|

시장보고서

상품코드

1632035

특수지 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Global Specialty Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

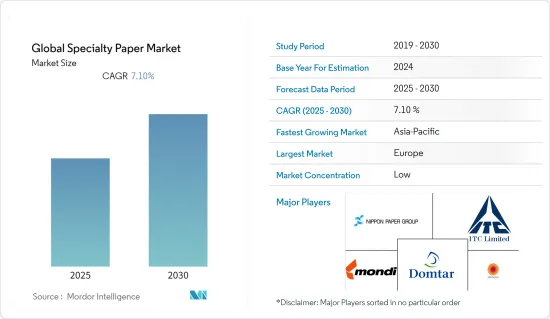

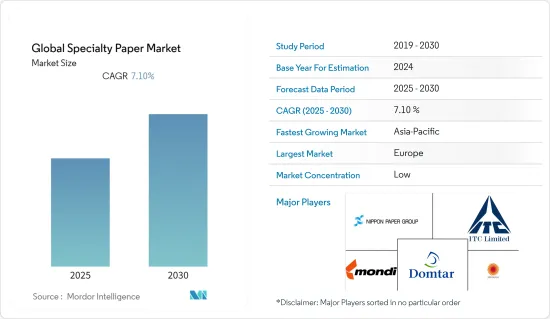

세계의 특수지 시장은 예측 기간 중 CAGR 7.1%를 기록할 것으로 예측됩니다.

외식 산업에서는 포장 박스, 포장 봉투, 종이 튜브, 종이 접시, 종이컵에 특수 용지를 사용하는 경우가 증가하고 있습니다. 특수 용지는 우수한 장벽 성능, 높은 습윤 강도, 우수한 유연성, 인쇄 적합성, 제품 저장 수명 연장, 원활한 운송 처리를 가능하게 합니다.

주요 하이라이트

- 특수지는 비반응성, 고품질, 방수, 내열성, 경량 등의 매력적인 특성으로 인해 포장 산업에서 수요가 증가하고 있습니다. 세계 인테리어 디자인 동향은 포장 및 E-Commerce 산업에서 특수 용지 판매를 증가시켰습니다.

- 크라프트 종이는 자체 접착식 루핑 및 바닥재에 널리 사용되며, 이형 라이너는 자재 설치 및 운송에 사용됩니다. 종이는 무거운 건축자재를 견딜 수 있는 내구성이 있어야 하며, 설치시 쉽게 벗겨질 수 있어야 합니다. 이는 크라프트지와 같은 특수 용지를 사용하여 실현할 수 있습니다. 건설 프로젝트가 증가함에 따라 특수지 시장은 산업의 주요 부분을 차지하고 있는 것으로 보입니다.

- 특수 종이의 분자 구조는 생분해성 옵션과 같은 사용자 요구에 따라 맞춤형 새로운 제품 변형을 개발하는 데 효과적입니다. 또한 특수지에 함유된 나노 물질은 일부 제품별로 적합합니다. 특수지의 이러한 모든 특성으로 인해 특수지는 많은 최종사용자들이 선호하는 선택지 중 하나가 되었습니다.

- 친환경 제품 사용 증가와 특수지 비용 상승이 시장에 영향을 미치고 있는 것으로 보입니다. 예를 들어 버진 페이퍼의 가장 일반적인 대체품은 소비 후 폐기물을 사용하는 것입니다. 이 유형의 종이는 소비자 폐기물(재활용 상자에 넣어지는 종이)의 비율이 높습니다. 종이를 매립지에 버리지 않고, 나무를 덜 심고, 에너지를 절약할 수 있습니다.

- 특수지 시장은 SARS-CoV-2 감염의 영향을 받았으며, COVID 기간 전반에는 이동 제한, 엄격한 출입 통제 기준, 노동력 감소로 인해 시장에 부정적인 영향을 미쳤습니다. 그러나 발병 후반기에는 E-Commerce 산업의 부상과 포장 식품 소비 증가로 인해 전 세계에서 특수 용지 판매가 증가했습니다.

특수용지 시장 동향

포장 및 라벨링이 가장 큰 비중을 차지

- 의료 산업을 위한 특수 용지는 오염이 없고 가벼워야 합니다. 최근 제약업계의 특수지 사용 추세는 더욱 정교한 포장 요건을 요구하고 있으며, 특수지는 오염이 없는 포장과 더 매력적이고 보기 쉬운 라벨링과 같은 과제에 대한 해결책을 제시하고 있습니다.

- 특수 용지의 사용은 어떤 유형의 장비 부품이든 특정 보호 오일로 덮인 후 종이로 싸여 있습니다. 크라프트 종이를 사용하면 포장 내부의 부품을 보호하고 오일이 상자 전체에 달라 붙는 것을 방지 할 수 있습니다.

- 예를 들어 BIOCARBON LAMINATES는 영국 최초의 탄소중립 라미네이트를 제공합니다. 바이오카본 라미네이트 제품군은 수명주기 분석(LCA)을 통해 환경 제품 선언(EPD) 및 환경 성능 인증을 받았습니다.

- 또한 호텔, 의료, 라커룸, 화장실, 레저시설, 상업시설, 교육시설, 소매점 등 위생을 중시하는 곳에서도 안심하고 사용할 수 있습니다.

- CEPI 회원국의 종이 및 판지 생산량은 2021년에 전년 대비 약 5.0% 증가한 5.8%로 2021년 총 생산량은 9,020만 톤에 달할 것으로 예상되며, 거의 모든 종이 및 판지 등급의 생산량이 증가할 것으로 보고되었습니다.

유럽이 주요 시장 점유율을 차지

- 유럽제지산업연맹(CEPI)이 발표한 보고서에 따르면 2021년도 포장용 등급 생산량은 2020년도 대비 약 7.1% 증가하여 유럽에서 사상 최고치를 기록했습니다. 포장용 등급 중 주로 운송 포장 및 골판지에 사용되는 케이스 재료는 E-Commerce 산업 증가 추세에 따라 증가하여 7.8% 증가했습니다.

- 종이 봉투 생산에 사용되는 포장재 등급은 11.7% 증가하여 EU가 지원하는 플라스틱 포장의 단계적 폐지에 따른 대체 효과의 혜택을 받았습니다.

- 주로 소매 포장에 사용되는 판지 생산량은 4.1% 증가했으며, 2021년 종이 및 판지 생산량에서 포장용 등급이 차지하는 비중은 58.7%, 그래픽용 등급은 27.8%를 차지했습니다. 기타 종이 및 판지 생산량은 9.6% 증가하여 전체 종이 및 판지 생산량에서 차지하는 비중은 4.8%였습니다(출처: CEPI).

- 예비 조사에 따르면 2021년세피 지구의 종이 및 판지 수입량은 약 1.5% 증가했으며, 주로 다른 유럽 국가로부터의 수입량은 21.8% 증가했습니다. 기타 유럽 국가의 수입량은 유럽 전체의 50.0%를 차지합니다.

- 2021년 펄프 생산량(종합+시장)은 2.2% 증가하였습니다. 전년 대비 총 생산량은 약 3,700만 톤이다(출처: CEPI).

특수용지 산업 개요

세계 특수지 시장은 경쟁이 치열합니다. 특수지 시장 진출기업은 지속가능성과 재활용성에 초점을 맞추었습니다. 제품 차별화를 통한 품질 유지는 특수지 시장의 주요 기업이 중점을 두고 있는 분야입니다.

- 2021년 12월 - Stora Enso Oyj는 핀란드 Varkaussite의 판지 생산에 2,300만 유로를 투자했습니다. 이 투자는 2022년 말에 완료될 예정이며, 고객에게 제공할 수 있는 제품 범위의 유연성을 높이고 이 사이트의 총 생산 능력을 약 10% 확대하는 것을 목표로 하고 있습니다.

- 2021년 3월-Pixelle은 Veritiv Corporation으로부터 특수지 사업 롤 소스를 인수했으며, 4월 5일에는 Appvion Operations Inc.로부터 무탄소 롤 및 보안지 사업을 인수했습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 신규 진출업체의 위협

- 구매자·소비자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간 경쟁 강도

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 지속가능 장식 라미네이션의 채택에 대한 소비자 선호도의 변화

- 간판에 대한 지출의 증가와 COVID-19 규제 해제

- 시장 성장 억제요인

- 특수지 제조시 화학제품 사용에 관한 엄격한 정부 규제

제6장 시장 세분화

- 용도별

- 포장 & 라벨링

- 푸드서비스 관리

- 인쇄·출판(포스터 용지)

- 건축·건설(벽지)

- 비즈니스 커뮤니케이션

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 기타 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 개요

- Stora Enso Oyj

- Nippon Paper Industries Co. Ltd

- Mondi Group PLC

- ITC Limited

- Domtar Corporation

- Nordic Paper AS

- Twin Rivers Paper Company

- LINTEC Corporation

- Sappi Limited

- BillerudKorsns AB

- Glatfelter Corporation

- Fedrigoni SPA

- Munksjo Group

- KAMMERER Spezialpapiere GmbH

- Mosaico SpA

제8장 투자 분석

제9장 시장의 미래

KSA 25.01.31The Global Specialty Paper Market is expected to register a CAGR of 7.1% during the forecast period.

In the Foodservice industry, specialty papers are increasingly being used for carryout boxes, carryout bags, paper tubes, paper plates, and cups. They provide good barrier performance, high wet strength, excellent flexibility, print-ability, increase the shelf life of a product, and also enable seamless transportation handling.

Key Highlights

- Specialty papers attractive features like non-reactance, high-quality, waterproof, temperature resistance, and lightweight have increased their demand in packaging industries. The surging trend of interior designing across the globe increased the sales of specialty papers in the packaging and e-commerce Industry.

- Kraft papers are used extensively for self-adhesive roofing and flooring, and release liners are used to install and transport materials. The paper needs to be durable enough to hold heavy construction materials and must be easily removed during installation. These can be achieved using specialty papers like Kraft paper. With growing trends in construction projects, the specialty paper market seems to be a major part of the industry.

- The molecular structure of specialty paper is effective in developing new product variants customized to the requirement of users, including biodegradable options. Also, nanomaterials in specialty papers make it suitable for several by-products. All these properties of specialty papers make it one of the favorite options for several end users.

- The rising trends of using eco-friendly products and the increased cost of specialty papers seem to impact the market. For example, the use of Post-Consumer Waste is the most common alternative to virgin paper. This type of paper is made from a high percentage of post-consumer waste - those paper items that are put into the recycling bin. It keeps paper out of landfills, reduces the number of trees used, and it also saves energy.

- The specialty paper market has been moderately affected by SARS-CoV-2 infections. In the first half of the COVID period, the market was negatively affected by movement restrictions, stringent lockdown norms, and a reduced workforce. However, the rising e-commerce industry and increased packaged food consumption during the 2nd half of the outbreak increased the sales of specialty papers worldwide.

Specialty Paper Market Trends

Packaging and Labeling holds the major market share

- Specialty papers for the medical industry need to be contamination-free and lightweight. With the recent trends of more sophisticated packaging requirements in the pharmaceutical industry's use of specialty, papers will provide solutions to challenges like contamination-free packaging and more attractive and visible labeling.

- The use of specialty papers while packaging parts of any equipment they are covered in a specific, protecting oil and then wrapped in paper. Kraft paper can be used to protect the parts in the packaging and keep the oil from getting all over the box.

- For Instance, BIOCARBON LAMINATES supply the UK's First Carbon Neutral Laminate. The BioCarbon Laminates range has received recognition of Environmental Product Declaration (EPD and environmental performance through a Life Cycle Analysis (LCA).

- The decorative laminate also provides the security of Anti-Microbial protection for hygiene-sensitive areas in industries such as hospitality, healthcare, locker rooms, washrooms, Leisure facilities, commercial interiors, and educational and retail.

- CEPI member countries' paper and board production increased by around 5.0% to 5.8% in 2021 compared to the previous year. Total production in 2021 reached 90.2 million ton, with an increase reported in almost all paper and board grades.

Europe Accounted to Hold the Major Market Share

- As per the report published by the Confederation of European Paper Industries (CEPI), the production of packaging grades increased by approximately 7.1% in FY 2021 compared to FY2020 reaching the highest level ever in Europe. Within packaging grades, case materials - mainly used for transport packaging and corrugated boxes, increased by upward trends in the e-commerce industry, recording an increase of 7.8%.

- The wrapping grades used for paper bag production - increased by 11.7% and benefited from substitution effects resulting from the EU-backed phase-out of plastic packaging.

- The output of carton boards, mainly used for retail packaging, increased by 4.1%. The share of packaging grades accounted for 58.7% in FY 2021 of the total paper and board production, with graphic grades 27.8%. The output of all other paper and board rates - mainly for particular and industrial purposes- was up by 9.6%, with a share of 4.8% of total paper and board production (source: CEPI).

- Preliminary indications show that imports of paper and board into the Cepi area increased by around 1.5% in FY 2021, primarily increasing volumes from other European countries by 21.8%. Other European countries account for 50.0% of all European imports.

- The production of pulp (integrated + market) was up by 2.2% in 2021. Compared to its previous year, with a total output of approximately 37.0 million ton (source: CEPI).

Specialty Paper Industry Overview

The global specialty papers market is highly competitive. The players in the specialty papers market are focusing on sustainability and recyclability. Maintaining quality with Product differentiation enhancement is a key focus area of key players in the specialty papers market.

- December 2021 - The company Stora Enso Oyj invested EUR 23 million into board production at a Varkaussite in Finland. The investment will be completed at the end of 2022 with an aim to increase the flexibility of the product range available for customers and to grow the site's total capacity by approximately 10%.

- March 2021 - Pixelle acquired the specialty paper business Rollsource from Veritiv Corporation. On April 5th, Pixelle acquired the carbonless rolls and security papers business from Appvion Operations Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porters 5 Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Changing consumer preference to adopt sustainable decorative lamination

- 5.1.2 Increased spending on signages and lifting of COVID-19 regulations

- 5.2 Market Restraints

- 5.2.1 Stringent Government Regulations Pertaining to the Usage of Chemicals While Manufacturing of Specialty Papers

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Packaging & Labelling

- 6.1.2 Food Service Management

- 6.1.3 Printing & Publication (Poster Paper|

- 6.1.4 Building & Construction (Wallpaper

- 6.1.5 Business and Communication

- 6.1.6 Others End User

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Stora Enso Oyj

- 7.1.2 Nippon Paper Industries Co. Ltd

- 7.1.3 Mondi Group PLC

- 7.1.4 ITC Limited

- 7.1.5 Domtar Corporation

- 7.1.6 Nordic Paper AS

- 7.1.7 Twin Rivers Paper Company

- 7.1.8 LINTEC Corporation

- 7.1.9 Sappi Limited

- 7.1.10 BillerudKorsns AB

- 7.1.11 Glatfelter Corporation

- 7.1.12 Fedrigoni SPA

- 7.1.13 Munksjo Group

- 7.1.14 KAMMERER Spezialpapiere GmbH

- 7.1.15 Mosaico SpA