|

시장보고서

상품코드

2061165

아페레시스 시장 예측(-2031년) : 유형별, 최종사용자별, 시술별, 제품별, 기술별, 지역별Apheresis Market by Product (Device, Disposable), Procedure [Donor, Therapeutic (Neurological, Blood)], Application (Plasmapheresis, Plateletpheresis), Technology (Centrifugation, Membrane Separation), End User (Clinic) - Global Forecast to 2031 |

||||||

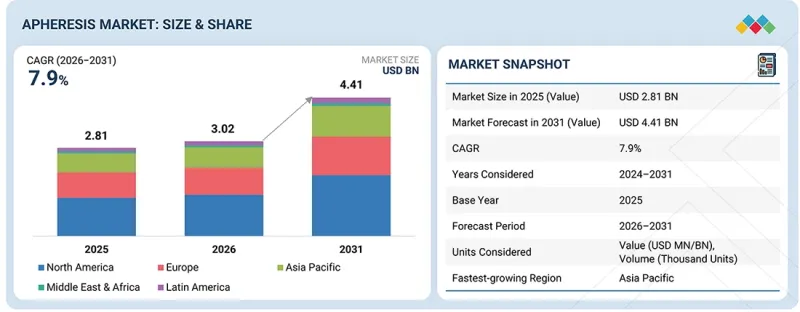

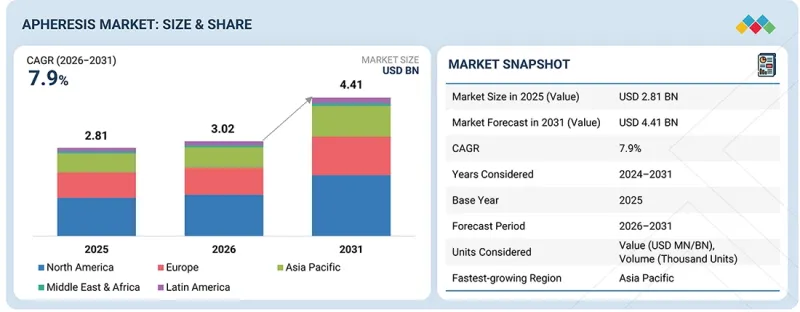

세계의 아페레시스 시장 규모는 2026년 30억 2,000만 달러에서 2031년에는 44억 1,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR 7.9%로 성장할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 최종사용자별, 시술별, 제품별, 기술별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

혈액 질환, 자가면역 질환, 신경질환, 신장 질환의 발병률 증가에 더해, 전 세계에서 혈액 성분 및 혈장 유래 제품에 대한 높은 수요가 견인하는 가운데, 아페레시스 기기 및 기술에 대한 수요는 꾸준히 확대되고 있습니다. 병원, 혈액은행, 전문 클리닉에서 치료용 및 기증자용 아페레시스 기술의 활용이 확대되면서 시장 성장을 지원하고 있습니다. 현재 의료 기관에서는 채혈 효율을 높이고 환자의 예후를 개선하기 위해, 고효율이며 완전 자동화되고 환자에게 편리한 아페레시스 시스템 개발에 주력하고 있습니다. 또한 자동 혈액 성분 분리 장치나 연속 유동 원심분리기 등의 기술 혁신도 시장 성장에 기여하고 있습니다. 또한 개발도상국에서의 채혈 시설 확충과 의료 기관의 노력 덕분에 효과적인 혈액 관리가 이루어지고 있으며, 향후 수년간 시장의 강력한 성장이 지속될 것으로 예상됩니다.

“제품별로는 일회용 제품이 시장 점유율의 상당 부분을 차지할 것으로 예상됩니다. '

제품별로는 전 세계 채혈 건수 및 치료용 아페레시스 시술의 증가에 힘입어, 일회용 제품 부문이 전 세계 아페레시스 시장에서 가장 큰 점유율을 차지하고 있습니다. 일회용 키트, 튜브 어셈블리, 바늘 및 채혈 챔버는 무균 상태를 확보하고 오염 위험을 최소화하며 환자와 기증자의 안전을 보호하기 위해 아페레시스 시스템의 필수 구성 요소입니다. 일회용 제품을 반복적으로 사용하거나, 새로운 아페레시스 시술 시마다 제품을 교체하는 것은 안정적인 매출을 창출하고 제품 수요를 확보하는 데 중요한 역할을 하고 있습니다. 혈장 채취, 혈소판 아페레시스, 백혈구 아페레시스 및 치료용 혈장 교환 시술 건수의 증가 역시 일회용 제품 부문의 성장을 이끄는 또 다른 중요한 요인입니다. 또한 혈장 유래 치료제에 대한 수요 증가, 헌혈 증가, 그리고 자동 아페레시스 기술의 보급 확대도 일회용 제품의 사용 확대에 기여하고 있습니다.

“기술별로는 2025년에 혈장 분리 부문이 가장 큰 점유율을 차지할 것으로 예상됩니다. ” '

시술 유형별로는 면역계, 신경계, 혈액계 질환 치료에 사용되는 혈장 유래 요법에 대한 전 세계적 수요 증가를 배경으로, 혈장 분리법 부문이 아페레시스 시장에서 가장 큰 시장 점유율을 차지하고 있습니다. 혈장 분리법은 혈장의 분리 및 채취에 있으며, 높은 효율성을 발휘하며, 혈액의 다른 성분을 체내로 되돌릴 수 있으므로 기증자 혈장 채취나 혈장 교환 요법의 시행에 널리 활용되고 있습니다. 자가면역 질환의 발병률 증가, 면역글로불린 및 응고 인자에 대한 수요 증가, 그리고 전 세계 혈장 기증 건수의 증가 역시 해당 부문의 성장을 지원하는 요인으로 작용하고 있습니다. 또한 혈액센터와 병원에서 혈장 분리법의 보급은 공정의 효율화와 기증자의 안전성 및 생산성 향상을 초래하는 자동화 혈장 분리 기술의 최근 동향에 힘입어 촉진되고 있습니다.

2025년, 지역별로는 북미가 아페레시스 시장에서 가장 큰 점유율을 차지했습니다.

아페레시스 시장은 북미, 유럽, 라틴아메리카, 아시아태평양, 중동 및 아프리카로 구분됩니다. 북미는 전 세계 아페레시스 시장을 선도하고 있으며, 이러한 우위는 혈액 질환, 자가면역 질환, 신경질환, 신장 질환의 유병률이 높다는 점과 혈장 유래 제품 및 혈액 성분에 대한 꾸준한 수요에 기인합니다. 이 지역은 광범위한 의료 및 헌혈 네트워크, 아페레시스 기술의 보급, 주요 시장 진출 기업 및 혈장 채취 기업의 진출과 같은 혜택을 누리고 있습니다. 또한 헌혈에 대한 의식의 향상, 아페레시스 치료 사례 증가, 유리한 환급 정책, 수혈 의학 및 혈장 채취 시설에 대한 투자가 해당 지역의 시장 우위 확보에 기여하고 있습니다.

아페레시스 시장의 주요 기업으로는 Terumo Corporation(일본), Fresenius SE & Co. KGaA(독일), Haemonetics Corporation(미국), Fresenius Medical Care AG(독일), Asahi Kasei Medical(일본), Becton, Dickinson and Company(미국), Macopharma SA(프랑스), Miltenyi Biotec(독일), Therakos LLC(미국), Toray Industries Inc.(일본), Kaneka Corporation(일본), 그리고 B. Braun SE(독일) 등이 있습니다.

조사 범위

이 보고서에서는 아페레시스 시장을 제품, 유형, 시술법, 기술, 최종사용자 및 지역별로 분석하고 있습니다. 또한 시장 성장에 영향을 미치는 요인을 포괄적으로 다루고, 시장내 기회와 과제를 분석하는 한편, 시장 선도 기업 간의 경쟁 구도에 대한 상세한 정보를 제공하고 있습니다. 또한 이 보고서에서는 개별 동향을 바탕으로 마이크로마켓을 분석하고, 5개 주요 지역(및 해당 지역내 각국)의 시장 부문별 매출 전망을 제시하고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 기존 기업뿐만 아니라 신규 진입 기업 및 중소규모 기업에게도 시장 동향을 파악하는 데 도움이 되며, 결과적으로 시장 점유율 확대로 이어질 것입니다. 이 보고서를 구매하신 기업은 다음 전략 중 하나 또는 여러 가지를 조합하여 활용함으로써 시장에서 입지를 강화할 수 있습니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

주요 촉진요인 분석(자가면역 질환 및 신경질환 유병률 상승, 바이오의약품 기업의 혈장 유래 바이오의약품 활용 확대, 혈액 성분에 대한 수요 증가, 수혈 안전성에 대한 중요성 부각, 복잡한 종양학 및 이식 수술 건수 증가, 성분별 채혈 기술의 발전, 그리고 세포·유전자 치료의 보급 확대) , 제약 요인(아페레시스 기술 도입을 제한하는 높은 시술 및 운영 비용, 신흥 국가에서의 아페레시스 헌혈 시술의 제한적인 도입, 아페레시스 시술을 제약하는 엄격한 기증자 적격 기준과 기증자 확보의 어려움, 그리고 아페레시스 시술 도입에 영향을 미치는 숙련된 전문가의 부족), 기회(백혈병 및 소아 환자에 대한 아페레시스 시술 도입이 아페레시스 시장의 성장 기회를 창출하고 있다는 점 및 정부와 주요 업계 참여 기업의 신흥 시장 투자 확대), 그리고 과제(시술과 관련된 유해 사건의 위험, 수혈을 통한 감염 위험, 그리고 신흥 국가의 미흡한 혈액 선별 검사 인프라)가 아페레시스 시장의 성장에 영향을 미치고 있습니다.

- 시장 침투도: 아페레시스 시장의 주요 기업이 제공하는 제품 포트폴리오에 대한 포괄적인 정보

- 제품 개발/혁신: 아페레시스 시장의 향후 동향, 연구개발 활동 및 제품 개발에 대한 심층적인 인사이트

- 시장 개발: 수익성이 높은 신흥 지역에 대한 포괄적인 정보

- 시장의 다각화: 아페레시스 시장의 신제품, 성장 지역 및 최근 동향에 관한 포괄적인 정보

- 경쟁사 분석: 시장 세분화, 성장 전략, 매출 분석 및 주요 시장 참여자의 제품에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 아페레시스 시장(유형별)

제10장 아페레시스 시장(최종사용자별)

제11장 아페레시스 시장(시술별)

제12장 아페레시스 시장(제품별)

제13장 아페레시스 시장(기술별)

제14장 아페레시스 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.06.25The global apheresis market is projected to reach USD 4.41 billion by 2031 from USD 3.02 billion in 2026, growing at a CAGR of 7.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Type, Procedure, Technology, End User, and region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa |

The demand for apheresis equipment and techniques is growing steadily, driven by the rising incidence of hematological, autoimmune, neurological, and renal diseases, as well as the high demand for blood components and plasma-based products worldwide. Increasing use of therapeutic and donor apheresis techniques in hospitals, blood banks, and specialized clinics is supporting the growth of the market. Healthcare facilities are now focusing on developing highly efficient, fully automated, and patient-friendly apheresis systems to increase collection efficacy and improve patient outcomes. Additionally, technological innovations, including automated blood component separators and continuous flow centrifuges, are contributing to market growth. Moreover, improved blood collection facilities in developing countries and healthcare organizations' initiatives ensure effective blood management and are expected to sustain strong market growth in the coming years.

"By product, the disposables are projected to capture a significant market share."

By product, the disposables category holds the largest share of the global apheresis market, driven by rising numbers of blood collections and therapeutic apheresis procedures worldwide. Disposable kits, tubing assemblies, needles, and collection chambers are vital components of apheresis systems, as they ensure sterility, minimize the risk of contamination, and safeguard patients and donors. The repeated consumption of disposables and their replacement at each new apheresis procedure play a significant role in generating consistent revenue and ensuring product demand. The growing number of plasma collection, plateletpheresis, leukapheresis, and therapeutic plasma exchange procedures is another important factor driving growth in the disposables category. In addition, the increasing demand for plasma-based therapeutics, the rise in blood donations, and the growing acceptance of automated apheresis technology are contributing to the growing use of disposables.

"By procedure, the plasmapheresis segment is expected to register the highest share in 2025."

By procedure, the plasmapheresis segment holds the largest market share in the apheresis market, driven by growing worldwide demand for plasma-derived therapies used to treat immunological, neurological, and hematological conditions. The plasmapheresis method is widely applied for obtaining donor plasma as well as conducting plasma exchange therapy, since it is highly efficient in plasma separation and collection while other components of the blood are returned to the body. Growth in the incidence of autoimmune diseases, higher demand for immunoglobulins and coagulation factors, and an increasing number of plasma donations worldwide are additional factors supporting the segment's growth. Additionally, the widespread use of plasmapheresis procedures in blood centers and hospitals is facilitated by recent developments in automated plasmapheresis technology, which increase process efficiency and improve donor safety and productivity.

In 2025, North America accounted for the largest market share of the apheresis market by region.

The apheresis market is segmented into North America, Europe, Latin America, Asia-Pacific, and the Middle East & Africa. North America leads the global apheresis market; this dominance is attributed to the high incidence of hematological, autoimmune, neurological, and renal disorders, as well as robust demand for plasma-based products and blood components. The region benefits from an extensive healthcare and blood donation network, widespread use of apheresis techniques, and the involvement of major market players and plasma collection companies. In addition, increased awareness of blood donation, rising cases of apheresis treatment, favorable reimbursement policies, and investment in transfusion medicine and plasma collection facilities contribute to the market's dominance in the region.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-40%, Tier 2-35%, and Tier 3- 25%

- By Designation: Directors-23%, Managers-30%, and Others-47%

- By Region: North America-25%, Europe-35%, the Asia Pacific-20%, Latin America- 13%, and the Middle East & Africa- 7%

The prominent players in the apheresis market include Terumo Corporation (Japan), Fresenius SE & Co. KGaA (Germany), Haemonetics Corporation (US), Fresenius Medical Care AG (Germany), Asahi Kasei Medical Co., Ltd. (Japan), Becton, Dickinson and Company (US), Macopharma SA (France), Miltenyi Biotec (Germany), Therakos LLC (US), Toray Industries Inc. (Japan), Kaneka Corporation (Japan), and B. Braun SE (Germany).

Research Coverage

This report examines the apheresis market by product, type, procedure, technology, end user, and region. It also covers the factors affecting market growth, analyzes the opportunities and challenges in the market, and provides details on the competitive landscape among market leaders. Furthermore, the report analyzes micro-markets by their individual growth trends and forecasts revenue for market segments across five main regions (and the countries within these regions).

Reasons to Buy the Report

The report will enable established firms, as well as entrants/smaller firms, to gauge the market pulse, which, in turn, will help them gain a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

Analysis of key drivers (rising prevalence of autoimmune and neurological disorders, increasing utilization of plasma-derived biologics by biopharmaceutical companies, rising demand for blood components, increasing emphasis on transfusion safety, growing volume of complex oncological and transplant procedures, technological improvements in component-specific blood collection, and expanding adoption of cell and gene therapies), restraints (high procedural and operational costs limiting adoption of apheresis technologies, limited adoption of apheresis donation procedures in emerging economies, stringent donor eligibility criteria and limited donor availability restraining apheresis procedures and dearth of skilled professionals impacting the adoption of apheresis procedures), opportunities (adoption of apheresis procedures in leukemia and pediatric patients creating growth opportunities for the apheresis market, and growing investments in emerging markets by governments and key industry players), and challenges (risk of procedure-related adverse events and risk of transfusion-transmitted infections and inadequate blood screening infrastructure in emerging countries) influencing the growth of apheresis market

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the apheresis market

- Product Development/Innovation: Detailed insights into the upcoming trends, R&D activities, and product developments in the apheresis market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the apheresis market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 PRODUCT DEFINITION

- 1.2.2 TECHNOLOGY DEFINITION

- 1.2.3 PROCEDURE DEFINITION

- 1.2.4 END USER DEFINITION

- 1.2.5 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN APHERESIS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 APHERESIS MARKET OVERVIEW

- 3.2 ASIA PACIFIC: APHERESIS MARKET, BY COUNTRY AND END USER

- 3.3 GEOGRAPHIC SNAPSHOT OF APHERESIS MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising prevalence of autoimmune and neurological disorders driving demand for therapeutic apheresis procedures

- 4.2.1.2 Rising demand for blood components and increasing emphasis on transfusion safety to support market expansion

- 4.2.1.3 Growing volume of complex oncological and transplant procedures to support growth of apheresis

- 4.2.1.4 Technological improvements in component-specific blood collection to support market expansion

- 4.2.1.5 Expanding adoption of cell and gene therapies to create growth opportunities for apheresis market

- 4.2.2 RESTRAINTS

- 4.2.2.1 High procedural and operational costs limit adoption of apheresis technologies

- 4.2.2.2 Limited adoption of apheresis donation procedures in emerging economies

- 4.2.2.3 Stringent donor eligibility criteria and limited donor availability to restrain apheresis procedures

- 4.2.2.4 Dearth of skilled professionals impacting adoption of apheresis procedures

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Adoption of apheresis procedures in leukemia and pediatric patients creating growth opportunities

- 4.2.3.2 Growing investments in emerging markets by governments and key industry players

- 4.2.4 CHALLENGES

- 4.2.4.1 Risk of procedure-related adverse events and donor safety concerns

- 4.2.4.2 Risk of transfusion-transmitted infections and inadequate blood screening infrastructure in emerging countries

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN APHERESIS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES IN APHERESIS MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT FROM NEW ENTRANTS

- 5.1.2 THREAT FROM SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 MANUFACTURERS

- 5.5.2 END USERS

- 5.5.3 REGULATORY BODIES

- 5.6 PRICING ANALYSIS

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA (HS CODE 901890)

- 5.7.2 EXPORT DATA FOR (HS CODE 901890)

- 5.8 REIMBURSEMENT SCENARIO

- 5.9 KEY CONFERENCES & EVENTS, 2026-2027

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.11 INVESTMENT & FUNDING SCENARIO

- 5.12 CASE STUDY ANALYSIS

- 5.13 IMPACT OF 2025 US TARIFF

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRY/REGION

- 5.13.5 IMPACT ON END-USE SEGMENTS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Automation and AI-enabled procedure optimization in apheresis systems

- 6.1.1.2 Closed-loop and automated cell therapy collection/manufacturing workflows

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Real-time biosensors and digital monitoring in apheresis procedures

- 6.1.2.2 RFID, barcode, and digital traceability technologies in blood and cell collection management

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Cell and gene therapy manufacturing technologies

- 6.1.3.2 Therapeutic filtration, adsorption, and extracorporeal blood purification technologies

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR TERM (2025-2027)

- 6.2.2 MID-TERM (2028-2030)

- 6.2.3 LONG TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-ENABLED AND DATA-DRIVEN APHERESIS PROCEDURE OPTIMIZATION

- 6.4.2 PERSONALIZED THERAPEUTIC APHERESIS

- 6.4.3 CONNECTED APHERESIS WORKFLOWS AND DIGITAL TRACEABILITY

- 6.5 IMPACT OF AI/GEN AI ON APHERESIS

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL OF AI IN APHERESIS

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.4 Latin America

- 7.1.1.5 Middle East & Africa

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 REDUCING SINGLE-USE APHERESIS WASTE

- 7.2.2 USE OF LOWER-IMPACT MATERIALS AND PACKAGING

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 APHERESIS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 DONOR APHERESIS

- 9.2.1 INCREASING BLOOD DONATIONS AND EXPANDING CELL THERAPY COLLECTIONS TO SUPPORT DONOR APHERESIS MARKET GROWTH

- 9.3 THERAPEUTIC APHERESIS

- 9.3.1 GROWING CLINICAL UTILIZATION OF THERAPEUTIC PLASMA EXCHANGE AND EXPANDING NEUROLOGICAL APPLICATIONS TO DRIVE MARKET

- 9.4 NEUROLOGICAL DISORDERS

- 9.4.1 GROWING BURDEN OF NEUROLOGICAL DISORDERS TO DRIVE MARKET GROWTH

- 9.5 BLOOD DISORDERS

- 9.5.1 RISING PREVALENCE OF HEMATOLOGICAL AND GENETIC BLOOD DISORDERS TO DRIVE DEMAND

- 9.6 RENAL DISORDERS

- 9.6.1 RISING BURDEN OF CHRONIC KIDNEY DISEASE AND AUTOIMMUNE RENAL COMPLICATIONS TO DRIVE DEMAND

- 9.7 AUTOIMMUNE DISORDERS

- 9.7.1 INCREASING PREVALENCE OF AUTOIMMUNE DISORDERS AND CONTINUED CLINICAL IMPORTANCE OF THERAPEUTIC APHERESIS TO DRIVE GROWTH

- 9.8 METABOLIC DISORDERS

- 9.8.1 GROWING BURDEN OF DIABETES AND METABOLIC CONDITIONS TO SUPPORT THERAPEUTIC APHERESIS MARKET GROWTH

- 9.9 CARDIOVASCULAR DISORDERS

- 9.9.1 RISING LONG-TERM BURDEN OF CARDIOVASCULAR DISORDERS TO DRIVE MARKET GROWTH

- 9.10 OTHER DISORDERS

10 APHERESIS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 BLOOD COLLECTION CENTERS & BLOOD COMPONENT PROVIDERS

- 10.2.1 INCREASING DEMAND FOR COMPONENT-SPECIFIC BLOOD COLLECTION AND COMMERCIAL PLASMA SUPPLY TO DRIVE MARKET GROWTH

- 10.3 HOSPITALS & TRANSFUSION CENTERS

- 10.3.1 EXPANDING TRANSFUSION REQUIREMENTS IN ONCOLOGY, TRANSPLANT, AND CRITICAL CARE SETTINGS TO DRIVE MARKET GROWTH

- 10.4 OTHER END USERS

11 APHERESIS MARKET, BY PROCEDURE

- 11.1 INTRODUCTION

- 11.2 PLASMAPHERESIS

- 11.2.1 INCREASING GLOBAL DEMAND FOR PLASMA-DERIVED THERAPIES AND THERAPEUTIC PLASMA EXCHANGE TO DRIVE MARKET GROWTH

- 11.3 PLATELETAPHERESIS

- 11.3.1 INCREASING DEMAND FOR PLATELET TRANSFUSIONS IN ONCOLOGY, TRANSPLANT, AND CRITICAL CARE SETTINGS TO DRIVE MARKET GROWTH

- 11.4 ERYTHROCYTAPHERESIS

- 11.4.1 INCREASING BURDEN OF SICKLE CELL DISEASE AND RISING DEMAND FOR TARGETED RED BLOOD CELL EXCHANGE PROCEDURES TO DRIVE GROWTH

- 11.5 LEUKAPHERESIS

- 11.5.1 EXPANDING CELL AND GENE THERAPY PIPELINE AND INCREASING CAR-T CELL MANUFACTURING ACTIVITIES TO DRIVE MARKET GROWTH

- 11.6 PHOTOPHERESIS

- 11.6.1 INCREASING TRANSPLANT PROCEDURES AND RISING USE OF IMMUNE-MODULATING THERAPIES TO SUPPORT MARKET GROWTH

- 11.7 OTHER PROCEDURES

12 APHERESIS MARKET, BY PRODUCT

- 12.1 INTRODUCTION

- 12.2 APHERESIS DEVICES

- 12.2.1 RISING DEMAND FOR PLASMA-DERIVED THERAPIES TO DRIVE SEGMENT GROWTH

- 12.3 APHERESIS DISPOSABLES

- 12.3.1 RECURRING UTILIZATION OF SINGLE-USE CONSUMABLES AND RISING THERAPEUTIC PROCEDURE VOLUMES TO DRIVE GROWTH

13 APHERESIS MARKET, BY TECHNOLOGY

- 13.1 INTRODUCTION

- 13.2 CENTRIFUGATION

- 13.3 CONTINUOUS FLOW CENTRIFUGATION

- 13.3.1 INCREASING NEED FOR HIGH-THROUGHPUT BLOOD COMPONENT COLLECTION AND EFFICIENT PLASMA PROCESSING TO DRIVE GROWTH

- 13.4 INTERMITTENT FLOW CENTRIFUGATION

- 13.4.1 INCREASING DEMAND FOR COST-EFFECTIVE AND FLEXIBLE APHERESIS SYSTEMS IN HEALTHCARE SETTINGS TO SUPPORT MARKET GROWTH

- 13.5 MEMBRANE SEPARATION

- 13.5.1 INCREASING UTILIZATION OF MEMBRANE-BASED PLASMA FILTRATION TECHNOLOGIES IN THERAPEUTIC APHERESIS TO DRIVE MARKET GROWTH

14 APHERESIS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 14.2.2 US

- 14.2.2.1 Strong economic capacity and high healthcare spending to support north america apheresis market growth

- 14.2.3 CANADA

- 14.2.3.1 Rising demand for blood components and plasma protein products to drive market growth

- 14.3 ASIA PACIFIC

- 14.3.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 14.3.2 CHINA

- 14.3.2.1 Expanding healthcare infrastructure and growing demand for advanced blood management procedures to accelerate growth

- 14.3.3 JAPAN

- 14.3.3.1 Aging-driven treatment demand and advanced hospital infrastructure to support market growth

- 14.3.4 INDIA

- 14.3.4.1 Large patient base and expanding healthcare infrastructure to drive market

- 14.3.5 AUSTRALIA

- 14.3.5.1 Strong healthcare infrastructure and growing demand for specialized therapies to support market growth

- 14.3.6 SOUTH KOREA

- 14.3.6.1 Advanced healthcare technologies and growing specialty care adoption to support market growth

- 14.3.7 THAILAND

- 14.3.7.1 Expanding specialty care infrastructure and rising chronic disease burden to support market growth

- 14.3.8 SINGAPORE

- 14.3.8.1 Advanced healthcare infrastructure and regional medical hub status to support market growth

- 14.3.9 REST OF ASIA PACIFIC

- 14.4 EUROPE

- 14.4.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 14.4.2 GERMANY

- 14.4.2.1 High healthcare spending and strong reimbursement support to drive market growth

- 14.4.3 FRANCE

- 14.4.3.1 Centralized healthcare system and growing therapeutic apheresis utilization to propel growth

- 14.4.4 ITALY

- 14.4.4.1 Rising elderly population and growing demand for therapeutic procedures to drive growth

- 14.4.5 UK

- 14.4.5.1 Expanding apheresis infrastructure and specialized care services to support market growth

- 14.4.6 SPAIN

- 14.4.6.1 Growing chronic disease burden and expanding specialty treatment centers to support market growth

- 14.4.7 SWITZERLAND

- 14.4.7.1 Advanced healthcare funding and specialized treatment capabilities to support growth

- 14.4.8 NETHERLANDS

- 14.4.8.1 Advanced healthcare infrastructure and strong academic network to support market

- 14.4.9 REST OF EUROPE

- 14.5 LATIN AMERICA

- 14.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 14.5.2 BRAZIL

- 14.5.2.1 Cancer burden, blood donation recovery, and CAR-T access to strengthen market growth

- 14.5.3 MEXICO

- 14.5.3.1 Expanding leukemia treatment access and rising blood component demand to support market growth

- 14.5.4 REST OF LATIN AMERICA

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 14.6.2 GCC COUNTRIES

- 14.6.2.1 Expanding advanced healthcare infrastructure and cell therapy capabilities to support market

- 14.6.3 KINGDOM OF SAUDI ARABIA (KSA)

- 14.6.3.1 Expanding cell therapy infrastructure and clinical trial ecosystem to support market growth

- 14.6.3.2 United Arab Emirates (UAE)

- 14.6.3.2.1 Growing precision medicine initiatives and advanced oncology capabilities to support market growth

- 14.6.4 OTHER GCC COUNTRIES

- 14.6.5 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGY/RIGHT TO WIN, 2023-2026

- 15.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN APHERESIS MARKET

- 15.3 REVENUE ANALYSIS, 2023-2025

- 15.4 GLOBAL MARKET SHARE ANALYSIS, 2025

- 15.4.1 US: MARKET SHARE ANALYSIS, 2025

- 15.4.2 EUROPE: MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Product footprint

- 15.5.5.4 Type footprint

- 15.5.5.5 Technology footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7.1 FINANCIAL METRICS

- 15.7.2 COMPANY VALUATION

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES & APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS (APHERESIS PRODUCTS MARKET)

- 16.1.1 TERUMO CORPORATION

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches & approvals

- 16.1.1.3.2 Deals

- 16.1.1.3.3 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 FRESENIUS SE & CO. KGAA

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches

- 16.1.2.3.2 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 FRESENIUS MEDICAL CARE AG

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 HAEMONETICS CORPORATION

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 B. BRAUN SE

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 MnM view

- 16.1.5.3.1 Key strengths/Right to win

- 16.1.5.3.2 Strategic choices

- 16.1.5.3.3 Weaknesses and competitive threats

- 16.1.6 BD

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.6.3.2 Expansions

- 16.1.7 ASAHI KASEI MEDICAL CO., LTD.

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Other developments

- 16.1.8 OTSUKA HOLDINGS CO., LTD.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.9 MEDICA S.P.A

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.10 SUMITOMO BAKELITE CO., LTD.

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 MnM view

- 16.1.10.3.1 Right to win

- 16.1.10.3.2 Strategic choices

- 16.1.10.3.3 Weaknesses & competitive threats

- 16.1.11 KANEKA CORPORATION

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.11.3.2 Expansions

- 16.1.12 VANTIVE

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.12.3.2 Other developments

- 16.1.13 MILTENYI BIOTEC

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.13.3.2 Expansions

- 16.1.14 NIKKISO CO., LTD.

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Deals

- 16.1.14.3.2 Other developments

- 16.1.15 TORAY INDUSTRIES, INC.

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.1 TERUMO CORPORATION

- 16.2 OTHER PLAYERS

- 16.2.1 MACOPHARMA SA

- 16.2.2 INFOMED SA

- 16.2.3 THERAKOS LLC.

- 16.2.4 MEDICAP GMBH

- 16.2.5 HAIER BIOMEDICAL

- 16.2.6 SICHUAN NIGALE BIOTECHNOLOGY CO, LTD.

- 16.2.7 JAFRON BIOMEDICAL CO., LTD.

- 16.2.8 SHANGHAI DAHUA MEDICAL APPARATUS CO., LTD

- 16.2.9 KENTEC MEDICAL

- 16.2.10 SCINOMED LTD.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION METHODOLOGY

- 17.3 MARKET GROWTH RATE PROJECTIONS

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.5.1 GROWTH RATE ASSUMPTIONS

- 17.6 RISK ASSESSMENT

- 17.7 LIMITATIONS

- 17.7.1 METHODOLOGY-RELATED LIMITATIONS

- 17.7.2 SCOPE-RELATED LIMITATIONS

- 17.8 RESEARCH LIMITATIONS

- 17.9 RISK ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGE STORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.3.1 COMPANY INFORMATION

- 18.3.2 COUNTRY ANALYSIS

- 18.3.3 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 18.3.4 COUNTRY-LEVEL VOLUME ANALYSIS

- 18.3.5 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS