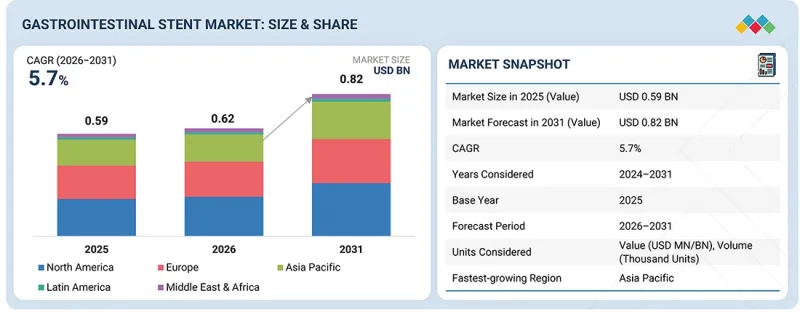

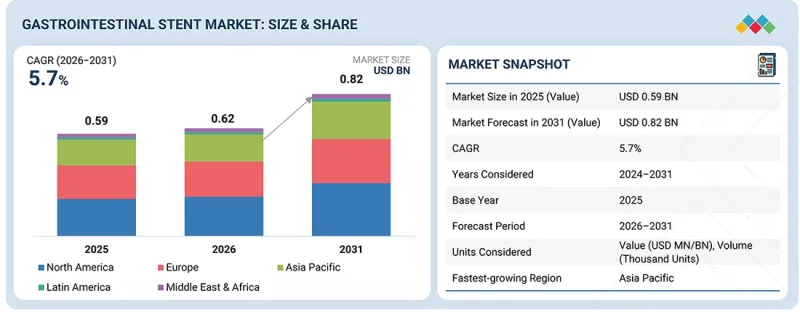

소화기계 스텐트 시장 규모는 2026년 6억 2,000만 달러에서 2031년까지 8억 2,000만 달러에 이르고, CAGR 5.7%를 기록할 것으로 예측됩니다.

이러한 성장은 저침습적 소화기 질환 관리, 내시경 치료, 그리고 스텐트를 활용한 치료 솔루션의 미래를 형성하는 몇 가지 주요 요인에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 유형별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

소화기계 스텐트 시장은 암, 협착, 폐색 등 소화기 질환으로 인한 전 세계적 부담 증가와 더불어, 저침습적 치료법에 대한 선호도가 높아짐에 따라 주로 성장하고 있습니다. 의료 시스템이 환자의 예후 개선과 입원 기간 단축에 주력하는 가운데, 임상의들은 복잡한 소화기 질환을 효과적으로 관리하기 위해 스텐트 삽입과 같은 내시경적 중재술을 점점 더 많이 도입하고 있습니다. 이에 따라 병원, 전문 클리닉, 내시경 센터에서는 식도암, 담도 폐쇄, 대장 협착 등의 질환에 대해 정밀한 치료와 신속한 증상 완화를 실현하기 위해 자가팽창형 금속 스텐트(SEMS), 생분해성 스텐트, 약물 방출형 스텐트와 같은 첨단 스텐트 기술의 활용이 확대되고 있습니다.

수요를 다시 불러일으키는 또 다른 중요한 요인은 만성 및 악성 소화기 질환 환자에 대한 조기 개입, 완화 치료, 그리고 삶의 질 향상에 대한 관심이 높아지고 있다는 점입니다. 의료 종사자와 규제 당국 역시 시술에 수반되는 위험을 줄이고 임상 효율을 높이는 데 주력하고 있으며, 그 결과 기술적으로 진보된 스텐트 솔루션의 사용이 증가하고 있습니다. 그 결과, 위장관 스텐트는 관강의 개통성 회복, 누출 및 누공 제어, 수술 후 회복 지원을 위한 1차 치료법이 되었으며, 이는 결국 적시 치료와 더 나은 질환 관리 성과로 이어지고 있습니다.

또한, 생체 재료, 스텐트 설계 및 전달 시스템에 대한 지속적인 연구 개발을 통해 위장관 스텐트의 성능과 안전성이 크게 향상되었습니다. 이동 방지 기능, 유연하고 슬림한 전달 시스템, 생체 적합성 코팅, 생분해성 소재와 같은 혁신적인 기술은 합병증 감소와 장기적인 치료 성과 향상에 기여하고 있습니다. 이러한 기술적 진보 덕분에 의료진은 시술 성공률을 높이고, 보다 일관된 환자 예후를 확보하며, 더 광범위한 임상 적응증에서 위장관 스텐트의 사용을 확대할 수 있게 됩니다.

“제품별로는 예측 기간 동안 식도 스텐트 부문이 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. '

식도 스텐트 부문은 식도암 및 양성 협착의 유병률 증가와 더불어, 연하곤란의 신속한 완화에 대한 수요가 높아짐에 따라 소화기계 스텐트 시장에서 가장 높은 성장세를 보일 것으로 전망됩니다. 이러한 스텐트는 최소 침습적 시술을 통해 삼킴 기능을 즉시 회복시키고, 복잡한 수술의 필요성을 줄여주기 때문에 널리 선호되고 있습니다. 또한, 완전 피복형 디자인, 이동 방지 기능, 생분해성 옵션 등의 기술적 진보로 인해 안전성이 향상되고, 악성 및 양성 질환 모두에서 사용 범위가 확대됨에 따라 그 도입이 더욱 가속화되고 있습니다.

“최종 사용자별로는 2025년에 병원 및 진료소 부문이 가장 큰 시장 점유율을 차지했습니다.” '

2025년, 병원 및 진료소 부문이 위장관 스텐트 시장을 독점한 것은 이곳이 대부분의 내시경 검사가 주로 시행되는 장소이기 때문입니다. 또한, 이러한 시설에는 일반적으로 스텐트 삽입에 필요한 첨단 인프라, 전문 소화기내과 전문의, 그리고 전용 장비가 갖춰져 있습니다. 또한 암, 협착, 수술 후 합병증 등 복잡한 소화기 질환에 대한 주요 치료 거점 역할을 수행하고 있으며, 스텐트를 이용한 시술에 대한 지속적인 수요를 창출하고 있습니다. 또한, 이러한 시설들은 보다 충실한 보험 환급 체계를 갖추고 있어 첨단 기술을 이용할 수 있을 뿐만 아니라, 응급 상황이나 고위험 사례에도 대응할 수 있기 때문에 시장 내 주도적인 점유율이 더욱 공고해지고 있습니다.

“아시아태평양 지역은 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다.” '

아시아태평양은 위장관 스텐트 시장에서 가장 빠른 성장세를 보이고 있습니다. 이러한 성장의 주된 요인은 주로 소화기 질환 및 암 발병률이 급격히 증가하고 있는 데다, 중국이나 인도 등 신흥 경제국에서의 의료시설 확충에 있습니다. 의료 분야로의 자금 투입 증가, 최소 침습 치료에 대한 인식 제고, 그리고 첨단 내시경 치료에 대한 접근성 개선이 해당 지역에서 제품 사용을 촉진하는 요인으로 작용하고 있습니다. 또한, 막대한 환자 수, 의료시설에 대한 투자 확대, 그리고 전 세계 및 지역 의료기기 기업들 시장 진입이 아시아태평양 시장 급성장에 기여하고 있습니다.

조사 범위

본 시장 조사는 위장용 스텐트 시장의 다양한 부문을 대상으로 합니다. 제품, 유형, 용도, 최종 사용자, 지역별로 이 시장 규모와 성장 잠재력을 추정하는 것을 목적으로 합니다. 또한, 본 조사에는 시장 내 주요 기업에 대한 상세한 경쟁 분석 외에도 각 기업프로파일, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 주요 시장 전략도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유

본 보고서는 기존 기업과 신생·중소기업이 시장 동향을 파악하고, 더 큰 시장 점유율을 확보하는 데 도움이 될 것입니다. 본 보고서를 입수한 기업은 아래에 개략적으로 설명된 5가지 전략 중 1가지 이상을 실행할 수 있습니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(대장암, 식도암, 담도 질환을 포함한 소화기 계통 암 및 폐쇄성 질환의 발생률 증가, 저침습 및 내시경 시술의 보급 확대), 제약 요인(첨단 스텐트 및 내시경 시술의 높은 비용, 개발도상 지역에서의 첨단 내시경 인프라 접근 제한), 기회(기술 발전(생분해성 스텐트, 약물 방출형 스텐트, LAMS), 완화 치료 및 비수술적 치료 옵션에 대한 수요 증가), 그리고 과제(엄격한 규제 승인 및 임상 검증 요건, 자원이 부족한 환경에서의 숙련된 내시경 전문의 부족) 등, 위장관 스텐트 시장의 성장에 영향을 미치는 요인 분석

- 제품 개발/혁신 : 위장관 스텐트 시장의 향후 기술 동향 및 신제품 출시에 관한 상세한 분석

- 시장 개발: 수익성이 높은 신흥 시장에 대한 종합적인 정보. 본 보고서에서는 지역별 각종 위장용 스텐트 제품 시장을 분석했습니다.

- 시장의 다양화: 위장관 스텐트 시장의 제품, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : 위장관 스텐트 시장에서 주요 기업의 시장 점유율, 전략, 제품, 유통망 및 생산 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 지속가능성과 규제 상황

제7장 고객 현황과 구매 행동

제8장 기술, 특허, 디지털 기술, AI 도입에 의한 전략적 파괴적 변혁

제9장 소화기계 스텐트 시장(제품별)

제10장 소화기계 스텐트 시장(유형별)

제11장 소화기계 스텐트 시장(용도별)

제12장 소화기계 스텐트 시장(최종사용자별)

제13장 소화기계 스텐트 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSH 26.06.25The gastrointestinal stent market is expected to grow from USD 0.62 billion in 2026 to USD 0.82 billion by 2031, at a CAGR of 5.7%. This growth is driven by several key factors shaping the future of minimally invasive gastrointestinal disease management, endoscopic interventions, and stent-based therapeutic solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Product, Type, Application, End User, Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The gastrointestinal stent market is primarily driven by the rising global burden of gastrointestinal diseases, including cancers, strictures, and obstructions, as well as the growing preference for minimally invasive treatment approaches. As healthcare systems focus on improving patient outcomes and reducing hospital stays, clinicians are increasingly adopting endoscopic interventions, such as stent placement, to effectively manage complex GI conditions. In response, hospitals, specialty clinics, and endoscopy centers are increasingly using advanced stent technologies, such as self-expanding metal stents (SEMS), biodegradable stents, and drug-eluting stents, to enable precise treatment and rapid symptom relief for conditions including esophageal cancer, biliary obstruction, and colorectal strictures.

Another important factor that will renew demand is the increasing focus on early intervention, palliative care, and enhancement of the quality of life of patients with chronic and malignant gastrointestinal diseases. Healthcare providers and regulatory bodies have also focused on reducing procedural risks and improving clinical efficiency, which has resulted in increasing use of technologically advanced stent solutions. As a result, GI stents have turned into a go-to treatment for restoring luminal patency, controlling leaks and fistulas, and assisting post-surgical recovery, which in turn facilitates timely treatment and better disease management outcomes.

Besides, ongoing research and development in biomaterials, stent design, and delivery systems have significantly improved the performance and safety of gastrointestinal stents. Innovations such as anti-migration features, flexible and low-profile delivery systems, biocompatible coatings, and biodegradable materials are helping reduce complications and improve long-term outcomes. With these technological advancements, healthcare providers can enhance procedural success rates, ensure more consistent patient outcomes, and expand the use of GI stents across a broader range of clinical indications.

"By product, the esophageal stents segment is projected to grow at the highest CAGR during the forecast period."

The esophageal stents segment is expected to see the highest growth in the gastrointestinal stent market due to the increasing prevalence of esophageal cancer and benign strictures, along with the high demand for rapid relief from dysphagia. These stents are widely preferred as they provide immediate restoration of swallowing function through minimally invasive procedures, reducing the need for complex surgeries. Additionally, advancements such as fully covered designs, anti-migration features, and biodegradable options have improved safety and expanded their use in both malignant and benign conditions, further accelerating their adoption.

"By end user, the hospitals and clinics segment accounted for the largest market share in 2025."

In 2025, the hospitals and clinics segment dominated the gastrointestinal stent market because it is the primary setting for most endoscopic procedures. Besides that, these places usually have the advanced infrastructure, expert gastroenterologists, and specialized equipment necessary for the installation of a stent. Moreover, they serve as the primary treatment for complex gastrointestinal conditions, such as cancers, strictures, and post-surgical complications, leading to a continuous demand for stent-based procedures. Additionally, they provide better reimbursement support, have access to more advanced technologies, and can manage emergency and high-risk cases, which makes their leading share in the market more conclusive.

"The Asia Pacific region is expected to witness the highest growth rate during the forecast period."

The Asia Pacific region is growing at the fastest rate in the gastrointestinal stent market. The main reason for this growth is mainly because of the swiftly rising incidence of gastrointestinal diseases and cancers, along with better healthcare facilities in emerging economies like China and India. Increasing funding for healthcare, enhancing awareness of less invasive procedures, and better accessibility to advanced endoscopic treatments are the factors encouraging the use of the products in the region. Besides that, a large patient pool, increased investments in healthcare centers, and the entry of global and regional medical device companies are contributing to the rapid growth of the market in the Asia Pacific.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (45%), Europe (15%), Asia Pacific (25%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By End User: Hospitals & Clinics (54%), Ambulatory Surgical Centers (29%), and Specialty Endoscopy Centers/GI Clinics (17%)

- By Designation: Gastroenterologists/Interventional Endoscopists (47%), General & GI Surgeons (22%), Heads/Directors of Gastroenterology Departments (15%), and Others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the gastrointestinal stent market in various segments. It aims to estimate the market size and growth potential of this market by product, type, application, end user, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger market share. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (increasing incidence of gastrointestinal cancers and obstructive conditions, including colorectal, esophageal, and biliary disorders, increasing adoption of minimally invasive and endoscopic procedures), restraints (high cost of advanced stents and endoscopic procedures, limited access to advanced endoscopic infrastructure in developing regions), opportunities (technological advancements (biodegradable stents, drug-eluting stents, LAMS), increasing demand for palliative care and non-surgical treatment options), and challenges (stringent regulatory approvals and clinical validation requirements, lack of skilled endoscopists in low-resource settings) influencing the growth of the gastrointestinal stent market

- Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the gastrointestinal stent market

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of gastrointestinal stent products across regions

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the gastrointestinal stent market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the gastrointestinal stent market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 LIMITATIONS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN GASTROINTESTINAL STENTS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 GASTROINTESTINAL STENTS MARKET OVERVIEW

- 3.2 ASIA PACIFIC: GASTROINTESTINAL STENTS MARKET, BY TYPE AND COUNTRY (2025)

- 3.3 GASTROINTESTINAL STENTS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 GASTROINTESTINAL STENTS MARKET: REGIONAL MIX (2026-2031)

- 3.5 GASTROINTESTINAL STENTS MARKET: DEVELOPED VS. DEVELOPING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising burden of GI cancers and pancreaticobiliary diseases

- 4.2.1.2 Growing preference for minimally invasive endoscopic palliation

- 4.2.1.3 Technological advancements in GI stents

- 4.2.1.4 Expanding use of SEMS over plastic stents

- 4.2.2 RESTRAINTS

- 4.2.2.1 High device and procedure costs

- 4.2.2.2 Risk of stent migration, perforation, bleeding, and re-obstruction

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising adoption in emerging markets

- 4.2.3.2 Expansion of EUS-guided stenting procedures

- 4.2.4 CHALLENGES

- 4.2.4.1 Need for high operator expertise

- 4.2.4.2 Regulatory and post-market safety scrutiny

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN GASTROINTESTINAL STENTS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF GASTROINTESTINAL STENTS, BY KEY PLAYER, 2023-2025

- 5.5.1.1 Average selling price trend of gastrointestinal stents, by key player, 2023-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF GASTROINTESTINAL STENTS, BY REGION, 2023-2025

- 5.5.2.1 Average selling price trend of nitinol stents, by region, 2023-2025

- 5.5.2.2 Average selling price trend of stainless-steel stents, by region, 2023-2025

- 5.5.2.3 Average selling price trend of plastic stents, by region, 2023-2025

- 5.5.1 AVERAGE SELLING PRICE TREND OF GASTROINTESTINAL STENTS, BY KEY PLAYER, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 TRADE DATA FOR HS CODE 9018

- 5.6.1.1 Import data for HS Code 9018

- 5.6.1.2 Export data for HS Code 9018

- 5.6.2 TRADE DATA FOR HS CODE 9021

- 5.6.2.1 Import data for HS Code 9021

- 5.6.2.2 Export data for HS Code 9021

- 5.6.1 TRADE DATA FOR HS CODE 9018

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 5.10.1 COLONIC STENTS FOR MALIGNANT COLORECTAL OBSTRUCTION

- 5.10.2 DUODENAL STENTS FOR GASTRODUODENAL OUTLET OBSTRUCTION

- 5.10.3 LARGE-CELL STENTS FOR MULTIPLE STENTING IN MALIGNANT HILAR BILIARY OBSTRUCTION

- 5.11 IMPACT OF 2025 US TARIFFS ON GASTROINTESTINAL STENTS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Hospitals & clinics

- 5.11.5.2 Specialty endoscopy centers/GI clinics

- 5.11.5.3 Ambulatory surgical centers

6 SUSTAINABILITY & REGULATORY LANDSCAPE

- 6.1 REGIONAL REGULATIONS & COMPLIANCE

- 6.1.1 REGULATORY ANALYSIS

- 6.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.3 INDUSTRY STANDARDS

- 6.2 SUSTAINABILITY INITIATIVES

- 6.2.1 RECYCLED & ECO-FRIENDLY MATERIALS FOR GASTROINTESTINAL STENTS

- 6.2.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 6.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 7.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.1.2 BUYING CRITERIA

- 7.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.2.1 DECISION-MAKING PROCESS

- 7.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 7.2.4 MARKET PROFITABILITY

8 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 8.1 TECHNOLOGY ANALYSIS

- 8.1.1 KEY EMERGING TECHNOLOGIES

- 8.1.1.1 Biodegradable gastrointestinal stents

- 8.1.1.2 3D-printed personalized stents

- 8.1.2 COMPLEMENTARY TECHNOLOGIES

- 8.1.2.1 Advanced endoscopic imaging & AI-assisted endoscopy

- 8.1.2.2 Minimally invasive surgical devices

- 8.1.3 ADJACENT TECHNOLOGIES

- 8.1.3.1 Surface modification technologies

- 8.1.3.2 Nitinol alloy technology

- 8.1.1 KEY EMERGING TECHNOLOGIES

- 8.2 TECHNOLOGY/PRODUCT ROADMAP

- 8.2.1 NEAR TERM (2025-2027)

- 8.2.2 MID TERM (2028-2030)

- 8.2.3 LONG TERM (2030+)

- 8.3 PATENT ANALYSIS

- 8.3.1 PATENT PUBLICATION TRENDS FOR GASTROINTESTINAL STENTS

- 8.3.2 JURISDICTION & TOP APPLICANT ANALYSIS

- 8.4 FUTURE APPLICATIONS

- 8.4.1 AI-ASSISTED ENDOSCOPY & STENT PLACEMENT

- 8.4.2 NEXT-GENERATION BIODEGRADABLE GI STENTS

- 8.4.3 PERSONALIZED & 3D-PRINTED GI STENTS

- 8.4.4 DRUG-ELUTING & SMART GI STENTS

- 8.4.5 ROBOTIC-ASSISTED & IMAGE-GUIDED GI INTERVENTIONS

- 8.5 IMPACT OF AI/GENERATIVE AI ON GASTROINTESTINAL STENTS MARKET

- 8.5.1 INTRODUCTION

- 8.5.2 MARKET POTENTIAL IN GASTROINTESTINAL STENTS ECOSYSTEM

- 8.5.3 AI USE CASES

- 8.5.4 KEY COMPANIES IMPLEMENTING AI IN GASTROINTESTINAL STENTS MARKET

9 GASTROINTESTINAL STENTS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 BILIARY STENTS

- 9.2.1 RISING BURDEN OF HEPATOBILIARY AND PANCREATIC DISORDERS TO BOOST DEMAND

- 9.3 ESOPHAGEAL STENTS

- 9.3.1 INCREASING ESOPHAGEAL CANCER INCIDENCE TO DRIVE MARKET

- 9.4 COLONIC STENTS

- 9.4.1 GROWING PREFERENCE FOR MINIMALLY INVASIVE MANAGEMENT OF COLORECTAL OBSTRUCTIONS TO DRIVE MARKET

- 9.5 DUODENAL STENTS

- 9.5.1 EXPANDING USE OF ENDOSCOPIC PALLIATION TO FUEL MARKET GROWTH

- 9.6 PANCREATIC STENTS

- 9.6.1 RISING VOLUME OF ERCP PROCEDURES AND PANCREATIC DISEASE MANAGEMENT TO SUPPORT GROWTH

10 GASTROINTESTINAL STENTS MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 METAL STENTS

- 10.2.1 METAL STENTS MARKET, BY TYPE

- 10.2.1.1 Nitinol stents

- 10.2.1.1.1 Growing demand for flexible and conformable stents to fuel demand

- 10.2.1.1.2 Global volume analysis of nitinol stents, 2024-2031 (thousand units)

- 10.2.1.2 Stainless steel stents

- 10.2.1.2.1 Increasing need for high radial force solutions to support adoption

- 10.2.1.2.2 Global volume analysis of stainless steel stents, 2024-2031 (thousand units)

- 10.2.1.3 Other metal stents

- 10.2.1.1 Nitinol stents

- 10.2.2 METAL STENTS MARKET, BY MECHANISM

- 10.2.2.1 Self-expanding metal stents (SEMS)

- 10.2.2.1.1 Expanding preference for minimally invasive cancer palliation to drive market growth

- 10.2.2.2 Balloon-expandable metal stents (BEMS)

- 10.2.2.2.1 Rising demand for precise stent deployment to support growth

- 10.2.2.1 Self-expanding metal stents (SEMS)

- 10.2.3 METAL STENTS MARKET, BY COVERAGE

- 10.2.3.1 Uncovered stents

- 10.2.3.1.1 Growing use in malignant biliary obstruction management to support adoption

- 10.2.3.2 Fully covered stents

- 10.2.3.2.1 Greater focus on preventing tissue ingrowth to fuel adoption

- 10.2.3.3 Partially covered stents

- 10.2.3.3.1 Increasing emphasis on balancing patency and migration control to boost demand

- 10.2.3.1 Uncovered stents

- 10.2.1 METAL STENTS MARKET, BY TYPE

- 10.3 PLASTIC STENTS

- 10.3.1 INCREASING VOLUME OF TEMPORARY BILIARY AND PANCREATIC DRAINAGE PROCEDURES TO DRIVE DEMAND

- 10.3.2 GLOBAL VOLUME ANALYSIS OF PLASTIC STENTS, 2024-2031 (THOUSAND UNITS)

- 10.4 BIODEGRADABLE STENTS

- 10.4.1 GLOBAL VOLUME ANALYSIS OF BIODEGRADABLE STENTS, 2024-2031 (THOUSAND UNITS)

- 10.4.2 POLYMER-BASED BIODEGRADABLE STENTS

- 10.4.2.1 Rising utilization in benign stricture treatment to support growth

- 10.4.3 MAGNESIUM-BASED BIODEGRADABLE STENTS

- 10.4.3.1 Advancements in bioresorbable metal technologies to drive market growth

- 10.4.4 OTHER BIODEGRADABLE STENTS

11 GASTROINTESTINAL STENTS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 GASTROINTESTINAL CANCER

- 11.2.1 PANCREATIC CANCER

- 11.2.1.1 Increasing pancreatic cancer burden to support growth

- 11.2.2 COLORECTAL CANCER

- 11.2.2.1 Rising colorectal cancer incidence to drive demand

- 11.2.3 ESOPHAGEAL CANCER

- 11.2.3.1 Growing need for dysphagia relief to accelerate esophageal stent adoption

- 11.2.4 STOMACH CANCER

- 11.2.4.1 Expanding use of minimally invasive palliation to boost market growth

- 11.2.1 PANCREATIC CANCER

- 11.3 BILIARY DISEASE

- 11.3.1 INCREASING PREVALENCE OF BILIARY OBSTRUCTIONS TO ACCELERATE MARKET GROWTH

- 11.4 BENIGN STRICTURES & LEAKS

- 11.4.1 GROWING ADOPTION OF ENDOSCOPIC MANAGEMENT OF BENIGN GI CONDITIONS TO FUEL MARKET GROWTH

- 11.5 OTHER APPLICATIONS

12 GASTROINTESTINAL STENTS MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITALS & CLINICS

- 12.2.1 RISING GASTROINTESTINAL CANCER BURDEN AND ADVANCED ENDOSCOPY CAPABILITIES TO DRIVE MARKET GROWTH

- 12.3 SPECIALTY ENDOSCOPY CENTERS/GI CLINICS

- 12.3.1 GROWING PREFERENCE FOR SPECIALIZED THERAPEUTIC ENDOSCOPY TO PROPEL MARKET

- 12.4 AMBULATORY SURGICAL CENTERS

- 12.4.1 SHIFT TOWARD OUTPATIENT MINIMALLY INVASIVE PROCEDURES TO FUEL GROWTH

13 GASTROINTESTINAL STENTS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 NORTH AMERICA: VOLUME ANALYSIS OF GASTROINTESTINAL STENTS, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 13.2.3 US

- 13.2.3.1 High GI disease burden and procedural volume to support adoption of GI stents

- 13.2.4 CANADA

- 13.2.4.1 Expanding minimally invasive GI interventions and aging demographics to drive market

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 EUROPE: VOLUME ANALYSIS OF BIODEGRADABLE GASTROINTESTINAL STENTS, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 13.3.3 GERMANY

- 13.3.3.1 Germany to dominate European market

- 13.3.4 UK

- 13.3.4.1 Expanding NHS adoption of innovative devices to support market growth

- 13.3.5 FRANCE

- 13.3.5.1 Strong focus on advanced GI treatments and reimbursement coverage to boost adoption

- 13.3.6 ITALY

- 13.3.6.1 Growing preference for minimally invasive procedures to drive market penetration

- 13.3.7 SPAIN

- 13.3.7.1 Expanding endoscopy infrastructure to fuel gradual market growth

- 13.3.8 NETHERLANDS

- 13.3.8.1 Advanced gastroenterology services and increasing GI cancer burden to boost adoption

- 13.3.9 SWEDEN

- 13.3.9.1 High healthcare expenditure to fuel market growth

- 13.3.10 POLAND

- 13.3.10.1 Rising cancer incidence and modernization of endoscopy services to boost market

- 13.3.11 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 ASIA PACIFIC: VOLUME ANALYSIS OF GASTROINTESTINAL STENTS, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 13.4.3 CHINA

- 13.4.3.1 China to dominate APAC market

- 13.4.4 JAPAN

- 13.4.4.1 Aging population and advanced endoscopy ecosystem to fuel market growth

- 13.4.5 INDIA

- 13.4.5.1 Growing cancer incidence and improving healthcare access to boost market growth

- 13.4.6 AUSTRALIA

- 13.4.6.1 Mature healthcare system and favorable regulatory pathways to enable early adoption

- 13.4.7 SOUTH KOREA

- 13.4.7.1 High screening rates and advanced clinical capabilities to boost market growth

- 13.4.8 THAILAND

- 13.4.8.1 Increasing colorectal and hepatobiliary cancer cases to support market growth

- 13.4.9 NEW ZEALAND

- 13.4.9.1 Expanding elderly population and strong cancer care services to boost demand

- 13.4.10 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 LATIN AMERICA: VOLUME ANALYSIS OF GASTROINTESTINAL STENTS, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 13.5.3 BRAZIL

- 13.5.3.1 Large patient population and rising colorectal cancer cases to propel market demand

- 13.5.4 MEXICO

- 13.5.4.1 Growing endoscopy capacity and disease burden to support steady market growth

- 13.5.5 ARGENTINA

- 13.5.5.1 Increasing gastrointestinal cancer incidence and advanced clinical capabilities to drive growth

- 13.5.6 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS OF BIODEGRADABLE GASTROINTESTINAL STENTS, BY TYPE, 2024-2031 (THOUSAND UNITS)

- 13.6.3 GCC COUNTRIES

- 13.6.3.1 Kingdom of Saudi Arabia (KSA)

- 13.6.3.1.1 Healthcare transformation initiatives and rising cancer prevalence to fuel market expansion

- 13.6.3.2 United Arab Emirates (UAE)

- 13.6.3.2.1 Medical tourism growth and advanced healthcare investments to strengthen adoption

- 13.6.3.3 Rest of GCC Countries

- 13.6.3.1 Kingdom of Saudi Arabia (KSA)

- 13.6.4 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.1.1 KEY STRATEGIES ADOPTED BY PLAYERS IN GASTROINTESTINAL STENTS MARKET

- 14.2 REVENUE ANALYSIS, 2023-2025

- 14.3 MARKET SHARE ANALYSIS, 2025

- 14.3.1 US GASTROINTESTINAL STENTS MARKET SHARE ANALYSIS, 2025

- 14.3.2 EUROPE GASTROINTESTINAL STENTS MARKET SHARE ANALYSIS, 2025

- 14.4 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.4.1 STARS

- 14.4.2 EMERGING LEADERS

- 14.4.3 PERVASIVE PLAYERS

- 14.4.4 PARTICIPANTS

- 14.4.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.4.5.1 Company footprint

- 14.4.5.2 Region footprint

- 14.4.5.3 Product footprint

- 14.4.5.4 Type footprint

- 14.5 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 14.5.1 PROGRESSIVE COMPANIES

- 14.5.2 RESPONSIVE COMPANIES

- 14.5.3 DYNAMIC COMPANIES

- 14.5.4 STARTING BLOCKS

- 14.5.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2025

- 14.5.5.1 Detailed list of key start-ups/SMEs

- 14.5.5.2 Competitive benchmarking of start-ups/SMEs

- 14.6 COMPANY VALUATION & FINANCIAL METRICS

- 14.6.1 FINANCIAL METRICS

- 14.6.2 COMPANY VALUATION

- 14.7 PRODUCT/BRAND COMPARISON

- 14.8 COMPETITIVE SCENARIO

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 BOSTON SCIENTIFIC CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 MnM view

- 15.1.1.3.1 Right to win

- 15.1.1.3.2 Strategic choices

- 15.1.1.3.3 Weaknesses & competitive threats

- 15.1.2 COOK MEDICAL

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 OLYMPUS CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 M.I. TECH

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 MICRO-TECH (NANJING) CO., LTD.

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 MERIT MEDICAL SYSTEMS

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches & approvals

- 15.1.7 MEDTRONIC

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.8 ELLA-CS, S.R.O.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 ther developments

- 15.1.9 STERIS

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.10 W. L. GORE & ASSOCIATES, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.11 BD

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 Q3 MEDICAL GROUP

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product approvals & enhancements

- 15.1.12.3.2 Other developments

- 15.1.13 MEDI-GLOBE GMBH

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.14 HOBBS MEDICAL INC.

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.15 BVM

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.1 BOSTON SCIENTIFIC CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 LEUFEN

- 15.2.2 ALLIUM

- 15.2.3 MEDORAH MEDITEK PVT. LTD.

- 15.2.4 MITRA INDUSTRIES

- 15.2.5 ENDOGI MEDICAL

- 15.2.6 ADVIN HEALTH CARE

- 15.2.7 HUNAN FUDE TECHNOLOGY CO., LTD.

- 15.2.8 HOSPI LINE EQUIPMENTS PVT. LTD.

- 15.2.9 CITEC

- 15.2.10 G-FLEX

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.3 PRIMARY SOURCES

- 16.1.3.1 Key data from primary sources

- 16.1.3.2 Key industry insights

- 16.1.3.3 Breakdown of primaries

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 APPROACH 1: COMPANY REVENUE ANALYSIS APPROACH

- 16.2.2 APPROACH 2: CUSTOMER-BASED MARKET ESTIMATION

- 16.2.3 APPROACH 3: TOP-DOWN APPROACH

- 16.2.4 APPROACH 4: BOTTOM-UP APPROACH

- 16.2.5 APPROACH 5: PRIMARY INTERVIEWS

- 16.2.6 APPROACH 6: DEMAND-SIDE APPROACH

- 16.2.7 APPROACH 7: VOLUME DATA ANALYSIS

- 16.3 DATA TRIANGULATION & MARKET BREAKDOWN

- 16.4 MARKET SHARE ASSESSMENT

- 16.5 RESEARCH ASSUMPTIONS

- 16.5.1 STUDY ASSUMPTIONS

- 16.5.2 GROWTH RATE ASSUMPTIONS

- 16.6 RISK ASSESSMENT

- 16.6.1 RESEARCH LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.3.1 PRODUCT ANALYSIS

- 17.3.2 COMPANY INFORMATION

- 17.3.3 GEOGRAPHIC ANALYSIS

- 17.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 17.3.5 COUNTRY-LEVEL VOLUME ANALYSIS, BY PRODUCT

- 17.3.6 MARKET SHARE ANALYSIS, BY PRODUCT (TOP 5 PLAYERS)

- 17.3.7 ANY CONSULT/CUSTOM REQUIREMENTS AS PER CLIENT REQUESTS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS