|

시장보고서

상품코드

1536962

세계 소방용 항공기 시장 - 점유율 분석, 산업 동향, 성장 예측(2024-2029년)Firefighting Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

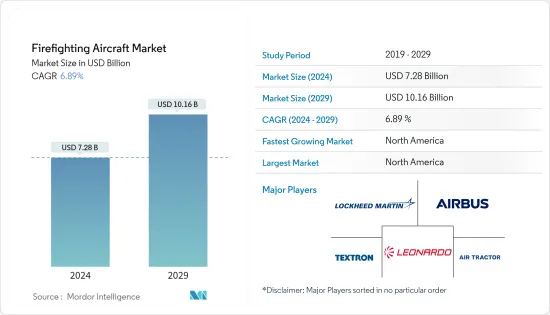

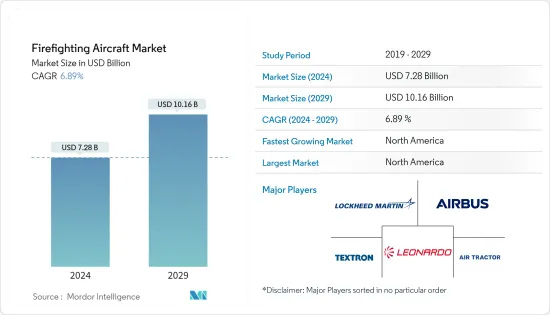

소방용 항공기 시장 규모는 2024년에 72억 8,000만 달러로 추정·예측되고, 2029년에는 101억 6,000만 달러에 이르고, 예측 기간(2024-2029년)의 CAGR은 6.89%로 성장할 것으로 예측됩니다.

소방용 항공기는 액체 저장용 대형 용기가 필요합니다. 여기에는 항공기의 홀드 영역에 있는 탱크, 외부 탱크 또는 그 조합이 포함됩니다. 탱크는 물과 다른 소화제를 저장하는 데 도움이되며 항공기에서 던져 소화에 사용됩니다. 세계의 산불의 심각화와 빈도 증가에 의해 적재량과 운용 범위의 확대라는 점에서 소방용 항공기의 기술적 진보에 대한 수요가 높아지고 있습니다.

기술의 진보에는 적재량 증가, 운용 범위의 확대, 소화제의 전개 정밀도의 향상 등이 포함됩니다. 산불 관리와 공중 소방대에 대한 정부의 투자가 시장을 견인하고 있습니다. 널리 사용되는 소방 항공기에는 Boeing B747, McDonnell Douglas DC-10, BAe146 등이 있습니다.

시장의 성장을 방해하는 것은 운항 비용의 높이, 항공 안전을 위한 엄격한 규제 기준, 소화 활동에 사용되는 화학물질에 대한 환경 문제 등의 과제입니다. 운항 비용의 높이는 소방용 항공기 시장이 직면하는 심각한 과제의 하나이며, 주로 연료비의 상승, 유지 보수 비용, 특수 장비의 필요성 등이 원인이 되고 있습니다.

소방용 항공기 시장 동향

예측기간 동안 회전익기 부문이 시장을 독점

소방 임무는 비용 효과와 적합성에 따라 다양한 헬리콥터를 선택합니다. 고정날개기에 비해 회전날개기는 물이나 소화제의 운반량이 적고 소방관이나 장비의 수송량도 적습니다. 헬리콥터는 소규모 산 불에 대한 빠른 초기 공격에 도움이 됩니다. 새로운 기술 개발에 의해 운용 효율이 향상되어, 보다 안전하고 신뢰성이 높은 것이 되었습니다. 양력은 증가하고 첨단 물방울 강하 시스템과 강화된 비행 제어 시스템이 도입되어 소화 임무에서의 효율성이 높아졌습니다. 게다가 고급 조정 기술과 통신 기술을 도입함으로써 공중에서의 활동과 지상에서의 활동을 보다 잘 통합할 수 있게 되어 전체적인 소화 전략의 향상이 확실해졌습니다.

다양한 국가에서 헬리콥터에 최신 내부 물 탱크를 탑재하여 헬리콥터를 소방관으로 개조하고 있습니다. 2023년 3월 United Rotorcraft는 긴급 구조, 소방 헬리콥터 프로그램에 대한 몇 가지 옵션과 현대화 평가를 시작했습니다. 업그레이드에는 이 회사가 Dart와 공동으로 개발한 1,000갤런 복합 물 탱크가 포함됩니다. 또한 2023년 11월, Leonardo는 Omni Helicopters International과 소방 능력을 강화하기 위해 AW189 및 A189 K 헬리콥터를 공급하는 계약을 체결했습니다. 이러한 고효율로 내구성이 높은 헬리콥터는 이 지역에서의 소방 임무의 운용 효율을 향상시킵니다. 이 계약은 소방 활동의 지속가능성과 신뢰성을 강조하는 OHI 헬리콥터스 국제 정책을 준수합니다.

예측 기간 동안 북미가 가장 높은 시장 점유율을 차지할 것으로 예측

예측 기간 동안 북미가 가장 높은 시장 점유율을 차지할 것으로 예측됩니다. 산불은 미국이나 캐나다 등 북미 국가에서 다발하고 있습니다. 산불의 원인은 낙뢰 등의 자연 현상에 의한 것, 전기 기기의 문제, 발연통의 미소화, 자동차의 과열, 방화 등의 인위적 행위에 의한 것이 있습니다. 미국 국가기관간 화재센터의 보고서에 따르면 2023년에는 약 55,571건의 산불사고가 발생했습니다. 마찬가지로 캐나다에서는 같은 해 1,650만 헥타르의 땅에서 6,132건의 산불이 발생했다고 보고되었습니다.

이 지역의 산 화재 대책 기관은 대형 에어 탱커(LAT), 싱글 엔진 에어 탱커(SEAT), 초대형 에어 탱커(VLAT), 훈제 점퍼, 워터 스쿠퍼 등 다양한 유형의 소화 항공기를 사용 하고 있습니다. 한마디로 높은 기술력, 강력한 정부지원, 산불이 많아지면서 이 지역의 세계소방시장에서의 최대 점유율을 뒷받침하고 있습니다. 이러한 이점은 항공기 기술의 지속적인 발전과 산불 관리의 효율성 향상을 목표로 하는 전략적 이니셔티브에 의해 지원됩니다.

예를 들어, 2024년 4월 서스캐처원 주 공공기관은 4대의 재사용 에어탱커 조달에 약 1억 8,700만 달러를 투자할 계획을 발표했습니다. 연방 정부는 이 투자를 지원하기 위해 1,600만 달러를 기부하고 있으며, 항공 소방대의 갱신과 현대화에 대한 헌신이 커지고 있음을 보여주고 있습니다.

소방용 항공기 산업 개요

소방용 항공기 시장은 통합되어 있으며 소수의 기업이 시장에서 큰 점유율을 차지하고 있습니다. 시장의 주요 기업으로는 Lockheed Martin Corporation, Airbus SE, Leonardo SpA, Textron Inc., and Air Tractor Inc 등이 있습니다. 주요 기업은 합작 투자와 파트너십 형성으로 전략적 움직임을 보이고 있습니다. 주요 OEM은 제휴를 통해 세계 시장에서의 존재를 확대하는 데 주력하고 있습니다. 예를 들어, 2024년 1월, Airbus(프랑스)와 Tata Group(인도)은 H125 헬리콥터의 최종 조립 라인을 위해 제휴했습니다. 이 제휴는 항공우주 산업에서 인도와 프랑스의 관계 강화를 강조합니다. 이러한 움직임은 항공기의 능력을 강화하고 세계 시장에서 주요 기업의 사업 전개 발자국을 늘릴 것입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자·소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 항공기의 유형

- 회전익기

- 고정익기

- 최대 이륙 중량

- 50,000kg 미만

- 50,000kg 이상

- 지역

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Lockheed Martin Corporation

- Viking Air Ltd

- ShinMaywa Industries Ltd

- MD Helicopters Inc.

- Textron Inc.

- Kaman Corporation

- Airbus SE

- Leonardo SpA

- Hynaero

- Air Tractor Inc.

- De Havilland Aircraft of Canada Limited

제7장 시장 기회와 앞으로의 동향

JHS 24.08.29The Firefighting Aircraft Market size is estimated at USD 7.28 billion in 2024, and is expected to reach USD 10.16 billion by 2029, growing at a CAGR of 6.89% during the forecast period (2024-2029).

Firefighting aircraft need large containers for liquid storage. These include tanks in the airplane hold area, external tanks, or a combination. The tank helps store water or any other retardant, which is used to extinguish the fire by dropping it from the aircraft. Increasingly, the higher severity and frequency of wildfires worldwide are driving the demand for technological advancements in firefighting aircraft in terms of increasing payload capacities and operational range.

Technological advances include increases in payload capacities, operational range, and accuracy of retardant deployment. Government investments in wildfire management and aerial firefighting fleets are driving the market. Some of the widely used firefighting aircraft are Boeing B747, McDonnell Douglas DC-10, and BAe 146 aerial firefighting aircraft.

The market's growth is hampered by challenges such as the high cost of operations, stringent regulatory standards for aviation safety, and environmental concerns over the chemicals used in fighting fires. The high cost of operations is among the severe challenges faced by the firefighting aircraft market, mainly attributed to higher fuel costs, maintenance costs, and specialized equipment requirements.

Firefighting Aircraft Market Trends

The Rotorcraft Segment will Dominate the Market During the Forecast Period

A wide range of helicopters are selected for firefighting missions based on cost-effectiveness and suitability. Compared to fixed-wing aircraft, rotorcrafts can carry less water or fire retardant and transport fewer firefighters and equipment. Helicopters are helpful for quick initial attacks on smaller wildfires. The new technological developments have improved operational efficiency and made them safer and more reliable. The lift capacity has increased, and advanced water drop systems and enhanced flight control systems have been installed to increase their effectiveness in firefighting missions. Furthermore, incorporating advanced coordination and communication technologies enables better integration of aerial efforts with ground operations, ensuring an improvement in overall firefighting strategies.

Various countries are converting helicopters into firefighters by installing modern internal water tanks. In March 2023, United Rotorcraft started evaluating several options and modernizations for the emergency rescue and firefighting helicopter program. The upgrades included a 1,000-gallon composite water tank, which the company developed in collaboration with Dart. Furthermore, in November 2023, Leonardo signed a contract with Omni Helicopters International to supply AW189 and A189 K helicopters to enhance firefighting capabilities. These high-efficiency, extended-endurance helicopters will improve the operational effectiveness of firefighting missions within the region. The deal aligns with OHI Helicopters International's focus on sustainability and reliability in firefighting operations.

North America Projected to Hold the Highest Market Share During the Forecast Period

North America is projected to hold the highest market share during the forecast period. Wildfires are prevalent in North American countries such as the United States and Canada. They may be caused by natural causes such as lightning or human activity, such as faulty electrical equipment, unextinguished smoking materials, overheating automobiles, or arson. The US National Interagency Fire Center report stated that around 55,571 wildfire incidents occurred in 2023. Similarly, Canada reported 6,132 incidents of wildfires that affected an area of 16.5 million hectares of land in the same year.

Wildfire control agencies in the region use different types of firefighting aircraft, such as Large Airtankers (LATs), Single Engine Airtankers (SEATs), Very Large Airtankers (VLATs), Smokejumpers, and Water Scoopers. In a nutshell, high technological capabilities, strong government support, and a high number of wildfires help the region account for the largest share of the global firefighting market. The dominance is supported by ongoing advancements in aircraft technology and strategic initiatives aimed at improving the effectiveness of wildfire management.

For instance, in April 2024, the Saskatchewan Public Agency announced plans to invest approximately USD 187 million in procuring four repurposed air tankers. The federal government has contributed USD 16 million to support the investment, which underlines a growing commitment to updating and modernizing aerial firefighting fleets.

Firefighting Aircraft Industry Overview

The firefighting aircraft market is consolidated, with a few players holding significant shares in the market. Some of the key players in the market are Lockheed Martin Corporation, Airbus SE, Leonardo SpA, Textron Inc., and Air Tractor Inc. Key players are making strategic moves by forming joint ventures and partnerships. The key OEMs are focusing on expanding their global market presence through alliances. For instance, in January 2024, Airbus (France) and Tata Group (India) partnered for a final assembly line for the H125 Helicopter. The partnership emphasizes strengthening ties between India and France in the aerospace industry. These moves will enhance aircraft capabilities and increase key players' operational footprint in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Driver

- 4.3 Market Restraint

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Rotorcraft

- 5.1.2 Fixed-wing

- 5.2 Maximum Take-off Weight

- 5.2.1 Below 50,000 kg

- 5.2.2 Above 50,000 kg

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 Viking Air Ltd

- 6.2.3 ShinMaywa Industries Ltd

- 6.2.4 MD Helicopters Inc.

- 6.2.5 Textron Inc.

- 6.2.6 Kaman Corporation

- 6.2.7 Airbus SE

- 6.2.8 Leonardo SpA

- 6.2.9 Hynaero

- 6.2.10 Air Tractor Inc.

- 6.2.11 De Havilland Aircraft of Canada Limited