|

시장보고서

상품코드

2066268

엔터테인먼트 분야 메타버스 시장 : 제공별, 기술별, 엔터테인먼트 유형별, 지역별 - 세계 예측(-2032년)Metaverse in Entertainment Market by Offering (Hardware, Software, Professional Services), Technology (XR, AI, Blockchain, Cloud & Edge), Entertainment Type (Gaming, Live Events, Sports, Music, Films & TV), and Region - Global Forecast to 2032 |

||||||

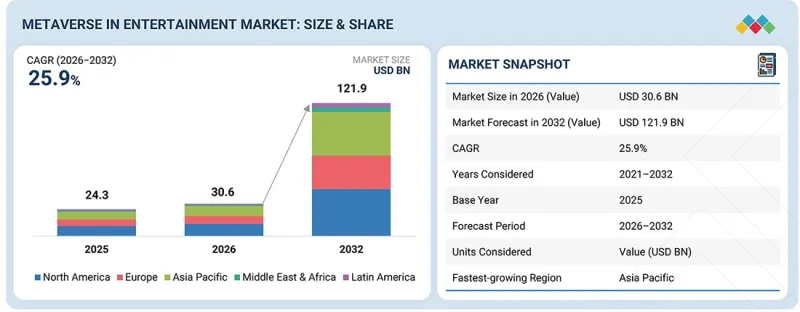

세계의 엔터테인먼트 분야 메타버스 시장 규모는 빠르게 확대하고 있으며, 시장 규모는 2026년 306억 달러에서 2032년까지 1,219억 달러로 크게 확대될 것으로 예측됩니다.

이는 몰입형 가상 엔터테인먼트 환경을 개발하기 위해 게임 기업, 미디어 플랫폼, 스트리밍 제공업체, 기술 공급업체들의 투자가 증가하고 있는 데 그 배경이 있습니다. 이 시장의 성장은 주로 게임, 라이브 이벤트, 스포츠, 음악 콘서트, 가상 영화관 등에서 제공되는 상호작용적이고 실시간적인 디지털 경험에 대한 소비자의 수요 증가에 힘입어 이루어지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 산정 단위 | 금액(10억 달러) |

| 부문 | 제공별, 기술별, 엔터테인먼트 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

증강현실(AR), 가상현실(VR), 혼합현실(MR), 블록체인 및 인공지능(AI) 기술의 도입이 확대됨에 따라, 지속가능하고 몰입감 있는 가상 엔터테인먼트 생태계의 개발이 가속화되고 있습니다. 디지털 아바타, 가상 자산, NFT, 크리에이터 경제 및 가상 소셜 공간의 통합을 통해 엔터테인먼트 제공업체는 시청자의 참여도를 높이고, 맞춤형 경험을 제공하며, 새로운 수익 창출 기회를 확보할 수 있게 됩니다.

“예측 기간 동안 MR 기기가 가장 빠른 성장세를 보일 것으로 전망”

MR 기기는 물리적 환경과 가상 환경을 융합하여 몰입감이 높고 상호작용이 가능한 경험을 구현할 수 있는 능력을 갖추고 있어, 예측 기간 동안 엔터테인먼트 시장의 메타버스 분야에서 가장 빠른 성장을 이룰 것으로 예상됩니다. 이러한 기기들은 혼합 환경에서 디지털 콘텐츠와의 실시간 상호작용을 가능하게 함으로써, 게임, 라이브 엔터테인먼트 행사, 가상 콘서트, 스포츠 중계, 인터랙티브 스토리텔링 등 다양한 분야에서 사용자의 참여도를 높입니다. 실감 나는 가상 체험에 대한 수요가 증가하고 공간 컴퓨팅 기술이 발전함에 따라, 엔터테인먼트 생태계 전반에 걸쳐 MR 기기의 도입이 가속화되고 있습니다.

주요 기술 기업들은 메타버스 기능을 강화하기 위해 혼합현실(MR) 하드웨어와 몰입형 콘텐츠 플랫폼에 대한 투자를 확대하고 있습니다. 예를 들어, 2024년 2월, Apple Inc.는 몰입형 엔터테인먼트, 공간 비디오, 상호작용형 가상 체험을 위한 혼합 현실 기능을 통합한 ‘Apple Vision Pro’를 출시했습니다. 마찬가지로, Meta Platforms, Inc.나 Microsoft Corporation과 같은 기업들도 몰입형 게임, 협업이 가능한 가상 환경, 홀로그램 콘텐츠 체험을 통해 MR 생태계를 지속적으로 확장하고 있습니다. 이러한 움직임에 힘입어 차세대 몰입형 엔터테인먼트 플랫폼에 대한 소비자들의 관심이 높아지고 있습니다. 또한, AI, 제스처 인식, 공간 오디오, 클라우드 렌더링 기술의 통합이 진행됨에 따라 MR 기기의 성능과 사용 편의성이 향상되고 있습니다. 엔터테인먼트 제공업체와 콘텐츠 제작자들은 MR 기술을 활용하여 몰입형 팬 참여 체험, 가상 테마파크, 혼합현실 콘서트, 상호작용형 디지털 이벤트 등을 개발하고 있습니다. 메타버스 플랫폼이 지속적이고 몰입도가 높은 디지털 생태계로 계속 진화함에 따라, MR 기기는 가상과 현실의 엔터테인먼트 환경 간 원활한 상호작용을 가능하게 하는 데 중요한 역할을 할 것으로 기대되며, 이를 통해 예측 기간 동안 시장의 상당한 성장을 견인할 것으로 전망됩니다.

“확장현실(XR)이 가장 큰 시장 점유율을 차지할 것으로 전망”

확장현실(XR)은 게임, 가상 콘서트, 라이브 이벤트, 스포츠 엔터테인먼트, 소셜 참여 플랫폼 등에서 몰입감 있고 상호작용적인 디지털 경험을 구현하는 데 중요한 역할을 하기 때문에 예측 기간 동안 엔터테인먼트 분야의 메타버스 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. XR은 증강현실(AR), 가상현실(VR), 혼합현실(MR) 기술을 결합하여 메타버스 생태계 내에서 사용자의 참여와 실시간 상호작용을 촉진하는, 몰입감이 높은 가상 환경을 창출합니다. 몰입형 디지털 엔터테인먼트 경험에 대한 소비자의 수요가 증가하고, 공간 컴퓨팅 기술이 발전함에 따라 전 세계적으로 XR 도입이 가속화되고 있습니다. 주요 기술 기업과 엔터테인먼트 기업들은 메타버스의 기능을 강화하기 위해 XR 하드웨어, 소프트웨어 플랫폼 및 몰입형 콘텐츠 개발에 막대한 투자를 하고 있습니다. 예를 들어, 2024년 2월, Apple Inc.는 몰입형 엔터테인먼트, 공간 체험 및 혼합 현실(MR)을 통한 상호 작용을 지원하는 ‘Apple Vision Pro’를 출시했습니다. 마찬가지로, Meta Platforms, Inc.도 Quest 생태계와 Horizon 플랫폼을 통해 XR을 활용한 가상 환경 및 메타버스 경험을 지속적으로 확대하고 있습니다.

“북미, 엔터테인먼트 분야의 메타버스 시장을 주도”

예측 기간 동안 북미는 해당 지역 전체에 주요 기술 기업, 게임 플랫폼, 엔터테인먼트 제공업체, 몰입형 기술 혁신 기업들이 강력하게 자리 잡고 있어, 엔터테인먼트 분야 메타버스 시장의 시장 점유율에서 가장 큰 비중을 차지할 것으로 예상됩니다. 가상현실(VR), 증강현실(AR), 혼합현실(MR), 인공지능(AI) 및 클라우드 컴퓨팅 기술의 급속한 보급에 힘입어, 미국과 캐나다에서 몰입형 엔터테인먼트 생태계의 개발이 가속화되고 있습니다. 가상 게임, 몰입형 라이브 이벤트, 디지털 소셜 체험 및 메타버스 기반 콘텐츠 플랫폼에 대한 소비자의 수요가 증가함에 따라, 해당 지역의 시장 성장이 더욱 가속화되고 있습니다.

이 지역은 첨단 디지털 인프라, 높은 인터넷 보급률, 커넥티드 기기의 광범위한 보급, 그리고 공간 컴퓨팅 기술에 대한 투자 확대 등의 혜택을 누리고 있습니다. Meta Platforms, Inc., Microsoft Corporation, Apple Inc., NVIDIA Corporation 등 주요 기업들은 엔터테인먼트 기능을 강화하기 위해 몰입형 하드웨어, 가상 환경, AI 기반 아바타, 메타버스 콘텐츠 생태계에 대한 투자를 지속하고 있습니다. 예를 들어, ‘Apple Vision Pro’의 출시와 Meta의 ‘Horizon’ 생태계 확장은 엔터테인먼트 분야에서 XR의 보급을 지속적으로 뒷받침하고 있습니다.

또한, 게임 기업, 미디어 기관, 스트리밍 플랫폼, 기술 공급업체 간의 협력이 강화됨에 따라 몰입형 엔터테인먼트 경험의 상용화가 가속화되고 있습니다. 가상 콘서트, e스포츠, 몰입형 스포츠 중계, 상호작용형 디지털 팬 참여 플랫폼은 북미 전역에서 큰 주목을 받고 있습니다. 해당 지역의 강력한 혁신 생태계, 디지털 엔터테인먼트에 대한 높은 소비자 지출, 그리고 차세대 몰입형 기술에 대한 지속적인 투자로 인해, 예측 기간 동안 엔터테인먼트 분야의 메타버스 시장에서 북미가 주도적인 위치를 유지할 것으로 예상됩니다.

본 보고서에는 엔터테인먼트 분야의 메타버스 제품을 제공하는 주요 기업에 대한 조사 결과가 포함되어 있습니다. 또한, 자산 성과 관리 시장의 주요 공급업체에 대해서도 소개하고 있습니다. 주요 시장 진출 기업으로는 Roblox(미국), Epic Games(미국), Meta(미국), Microsoft(미국), Take-Two Interactive(미국), Electronic Arts(미국), Apple(미국), Sony Group Corporation(일본), Google(미국), Unity Technologies(미국), Deloitte(영국), Tata Consultancy Services(TCS)(인도), DPVR(중국), 그리고 Capgemini(프랑스) 등이 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 엔터테인먼트 분야 메타버스 시장(제공별)

제10장 엔터테인먼트 분야 메타버스 시장(기술별)

제11장 엔터테인먼트 분야 메타버스 시장(엔터테인먼트 유형별)

제12장 엔터테인먼트 분야 메타버스 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

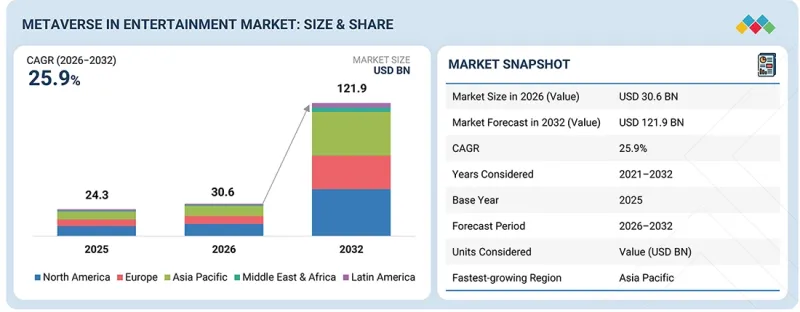

KSM 26.06.30The global metaverse in entertainment market is expanding rapidly, with a projected market size anticipated to rise from USD 30.6 billion in 2026 to USD 121.9 billion by 2032, expanding significantly, with increasing investments from gaming companies, media platforms, streaming providers, and technology vendors to develop immersive virtual entertainment environments. The market growth is primarily driven by rising consumer demand for interactive and real-time digital experiences across gaming, live events, sports, music concerts, and virtual cinemas.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | Offering, Technology, and Entertainment Type |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

The growing adoption of augmented reality (AR), virtual reality (VR), mixed reality (MR), blockchain, and artificial intelligence technologies is accelerating the development of persistent and immersive virtual entertainment ecosystems. Integration of digital avatars, virtual assets, NFTs, creator economies, and virtual social spaces enables enhanced audience engagement, personalized experiences, and new monetization opportunities for entertainment providers.

"MR devices to account for the fastest growth during the forecast period"

MR devices are expected to witness the fastest growth in the metaverse in entertainment market during the forecast period due to their ability to blend physical and virtual environments into highly immersive and interactive experiences. These devices enhance user engagement across gaming, live entertainment events, virtual concerts, sports broadcasting, and interactive storytelling by enabling real-time interaction with digital content in mixed environments. The increasing demand for realistic virtual experiences and advancements in spatial computing technologies are accelerating adoption of MR devices across the entertainment ecosystem.

Major technology companies are increasingly investing in mixed reality hardware and immersive content platforms to strengthen metaverse capabilities. For instance, in February 2024, Apple Inc. launched Apple Vision Pro, integrating mixed reality capabilities for immersive entertainment, spatial video, and interactive virtual experiences. Similarly, companies such as Meta Platforms, Inc. and Microsoft Corporation continue expanding MR ecosystems through immersive gaming, collaborative virtual environments, and holographic content experiences. These developments are increasing consumer interest in next-generation immersive entertainment platforms. Additionally, growing integration of AI, gesture recognition, spatial audio, and cloud rendering technologies is improving the performance and usability of MR devices. Entertainment providers and content creators are leveraging MR technologies to develop immersive fan engagement experiences, virtual theme parks, mixed reality concerts, and interactive digital events. As metaverse platforms continue evolving toward persistent and highly immersive digital ecosystems, MR devices are expected to play a critical role in enabling seamless interaction between virtual and physical entertainment environments, thereby driving significant market growth during the forecast period.

"Extended reality (XR) to account for the largest market share"

Extended Reality (XR) is expected to account for the largest market share in the metaverse in entertainment market during the forecast period due to its critical role in enabling immersive and interactive digital experiences across gaming, virtual concerts, live events, sports entertainment, and social engagement platforms. XR combines augmented reality (AR), virtual reality (VR), and mixed reality (MR) technologies to create highly engaging virtual environments that enhance user participation and real-time interaction within metaverse ecosystems. The growing consumer demand for immersive digital entertainment experiences and advancements in spatial computing technologies are accelerating XR adoption globally. Major technology and entertainment companies are investing heavily in XR hardware, software platforms, and immersive content development to strengthen metaverse capabilities. For instance, in February 2024, Apple Inc. launched Apple Vision Pro, supporting immersive entertainment, spatial experiences, and mixed reality interactions. Similarly, Meta Platforms, Inc. continues expanding XR-driven virtual environments and metaverse experiences through its Quest ecosystem and Horizon platforms.

"North America leads the metaverse in entertainment market"

North America is expected to account for the largest market share in the metaverse in entertainment market during the forecast period due to the strong presence of major technology companies, gaming platforms, entertainment providers, and immersive technology innovators across the region. The rapid adoption of virtual reality (VR), augmented reality (AR), mixed reality (MR), artificial intelligence (AI), and cloud computing technologies is accelerating the development of immersive entertainment ecosystems in the US and Canada. Rising consumer demand for virtual gaming, immersive live events, digital social experiences, and metaverse-based content platforms further supports regional market growth.

The region benefits from advanced digital infrastructure, high internet penetration, widespread adoption of connected devices, and increasing investments in spatial computing technologies. Major companies such as Meta Platforms, Inc., Microsoft Corporation, Apple Inc., and NVIDIA Corporation continue investing in immersive hardware, virtual environments, AI-powered avatars, and metaverse content ecosystems to strengthen entertainment capabilities. For instance, the launch of Apple Vision Pro and the expansion of Meta's Horizon ecosystem continue driving XR adoption across entertainment applications.

Additionally, increasing collaboration between gaming companies, media organizations, streaming platforms, and technology vendors is accelerating the commercialization of immersive entertainment experiences. Virtual concerts, esports, immersive sports broadcasting, and interactive digital fan engagement platforms are gaining significant traction across North America. The region's strong innovation ecosystem, high consumer spending on digital entertainment, and continuous investment in next-generation immersive technologies are expected to maintain North America's leadership position in the metaverse in entertainment market during the forecast period.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the metaverse in entertainment market.

- By Company: Tier I - 34%, Tier II - 43%, and Tier III - 23%

- By Designation: C-Level Executives - 50%, Directors - 30%, and others - 20%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 30%, Middle East & Africa - 5%, and Latin America - 5%

The report includes a study of key players offering metaverse in entertainment products. It profiles major vendors in the asset performance management market. The major market players include Roblox (US), Epic Games (US), Meta (US), Microsoft (US), Take-Two Interactive (US), Electronic Arts (US), Apple (US), Sony Group Corporation (Japan), Google (US), Unity Technologies (US), Deloitte (UK), Tata Consultancy Services (TCS) (India), DPVR (China), and Capgemini (France).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN METAVERSE IN ENTERTAINMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN METAVERSE IN ENTERTAINMENT MARKET

- 3.2 METAVERSE IN ENTERTAINMENT MARKET, BY OFFERING

- 3.3 METAVERSE IN ENTERTAINMENT MARKET, BY HARDWARE

- 3.4 METAVERSE IN ENTERTAINMENT MARKET, BY ENTERTAINMENT TYPE

- 3.5 METAVERSE IN ENTERTAINMENT MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Evolution of gaming platforms into persistent social entertainment ecosystems

- 4.2.1.2 Expanding creator monetization models

- 4.2.1.3 Increasing launch of immersive MR and VR devices

- 4.2.2 RESTRAINTS

- 4.2.2.1 High infrastructure, content, and ecosystem maintenance costs

- 4.2.2.2 Increasing regulatory scrutiny around user safety and digital interactions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding integration of entertainment IPs into virtual worlds

- 4.2.3.2 Expanding in-world advertising, branded experiences, and virtual commerce models

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited interoperability across virtual platforms

- 4.2.4.2 Delivering stable real-time performance during large-scale virtual events and immersive entertainment experiences

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN METAVERSE IN ENTERTAINMENT MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Metaverse in entertainment business models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN GLOBAL METAVERSE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL VIRTUAL REALITY (VR) INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF VR HEADSETS, BY REGION, 2026

- 5.5.2 AVERAGE SELLING PRICE VR HEADSETS, BY KEY PLAYER, 2026

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO

- 5.6.2 IMPORT SCENARIO

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ACCENTURE ENABLED CHANGI AIRPORT GROUP TO BUILD CHANGIVERSE ON ROBLOX FOR IMMERSIVE DIGITAL ENGAGEMENT

- 5.10.2 MONKS ENABLED META AND NBA TO DELIVER IMMERSIVE VR SPORTS VIEWING EXPERIENCES

- 5.10.3 DELOITTE ENABLED DIAGEO TO DELIVER IMMERSIVE VR & AR CONCERT EXPERIENCE FOR JOHNNIE WALKER

- 5.11 IMPACT OF 2025 US TARIFF - METAVERSE IN ENTERTAINMENT MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON ENTERTAINMENT TYPES

- 5.11.5.1 Gaming

- 5.11.5.2 Live events & concerts

- 5.11.5.3 Film & tv (ott & cinematic experiences)

- 5.11.5.4 Sports & esports

- 5.11.5.5 Music & artist engagement

- 5.11.5.6 Social entertainment

- 5.11.5.7 Anime, virtual characters, & ip-based entertainment

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Extended reality (XR)

- 6.1.1.2 Real-time 3D & game engines

- 6.1.1.3 Artificial intelligence (AI)

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Blockchain & digital assets

- 6.1.2.2 Cloud computing & edge computing

- 6.1.2.3 Spatial audio & haptic technologies

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Digital twin technology

- 6.1.3.2 Generative AI content creation

- 6.1.3.3 5G & advanced connectivity infrastructure

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2026-2028) | IMMERSIVE ECOSYSTEM EXPANSION & XR OPTIMIZATION

- 6.2.1.1 Focus areas:

- 6.2.1.1.1 Technology development

- 6.2.1.1.2 Product/Service innovations

- 6.2.1.1.3 Market adoption

- 6.2.1.1 Focus areas:

- 6.2.2 MID-TERM (2028-2031) | PERSISTENT VIRTUAL WORLDS & AI-DRIVEN IMMERSION

- 6.2.2.1 Focus areas

- 6.2.2.1.1 Technology development

- 6.2.2.1.2 Product/Service innovations

- 6.2.2.1.3 Market adoption

- 6.2.2.1 Focus areas

- 6.2.3 LONG-TERM (2031-2035) | FULLY CONNECTED IMMERSIVE ENTERTAINMENT ECOSYSTEMS

- 6.2.3.1 Focus areas

- 6.2.3.1.1 Technology development

- 6.2.3.1.2 Product/Service innovations

- 6.2.3.1.3 Market adoption

- 6.2.3.1 Focus areas

- 6.2.1 SHORT-TERM (2026-2028) | IMMERSIVE ECOSYSTEM EXPANSION & XR OPTIMIZATION

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-DRIVEN VIRTUAL CHARACTERS & INTELLIGENT FAN ENGAGEMENT

- 6.4.2 PERSISTENT CROSS-PLATFORM VIRTUAL WORLDS

- 6.4.3 IMMERSIVE LIVE EVENTS & HYPER-INTERACTIVE CONCERT ECOSYSTEMS

- 6.4.4 AI-GENERATED CONTENT & REAL-TIME VIRTUAL PRODUCTION

- 6.4.5 SPATIAL COMMERCE & VIRTUAL MERCHANDISE ECOSYSTEMS

- 6.5 IMPACT OF AI/GENERATIVE AI ON METAVERSE IN ENTERTAINMENT MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN METAVERSE IN ENTERTAINMENT

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN METAVERSE IN ENTERTAINMENT MARKET

- 6.5.3.1 Enabling Scalable Immersive VR Gaming Experiences Through AI-Driven Cloud Infrastructure

- 6.5.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN METAVERSE IN ENTERTAINMENT MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 ROBLOX: CUBE 3D AND AI-ASSISTED VIRTUAL WORLD CREATION

- 6.6.2 META: GENERATIVE AI TOOLS FOR SOCIAL METAVERSE EXPERIENCES

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS, BY REGION

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Middle East & Africa

- 7.1.2.5 Latin America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS ACROSS ENTERTAINMENT TYPES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY ENTERTAINMENT TYPES

9 METAVERSE IN ENTERTAINMENT MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: METAVERSE IN ENTERTAINMENT MARKET DRIVERS

- 9.2 SOFTWARE

- 9.2.1 TOOLS TO DESIGN, CREATE, & TEST AR, VR, & MR EXPERIENCES

- 9.2.1.1 Expanding developer participation across immersive entertainment ecosystems

- 9.2.2 SOFTWARE: METAVERSE MARKET DRIVERS

- 9.2.3 EXTENDED REALITY SOFTWARE

- 9.2.3.1 Open XR ecosystems and cross-platform software frameworks accelerating spatial entertainment adoption

- 9.2.4 GAMING ENGINES

- 9.2.4.1 Foundation of creator-led immersive entertainment platforms

- 9.2.5 3D MAPPING, MODELING, & RECONSTRUCTION

- 9.2.5.1 Expanding realistic immersive content creation across entertainment platforms

- 9.2.6 METAVERSE PLATFORMS

- 9.2.6.1 Creator economies and user-generated virtual worlds scaling persistent immersive entertainment ecosystems

- 9.2.7 FINANCIAL PLATFORMS

- 9.2.7.1 Virtual commerce, immersive advertising, and digital payments strengthening metaverse entertainment monetization models

- 9.2.8 OTHER SOFTWARE

- 9.2.1 TOOLS TO DESIGN, CREATE, & TEST AR, VR, & MR EXPERIENCES

- 9.3 HARDWARE

- 9.3.1 AR DEVICES

- 9.3.1.1 Expanding immersive entertainment through lightweight spatial experiences and always-connected digital interaction

- 9.3.2 VR DEVICES

- 9.3.2.1 Driving deeply immersive gaming, social, and virtual entertainment ecosystems

- 9.3.3 MR DEVICES

- 9.3.3.1 Redefining premium immersive entertainment experiences

- 9.3.4 DISPLAYS

- 9.3.4.1 Enhancing visual realism across spatial entertainment and virtual experience ecosystems

- 9.3.1 AR DEVICES

- 9.4 PROFESSIONAL SERVICES

- 9.4.1 APPLICATIONS DEVELOPMENT & SYSTEM INTEGRATION.

- 9.4.1.1 Immersive experience deployment increasing demand for real-time 3D integration and spatial computing services

- 9.4.2 STRATEGY & BUSINESS CONSULTING SERVICES

- 9.4.2.1 Enterprises increasingly seeking strategic guidance to commercialize immersive and spatial entertainment ecosystems

- 9.4.1 APPLICATIONS DEVELOPMENT & SYSTEM INTEGRATION.

10 METAVERSE IN ENTERTAINMENT MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.1.1 TECHNOLOGY: METAVERSE IN ENTERTAINMENT MARKET DRIVERS

- 10.2 EXTENDED REALITY (XR)

- 10.2.1 SPATIAL COMPUTING ECOSYSTEMS EXPANDING XR ADOPTION ACROSS IMMERSIVE ENTERTAINMENT AND SHARED DIGITAL EXPERIENCES

- 10.3 REAL-TIME 3D & GAME ENGINES

- 10.3.1 CREATOR ECONOMIES AND REAL-TIME 3D PLATFORMS SCALING PERSISTENT IMMERSIVE ENTERTAINMENT ECOSYSTEMS

- 10.4 BLOCKCHAIN

- 10.4.1 DIGITAL OWNERSHIP AND TOKENIZED ECOSYSTEMS EXPANDING BLOCKCHAIN ADOPTION ACROSS IMMERSIVE ENTERTAINMENT PLATFORMS

- 10.5 CLOUD COMPUTING & EDGE COMPUTING

- 10.5.1 LOW-LATENCY CLOUD INFRASTRUCTURE ENABLING SCALABLE REAL-TIME IMMERSIVE ENTERTAINMENT AND PERSISTENT VIRTUAL EXPERIENCES

- 10.6 ARTIFICIAL INTELLIGENCE (AI)

- 10.6.1 ACCELERATING CONTENT CREATION, PERSONALIZATION, AND INTERACTIVE ENGAGEMENT ACROSS IMMERSIVE ENTERTAINMENT ECOSYSTEMS

- 10.7 OTHER TECHNOLOGIES

11 METAVERSE IN ENTERTAINMENT MARKET, BY ENTERTAINMENT TYPE

- 11.1 INTRODUCTION

- 11.1.1 ENTERTAINMENT TYPE: METAVERSE IN ENTERTAINMENT MARKET DRIVERS

- 11.2 GAMING

- 11.2.1 PERSISTENT VIRTUAL WORLDS DRIVING IMMERSIVE ENTERTAINMENT THROUGH LARGE-SCALE SOCIAL INTERACTION, CREATOR ECONOMIES, AND DIGITAL ENGAGEMENT

- 11.2.2 MASSIVELY MULTIPLAYER VIRTUAL WORLDS

- 11.2.3 USER-GENERATED GAMING PLATFORMS

- 11.2.4 COMPETITIVE & ESPORTS GAMING

- 11.2.5 OTHER GAMING

- 11.3 LIVE EVENTS & CONCERTS

- 11.3.1 IMMERSIVE VIRTUAL EVENTS REDEFINING FAN ENGAGEMENT THROUGH INTERACTIVE, SOCIALLY CONNECTED, AND DIGITALLY MONETIZED ENTERTAINMENT EXPERIENCES

- 11.3.2 TICKETED PREMIUM EVENTS

- 11.3.3 VIRTUAL CONCERTS & MUSIC FESTIVALS

- 11.3.4 BRANDED & SPONSORED VIRTUAL EVENTS

- 11.3.5 OTHER LIVE EVENTS & CONCERTS

- 11.4 FILM & TV (OTT & CINEMATIC EXPERIENCES)

- 11.4.1 INTERACTIVE CINEMATIC ECOSYSTEMS RESHAPING STREAMING THROUGH IMMERSIVE STORYTELLING, VIRTUAL PARTICIPATION, AND FRANCHISE-LED DIGITAL ENGAGEMENT

- 11.4.2 VIRTUAL CINEMAS & SCREENING ROOMS

- 11.4.3 VIRTUAL FILM PREMIERES & PROMOTIONS

- 11.4.4 IMMERSIVE 360°/VR CONTENT

- 11.4.5 OTHER FILM & TV (OTT & CINEMATIC EXPERIENCES)

- 11.5 SPORTS & ESPORTS

- 11.5.1 IMMERSIVE SPORTS ECOSYSTEMS TRANSFORMING SPECTATORSHIP THROUGH VIRTUAL VIEWING, INTERACTIVE PARTICIPATION, AND DIGITALLY CONNECTED FAN COMMUNITIES

- 11.5.2 VIRTUAL STADIUMS & LIVE MATCH VIEWING

- 11.5.3 IMMERSIVE MATCH SIMULATIONS & REPLAYS

- 11.5.4 FANTASY SPORTS & PREDICTIVE GAMING

- 11.5.5 OTHER SPORTS & ESPORTS

- 11.6 MUSIC & ARTIST ENGAGEMENT

- 11.6.1 IMMERSIVE MUSIC ECOSYSTEMS DEEPENING FAN PARTICIPATION THROUGH VIRTUAL PERFORMANCES, DIGITAL OWNERSHIP, AND COMMUNITY-DRIVEN ARTIST ENGAGEMENT

- 11.6.2 VIRTUAL MUSIC EXPERIENCES & PERFORMANCES

- 11.6.3 DIGITAL ALBUMS & NFT DROPS

- 11.6.4 FAN COMMUNITIES & MEMBERSHIP PLATFORMS

- 11.6.5 OTHER MUSIC & ARTIST ENGAGEMENTS

- 11.7 SOCIAL ENTERTAINMENT

- 11.7.1 PERSISTENT VIRTUAL SOCIAL SPACES REDEFINING DIGITAL INTERACTION THROUGH AVATARS, CREATOR ECONOMIES, AND IMMERSIVE COMMUNITY ENGAGEMENT

- 11.7.2 VIRTUAL HANGOUTS & SOCIAL SPACES

- 11.7.3 TRAVEL & EXPLORATION EXPERIENCES

- 11.7.4 VIRTUAL FASHION & IDENTITY EXPERIENCES

- 11.7.5 OTHER SOCIAL ENTERTAINMENTS

- 11.8 ANIME, VIRTUAL CHARACTERS, & IP-BASED ENTERTAINMENT

- 11.8.1 FRANCHISE-DRIVEN VIRTUAL ECOSYSTEMS EXPANDING FAN ENGAGEMENT THROUGH IMMERSIVE WORLDS, DIGITAL IDENTITIES, AND INTERACTIVE IP EXPERIENCES

- 11.8.2 VIRTUAL CHARACTERS & DIGITAL AVATARS

- 11.8.3 ANIME & FRANCHISE-BASED VIRTUAL WORLDS

- 11.8.4 CHARACTER-BASED FAN ENGAGEMENT PLATFORMS

- 11.8.5 VIRTUAL MERCHANDISE & COLLECTIBLES (CHARACTER-LED)

- 11.8.6 OTHER ANIME, VIRTUAL CHARACTERS, & IP-BASED ENTERTAINMENTS

12 METAVERSE IN ENTERTAINMENT MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Leading immersive entertainment through creator platforms, spatial media, and cloud infrastructure

- 12.2.2 CANADA

- 12.2.2.1 Strengthening immersive entertainment through game development talent and expanding digital infrastructure

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 UK

- 12.3.1.1 Strong gaming demand and advanced connectivity strengthening immersive entertainment ecosystem

- 12.3.2 GERMANY

- 12.3.2.1 Strengthening immersive entertainment growth through gaming scale, hardware demand, and edge infrastructure

- 12.3.3 FRANCE

- 12.3.3.1 Strengthening immersive entertainment through strong gaming engagement and expanding digital community ecosystems

- 12.3.4 ITALY

- 12.3.4.1 Expanding software-led gaming and mobile entertainment ecosystems through growing developer and fiber infrastructure

- 12.3.5 REST OF EUROPE

- 12.3.1 UK

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Strengthening immersive entertainment leadership through gaming scale, social platforms, and advanced 5G infrastructure

- 12.4.2 JAPAN

- 12.4.2.1 Strengthening immersive entertainment through console ecosystems, premium IP, and fan-driven gaming culture

- 12.4.3 INDIA

- 12.4.3.1 Expanding immersive entertainment through AVGC-XR policy support, creator ecosystems, and nationwide 5G growth

- 12.4.4 AUSTRALIA & NEW ZEALAND (A&NZ)

- 12.4.4.1 Strengthening global game development and immersive content production ecosystems

- 12.4.5 SOUTH KOREA

- 12.4.5.1 Strengthening global immersive entertainment through gaming, K-content, and advanced 5G infrastructure

- 12.4.6 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 AI-led national programs and hyperscale infrastructure expansion driving high-value cloud services demand

- 12.5.1.2 United Arab Emirates (UAE)

- 12.5.1.2.1 Strengthening position through esports expansion, phygital experiences, and advanced digital infrastructure

- 12.5.1.3 Rest of GCC countries

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Expanding role through gaming production, immersive storytelling, and mobile-first digital engagement

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 LATIN AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Strengthening regions position in gaming and creator-driven immersive entertainment market

- 12.6.2 MEXICO

- 12.6.2.1 Strengthening position through gaming events, creator ecosystems, and youth digital engagement

- 12.6.3 REST OF LATIN AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Hardware footprint

- 13.6.5.4 Software footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.7.1 EVALUATION MATRIX FOR STARTUPS/SMES: CRITERIA WEIGHTAGE

- 13.7.2 PROGRESSIVE COMPANIES

- 13.7.3 RESPONSIVE COMPANIES

- 13.7.4 DYNAMIC COMPANIES

- 13.7.5 STARTING BLOCKS

- 13.7.6 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.7.6.1 Detailed list of key startups/SMEs

- 13.7.6.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 13.8.1 COMPANY VALUATION OF KEY VENDORS

- 13.8.2 FINANCIAL METRICS OF KEY VENDORS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 13.9.2 DEALS

14 COMPANY PROFILES

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS

- 14.2.1 ROBLOX

- 14.2.1.1 Business overview

- 14.2.1.2 Products/Solutions/Services offered

- 14.2.1.3 Recent developments

- 14.2.1.3.1 Product launches and enhancements

- 14.2.1.3.2 Deals

- 14.2.1.4 MnM view

- 14.2.1.4.1 Right to win

- 14.2.1.4.2 Strategic choices

- 14.2.1.4.3 Weaknesses and competitive threats

- 14.2.2 EPIC GAMES

- 14.2.2.1 Business overview

- 14.2.2.2 Products/Solutions/Services offered

- 14.2.2.3 Recent developments

- 14.2.2.3.1 Product launches and enhancements

- 14.2.2.3.2 Deals

- 14.2.2.4 MnM view

- 14.2.2.4.1 Right to win

- 14.2.2.4.2 Strategic choices

- 14.2.2.4.3 Weaknesses and competitive threats

- 14.2.3 META

- 14.2.3.1 Business overview

- 14.2.3.2 Products/Solutions/Services offered

- 14.2.3.3 Recent developments

- 14.2.3.3.1 Product launches and enhancements

- 14.2.3.3.2 Deals

- 14.2.3.4 MnM view

- 14.2.3.4.1 Right to win

- 14.2.3.4.2 Strategic choices

- 14.2.3.4.3 Weaknesses and competitive threats

- 14.2.4 MICROSOFT

- 14.2.4.1 Business overview

- 14.2.4.2 Products/Solutions/Services offered

- 14.2.4.3 Recent developments

- 14.2.4.3.1 Product launches and enhancements

- 14.2.4.3.2 Deals

- 14.2.4.4 MnM view

- 14.2.4.4.1 Right to win

- 14.2.4.4.2 Strategic choices

- 14.2.4.4.3 Weaknesses and competitive threats

- 14.2.5 TAKE-TWO INTERACTIVE

- 14.2.5.1 Business overview

- 14.2.5.2 Products/Solutions/Services offered

- 14.2.5.3 Recent developments

- 14.2.5.3.1 Product launches and enhancements

- 14.2.5.3.2 Deals

- 14.2.5.4 MnM view

- 14.2.5.4.1 Right to win

- 14.2.5.4.2 Strategic choices

- 14.2.5.4.3 Weaknesses and competitive threats

- 14.2.6 ELECTRONICS ARTS

- 14.2.6.1 Business overview

- 14.2.6.2 Products/Solutions/Services offered

- 14.2.6.3 Recent developments

- 14.2.6.3.1 Product launches and enhancements

- 14.2.6.3.2 Deals

- 14.2.7 APPLE

- 14.2.7.1 Business overview

- 14.2.7.2 Products/Solutions/Services offered

- 14.2.7.3 Recent developments

- 14.2.7.3.1 Product launches and enhancements

- 14.2.7.3.2 Deals

- 14.2.8 SONY

- 14.2.8.1 Business overview

- 14.2.8.2 Products/Solutions/Services offered

- 14.2.8.3 Recent developments

- 14.2.8.3.1 Product launches and enhancements

- 14.2.8.3.2 Deals

- 14.2.9 GOOGLE

- 14.2.9.1 Business overview

- 14.2.9.2 Products/Solutions/Services offered

- 14.2.9.3 Recent developments

- 14.2.9.3.1 Product launches and enhancements

- 14.2.9.3.2 Deals

- 14.2.10 UNITY TECHNOLOGIES

- 14.2.10.1 Business overview

- 14.2.10.2 Products/Solutions/Services offered

- 14.2.10.3 Recent developments

- 14.2.10.3.1 Product launches and enhancements

- 14.2.10.3.2 Deals

- 14.2.1 ROBLOX

- 14.3 OTHER PLAYERS

- 14.3.1 DELOITTE

- 14.3.2 TATA CONSULTANCY SERVICES (TCS)

- 14.3.3 DPVR

- 14.3.4 CAPGEMINI

- 14.3.5 PIMAX

- 14.3.6 ROKID

- 14.3.7 MAGIC LEAP

- 14.3.8 TENCENT

- 14.3.9 NETEASE

- 14.3.10 VALVE

- 14.3.11 HTC CORPORATION

- 14.3.12 TCL

- 14.3.13 SAMSUNG ELECTRONICS

- 14.3.14 BYTEDANCE

- 14.3.15 XREAL

- 14.3.16 DECENTRALAND

- 14.3.17 NIANTIC

- 14.3.18 VRCHAT

- 14.3.19 SANDBOX

- 14.3.20 UPLANDME, INC.

- 14.3.21 PLAY FOR DREAM

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Data & list of key secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Breakdown of primary interviews

- 15.1.2.2 Key industry insights

- 15.1.3 MARKET SIZE ESTIMATION

- 15.1.1 SECONDARY DATA

- 15.2 DATA TRIANGULATION

- 15.3 FACTOR ANALYSIS

- 15.3.1 RESEARCH ASSUMPTIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS