|

시장보고서

상품코드

1537645

코히어런트 레이더 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Coherent Radar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

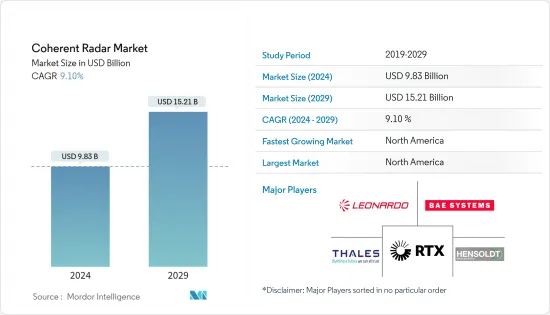

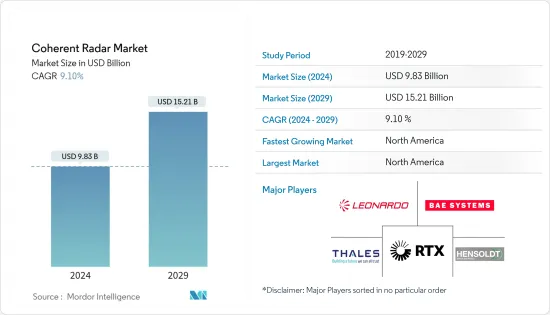

코히어런트 레이더의 시장 규모는 2024년 98억 3,000만 달러로 추정되며, 2029년에는 152억 1,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 9.10%의 CAGR로 성장할 것으로 예상됩니다.

코히어런트 레이더는 군사 분야에서 다양한 용도로 사용됩니다. 코히어런트 레이더는 고속으로 이동하는 스텔스 표적을 탐지하고 추적할 수 있으며, 지형과 물체의 고해상도 이미지를 제공할 수 있습니다. 중동, 아시아태평양 등 특정 지역의 테러와 지정학적 긴장이 고조됨에 따라 군사 분야에서 코히어런트 레이더에 대한 수요는 향후 몇 년 동안 증가할 것으로 예상됩니다. 이러한 요인으로 인해 모든 잠재적 위협을 탐지하기 위해 코히어런트 레이더와 같은 감시 기술의 현대화에 대한 국방 지출이 증가하고 있습니다.

전장의 급속한 디지털화는 적군에 대한 전술적 우위를 확보하기 위해 C4ISR 시스템의 채택을 촉진했습니다. 여기에는 코히어런트 레이더를 이용한 수동적 탐지 및 감시를 포함한 다양한 소스로부터의 데이터 동화가 포함되며, 이는 전장에서 이러한 시스템을 채택할 수 있는 기회를 창출하고 있습니다.

그러나 첨단 코히어런트 트레이더 시스템을 채택하는 것은 기술 선진국에 국한됩니다. 따라서 조달 및 연구개발 자금이 다른 분야로 전용될 경우 시장 성장에 부정적인 영향을 미칠 수 있습니다. 이러한 요인에도 불구하고 지정학적 긴장이 고조되고 세계 각국의 국방비 지출 증가로 인한 수요로 인해 예측 기간 동안 시장은 긍정적인 성장을 보일 것으로 예상됩니다.

고체 레이더 시스템의 개발 및 인공지능의 통합과 같은 레이더 기술의 지속적인 발전은 레이더 시스템의 성능과 효율성을 향상시킬 수 있기 때문에 이 시장의 성장을 촉진할 것으로 예상됩니다.

코히어런트 레이더 시장 동향

공중 코히어런트 레이더 분야가 가장 높은 성장률 기록

공중 코히어런트 레이더는 항공방위, 미사일 방어, 정보, 감시, 정찰(ISR) 등 군사 분야에서 다양한 용도로 활용되고 있습니다. 이에 따라 세계 각국은 첨단 EO/IR 시스템, 조기경보 시스템, 전천후 레이더 시스템을 탑재한 멀티롤 전투기 및 스텔스 전투기 개발 및 조달에 대한 군사비 지출을 크게 늘리고 있습니다.

세계 주요 국가의 군사비 증가와 다양한 현대화 노력으로 인해 이 부문의 성장이 증가할 것으로 예상됩니다. 예를 들어, 2022년 세계 군사비는 2조 2,400억 달러에 달해 2021년 대비 6% 성장할 것으로 예상됩니다. 이러한 국방비 증가에 따라 미국, 프랑스, 독일, 러시아, 영국, 일본 등 다양한 국가들이 스텔스 전투기 기술 개발에 박차를 가하고 있습니다. 예를 들어, 2022년 11월 프랑스, 독일, 스페인은 Future Combat Air System 프로그램에 따라 새로운 전투기 개발의 다음 단계를 시작하는 협정에 서명했습니다. 이 국방 프로젝트는 1,034억 달러 이상의 비용이 소요될 것으로 추정됩니다. 이 프로그램에 따라 이들 국가는 F-18과 타이푼과 같은 구식 전투기를 대체할 것으로 예상됩니다.

또한 2023년 12월 영국은 일본, 이탈리아와 함께 미래 전투 항공 계획의 일환으로 차세대 스텔스 전투기를 개발하기로 합의했습니다. 이 전투기는 초음속 능력을 갖추고 코히어런트 공중 레이더 등 군용기의 최신 기술을 탑재할 것으로 예상됩니다.

인도, 이스라엘, 터키 등 국가들도 ISR 전력을 강화하기 위해 무인항공기 개발 및 조달에 투자하고 있습니다. 예를 들어, 2023년 11월 인도는 IAI와 계약을 체결하여 비무장 무인항공기 Hermes 900 6대를 조달하여 감시 능력을 강화했습니다. 전반적으로 여러 국가의 방위군에 의한 스텔스 기술의 채택은 적의 방공망을 관통하여 조용히 표적을 감시하고 필요할 경우 무력화하기 위해 적의 방공망을 관통하기 위해 항공기에 일관된 레이더 시스템을 통합해야 합니다. 이 때문에 예측 기간 동안 이 부문의 수요를 촉진할 것으로 예상됩니다.

북미가 가장 높은 성장률을 보임

미국은 북미에서 코히어런트 레이더와 같은 첨단 레이더 기술의 열렬한 개발자이자 사용자입니다. 군사 분야의 이 시장 수요는 미국의 대규모 군사비 지출로 인해 코히어런트 레이더 기술을 포함한 다양한 레이더 기술의 개발 및 조달을 뒷받침하고 있습니다. 예를 들어, 2022년 미국 국방비는 8,770억 달러에 달해 2021년 대비 9% 성장했습니다. 기술적으로 진보된 무기에 대한 투자 증가는 전장에서 중국과 러시아의 역량 강화로 인한 위협이 증가함에 따라 이 요인으로 인해 미국 내 코히어런트 레이더 시스템에 대한 수요가 크게 증가하고 있습니다.

이러한 국방비 증가에 따라 미국은 국방력 강화를 위해 대형 군용기를 적극적으로 발주하고 있으며, 이는 미국 내 해당 시장의 수요를 증가시키고 있습니다. 예를 들어, 2022년 12월 현재 미군은 약 2,000대의 F-35A/B/C를 주문했습니다. 이러한 F-35를 위해 노스롭그루먼은 능동형 전자 스캐닝 어레이(AESA) 레이더를 공급하고 있으며, 이 AESA 레이더 시스템에는 각각 송수신 모듈을 가진 다수의 개별 방사 소자가 포함되어 있습니다. 이 모듈들은 서로 조화를 이루어 일관된 레이더 빔을 형성하여 잠재적인 공중 위협을 탐지합니다.

북미에는 첨단 상황 인식 능력 강화 시스템 개발에 지속적으로 투자하고 있는 주요 방산 기술 기업들이 있습니다. 예를 들어, Raven Industries Inc.는 하이포인터 100 코히어런트 레이더 시스템 솔루션으로 코히어런트 레이더 시장에 솔루션을 제공하는 OEM 중 하나입니다. 하이포인터 100은 다양한 유인 및 무인 플랫폼의 종합적인 상황 인식을 향상시키고 오경보를 최소화하여 최종사용자와 의사결정권자가 육상, 해상, 공중에서 역동적인 정보, 감시 및 정찰(ISR) 임무를 성공적으로 수행할 수 있도록 지원합니다. 성공할 수 있도록 지원합니다.

코히어런트 레이더 산업 개요

코히어런트 트레이더 시스템 시장은 HENSOLDT AG, RTX Corporation, BAE Systems PLC, Leonardo SpA, Thales 등 주요 기업들이 시장 점유율의 대부분을 차지하고 있습니다.

국방 분야의 엄격한 안전 및 규제 정책은 신규 진입을 제한할 것으로 예상됩니다. 적대적인 항공 플랫폼과 무기에 스텔스 기술이 도입되면서 시장 개발자들은 레이더 단면적이 작은 표적을 효과적으로 탐지할 수 있는 첨단 레이더 시스템 개발에 집중하고 있습니다. 최종사용자 국가와의 장기적인 파트너십을 보장하고 광범위한 군사 자산과의 통합을 용이하게 하기 위해 이들 기업은 최첨단 레이더 기술 개발에 자원을 투입하고 있습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자·소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 플랫폼별

- 항군

- 지상

- 해군

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 라틴아메리카

- 중동 및 아프리카

- 북미

제6장 경쟁 상황

- 벤더 시장 점유율

- 기업 개요

- HENSOLDT AG

- BAE Systems PLC

- IAI

- Leonardo SpA

- RTX Corporation

- Lockheed Martin Corporation

- Thales

- Saab AB

- L3 Harris Technologies Inc.

- Indra Sistemas SA

제7장 시장 기회와 향후 동향

ksm 24.08.29The Coherent Radar Market size is estimated at USD 9.83 billion in 2024, and is expected to reach USD 15.21 billion by 2029, growing at a CAGR of 9.10% during the forecast period (2024-2029).

Coherent radar has various applications in the military. It can detect and track fast-moving and stealthy targets and provide high-resolution images of the terrain and objects of interest. The demand for coherent radar in the military is expected to grow in the coming years due to the rise in terrorism and geopolitical tensions in certain regions like the Middle East and Asia-Pacific. This factor has led to a rise in defense expenditure on modernizing surveillance technology, such as coherent radar, to detect any potential threat.

The rapid digitization of the battlefield has fostered the adoption of C4ISR systems to gain a tactical edge over hostile forces. These include the assimilation of data from various sources, including passive detection and monitoring through the use of coherent radars, thereby creating an opportunity for adopting these systems on the battlefield.

However, adopting advanced coherent radar systems is limited to technologically advanced countries. Hence, the diversion of procurement and R&D funds toward other sectors can deleteriously affect market growth. Despite this factor, the market is expected to grow positively during the forecast period due to the demand driven by rising geopolitical tensions and increasing defense expenditures in various economies worldwide.

Continuous advancements in radar technologies, such as the development of solid-state radar systems and the integration of artificial intelligence, are expected to drive the growth of this market as these technological advancements enable improved performance and increased efficiency of radar systems.

Coherent Radar Market Trends

Airborne Coherent Radar Segment to Exhibit the Highest Growth Rate

Airborne coherent radar has various applications in the military, such as air and missile defense, intelligence, surveillance, and reconnaissance (ISR). Hence, various countries worldwide are significantly increasing their military spending in developing and procuring multirole and stealth fighter aircraft equipped with advanced EO/IR systems, early warning systems, and all-weather radar systems.

The growth of this segment is expected to increase due to rising military expenditure and various modernization efforts by major global powers. For instance, in 2022, the global military expenditure reached USD 2,240 billion, a growth of 6% from 2021. With this increased defense expenditure, various countries, such as the United States, France, Germany, Russia, the United Kingdom, and Japan, are currently working on the development of stealth fighter jet technology. For instance, in November 2022, France, Germany, and Spain signed an agreement to start the next phase of development of a new fighter jet under the Future Combat Air System program. The defense project is estimated to cost more than USD 103.4 billion. Under the program, these countries are expected to replace older fighter aircraft fleets such as the F-18 and Typhoon.

Similarly, in December 2023, the United Kingdom entered an agreement with Japan and Italy to create a next-generation stealth fighter as part of the future combat air program. The fighter is expected to have supersonic capabilities and be equipped with the latest technology in these military aircraft, such as coherent airborne radars.

Countries such as India, Israel, and Turkey are also investing in developing and procuring unmanned air vehicles to boost their ISR strength. For instance, in November 2023, India awarded a contract to IAI to procure six Hermes 900 unarmed drones to augment the country's surveillance capabilities. Overall, the adoption of stealth technology by the defense forces of several countries necessitates the integration of coherent radar systems on board the aircraft to silently monitor the target and penetrate enemy air defenses to neutralize them if the need arises. This is expected to drive the demand for this segment during the forecast period.

North America to Exhibit the Highest Growth Rate

The United States is an avid developer and user of sophisticated radar technologies such as coherent radar in North America. The demand for this market in the military is driven by the large military spending of the United States, which, in turn, supports the development and procurement of various radar technologies, including coherent radar technologies. For instance, in 2022, the US military defense expenditure rose to USD 877 billion, a growth of 9% compared to 2021. The increased investments toward technologically advanced weaponry are due to the growing threat to the country from the enhanced capabilities of China and Russia on the battlefield, and this factor is heavily driving the demand for coherent radar systems in the country.

With this increased defense spending, the United States is actively ordering huge military aircraft to enhance its defense capabilities, which is driving the demand for this market in the United States. For instance, as of December 2022, the US military had placed orders for around 2,000 F-35A/B/C aircraft variants. For these F-35s, Northrop Grumman provides its active electronically scanned array (AESA) radar, and these AESA radar systems involve numerous individual radiating elements, each with its own transmit and receive module. These modules work harmoniously to form a coherent radar beam to detect potential airborne threats.

North America is also home to leading defense technology firms that are constantly investing in developing advanced situational awareness enhancement systems. For instance, Raven Industries Inc. is one of the OEMs that provides its solutions in the coherent radar market with its HiPointer 100 coherent radar system solution. The company's HiPointer 100 increases persistent surveillance capabilities, enhances total situational awareness from a diverse set of manned and unmanned platforms with extremely low false alarms, and enables end users and decision-makers to achieve success in dynamic intelligence, surveillance, and reconnaissance (ISR) missions spanning land, sea, and air.

Coherent Radar Industry Overview

The coherent radar systems market is consolidated with leading players, such as HENSOLDT AG, RTX Corporation, BAE Systems PLC, Leonardo SpA, and Thales, accounting for a majority of the market share.

The stringent safety and regulatory policies in the defense segment are expected to restrict the entry of new players. With the growing implementation of stealth technologies in adversary aerial platforms and weapons, market players are focusing on the development of sophisticated radar systems that can effectively detect targets with lower radar cross-sections. To ensure long-term partnerships with end-user countries and easy integration with a broad spectrum of military assets, these companies are dedicating their resources to the development of cutting-edge radar technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Airborne

- 5.1.2 Terrestrial

- 5.1.3 Naval

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.4.1 Latin America

- 5.2.4.2 Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 HENSOLDT AG

- 6.2.2 BAE Systems PLC

- 6.2.3 IAI

- 6.2.4 Leonardo SpA

- 6.2.5 RTX Corporation

- 6.2.6 Lockheed Martin Corporation

- 6.2.7 Thales

- 6.2.8 Saab AB

- 6.2.9 L3 Harris Technologies Inc.

- 6.2.10 Indra Sistemas SA