|

시장보고서

상품코드

2066955

줄기세포 치료 시장 : 세포 유래별, 유형별, 치료 용도별, 최종사용자별, 지역별 - 세계 예측(-2035년)Stem Cell Therapy Market by Cell Source, Type, Therapeutic Application, End User - Global Forecast to 2035 |

||||||

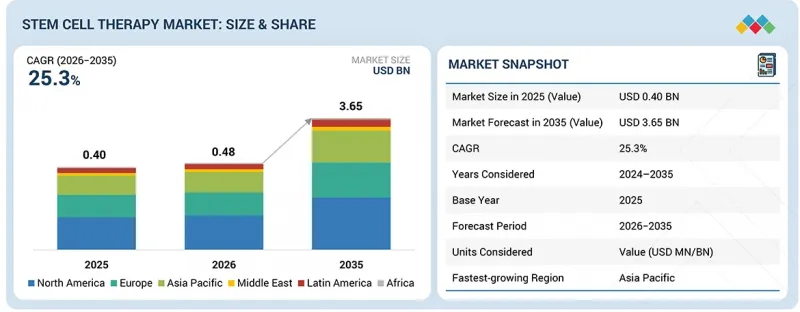

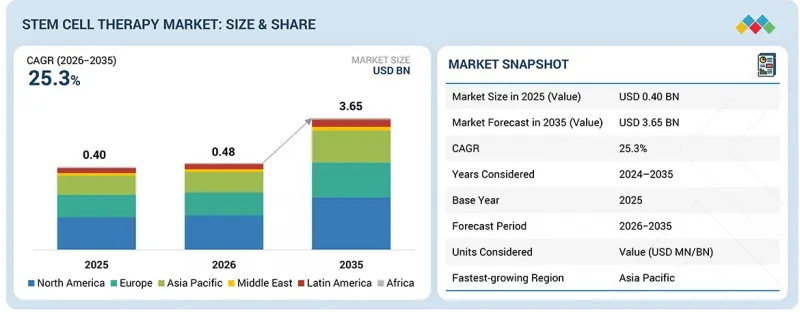

줄기세포 치료 시장 규모는 2026년 4억 8,000만 달러에서 2035년까지 36억 5,000만 달러에 달할 것으로 예측되며, 2026년에서 2035년까지 연평균 성장률(CAGR)은 25.3%를 기록할 전망입니다.

이 시장의 성장을 주도하고 있는 요인은 줄기세포를 활용한 치료법 파이프라인의 확대, 재생의학에 대한 수요 증가, 그리고 iPS 세포 유래 치료법이나 동종 세포 제제와 같은 첨단 치료법의 보급입니다. 시장 전망에 따르면, 세포 처리 및 제조 기술의 발전과 승인된 줄기세포 치료법의 임상 현장 도입 확대에 힘입어 2035년까지 꾸준한 성장이 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2035년 |

| 기준 연도 | 2026년 |

| 예측 기간 | 2026-2035년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 세포 유래별, 유형별, 치료 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

그러나 높은 제조 및 치료 비용, 지역별 복잡한 규제 절차, 실험 단계에서 상업적 생산으로의 규모 확대 과정에서 발생하는 과제, 그리고 전문적인 인프라와 전문 지식의 필요성 등이 시장의 추가적인 성장을 저해할 것으로 예상됩니다.

“예측 기간 동안 줄기세포 치료 시장 내에서 iPS 세포(유도 만능 줄기세포) 부문이 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다.”

세포 출처에 따라 줄기세포 치료 시장은 지방 조직 유래 MSC, 골수 유래 MSC, 태반/제대 유래 MSC, 유도 만능 줄기세포, 배아 줄기세포, 조직 특이적 줄기세포 및 기타 세포 출처로 크게 분류됩니다. 유도 만능 줄기세포(iPSC) 부문은 비교적 낮은 수익 기반에서 출발했으나, 높은 잠재력을 지닌 연구 플랫폼에서 초기 상업적 검증 단계로 전환되고 있기 때문에 줄기세포 치료 시장에서 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. iPS 세포는 도파민 작용성 뉴런, 심근 세포, 망막 세포, 췌장 β세포 유사 세포, 그 밖의 조직 특이적 세포 등 여러 가지 치료용 세포 유형으로 분화할 수 있는, 재생 가능하고 확장성이 뛰어난 세포 공급원을 제공합니다. 따라서 파킨슨병, 심부전, 당뇨병, 망막 질환, 기타 퇴행성 질환 등 의료적 요구가 충분히 충족되지 않은 적응증 분야에서 iPS 세포는 매력적인 선택지로 떠오르고 있습니다.

“2025년 시점에서, 줄기세포 치료 시장에서 유형별로는 동종 줄기세포 치료가 가장 큰 점유율을 차지했습니다.”

유형별로 보면 전 세계 줄기세포 치료 시장은 동종 줄기세포 치료와 자가 줄기세포 치료로 구분됩니다. 2025년, 동종 줄기세포 치료 부문은 확장성, 즉시 사용 가능성 확보, 그리고 상업적 생산 측면에서의 비용 우위 덕분에 줄기세포 치료 시장에서 가장 큰 점유율을 차지했습니다. 이러한 치료법은 임상 및 상업적 적용에 필수적인 표준화된 생산과 환자들의 폭넓은 접근을 가능하게 합니다. 또한, 동종 세포 치료제 후보 파이프라인의 확대, 규제 당국의 승인 증가, 그리고 상업적 규모의 생산 활동 확대로 인해 이 부문 세계 시장 내 선도적 입지는 지속적으로 강화되고 있습니다.

“2026년부터 2035년까지, 줄기세포 치료 시장에서 유럽이 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다.”

줄기세포 치료 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 구분됩니다. 예측 기간 동안 유럽은 첨단 치료 의약품(ATMP)에 대한 견고한 규제 체계, 이식 및 세포 치료 인프라 확충, 활발한 임상시험 활동, 그리고 확장 가능한 ATMP 제조에 대한 투자 증가에 힘입어 줄기세포 치료 시장에서 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 유럽의약품청(EMA)은 대대적인 조작이 가해졌거나 비동종 유래인 줄기세포 제품을 ATMP로 분류하고 있으며, 첨단치료전문위원회를 설치함으로써 줄기세포 기반 제품의 평가, 과학적 자문 및 시장 승인을 위한 명확한 절차를 확립하고 있습니다.

본 보고서에서 다룬 기업 개요 목록

세계 줄기세포 치료 시장의 주요 기업으로는 Vericel Corporation(미국), Mesoblast(호주), MEDIPOST(한국), JCR Pharmaceuticals(일본), Takeda Pharmaceutical Company Limited(일본), Anterogen(한국), CorestemChemon Inc./Corestem, Inc.(한국), Vertex Pharmaceuticals(미국), Pharmicell(한국), Holostem Terapie Avanzate Srl(이탈리아), Stempeutics Research Pvt. Ltd.(인도), Cipla Limited(인도), Bayer AG(독일), Aspen Neuroscience(미국), Longeveron Inc.(미국), 그리고 Smith+Nephew(영국) 등이 있습니다.

조사 범위

본 조사 보고서에서는 줄기세포 치료 시장을 ‘세포 출처’(지방 조직 유래 중간엽 줄기세포, 골수 유래 중간엽 줄기세포, 태반/제대 유래 중간엽 줄기세포, 유도 만능 줄기세포, 배아 줄기세포, 조직 특이적 줄기세포, 기타 세포 출처), 유형(동종 줄기세포 치료, 자가 줄기세포 치료), 치료 용도(근골격계 질환, 상처·외과 수술, 염증성·자가면역 질환, 심혈관질환, 신경계 질환, 당뇨병·대사성 질환, 기타 치료 용도), 최종사용자(병원, 전문 클리닉/줄기세포 클리닉, 기타 최종사용자), 및 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)

본 보고서의 조사 범위에는 줄기세포 치료 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 과제, 기회, 제약 등)에 관한 상세한 정보가 포함되어 있습니다. 주요 업계 기업들에 대한 상세한 분석을 통해 각 기업의 사업 개요, 제품 포트폴리오, 제품 및 서비스의 승인 및 출시, 제휴, 파트너십, 사업 확장, 계약, 그리고 줄기세포 치료 시장과 관련된 최근 동향 등 주요 전략에 대한 인사이트를 제공합니다. 본 보고서에서는 줄기세포 치료 시장 생태계 내 주요 기업 및 신생 스타트업 기업들의 경쟁 구도를 포괄적으로 분석하고 있습니다.

본 보고서를 구매할 때의 주요 이점

본 보고서는 줄기세포 치료 시장 전체 및 그 하위 부문의 매출에 대해 가장 정확한 추정치를 제공함으로써, 시장을 선도하는 기업과 신규 진입 기업을 지원합니다. 또한, 이해관계자들이 경쟁 구도를 더 깊이 이해하고, 비즈니스를 보다 효과적으로 포지셔닝하며, 적절한 시장 진입 전략을 수립하는 데 필요한 인사이트를 얻는 데에도 도움이 됩니다. 본 보고서를 통해 이해관계자들은 시장 동향을 파악하고, 주요 시장 촉진요인, 억제요인, 기회 및 과제에 관한 정보를 얻을 수 있습니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인 분석(규제 당국별 승인 증가로 인해 줄기세포 치료가 실용적인 상업적 치료법으로 자리 잡아가고 있는 점, 희귀질환 및 만성질환 분야에서 높은 미충족 의료 수요가 근치적 치료법에 대한 수요를 견인하고 있다는 점, 유전자 변형 HSPC 요법이 줄기세포 치료 시장에서 고부가가치 부문을 창출하고 있다는 점, 동종 이식 및 기성(오프-더-셸프) 접근법이 자가 요법에 비해 확장성을 향상시키고 있다는 점), 제약요인(높은 치료비와 보험 급여의 불확실성이 여전히 시장 도입에 있어 가장 큰 제약요인으로 작용하고 있다는 점, 제조 과정의 복잡성과 높은 원가가 확장성과 이익률을 제한하고 있다는 점, 일부 재생의학 적응증에 대한 임상적 근거의 불일치가 지불자 및 의사의 신뢰를 저하시키고 있다는 점, 국가 간 규제 불일치가 전 세계적인 상용화를 복잡하게 만들고 있다는 점.), 기회(iPSC 유래 치료법은 확장 가능한 세포 대체 요법으로서 장기적인 기회를 제공하며, 동종 MSC 및 전구세포 플랫폼은 맞춤형 치료의 범위를 넘어 접근성을 확대할 수 있을 뿐만 아니라, 신경계, 심혈관계, 대사계, 안과 질환으로의 확장을 통해 시장의 가능성을 넓힐 수 있으며, 유전자 변형 HSPC 요법은 더 젊은 연령대의 환자 및 기타 헤모글로빈 질환, 면역 질환, 대사성 질환으로의 적용을 확대할 수 있습니다), 및 과제(효능 시험 및 제품 특성 평가의 과제, 이질성이 높은 재생의료 적응증에서 명확한 임상적 유효성을 입증하기 어려운 점, 공정 변경 후 제조의 동등성 확보가 규모 확대나 승인을 지연시킬 가능성이 있는 점, 환자 소개, 적격성, 치료 준비 상황이 실제 임상에서의 보급을 지연시킬 가능성이 있는 점)

- 제품 개발/혁신 : 전 세계 줄기세포 치료 시장의 향후 기술 동향 및 연구 개발 활동에 대한 상세한 인사이트

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보(본 보고서에서는 다양한 지역에 걸친 시장을 분석하고 있습니다)

- 시장의 다양화 : 전 세계 줄기세포 치료 시장의 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 평가 : 주요 기업의 시장 점유율, 성장 전략, 제품 라인업에 대한 상세한 평가(주요 업계 참여자에 대한 상세한 분석을 통해, 주요 전략, 제품 출시 및 승인, 인수, 제휴, 계약, 공동 연구, 기타 최근 동향, 투자·자금 조달 활동, 브랜드·제품 비교 분석, 그리고 전 세계 줄기세포 치료 시장에서 공급업체의 기업 가치 평가 및 재무 지표에 대한 인사이트를 제공합니다)

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 줄기세포 치료 시장(세포 유래별)

제10장 줄기세포 치료 시장(유형별)

제11장 줄기세포 치료 시장(치료 용도별)

제12장 줄기세포 치료 시장(최종사용자별)

제13장 줄기세포 치료 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.06.30The stem cell therapy market is projected to reach USD 3.65 billion by 2035 from USD 0.48 billion in 2026, at a CAGR of 25.3% from 2026 to 2035. The market is driven by the expanding pipeline of stem cell-based therapies, increasing demand for regenerative treatments, and growth in advanced modalities such as iPSC-derived therapies and allogeneic cell products. Market estimates indicate robust expansion through 2035, supported by technological advancements in cell processing and manufacturing and rising clinical adoption of approved stem cell therapies.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2035 |

| Base Year | 2026 |

| Forecast Period | 2026-2035 |

| Units Considered | Value (USD billion) |

| Segments | Cell source, type, therapeutic application, and end user |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, Middle East, and Africa |

However, high manufacturing and treatment costs, complex regulatory pathways across regions, scalability challenges from bench to commercial manufacturing, and the need for specialized infrastructure and expertise are expected to restrain broader market growth.

"The induced pluripotent stem cell (iPSC) segment is projected to grow at the highest CAGR in the stem cell therapy market over the forecast period."

Based on cell source, the stem cell therapy market is broadly segmented into adipose tissue-derived MSCs, bone marrow-derived MSCs, placenta/umbilical cord-derived MSCs, induced pluripotent stem cells, embryonic stem cells, tissue-specific stem cells, and other cell sources. The induced pluripotent stem cell (iPSC) segment is expected to grow at the highest CAGR in the stem cell therapy market because it is moving from a high-potential research platform toward early commercial validation, while still starting from a relatively low revenue base. iPSCs provide a renewable and scalable cell source that can be differentiated into multiple therapeutic cell types, including dopaminergic neurons, cardiomyocytes, retinal cells, pancreatic beta-like cells, and other tissue-specific cells, making them attractive for large unmet-need indications such as Parkinson's disease, heart failure, diabetes, retinal disorders, and other degenerative diseases.

"Allogeneic stem cell therapy accounted for the largest share of the stem cell therapy market, by type, in 2025."

Based on type, the global stem cell therapy market is segmented into allogeneic and autologous stem cell therapies. The allogeneic stem cell therapy segment accounted for the largest share of the stem cell therapy market in 2025, due to its scalability, off-the-shelf availability, and cost advantages in commercial manufacturing. These therapies enable standardized production and broader patient access essential for clinical and commercial applications. Additionally, the expanding pipeline of allogeneic cell therapy candidates, increasing regulatory approvals, and growing commercial-scale manufacturing activities continue to strengthen the segment's leading market position globally.

"Europe is projected to grow at the highest CAGR in the stem cell therapy market from 2026 to 2035."

The stem cell therapy market is segmented into North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa. During the forecast period, Europe is projected to be the fastest-growing region in the stem cell therapy market due to its strong regulatory framework for advanced therapy medicinal products, expanding transplant and cell therapy infrastructure, high clinical trial activity, and rising investment in scalable ATMP manufacturing. The EMA classifies substantially manipulated or non-homologous stem-cell products as ATMPs and has a dedicated Committee for Advanced Therapies, creating a clear pathway for stem cell-based product assessment, scientific advice, and market authorization.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side (70%) and Demand Side (30%)

- By Designation: Managers (45%), CXOs & Directors (30%), and Executives (25%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and Middle East & Africa (5%)

List of Companies Profiled in the Report

Key players in the global stem cell therapy market include Vericel Corporation (US), Mesoblast (Australia), MEDIPOST (South Korea), JCR Pharmaceuticals Co., Ltd. (Japan), Takeda Pharmaceutical Company Limited (Japan), Anterogen Co., Ltd. (South Korea), CorestemChemon Inc. / Corestem, Inc. (South Korea), Vertex Pharmaceuticals (US), Pharmicell Co., Ltd. (South Korea), Holostem Terapie Avanzate Srl (Italy), Stempeutics Research Pvt. Ltd. (India), Cipla Limited (India), Bayer AG (Germany), Aspen Neuroscience (US), Longeveron Inc. (US), and Smith+Nephew (UK).

Research Coverage

This research report categorizes the stem cell therapy market by Cell Source (Adipose Tissue-Derived Mesenchymal Stem Cells, Bone Marrow-Derived Mesenchymal Stem Cells, Placenta/Umbilical Cord-Derived Mesenchymal Stem Cells, Induced Pluripotent Stem Cells, Embryonic Stem Cells, Tissue-Specific Stem Cells, Other Cell Sources), Type (Allogeneic Stem Cell Therapy, Autologous Stem Cell Therapy), Therapeutic Application (Musculoskeletal Disorders, Wounds & Surgeries, Inflammatory & Autoimmune Diseases, Cardiovascular Diseases, Neurological Disorders, Diabetes & Metabolic Diseases, Other Therapeutic Applications), End User (Hospitals, Specialty / Stem Cell Clinics, Other End Users), and Region (North America, Europe, Asia Pacific, Latin America, and Middle East, and Africa)

The scope of the report covers detailed information regarding the major factors, such as drivers, challenges, opportunities, and restraints, influencing the growth of the stem cell therapy market. A detailed analysis of the key industry players has been done to provide insights into their business overview, product portfolio, key strategies such as product and service approvals and launches, collaborations, partnerships, expansions, agreements, and recent developments associated with the stem cell therapy market. This report covers competitive analysis of top players and upcoming startups in the stem cell therapy market ecosystem.

Key Benefits of Buying the Report

The report will help market leaders/new entrants by providing the closest approximations of revenue for the overall stem cell therapy market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their business more effectively and develop suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide information on key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (rising regulatory approvals are validating stem cell therapy as a viable commercial treatment class, high unmet needs in rare and chronic diseases are driving demand for curative therapies, gene-modified HSPC therapies are creating a high-value segment in the stem cell therapy market, allogeneic and off-the-shelf approaches are improving scalability over autologous therapies), restraints (high therapy price and uncertain reimbursement remain the largest restraints on market adoption, manufacturing complexity and high cost of goods limit scalability and margins, inconsistent clinical evidence in some regenerative indications reduces payer and physician confidence, regulatory heterogeneity across countries complicates global commercialization.), opportunities (iPSC-derived therapies offer long-term opportunities for scalable cell replacement, allogeneic MSC and progenitor-cell platforms can expand access beyond individualized therapy, expansion into neurological, cardiovascular, metabolic, and ocular diseases can broaden market potential, Gene-modified HSPC therapies can expand into younger patients, additional hemoglobinopathies, immune diseases, and metabolic diseases), and challenges (potency testing and product characterization challenges, demonstrating clear clinical efficacy is difficult in heterogeneous regenerative indications, manufacturing comparability after process changes can delay scale-up and approval, patient referral, eligibility, and treatment readiness can slow real-world uptake)

- Product Development/Innovation: Detailed insights into upcoming technologies and research & development activities in the global stem cell therapy market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the market across varied regions)

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the global stem cell therapy market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players (a detailed analysis of the key industry players has been carried out to provide insights into their key strategies, product launches/approvals, acquisitions, partnerships, agreements, collaborations, other recent developments, investments & funding activities, brand/product comparative analysis, and vendor valuation & financial metrics of the global stem cell therapy market)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS SEGMENTATION AND REGIONAL SCOPE

- 1.4 INCLUSIONS & EXCLUSIONS

- 1.4.1 YEARS CONSIDERED

- 1.4.2 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHNAGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN STEM CELL THERAPY MARKET

- 3.2 STEM CELL THERAPY MARKET, BY TYPE AND REGION

- 3.3 STEM CELL THERAPY MARKET, BY COUNTRY

- 3.4 STEM CELL THERAPY MARKET SHARE, BY TYPE, 2026 VS 2035

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising regulatory approvals validating stem cell therapies

- 4.2.1.2 Unmet needs in rare and chronic diseases driving demand for curative therapies

- 4.2.1.3 Allogeneic and off-the-shelf approaches improving scalability over autologous therapies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High therapy price and uncertain reimbursement limiting adoption

- 4.2.2.2 Manufacturing complexity and high cost of goods limiting scalability and margins

- 4.2.2.3 Inconsistent clinical evidence reducing payer and physician confidence

- 4.2.2.4 Regulatory inconsistency across countries complicating global commercialization

- 4.2.3 OPPORTUNITY

- 4.2.3.1 iPSC-derived therapies offering long-term opportunities for scalable cell replacement

- 4.2.3.2 Allogeneic MSC and progenitor-cell platforms can support expansion beyond personalized treatment models

- 4.2.3.3 Expansion into neurological, cardiovascular, and metabolic diseases

- 4.2.4 CHALLENGES

- 4.2.4.1 Potency testing and product characterization challenges

- 4.2.4.2 Difficulty in demonstrating clear clinical efficacy in heterogeneous regenerative indications

- 4.2.4.3 Manufacturing comparability challenges following process changes may delay scale-up and regulatory approval

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL STEM CELL THERAPY MARKET

- 5.2.4 TRENDS IN GLOBAL STEM CELL THERAPY MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE SELLING PRICE OF KEY PLAYERS, BY PRODUCT

- 5.5.2 INDICATIVE SELLING PRICE, BY REGION

- 5.6 KEY CONFERENCES & EVENTS

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.8 INVESTMENT/FUNDING ACTIVITY

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF - STEM CELL THERAPY MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 North America

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

- 5.10.5.1 Hospitals

- 5.10.5.2 Specialty/Stem cell clinics

- 5.10.5.3 Other end users

- 5.11 SUPPLY CHAIN ANALYSIS

- 5.12 KEY STEM CELL THERAPY MANUFACTURING CAPACITY ADDITIONS

- 5.12.1 KEY CDMO CAPACITY ADDITIONS

- 5.12.2 KEY SPONSOR CAPACITY ADDITIONS

- 5.12.3 GLOBAL KEY STEM CELL THERAPY PRODUCT SALES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Bioreactor systems

- 6.1.1.2 Cell expansion & differentiation platforms

- 6.1.2 ADJACENT TECHNOLOGIES

- 6.1.2.1 Reprogramming & gene engineering tools

- 6.1.2.2 Downstream processing technologies

- 6.1.3 COMPLEMENTARY TECHNOLOGIES

- 6.1.3.1 Advanced cell culture consumables

- 6.1.3.2 Automation and robotics

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PIPELINE ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON STEM CELL THERAPY MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN STEM CELL THERAPY MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN STEM CELL THERAPY MARKET

- 6.6 SUCCESS STORIES AND REAL WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING & ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 STEM CELL THERAPY MARKET BY CELL SOURCE

- 9.1 INTRODUCTION

- 9.2 ADIPOSE TISSUE-DERIVED MSCS

- 9.2.1 GROWING ADOPTION OF ADIPOSE-DERIVED MSC THERAPIES IN RECONSTRUCTIVE SURGERY AND AESTHETIC MEDICINE DRIVING MARKET

- 9.3 BONE MARROW-DERIVED MSCS

- 9.3.1 ACCELERATING REGULATORY MILESTONES AND EXPANDING INDICATIONS FOR BONE MARROW-DERIVED MSC THERAPIES DRIVING MARKET GROWTH

- 9.4 PLACENTA/UMBILICAL CORD-DERIVED MESENCHYMAL STEM CELLS

- 9.4.1 EXPANDING CORD BLOOD BANKING INFRASTRUCTURE AND ALLOGENEIC PRODUCT DEVELOPMENT FUELING SEGMENT GROWTH

- 9.5 INDUCED PLURIPOTENT STEM CELLS (IPSCS)

- 9.5.1 BREAKTHROUGH CLINICAL PROGRAMS AND NEXT-GENERATION MANUFACTURING PLATFORMS POSITIONING IPSCS AS TRANSFORMATIVE CELL SOURCE

- 9.6 EMBRYONIC STEM CELLS (ESCS)

- 9.6.1 LANDMARK REGULATORY APPROVALS AND CLINICAL VALIDATION OF ESC-DERIVED ISLET CELL THERAPIES CATALYZING GROWTH

- 9.7 TISSUE-SPECIFIC STEM CELLS

- 9.7.1 ESTABLISHED COMMERCIAL PRODUCTS AND EXPANDING CLINICAL APPLICATIONS FUELING MARKET GROWTH

- 9.8 OTHER CELL SOURCES

10 STEM CELL THERAPY MARKET BY TYPE

- 10.1 INTRODUCTION

- 10.2 ALLOGENEIC STEM CELL THERAPY

- 10.2.1 SCALABLE OFF-THE-SHELF MANUFACTURING AND EXPANDING CLINICAL PIPELINES DRIVING RAPID GROWTH

- 10.3 AUTOLOGOUS STEM CELL THERAPY

- 10.3.1 ESTABLISHED COMMERCIAL PRODUCTS AND PATIENT-SPECIFIC IMMUNOLOGICAL ADVANTAGES TO SUSTAIN STEADY GROWTH

11 STEM CELL THERAPY MARKET BY THERAPEUTIC APPLICATION

- 11.1 INTRODUCTION

- 11.2 MUSCULOSKELETAL DISORDERS

- 11.2.1 RISING GLOBAL PREVALENCE OF OSTEOARTHRITIS AND GROWING ADOPTION OF CELL-BASED CARTILAGE REPAIR THERAPIES DRIVING SEGMENT GROWTH

- 11.3 WOUNDS & SURGERIES

- 11.3.1 EXPANDING APPLICATIONS OF STEM CELL THERAPIES IN WOUND HEALING, BURN TREATMENT, AND SURGICAL RECONSTRUCTION SUPPORTING SEGMENT GROWTH

- 11.4 INFLAMMATORY & AUTOIMMUNE DISEASES

- 11.4.1 EXPANDING CLINICAL VALIDATION OF MSC IMMUNOMODULATORY PROPERTIES AND FDA APPROVAL OF RYONCIL FOR GVHD DRIVING GROWTH

- 11.5 CARDIOVASCULAR DISEASES

- 11.5.1 ADVANCING LATE-STAGE CLINICAL PROGRAMS AND GROWING EVIDENCE FOR MSC-MEDIATED CARDIAC REPAIR SUPPORTING MARKET GROWTH

- 11.6 NEUROLOGICAL DISORDERS

- 11.6.1 BREAKTHROUGH IPSC-DERIVED NEURONAL THERAPIES AND EXPANDING CLINICAL PROGRAMS FOR NEURODEGENERATIVE CONDITIONS DRIVING SEGMENTAL GROWTH

- 11.7 DIABETES & METABOLIC DISEASES

- 11.7.1 TRANSFORMATIVE POTENTIAL OF ESC-DERIVED ISLET CELL THERAPIES FOR TYPE 1 DIABETES FUELING RAPID MARKET GROWTH

- 11.8 OTHER THERAPEUTIC APPLICATIONS

12 STEM CELL THERAPY MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITALS

- 12.2.1 ADVANCED TRANSPLANT INFRASTRUCTURE AND CONCENTRATION OF REGULATORY-APPROVED STEM CELL THERAPY ADMINISTRATION DRIVING GROWTH

- 12.3 SPECIALTY/STEM CELL CLINICS

- 12.3.1 GROWING NUMBER OF DEDICATED REGENERATIVE MEDICINE CENTERS AND EXPANDING AUTOLOGOUS MSC TREATMENT OFFERINGS DRIVING SEGMENTAL GROWTH

- 12.4 OTHER END USERS

- 12.4.1 AMBULATORY SURGICAL CENTERS, ACADEMIC RESEARCH INSTITUTES, AND CELL BANKS EXPANDING STEM CELL THERAPY DELIVERY ECOSYSTEM

13 STEM CELL THERAPY MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.2 CANADA

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.2 UK

- 13.3.3 FRANCE

- 13.3.4 ITALY

- 13.3.5 SPAIN

- 13.3.6 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.2 JAPAN

- 13.4.3 INDIA

- 13.4.4 SOUTH KOREA

- 13.4.5 AUSTRALIA

- 13.4.6 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.2 MEXICO

- 13.5.3 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Saudi Arabia

- 13.6.1.2 UAE

- 13.6.1.3 Rest of GCC Countries

- 13.6.2 REST OF MIDDLE EAST

- 13.6.1 GCC COUNTRIES

- 13.7 AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 STRATEGIES ADOPTED BY KEY PLAYERS/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2023-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Cell source footprint

- 14.5.5.4 Type footprint

- 14.5.5.5 Therapeutic application footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.6.5.1 List of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of key startups/SMEs

- 14.7 COMPANY VALUATION & FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.8 BRAND/PRODUCT COMPARISON

- 14.8.1 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 VERICEL CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product Approval

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 MESOBLAST

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product approval

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 JCR PHARMACEUTICALS CO., LTD.

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Product pipeline

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 MEDIPOST

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.3.2 OTHER DEVELOPMENTS

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 CO.DON GMBH

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 MnM view

- 15.1.5.3.1 Key strengths

- 15.1.5.3.2 Strategic choices

- 15.1.5.3.3 Weaknesses & competitive threats

- 15.1.6 SMITH+NEPHEW

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.7 ANTEROGEN CO., LTD.

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.8 CORESTEMCHEMON INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.9 VERTEX PHARMACEUTICALS INCORPORATED

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.2.1 Other developments

- 15.1.10 PHARMICELL CO., LTD

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.11 HOLOSTEM TERAPIE AVANZATE SRL

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 STEMPEUTICS RESEARCH PVT LTD.

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.13 CIPLA LIMITED

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product Launch

- 15.1.13.3.2 Deals

- 15.1.14 BAYER AG

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.2.1 OTHER DEVELOPMENTS

- 15.1.15 ASPEN NEUROSCIENCE

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.2.1 Other developments

- 15.1.16 LONGEVERON

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.16.2.1 Other developments

- 15.1.1 VERICEL CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 ATHERSYS, INC.

- 15.2.2 BIORESTORATIVE THERAPIES, INC.

- 15.2.3 KANGSTEM BIOTECH CO., LTD.

- 15.2.4 HOPE BIOSCIENCES

- 15.2.5 CELLULAR BIOMEDICINE GROUP

- 15.2.6 PERSONALIZED STEM CELLS

- 15.2.7 CHIESI FARMACEUTICI S.P.A.

- 15.2.8 CELL TECH PHARMED

- 15.2.9 SUMITOMO PHARMA

- 15.2.10 CYNATA THERAPEUTICS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.2 PRIMARY DATA

- 16.2 MARKET ESTIMATION METHODOLOGY

- 16.2.1 MARKET SIZE ESTIMATION

- 16.2.2 INSIGHTS OF PRIMARY EXPERTS

- 16.2.3 TOP-DOWN APPROACH

- 16.3 MARKET GROWTH RATE PROJECTIONS

- 16.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS