|

시장보고서

상품코드

1640494

바이오 접착제 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Bio-based Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

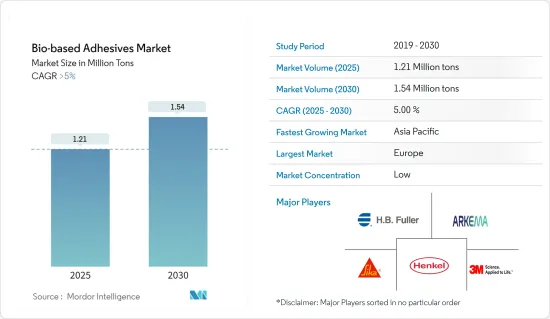

바이오 접착제 시장 규모는 2025년에 121만톤으로 추정되며, 예측기간 중(2025-2030년)의 CAGR은 5%를 초과하여, 2030년에는 154만톤에 달할 것으로 예측됩니다.

주요 하이라이트

- 포장 부문 수요 증가와 미국의 기존 접착제에 대한 엄격한 규제가 시장 성장을 가속하는 두 가지 주요 요인입니다.

- 그러나 석유계 첨가제에 비해 바이오계 첨가제의 짧은 저장 수명과 성능상 단점이 시장 성장을 방해할 가능성이 높습니다.

- 모듈 건설의 확대는 단기적으로 시장에 성장 기회를 가져올 가능성이 높습니다.

- 바이오 접착제 시장은 유럽이 세계를 주도하고 있으며 예측 기간 동안 가장 높은 성장률을 기록할 가능성이 높습니다.

바이오 접착제 시장 동향

포장산업이 시장을 독점할 전망

- 보관이나 운송에 안정성이 요구되기 때문에 또는 미관상의 이유로, 모든 공업 제품은 매우 높은 비율로 포장된 상태로 판매되고 있습니다. 현재 사용되는 포장재의 대부분은 접착제를 사용하여 다른 재료를 조합하여 라미네이트 가공한 것입니다.

- 바이오 접착제는 지속가능한 포장, 라벨링, 라미네이트, 보존 기간 연장을 위한 식용 코팅, 유제품 및 음료 가공 내 조립, 퇴비화 가능한 포장, 기능적 응용, 전환 우려에 대처할 수 있어 환경친화적인 산업에 기여하며 식품 산업에 필수적입니다.

- PMMI(The Association for Packaging and Processing)에 따르면, 북미의 음료 포장 산업은 2018-2028년에 걸쳐 4.5%의 성장을 기록할 것으로 예상되고 있으며, 미국이 음료 포장 부문의 발전에 중요한 역할을 하고 있습니다.

- Amazon Fresh와 같은 서비스의 보급은 점차 확대되고 있으며, 소비자는 집에서 신선한 농산물을 받을 수 있게 되었습니다. 또한, 식품 가공 공장의 대부분은 포장용 바이오 접착제를 주로 사용하고 있습니다.

- 유기농 식품의 세계적인 수요 증가는 식품 포장 소비를 밀어 올릴 것으로 예상됩니다. Organic Trade Association에 따르면 미국에서 유기농 포장 식품은 2025년까지 250억 6,040만 달러에 이를 것으로 예상됩니다.

- 인도포장산업협회(PIAI)에 따르면 인도의 포장산업은 예측기간 동안 22%의 성장률이 예상됩니다. 인도의 포장 시장은 2025년까지 2,048억 1,000만 달러에 이를 것으로 예상됩니다. 따라서 바이오 접착제 시장은 이 지역에서 성장할 것으로 예상됩니다.

- 특히 동유럽 국가와 북미 국가에서는 생활수준의 향상과 구매소득 증가에 따라 폭넓은 제품에 대한 수요가 높아지고 있으며, 이 제품은 모두 포장이 필요합니다. 따라서 포장에 대한 수요는 바이오 접착제의 소비를 증가시키고 있습니다.

- 앞서 언급한 모든 요인들은 포장 산업을 견인하고 예측 기간 동안 바이오 접착제에 대한 수요를 높일 것으로 예상됩니다.

유럽이 시장을 독점할 전망

- 독일과 영국 등의 국가의 높은 수요로 인해 유럽은 바이오 접착제 시장을 독점하고 있습니다.

- 독일은 유럽에서 바이오 접착제의 주요 소비국이며 많은 대기업이 진출하고 있습니다. 독일은 또한 세계적인 천연 고무계와 전분계 접착제의 주요 생산국입니다.

- 독일 내 바이오 숙신산 생산량 증가는 바이오 숙신산을 기반으로 하는 바이오 베이스 라벨용 접착제의 생산을 지원합니다.

- 바이오 베이스 접착제는 건설 산업에서 매우 중요한 역할을 하며 목재의 접착, 패널이나 복합재 제조, 단열재 접착, 환경친화적인 바닥재 설치, 건축용 실링재, 조립식 건축, 접착 테이프, 환경친화적인 지붕 설치, 생분해성 거푸집 접착제 등 전체적인 지속가능한 건설 프랙티스 등에 이용되어 환경친화적인 건축 공정에 기여하고 있습니다.

- 유럽위원회가 발표한 데이터에 따르면 2023년 12월 건설생산액의 2022년 12월 대비 성장은 유로존 전체에서 1.9%, 유럽연합 전체에서 2.4%였습니다. 2023년 건설생산 대 2022년 대비 평균 증가율은 유로존에서 0.2%, 유럽연합에서 0.1%였습니다.

- 의료 산업에서 바이오 접착제는 상처 치료, 의료기기 조립, 약물 전달 시스템 등 다양한 의료 제약 부문에서 사용되며 생체 적합성과 안전성이 우수한 접착 솔루션을 제공합니다.

- 경제협력개발기구(OECD)의 새로운 보고서에 따르면 2023년 독일이 GDP의 12.7%를 의료비에 지출하였고 프랑스가 GDP의 약 12.1%를 의료비에 지출하는 2위 지출국이 되었습니다.

- 퍼스널케어 산업에서는 바이오 접착제가 화장품 및 위생 용품 생산에 사용되어 붕대, 접착 테이프, 생리용품 등의 조립에 기여해, 종래의 접착제를 대신하는 지속가능하고 피부 친화적인 대체품을 제공합니다.

- 국가 통계국(영국)에 따르면 영국의 개인 관리에 대한 소비자 지출은 2023년 1분기에 78억 9,600만 파운드에 이르렀고, 2022년 1분기 73억 6,300만 파운드에서 증가했습니다.

- 이탈리아에서는 주택 건설 활동과 다양한 시설 프로젝트가 증가하고 있으며, 모듈형 건축 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다. Eurostat(유럽위원회 총국)에 따르면 이탈리아의 건설 수입은 2025년까지 약 576억 8,000만 달러에 달할 전망입니다.

- 따라서 유럽은 바이오 접착제 시장을 독점할 가능성이 높으며 예측 기간 동안 최대 시장 점유율을 차지할 것으로 예상됩니다.

바이오 산업 개요

세계 바이오 접착제 시장은 세분화되어 주요 기업 간의 경쟁이 치열합니다. 시장에 진입하는 주요 진출기업으로는 Henkel AG & Co. KGaA, HB Fuller, Arkema, Sika, 3M company 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 성과

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 촉진요인

- 포장 부문으로부터 수요 증가

- 미국 내 기존 접착제에 대한 엄격한 규제

- 기타 촉진요인

- 억제요인

- 석유계 접착제에 비해 짧은 저장 수명과 성능

- 기타 억제요인

- 산업 가치사슬 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 원료

- 송진

- 전분

- 리그닌

- 콩

- 기타 원료

- 최종 사용자 산업

- 건축 및 건설

- 종이 및 판지 포장

- 의료

- 퍼스널케어

- 목공 및 소목

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- 3M

- Arkema(bostik)

- Artimelt AG

- Beardow Adams

- Dow

- Emsland Group

- HB Fuller Company

- Henkel AG & Co. KGaA

- Ingredion Incorporated

- Paramelt BV

- Sika AG

- Solenis

제7장 시장 기회와 앞으로의 동향

- 엔지니어드 우드 제품에의 응용 확대

- 기타 기회

The Bio-based Adhesives Market size is estimated at 1.21 million tons in 2025, and is expected to reach 1.54 million tons by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

Key Highlights

- The increasing demand from the packaging sector and the stringent regulations for conventional adhesives in the United States are two main factors driving the market growth.

- However, the low shelf life and performance hindrance of bio-based additives compared to petroleum-based additives is likely to hinder market growth.

- Nevertheless, the growing modular construction activities are likely to provide growth opportunities for the market over the short term.

- Europe dominates the bio-based adhesives market across the world and is likely to witness the highest growth rate during the forecast period.

Bio-based Adhesives Market Trends

The Packaging Industry is Expected to Dominate the Market

- An extremely high proportion of all industrial products are sold in packaged form, either due to stability requirements for storage and transport or aesthetic reasons. Most of the packaging materials currently being used are made from a combination of different materials laminated together with the help of adhesives.

- Bio-based adhesives are integral to the food and beverage industry, facilitating sustainable packaging, labeling, laminates, edible coatings for extended shelf life, assembly in dairy and beverage processing, compostable packaging, functional applications, and addressing migration concerns, thereby contributing to a greener and more environment-friendly industry.

- As per PMMI (The Association for Packaging and Processing), the North American beverage packaging industry is expected to record a 4.5% growth from 2018 to 2028, with the United States taking a prominent role in advancing the beverage packaging sector.

- The prevalence of services like Amazon Fresh is on the rise, enabling consumers to acquire fresh produce from the comfort of their homes. Additionally, the majority of food and beverage processing plants are centered around bio-based adhesives for the packaging.

- The rising demand for organic food globally is expected to boost the consumption of food packaging. According to the Organic Trade Association, in the United States, organic packaged food is likely to reach a value of USD 25,060.4 million by 2025.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at a rate of 22% during the forecast period. The Indian packaging market is expected to reach USD 204.81 billion by 2025. Therefore, the bio-based adhesives market is expected to grow in the region.

- The improvement in living standards and higher purchasing incomes, especially in Eastern European and North American countries, has increased the demand for a broad range of products, all of which require packaging. Therefore, the demand for packaging has, in turn, increased the consumption of bio-based adhesives.

- Hence, all the aforementioned factors are expected to drive the packaging industry, enhancing the demand for bio-based adhesives during the forecast period.

Europe is Expected to Dominate the Market

- Europe dominated the bio-based adhesives market owing to the high demand from countries like Germany and the United Kingdom.

- Germany is the major consumer of bio-based adhesives in Europe, with many major companies having a presence in the country. It is a major producer of natural rubber- and starch-based adhesives in the global scenario.

- The increase in the production of bio-succinic acid in Germany has supported the production of bio-based label adhesives that are based on bio-succinic acid.

- Bio-based adhesives play a pivotal role in the construction industry, being utilized for wood bonding, panel and composite manufacturing, insulation material bonding, eco-friendly flooring installations, construction sealants, prefabricated construction, adhesive tapes, green roofing installations, biodegradable formwork adhesives, and overall sustainable construction practices, contributing to environmentally conscious building processes.

- As per the data released by the European Commission, growth in construction production in December 2023 compared to December 2022 was 1.9% across the euro area and 2.4% across the European Union. The year-on-year average increase in construction production in 2023 compared to 2022 was 0.2% for the euro area and 0.1% for the European Union.

- In the healthcare industry, bio-based adhesives find applications in various medical and pharmaceutical contexts, including wound care, medical device assembly, and drug delivery systems, providing biocompatible and safe bonding solutions.

- According to a new report by the Organisation for Economic Co-operation and Development (OECD), in 2023, Germany was the second-largest spender in healthcare, disbursing 12.7% of its GDP on healthcare, followed by France, which spent around 12.1% of its GDP.

- In the personal care industry, bio-based adhesives are employed in the production of cosmetic and hygiene products, contributing to the assembly of items such as bandages, adhesive tapes, and sanitary products, offering a sustainable and skin-friendly alternative to traditional adhesives.

- According to the Office for National Statistics (UK), consumer spending on personal care in the United Kingdom reached GBP 7,896 million in the first quarter of 2023, increasing from GBP 7,363 million in the first quarter of 2022.

- In Italy, the market for modular construction is expected to grow at a significant rate during the forecast period, with an increase in residential construction activities and various institutional projects. As per Eurostat (a directorate-general of the European Commission), the construction revenue in Italy will reach around USD 57.68 billion by 2025.

- Hence, Europe is likely to dominate the bio-based adhesives market and is expected to hold the largest market share during the forecast period.

Bio-based Industry Overview

The global bio-based adhesives market is fragmented, with high competition among the key players. Major players operating in the market include Henkel AG & Co. KGaA, H.B Fuller, Arkema, Sika, and 3M company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Packaging Sector

- 4.1.2 Stringent Regulations for Conventional Adhesives in the United States

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Low Shelf Life and Performance in Comparison to Petroleum-based Adhesives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Raw Materials

- 5.1.1 Rosin

- 5.1.2 Starch

- 5.1.3 Lignin

- 5.1.4 Soy

- 5.1.5 Other Raw Materials

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Paper and Board Packaging

- 5.2.3 Healthcare

- 5.2.4 Personal Care

- 5.2.5 Woodworking and Joinery

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema (bostik)

- 6.4.3 Artimelt AG

- 6.4.4 Beardow Adams

- 6.4.5 Dow

- 6.4.6 Emsland Group

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Ingredion Incorporated

- 6.4.10 Paramelt BV

- 6.4.11 Sika AG

- 6.4.12 Solenis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Application In Engineered Wood Products

- 7.2 Other Opportunities

샘플 요청 목록