|

시장보고서

상품코드

1435861

저GWP 냉매 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Low GWP Refrigerant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

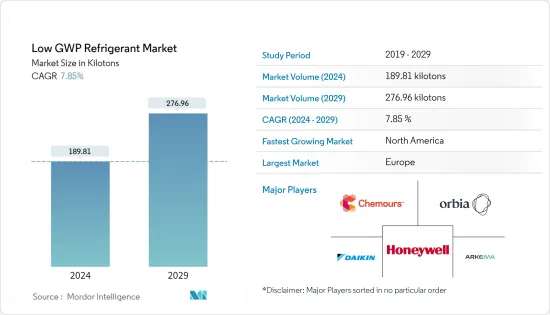

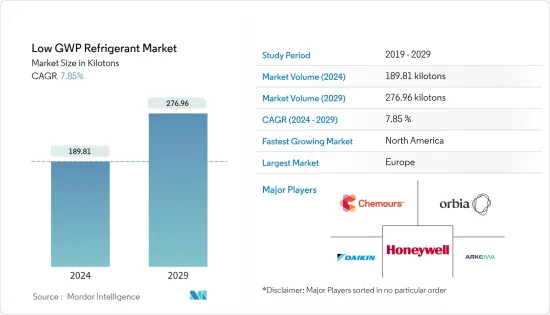

저GWP 냉매 시장 규모는 2024년에 18만 9,810톤으로 추정되고 2029년까지 27만 6,960톤에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 7.85%의 CAGR로 성장합니다.

저 GWP 냉매 시장은 신종 코로나바이러스 감염증(COVID-19) 팬데믹으로 인해 부정적인 영향을 받았습니다. 그러나 2021년에는 제약, 주거용, 상업용 등의 사용 증가로 인해 시장이 크게 회복되었습니다.

주요 하이라이트

- 환경에 미치는 영향이 적고 엄격한 규제가 중기적으로 저 GWP 냉매 시장 성장의 주요 원동력이 될 수 있습니다.

- 그러나 높은 가연성 및 기타 독성 특성으로 인해 저 GWP 냉매 시장의 성장은 제한적일 것으로 예상됩니다.

- 그럼에도 불구하고, 저 GWP 냉매를 촉진하기 위한 개발은 곧 세계 시장에서 유리한 성장 기회를 창출할 수 있습니다.

- 유럽이 가장 큰 시장이며, 가장 큰 소비국은 독일, 영국 등입니다.

저GWP 냉매 시장 동향

시장을 독식하는 상업용 냉동기

- 공조 및 냉동 분야에서 지구온난화지수(GWP)가 낮은 냉매 솔루션에 대한 수요가 증가하고 있습니다. 이러한 저 GWP 냉매는 에너지 소비를 증가시키고, 안전 위험을 초래하며, 장비의 대대적인 개조가 필요합니다.

- 또한 이들은 주로 HFC 및 CFC에 비해 서비스 장비의 에너지 소비와 탄소 배출량을 50% 감소시키는 데 주로 사용됩니다.

- 공조 및 냉동 분야에서 지구온난화지수(GWP)가 낮은 냉매 솔루션에 대한 수요가 증가하고 있습니다. 이러한 저 GWP 냉매는 에너지 소비를 증가시키고, 안전 위험을 초래하며, 장비의 대대적인 개조가 필요합니다.

- 저 GWP 냉매의 사용은 특히 유제품, 육류, 어업 및 효율적인 콜드체인 네트워크(상업용 냉동고 및 냉장고)에 의존하는 기타 식품 산업의 식품 안전을 포함하여 다양한 용도를 포함한 상업용 냉동 부문에서 증가하고 있습니다. 제약 산업 보존, 상업용 에어컨.

- 일본공조냉동협회가 2022년 6월에 발표한 자료에 따르면 2021년 세계 상업용 에어컨 수요가 크게 증가하여 1,488만 대에 달했습니다. 같은 해 북미가 총 737만 대를 기록해 전년도 실적을 웃돌며 1위를 차지했습니다.

- 하이얼 스마트홈에 따르면 아시아 에어컨 소매 판매량은 2022년 1억 3,230만 대에 달할 것이며, 2024년에는 1억 4,740만 대에 달할 것으로 추정됩니다.

- 또한 OEA(인도)에 따르면 에어컨 도매 가격 지수는 2022년 119.4에 도달했습니다.

- 냉동식품에 대한 수요가 증가하고 이익률이 낮은 경쟁이 치열한 시장에서 대부분의 식품 가공업체, 유통업체 및 소매업체는 수동으로 조작하는 구식 시설에서 상업용 냉장 설비가 널리 채택된 고층 냉동 창고로 전환하고 있습니다.

- 또한 다국적 기업의 소매 식품 체인의 확장과(무역 자유화로 인한) 국제 무역의 성장으로 인해 콜드체인 프로세스에 대한 수요가 증가하고 있습니다. 이로 인해 전 세계에서 상업용 냉동기에 대한 수요가 증가하고 있습니다.

독일, 유럽 시장을 제패

- 독일 경제는 유럽에서 가장 큰 경제 규모이며 세계 5위입니다. 독일은 특히 기계 및 자동차 분야에서 강력한 제조 부문을 보유하고 있습니다. 이를 통해 이 국가는 국제 무역에서 경쟁력을 유지하고 해외 투자를 유치할 수 있었습니다.

- 일본 공조냉동산업협회가 2022년 6월 발표한 데이터에 따르면 2021년 독일 상업용 에어컨 판매량이 크게 증가하여 수요가 5만 대에 달했습니다. 이러한 수요 급증은 전년 대비 눈에 띄는 증가를 보여주었습니다.

- 독일의 식품 및 음료 산업은 가장 큰 산업 분야입니다. 식품 가공은 국내 식품 및 음료 산업의 주요 활동 중 하나이며 냉장 보관이 크게 필요합니다. 이 국가의 식품 및 음료 수출 사업은 726억 유로(약 796억 달러)를 초과합니다.

- 국내에서 가공되는 주요 식품에는 육류 및 소시지 제품, 유제품, 구운 식품, 과자류 등이 포함됩니다. 이들 제품의 대부분은 유통기한을 연장하기 위해 냉장 보관이 필요하며, 이에 따라 냉장 수요가 더욱 증가하고 있습니다.

- 연방식품농업부(BMEL)에 따르면 독일의 1인당 육류 소비량은 2022년 77.5킬로그램에 달했습니다.

- 독일은 세계 최대 청량음료 소비국 중 하나로, 1인당 청량음료 소비량이 120리터를 넘습니다. 현재 독일 시장에서는 카페인이 함유된 음료가 가장 활발합니다. 이로 인해 스프라이트, 환타, 델타, 메조믹스, 코카콜라 등의 기업의 매출이 증가했습니다. 이러한 차가운 음료는 냉장 보관이 필요하기 때문에 냉장 수요가 크게 증가했습니다.

- 또한 더 나은 극저온 장비의 사용과 냉동식품에 대한 수요 증가로 인해 국내 저GWP 냉동 시장은 향후 수년간 성장률이 높아질 것으로 예상됩니다.

- 그러나 식품 가공 애프터마켓 수요가 크고, 향후 수년간 자동차 산업에서 냉매에 대한 수요가 증가할 것으로 예상됩니다.

저GWP 냉매 산업 개요

저 GWP 냉매 시장은 본질적으로 부분적으로 통합되어 있으며, 일부 기업은 조사 대상 시장의 작은 점유율을 차지하고 있습니다. 주요 기업으로는 Honeywell International Inc., The Chemours Company, Orbia, Arkema, DAIKIN INDUSTRIES, Ltd. 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 촉진요인

- 낮은 환경에 대한 영향

- 엄격한 규제

- 기타 촉진요인

- 억제요인

- 보다 높은 가연성 및 기타 독성 특성

- 기타 억제요인

- 업계의 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체품 및 서비스의 위협

- 경쟁의 정도

제5장 시장 세분화

- 유형

- 무기물

- 탄화수소

- 플루오로카본 및 플루오로 올레핀(HFC 및 HFO)

- 응용

- 상업용 냉장고

- 산업용 냉장고

- 가정용 냉장고

- 기타 용도

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 기타

- 아시아태평양

제6장 경쟁 구도

- 합병과 인수, 합병사업, 협업 및 계약

- 시장 순위 분석

- 유력 기업이 채택한 전략

- 기업 개요

- A-Gas

- Arkema

- DAIKIN INDUSTRIES, LTD.

- Danfoss

- engas Australasia

- GTS SPA

- HARP International

- Honeywell International Inc

- Linde

- Messer Group

- Orbia

- Tazzetti SpA

- The Chemours Company

제7장 시장 기회와 향후 동향

KSA 24.03.07The Low GWP Refrigerant Market size is estimated at 189.81 kilotons in 2024, and is expected to reach 276.96 kilotons by 2029, growing at a CAGR of 7.85% during the forecast period (2024-2029).

The low GWP refrigerant market was negatively impacted by the COVID-19 pandemic. However, the market recovered significantly in 2021, owing to rising applications in pharmaceuticals, residential, commercial, and others.

Key Highlights

- The low environmental impact and stringent regulations are likely to be the main driver of the low GWP refrigerant market's growth over the medium term.

- However, the higher flammability and other toxicity characteristics are expected to limit the growth of the low GWP refrigerant market.

- Nevertheless, developments for promoting low GWP refrigerants are likely to create lucrative growth opportunities for the global market soon.

- Europe represents the largest market,with the largest consumption coming from countries such as Germany,United Kingdom, etc.

Low GWP Refrigerant Market Trends

Commercial Refrigeration to Dominate the Market

- Low global warming potential (GWP) refrigerant solutions have been in greater demand for air conditioning and refrigeration applications. These low-GWP refrigerants increase energy consumption, introduces safety risks, and require significant equipment modifications.

- Moreover, these are primarily used to reduce service equipment energy consumption and carbon emissions by 50% compared to HFCs and CFCs.

- Low global warming potential (GWP) refrigerant solutions have been in greater demand for air conditioning and refrigeration applications. These low-GWP refrigerants increase energy consumption, introduces safety risks, and require significant equipment modifications.

- The usage of low GWP refrigerants is increasing, especially in the commercial refrigeration segment that includes varied applications, including food safety in dairy, meat, fisheries, and other food industries that rely on efficient cold chain networks (commercial freezers and refrigerators), cold chain preservation in the pharmaceutical industry, commercial air conditioners.

- Based on data published by the Air Conditioning and Refrigeration Association of Japan in June 2022, the worldwide demand for commercial air conditioners experienced a significant increase in 2021, reaching 14.88 million units. The North America region took the lead with a total of 7.37 million units in the same year, surpassing previous years figures.

- According to The Haier Smart Home, Asia's air-conditioners retail unit volume has reached 132.3 million units in 2022 and is estimated to reach 147.4 million units by 2024.

- Furthermore, according to OEA (India), the wholesale price index of air conditioners reached 119.4 in 2022.

- With the increasing demand for frozen food products and a highly competitive market with low margins, most food processors, distributors, and retailers are shifting from manually operated obsolete facilities to the high bay deep-freeze warehouses, where commercial refrigeration are widely employed.

- Moreover, the expansion of retail food chains by the multinational companies and the growth in international trade (due to trade liberalization) have led to an increase in the demand for the cold chain processes. This, in turn, is augmenting the demand for commercial refrigeration across the world.

Germany to Dominate the Europe Market

- The German economy is the largest in Europe and the fifth-largest in the world. Germany has a strong manufacturing sector, particularly in the areas of machinery and automotive. This has helped the country maintain a competitive edge in international trade and attract foreign investment.

- Based on the data published by the Association of Air Conditioning and Refrigeration Industry in Japan in June 2022, the sales of commercial air conditioning units in Germany experienced a significant increase in 2021, with the demand reaching 50 thousand units. This surge in demand marked a notable rise compared to previous years.

- The German food and beverage industry is the largest industry sector. Food processing is one of the major activities in the domestic food and beverage industry, which creates a significant need for refrigeration. The country's food and beverage export business exceeds more than EUR 72.6 billion (~USD 79.6 billion).

- Some of the major foods processed in the country include meat and sausage products, dairy products, baked goods, and confectionery. Most of these products need cold storage in order to increase their shelf life, further creating a demand for refrigeration.

- According to The Federal Ministry of Food and Agriculture( BMEL), Germany's per capita consumption of meat has reached 77.5 kilograms in 2022.

- Germany is one of the world's largest consumers of soft drinks with more than 120 liters of per-capita consumption. Caffeine-oriented drinks are the most dynamic in the present German market. This has given a boost to the sales of companies, such as Sprite, Fanta, Delta, Mezzo Mix, and Coca-Cola. The need for cold storage of these cold drinks has created a significant demand for refrigeration.

- Furthermore, with the use of better cryogenic equipment and the increased demand for frozen foods, the low GWP refrigeration market is poised to witness an increasing growth rate in the coming years in the country.

- However, there is significant demand from the food processing aftermarket, which is expected to increase the demand for refrigerants from the automotive industry in the coming years.

Low GWP Refrigerant Industry Overview

The low GWP refrigerants market is partially consolidated in nature, with players accounting for a marginal share of the market studied. A few major companies in the market (not in particular order) include Honeywell International Inc., The Chemours Company, Orbia, Arkema, and DAIKIN INDUSTRIES, Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Low Environmental Impact

- 4.1.2 Stringent Regulations

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Flammability and Other Toxicity Characteristics

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Inorganics

- 5.1.2 Hydrocarbons

- 5.1.3 Fluorocarbons and Fluoro-olefins (HFCs and HFOs)

- 5.2 Application

- 5.2.1 Commercial Refrigeration

- 5.2.2 Industrial Refrigeration

- 5.2.3 Domestic Refrigeration

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A-Gas

- 6.4.2 Arkema

- 6.4.3 DAIKIN INDUSTRIES, LTD.

- 6.4.4 Danfoss

- 6.4.5 engas Australasia

- 6.4.6 GTS SPA

- 6.4.7 HARP International

- 6.4.8 Honeywell International Inc

- 6.4.9 Linde

- 6.4.10 Messer Group

- 6.4.11 Orbia

- 6.4.12 Tazzetti S.p.A

- 6.4.13 The Chemours Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments for Promoting Low GWP Refrigerants

- 7.2 Other Opportunities