|

시장보고서

상품코드

1637758

북미의 무균 포장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

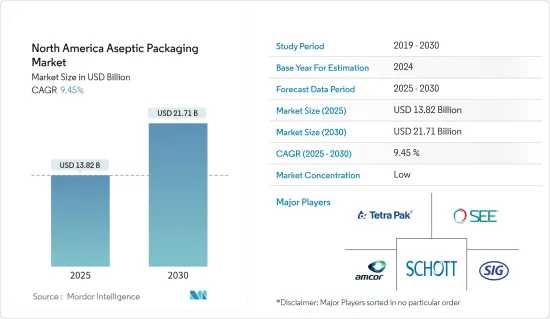

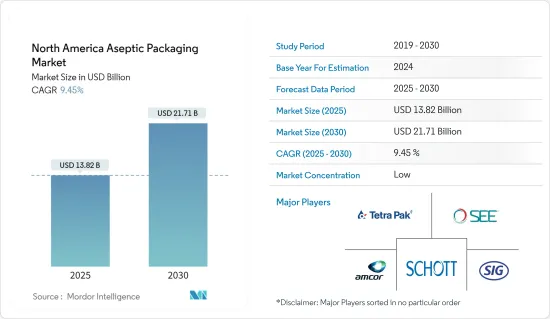

북미의 무균 포장 시장 규모는 2025년에 138억 2,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 9.45%로, 2030년에는 217억 1,000만 달러에 달할 것으로 예측됩니다.

이 시장은 유통기한 연장 및 냉장 보관이 필요 없는 식품 및 음료의 보존에 대한 요구가 증가함에 따라 크게 성장하고 있습니다. 또한 제품의 안전성과 품질을 강화하는 포장의 기술적 발전은 시장 발전에 매우 중요한 역할을 하고 있습니다.

주요 하이라이트

- 장거리 운송 수요가 급증함에 따라 유통기한 연장이 가장 중요한 과제로 떠오르고 있습니다. 제조 현장과 최종사용자 사이의 거리가 멀어짐에 따라 포장은 내구성과 보호 기능을 강화해야 합니다. 북미에서는 포장된 그대로 먹을 수 있는 식품을 선호하는 경향이 있으며, 무균 포장의 채택을 촉진하고 있습니다.

- 식품 및 음료와 같은 최종사용자 산업은 지속가능한 포장과 유통기한 연장을 우선시하고 있습니다. 많은 지역 식품 및 음료 공급업체는 특히 상온 배송 및 보존을 위해 비용과 환경적 이점을 고려하여 무균 포장으로 전환하고 있습니다. 또한 무균 포장은 재활용이 가능한 종이팩이나 환경 친화적인 파우치를 활용하고 있습니다. 이러한 선택은 소량으로 더 자주 구매하는 것을 선호하는 소비자들에게 어필하는 경우가 많으며, 이 지역에서 이러한 제품에 대한 큰 수요를 주도하고 있습니다.

- 소비자들은 건강에 대한 관심이 높아지고 있습니다. 소비자들은 아침 주스부터 에너지 음료에 이르기까지 이러한 웰빙 지향에 부합하는 제품에 더 적극적으로 투자하고 있습니다. 이에 따라 음료 포장 부문에서 비용 효율적인 포장 솔루션에 대한 수요가 급증하고 있습니다. 또한 특히 우유 및 유음료 부문에서 무균 카톤에 대한 선호도가 높아지고 있으며, 이는 시장을 활성화시킬 것으로 예상됩니다. 이러한 카톤은 쉽게 쌓을 수 있으며, 제품의 유통기한을 연장할 수 있습니다.

- 포장가공기술협회(PMMI)의 음료 보고서에 따르면 북미 음료 산업은 2028년까지 약 4.5% 성장할 것으로 예상됩니다. 이 급성장하는 음료 시장은 연구 시장의 성장을 가속할 준비가 되어 있습니다. 이 지역의 제약 부문, 특히 미국에서는 무균 포장에 대한 수요가 크게 증가하고 있습니다. 이러한 증가는 주로 생명공학으로 인한 의약품의 가용성 및 소비 증가, 다양한 액체 의약품의 무균 충전 요구로 인해 발생합니다.

- 고객의 요구사항 증가와 보관 및 유통 비용 절감의 필요성에 대응하기 위해 기업은 센서, RFID, NFC와 같은 커넥티드 기술을 활용하고 첨단 기술에 투자하고 있습니다. 이러한 투자는 제조업체에서 소매업체에 이르기까지 제품 관리와 관련된 비용을 크게 줄이거나 없애는 것을 목표로 하고 있습니다.

- 그러나 무균 포장 시장에는 몇 가지 문제가 있으며, 매출 성장에 걸림돌이 될 수 있습니다. 무균 포장의 초기 자본 지출은 기존 신선식품 제조 방법보다 2-3배 더 높을 수 있습니다. 또한 무균 처리에 특화된 배합을 미세 조정할 수 있도록 처음부터 연구팀을 참여시키는 것이 중요합니다. 그러나 이러한 필요성은 기존 방식과 비교했을 때 무균 포장의 비용을 크게 상승시킬 수 있습니다.

북미 무균 포장 시장 동향

음료 부문이 큰 시장 점유율을 차지할 것으로 예상

- 소비자들이 건강과 웰빙을 점점 더 우선시함에 따라 특히 비용 효율적인 포장에 중점을 둔 과일 베이스 레디 투 드링크 음료에 대한 수요가 급증하고 있습니다. 이러한 추세는 예측 기간 중 더욱 강화될 것으로 예상됩니다. 무균 포장은 이러한 음료의 유통기한을 연장할 뿐만 아니라 보존 가능한 과일 주스와 같은 혁신도 도입할 수 있습니다.

- 편의성은 북미 전역의 레디 투 드링크 음료 및 건강 지향적 카테고리에서 지배적인 동향으로 부상하고 있습니다. 홈메이드 음료는 많은 준비가 필요하므로 소비자들은 바로 마실 수 있는 칵테일을 선호하고 있습니다. 이러한 변화는 중요한 추세를 강조하고 있습니다. 소비자들은 이러한 칵테일의 독특한 맛에 매료되어 집 밖에서 쉽게 즐길 수 있다는 점에 가치를 두고 있습니다.

- 유제품 산업의 세계 동향은 혁신적인 포장을 통한 제품 차별화를 추구하고 있다는 것을 보여줍니다. 오늘날의 유제품 포장은 눈길을 끄는 디자인과 첨단 무균 기능을 갖춘 경우가 많습니다. 이러한 포장 혁신의 중요성은 북미 주요 시장에서의 치열한 경쟁에 대응하기 위한 것입니다.

- 초고온 살균 처리된 무균 우유는 유해한 박테리아를 효과적으로 제거합니다. 유제품의 카테고리는 다양하며, 흰 우유와 그 제품별 제품인 기, 버터밀크, 요구르트 기반 음료뿐만 아니라 향료첨가우유의 유망한 영역도 포함됩니다. 방부제를 사용하지 않는 무균 처리 및 포장은 우유와 같은 신선 식품에 중요한 보존 기간과 신선도를 크게 향상시킵니다.

- 무균 포장에 대한 유업계의 의욕이 높아지는 것은 보다 광범위한 추세를 시사합니다. 원유 생산량이 증가함에 따라 새로운 세계 시장 기회가 열리고 있습니다. 미국 농무부는 미국의 우유 생산량이 2018년 2,176억 파운드에서 2024년 약 2,282억 파운드로 증가할 것으로 예측했습니다. 또한 소비자의 눈에 띄는 변화로 유통기한이 길어 소비자들이 매장 방문 횟수를 줄일 수 있는 UHT 우유에 대한 수요가 급증하고 있습니다. 또한 COVID-19의 영향으로 기존 팩에 담긴 생우유나 벌크 우유보다 UHT 우유의 무균 포장을 선호하는 경향이 두드러져 유제품 소비 패턴이 크게 변화하고 있음을 알 수 있습니다.

시장 성장이 기대되는 캐나다

- 캐나다의 낙농 부문에 대한 투자는 계속되고 있으며, 캐나다의 경제를 강화하고 있습니다. 지역 수요를 충족시키기 위해 캐나다 정부는 첨단 포장 기술, 특히 무균 포장의 채택을 장려하고 있습니다. 건강을 중시하는 밀레니얼 세대와 캐나다의 젊은 세대는 과자, 탄산음료, 인공감미료의 위험성에 대한 인식이 높아지면서 우유, 주스, 에너지 드링크 등을 선호하고 있습니다.

- 2024년 5월 StatCan이 발표한 보고서에 따르면 캐나다의 표준 3.25% 우유 생산량은 2020년 약 43만 8,380킬로리터에서 2023년 46만 8,070킬로리터로 증가할 것으로 예상했습니다. 070 킬로리터로 증가했습니다. 유제품을 기반으로 한 음료 부문에서는 부패하기 쉬운 품목의 경우 무균 액체 포장을 선호합니다. 유제품의 특성을 고려할 때, 이러한 매우 부패하기 쉬운 액체 식품 및 음료의 경우 포장 품질이 가장 중요합니다.

- 무균 솔루션 프로바이더들은 유제품 포장 부문의 과제를 해결하고 있습니다. 무균 포장을 사용하는 제품의 약 60%가 유제품이며, 여기에는 숟가락으로 먹는 요구르트, 치즈, 크림, 아이스크림 등이 포함됩니다. 유제품의 소비는 천연치즈, 분말치즈, 가공치즈 등 다양하지만 부패성은 여전히 시급한 문제입니다. 무균 포장은 치즈의 유통기한을 60일까지 연장할 수 있습니다.

- 따라서 최종사용자는 포장에 많은 투자를 하고 있습니다. 유제품은 향의 이동과 산소 노출에 의한 분해에 취약하므로 포장에 우수한 장벽이 필요하며, StatCan의 데이터에 따르면 캐나다의 유제품 판매량이 눈에 띄게 증가하고 있으며, 2024년 1월부터 5월까지 월별 제조업체 매출은 13억 9,000만 캐나다 달러(10억 3,000만 달러)로부터 16억 7,000만 캐나다 달러(12억 4,000만 달러)로 급증했습니다.

- 또한 무균 의약품 제조(종종 충전 마감 제조라고도 함)는 백신, 생물제제, 주사제, 항암제, 다양한 형태의 귀, 코, 눈 점안제 제조에 있으며, 매우 중요합니다. 이 방법은 의약품이 박테리아 및 기타 유해 물질로 오염될 위험을 크게 줄입니다. 캐나다에서 제약 부문은 캐나다에서 가장 혁신적인 산업 중 하나로 자리 잡고 있습니다. 시판 의약품뿐만 아니라 독창적인 제네릭 의약품을 개발 및 제조하는 기업도 포함되어 있습니다.

북미 무균 포장 산업 개요

무균 포장은 카톤과 친환경 파우치를 사용하여 소량, 소량 구매를 선호하는 소비자들을 만족시키며 수요를 견인하고 있습니다. 또한 소비자들이 방부제를 사용하지 않는 유기농 제품을 찾는 추세에 따라 제조업체들은 신선도를 유지하고 유통기한을 연장하는 고급 포장 솔루션에 투자하여 대응하고 있습니다.

북미 무균 포장 시장은 여러 업체가 국내외 시장에 제품을 공급하고 있으며, 경쟁이 치열합니다. 시장은 세분화되어 있으며, 주요 업체들은 진입 범위를 확대하고 경쟁을 유지하기 위해 다양한 전략을 채택하고 있습니다. Amcor Group, DS Smith Plc, Schott AG 등이 주요 시장 진출기업으로 꼽힙니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 기술 스냅숏

제5장 시장 역학

- 시장 성장 촉진요인

- 콜드체인 물류의 비용 삭감에 대한 수요 증가

- 제품의 장기 보존에 대한 수요 증가

- 시장 성장 억제요인

- 제조의 복잡화와 투자수익률의 저하

제6장 시장 세분화

- 제품 유형

- 플라스틱병

- 프리필러블 시린지

- 바이알과 앰플

- 백과 파우치

- 카톤

- 컵

- 유리병

- 최종사용자 유형

- 의약품

- 음료

- 과일계

- 유음료

- RTD(Ready-to-Drink

- 기타 음료

- 식품

- 과일 기반

- 유제품

- 가공식품

- 이유식

- 수프·브로스(Broths)

- 기타 식품 산업

- 국명

- 미국

- 캐나다

제7장 경쟁 구도

- 기업 개요

- Tetra Pak International S.A.

- Amcor Group

- Sealed Air Corporation

- SIG Combibloc Group

- WestRock Company

- Schott AG

- Scholle IPN

- DS Smith PLC

- Elopak AS

- Mondi PLC

제8장 투자 분석

제9장 시장 기회와 향후 동향

KSA 25.02.10The North America Aseptic Packaging Market size is estimated at USD 13.82 billion in 2025, and is expected to reach USD 21.71 billion by 2030, at a CAGR of 9.45% during the forecast period (2025-2030).

The market is witnessing significant growth, driven by the rising need for extended shelf life and the preservation of food and beverages without refrigeration. Furthermore, technological advancements in packaging that bolster product safety and quality play a pivotal role in propelling the market forward.

Key Highlights

- As demand for long-distance transportation surges, extending shelf life has become paramount. Packaging must enhance its durability and protective features with growing distances between manufacturing sites and end users. North America's penchant for packaged and ready-to-eat meals is driving the adoption of aseptic packaging.

- The end-user industries, such as food and beverage, prioritize sustainable packaging and extended shelf life. Many regional food and beverage vendors are leaning towards aseptic packaging, weighing both cost and environmental benefits, particularly for ambient shipping and storage. Furthermore, aseptic packaging utilizes recyclable cartons and eco-friendly pouches. These options often appeal to consumers favoring smaller quantities and more frequent purchases, driving significant demand for such products in the region.

- Consumer health and wellness consciousness is on the rise. They are willing to invest more in products that align with this wellness trend, from morning juices to energy drinks. Therefore, there's a surging demand for cost-effective packaging solutions in the beverage packaging segment. Furthermore, the growing preference for aseptic cartons, especially from the milk and dairy beverage sectors, is set to invigorate the market. These cartons facilitate easy stacking and extend the product's shelf life.

- As per the Beverage Report by the Association for Packaging and Processing Technologies (PMMI), North America's beverage industry is projected to expand by approximately 4.5% by 2028. This burgeoning beverage market is poised to propel the growth of the studied market. In the region's pharmaceutical sector, particularly in the United States, there's been a significant surge in demand for aseptic packaging. This uptick is primarily driven by the increasing availability and consumption of biotechnology-based drugs and various liquid pharmaceuticals' aseptic filling needs.

- In response to rising customer demands and the imperative to control storage and distribution costs, companies are leveraging connected technologies like sensors, RFID, and NFC and channeling investments into advanced technologies. These investments aim to substantially cut down or eliminate costs associated with managing products from manufacturers to retailers.

- However, several challenges loom over the aseptic packaging market, potentially hindering its revenue growth. The initial capital outlay for aseptic packaging can be two to three times higher than that of conventional fresh production methods. Furthermore, involving research teams from the beginning is crucial, enabling formula tweaks specific to aseptic processing. Yet, this necessity can significantly escalate the costs of aseptic packaging when posed with traditional methods.

North America Aseptic Packaging Market Trends

Beverages Segment is Expected to Hold a Significant Market Share

- As consumers increasingly prioritize health and wellness, the demand for fruit-based ready-to-drink beverages is surging, especially with a focus on cost-effective packaging. This trend is expected to intensify over the forecast period. Aseptic packaging not only extends the shelf life of these beverages but also introduces innovations like shelf-stable fruit juices.

- Convenience is emerging as a dominant trend in ready-to-drink beverages and health-focused categories across North America. Given the extensive preparation required for homemade beverages, consumers gravitate towards ready-to-drink cocktails. This shift highlights a significant trend: consumers are drawn to the unique flavors of these cocktails and value the ease of enjoying them outside the home.

- Global trends in the dairy industry reveal a push towards product differentiation through innovative packaging. Today's dairy product packaging often boasts eye-catching designs and advanced aseptic features. This emphasis on packaging innovation is a response to fierce competition in key North American markets.

- Aseptic milk, treated with ultra-high-temperature pasteurization, effectively eliminates harmful bacteria. The dairy category is diverse, encompassing not just white milk and its byproducts like ghee, buttermilk, and yogurt-based beverages but also the promising realm of flavored milk. Aseptic processing and packaging, free from preservatives, significantly enhance shelf life and freshness-vital attributes for perishable items like milk.

- The dairy industry's growing appetite for aseptic packaging signals a broader trend. With rising milk production, new global market opportunities are on the horizon. For context, the USDA projects U.S. cow milk production to increase from 217,600 million pounds in 2018 to approximately 228,200 million in 2024. Additionally, a notable consumer shift has been the surging demand for UHT milk, prized for its extended shelf life, allowing consumers to reduce store visits. Furthermore, with the effect pandemic, there was a marked preference for the sterile packaging of UHT milk over traditional packaged fresh and bulk milk, underscoring a significant evolution in dairy consumption patterns.

Canada is Expected to Witness Growth in the Market

- Investments continue to flow into the Canadian dairy sector, bolstering the nation's economy. Responding to regional demands, the Canadian government is championing the adoption of advanced packaging technologies, particularly aseptic packaging. Health-conscious millennials and the younger generation in Canada increasingly gravitate towards milk, juices, and energy drinks, driven by a heightened awareness of the risks of excessive sweets, carbonated sodas, and artificial sugars.

- In Canada, consumers are increasingly opting for milk cartons over glass bottles and plastic alternatives, driven by eco-friendly concerns and the cost-effectiveness of cartons. A report from StatCan in May 2024 highlighted that Canada's production of standard 3.25% milk rose from about 438.38 thousand kiloliters in 2020 to 468.07 thousand kiloliters in 2023. Aseptic liquid packaging is preferred for perishable items in the dairy-based beverages sector. Given the nature of dairy products, the quality of packaging is paramount for these highly perishable liquid foods and beverages.

- Aseptic solution providers are addressing challenges in the dairy packaging arena. Nearly 60% of products using aseptic packaging are dairy items, including spoonable yogurt, cheese, cream, and ice cream. Dairy consumption spans natural, powdered, and processed cheese, but perishability remains a pressing concern. Aseptic packaging can extend cheese's shelf life by an impressive 60 days.

- Consequently, end users are channeling substantial investments into packaging. Given dairy's vulnerability to fragrance transfer and decomposition from oxygen exposure, packaging must boast superior barrier qualities. Data from StatCan reveals a notable uptick in Canada's dairy product sales: from January to May 2024, monthly manufacturer sales surged from CAD 1.39 billion (USD 1.03 billion) to CAD 1.67 billion (USD 1.24 billion).

- Further, aseptic pharmaceutical manufacturing, often termed fill-finish manufacturing, is crucial in producing vaccines, biologics, injectable drugs, cancer treatments, and various forms of ear, nasal, and eye drops. This method significantly reduces the risk of contaminating medications with germs or other harmful substances. In Canada, the pharmaceutical sector stands out as one of the nation's most innovative industries. It encompasses companies developing and producing creative and generic medicines alongside over-the-counter drug products.

North America Aseptic Packaging Industry Overview

Aseptic packaging utilizes cartons and eco-friendly pouches and caters to consumers who favor smaller, more frequent purchases, driving demand. Furthermore, as consumers increasingly seek organic products without preservatives, manufacturers are responding by investing in premium packaging solutions that preserve freshness and extend shelf life.

The North America Aseptic Packaging Market is competitive owing to the presence of multiple vendors in the market supplying their products in domestic and international markets. The market appears fragmented, with major players adopting various strategies to expand their reach and stay competitive. Some of the major players in the market are Amcor Group, DS Smith Plc, Schott AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness- Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand to Reduce the Cost of Cold Chain Logistics

- 5.1.2 Increasing Demand for the Longer Shelf Life of Products

- 5.2 Market Restraint

- 5.2.1 Manufacturing Complications and Lower Return on Investments

6 MARKET SEGMENTATION

- 6.1 Product Type

- 6.1.1 Plastic Bottles

- 6.1.2 Prefillabe Syringes

- 6.1.3 Vials and Ampoules

- 6.1.4 Bags and Pouches

- 6.1.5 Cartons

- 6.1.6 Cups

- 6.1.7 Glass Bottles

- 6.2 End- User Type

- 6.2.1 Pharmaceutical

- 6.2.2 Beverage

- 6.2.2.1 Fruit-based

- 6.2.2.2 Milk and Other Dairy Beverages

- 6.2.2.3 Ready-to-Drink

- 6.2.2.4 Other Beverage Industry Types

- 6.2.3 Food

- 6.2.3.1 Fruit-based

- 6.2.3.2 Dairy Food

- 6.2.3.3 Processed Foods

- 6.2.3.4 Baby Foods

- 6.2.3.5 Soups and Broths

- 6.2.3.6 Other Food Industry Types

- 6.3 Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tetra Pak International S.A.

- 7.1.2 Amcor Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 SIG Combibloc Group

- 7.1.5 WestRock Company

- 7.1.6 Schott AG

- 7.1.7 Scholle IPN

- 7.1.8 DS Smith PLC

- 7.1.9 Elopak AS

- 7.1.10 Mondi PLC