|

시장보고서

상품코드

1636490

미국의 전기자동차 전지 전해액 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)United States Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

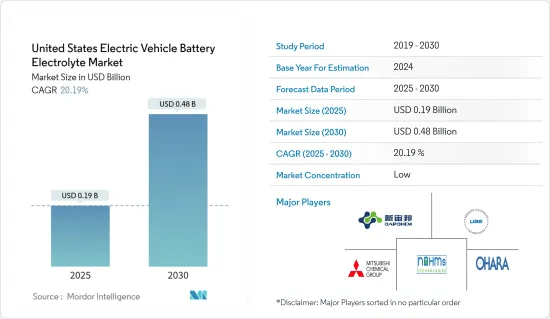

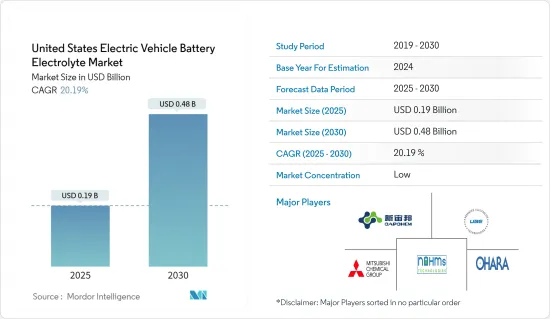

미국의 전기자동차 전지 전해액 시장 규모는 2025년에 1억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 20.19%로, 2030년에는 4억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 장기적으로 미국에서는 BEV, PHEV, HEV를 포함한 전기차 이용이 증가하고 있으며, 전기차 이용을 촉진하는 정부의 시책이 시장 성장을 가속할 것으로 예측됩니다.

- 한편, 중국과 같은 일부 국가의 독점으로 인한 전지 재료 공급망 격차는 향후 시장 성장을 억제할 것으로 예상됩니다.

- 전해질 재료와 효율적인 전해질 연구 및 진보가 진행되면서 시장 성장 기회를 제공할 수 있습니다.

미국 전기자동차 전지 전해질 시장 동향

리튬 이온 전지가 시장을 독점할 전망

- 전기자동차(EV)의 동력원으로서 매우 중요한 리튬 이온 전지는 전기자동차의 수명을 연장하고 전지 교체 빈도를 최소화합니다. 리튬 이온 전지는 다른 전지 유형과 달리 납이나 카드뮴과 같은 유해 물질이 없기 때문에 환경 친화적이고 깨끗하며 안전한 선택입니다. 또한 높은 출력은 빠른 가속과 고속 주행이 요구되는 EV에 필수적입니다.

- 지속가능 에너지 기업 회의(BCSE)에 따르면 2023년 시점에서 미국의 리튬 이온 전지 제조 능력은 114GWh에 육박하고 있습니다. 전기차 판매량이 증가하고 있기 때문에 자동차 부문의 리튬 이온 전지 수요는 향후 수년간 크게 성장할 전망입니다. 예를 들어 국제에너지기구의 보고에 따르면 미국과 캐나다에서 전기차 판매량은 2021-2023년에 걸쳐 54% 이상 급증했습니다. 이러한 리튬 이온 전지의 사용량 증가는 양극과 음극 사이에서 리튬 양이온을 수송하는데 필수적인 침투 전해질 용액 수요를 뒷받침합니다.

- 2023년 미국의 주요 화학 제조업체인 Huntsman Corporation은 텍사스 주에서 전해질 용매 에틸렌카보네이트의 생산을 강화할 계획을 발표했습니다. 또한 Capchem과 공동으로 미국에 공장을 설립하여 자국 내 전기자동차 전지 전해액 시장을 더욱 강화할 것입니다.

- 또한 2023년 3월 백악관은 'National Blueprint for Lithium Batteries'를 발표하여 2021-2030년까지의 산업의 방향성을 제시하였습니다. 이 청사진은 원료 조달의 강화와 자국 내 리튬 가공의 강화를 강조하고 있으며, 전기자동차 붐에 의한 미국의 리튬 이온 전지 수요의 급증이 예상되는 것을 강조하고 있습니다.

- 전기자동차에 리튬 이온 전지의 채용이 증가하고 가격도 하락하고 있기 때문에 이 부문은 향후 몇 년동안 크게 성장할 전망입니다.

전기차의 보급이 시장을 견인할 전망

- 소비자의 관심이 높아지고 정부의 지원 시책에 힘입어 미국에서는 전기자동차(EV)용 전지 전해질 시장이 급성장하고 있습니다.

- 특히 니켈과 전해액의 높은 기술 진보가 전지의 성능과 비용 효과를 높이고 있습니다. 동시에 미국은 리튬, 니켈, 코발트 등 중요한 재료의 자국 내 공급망을 강화하고 수입에 대한 의존도를 낮추며 안정성을 확보하는 것을 목표로 하고 있습니다.

- 2024년 1월, 매사추세츠 공과대학(MIT)의 연구원들은 전기자동차의 전원을 변화시킬 획기적인 전지 재료를 발표했습니다. 이 리튬 이온 전지는 혁신적인 유기 재료 기반 양극과 전해질 용액을 특징으로 하며 이는 기존의 코발트 및 니켈 사용으로부터의 전환을 의미합니다. 이러한 발전은 전지 전해질 재료의 내수를 증폭시킬 것입니다.

- 전기차 도입이 급증하는 가운데 미국은 전지 제조 공급망 강화를 선호하고 있습니다. 이 기세는 전해질을 포함한 전기자동차 전지 부품의 자국 내 생산에 박차를 가할 것으로 예상됩니다.

- 2023년 6월 중국 연구개발 중심 기업인 Capchem은 오하이오 주 남부에 1억 2,000만 달러의 전해질 공장을 건설할 계획을 발표했습니다. 동시에 Dongwha Electrolyte는 테네시에서 7,000만 달러의 시설을 건설하고 연간 7만 톤 이상의 전해액 생산을 목표로 하고 있습니다. 게다가 서울브레인은 인디애나주에 7,500만 달러의 전해액 공장을 설립하고 있으며, 인근 전지 공장에 대응하는 전략적인 입지가 되고 있습니다.

- EV의 보급이 상승 일변도를 따르는 가운데, 미국은 향후 에너지 밀도의 향상, 비용 절감, EV 주행 거리의 연장을 목적으로 한 전지 기술의 연구개발에 주력해 전지 양극 시장을 활성화시킬 것으로 예상됩니다.

- 국제에너지기구(IEA)의 데이터에 따르면 미국의 EV차 판매량은 크게 증가하여 2022년 99만대에서 2023년에는 139만대로 급증하였습니다.

- 2030년까지 2,600만대의 전기차가 보급될 것으로 예측됨에 따라, 미국에서는 1,290만개의 충전 포트가 필요할 것으로 예상되고, 이는 전기자동차 전지 양극 시장이 급성장하는 길을 열고 있습니다.

- 전기자동차의 보급이 가속되고 기술적인 진보도 관찰되므로 미국은 예측 기간 동안 시장을 선도해 나갈 것으로 예상됩니다.

미국 전기자동차 전지 전해질 산업 개요

미국의 전기자동차 전지 전해질 시장은 양분화되어 있습니다. 시장에 진출한 주요 기업(순서부동)에는 Advanced Electrolyte Technologies LLC, Mitsubishi Chemical Holdings, Shenzhen Capchem Technology, Nohms Technologies Inc., Ohara Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- BEV, PHEV, HEV를 포함한 전기자동차 이용 증가

- 전기자동차의 이용을 촉진하는 유리한 정부 시책

- 억제요인

- 전지 재료 공급망 격차

- 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자 분석

제5장 시장 세분화

- 전지 유형

- 리튬 이온 전지

- 납축전지

- 기타

- 전해질 유형

- 액체 전해질

- 겔 전해질

- 고체 전해질

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Advanced Electrolyte Technologies LLC

- Mitsubishi Chemical Holdings

- Shenzhen Capchem Technology Co., Ltd

- Nohms Technologies Inc

- Ohara Corporation

- BASF SE

- LG Chem Ltd

- Targray Industries Inc.

- 시장 순위/점유율(%) 분석

- 기타 유력 기업 목록

제7장 시장 기회와 앞으로의 동향

- 현재 진행중인 전해질 재료 조사와 진보

The United States Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.19 billion in 2025, and is expected to reach USD 0.48 billion by 2030, at a CAGR of 20.19% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing usage of electric vehicles, including BEVs, PHEVs, and HEVs, and favorable government policies to promote the usage of electric vehicles in the United States are expected to drive the market's growth.

- On the other hand, the supply chain gap in battery materials created by the monopoly of some countries like China is expected to restrain market growth in the future.

- Nevertheless, the ongoing research and advancement in electrolyte material and efficient electrolytes may offer opportunities for market growth.

United States Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery is Expected to Dominate the Market

- Lithium-ion batteries, pivotal for powering electric vehicles (EVs), extend the lifespan of these vehicles, thereby minimizing the frequency of battery replacements. Unlike some other battery types, lithium-ion batteries are deemed environmentally friendly, as they lack toxic materials such as lead or cadmium, making them a cleaner and safer option. Furthermore, their high power output is essential for EVs, which demand swift acceleration and elevated speeds.

- As of 2023, the United States boasts a lithium-ion battery manufacturing capacity of 114 GWh, according to the Business Council for Sustainable Energy (BCSE). With rising electric vehicle sales, the automotive sector's demand for lithium-ion batteries is poised for significant growth in the coming years. For example, the International Energy Agency reports that electric vehicle sales in the United States and Canada surged over 54% from 2021 to 2023. This uptick in lithium-ion battery usage will subsequently boost the demand for penetration electrolyte solutions, vital for transporting positive lithium ions between the cathode and anode.

- In 2023, Huntsman Corporation, a leading American chemical manufacturer, unveiled plans to boost production of the electrolyte solvent ethylene carbonate in Texas. Additionally, in collaboration with Capchem, they are establishing a plant in the United States, further bolstering the country's electric vehicle battery electrolyte solution market.

- Moreover, in March 2023, the White House unveiled the "National Blueprint for Lithium Batteries," charting the industry's course from 2021 to 2030. The blueprint emphasizes enhancing raw material sourcing and bolstering domestic lithium processing, underscoring the anticipated surge in lithium-ion battery demand in the United States driven by the electric vehicle boom.

- Given the rising adoption of lithium-ion batteries in electric vehicles and their declining prices, the segment is set for substantial growth in the coming years.

Increasing Adoption of Electric Vehicles is expected to Drive the Market

- Driven by rising consumer interest and supportive government policies, the United States is witnessing a rapid expansion in its electric vehicle (EV) battery electrolyte market.

- Technological advancements, particularly in high-nickel and electrolyte solutions, are boosting battery performance and cost-effectiveness. Concurrently, the U.S. is bolstering its domestic supply chain for critical materials such as lithium, nickel, and cobalt, aiming to reduce import reliance and ensure stability.

- In January 2024, MIT researchers unveiled a groundbreaking battery material set to transform electric vehicle power sources. This lithium-ion battery, featuring an innovative organic material-based cathode and electrolyte solution, marks a shift from the traditional cobalt or nickel usage. Such advancements are poised to amplify the nation's demand for battery electrolyte materials.

- As electric vehicle adoption surges, the United States is prioritizing the fortification of its battery manufacturing supply chain. This momentum is likely to spur domestic production of electric vehicle battery components, including electrolytes.

- In June 2023, Capchem, a China-based R&D-centric company, unveiled plans for a USD 120 million electrolyte plant in southern Ohio. Simultaneously, Dongwha Electrolyte commenced a USD 70 million facility in Tennessee, targeting an annual production of over 70,000 metric tons of electrolytes. Additionally, Soulbrain is establishing a USD 75 million electrolyte plant in Indiana, strategically located to cater to a nearby battery factory.

- Looking ahead, as EV adoption continues its upward trajectory, the United States's R&D focus on battery technology-aimed at boosting energy density, cutting costs, and extending EV range-will likely invigorate the battery cathode market.

- Data from the International Energy Agency highlights a significant jump in United States EV car sales, soaring to 1.39 million units in 2023 from 0.99 million in 2022.

- With projections of 26 million electric vehicles by 2030, the United States anticipates a need for 12.9 million charging ports, paving the way for a burgeoning electric vehicle battery cathode market.

- Given the accelerating adoption of EVs and technological strides, the United States is poised to lead the market during the forecast period.

United States Electric Vehicle Battery Electrolyte Industry Overview

The United States Electric Vehicle Battery Electrolyte Market is semi-fragmented. Some of the major companies operating in the market (in no particular order) include Advanced Electrolyte Technologies LLC, Mitsubishi Chemical Holdings, Shenzhen Capchem Technology Co., Ltd, Nohms Technologies Inc., and Ohara Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Usage of Electric Vehicles, including BEVs, PHEVs, and HEVs

- 4.5.1.2 Favorable government policies to promote the usage of electric vehicles

- 4.5.2 Restraints

- 4.5.2.1 The Supply chain gap in battery materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Other type of Batteries

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Advanced Electrolyte Technologies LLC

- 6.3.2 Mitsubishi Chemical Holdings

- 6.3.3 Shenzhen Capchem Technology Co., Ltd

- 6.3.4 Nohms Technologies Inc

- 6.3.5 Ohara Corporation

- 6.3.6 BASF SE

- 6.3.7 LG Chem Ltd

- 6.3.8 Targray Industries Inc.

- 6.4 Market Ranking/Share (%) Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Ongoing Research and Advancement in Electrolyte Material