|

시장보고서

상품코드

1906924

펄프 및 제지용 화학제품 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pulp And Paper Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

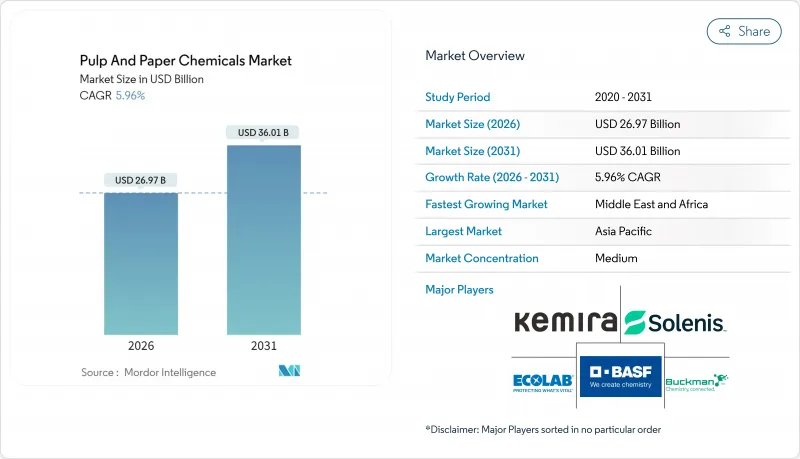

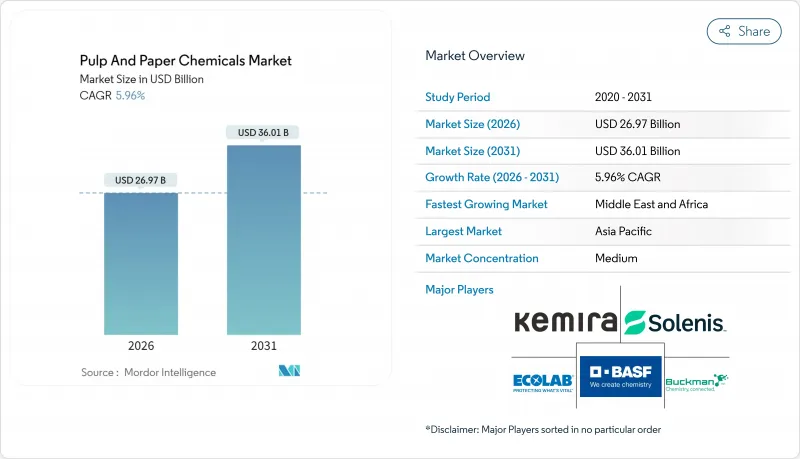

펄프 및 제지용 화학제품 시장은 2025년 254억 5,000만 달러에서 2026년에는 269억 7,000만 달러로 성장하여 2026년부터 2031년에 걸쳐 CAGR 5.96%를 나타낼 전망입니다. 2031년까지 360억 1,000만 달러에 이를 것으로 예상됩니다.

포장지 수요 증가, 표백·사이징 기술에 있어서 급속한 진보, 지속가능성에 대한 요구 강화가 더해져, 지속적인 성장의 추풍과 역풍이 태어나고 있습니다. 아시아태평양의 생산 능력 확대, 전자상거래의 지속적인 확대, 재생 섬유로의 현저한 전환이 휘도 향상, 강도 개선, 담수 사용량 삭감을 실현하는 특수 화학제품의 소비 증가에 기여하고 있습니다. 한편, 배출규제의 강화, 원료가격의 변동, 에너지 집약적인 종래 프로세스가 효소계·바이오베이스·폐쇄 루프 솔루션을 중심으로 한 기술 혁신을 공급업체에 육박하고 있습니다. 경쟁상의 차별화는 유지성, 배수성, 배리어 성능을 최적화하면서 제지 공장의 탄소 배출량, 배수 목표 달성을 지원하는 통합 프로그램에 달려 있습니다. 이를 위해 업계의 기존 기업은 가동 중지 시간과 화학 약품의 과도한 공급을 줄이는 대상을 좁힌 인수, 지역별 생산 거점, 디지털 서비스 모델에 주력하고 있습니다.

세계의 펄프 및 제지용 화학제품 시장 동향 및 인사이트

아시아의 포장용지 생산 능력 확대

그린베이 패키징사의 10억 달러 규모의 시설과 스자노사의 16억 6,000만 레알 투자 등 대규모 자본 프로젝트는 고속 기계용으로 특화된 유지 보조제, 배수 화학약품, 표면 사이징제에 대한 전례 없는 하류 수요를 일으키고 있습니다. 이 거대 제지 공장은 운송 비용 증가를 피하기 위해 현지 조달을 선호하고 있으며 공급업체는 지역 공장 및 서비스 실험실의 개발을 강요하고 있습니다. 생산 능력 증가는 세계의 섬유 수급 균형을 강조하고 간접적으로 수출 지향의 다른 지역 제지 공장에서 첨가제 소비를 촉진합니다. 기술 팀을 최종 사용자의 운영 시작 일정에 연동시키는 공급업체는 초기 단계 수요량과 장기 공급 계약을 획득할 수 있습니다. 마지막으로, 지역적 과잉생산 능력 위험이 증가함에 따라 비용 최적화 프로그램의 필요성을 강화하고 화학제품과 실시간 분석을 결합한 솔루션을 제공할 수 있는 공급업체가 유리합니다.

재생 섬유 원료의 채용 급증

순환형 경제의 요구와 브랜드 오너의 대처에 의해 특히 유럽과 북미에 있어서, 평균 재생 원료 함유율이 상승하고 있습니다. 2차 섬유에 포함되는 오염물질, 점착성 물질, 잉크 잔사 증가에 의해 제지 공장에서는 고도의 부선 약품, 효소 기반의 탈묵 처리, 휘도와 인장 강도를 유지하는 고전하 마이크로 입자의 채용이 진행되고 있습니다. 통합된 "전체 라인" 화학제품 패키지는 조달을 단순화하고, 데이터 풍부한 모니터링은 첨가제의 과다 투여를 감소시킵니다. 100% 재생 원료를 채용하는 골판지 원지 공장이나 티슈 공장에 있어서, 기회는 가장 급속하게 확대하고 있습니다.

AOX 및 COD 배출 기준 엄격화

EU 및 미국의 규제 당국은 허용되는 AOX(산성 유기물질) 및 COD(화학적 산소 요구량)의 기준치를 낮추고 있으며, 제지 공장은 표백 공정의 재설계와 고자본 비용을 수반하는 3차 처리 설비의 도입을 강요하고 있습니다. 규모의 경제성이 부족한 소규모 공장에서는 컴플라이언스 대응으로 연간 운영 비용이 15-20% 증가합니다. 화학제품 공급업체는 저 AOX 형광 증백제, 슬러지 탈수 보조제, 감사 대응에 유효한 성능 증명이 가능한 온라인 센서 등으로 대응하고 있습니다.

부문 분석

표백제는 펄프 및 제지용 화학제품 시장을 독점해 2025년에는 32.45%의 점유율을 차지했습니다. 이 부문의 이점은 백도 목표 달성에 필수적인 역할과 이산화 염소에서 과산화수소 및 산소 시스템으로의 전환이 진행되고 있기 때문입니다. 이러한 전환은 AOX 규제 강화와 염소계 잔류물에 대한 소비자 모니터링 강화에 의해 뒷받침됩니다. 공급업체는 화학적 산소 요구량(COD)을 줄이는 안정화된 과산화물 등급, 고효율 활성화제 및 분산제에 대한 투자를 추진하고 있습니다.

사이즈제는 절대적인 금액 규모에서는 작은 것, 2031년까지 연평균 복합 성장률(CAGR) 6.31%를 나타내 가장 급속하게 성장하는 부문입니다. 바이오기반 및 효소계 사이즈제는 푸드서비스 및 전자상거래용 포장에 필요한 잉크 유지성, 내유성, 탄소 삭감의 밸런스를 컨버터에 제공합니다. 펄프화 화학제품은 통합 공예 공장에 연동된 안정적인 기반을 유지합니다. 한편, GCC나 PCC 등의 충전제는 그램당 높은 불투명도를 요구하는 경량화 동향의 혜택을 받고 있습니다. 바인더, 특히 재생 티슈 및 수건 등급에 사용되는 습윤 강도 수지는 위생 제품 수요가 견조하게 추이하고 있기 때문에 완만한 성장을 보여줍니다.

지역별 분석

아시아태평양은 견조한 설비 투자와 1인당 포장 소비량 증가에 견인되어 2025년 펄프 및 제지용 화학제품 시장에서 46.85%의 점유율을 차지했습니다. 중국의 최근 5개년 계획은 컨테이너 보드와 특수 조직을 전략적 부문으로 자리매김하여 에너지 절약형 화학제품 패키지에 대한 보조금을 촉진하고 있습니다. 인도의 티슈 붐은 소프트 강도 수지와 향료 배합 기술 수요를 가속화하고 있습니다. 동남아시아는 공급망의 다양화의 혜택을 누리고 있으며 베트남과 인도네시아는 공예 라이너 공장에 외국 투자를 유치하고 있습니다.

북미에서는 경량화 컨테이너 보드로의 전환이나 캘리포니아주 등에서의 재생 섬유 사용 의무화의 진전을 배경으로 안정된 수요가 계속되고 있습니다. 제지공장에서는 기업의 넷 제로 목표에 따라 산소 탈리그닌화 설비의 개수와 이산화탄소 포집 파일럿 프로젝트에 대한 투자가 진행되고 있습니다. 유럽에서는 그린딜 및 엄격한 포장 지침을 배경으로 바이오 베이스 사이즈제나 PFAS 프리 배리어 코팅의 채용이 선행하고 있습니다.

중동 및 아프리카는 인프라 정비와 식품 및 음료 포장의 현지화를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 6.05%를 나타낼 것으로 전망됩니다. 사우디아라비아와 이집트에서 새로운 조직 제조 기계의 가동은 첨가제 수요를 견인하는 반면, 오만의 소할 석유 화학 투자는 지방산 유도체의 지역 조달을 강화합니다. 남미에서는 브라질의 펄프 생산 능력 확대를 기반으로 안정된 성장이 예상되고, 화학제품 공급업체는 목재 유래 원료 확보를 위해 업스트림 공정에 통합을 진행하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아의 포장용지 생산능력 확대

- 재생 섬유 원료의 채용 급증

- 무수 효소 표백 기술의 혁신

- 카본 네거티브형 바이오 베이스 사이징제

- 전자상거래 주도의 SKU 증가가 특수화학제품을 견인

- 시장 성장 억제요인

- AOX 및 COD 배출 기준의 엄격화

- 대체 기질에 비해 높은 에너지 집약도

- 염소 단체의 가격 변동성

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 바인더

- 표백제

- 충전제

- 펄프 제조용 화학제품

- 사이징제

- 기타 유형

- 용도별

- 신문 용지

- 포장 및 산업용지

- 인쇄 및 필기용지

- 펄프 공장 및 수처리

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 인도네시아

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율/순위 분석

- 기업 프로파일

- Arkema

- Ashland Inc.

- BASF

- Buckman

- Cargill Incorporated

- Celanese

- Chemours

- Clariant

- Ecolab

- ERCO Worldwide

- Georgia-Pacific

- Imerys SA

- Kemira

- Nouryon

- Omya International AG

- Solenis

- Solvay

- Stora Enso

- UPM

- Valmet

제7장 시장 기회와 향후 전망

KTH 26.01.20The Pulp & Paper Chemicals market is expected to grow from USD 25.45 billion in 2025 to USD 26.97 billion in 2026 and is forecast to reach USD 36.01 billion by 2031 at 5.96% CAGR over 2026-2031.

The rising demand for packaging-grade paper, rapid technological upgrades in bleaching and sizing, and intensifying sustainability mandates are combining to create persistent growth headwinds and tailwinds. Capacity additions in the Asia-Pacific region, continued e-commerce expansion, and a pronounced shift toward recycled fiber have all contributed to an increase in the consumption of specialty chemistries that enhance brightness, improve strength, and reduce freshwater use. At the same time, tightening discharge rules, volatile input prices, and energy-intensive legacy processes compel suppliers to innovate around enzymatic, bio-based, and closed-loop solutions. Competitive differentiation hinges on bundled programs that optimize retention, drainage, and barrier performance while helping mills meet carbon and effluent targets. Industry incumbents, therefore, focus on targeted acquisitions, regional production footprints, and digital service models that reduce downtime and chemical over-feed.

Global Pulp And Paper Chemicals Market Trends and Insights

Expansion of Packaging-Grade Paper Capacity in Asia

Massive capital projects such as Green Bay Packaging's USD 1 billion facility and Suzano's R$1.66 billion investment have triggered unprecedented downstream demand for retention aids, drainage chemistries, and surface sizing tailored for high-speed machines. These mega-mills prefer local chemical sourcing to avoid freight penalties, prompting suppliers to deploy regional plants and service labs. Capacity additions also tighten global fiber balances, indirectly boosting additive consumption in export-oriented mills elsewhere. Suppliers that align technical teams with end-user start-up schedules capture early-cycle volume and long-term supply contracts. Finally, regional overcapacity risks heighten the need for cost-optimizing programs, favoring vendors that can bundle chemistries with real-time analytics.

Surge in Recycled-Fiber Furnish Adoption

Circular-economy mandates and brand owner commitments push average recycled-content ratios higher, especially in Europe and North America. Increased contaminants, stickies, and ink residues in secondary fiber prompt mills to employ advanced flotation reagents, enzyme-based de-inking, and high-charge microparticles that preserve brightness and tensile strength. Integrated "full-line" chemical packages simplify procurement, while data-rich monitoring cuts additive overdosing. Opportunities grow fastest in containerboard and tissue mills adopting 100% recycled furnish.

Tightening AOX and COD Discharge Norms

EU and US regulators are lowering allowable AOX and COD baselines, compelling mills to redesign bleach sequences or install high-capex tertiary treatment. Compliance adds 15-20% to annual operating costs for smaller sites that lack economies of scale. Chemical suppliers respond with low-AOX brightening agents, sludge de-watering aids, and online sensors that prove performance to auditors.

Other drivers and restraints analyzed in the detailed report include:

- Water-Free Enzymatic Bleaching Breakthroughs

- Carbon-Negative Bio-Based Sizing Agents

- High Energy Intensity Vis-a-Vis Alternative Substrates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bleaching agents dominated the pulp and paper chemicals market, accounting for a 32.45% share in 2025. The segment's primacy stems from its indispensable role in brightness targets and its ongoing migration from chlorine dioxide toward hydrogen peroxide and oxygen sequences. This shift is reinforced by regulatory curbs on AOX and consumer scrutiny of chlorinated residues. Suppliers invest in stabilized peroxide grades, high-efficacy activators, and dispersants that lower total chemical oxygen demand.

Sizing agents, although smaller in absolute dollar terms, represent the fastest-growing segment with a 6.31% CAGR through 2031. Bio-based and enzymatic sizing gives converters the balance of ink hold-out, grease resistance, and carbon reduction they need for food-service and e-commerce packaging. Pulping chemicals maintain a steady baseline tied to integrated kraft mills, while fillers such as GCC and PCC benefit from lightweighting trends that call for higher opacity per gram. Binders, particularly wet-strength resins used in recycled tissue and towel grades, show moderate gains as hygiene product demand remains defensive.

The Pulp and Paper Chemicals Market Report is Segmented by Type (Binders, Bleaching Agents, Fillers, Pulping Chemicals, Sizing Agents, and More), Application (Newsprint, Packaging and Industrial Papers, Printing and Writing Papers, Pulp Mills and Water Treatment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region commanded a 46.85% share of the pulp and paper chemicals market in 2025, driven by robust capital investment and rising per-capita packaging consumption. China's latest five-year plan earmarks containerboard and specialty tissue as strategic segments, spurring subsidies for energy-efficient chemical packages. India's tissue boom intensifies demand for soft-strength resins and fragrance-incorporation technologies. Southeast Asia benefits from supply-chain diversification, with Vietnam and Indonesia courting foreign investment for kraft liner mills.

North America registers stable demand grounded in lightweight containerboard conversions and progressive recycled-fiber mandates in states such as California. Mills invest in oxygen delignification retrofits and carbon-capture pilots to align with corporate net-zero commitments. Europe leads the adoption of bio-based sizing agents and PFAS-free barrier coatings, driven by the Green Deal and strict packaging directives.

The Middle East and Africa region is projected to grow at a 6.05% CAGR through 2031, supported by infrastructure build-out and the localization of food and beverage packaging. New tissue machines in Saudi Arabia and Egypt fuel additive demand, while Oman's SOHAR petrochemical investments improve regional sourcing of fatty-acid derivatives. South America enjoys steady gains anchored by Brazil's pulp capacity expansions, with chemical suppliers integrating upstream to secure wood-derived feedstocks.

- Arkema

- Ashland Inc.

- BASF

- Buckman

- Cargill Incorporated

- Celanese

- Chemours

- Clariant

- Ecolab

- ERCO Worldwide

- Georgia-Pacific

- Imerys S.A.

- Kemira

- Nouryon

- Omya International AG

- Solenis

- Solvay

- Stora Enso

- UPM

- Valmet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of packaging-grade paper capacity in Asia

- 4.2.2 Surge in recycled-fiber furnish adoption

- 4.2.3 Water-free enzymatic bleaching breakthroughs

- 4.2.4 Carbon-negative bio-based sizing agents

- 4.2.5 E-commerce led SKU proliferation driving speciality chemicals

- 4.3 Market Restraints

- 4.3.1 Tightening AOX and COD discharge norms

- 4.3.2 High energy intensity vis-a-vis alternative substrates

- 4.3.3 Volatility in elemental chlorine prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Binders

- 5.1.2 Bleaching Agents

- 5.1.3 Fillers

- 5.1.4 Pulping Chemicals

- 5.1.5 Sizing Agents

- 5.1.6 Other Types

- 5.2 By Application

- 5.2.1 Newsprint

- 5.2.2 Packaging and Industrial Papers

- 5.2.3 Printing and Writing Papers

- 5.2.4 Pulp Mills and Water Treatment

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 UAE

- 5.3.5.3 Turkey

- 5.3.5.4 South Africa

- 5.3.5.5 Egypt

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core segments, Financials, Strategic info, Market rank/share, Products & Services, Recent developments)

- 6.4.1 Arkema

- 6.4.2 Ashland Inc.

- 6.4.3 BASF

- 6.4.4 Buckman

- 6.4.5 Cargill Incorporated

- 6.4.6 Celanese

- 6.4.7 Chemours

- 6.4.8 Clariant

- 6.4.9 Ecolab

- 6.4.10 ERCO Worldwide

- 6.4.11 Georgia-Pacific

- 6.4.12 Imerys S.A.

- 6.4.13 Kemira

- 6.4.14 Nouryon

- 6.4.15 Omya International AG

- 6.4.16 Solenis

- 6.4.17 Solvay

- 6.4.18 Stora Enso

- 6.4.19 UPM

- 6.4.20 Valmet

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-Need Assessment