|

시장보고서

상품코드

1851644

자율형 배송 로봇 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Autonomous Delivery Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

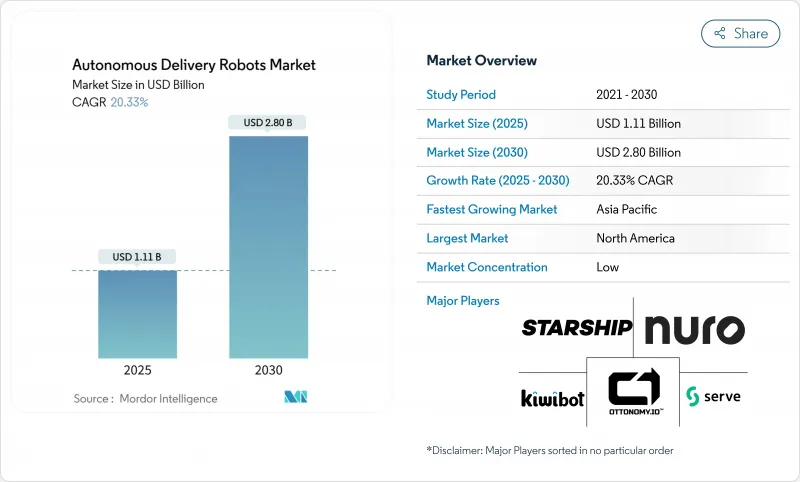

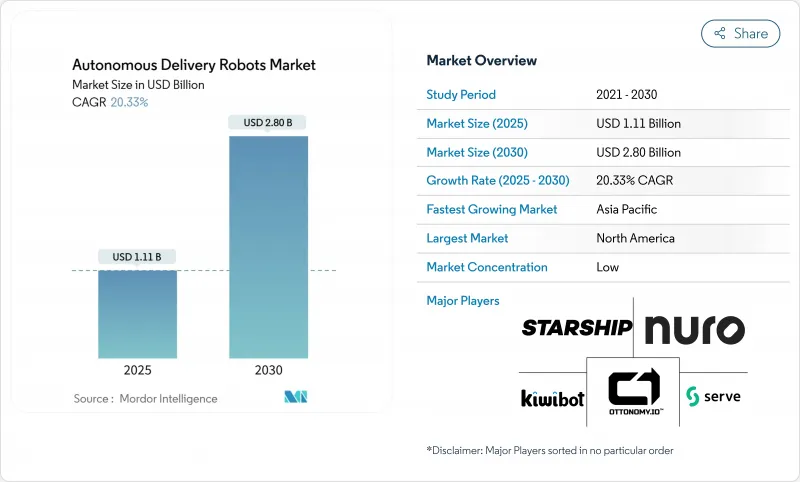

자율형 배송 로봇 시장은 현재 11억 1,000만 달러로 추정되고, 2030년에는 28억 달러에 이를 전망이며, CAGR 20.33%로 성장할 것으로 예측됩니다.

성장의 배경에는 노동력 부족의 심각화, 기술의 급속한 성숙, 사이드 워크의 배치를 용이하게 하는 지원적인 규제가 있습니다. 선도적인 물류 회사는 이 기술을 미션 크리티컬로 간주하고 있습니다. 아마존만으로도 로봇 솔루션에 의한 자동화로 2,000억 달러를 절약하고자 합니다. 북미의 2024년 점유율은 32.1%로 톱을 차지했고, 아시아태평양은 인구의 고령화로 비접촉형 헬스케어 물류 수요가 높아지는 가운데, 25%로 계속됩니다. 옥외 보도 로봇의 점유율이 58%로 압도적으로 높고, 하이브리드형 전지형 유닛이 CAGR 가장 빠른 27.8%로 성장을 지속하고 있어 도시와 실내 루트 모두에 대응하는 플랫폼이 분명히 선호되고 있음을 보여주고 있습니다. 벤처기업의 전문가가 배송 플랫폼과 제휴하여 플릿 규모를 확대하는 한편, 자동차 업계의 기존 기업은 헬스케어와 산업용 틈새 시장을 추구하기 때문에 경쟁은 격렬하게 남아 있습니다. 페이로드의 한계와 LiDAR의 고비용이라는 역풍은 여전히 계속되고 있지만, 센서의 급속한 가격 하락과 새로운 커뮤니티 참여 전략에 의해 예측 기간 동안 대응 가능한 베이스가 확대될 전망입니다.

세계의 자율형 배송 로봇 시장 동향 및 인사이트

온디맨드 식료품 납품의 급속한 확대

온디맨드 식료품 배송 서비스는 높은 주문 밀도가 기존의 운전자 비용을 상쇄하기 때문에 자율 주행 플릿에 지속 가능한 유닛 경제를 지원합니다. Kroger는 필러먼트를 가속화하고 물류 비용을 줄이기 위해 달라스 운영에 드라이버리스 트랙을 통합했습니다. 소매업체는 또한 SpartanNash의 60개 매장에서의 Simbe Robotics의 전개에서 알 수 있듯이 재고 부족과 관련된 4.5%의 수익 누출을 줄이기 위해 매장 내 선반 스캔 로봇을 통합하고 있습니다. 이러한 움직임을 합치면 식료품 체인은 로봇 공학을 시험적인 것에서 핵심 인프라로 이동시켜 라스트 원마일 로봇이 사용할 수 있는 주문량을 확대하고 있는 것을 확인할 수 있습니다.

증가하는 노동력 부족 및 임금 인플레이션

북미의 풀필먼트 센터는 심각한 인력 부족에 직면하고 있으며, 기업은 자동화된 대안으로 향하고 있습니다. 미국의 제조업에서는 2030년까지 200만 명의 노동력 부족이 예측되고 있으며, 라스트원마일 운전자의 이직률이 비용 압력을 높이고 있습니다. 산업용 로봇의 가격은 지난 10년간 50% 하락했으며, EY는 추가 하락을 예측했습니다. 도시 지역의 배송 밀도가 높아지면 사업자는 가동률 목표를 달성하고 자율 자산의 투자 회수를 가속화 할 수 있습니다.

LiDAR 및 센서 스위트의 높은 초기 비용

네비게이션 하드웨어는 종종 배송 로봇의 가장 큰 자본 항목을 차지합니다. Sonair와 같은 새로운 초음파 센서는 180도 x 180도 감지 범위를 유지하면서 센서 비용을 최대 80% 절감합니다. 카트켄의 라이더 프리 비전 스택은 이미 공공 보도에서 유익하게 작동하고 있으며 비용 효율적인 감지가 신뢰성 임계값을 충족할 수 있음을 입증합니다. 그럼에도 불구하고 이러한 새로운 센서 믹스의 규제 검증을 기다리고 광범위한 배포가 기다립니다.

부문 분석

옥외 로봇은 2024년 매출의 58%를 차지했으며, 보도에서의 실증 실험을 통해 자율형 배송 로봇 시장을 지원하고 있습니다. 이러한 이점은 확장 가능한 도시 개발을 가능하게 하는 식품 집계기 및 지역 규제 당국과의 신뢰할 수 있는 파트너십을 반영합니다. 사업자들은 계속해서 연석, 횡단보도 및 보행자와의 상호작용을 위한 섀시를 개선하여 도시 지역에서 아성을 강화하고 있습니다.

하이브리드 전지형 대응 유닛이 CAGR 27.8%로 급증하고 있는 것은 소매업이나 접객업의 고객이, 문턱을 넘은 원활한 도어 투 도어의 서비스를 요구하고 있기 때문입니다. 공급업체는 사륜 조타, 모듈식 카고 포드, 견고한 서스펜션을 통합하여 대응하고 있으며, 이 동향은 Avride가 NVIDIA를 탑재한 사륜 플랫폼으로 축발을 옮기고 있는 것에서도 분명합니다. 실내 서비스 로봇은 관리되는 복도에서 완전한 거리 등급의 감지없이 높은 자율성을 제공하는 캠퍼스와 병원에서 틈새 역할을 유지합니다.

푸드 딜리버리는 2024년 매출 점유율 42.5%를 유지했으며, 빈번한 소량 주문이 여전히 자율적 배송 로봇 시장을 지원하고 있음을 증명합니다. 높은 반복성은 자산 활용을 최적화하고, 루트 학습을 단순화하며, Server Robotics와 같은 플랫폼의 플릿 수준 수익성을 지원합니다.

식료품과 편의 분야는 소매업체가 1시간 미만의 풀필먼트를 추구하는 가운데 연간 24.3% 증가했습니다. 로봇은 온도관리된 토트백이나 도어스텝 프로토콜에 대응하여 바스켓 크기와 칩에 영향을 받는 경제성을 높입니다. 택배 서비스도 진보하고 있지만, 적재량의 상한은 아직 무거운 SKU로 제한되고 있으며, 당분간은 경량의 전자상거래 주문에 초점을 맞추었습니다.

지역 분석

북미는 2024년에 32.1%의 점유율을 유지했는데, 이는 높은 임금 인플레이션과 주 수준의 규칙이 패치워크처럼 지지되고 있음을 반영합니다. 캘리포니아 주와 텍사스 주에서는 도시 지역의 시험 도입이 가장 진행 중이며, Server Robotics는 Uber Eats의 틀 아래 2025년 말까지 2,000대의 도입을 목표로 하고 있습니다. 글러브허브(Grubhub)와 양덱스(Yandex)는 250개 캠퍼스에 배포할 계획이며, 세계에서 가장 고밀도 로봇 네트워크를 형성할 수 있습니다.

일본과 한국이 헬스케어와 스마트시티 프로그램을 가속화하고 있기 때문에 아시아태평양은 25%의 출자로 계속되고 있습니다. 한국의 보도 친화적인 법률에서는 로봇의 속도는 시속 15km, 무게는 500kg까지로, 집합 주택이나 병원에서의 상업적 시도가 해금되었습니다. 도요타의 포탈로 시스템은 병원 내에서의 사용을 상정하고 있으며, APAC가 고령화 관련 물류에 주력하고 있음을 부각하고 있습니다.

유럽은 도심지에서 디젤 밴에 대한 처벌을 부과하는 엄격한 ESG 지침에 도움을 받아 견고한 수익 기반에 기여하고 있습니다. 스타쉽 테크놀로지스는 독일과 영국에서 저속 주행 로봇에 보행자 천국을 공유하는 규제 면제하에 사업을 전개하고 있습니다. 사업자는 여전히 복잡한 여러 관할 구역의 승인 프로세스를 거치고 있기 때문에 규모의 확대는 늦었지만, 환경면에서의 돌풍도 있어 도입은 꾸준히 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아 도시에서 온디맨드 식료품 택배의 급속한 확대

- 북미의 노동력 부족 및 임금 인플레이션 증가

- EU에 있어서 ESG 주도의 라스트원마일 제로에미션 차의 추진

- 고령화가 가속하는 일본에서 원내 배송의 자동화

- 중동의 고급 호텔에 있어서 24시간 365일 연락 불필요 서비스 수요

- 5G 엣지 컴퓨팅이 고밀도 도시 코어에서 로봇의 자율성 향상 도모

- 시장 성장 억제요인

- 미국 각 도시에서의 보도 규제의 변동

- 적재량의 제한이 벌크화물의 ROI 제한

- LiDAR과 센서 스위트의 높은 초기 비용

- 미국 도시에서의 파괴행위 및 도난 사건

- 밸류체인 분석

- 기술의 전망

- 매크로 동향 분석의 영향 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 및 자금 조달 분석

제5장 시장 규모 및 성장 예측

- 로봇 유형별

- 실내 서비스 로봇

- 아웃도어 자율형 배송 로봇

- 하이브리드 전지형 대응 로봇

- 용도별

- 푸드 딜리버리

- 식료품 및 편의점 납품

- 소포 및 택배(전자상거래)

- 헬스케어 공급 및 의약품

- 접객 룸 서비스

- 산업 캠퍼스 물류

- 적재 용량별

- 10kg 미만

- 10-25 kg

- 25-80 kg

- 80kg 이상

- 최종 사용자 업계별

- 의료시설

- 접객 및 호텔

- 소매 및 전자상거래 물류

- 기업 및 대학 캠퍼스

- 공항 및 교통 허브

- 스마트 시티 및 지자체 기관

- 컴포넌트별

- 하드웨어

- 소프트웨어 및 AI 스택

- 애프터 서비스 및 플리트 매니지먼트

- 추진 유형별

- 전동 배터리

- 수소 연료전지

- 하이브리드 에너지 하베스팅

- 자율성 레벨별

- 반자율형(인간 감시형)

- 완전 자율형(레벨 4)

- 그룹 및 클러스터형 자율형 네트워크(레벨 5)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 아프리카

- 남아프리카

- 케냐

- 아시아태평양

- 중국

- 호주

- 일본

- 싱가포르

- 인도

- 한국

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Starship Technologies

- Nuro Inc.

- Kiwibot

- Serve Robotics Inc.

- Ottonomy.IO

- Relay Robotics Inc.

- Postmates Inc.(Serve by Uber)

- Aethon Inc.

- Segway Robotics Inc.

- Neolix

- Udelv Inc.

- JD Logistics(Jian Robots)

- Alibaba Cainiao(Xiaomanlv)

- Yandex Rover

- FedEx Roxo

- Amazon Scout

- Rival Robotics Inc.

- TeleRetail(Aitonomi AG)

- Daxbot

- Locus Robotics(campus variant)

- Kiwi Campus SAS

제7장 시장 기회 및 향후 전망

AJY 25.11.24The autonomous delivery robots market is currently valued at USD 1.11 billion and is projected to reach USD 2.8 billion by 2030, advancing at a 20.33% CAGR.

Growth is grounded in rising labor shortages, swift technological maturation, and supportive regulations that ease sidewalk deployments. Major logistics spenders continue to view the technology as mission-critical; Amazon alone targets USD 200 billion of automation savings through robotic solutions. North America leads adoption thanks to 32.1% 2024 share, while Asia-Pacific follows at 25% as aging populations increase demand for contact-free healthcare logistics. Outdoor sidewalk robots dominate with 58% share, and hybrid all-terrain units post the fastest 27.8% CAGR, signaling a clear preference for platforms that handle both urban and indoor routes. Competitive activity remains intense as venture-backed specialists scale fleets in partnership with delivery platforms, while automotive incumbents pursue healthcare and industrial niches. Headwinds tied to payload limits and high LiDAR costs persist, yet rapid sensor price declines and new community-engagement strategies point to a wider addressable base over the forecast horizon.

Global Autonomous Delivery Robots Market Trends and Insights

Rapid Expansion of On-Demand Grocery Delivery

On-demand grocery services now anchor sustainable unit economics for autonomous fleets because high order density offsets traditional driver costs. Kroger integrated driverless trucks into its Dallas operations to accelerate fulfillment and trim logistics spend. Retailers also embed in-store shelf-scanning robots to reduce the documented 4.5% revenue leakage linked to stock-outs, as shown by Simbe Robotics' rollout across 60 SpartanNash stores. Together these moves confirm that grocery chains are shifting robotics from pilot status to core infrastructure, widening order volumes available to last-mile robots.

Rising Labor Shortages and Wage Inflation

North American fulfillment centers face acute staffing gaps that push companies toward automated alternatives. The U.S. manufacturing sector projects a 2 million-worker shortage by 2030, and last-mile driver turnover amplifies cost pressure. Falling industrial robot prices-down 50% in the past decade-and further declines predicted by EY strengthen the investment case. High urban delivery density then allows operators to hit utilization targets that yield faster payback on autonomous assets.

High Upfront Cost of LiDAR and Sensor Suites

Navigation hardware often accounts for the largest capital item in a delivery robot. Emerging ultrasonic alternatives such as Sonair cut sensor spend by up to 80% while keeping a 180 X 180 degree detection envelope. Cartken's lidar-free vision stack already operates profitably on public sidewalks, proving that cost-efficient sensing can meet reliability thresholds. Even so, broad rollout waits on regulatory validation of these novel sensor mixes.

Other drivers and restraints analyzed in the detailed report include:

- ESG-Driven Push for Zero-Emission Last-Mile Vehicles

- Aging Population Spurring Intra-Hospital Delivery Automation

- Vandalism and Theft Incidents in South-American Metros

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Outdoor robots generated 58% of 2024 revenue, anchoring the autonomous delivery robots market through well-tested sidewalk operations. This dominance reflects reliable partnerships with food aggregators and local regulators that allow scalable city deployments. Operators continue to refine chassis for curbs, crosswalks, and pedestrian interaction, reinforcing their urban stronghold.

Hybrid all-terrain units expand rapidly at 27.8% CAGR because retail and hospitality customers ask for seamless door-to-door service that crosses thresholds. Suppliers respond by integrating four-wheel steering, modular cargo pods, and ruggedized suspension, a trend evident in Avride's pivot to NVIDIA-powered four-wheel platforms. Indoor service robots maintain niche roles in campuses and hospitals where controlled corridors permit higher autonomy without full street-grade sensing.

Food delivery retained 42.5% revenue share in 2024, proving that frequent small-ticket orders still underpin the autonomous delivery robots market. High repetition optimizes asset utilization and simplifies route learning, supporting fleet-level profitability for platforms such as Serve Robotics.

Grocery and convenience segments rise 24.3% annually as retailers chase sub-hour fulfillment. Robots accommodate temperature-controlled totes and door-step protocols that boost basket size and tip-influenced economics. Parcel courier services also advance, but payload ceilings still limit heavier SKUs, keeping focus on lightweight e-commerce orders for now.

The Autonomous Delivery Robots Market Report is Segmented by Robot Type (Indoor, Outdoor, Hybrid), Application (Food, Grocery, Parcel, and More), Load Capacity (Up To 10kg, 10-25kg, 25-80kg, Above 80kg), End-User (Healthcare, Hotels, Retail, and More), Component (Hardware, Software and More), Propulsion (Electric, Hydrogen, Hybrid), Level of Autonomy, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 32.1% share in 2024, reflecting high wage inflation and a supportive patchwork of state-level rules. California and Texas host the largest urban pilots, with Serve Robotics targeting 2,000 units by year-end 2025 under an Uber Eats framework. College-town deployments add scale; Grubhub and Yandex plan rollouts across 250 campuses, potentially forming the world's densest robot network.

Asia-Pacific followed with a 25% stake as Japan and South Korea accelerate healthcare and smart-city programs. South Korea's sidewalk-friendly legislation caps robot speed at 15 km/h and weight at 500 kg, unlocking commercial trials in apartment complexes and hospitals. Toyota's Potaro system shows the model for intra-hospital use, highlighting APAC's focus on aging-related logistics.

Europe contributes a solid revenue base, aided by stringent ESG mandates that penalize diesel vans in city centers. Starship Technologies operates in Germany and the UK under regulatory exemptions that let slow-moving robots share pedestrian zones. Operators still navigate complex, multi-jurisdiction approval processes, slowing scale, yet the environmental tailwinds keep adoption on a steady path.

- Starship Technologies

- Nuro Inc.

- Kiwibot

- Serve Robotics Inc.

- Ottonomy.IO

- Relay Robotics Inc.

- Postmates Inc. (Serve by Uber)

- Aethon Inc.

- Segway Robotics Inc.

- Neolix

- Udelv Inc.

- JD Logistics (Jian Robots)

- Alibaba Cainiao (Xiaomanlv)

- Yandex Rover

- FedEx Roxo

- Amazon Scout

- Rival Robotics Inc.

- TeleRetail (Aitonomi AG)

- Daxbot

- Locus Robotics (campus variant)

- Kiwi Campus SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid expansion of on-demand grocery delivery in urban Asia

- 4.2.2 Rising labor shortages and wage inflation in North-American fulfilment

- 4.2.3 ESG-driven push for zero-emission last-mile vehicles in the EU

- 4.2.4 Aging population spurring intra-hospital delivery automation in Japan

- 4.2.5 24/7 contact-free services demand in Middle-East luxury hotels

- 4.2.6 5G edge-compute enabling higher robot autonomy in dense city cores

- 4.3 Market Restraints

- 4.3.1 Municipal sidewalk regulation variability in US cities

- 4.3.2 Limited payload capacity restricting ROI for bulk goods

- 4.3.3 High upfront cost of LiDAR and sensor suites

- 4.3.4 Vandalism and theft incidents in S-American metros

- 4.4 Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Impact of Macro-Trend Analysis

- 4.7 Regulatory Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Robot Type

- 5.1.1 Indoor Service Robots

- 5.1.2 Outdoor Autonomous Delivery Robots

- 5.1.3 Hybrid All-Terrain Robots

- 5.2 By Application

- 5.2.1 Food Delivery

- 5.2.2 Grocery and Convenience Deliveries

- 5.2.3 Parcel and Courier (E-commerce)

- 5.2.4 Healthcare Supply and Medication

- 5.2.5 Hospitality Room-Service

- 5.2.6 Industrial Campus Logistics

- 5.3 By Load Capacity

- 5.3.1 Up to 10 kg

- 5.3.2 10 - 25 kg

- 5.3.3 25 - 80 kg

- 5.3.4 Above 80 kg

- 5.4 By End-User Industry

- 5.4.1 Healthcare Facilities

- 5.4.2 Hospitality and Hotels

- 5.4.3 Retail and E-commerce Logistics

- 5.4.4 Corporates and Academic Campuses

- 5.4.5 Airports and Transportation Hubs

- 5.4.6 Smart Cities and Municipal Agencies

- 5.5 By Component

- 5.5.1 Hardware

- 5.5.2 Software / AI Stack

- 5.5.3 After-Sales Services and Fleet Management

- 5.6 By Propulsion Type

- 5.6.1 Electric Battery

- 5.6.2 Hydrogen Fuel Cell

- 5.6.3 Hybrid Energy Harvesting

- 5.7 By Level of Autonomy

- 5.7.1 Semi-Autonomous (Human-Supervised)

- 5.7.2 Fully Autonomous (Level 4)

- 5.7.3 Swarm/Clustered Autonomous Network (Level 5)

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Chile

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.4 Middle East

- 5.8.4.1 United Arab Emirates

- 5.8.4.2 Saudi Arabia

- 5.8.4.3 Turkey

- 5.8.5 Africa

- 5.8.5.1 South Africa

- 5.8.5.2 Kenya

- 5.8.6 Asia-Pacific

- 5.8.6.1 China

- 5.8.6.2 Australia

- 5.8.6.3 Japan

- 5.8.6.4 Singapore

- 5.8.6.5 India

- 5.8.6.6 South Korea

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Starship Technologies

- 6.4.2 Nuro Inc.

- 6.4.3 Kiwibot

- 6.4.4 Serve Robotics Inc.

- 6.4.5 Ottonomy.IO

- 6.4.6 Relay Robotics Inc.

- 6.4.7 Postmates Inc. (Serve by Uber)

- 6.4.8 Aethon Inc.

- 6.4.9 Segway Robotics Inc.

- 6.4.10 Neolix

- 6.4.11 Udelv Inc.

- 6.4.12 JD Logistics (Jian Robots)

- 6.4.13 Alibaba Cainiao (Xiaomanlv)

- 6.4.14 Yandex Rover

- 6.4.15 FedEx Roxo

- 6.4.16 Amazon Scout

- 6.4.17 Rival Robotics Inc.

- 6.4.18 TeleRetail (Aitonomi AG)

- 6.4.19 Daxbot

- 6.4.20 Locus Robotics (campus variant)

- 6.4.21 Kiwi Campus SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment