|

시장보고서

상품코드

2072268

블록체인 시장 : 제공 제품별, 프로바이더별, 유형별, 도입 모드별, 조직 규모별, 업계별, 지역별 - 예측(-2031년)Blockchain Market by Offering (Middleware/Web3 Infrastructure, Platforms, Services), Provider (Application, Infrastructure, Middleware), Type (Public, Private, Hybrid, Consortium), Deployment Mode, Vertical, and Region - Global Forecast to 2031 |

||||||

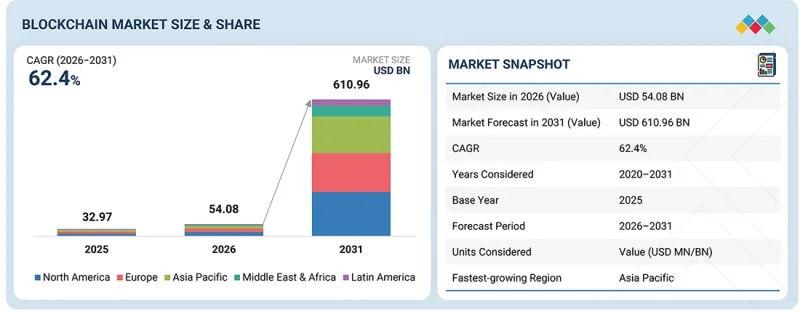

블록체인 시장 규모는 2026년 540억 8,000만 달러에서 2031년까지 6,109억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 62.4%를 기록할 전망입니다.

이 시장은 금융 서비스, 의료, 정부 및 기업 분야에서 안전한 디지털 신원 인증, 개인정보를 보호하는 데이터 공유, 그리고 규정을 준수하는 인증에 대한 수요가 증가함에 따라 성장하고 있습니다. 조직에서는 ID 사기를 줄이고, 온보딩 프로세스의 효율성을 높이며, 신뢰할 수 있는 디지털 상호작용을 실현하기 위해 블록체인 기반의 분산형 ID(DID) 프레임워크와 검증 가능한 자격 증명을 도입하는 움직임이 점점 더 확산되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(10억 달러) |

| 부문 | 제공 제품별, 프로바이더별, 유형별, 도입 모드별, 조직 규모별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

자기주권형 신원(SSI), 제로 지식 증명(ZKP), 상호 운용 가능한 인증 표준의 발전에 힘입어 도입이 더욱 가속화되고 있습니다. 한편, 정부 주도의 디지털 신원 인증 구상과 보안이 강화된 AI 기반 디지털 서비스에 대한 수요 증가가 계속해서 시장 확대를 뒷받침하고 있습니다.

“예측 기간 동안 전문 서비스 부문이 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망된다”

서비스별로 살펴보면, 블록체인 전략, 컨설팅, 구현, 통합 및 스마트 계약 개발에 대한 전문적인 노하우에 대한 수요가 증가하고 있어, 예측 기간 동안 블록체인 시장에서 전문 서비스 부문이 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측됩니다. BFSI, 정부, 소매 및 전자상거래, 헬스케어, 공급망 등 각 업계의 기업들이 블록체인 도입을 가속화함에 따라, 이용 사례 평가, 적절한 블록체인 플랫폼 선정, 규제 준수 확보, 그리고 블록체인과 기존 기업 시스템 간의 통합을 수행하기 위한 전문 서비스가 필요해지고 있습니다. 토큰화, 디지털 ID, 분산형 용도(dApps), 크로스체인 상호운용성의 복잡성이 점점 더 커지고 있는 점도 자문, 보안 감사, 도입 서비스에 대한 수요를 더욱 부추기고 있습니다. 또한, 기업들은 도입 위험을 줄이고, 투자 수익률(ROI)을 최적화하며, 기업 차원의 블록체인 혁신 이니셔티브를 가속화하기 위해 블록체인 컨설팅 회사 및 시스템 통합 업체에 대한 의존도를 높이고 있습니다.

“2026년에는 프라이빗 블록체인 부문이 블록체인 시장에서 가장 큰 점유율을 차지할 것으로 전망된다”

유형별로는 프라이빗 블록체인 부문이 2026년에 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이는 데이터 개인정보 보호, 보안, 거버넌스 및 규제 준수와 관련된 기업의 요구 사항과 밀접하게 부합하기 때문입니다. BFSI(은행 및 금융 및 보험), 정부 기관, 의료, 소매 및 전자상거래, 공급망 등의 분야에 속한 조직들은 참가자의 접근 및 거래 검증에 대한 통제를 유지하면서 기밀 정보를 안전하게 공유하기 위해 허가형 블록체인 네트워크를 점점 더 선호하고 있습니다. 프라이빗 블록체인은 퍼블릭 네트워크보다 높은 처리량, 낮은 지연 시간, 뛰어난 확장성을 제공하기 때문에 국경을 초월한 결제, 디지털 ID, 무역 금융, 자산 토큰화, 공급망 추적성 등 미션 크리티컬한 엔터프라이즈 용도에 가장 적합합니다. Hyperledger Fabric, R3 Corda, Canton과 같은 엔터프라이즈 플랫폼의 도입 확대에 더해, 주요 벤더들의 Blockchain-as-a-Service(BaaS) 및 디지털 자산 인프라에 대한 투자 증가로 인해 프라이빗 블록체인 부문의 우위는 계속해서 강화되고 있습니다.

“2026년부터 2031년에 걸쳐 아시아태평양의 블록체인 시장에서 한국이 가장 높은 성장률을 나타낼 것으로 전망된다”

국가별로 살펴보면, 디지털 혁신에 대한 정부의 강력한 지원, 디지털 결제 기술의 광범위한 보급, 그리고 선진적인 ICT 인프라를 바탕으로, 예측 기간 동안 한국이 블록체인 시장에서 가장 높은 성장률을 보일 것으로 예측됩니다. Web3 생태계 육성, 디지털 자산 혁신, 그리고 블록체인을 활용한 공공 서비스에 대한 집중이 기업들의 블록체인 도입을 가속화하고 있습니다. 금융기관들은 결제, 자산의 토큰화, 디지털 ID 관리 분야에서 블록체인의 활용 방안을 점점 더 모색하고 있습니다. 또한, 메타버스 플랫폼, 게임 용도, 분산형 기술에 대한 투자 확대가 블록체인 솔루션의 새로운 활용 사례를 창출하고 있습니다. 기술적으로 선진적인 한국의 소비자층에 더해, 안전하고 투명성이 높은 디지털 거래에 대한 수요가 증가함에 따라 시장 성장이 지속적으로 뒷받침되고 있습니다. 대형 기술 기업의 존재와 활발한 스타트업 생태계가 블록체인 혁신과 상용화를 더욱 촉진하고 있습니다.

블록체인 시장의 주요 업체로는 OVHcloud(프랑스), AWS(미국), IBM(미국), Oracle(미국), Huawei(중국), Accenture(아일랜드), TCS(인도), Google(미국), Alibaba Cloud(중국), Microsoft(미국), SAP(독일), HPE(미국), Tencent Cloud(중국), Wipro(인도), Infosys(인도), Lumen Technologies(미국), DigitalOcean(미국), VMware(미국), Linode(Akamai)(미국), Applied Blockchain(영국), Consensys(미국), Contabo(독일), LeewayHertz(미국), Vultr(미국), CloudSigma(스위스), MEVSPACE(폴란드), Scaleway(프랑스), Kaleido(미국), Chainlink Labs(미국), Alchemy(미국), Blockdaemon(미국), Qubetics(벨리즈), CoreWeave(미국), Hetzner(독일), T-Cloud Public(독일), Exoscale(스위스), UpCloud(핀란드), TeraSwitch(미국), Latitude.sh(브라질), Limestone Networks(미국), Allnodes(미국), Cherry Servers(리투아니아). 본 조사에서는 블록체인 시장의 주요 시장 진출기업에 대한 상세한 경쟁 분석, 각 기업프로파일, 최근 동향 및 주요 시장 전략을 종합적으로 다루고 있습니다.

조사 범위

본 보고서에서는 블록체인 시장을 세분화하여, 제공 서비스별, 공급업체별, 유형별, 배포 방식별, 조직 규모별, 산업별 및 지역별로 분석했습니다.

또한, 본 조사에서는 시장의 주요 시장 진출기업에 대한 상세한 경쟁 분석, 각 기업프로파일, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 주요 시장 전략에 대해서도 다루고 있습니다.

본 보고서를 구매할 때의 주요 이점

본 보고서는 블록체인 시장 전체 및 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써, 시장을 선도하는 기업과 신규 진출기업 여러분을 지원합니다. 본 보고서는 이해관계자 여러분이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 나은 위치로 이끌며, 적절한 시장 진출 전략을 수립하는 데 필요한 귀중한 인사이트를 얻는 데 도움이 될 것입니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 성장 촉진요인, 시장 성장 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(실물 자산의 토큰화, 프라이빗 및 퍼미션형 블록체인을 통한 기업 도입, BaaS(Blockchain-as-a-Service) 및 클라우드 도입, 소매, 공급망 관리(SCM), 은행 업무에서 안전하고 투명한 거래에 대한 수요 증가), 제약 요인(지역별로 달라지고 파편화된 규제 환경, 대규모 도입 시 확장성 및 성능의 한계), 기회(블록체인 플랫폼 및 서비스와 관련된 정부 주도 이니셔티브 증가, 블록체인과 인공지능 및 사물인터넷(IoT)의 융합, 분산형 ID 및 디지털 ID 솔루션 채택 확대, 탈중앙화 금융(DeFi)의 성장과 기존 금융 시스템과의 통합), 그리고 과제(블록체인 생태계의 보안 취약점, 개인정보 보호에 대한 우려 및 키 관리상의 과제, 블록체인 및 Web3에 관한 전문적인 기술 노하우 부족)

- 제품 개발/혁신 : 블록체인 시장의 향후 기술, 연구개발 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 종합적인 정보 -- 본 보고서에서는 다양한 지역에 걸친 블록체인 시장을 분석했습니다.

- 시장의 다양화: 블록체인 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : 블록체인 시장의 주요 기업(AWS(미국), IBM(미국), OVHcloud(프랑스), Huawei(중국), Oracle(미국), Accenture(아일랜드) 등) 시장 점유율, 성장 전략 및 서비스 제공 내용에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 소비자 상황과 구매 행동

제9장 블록체인 시장(제공 제품별)

제10장 블록체인 시장(프로바이더별)

제11장 블록체인 시장(유형별)

제12장 블록체인 시장(도입 모드별)

제13장 블록체인 시장(조직 규모별)

제14장 블록체인 시장(업계별)

제15장 블록체인 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

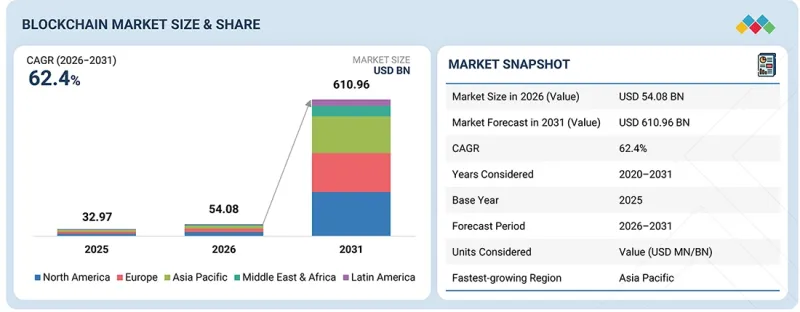

LSH 26.07.03The blockchain market size is anticipated to reach USD 610.96 billion by 2031 from USD 54.08 billion in 2026, recording a CAGR of 62.4% during the forecast period. This market is driven by the increasing need for secure digital identity verification, privacy-preserving data sharing, and regulatory-compliant authentication across financial services, healthcare, government, and enterprise environments. Organizations are increasingly adopting blockchain-based decentralized identity (DID) frameworks and verifiable credentials to reduce identity fraud, streamline onboarding processes, and enable trusted digital interactions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | Offering, Provider, Type, Deployment Mode, Organization Size, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, Latin America |

Advancements in self-sovereign identity (SSI), zero-knowledge proofs (ZKPs), and interoperable credential standards are further accelerating deployment. In contrast, government-led digital identity initiatives and growing demand for secure AI-enabled digital services continue to support market expansion.

"Professional services segment to witness the highest CAGR during the forecast period"

By service, the professional services segment is expected to witness the highest CAGR in the blockchain market during the forecast period due to the mounting demand for specialized expertise in blockchain strategy, consulting, implementation, integration, and smart contract development. As enterprises across BFSI, government, retail & e-commerce, healthcare, and supply chain accelerate blockchain adoption, they require professional services to assess business use cases, select appropriate blockchain platforms, ensure regulatory compliance, and integrate blockchain with existing enterprise systems. The growing complexity of tokenization, digital identity, decentralized applications (dApps), and cross-chain interoperability is further driving the demand for advisory, security auditing, and implementation services. Additionally, organizations are increasingly relying on blockchain consulting firms and system integrators to reduce deployment risks, optimize return on investment, and accelerate enterprise-scale blockchain transformation initiatives.

"Private segment to capture the largest share of the blockchain market in 2026"

By type, the private blockchain segment is projected to hold the largest market share in 2026, which can be attributed to its strong alignment with enterprise requirements for data privacy, security, governance, and regulatory compliance. Organizations across BFSI, government, healthcare, retail & e-commerce, and supply chain increasingly prefer permissioned blockchain networks to securely share sensitive information while maintaining control over participant access and transaction validation. Private blockchains offer higher throughput, lower latency, and greater scalability than public networks, making them well-suited for mission-critical enterprise applications such as cross-border payments, digital identity, trade finance, asset tokenization, and supply chain traceability. Growing adoption of enterprise platforms, such as Hyperledger Fabric, R3 Corda, and Canton, along with increasing investment in Blockchain-as-a-Service (BaaS) and digital asset infrastructure by leading technology vendors, continues to strengthen the dominance of the private blockchain segment.

"South Korea to grow at the highest rate in the Asia Pacific blockchain market from 2026 to 2031"

By country, South Korea is expected to be the fastest-growing in the blockchain market during the forecast period, driven by strong government support for digital innovation, widespread adoption of digital payment technologies, and an advanced ICT infrastructure. The focus on fostering Web3 ecosystems, digital asset innovation, and blockchain-based public services is accelerating enterprise adoption. Financial institutions are increasingly exploring blockchain for payments, asset tokenization, and digital identity management. Additionally, increasing investments in metaverse platforms, gaming applications, and decentralized technologies are creating new use cases for blockchain solutions. South Korea's technologically advanced consumer base, coupled with the increasing demand for secure and transparent digital transactions, continues to strengthen market growth. The presence of major technology firms and active startup ecosystems further supports blockchain innovation and commercialization.

Breakdown of Primaries

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 30%, Tier 2 - 50%, and Tier 3 - 20%

- By Designation: C-level Executives - 50% and Managers and Other Levels - 50%

- By Region: North America - 25%, Europe - 25%, Asia Pacific - 25%, Middle East & Africa - 15%, Latin America - 10%

Major vendors in the blockchain market include OVHcloud (France), AWS (US), IBM (US), Oracle (US), Huawei (China), Accenture (Ireland), TCS (India), Google (US), Alibaba Cloud (China), Microsoft (US), SAP (Germany), HPE (US), Tencent Cloud (China), Wipro (India), Infosys (India), Lumen Technologies (US), DigitalOcean (US), VMware (US), Linode (Akamai) (US), Applied Blockchain (UK), Consensys (US), Contabo (Germany), LeewayHertz (US), Vultr (US), CloudSigma (Switzerland), MEVSPACE (Poland), Scaleway (France), Kaleido (US), Chainlink Labs (US), Alchemy (US), Blockdaemon (US), Qubetics (Belize), CoreWeave (US), Hetzner (Germany), T-Cloud Public (Germany), Exoscale (Switzerland), UpCloud (Finland), TeraSwitch (US), Latitude.sh (Brazil), Limestone Networks (US), Allnodes (US), and Cherry Servers (Lithuania). The study includes an in-depth competitive analysis of the key players in the blockchain market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the blockchain market and forecasts its size based on offering [infrastructure (compute infrastructure, storage & networking, node/validator hosting infrastructure, and other infrastructure), platforms (core blockchain platforms and blockchain-as-a-service), middleware/web3 infrastructure (node services/RPC infrastructure, APIs & integration layers, and developer tools), services (professional (technology advisory & consulting, integration & deployment, and support & maintenance), managed services)], provider (application providers, infrastructure providers, and middleware providers), type (public, private, hybrid, and consortium), deployment mode (on-premises, cloud-based, and hybrid), organization size (SMEs and large-sized enterprises), vertical (transportation & logistics, agriculture & food, manufacturing, energy & utilities, healthcare & life sciences, media, advertising, & entertainment, banking & financial services, insurance, it & telecom, retail & ecommerce, government, real estate & construction, and other verticals), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall blockchain market and its sub-segments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Tokenization of real-world assets, Enterprise adoption via private and permissioned blockchains, Blockchain-as-a-Service and cloud adoption, Growing demand for secure and transparent transactions in retail, SCM, and banking applications), restraints (Evolving and fragmented regulatory landscape across regions, Scalability and performance limitations in large-scale deployments), opportunities (Increase in government initiatives related to blockchain platforms and services, Convergence of blockchain with artificial intelligence and the Internet of Things (IoT), Rising adoption of Decentralized Identity and digital identity solutions, Growth of Decentralized Finance and integration with traditional financial systems), and challenges (Security vulnerabilities, privacy concerns, and key management challenges in blockchain ecosystems, Shortage of specialized blockchain and Web3 technical expertise)

- Product Development/Innovation: Detailed insights on upcoming technologies, research development activities, new products, and service launches in the blockchain market

- Market Development: Comprehensive information about lucrative markets-the report analyses the blockchain market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the blockchain market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as AWS (US), IBM (US), OVHcloud (France), Huawei (China), Oracle (US), and Accenture (Ireland), among others, in the blockchain market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMMENTATION & REGION COVERAGE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BLOCKCHAIN MARKET

- 3.2 BLOCKCHAIN MARKET, BY OFFERING

- 3.3 BLOCKCHAIN MARKET, BY SERVICE

- 3.4 BLOCKCHAIN MARKET, BY PROFESSIONAL SERVICE

- 3.5 BLOCKCHAIN MARKET, BY PROVIDER

- 3.6 BLOCKCHAIN MARKET, BY TYPE

- 3.7 BLOCKCHAIN MARKET, BY DEPLOYMENT MODE

- 3.8 BLOCKCHAIN MARKET, BY ORGANIZATION SIZE

- 3.9 BLOCKCHAIN MARKET, BY VERTICAL

- 3.10 BLOCKCHAIN MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Tokenization of real-world assets (RWA)

- 4.2.1.2 Enterprise adoption via private & permissioned blockchains

- 4.2.1.3 Blockchain-as-a-Service (BaaS) & cloud adoption

- 4.2.1.4 Growing demand for secure and transparent transactions in retail, SCM, and banking applications

- 4.2.2 RESTRAINTS

- 4.2.2.1 Evolving and fragmented regulatory landscape across regions

- 4.2.2.2 Scalability and performance limitations in large-scale deployments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increase in government initiatives to boost demand for blockchain platforms and services

- 4.2.3.2 Convergence of blockchain with Artificial Intelligence (AI) and Internet of Things (IoT)

- 4.2.3.3 Rising adoption of Decentralized Identity (DID) and digital identity solutions

- 4.2.3.4 Growth of Decentralized Finance (DeFi) and integration with traditional financial systems

- 4.2.4 CHALLENGES

- 4.2.4.1 Security vulnerabilities, privacy concerns, and key management challenges in blockchain ecosystems

- 4.2.4.2 Shortage of specialized blockchain and Web3 technical expertise

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER -1/2/3 PLAYERS

- 4.5.1 CROSS-TIER STRATEGIC PATTERNS

- 4.5.2 STRATEGIC TRENDS

- 4.5.2.1 Institutional adoption and tokenized financial infrastructure

- 4.5.2.2 Emergence of modular blockchain architectures and layer-2 scaling

- 4.5.2.3 Growth of stablecoins and blockchain-based payment systems

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL BLOCKCHAIN INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 PLANNING & DESIGN

- 5.3.2 INFRASTRUCTURE DEVELOPMENT (BLOCKCHAIN PLATFORMS)

- 5.3.3 SYSTEM INTEGRATION

- 5.3.4 ECOSYSTEM PARTNERS & PLATFORM PROVIDERS

- 5.3.5 CONSULTATION & ADVISORY (CROSS-STAGE LAYER)

- 5.3.6 END USER GROUPS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PLATFORM

- 5.5.2 INDICATIVE PRICING ANALYSIS FOR KEY PLAYERS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8471)

- 5.6.2 EXPORT SCENARIO (HS CODE 8471)

- 5.7 KEY CONFERENCES & EVENTS, 2026

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 KEY BLOCKCHAIN USE CASES AND REAL-WORLD IMPLEMENTATIONS

- 5.10.1.1 Smart Dubai Initiative - Blockchain-Enabled Government Transformation

- 5.10.1.2 Estonia - National Blockchain Infrastructure for Digital Governance

- 5.10.1.3 Central Bank Digital Currencies (CBDCs) - Digital Currency Innovation

- 5.10.1.4 Blockchain in Supply Chain Traceability & ESG Compliance

- 5.10.1.5 Blockchain for Cross-Border Payments and Financial Settlement Modernization

- 5.10.2 CASE STUDIES

- 5.10.2.1 Maersk collaborated with IBM to streamline global shipping through blockchain-enabled logistics visibility

- 5.10.2.2 HSBC leveraged R3's Corda platform to digitize trade finance and streamline cross-border transactions

- 5.10.2.3 Singapore Exchange implemented Nasdaq blockchain solutions to modernize post-trade settlement processes

- 5.10.2.4 Walmart used IBM's blockchain platform to reduce the wastage of food by improving food safety and traceability

- 5.10.2.5 De Beers utilized Everledger to ensure diamond provenance and authenticity tracking

- 5.10.2.6 IBM Blockchain helped Home Depot streamline supply chain

- 5.10.2.7 Arab Jordan Investment Bank (AJIB) leveraged Oracle's blockchain platform for cross-border money transfers

- 5.10.2.8 Platon Finance partnered with Broadcom (Symantec) to strengthen crypto platform security

- 5.10.1 KEY BLOCKCHAIN USE CASES AND REAL-WORLD IMPLEMENTATIONS

- 5.11 IMPACT OF 2025 US TARIFFS - BLOCKCHAIN MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Distributed Ledger Technology (DLT)

- 6.1.1.2 Smart Contracts

- 6.1.1.3 Zero-Knowledge Proofs (ZKPs)

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Secure Multi-Party Computation (SMPC/MPC)

- 6.1.2.2 Digital Identity Solutions

- 6.1.2.3 Edge Computing

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 5G Networks

- 6.1.3.2 Digital Twins

- 6.1.3.3 Quantum Computing

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2026-2027) | FOUNDATION & EARLY ENTERPRISE ADOPTION

- 6.2.2 MID-TERM (2027-2030) SCALE-UP, INTEROPERABILITY & INTELLIGENT AUTOMATION

- 6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, TOKENIZED & DECENTRALIZED DIGITAL ECOSYSTEMS

- 6.3 IMPLEMENTATION OF BLOCKCHAIN TECHNOLOGY

- 6.4 COMPARISON BETWEEN CENTRALIZED/PERMISSIONED AND DECENTRALIZED/PERMISSIONLESS BLOCKCHAINS

- 6.4.1 TYPES OF BLOCKCHAIN TECHNOLOGY

- 6.4.1.1 Private blockchain

- 6.4.1.2 Public blockchain

- 6.4.1.3 Permissioned/Hybrid blockchain

- 6.4.1 TYPES OF BLOCKCHAIN TECHNOLOGY

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-INTEGRATED DECENTRALIZED FINANCE (DEFI) PLATFORMS

- 6.6.2 CENTRAL BANK DIGITAL CURRENCIES (CBDCS)

- 6.6.3 BLOCKCHAIN-ENABLED DIGITAL TWINS

- 6.6.4 DECENTRALIZED DIGITAL IDENTITY (DID) SYSTEMS

- 6.6.5 BLOCKCHAIN-POWERED SUPPLY CHAIN & TRADE FINANCE NETWORKS

- 6.7 IMPACT OF AI/GEN AI ON BLOCKCHAIN MARKET

- 6.7.1 BEST PRACTICES IN BLOCKCHAIN MARKET

- 6.7.2 CASE STUDIES OF AI IMPLEMENTATION IN THE BLOCKCHAIN MARKET

- 6.7.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN BLOCKCHAIN MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 MICROSOFT: ION DIGITAL IDENTITY PLATFORM

- 6.8.2 RIPPLE: SBI REMIT CROSS-BORDER PAYMENT MODERNIZATION

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CONSUMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

9 BLOCKCHAIN MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: BLOCKCHAIN MARKET DRIVERS

- 9.2 INFRASTRUCTURE

- 9.2.1 RISING DEMAND FOR HIGH-PERFORMANCE, SECURE, AND DISTRIBUTED INFRASTRUCTURE DRIVES BLOCKCHAIN ADOPTION

- 9.3 PLATFORMS

- 9.3.1 GROWING DEMAND FOR SECURE, TRANSPARENT, AND SCALABLE DIGITAL TRANSACTIONS ACCELERATES ADOPTION OF BLOCKCHAIN PLATFORMS

- 9.4 MIDDLEWARE/WEB3 INFRASTRUCTURE

- 9.4.1 INTENSIFYING DEMAND FOR MULTI-CHAIN CONNECTIVITY, REAL-TIME DATA ACCESS, AND DEVELOPER ENABLEMENT TO DRIVE WEB3 INFRASTRUCTURE GROWTH

- 9.5 SERVICES

- 9.5.1 FOCUS ON ENTERPRISE DEPLOYMENT, OPERATIONAL SCALABILITY, AND LONG-TERM BLOCKCHAIN MANAGEMENT TO DRIVE SERVICES DEMAND

- 9.5.2 PROFESSIONAL SERVICES

- 9.5.2.1 Technology advisory & consulting

- 9.5.2.2 Integration & Deployment

- 9.5.2.3 Support & maintenance

- 9.5.3 MANAGED SERVICES

10 BLOCKCHAIN MARKET, BY PROVIDER

- 10.1 INTRODUCTION

- 10.1.1 PROVIDERS: BLOCKCHAIN MARKET DRIVERS

- 10.2 APPLICATION PROVIDERS

- 10.2.1 NEED FOR COMPANIES TO LEVERAGE BENEFITS OF BLOCKCHAIN TECHNOLOGY TO DRIVE POPULARITY OF APPLICATION PROVIDERS

- 10.3 INFRASTRUCTURE PROVIDERS

- 10.3.1 INFRASTRUCTURE MANAGEMENT TO HELP MANAGE BACKEND OPERATIONS OF BLOCKCHAIN APPLICATIONS FOR BUSINESSES

- 10.4 MIDDLEWARE PROVIDERS

- 10.4.1 BLOCKCHAIN MIDDLEWARE PROVIDERS TO ENSURE QUICK DEVELOPMENT OF APPLICATIONS AND INTERFACES

11 BLOCKCHAIN MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.1.1 TYPES: BLOCKCHAIN MARKET DRIVERS

- 11.2 PUBLIC

- 11.2.1 NEED FOR MAINTAINING SAFETY AND TRANSPARENCY OF NETWORKS TO DRIVE DEMAND FOR PUBLIC BLOCKCHAIN SERVICES

- 11.3 PRIVATE

- 11.3.1 PRIVATE BLOCKCHAIN TO PROVIDE OPPORTUNITIES TO LEVERAGE BLOCKCHAIN TECHNOLOGY FOR BUSINESS-TO-BUSINESS USE CASES

- 11.4 HYBRID

- 11.4.1 BLEND OF ESSENTIAL FEATURES OF PUBLIC AND PRIVATE BLOCKCHAIN TO MAKE TRANSACTIONS MORE SECURE

- 11.5 CONSORTIUM

- 11.5.1 CONSORTIUM BLOCKCHAIN TO OFFER ENHANCED SECURITY AND CONTROL WHILE STILL ENABLING COLLABORATION AMONG TRUSTED PARTIES

12 BLOCKCHAIN MARKET, BY DEPLOYMENT MODE

- 12.1 INTRODUCTION

- 12.1.1 DEPLOYMENT MODE: BLOCKCHAIN MARKET DRIVERS

- 12.2 ON-PREMISES

- 12.2.1 DATA SOVEREIGNTY, REGULATORY COMPLIANCE, AND FULL INFRASTRUCTURE CONTROL ARE DRIVING ON-PREMISES MODEL

- 12.3 CLOUD

- 12.3.1 CLOUD BLOCKCHAIN ADOPTION IS ACCELERATED BY SCALABLE BAAS MODELS, COST EFFICIENCY, AND ENTERPRISE-GRADE MANAGED SERVICES

- 12.4 HYBRID

- 12.4.1 HYBRID DEPLOYMENT MODE TO OFFER BALANCED SECURITY, SCALABILITY, AND INTEROPERABILITY ACROSS ENVIRONMENTS

13 BLOCKCHAIN MARKET, BY ORGANIZATION SIZE

- 13.1 INTRODUCTION

- 13.1.1 ORGANIZATION SIZE: BLOCKCHAIN MARKET DRIVERS

- 13.2 SMES

- 13.2.1 NEED FOR GROWTH AND DEVELOPMENT OF SMES TO BOOST POPULARITY OF BLOCKCHAIN SERVICES

- 13.3 LARGE ENTERPRISES

- 13.3.1 FINANCIAL CAPACITY OF LARGE ENTERPRISES TO INCORPORATE NEW TECHNOLOGIES TO DRIVE ADOPTION OF BLOCKCHAIN SERVICES

14 BLOCKCHAIN MARKET, BY VERTICAL

- 14.1 INTRODUCTION

- 14.1.1 VERTICAL: BLOCKCHAIN MARKET DRIVERS

- 14.2 TRANSPORTATION & LOGISTICS

- 14.2.1 NEED FOR CLOSE COORDINATION BETWEEN MULTIPLE PARTIES TO BOLSTER ADOPTION OF BLOCKCHAIN SERVICES

- 14.2.2 TRANSPORTATION & LOGISTICS: BLOCKCHAIN APPLICATIONS

- 14.2.2.1 Financing

- 14.2.2.2 Mobility solutions

- 14.2.2.3 Smart contracts

- 14.2.2.4 Other transportation & logistics applications

- 14.3 AGRICULTURE & FOOD

- 14.3.1 DEMAND FOR SUSTAINABLE FOOD ECOSYSTEM AND FOOD CERTIFICATION TO SPUR GROWTH

- 14.3.2 AGRICULTURE & FOOD: BLOCKCHAIN APPLICATIONS

- 14.3.2.1 Product traceability, tracking, and visibility

- 14.3.2.2 Payment & settlement

- 14.3.2.3 Smart contracts

- 14.3.2.4 Improved quality control & food safety

- 14.4 MANUFACTURING

- 14.4.1 USE OF SMART TAGS AND RFID SENSORS TO ENSURE TRACEABILITY IN MANUFACTURING INDUSTRY

- 14.4.2 MANUFACTURING: BLOCKCHAIN APPLICATIONS

- 14.4.2.1 Predictive maintenance

- 14.4.2.2 Asset tracking & management

- 14.4.2.3 Business process optimization

- 14.4.2.4 Logistics & supply chain management

- 14.4.2.5 Quality control & compliance

- 14.4.2.6 Other manufacturing applications

- 14.5 ENERGY & UTILITIES

- 14.5.1 MARKET DIGITALIZATION TO ACCELERATE BLOCKCHAIN ADOPTION IN ENERGY & UTILITIES SECTOR

- 14.5.2 ENERGY & UTILITIES: BLOCKCHAIN APPLICATIONS

- 14.5.2.1 Grid management

- 14.5.2.2 Energy trading

- 14.5.2.3 GRC management

- 14.5.2.4 Payment schemes

- 14.5.2.5 Supply chain management

- 14.5.2.6 Other energy & utility applications

- 14.6 HEALTHCARE & LIFE SCIENCES

- 14.6.1 NEED TO SECURE CRITICAL PATIENT DATA, IMPROVE INTEROPERABILITY, AND COMBAT COUNTERFEIT MEDICINES TO DRIVE BLOCKCHAIN ADOPTION

- 14.6.2 HEALTHCARE & LIFE SCIENCES: BLOCKCHAIN APPLICATIONS

- 14.6.2.1 Clinical data exchange & interoperability

- 14.6.2.2 Supply chain management

- 14.6.2.3 Claims adjudication & billing management

- 14.6.2.4 Other healthcare & life science applications

- 14.7 MEDIA, ADVERTISING, AND ENTERTAINMENT

- 14.7.1 BLOCKCHAIN-BASED CONTENT MONETIZATION, DIGITAL RIGHTS PROTECTION, AND ADVERTISING TRANSPARENCY TO DRIVE MARKET GROWTH

- 14.7.2 MEDIA, ADVERTISING, AND ENTERTAINMENT: BLOCKCHAIN APPLICATIONS

- 14.7.2.1 Licensing & rights management

- 14.7.2.2 Digital advertising

- 14.7.2.3 Smart contracts

- 14.7.2.4 Content security

- 14.7.2.5 Online gaming

- 14.7.2.6 Payments

- 14.7.2.7 Other media, advertising, and entertainment applications

- 14.8 BANKING & FINANCIAL SERVICES

- 14.8.1 RISE IN TOKENIZATION, INSTITUTIONAL DIGITAL ASSETS, AND REAL-TIME SETTLEMENT NETWORKS TO DRIVE BLOCKCHAIN ADOPTION

- 14.8.2 BANKING & FINANCIAL SERVICES: BLOCKCHAIN APPLICATIONS

- 14.8.2.1 Payments, clearing, and settlement

- 14.8.2.2 Exchanges & remittance

- 14.8.2.3 Smart contracts

- 14.8.2.4 Identity management

- 14.8.2.5 Compliance management/KYC

- 14.8.2.6 Other banking & financial service applications

- 14.9 INSURANCE

- 14.9.1 RAPID AUTOMATION ACROSS INSURANCE AND RISK MANAGEMENT SERVICES TO DRIVE ADOPTION OF BLOCKCHAIN PLATFORMS

- 14.9.2 INSURANCE: BLOCKCHAIN APPLICATIONS

- 14.9.2.1 GRC management

- 14.9.2.2 Death & claims management

- 14.9.2.3 Payments

- 14.9.2.4 Identity management & fraud detection

- 14.9.2.5 Smart contracts

- 14.9.2.6 Other insurance applications

- 14.10 IT & TELECOM

- 14.10.1 NEED FOR PROTECTING SENSITIVE TELECOM DATA TO FUEL DEMAND FOR BLOCKCHAIN SOLUTIONS

- 14.10.2 IT & TELECOM: BLOCKCHAIN APPLICATIONS

- 14.10.2.1 OSS/BSS processes

- 14.10.2.2 Identity management

- 14.10.2.3 Payments

- 14.10.2.4 Smart contracts

- 14.10.2.5 Connectivity provisioning

- 14.10.2.6 Other IT & telecom applications

- 14.11 RETAIL & ECOMMERCE

- 14.11.1 AUTOMATION ACROSS RETAIL CHANNELS FOR CURBING DATA THEFT TO PROPEL GROWTH

- 14.11.2 RETAIL & ECOMMERCE: BLOCKCHAIN APPLICATIONS

- 14.11.2.1 Compliance management

- 14.11.2.2 Identity management

- 14.11.2.3 Loyalty & rewards management

- 14.11.2.4 Payments

- 14.11.2.5 Smart contracts

- 14.11.2.6 Supply chain management

- 14.11.2.7 Other retail & eCommerce applications

- 14.12 GOVERNMENT

- 14.12.1 RISE IN CONCERNS ABOUT IDENTITY THEFT, CYBERATTACKS, AND BUSINESS FRAUD TO DRIVE SEGMENT GROWTH

- 14.12.2 GOVERNMENT: BLOCKCHAIN APPLICATIONS

- 14.12.2.1 Asset registry

- 14.12.2.2 Identity management

- 14.12.2.3 Payments

- 14.12.2.4 Smart contracts

- 14.12.2.5 Voting

- 14.13 REAL ESTATE & CONSTRUCTION

- 14.13.1 TENANCY AGREEMENTS CREATED USING SMART CONTRACTS TO EASE PROCESS OF TRANSACTIONS BETWEEN PARTIES

- 14.13.2 REAL ESTATE & CONSTRUCTION: BLOCKCHAIN APPLICATIONS

- 14.13.2.1 Tokenization & asset management

- 14.13.2.2 Smart contracts

- 14.13.2.3 Other real estate & construction applications

- 14.14 OTHER VERTICALS

15 BLOCKCHAIN MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 NORTH AMERICA: BLOCKCHAIN MARKET DRIVERS

- 15.2.2 US

- 15.2.2.1 US strengthens blockchain ecosystem through regulatory and infrastructure expansion

- 15.2.3 CANADA

- 15.2.3.1 Canada accelerates blockchain development across industry, sustainability, and digital infrastructure

- 15.3 EUROPE

- 15.3.1 EUROPE: OPERATIONAL TECHNOLOGY SECURITY MARKET DRIVERS

- 15.3.2 UK

- 15.3.2.1 UK strengthens regulated blockchain ecosystem through financial innovation and enterprise adoption

- 15.3.3 GERMANY

- 15.3.3.1 Germany advances blockchain adoption with tokenized financial infrastructure

- 15.3.4 FRANCE

- 15.3.4.1 France drives blockchain growth through web3 innovation and wholesale CBDC initiatives

- 15.3.5 ITALY

- 15.3.5.1 Italy accelerates blockchain adoption through tokenized securities and DLT settlement

- 15.3.6 SPAIN

- 15.3.6.1 Spain strengthens blockchain innovation through fintech growth and digital asset adoption

- 15.3.7 SWITZERLAND

- 15.3.7.1 Switzerland strengthens blockchain leadership through crypto valley and tokenized finance

- 15.3.8 NETHERLANDS

- 15.3.8.1 Netherlands to strengthen blockchain adoption through digital asset innovation, enterprise integration, and financial sector modernization

- 15.3.9 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: BLOCKCHAIN MARKET DRIVERS

- 15.4.2 CHINA

- 15.4.2.1 China strengthens blockchain ecosystem through national data infrastructure and digital finance

- 15.4.3 JAPAN

- 15.4.3.1 Japan accelerates Web3 and blockchain innovation through digital infrastructure and Supply Chain 4.0 initiatives

- 15.4.4 AUSTRALIA

- 15.4.4.1 Australia reinforces blockchain adoption through next-generation settlement infrastructure

- 15.4.5 SINGAPORE

- 15.4.5.1 Singapore expands blockchain ecosystem through institutional DeFi and tokenized assets

- 15.4.6 INDIA

- 15.4.6.1 India accelerates blockchain adoption through digital public infrastructure and government-led innovation

- 15.4.7 SOUTH KOREA

- 15.4.7.1 South Korea advances blockchain leadership through security tokenization and digital assets

- 15.4.8 REST OF ASIA PACIFIC

- 15.5 MIDDLE EAST & AFRICA

- 15.5.1 MIDDLE EAST & AFRICA: BLOCKCHAIN MARKET DRIVERS

- 15.5.2 GULF COOPERATION COUNCIL (GCC)

- 15.5.2.1 Acceleration in blockchain adoption through digital finance and government modernization initiatives

- 15.5.2.2 KSA

- 15.5.2.2.1 Saudi Arabia accelerates blockchain growth through digital finance, infrastructure investment, and Vision 2030 initiatives

- 15.5.2.3 UAE

- 15.5.2.3.1 UAE accelerates blockchain-led digital economy expansion through tokenization, institutional investments, and smart government initiatives

- 15.5.2.4 Rest of GCC

- 15.5.3 SOUTH AFRICA

- 15.5.3.1 Surge in blockchain adoption through financial modernization, CBDC pilots, and public sector digitization initiatives

- 15.5.4 REST OF MIDDLE EAST & AFRICA

- 15.6 LATIN AMERICA

- 15.6.1 LATIN AMERICA: BLOCKCHAIN MARKET DRIVERS

- 15.6.2 BRAZIL

- 15.6.2.1 Expansion of blockchain adoption through digital identity systems, tokenization infrastructure, and financial innovation ecosystems

- 15.6.3 MEXICO

- 15.6.3.1 Regulatory modernization, remittance innovation, and financial ecosystem digitization to drive blockchain adoption

- 15.6.4 REST OF LATIN AMERICA

16 COMPETITIVE LANDSCAPE

- 16.1 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.2 REVENUE ANALYSIS

- 16.3 MARKET SHARE ANALYSIS

- 16.4 BRAND/PRODUCT COMPARISON

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.5.1 COMPANY VALUATION

- 16.5.2 FINANCIAL METRICS USING EV/EBIDTA

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS

- 16.6.5.1 Company footprint

- 16.6.5.2 Provider footprint

- 16.6.5.3 Service footprint

- 16.6.5.4 Vertical footprint

- 16.6.5.5 Regional footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.7.5.2.1 Provider footprint

- 16.7.5.2.2 Service footprint

- 16.7.5.2.3 Vertical footprint

- 16.7.5.2.4 Regional footprint

- 16.8 COMPANY EVALUATION MATRIX: BLOCKCHAIN HOSTING INFRASTRUCTURE MARKET (KEY PLAYERS), 2025

- 16.8.1 STARS

- 16.8.2 EMERGING LEADERS

- 16.8.3 PERVASIVE PLAYERS

- 16.8.4 PARTICIPANTS

- 16.9 COMPETITIVE SCENARIO AND TRENDS

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 AWS

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches/enhancements

- 17.1.1.3.2 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 IBM

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches/enhancements

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 ORACLE

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches/enhancements

- 17.1.3.3.2 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 HUAWEI

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 ACCENTURE

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses & competitive threats

- 17.1.6 OVHCLOUD

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product enhancements

- 17.1.6.3.2 Deals

- 17.1.6.3.3 Expansions

- 17.1.6.4 MnM view

- 17.1.6.4.1 Key strengths

- 17.1.6.4.2 Strategic choices

- 17.1.6.4.3 Weaknesses and competitive threats

- 17.1.7 TCS

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Deals

- 17.1.8 GOOGLE

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches/enhancements

- 17.1.8.3.2 Deals

- 17.1.9 ALIBABA

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Deals

- 17.1.10 MICROSOFT

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deals

- 17.1.11 SAP

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.12 HPE

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.13 HETZNER

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Expansions

- 17.1.14 TERASWITCH

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Solutions/Services offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Deals

- 17.1.1 AWS

- 17.2 OTHER KEY PLAYERS

- 17.2.1 TENCENT CLOUD

- 17.2.2 WIPRO

- 17.2.3 INFOSYS

- 17.2.4 LUMEN TECHNOLOGIES

- 17.2.5 DIGITALOCEAN

- 17.2.6 VMWARE

- 17.2.7 AKAMAI TECHNOLOGIES

- 17.2.8 APPLIED BLOCKCHAIN

- 17.2.9 CONSENSYS

- 17.2.10 CONTABO

- 17.2.11 LEEWAYHERTZ

- 17.2.12 VULTR

- 17.2.13 CLOUDSIGMA

- 17.2.14 MEVSPACE

- 17.2.15 SCALEWAY

- 17.2.16 KALEIDO

- 17.2.17 CHAINLINK LABS

- 17.2.18 ALCHEMY

- 17.2.19 BLOCKDAEMON

- 17.2.20 QUBETICS

- 17.2.21 COREWEAVE

- 17.2.22 T CLOUD PUBLIC

- 17.2.23 EXOSCALE

- 17.2.24 UPCLOUD

- 17.2.25 LATITUDE.SH

- 17.2.26 LIMESTONE NETWORKS

- 17.2.27 ALLNODES

- 17.2.28 CHERRY SERVERS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Breakup of primary profiles

- 18.1.2.2 Key industry insights

- 18.2 DATA TRIANGULATION

- 18.3 MARKET SIZE ESTIMATION

- 18.4 MARKET FORECAST

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 LIMITATIONS & RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS