|

시장보고서

상품코드

1923671

스마트 빌딩 부문 스타트업(2026년) : M&A 및 투자|AEC/O 라이프 사이클 전체의 디지털 트윈 및 AI 스타트업StartUps in Smart Buildings 2026: M&A & Investments | Digital Twin & AI Startups across the AEC/O Lifecycle |

||||||

스마트 빌딩 스타트업 생태계는 전환점에 도달했습니다. 벤처 캐피털의 자금 조달은 안정세를 보이는 반면, M&A 활동은 급증하여 2025년 한 해에만 98건의 스타트업 인수가 이루어졌습니다. 이는 2024년 대비 75% 증가한 수치로, 지난 10년간 최고 연간 총합입니다. 이러한 통합 움직임은 검증된 비즈니스 모델이 전략적 인수 기업의 주목을 받는 성숙한 시장을 시사합니다.

본 리포트는 스마트 빌딩 산업에 대한 조사 분석을 제공하며(2025년) 전체 자금 조달 라운드, 기업 투자자, M&A 활동, 기술 카테고리, AEC/O 라이프사이클 전반에 걸친 84개 디지털 트윈 및 AI 스타트업 목록이 포함된 스프레드시트와 고해상도 차트가 포함된 2개의 프레젠테이션 파일을 제공합니다. 본 리포트는 당사의 2026 엔터프라이즈 구독 서비스에 포함됩니다.

2026년에 이 조사가 중요한 이유

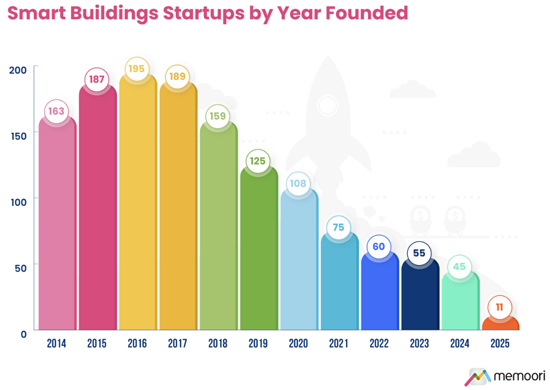

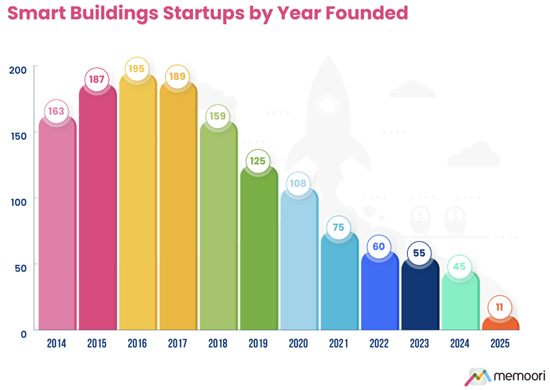

- 생태계는 성장 단계에서 통합 단계로 근본적으로 전환했습니다. 2025년 설립된 신규 스타트업은 단 11개사만 확인되었으며, 정점이었던 2016년 195개사에서 꾸준히 감소하고 있습니다.

- 그러나 스마트 빌딩 스타트업에 대한 자금 조달 활동은 그다지 줄지 않았습니다. 2025년에는 281건의 자금 조달 라운드를 통해 65억 달러에 달했으며, 라운드 수는 5% 감소한 반면 총액은 14% 감소했습니다.

- 또한 시드/시리즈 A 투자 평균 금액은 증가하고 있습니다. 투자자들은 더 선택적인 태도를 보이며 투자 건수는 감소하는 반면 건당 투자 금액은 확대되고 있습니다.

- 현재는 스타트업에게 어려운 환경입니다. 투자 유치 자체가 어려워졌으며, 투자자들은 확고한 기반과 명확한 수익원을 가진 기업을 우선시하고 있습니다. 주요 PropTech 벤처캐피털인 Fifth Wall은 최근 높은 금리와 트럼프 행정부의 기후 정책을 이유로 인원을 감축하고 활발한 자금 조달을 중단했습니다.

활발한 M&A 동향

2025년은 M&A 활동이 활발해진 해로, 2014년 이후 설립된 스타트업 98개사가 인수되었습니다. 이는 2024년 동기 대비 75% 증가한 수치입니다. 2014년 이후 스마트 상업용 건물 부문 스타트업 인수 건수는 누적 554건을 기록했습니다.

2025년에는 Vertiv의 Waylay NV 인수를 포함해 20건의 IoT 플랫폼 인수가 이루어졌습니다. 디지털 트윈 관련 거래로는 Oakglen Group의 Pupil(영국) 인수, Zutec의 Operance(영국) 인수 등이 있습니다.

2026년 전망

스마트 빌딩 부문의 스타트업 상황에는 다음과 같은 큰 변화가 예상됩니다.

- 시장 성숙에 따라 거래 건수는 감소하는 반면, 자금 조달 라운드는 대형화되고 전략적 참여가 더욱 활발해질 것으로 예상됩니다.

- 기존 기업들이 소수 주주 투자에서 인수 플랫폼 통합으로 전환함에 따라 업계 재편이 가속화될 것입니다.

- 전략적 인수 기업들은 AI로 강화된 디지털 빌딩 운영을 중심으로 포트폴리오 재구성을 지속할 것입니다.

This Report is the Definitive Resource for Evaluating Startups, Innovation, & Investment Trends in the Smart Building & PropTech Space 2026

The smart building startup ecosystem has reached an inflection point. While venture capital funding has moderated, M&A activity has exploded, with 98 startup acquisitions in 2025 alone, a 75% increase on 2024 and the highest annual total in the last decade. This consolidation signals a maturing market where proven business models are commanding attention from strategic buyers.

It is our 8th comprehensive evaluation of startups and scaleups in the operations and maintenance phase of the lifecycle of commercial real estate. It builds on our previous research into Grid-Interactive Buildings, HVAC Optimization, Artificial Intelligence, the Internet of Things, Video Surveillance, and Access Control.

The research includes a spreadsheet listing all 2025 funding rounds, corporate investors, M&A activity, technology categories, and 84 digital twin and AI startups across the AEC/O lifecycle, plus 2 presentation files with high-resolution charts. This report is included in our 2026 Enterprise Subscription Service.

Why This Research Matters in 2026?

- The ecosystem has fundamentally shifted from a growth phase to a consolidation phase. We identified only 11 new startups founded in 2025, and there has been a steady decline from the peak of 195 in 2016.

- BUT Funding Activity for smart building startups is not down that much. It reached $6.5 billion in 2025, spread across 281 funding rounds, a 5% decrease in the number of rounds, and a 14% decrease in total value.

- AND the average value of Seed and Series A investments has increased. Investors are being much more selective, making fewer but larger investments.

- What does this all mean? Currently, it is a tough environment for startups. Investment is harder to come by, and investors are prioritizing companies with solid fundamentals and clear revenue streams. Fifth Wall, a prominent PropTech VC, recently cut staff and stopped active fundraising, citing high interest rates and the Trump Administration's climate policies as factors in the decision.

Our definition of a startup is "a private company formed no earlier than 2014 that is focused on the commercial and industrial buildings market, is not a subsidiary or an acquisition of a larger company, and is generally financed by venture capital or private equity funding."

Intense M&A Activity

2025 saw an intense year of M&A activity, with 98 startups founded since 2014 acquired in 2025, representing a 75% increase compared to the same period in 2024. Since 2014, we have recorded 554 startup acquisitions in the smart commercial buildings sector.

There were 20 IoT platform acquisitions in 2025, including Vertiv's purchase of Waylay NV. Digital twin deals including Oakglen Group acquiring Pupil (UK) and Zutec purchasing Operance (UK).

NEW in 2026: Digital Twin & AI Startups Across the AEC/O Lifecycle

Part 2 of this report introduces expanded coverage of new companies applying digital twin and AI technologies across all stages of the building lifecycle, from architecture and design through engineering, construction, and operations.

84 companies are profiled in our comprehensive appendix, categorized by: Lifecycle stage (Architecture, Engineering, Construction, Operations), founding date and headquarters location, funding stage, and technology focus (52 AI-focused, 32 digital twin-focused). We profile 20 of these companies with an in-depth analysis of their offering, strategic focus, funding history, and market positioning.

2026 Outlook

We forecast significant shifts in the smart buildings startup landscape:

- Fewer deals, larger rounds, and heavier strategic participation as the market continues to mature.

- Consolidation will accelerate as incumbents move from minority investments to acquisitions and platform consolidation.

- Strategic buyers will continue repositioning portfolios around AI-enhanced digital building operations.

40 Startups Who Gained Traction in 2025

As part of this research, we also identified 40 startups that we believe gained market traction in 2025, selected based on organic growth, innovative business models, strategic investor interest, and headcount growth.

Who Should Buy This Report?

This research will be valuable to:

- Strategic acquirers seeking targets to expand technology portfolios.

- Building owners and operators assessing emerging technologies.

- Technology vendors who want to understand competitive positioning.

- Investors (VCs, PE firms, corporate VC arms) evaluating smart building opportunities.