|

시장보고서

상품코드

1683095

미국의 종자 처리 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)United States Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

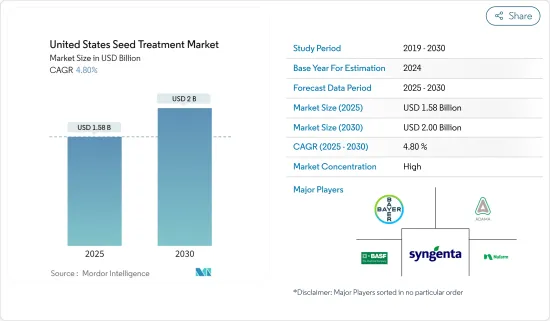

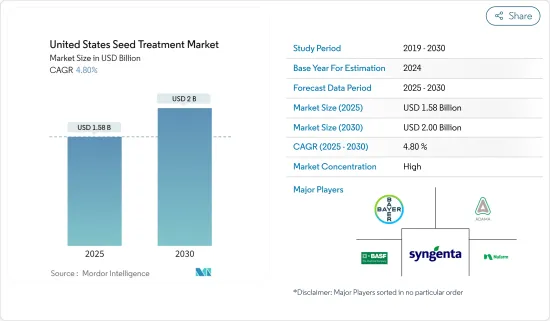

미국의 종자 처리 시장 규모는 2025년에 15억 8,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR은 4.8%로 전망되며, 2030년에는 20억 달러에 달할 것으로 예측되고 있습니다.

미국의 종자 처리 시장은 식량 안보에 대한 수요 증가, 종자 처리 제품의 채용률 상승, 종자 처리의 이점에 대한 농업 종사자의 의식 증가 등의 요인에 의해 크게 성장하고 있습니다. 종자 처리 제품은 매년 미국에서 심어지는 옥수수의 거의 모든 에이커에 적용되며 미국 농업 종사자가 재배하는 약 800억 달러 상당의 작물을 지원하는 데 도움이 됩니다.

인구가 계속 증가하는 가운데 농업 생산성을 높이고 식량 안보를 확보할 필요성이 높아지고 있습니다. 이러한 목적을 달성하기 위해 종자 처리는 중요한 역할을 수행합니다. 종자를 처리함으로써 농업 종사자는 작물의 성장을 방해하고 수율을 감소시키는 다양한 질병과 해충, 환경 스트레스로부터 종자를 보호할 수 있습니다. 종자 처리는 초기 방어선을 제공하고 성장의 중요한 단계에서 종자와 묘목을 보호합니다.

미국 종자 처리 시장 동향

고품질 종자의 비용 상승

하이브리드 및 유전자 변형 종자와 관련된 높은 비용은 종자 처리 시장의 성장을 가속하는 주요 요인 중 하나입니다. 종자 처리는 훈증과 농약의 잎 표면 살포에 대한 규제 문제가 증가하고 있기 때문에 농업 종사자가 고품질의 종자에 대한 투자를 보호하는 수단으로 검토되고 있습니다. 원하는 농학적 특성을 지닌 고품질 종자에 대한 수요가 증가함에 따라 종자 비용이 상승할 것으로 예상됩니다. 기업과 농업 종사자 모두 고품질의 종자를 보존하기 위해 종자 처리 솔루션에 비용을 지불할 준비가 되어 있습니다. GM 씨앗의 대부분은 비용이 많이 들고 화학 처리로 처리되기 때문에 GM 작물의 재배 면적이 증가하여 시장 성장에 긍정적인 영향을 미칩니다.

처리된 종자 사용 증가

농작물 소비량의 급격한 증가로 인한 높은 수율에 대한 수요는 미국에서 종자 처리 시장 수요를 증가시키고 있습니다. 농장 규모의 확대와 윤작의 감소가 종자 처리 제품 수요 증가로 이어지는 주요 요인입니다. 옥수수는 미국에서 재배되는 주요 작물 중 하나이며, 2018년에는 약 3,310만 헥타르가 수확되었습니다. 미국에서는 옥수수 종자의 약 90%가 종자 처리되고 있으며, 종자 처리의 성장률은 큽니다.

미국 종자 처리 산업 개요

주요 시장 진출 기업이 가장 널리 채용하고 있는 전략에는 신제품의 출시(다른 모든 전략 시장 점유율의 41%로 채용)가 있으며, 이어 인수(20% 초과)입니다. 연구 개발 확대, 파트너십 및 합작 투자는 시장의 주요 기업이 채택한 다른 중요한 전략의 일부입니다. 농업에서 종자 처리의 의의를 이해하기 위한 조사를 실시하면서, 보다 넓은 지역을 커버하기 위해 판매팀을 확대하고 있는 주요 기업에 의해 대면적의 기회에 대처하기 위한 전략적 파트너십의 라이선스 계약이나 판매 계약이 이용되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자 및 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 제품 유형별

- 살충제

- 살균제

- 살선충제

- 작물 유형별

- 곡물

- 지방종자 및 콩류

- 과일 및 채소

- 상업 작물

- 잔디 및 관상용 작물

제6장 경쟁 구도

- 가장 채용된 전략

- 시장 점유율 분석

- 기업 프로파일

- Syngenta International AG

- Bayer CropScience AG

- BASF SE

- Corteva Agriscience

- Adama Agricultural Solutions Ltd

- Germains Seed Technology

- UPL Limited

- Incotec Group BV

제7장 시장 기회 및 향후 동향

AJY 25.03.31The United States Seed Treatment Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 2.00 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

The seed treatment market in the United States has been witnessing substantial growth driven by factors such as increasing demand for food security, rising adoption of seed treatment products, and growing awareness among farmers about the benefits of seed treatment. Seed treatment products, applied to nearly every acre of corn planted in the United States every year, helped support nearly USD 80 billion worth of crops grown by the American farmers.

As the population continues to grow, there is a greater need to enhance agricultural productivity and ensure food security. Seed treatments play a crucial role in achieving these objectives. By treating seeds, farmers can protect them from various diseases, pests, and environmental stresses, which can hinder crop growth and reduce yields. Seed treatments provide an early line of defense and protect seeds and young seedlings during critical stages of growth.

US Seed Treatment Market Trends

Increase in Cost of High-quality Seeds

High costs associated with hybrids and genetically modified seeds are among the major factors driving the growth of the seed treatment market. Seed treatment is being increasingly considered by farmers as a mode to protect investments made on good-quality seeds, due to an increase in regulatory issues relating to fumigation, as well as the foliar application of pesticides. The cost of seeds is expected to increase, owing to an increase in the demand for high-quality seeds with desirable agronomic traits. Both companies and farmers are ready to spend on seed-treatment solutions, in order to save high-quality seeds. Since most of the GM seeds are costly and treated with chemical treatments, there is an increase in the area under GM crops, which is positively affecting the market growth.

Increasing Usage of Treated Seeds

The demand for higher yield due to the rapid increase in the consumption of crops has increased the demand for the seed treatment market in the United States. Increasing farm size and decreasing crop rotation are the major factors that lead to an increase in the demand for seed-treatment products. Corn is one of the major crops grown in the United States, with around 33.1 million hectares harvested in 2018. In the United States, around 90% of the corn seeds are treated with seed treatment, and there is a significant percentage of growth in seed treatment.

US Seed Treatment Industry Overview

The most widely adopted strategies by major market players include new product launches (which is being adopted 41% times of all other strategies market share), followed by acquisitions (over 20% of the time). R&D expansion and partnerships or joint ventures are some of the other important strategies, followed by major companies in the market. Strategic partnership licensing and distribution agreements to address broad-acre opportunities are being used by top players, who are expanding their sales teams for larger geographic coverage, with researches on understanding the significance of seed treatment in agriculture.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Insecticides

- 5.1.2 Fungicides

- 5.1.3 Nematicides

- 5.2 Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Oilseeds and Pulses

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial crops

- 5.2.5 Turf and Ornamentals

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta International AG

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 Corteva Agriscience

- 6.3.5 Adama Agricultural Solutions Ltd

- 6.3.6 Germains Seed Technology

- 6.3.7 UPL Limited

- 6.3.8 Incotec Group BV