|

시장보고서

상품코드

2066985

전기강판 시장 : 유형별, 용도별, 최종 이용 산업별, 지역별 - 세계 예측(-2031년)Electrical Steel Market by Type (Grain-oriented, Non-grain-oriented), Application (Transformers, Motors, Inductors), End-use Industry (Energy, Automotive, Manufacturing, Household Appliances), and Region - Global Forecast to 2031 |

||||||

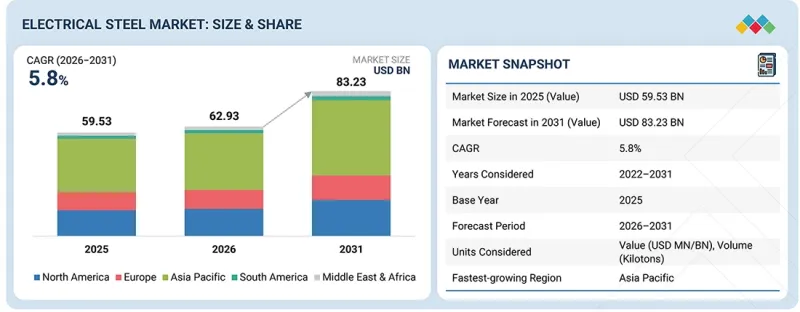

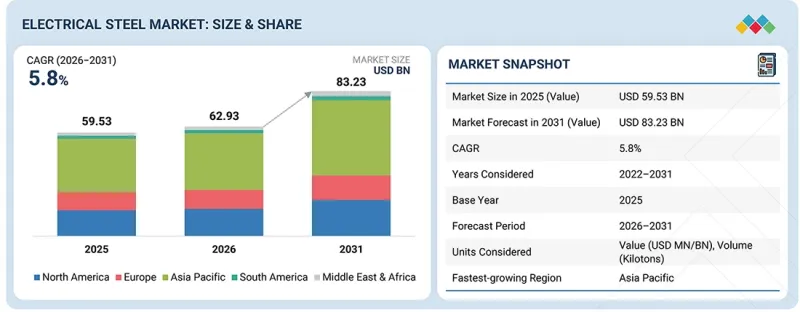

전기강판 시장 규모는 2026년 629억 3,000만 달러에서 2031년까지 832억 3,000만 달러로 성장할 것으로 예측되며, 이 기간 동안의 연평균 성장률(CAGR)은 5.8%가 될 것으로 보입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만/10억 달러), 킬로톤 |

| 부문 | 유형별, 용도별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

전자강판의 수요는 전기화의 가속화, 재생에너지의 확대, 그리고 고효율 변압기 및 전동기에 대한 수요에 힘입어 증가하고 있습니다.

“예측 기간 동안 비결정립 배향 전기강판 부문이 가장 큰 부문이 될 것으로 전망됩니다.”

비결정 배향(NGO) 전기강판 부문은 전기자동차, 산업용 모터, 가전제품 등 고성장 분야에서의 폭넓은 활용에 힘입어, 예측 기간 동안 전기강판 시장에서 가장 큰 점유율을 차지할 것으로 전망됩니다. 결정 배향 등급과는 달리, NGO 강판은 등방성 자기 특성을 가지고 있어, 가변 속도나 가변 방향으로 작동하는 회전 기기에 매우 적합합니다. 전기자동차(EV) 생산의 급속한 확대와 제조업 및 HVAC 시스템에서 고효율 모터의 도입 증가로 인해 고성능 NGO 등급에 대한 수요가 크게 증가하고 있습니다. 또한, 박판 가공 및 코팅 기술의 발전으로 인해 코어 손실을 줄이고 효율을 높일 수 있게 되었으며, NGO 전자강은 전 세계가 전동화 및 고효율 시스템으로 전환해 나가는 과정에서 중요한 소재로서의 입지를 확고히 다지고 있습니다.

“예측 기간 동안 모터 분야는 시장 규모 면에서 2위를 차지할 것으로 전망됩니다.”

모터 분야는 산업 기계, 전기자동차, HVAC 시스템 및 가정용 가전제품에 전자강판이 광범위하게 도입됨에 따라, 예측 기간 동안 전자강판 시장에서 2위의 점유율을 차지할 것으로 전망됩니다. 모터의 경우, 모터 코어 전체에 걸쳐 균일한 자속 밀도를 확보하고 회전 자기장 속에서 효율적으로 작동시키기 위해서는 비결정립 배향 전기자철심을 널리 사용해야 합니다. 에너지 효율이 높은 제조 방식에 대한 관심이 높아지고, 모터의 에너지 효율에 관한 규제가 강화됨에 따라 많은 기존형 모터가 고효율 모델로 교체되고 있습니다. 그 결과, 이러한 추세가 고성능 특성을 갖춘 새로운 등급의 전자강판에 대한 수요를 견인하고 있습니다. 또한, 전기자동차의 보급과 제조 시설의 자동화 진전에 따라, 전기 모터 및 그 용도에 특화되어 설계된 전기강판 등급에 대한 수요는 앞으로도 계속 확대될 것입니다. 마지막으로, 박판 전자철 및 코팅 기술의 지속적인 발전으로 인해 모터의 효율이 향상되고, 세계 전자철 시장에서 모터 분야의 입지가 더욱 공고해질 것입니다.

“예측 기간 동안 자동차용 최종 용도 부문은 규모 면에서 2위를 차지할 것으로 전망됩니다.”

자동차 부문은 전동 모빌리티로의 급속한 전환과 자동차 시스템의 전동화가 진행되고 있는 것을 배경으로, 예측 기간 동안 전자강판 시장에서 2위의 점유율을 차지할 것으로 예상됩니다. 전자강은, 특히 비결정립 배향 등급의 경우, 차량의 구동 모터에 없어서는 안 될 소재입니다. 이 소재의 높은 자기 효율과 낮은 코어 손실은 전기자동차(EV)의 주행 거리와 성능에 직접적으로 기여합니다. 현대 자동차의 복잡화가 진행됨에 따라 보조 모터, 센서, 차량용 전기 시스템 등 전기자동차(EV)의 많은 부품에서 전자강판의 사용이 증가하고 있습니다. EV 수요가 증가함에 따라, 자동차 제조사들은 출력 밀도가 더 높고 소형인 모터를 설계하기 위해 새로운 박판 전기강판에 대한 수요를 높이고 있습니다. 전기자동차 생산에 대한 정부의 인센티브와 배기가스 감축 목표가 도입됨에 따라, 자동차 부문이 전 세계 전기강판 수요의 주요 견인 역할을 계속할 이유는 많습니다.

"금액 기준으로 볼 때, 예측 기간 동안 북미가 시장 규모 2위를 차지할 것으로 전망됩니다.”

북미는 송전망 현대화, 재생에너지 통합, 전기자동차 보급을 위한 막대한 투자에 힘입어, 예측 기간 동안 전자강판 시장에서 2위의 점유율을 차지할 것으로 전망됩니다. 미국과 캐나다에서는 노후화된 송전·배전 인프라의 현대화가 적극적으로 추진되고 있으며, 결정립 배향 전자강판을 사용한 고효율 변압기에 대한 수요가 증가하고 있습니다. 동시에, 전기자동차(EV) 제조 및 배터리 생산의 급속한 확대로 인해 구동 모터용 비결정립 배향 전기강판의 소비가 증가하고 있습니다. 에너지 효율과 배기가스 감축에 대한 규제 당국의 강력한 관심으로 인해, 첨단 전자강판 등급의 채택이 더욱 가속화되고 있습니다. 또한, 확고히 자리 잡은 자동차 및 산업용 제조 거점이 안정적인 수요를 뒷받침하고 있어, 북미는 전 세계 전기강판 소비에서 중요한 역할을 담당하는 지역이 되었습니다.

대상 기업 : ArcelorMittal(룩셈부르크), POSCO(한국), China Baowu Steel Group Corporation Limited(중국), voestalpine AG(오스트리아), Nippon Steel Corporation(일본), United States Steel Corporation(미국), Steel Authority of India Limited(SAIL)(인도), Tata Steel(인도), thyssenkrupp AG(독일) 등이 본 보고서의 대상입니다.

본 조사에서는 전기강판 시장 내 이러한 주요 기업들에 대해 기업 개요, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

본 조사 보고서에서는 전기강판 시장을 ‘종류’(결정립 배향형, 비결정립 배향형), ‘용도’(변압기, 모터, 인덕터), ‘최종 이용 산업’(에너지, 자동차, 제조, 가전), 그리고 ‘지역’(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류하고 있습니다. 본 보고서의 범위에는 전기강판 시장의 성장에 영향을 미치는 촉진요인, 제약요인, 과제 및 기회에 관한 상세한 정보가 포함되어 있습니다. 주요 업계 업체에 대한 상세한 분석을 통해 사업 개요, 제공 제품, 그리고 전기강판 시장에 관련된 파트너십, 제휴, 제품 출시, 사업 확장, 인수합병 등 주요 전략에 대한 인사이트를 제공합니다. 또한, 본 보고서에서는 전기강판 시장의 생태계에서 두각을 나타내고 있는 스타트업 기업들에 대한 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

본 보고서는 시장 선도 기업 및 신규 진입 기업을 대상으로 전기강판 시장 전체 및 그 하위 부문의 매출 전망을 제공합니다. 본 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치에 놓을 수 있는 심층적인 인사이트를 얻어, 적절한 시장 진입 전략을 수립하는 데 도움이 됩니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 관한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

주요 촉진요인(전기강판 생산을 위한 철광석 및 기타 광물의 풍부함, 도시 인프라 네트워크의 확대, 소재 사용량 증가를 촉진하는 전기자동차(EV) 모터 기술의 발전) , 제약요인(원자재 품질의 변동 및 공급 안정성, 탈탄소화 압력이 높아지는 가운데 에너지 집약적인 가공 공정), 기회(EV 전용 전기강판 등급으로의 확대, 기존 한계를 뛰어넘는 실리콘 함량의 정밀 제어, 전기강판용 스크랩 선별 및 폐쇄형 재활용), 그리고 과제(고주파에서 초저 코어 손실 실현, 유해 공정 배출물에 대한 환경 규제 강화)에 대한 분석.

- 제품 개발 및 혁신 : 전기강판 시장의 향후 기술, 연구개발 활동, 그리고 제품 및 서비스 출시에 관한 상세한 인사이트

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 다양한 지역에 걸친 전기강판 시장을 분석하고 있습니다.

시장의 다양화 : 전기강판 시장 내 신제품 및 서비스, 미개척 지역, 최근 동향, 그리고 투자에 관한 종합적인 정보.

- 경쟁사 분석 : ArcelorMittal(룩셈부르크), POSCO(한국), China Baowu Steel Group Corporation Limited(중국), voestalpine AG(오스트리아), Nippon Steel Corporation(일본), United States Steel Corporation(미국), Steel Authority of India Limited(SAIL)(인도), Tata Steel(인도), thyssenkrupp AG(독일) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 전기강판 시장(유형별)

제10장 전기강판 시장(용도별)

제11장 전기강판 시장(용도별)

제12장 전기강판 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.30The electrical steel market is projected to grow from USD 62.93 billion in 2026 to USD 83.23 billion by 2031, representing a compound annual growth rate (CAGR) of 5.8% during this period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion), Volume (Kilotons) |

| Segments | Type, Application, End-Use Industry and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Demand for electrical steel is driven by accelerating electrification, the expansion of renewable energy, and the need for high-efficiency transformers and electric motors.

"Non-grain-oriented electrical steel segment projected to be the largest segment during the forecast period."

The Non-Grain-Oriented (NGO) electrical steel segment is expected to account for the largest share of the electrical steel market during the forecast period, driven by its extensive use across high-growth applications such as electric vehicles, industrial motors, and household appliances. Unlike grain-oriented grades, NGO steel offers isotropic magnetic properties, making it highly suitable for rotating equipment operating under variable speeds and directions. The rapid expansion of EV production and increasing deployment of energy-efficient motors in manufacturing and HVAC systems are significantly boosting demand for high-performance NGO grades. Additionally, advancements in thin-gauge processing and coating technologies are enabling lower core losses and improved efficiency, positioning NGO electrical steel as a critical material in the global transition toward electrification and energy-efficient systems.

"Motors segment projected to be the second-largest segment during the forecast period."

The motors segment is expected to account for the second-largest share of the electrical steel market during the forecast period, driven by the widespread deployment of electrical steel in industrial machinery, electric vehicles, HVAC systems, and consumer appliances. Motors will require extensive use of non-grain-oriented electrical steel to ensure uniform magnetic strength throughout the motor core, thereby allowing them to operate efficiently in a rotating magnetic field. An increased focus on energy-efficient manufacturing and stricter regulations on motor energy efficiency have led many conventional motors to be replaced with higher-efficiency models. Consequently, these developments are driving demand for new grades of electrical steel with advanced properties. Additionally, electric transportation and increased automation within manufacturing facilities will continue to drive demand for electric motors and electrical steel grades specifically designed for that purpose. Finally, further improvements in thin-gauge electrical steel and coating technology will improve motor efficiency and further solidify the motor segment of the global electrical steel market.

"Automotive end-use industry segment projected to be the second-largest segment during the forecast period."

The automotive segment is expected to account for the second-largest share of the electrical steel market during the forecast period, driven by the fast-moving shift to electric mobility and the increasing electrification of car systems. Electrical steel is a vital material for traction motors in vehicles, especially in non-grain-oriented grades. High magnetic efficiency and low core losses from this material directly contribute to the range and performance of electric vehicles (EVs). The use of electrical steel is increasing in many parts of EVs, including auxiliary motors, sensors, and onboard electrical systems, due to the growing complexity of cars today. With the growing demand for EVs, automakers have increased demand for new, thin-gauge electrical steel to design more compact motors with higher power density. With government incentives for EV production and emissions-reduction targets in place, there are many reasons the automotive sector remains a key driver of electrical steel demand worldwide.

"In terms of value, the North America region is projected to be the second-largest segment during the forecast period."

The North America region is expected to account for the second-largest share of the electrical steel market during the forecast period, driven by substantial investments in grid modernization, renewable energy integration, and electric vehicle adoption. The US and Canada are actively upgrading aging transmission and distribution infrastructure, increasing demand for high-efficiency transformers that rely on grain-oriented electrical steel. Simultaneously, the rapid expansion of EV manufacturing and battery production is boosting consumption of non-grain-oriented electrical steel for traction motors. Strong regulatory focus on energy efficiency and emissions reduction is further accelerating the adoption of advanced electrical steel grades. Additionally, the presence of established automotive and industrial manufacturing bases supports consistent demand, positioning North America as a key contributor to global electrical steel consumption.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: ArcelorMittal (Luxembourg), POSCO (South Korea), China Baowu Steel Group Corporation Limited (China), voestalpine AG (Austria), Nippon Steel Corporation (Japan), United States Steel Corporation (US), Steel Authority of India Limited (SAIL) (India), Tata Steel (India), and thyssenkrupp AG (Germany) among others are covered in the report.

The study includes an in-depth competitive analysis of these key players in the electrical steel market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the electrical steel market by Type (Grain-oriented, Non-grain-oriented), Application (Transformers, Motors, Inductors), End-use Industry (Energy, Automotive, Manufacturing, Household Appliances), and Region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the electrical steel market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the electrical steel market. This report covers a competitive analysis of upcoming startups in the electrical steel market ecosystem.

Reasons to Buy the Report

The report will provide market leaders/new entrants with estimates of revenue for the overall electrical steel market and its subsegments. This report will help stakeholders understand the competitive landscape, gain deeper insights into better positioning their businesses, and plan suitable go-to-market strategies. The report will help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (abundance of iron ore and other minerals for electrical steel production, expansion of urban infrastructure networks, advancements in electric vehicle motor technologies driving higher material intensity), restraints (volatility in raw material quality and supply security, energy-intensive processing with rising decarbonization pressure), opportunities (expansion into ev-specific ngo steel grades, precision control of silicon content above conventional limits, scrap segregation and closed-loop recycling for electrical steel), and challenges (achieving ultra-low core loss at high frequencies, increasingly stringent environmental compliance for hazardous process emissions).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the electrical steel market

- Market Development: Comprehensive information about profitable markets - the report analyzes the electrical steel market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the electrical steel market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as ArcelorMittal (Luxembourg), POSCO (South Korea), China Baowu Steel Group Corporation Limited (China), voestalpine AG (Austria), Nippon Steel Corporation (Japan), United States Steel Corporation (US), Steel Authority of India Limited (SAIL) (India), Tata Steel (India), and thyssenkrupp AG (Germany).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRICAL STEEL MARKET

- 3.2 ELECTRICAL STEEL MARKET, BY TYPE AND END-USE INDUSTRY

- 3.3 ELECTRICAL STEEL MARKET, BY APPLICATION

- 3.4 ELECTRICAL STEEL MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Abundance of iron ore & other minerals for electrical steel production

- 4.2.1.2 Expansion of urban infrastructure networks

- 4.2.1.3 Expansion of renewable energy infrastructure increasing transformer and grid equipment demand

- 4.2.1.4 Advancements in electric vehicle motor technologies driving higher material intensity

- 4.2.2 RESTRAINTS

- 4.2.2.1 Volatility in raw material quality and supply security

- 4.2.2.2 Energy-intensive processing with rising decarbonization pressure

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion into EV-specific NGO steel grades

- 4.2.3.2 Precision control of silicon content above conventional limits

- 4.2.3.3 Scrap segregation and closed-loop recycling for electrical steel

- 4.2.4 CHALLENGES

- 4.2.4.1 Achieving ultra-low core loss at high frequencies

- 4.2.4.2 Increasingly stringent environmental compliance for hazardous process emissions

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ELECTRICAL STEEL MARKET

- 4.3.1.1 Cost-efficient production of low core loss electrical steel without compromising material purity

- 4.3.1.2 Electrical steel with consistent performance under high-frequency and variable load conditions

- 4.3.1.3 Ultra-thin electrical steel with high mechanical stability for advanced motor designs

- 4.3.2 WHITE SPACES OPPORTUNITIES

- 4.3.2.1 Next-generation alloy systems for high-frequency, low-loss applications

- 4.3.2.2 Advanced coating and insulation technologies for dynamic grid environments

- 4.3.2.3 Scalable low-carbon electrical steel production with high recycled content

- 4.3.1 UNMET NEEDS IN ELECTRICAL STEEL MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES' ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 ACCELERATING ELECTRIFICATION OF AUTOMOTIVE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA RELATED TO HS CODE 722511, BY COUNTRY

- 5.6.2 EXPORT DATA RELATED TO HS CODE 722511, BY COUNTRY

- 5.6.3 IMPORT DATA RELATED TO HS CODE 722519, BY COUNTRY

- 5.6.4 EXPORT DATA RELATED TO HS CODE 722519, BY COUNTRY

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 NIPPON STEEL CORPORATION - EV MOTOR EFFICIENCY ENHANCEMENT INITIATIVE

- 5.10.2 POSCO: TRANSFORMER PERFORMANCE FOR RENEWABLE GRIDS

- 5.10.3 THYSSENKRUPP STEEL - LOW-CARBON ELECTRICAL STEEL PRODUCTION SHIFT

- 5.11 IMPACT OF 2025 US TARIFFS ON ELECTRICAL STEEL MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON KEY COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 LASER DOMAIN REFINEMENT (LDR)

- 6.1.2 SECONDARY RECRYSTALLIZATION CONTROL (HI-B PROCESSING)

- 6.1.3 ULTRA-THIN GAUGE COLD ROLLING (<0.1 MM)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 VACUUM DEGASSING (VD/VOD) FOR ULTRA-LOW IMPURITY STEEL

- 6.2.2 MOTOR CORE LASER CUTTING & STACKING AUTOMATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 SOFT MAGNETIC COMPOSITES (SMC) FOR 3D FLUX PATHS

- 6.3.2 HYDROGEN-BASED DIRECT REDUCED IRON (H-DRI)

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | PROCESS PRECISION & LOSS REDUCTION PHASE

- 6.4.2 MID-TERM (2027-2030) | HIGH-FREQUENCY PERFORMANCE & PROCESS INTEGRATION PHASE

- 6.4.3 LONG-TERM (2030-2035+): LOW-CARBON & NEXT-GENERATION MATERIAL PHASE

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 APPROACH

- 6.6 FUTURE APPLICATIONS

- 6.6.1 ULTRA-HIGH-FREQUENCY EV TRACTION MOTORS (>20 KHZ SWITCHING)

- 6.6.2 AEROSPACE ELECTRIC PROPULSION MOTORS

- 6.6.3 WIRELESS POWER TRANSFER SYSTEMS (HIGH-EFFICIENCY MAGNETIC CORES)

- 6.7 IMPACT OF AI/GENERATIVE AI ON ELECTRICAL STEEL MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN ELECTRICAL STEEL MARKET

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN ELECTRICAL STEEL MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ELECTRICAL STEEL MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ELECTRICAL STEEL

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ELECTRICAL STEEL

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 ELECTRICAL STEEL MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 GRAIN-ORIENTED ELECTRICAL STEEL

- 9.2.1 RISING FOCUS ON ENERGY-EFFICIENT GRID INFRASTRUCTURE AND POWER CONSERVATION TO DRIVE DEMAND

- 9.3 NON-GRAIN-ORIENTED ELECTRICAL STEEL

- 9.3.1 RISING DEMAND FROM ELECTRIC MOTORS, GENERATORS, AND SMALL TRANSFORMERS TO AUGMENT DEMAND

10 ELECTRICAL STEEL MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 TRANSFORMERS

- 10.2.1 INCREASE IN DEMAND FOR ENERGY TO DRIVE DEMAND

- 10.3 MOTORS

- 10.3.1 INCREASING APPLICATIONS IN TRANSPORTATION AND AUTOMOTIVE TO AUGMENT DEMAND

- 10.4 INDUCTORS

- 10.4.1 INCREASE IN DEPLOYMENT OF SMART GRIDS TO PROPEL MARKET GROWTH

- 10.5 OTHER APPLICATIONS

11 ELECTRICAL STEEL MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 ENERGY

- 11.2.1 RAPID EXPANSION OF RENEWABLE ENERGY PROJECTS TO DRIVE DEMAND

- 11.3 AUTOMOTIVE

- 11.3.1 RAPID GROWTH IN ELECTRIC VEHICLE PRODUCTION AND GLOBAL EV SALES TO FUEL DEMAND

- 11.4 MANUFACTURING

- 11.4.1 RISING ADOPTION OF INDUSTRIAL AUTOMATION AND SMART MANUFACTURING TECHNOLOGIES TO DRIVE MARKET

- 11.5 HOUSEHOLD APPLIANCES

- 11.5.1 HIGHER LIVING STANDARDS AND RISE IN INCOME TO PROPEL MARKET

- 11.6 OTHER END-USE INDUSTRIES

12 ELECTRICAL STEEL MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Strong consumer appliance production and export-led manufacturing growth to propel market

- 12.2.2 JAPAN

- 12.2.2.1 Offshore wind capacity development and renewable energy investments to drive market

- 12.2.3 INDIA

- 12.2.3.1 Rapid renewable energy expansion and power grid modernization to boost market growth

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Rapid electric vehicle growth to augment market

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Growth in electric vehicles to propel market growth

- 12.3.2 CANADA

- 12.3.2.1 Large-scale renewable energy capacity expansion and power generation growth to support market

- 12.3.3 MEXICO

- 12.3.3.1 Electric vehicle adoption and e-mobility infrastructure development to drive market

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Energy transition, EV growth, and industrial strength driving demand

- 12.4.2 UK

- 12.4.2.1 Clean energy transition and electrification driving electrical steel demand

- 12.4.3 RUSSIA

- 12.4.3.1 Industrial recovery, electrification trends, and energy diversification to boost demand

- 12.4.4 FRANCE

- 12.4.4.1 Low-carbon electricity dominance and electrification driving market growth

- 12.4.5 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Energy transition and industrial expansion supporting market expansion

- 12.5.1.1 Saudi Arabia

- 12.5.2 UAE

- 12.5.2.1 Energy diversification and industrial growth to drive demand

- 12.5.2.2 Rest of GCC Countries

- 12.5.3 SOUTH AFRICA

- 12.5.3.1 Energy transition and automotive sector growth to increase demand

- 12.5.4 EGYPT

- 12.5.4.1 Industrial growth and energy transition accelerating market growth

- 12.5.5 QATAR

- 12.5.5.1 Electrification initiatives and renewable energy expansion increasing demand

- 12.5.6 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Expansion of renewable energy and industrial sectors to accelerate market growth

- 12.6.2 ARGENTINA

- 12.6.2.1 Economic recovery and electrification trends to drive demand

- 12.6.3 PERU

- 12.6.3.1 Energy diversification activities and industrial expansion to drive market

- 12.6.4 CHILE

- 12.6.4.1 Renewable leadership and electrification trends driving market expansion

- 12.6.5 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 FINANCIAL METRICS

- 13.7 BRAND COMPARISON

- 13.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.8.1 STARS

- 13.8.2 EMERGING LEADERS

- 13.8.3 PERVASIVE PLAYERS

- 13.8.4 PARTICIPANTS

- 13.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.8.5.1 Company footprint

- 13.8.5.2 Region footprint

- 13.8.5.3 Type footprint

- 13.8.5.4 Application footprint

- 13.8.5.5 End-use industry footprint

- 13.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.9.1 PROGRESSIVE COMPANIES

- 13.9.2 RESPONSIVE COMPANIES

- 13.9.3 DYNAMIC COMPANIES

- 13.9.4 STARTING BLOCKS

- 13.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.9.5.1 Detailed list of key startups/SMEs

- 13.9.5.2 Competitive benchmarking of key startups/SMEs

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES

- 13.10.2 DEALS

- 13.10.3 EXPANSIONS

- 13.10.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 ARCELORMITTAL

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.3.2 Expansions

- 14.1.1.3.3 Others

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 POSCO

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Deals

- 14.1.2.3.2 Expansions

- 14.1.2.3.3 Others

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 CHINA BAOWU STEEL GROUP CORPORATION LIMITED

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 VOESTALPINE AG

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Expansions

- 14.1.4.3.3 Others

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 NIPPON STEEL CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Deals

- 14.1.5.3.2 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 UNITED STATES STEEL CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Deals

- 14.1.6.3.3 Expansions

- 14.1.6.4 MnM view

- 14.1.7 STEEL AUTHORITY OF INDIA LIMITED (SAIL)

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.7.3.2 Expansions

- 14.1.7.4 MnM view

- 14.1.8 TATA STEEL

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.8.3.2 Others

- 14.1.8.4 MnM view

- 14.1.9 THYSSENKRUPP AG

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Expansions

- 14.1.9.3.2 Others

- 14.1.9.4 MnM view

- 14.1.10 JFE STEEL CORPORATION

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.10.3.2 Expansions

- 14.1.10.3.3 Others

- 14.1.10.4 MnM view

- 14.1.1 ARCELORMITTAL

- 14.2 OTHER PLAYERS

- 14.2.1 CLEVELAND-CLIFFS INC.

- 14.2.2 HEBEI PUYANG IRON AND STEEL GROUP

- 14.2.3 JIANGSU SHAGANG INTERNATIONAL TRADE CO., LTD.

- 14.2.4 CHINA STEEL CORPORATION

- 14.2.5 JSW STEEL

- 14.2.6 LEICONG INDUSTRIAL CO., LTD.

- 14.2.7 ANGANG STEEL COMPANY LIMITED

- 14.2.8 APERAM S.A.

- 14.2.9 ALLEGHENY TECHNOLOGIES

- 14.2.10 UNION ELECTRIC STEEL CORPORATION

- 14.2.11 EURO-MIT STAAL B.V.

- 14.2.12 TC METAL

- 14.2.13 VESUVIUS PLC

- 14.2.14 FERRIC SRL

- 14.2.15 WAELZHOLZ GMBH & CO.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.1.2 List of secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key primary participants

- 15.1.2.2 Key data from primary sources

- 15.1.2.3 Breakdown of interviews with experts

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 TOP-DOWN APPROACH

- 15.2.2 BOTTOM-UP APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 SUPPLY-SIDE APPROACH

- 15.4 GROWTH FORECAST

- 15.5 DATA TRIANGULATION

- 15.6 RESEARCH ASSUMPTIONS

- 15.7 RESEARCH LIMITATIONS & RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS