|

시장보고서

상품코드

1436022

심장 임플란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Cardiac Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

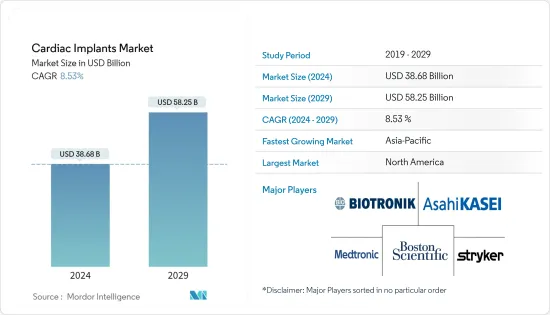

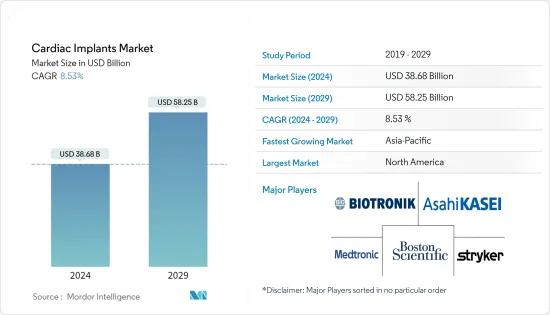

심장 임플란트 시장 규모는 2024년 386억 8,000만 달러로 추정되고, 2029년까지 582억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 8.53%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19의 발생은 심장 임플란트 장비 시장을 포함한 의료기기 산업의 모든 측면에 큰 영향을 미쳤습니다. 팬데믹 기간 동안 순환기과에서 응급 치료를 받았음에도 불구하고 환자의 방문 수는 크게 감소했습니다. 심지어 COVID-19 환자 가까이서 치료를 하는 것도 심장 전문의에게는 과제였습니다. 의료진이 COVID-19 환자의 치료에 참여했기 때문에 접근은 필수적인 치료로만 제한되었으며 심장병 센터의 일시 폐쇄로 심장 수술이 크게 감소했습니다. 메드트로닉 PLC와 같은 심장 임플란트 업계의 주요 기업은 2020년 4분기에 60억 달러의 수익 감소를 보고했습니다. 그러나 2022 회계연도의 수익은 2021 회계연도에 비해 16억 달러가 약간 증가했습니다. COVID-19의 팬데믹의 영향으로 2021 회계연도의 1분기와 2분기에 경험한 침체로부터 세계의 수술 건수가 회복했기 때문입니다. 따라서 COVID-19가 시장 성장에 미치는 영향은 팬데믹의 초기 단계에서는 악영향을 미쳤지만, 세계에서 수술과 치료가 재개되고 있기 때문에 가까운 미래 시장은 팬데믹 전 수준까지 견인력을 얻을 것으로 예상됩니다.

심혈관 질환의 발생률과 노인 인구 증가는 심장 임플란트 시장 성장 촉진요인이 되었습니다. 예를 들어 2022년 2월 발표된 미국 심장협회 보고서에 따르면 세계에서는 2020년 2억 4,410만 명이 허혈성 심장병(IHD)을 앓고 있는 것으로 추정되고 있으며, 여성보다 남성에서 더 유병률이 높아졌습니다(각각 1억 4,100만명, 1억 310만명). 마찬가지로 질병관리 예방센터의 2022년 6월 최신정보에 따르면 2020년 미국에서는 20세 이상의 성인 약 2,010만명이 관상동맥성 심질환(CAD)을 앓고 있었습니다. 또한 관상 동맥 심장 질환은 미국에서 가장 흔한 유형의 심장 질환이라고 말합니다. 당뇨병, 과체중 또는 비만, 건강에 해로운 식사, 운동 부족, 과도한 알코올 섭취가 심장 질환의 주요 원인이었습니다. 전 세계적으로 심장병의 빈도가 증가함에 따라 심장병을 앓고 있는 사람들은 심장 임플란트를 포함한 수술을 받아들이고 있는데, 이는 시장 성장을 가속하고 있습니다.

또한, 기술의 진보와 신제품의 승인과 출시는 조사 기간 동안 시장의 성장을 가속합니다. 예를 들어, 2020년 10월, 애봇은 비정상적인 심박 리듬과 심부전을 위한 새로운 이식형 제세동기(ICD)와 심장 재동기 치료 제세동기(CRT-D) 장치를 인도에서 출시했습니다.

그러므로 위의 요인들로 인해 시장은 향후 상당한 성장을 이룰 것으로 예상됩니다. 그러나 심장 임플란트의 높은 비용 및 심장 임플란트와 관련된 부작용은 시장 성장을 억제할 수 있는 요인의 일부입니다.

심장 임플란트 시장 동향

이식형 제세동기(ICD) 부문은 예측 기간 동안 더욱 빠르게 성장하고 시장을 독점할 것으로 예상됩니다.

이식형 제세동기(ICD)는 불규칙한 심박(부정맥)을 감지하고 정지하기 위해 흉부에 설치되는 배터리 구동 소형 장치입니다. 심박동을 지속적으로 모니터링하고 필요에 따라 충격을 주어 일정한 심박 리듬을 회복합니다. 이식형 제세동기(ICD) 부문은 심혈관 질환의 증례 증가와 기술적으로 선진적인 제품의 채용 증가 등의 요인에 의해 큰 성장이 예상되고 있습니다.

세계보건기구에 따르면 2020년에는 매년 1,790만명이 심혈관질환으로 사망하고 있는 것으로 추정되고 있으며, 이는 세계 전체 사망자 수의 32%를 차지하며, 그 중 85%는 심장발작과 뇌졸중 때문입니다. 그러나 개인에 미치는 영향을 최소화하기 위해 가능한 한 빨리 심혈관 질환을 탐지하는 것이 중요합니다.

게다가 2022년 6월에 발표된 「중국에서의 심방세동의 유병률과 리스크 : 국가횡단적역학연구」라는 제목의 2020년부터 2021년에 실시된 연구에 의하면, 심방세동의 유병률은 중국 성인 인구의 1.6%이며, 그 후 증가 경향에 있습니다. 노인 인구가 증가함에 따라 심장병의 유병률이 증가하며 심장 수술, 특히 심장 임플란트의 범위는 향후 몇 년동안 확대될 것으로 추정됩니다. 또한 2020년 1월 메드트로닉 plc는 이식형 제세동기(ICD)의 코발트 및 크롬 포트폴리오에 대해 CE(Conformite Europeenne) 마크를 획득했습니다.

따라서, 상기 요인을 고려하면, 이식형 제세동기(ICD) 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

북미가 시장을 독점하고 있으며 예측기간에도 비슷한 성장이 예상됩니다.

심장 임플란트 시장에서 북미는 주요 시장 점유율을 차지합니다. 질병관리 예방센터(CDC)의 최신 보고서 2022년에 따르면 미국에서 보고된 심장병으로 인한 사망자 수는 2019년에 65만 9,041명으로, 2020년에는 69만 882명으로 증가했습니다. 미국 질병 관리 예방 센터(CDC)는 심장 질환과 뇌졸중의 주요 위험 요소는 고혈압, 당뇨병, 높은 LDL(악마) 콜레스테롤, 흡연이라고 말합니다. 또한 위의 동일한 출처에 따르면 미국에서는 2030년까지 1,210만 명이 심방세동이 될 것으로 추정됩니다.

시장에서 활동하는 유명한 기업들이 신제품을 승인하고 출시하면 이 지역 시장 성장이 더욱 촉진될 것으로 예상됩니다. 예를 들어, 2022년 2월 애봇은 심부전을 겪고 살아가는 더 많은 사람들의 케어를 지원하기 위해 미국 식품의약국(FDA)으로부터 CardioMEMS HF 시스템의 적응 확대 승인을 받았습니다. CardioMEMS HF 시스템은 카테터를 사용하여 환자의 폐동맥에 내장된 종이 클립 크기 센서입니다. 또한, 2022년 4월, Abbot은 미국 식품의약국(FDA)으로부터 미국 심박 리듬이 느린 환자의 치료를 위한 Aveir 단강(VR) 리드레스페이스메이커의 승인을 받았습니다.

따라서 위의 요인과 새로운 승인 및 출시로 북미는 예측기간 동안 시장이 크게 성장할 것으로 예상됩니다.

심장 임플란트 산업 개요

심장 임플란트 시장은 본질적으로 전 세계의 유명한 기업에 의해 통합됩니다. 시장 점유율의 점에서 현재, 몇몇 대기업은 시장을 독점하고 있습니다. 심장 임플란트 기업은 기술적으로 첨단 솔루션을 환자에게 제공하기 위한 신제품 개발에 더욱 주력하고 있으며, 주요 기업 간의 경쟁이 치열해지고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 심혈관 질환의 발생률 증가

- 움직이지 않는 라이프스타일 채용 증가 및 노인 인구 증가

- 상환에 관한 정부의 유리한 정책

- 시장 성장 억제요인

- 심장 임플란트의 고액의 비용

- 심장 임플란트에 의한 부작용

- 업계의 매력-Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 제품별

- 이식형 제세동기(ICD)

- 페이스메이커

- 관상동맥 스텐트

- 이식형 심박 리듬 모니터

- 이식형 혈행동태 모니터

- 기타

- 용도별

- 부정맥

- 급성 심근경색

- 심근 허혈

- 기타

- 최종 사용자별

- 병원

- 순환기 센터

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Medtronic

- Boston Scientific Corporation

- Stryker(Physio-Control Inc.)

- Biotronik

- Asahi Kasei Corporation(ZOLL Medical Corporation)

- Pacetronix.com

- Schiller AG

- Koninklijke Philips NV

- LivaNova PLC

- Abbott.

- Impulse Dynamics

- Angel Medical Systems, Inc.

제7장 시장 기회 및 미래 동향

AJY 24.03.08The Cardiac Implants Market size is estimated at USD 38.68 billion in 2024, and is expected to reach USD 58.25 billion by 2029, growing at a CAGR of 8.53% during the forecast period (2024-2029).

The COVID-19 outbreak greatly impacted every aspect of the medical device industry, including the cardiac implants devices market. The number of patient visits during the pandemic was drastically reduced, despite having access to emergency care in the cardiology department. Even the treatment proximity to infected patients with COVID-19 was a challenge for cardiologists. Access was restricted to essential care only, and the temporary closure of cardiology centers considerably reduced cardiac surgeries, as the healthcare providers were engaged with COVID-19 patients. Major players in the cardiac implant industry, such as Medtronic PLC, reported a decline in revenue of 6 billion USD in Q4 2020. But the revenue was slightly increased by 1.6 billion USD in the fiscal year 2022 compared with the fiscal year 2021. This was due to the recovery of global procedure volumes from the downturn experienced in the first and second quarters of the fiscal year 2021 as a result of the COVID-19 pandemic. Hence, the impact of COVID-19 on the market's growth was adverse in the initial phase of the outbreak, however, as surgeries and treatments have resumed worldwide, the market is anticipated to gain traction to its pre-pandemic levels in the near future.

The increase in the incidence of cardiovascular diseases and the geriatric population are the driving factors for the cardiac implants market. For instance, as per the report of the American Heart Association published in February 2022, globally, it was estimated that in 2020, 244.1 million people had ischemic heart disease (IHD), and it was more prevalent in males than in females (141.0 and 103.1 million people, respectively). Likewise, according to the Centers for Disease Control and Prevention, in June 2022 update, about 20.1 million adults aged 20 and older had coronary heart disease (CAD) in 2020 in the United States. It also stated that coronary heart disease is the most common type of heart disease in the United States. Diabetes, overweight or obesity, an unhealthy diet, physical inactivity, and excessive alcohol use were the main causes of heart disease. As a result of the increasing frequency of heart illnesses worldwide, people who are affected by them are increasingly embracing surgical procedures, including cardiac implants, which is fueling the market's growth.

In addition, advancements in technology and new product approvals and launches drive the market's growth during the study period. For instance, in October 2020, Abbott launched its new implantable cardioverter defibrillator (ICD) and cardiac resynchronization therapy defibrillator (CRT-D) devices in India for abnormal heart rhythms and heart failure.

Hence, owing to the factors mentioned above, the market is expected to witness significant growth in the future. However, the high cost of cardiac implants and the side effects associated with cardiac implants are some of the factors that may restrain the market's growth.

Cardiac Implants Market Trends

Implantable Cardioverter-Defibrillators (ICDs) Segment is Expected to Grow Faster and Dominate the Market Over the Forecast Period

An implantable cardioverter-defibrillator (ICD) is a small battery-powered device placed in the chest to detect and stop irregular heartbeats (arrhythmias). It continuously monitors the heartbeat and delivers electric shocks, when needed, to restore a regular heart rhythm. The implantable cardioverter-defibrillators (ICDs) segment is expected to witness significant growth owing to factors such as increasing cases of cardiovascular diseases and increasing adoption of technologically advanced products.

According to the World Health Organization, in 2020, it is estimated that 17.9 million people die from cardiovascular diseases each year, which is 32% of all global deaths, of which 85% were due to heart attack and stroke. However, it is important to detect cardiovascular diseases as early as possible to minimize their effect on individuals.

Furthermore, as per the study conducted from 2020 to 2021 titled "Prevalence and risk of atrial fibrillation in China: A national cross-sectional epidemiological study" published in June 2022, the prevalence of atrial fibrillation was 1.6% in the Chinese adult population and increased with age. By considering the increase in the prevalence of heart diseases with an increase in the geriatric population, the scope for heart procedures, especially cardiac implants, is estimated to grow over the coming years. Moreover, in January 2020, Medtronic plc received the CE (Conformite Europeenne) mark for its Cobalt and Crome portfolio of implantable cardioverter-defibrillators (ICD).

Thus, considering the abovementioned factors, the implantable cardioverter-defibrillators (ICDs) segment is expected to grow over the forecast period.

North America Dominates the Market and is Expected to do Same in the Forecast Period

North America holds the major market share in the cardiac implants market. According to the Centers for Disease Control and Prevention (CDC) updated report 2022, the number of deaths reported due to heart diseases was 659,041 in 2019 and increased to 690,882 in 2020 in the United States. The Centers for Disease Control and Prevention (CDC) stated that the key risk factors for heart disease and stroke are high blood pressure, diabetes, high LDL (bad) cholesterol, and smoking. Also, according to the same above-mentioned source, it is estimated that 12.1 million people in the United States will have atrial fibrillation by 2030. Thus, an increase in the prevalence of cardiovascular diseases will have a positive impact on the usage of cardiac implants and drive the market growth.

New product approvals and launches by the prominent players operating in the market are anticipated to further boost the market's growth in the region. For instance, in February 2022, Abbott received expanded indication approval for the CardioMEMS HF System from the United States Food and Drug Administration (FDA) to support the care of more people living with heart failure. The CardioMEMS HF System is a paperclip-sized sensor implanted in a patient's pulmonary artery using a catheter. Also, in April 2022, Abbott received approval from the United States Food and Drug Administration (FDA) for the Aveir single-chamber (VR) leadless pacemaker for the treatment of patients in the United States with slow heart rhythms.

Hence, due to the factors mentioned above and new approvals and launches, North America is expected to witness significant growth in the market over the forecast period.

Cardiac Implants Industry Overview

The cardiac implants market is consolidated in nature with prominent players across the world. In terms of market share, a few of the major players currently dominate the market. The cardiac implant companies are focusing more on new product development to provide technologically advanced solutions to patients, which is boosting the competition among the key players. Some of the major players in the market are Medtronic, Boston Scientific Corporation, Stryker (Physio-Control Inc.), Biotronik, Asahi Kasei Corporation (ZOLL Medical Corporation), Pacetronix.com, Schiller AG, Koninklijke Philips NV, LivaNova PLC, Abbott, Impulse Dynamics, and Angel Medical Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Cardiovascular Diseases

- 4.2.2 Increase in Adoption of Torpid Lifestyle and Rising Incidence of Geriatric Population

- 4.2.3 Favourable Government Policies for Reimbursement

- 4.3 Market Restraints

- 4.3.1 High Cost of Cardiac Implants

- 4.3.2 Side Effects due to Cardiac Implants

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Implantable Cardioverter-defibrillators (ICDs)

- 5.1.2 Pacemakers

- 5.1.3 Coronary Stents

- 5.1.4 Implantable Heart Rhythm Monitors

- 5.1.5 Implantable Hemodynamic Monitors

- 5.1.6 Other Products

- 5.2 By Application

- 5.2.1 Arrhythmias

- 5.2.2 Acute Myocardial Infarction

- 5.2.3 Myocardial Ischemia

- 5.2.4 Other Applications

- 5.3 By End Users

- 5.3.1 Hospitals

- 5.3.2 Cardiology Centers

- 5.3.3 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Stryker (Physio-Control Inc.)

- 6.1.4 Biotronik

- 6.1.5 Asahi Kasei Corporation (ZOLL Medical Corporation)

- 6.1.6 Pacetronix.com

- 6.1.7 Schiller AG

- 6.1.8 Koninklijke Philips N.V.

- 6.1.9 LivaNova PLC

- 6.1.10 Abbott.

- 6.1.11 Impulse Dynamics

- 6.1.12 Angel Medical Systems, Inc.