|

시장보고서

상품코드

1683225

전기 및 전자 테스트 장비 시장 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Electrical and Electronic Test Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

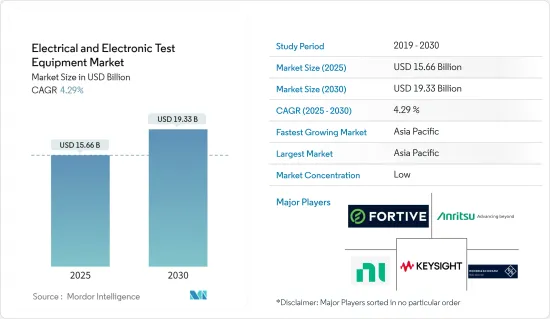

전기 및 전자 테스트 장비 시장 규모는 2025년에 156억 6,000만 달러에 달했으며, 예측 기간(2025-2030년) 동안 4.29%의 CAGR로 2030년에는 193억 3,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 전기 및 전자 테스트 장비는 전기 및 전자 시스템의 다양한 측면을 측정, 테스트, 진단 및 문제 해결에 사용되는 도구입니다. 이 장비는 전자 장치, 회로 및 구성 요소의 적절한 기능, 안전 및 성능을 보장하는 데 도움이 됩니다. 테스트 장비는 실시간 환경을 최대한 가깝게 시뮬레이션하여 테스트 대상 장치(DUT)를 검증하는 데 도움이 됩니다.

- 테스트 장비는 디바이스 자체만큼이나 중요합니다. 모든 전자 장비는 가열, 습기, 충격 또는 진동으로 인해 시간이 지남에 따라 마모되는 경향이 있습니다. 이는 성능 저하로 이어질 수 있습니다. 따라서 모든 전자 테스트 시설에는 간단한 멀티미터든 복잡한 오실로스코프든 필요한 장비가 있어야 합니다.

- 전자 제품의 설계, 제조 또는 수리에서 정확성과 속도에 대한 요구가 증가하는 것은 산업 전반에 걸쳐 전기 및 전자 테스트 장비에 대한 수요를 증가시키는 주요 요인 중 하나입니다. 전기 자동차, 자율 주행, 5G와 같은 새로운 커넥티드 전자 기기와 신흥 첨단 기술의 채택이 증가하면서 시장 수요도 증가하고 있습니다.

- 예를 들어, 배터리 전기 자동차의 경우 배터리 손상이 제어할 수 없는 과열로 이어지는 열 폭주로 인해 화재가 발생할 위험이 있습니다. 게다가 화재가 발생한 많은 전기 자동차(EV)는 NMC라는 온도에 더 민감한 배터리 화학 물질을 사용했습니다. 온도에 더 민감한 배터리를 사용하기 위해 배터리 팩 수준에서 열을 적절히 냉각할 수 있는 설계 조치가 취해지지 않았습니다. 제조업체와 엔지니어는 엄격한 전기 및 전자 테스트 관행을 채택함으로써 전기 자동차의 성능과 안전성을 최적화할 수 있습니다.

- 또한 자율주행의 보급이 증가함에 따라 자율주행 시스템이 신뢰할 수 있고 안전하며 복잡한 환경에서 순식간에 결정을 내릴 수 있는지 확인하기 위한 테스트 장비의 사용이 요구될 것입니다. 이러한 테스트 프로세스는 자율주행 차량의 성능과 안전성에 대한 높은 신뢰도를 바탕으로 도로에 자율주행 차량을 출시하는 데 필수적입니다.

- 다른 시장과 마찬가지로 전기 및 전자 테스트 장비 시장도 극복해야 할 과제가 있으며, 치열한 가격 경쟁은 주문자 상표 부착 생산업체(OEM)의 주요 문제 중 하나였습니다. 인도와 같은 대부분의 개발도상국은 가격에 매우 민감하기 때문에 테스트 서비스 가격을 상당히 낮게 유지합니다. 이로 인해 부정확한 측정을 제공하는 오래된 리퍼브, 보정되지 않은 계측기가 시장에 많이 유통되고 있습니다.

- 신제품을 개발하려면 막대한 자본이 필요하기 때문에 비용 증가와 신제품에 대한 저항도 또 다른 문제입니다. 조달과 관련해서는 고객이 이러한 장비에 대해 높은 가격을 지불하지 않으려는 경향이 있으며, 때로는 우선 순위가 낮은 품목으로 간주되기도 합니다.

- COVID-19 팬데믹은 반도체 제조 시장 전체에 수요 및 공급의 양면에서 영향을 미쳤습니다. 전 세계적인 봉쇄와 반도체 공장 폐쇄는 공급 부족으로 이어졌습니다. 이러한 영향은 시장에도 반영되었습니다. 그러나 이러한 영향은 대부분 단기적인 것이었습니다. 자동차 및 반도체 부문을 지원하기 위한 각국 정부의 예방 조치가 시장을 되살리는 데 도움이 되었습니다.

전기 및 전자 테스트 장비 시장 동향

반도체와 컴퓨팅이 최대의 최종 사용자 산업이 될 전망

- 반도체 제조 기업들이 반도체 소자의 성능 동작 속도를 향상시키고 비용을 절감하기 위해 자동화 테스트 장비(ATE)를 도입하는 것이 시장 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

- 반도체 자동화 테스트 장비(ATE)는 저항기, 커패시터, 인덕터와 같은 필수 부품부터 복잡한 집적 회로(IC), 인쇄 회로 기판(PCB), 완전 조립된 전자 시스템에 이르기까지 다양한 전자 장치 및 시스템을 테스트할 수 있습니다. ATE는 전자 제조 부문에서 전자 부품과 시스템을 제조 후 검사하는 데 광범위하게 사용되고 있습니다. 반도체 산업의 성장세를 고려할 때 ATE에 대한 수요는 상당히 증가할 것으로 예상됩니다.

- 반도체 산업은 현대 기술의 기본 구성 요소 역할을 하는 반도체와 함께 급속도로 확장되고 있습니다. SIA에 따르면 2023년 2분기 전 세계 반도체 매출은 1,245억 달러로 2023년 1분기 대비 4.7% 증가했습니다. 또한 2030년까지 전 세계 반도체 제조 능력에 대한 수요가 56% 급증할 것으로 예상하고 있습니다. 이러한 미래 발전은 전자 테스트 장비에 대한 상당한 수요를 창출할 것으로 예상됩니다.

- 이 시장에서는 IoT, 빅 데이터, 인공지능(AI)과 같은 기술의 등장으로 인해 칩 전력 성능, 효율성, 비용, 면적, 출시 기간을 빠르고 크게 개선해야 한다는 요구가 증가하고 있습니다. 이러한 고객 요구와 선호도의 변화는 반도체 테스트 장비 시장의 성장에 중요한 동력 중 하나가 될 것으로 예상됩니다.

- SIA는 2023년 6월에 2023년 전 세계 반도체 매출 예측을 공식적으로 지지했습니다. 이 전망에 따르면 2023년 전 세계 연간 매출은 5,151억 달러로 2022년 매출 총액인 5,741억 달러보다 감소할 것으로 예상됩니다. 2024년 세계 매출은 5,760억 달러에 이르고, 산업 역사상 최고가 될 전망입니다. 정부의 우호적인 전략과 반도체 칩에 대한 수요가 증가함에 따라 반도체 설비에 대한 지출이 증가하고 있으며, 세계적으로 새로운 파운드리 설립에 대한 관심이 높아지고 있습니다. 이러한 칩 생산량 증가는 전자 테스트 장비에 대한 수요를 견인할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

- 아시아태평양 지역은 중국, 일본, 한국, 인도의 광범위한 제조 기지에 힘입어 반도체 및 전자 산업을 크게 지배하고 있으며, 전자 산업의 최종 조립 분야에서도 빠르게 성숙하고 있습니다.

- Foxconn Technology Group, Megatron Asia Pacific Ltd 등 대기업이 인도에서 공장 설립을 진행하고 있습니다. IBEF에 따르면 인도는 2025-2026년까지 3,000억 달러 상당의 전자제품 제조와 1,200억 달러의 수출을 달성할 것을 약속하고 있습니다. 또한 2023-2024년도 연방예산에서는 전자정보기술성에 1,654억 9,000만 루피(20억 달러)가 할당되어 있으며, 이는 매년 약 40% 증가하고 있습니다.

- 이 지역의 테스트 및 검사 활동이 증가함에 따라 전기 테스트 장비에 대한 상당한 수요가 창출될 것으로 예상됩니다. 이전에는 대부분의 지역 기업들이 자체적으로 테스트 및 인증 작업을 수행했습니다. 그러나 중국의 강제 인증 규정으로 인해 엄격한 규제 표준의 필요성이 더욱 강조되고 있습니다. 이로 인해 테스트 서비스의 아웃소싱이 증가하면서 테스트 서비스 업체들 사이에서 테스트 장비에 대한 수요가 증가하고 있습니다.

- 소비자 가전 산업을 제외하고는 저가 통신사가 이 지역을 지배하고 있습니다. 따라서 대부분의 검사 및 서비스 활동이 아웃소싱으로 이루어지고 있습니다. 이로 인해 싱가포르는 유지보수 및 검사 서비스의 지역 허브로 부상했습니다. 싱가포르에서 활동하는 연합 업체들은 20년 넘게 이 지역에서 지배력을 유지해 왔습니다. 그러나 인도네시아, 베트남, 태국과 같은 국가들이 싱가포르의 지배력에 도전하고 있습니다.

- 또한 이 지역은 요코가와(일본), Advantest Corp(일본), Anritsu Corporation(일본), Rigol Technologies(중국), ScienceTech Technologies(인도) 등 여러 주요 기업의 거점이 되고 있습니다. 이 기업들은 이 지역의 다양한 다른 기업들과 함께 제품 혁신에 지속적으로 참여하여 다양한 산업 분야에 걸쳐 솔루션을 제공하고 있습니다.

- 2022년 8월, Advantest Corp.는 고속 SoC 테스터의 대량 전시 평가를 위해 로데슈바르즈 RTP 고성능 오실로스코프와 협력했습니다. 이 파트너십에 따라 이 회사는 최신 요구 사항을 충족하기 위해 제품의 품질을 향상시키는 것을 목표로 하고 있습니다. 지역 기업들의 이러한 이니셔티브는 시장 성장을 촉진할 것으로 기대됩니다.

- 또한 고전압 송전선 및 발전소 건설과 같은 여러 인프라 프로젝트가 이 지역의 전기 테스트 장비에 대한 수요를 견인할 것으로 예상됩니다. 예를 들어 2022년 8월 중국의 국소비자용전자장비망은 2022년 하반기에 1,500억 위안(220억 달러) 이상의 자금을 UHV송전선에 투입할 계획입니다.8개의 새로운 UHV 프로젝트가 건설되면 태양광, 풍력, 수력 발전소가 주로 위치한 중국의 극서부 지역과 주요 도시를 연결하여 시장 성장을 더욱 촉진할 것으로 예상됩니다.

전기 및 전자 테스트 장비 시장 개요

전기 및 전자 테스트 장비 시장은 Fortive Corporation, Keysight Technologies Inc., Rohde & Schwarz GmbH & Co. KG 등 주요 기업이 참가하고 있어 세분화가 진행되고 있는 것이 특징입니다. KG, National Instruments Corporation, Anritsu Corporation 등입니다. 시장 참여자들은 제품 포트폴리오를 강화하고 지속 가능한 경쟁 우위를 확보하기 위해 전략적으로 파트너십과 인수를 활용하고 있습니다.

2023년 8월 Yokogawa Electric Corporation의 자회사인 Yokogawa Test & Measurement Corporation은 고정밀 오실로스코프 DLM5,000HD 시리즈를 발표했습니다. DLM5,000HD 시리즈는 DLM5,000 시리즈를 더욱 진화시킨 오실로스코프로, 주파수대폭 500MHz와 350MHz의 모델을 라인업하고 있습니다. 이 모델들은 정밀한 파형 분석을 위해 향상된 분해능을 제공하고 설정과 작동을 간소화하는 사용자 친화적인 기능을 통합합니다.

2023년 6월 Advantest Corporation은 애리조나 주립 대학(ASU)과 협력하여 NXP와 공동으로 새로운 테스트 엔지니어링 프로그램을 설립할 것이라고 발표했습니다. 이 프로그램의 커리큘럼은 처음에 ASU의 아이라 및 풀턴 공과대학 교수진에 의해 개발되었으며, 어드밴테스트가 고안한 실험실 실험을 통해 더욱 강화되었습니다. 이러한 실험은 어드밴테스트와 NXP가 공동으로 관리하여 중요한 교육적 이정표가 되었습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 산업 밸류체인 분석

- 주요 거시 경제 동향의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 테스트 및 측정 장비의 필요성으로 이어지는 기술 발전

- 전기자동차와 하이브리드차의 신흥 동향

- 시장의 과제 및 억제요인

- 가격 민감성 및 렌탈 서비스에 대한 선호도 증가

제6장 시장 세분화

- 유형별

- 반도체 자동화 테스트 장비(ATE)

- 무선 주파수(RF) 테스트 장비

- 디지털 테스트 장비

- 전기 및 환경테스트

- 데이터 수집(DAQ)

- 최종 사용자 산업별

- 통신

- 반도체와 컴퓨팅

- 항공우주 및 방위

- 소비자 가전

- 전기자동차(EV)

- 기타

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 벤더의 시장 점유율 분석

제8장 경쟁 구도

- 기업 프로파일

- Fortive Corporation

- Keysight Technologies Inc.

- Rohde & Schwarz GmbH & Co. KG

- National Instruments Corporation

- Anritsu Corporation

- Teledyne Lecroy(Teledyne Technologies Incorporated)

- Yokogawa Test & Measurement Corporation(Yokogawa Electric Corporation)

- Teradyne Inc.

- Chauvin Arnoux Group

- Advantest Corporation

제9장 투자 분석

제10장 시장 기회와 앞으로의 동향

HBR 25.04.01The Electrical and Electronic Test Equipment Market size is estimated at USD 15.66 billion in 2025, and is expected to reach USD 19.33 billion by 2030, at a CAGR of 4.29% during the forecast period (2025-2030).

Key Highlights

- Electrical and electronic test equipment are tools used to measure, test, diagnose, and troubleshoot various aspects of electrical and electronic systems. This equipment helps ensure the proper functioning, safety, and performance of electronic devices, circuits, and components. Test equipment helps simulate the real-time environment as closely as possible to verify the device under test (DUT).

- Testing equipment is as important as the device itself. All electronic equipment tends to wear out over time due to heating, moisture, shock, or vibration. This can lead to performance degradation. Therefore, every electronic testing facility must have the required equipment, whether a simple multimeter or a complex oscilloscope.

- The increasing need for accuracy and speed in designing, manufacturing, or repairing electronic products is one of the major factors driving the demand for electric and electronic test equipment across industries. The increase in the adoption of new and connected electronic devices and emerging advanced technologies, such as electric vehicles, autonomous driving, and 5G, is also fueling the demand in the market.

- For instance, the risk associated with battery-electric vehicles is catching fire due to thermal runaway, where damage to the battery leads to uncontrollable overheating. Moreover, many electric vehicles (EVs) that caught fire used more temperature-sensitive battery chemistry called NMC. To use a more temperature-sensitive battery, no design measures were taken to ensure that it's thermally cooled properly at the battery pack level. By employing rigorous electrical and electronic testing practices, manufacturers and engineers can optimize the performance and safety of electric vehicles.

- Moreover, the increasing deployment of autonomous driving will demand the use of test equipment to ensure that autonomous driving systems are reliable, safe, and capable of making split-second decisions in complex environments. These testing processes are essential to bring autonomous vehicles to the roads with high confidence in their performance and safety.

- Like other markets, the electrical and electronics test equipment market also has some challenges to overcome, and fierce price competition has been one of the key issues for original equipment manufacturers (OEMs). Most developing nations, such as India, are very price-sensitive, which makes them keep the prices of testing services significantly low. This further leads to the presence of many old, refurbished, non-calibrated instruments operating in the market that provide inaccurate measurements.

- Resistance toward increased cost and new products is another issue, as developing a new product requires huge capital. When it comes to procurement, it has been observed that the customers are not willing to pay well for such equipment, and sometimes it is considered the last priority item.

- The COVID-19 pandemic influenced the overall semiconductor manufacturing market on both the demand and supply sides. The global lockdowns and closure of semiconductor plants led to a supply shortage. The effects were also reflected in the market. However, many of these effects were short-term. Precautions by governments worldwide to support the automotive and semiconductor sectors helped revive the market.

Electrical and Electronic Test Equipment Market Trends

Semiconductors and Computing are Expected to be the Largest End-user Industry

- The adoption of automated test equipment (ATE) by semiconductor manufacturing firms to improve performance operational speed and reduce costs of semiconductor devices is anticipated to have a favorable impact on market growth.

- Semiconductor automated test equipment (ATE) is capable of testing a diverse array of electronic devices and systems, ranging from essential components such as resistors, capacitors, and inductors to complex integrated circuits (ICs), printed circuit boards (PCBs), and fully assembled electronic systems. ATE is extensively employed in the electronic manufacturing sector to examine electronic components and systems post-fabrication. Given the rising semiconductor industry, the demand for ATE is anticipated to escalate considerably.

- The semiconductor industry is experiencing a rapid expansion, with semiconductors serving as the fundamental components of contemporary technology. According to SIA, the global sales of semiconductors amounted to USD 124.5 billion in Q2 2023, marking a 4.7% rise from Q1 2023. Additionally, it foresees a 56% surge in the worldwide demand for semiconductor manufacturing capacity by 2030. Such futuristic developments are expected to create a significant need for electronic testing equipment.

- The market is witnessing an increase in demand for rapid and significant improvements in chip power performance, efficiency, cost, area, and time to market due to the emergence of technologies such as the IoT, Big Data, and artificial intelligence (AI). This shift in customer demands and preferences is expected to be one of the critical drivers for the growth of the semiconductor testing equipment market.

- SIA officially supported the WSTS Spring 2023 worldwide semiconductor sales forecast in June 2023. The forecast estimated annual global sales to amount to USD 515.1 billion in 2023, a decrease from the 2022 sales total of USD 574.1 billion. In 2024, global sales are expected to reach USD 576.0 billion, the highest-ever total in the industry. The escalating demand for chips, coupled with favorable government initiatives and rising demand for semiconductor chips, has led to an increase in semiconductor equipment spending, indicating a growing interest in establishing new foundries worldwide. Such increasing chip production is expected to drive the demand for electronic testing equipment.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific region significantly dominates the semiconductor and electronics industry, primarily driven by the extensive manufacturing bases in China, Japan, South Korea, and India, which have also been rapidly maturing in the final assembly of the electronics industry.

- Large contractors, such as Foxconn Technology Group and Megatron Asia Pacific Ltd, are in the process of setting up plants in India. According to IBEF, India is committed to reaching USD 300 billion worth of electronics manufacturing and exports of USD 120 billion by 2025-26. In addition, the Union Budget 2023-24 allocated INR 16,549 crore (USD 2 billion) for the Ministry of Electronics and Information Technology, which is about 40% more elevated annually.

- The region's increasing testing and inspection activities are expected to create a considerable demand for electrical test equipment. Previously, most regional firms conducted their testing and certification operations in-house. However, due to China's Compulsory Certification regulations, greater emphasis is now placed on the need for strict regulatory standards. This has led to increased outsourcing of testing services, thereby increasing the demand for test equipment among testing services companies.

- Apart from the consumer electronics industry, low-cost carriers dominate the region. Thus, the majority of the inspection and service activities are outsourced. Due to this, Singapore has emerged as a regional hub for maintenance and inspection services. Allied players operating from Singapore have maintained dominance in the region for over two decades. However, countries like Indonesia, Vietnam, and Thailand are challenging the country's dominance.

- Additionally, the region has been a base for multiple key players, including Yokogawa (Japan), Advantest Corp (Japan), Anritsu Corporation (Japan), Rigol Technologies (China), and ScienceTech Technologies (India). These companies, along with various other companies in the region, are continuously involved in product innovations, providing solutions across various industry applications.

- In August 2022, Advantest Corp. collaborated with the Rohde & Schwarz RTP high-performance oscilloscope for mass exhibition evaluation of high-speed SoC testers. In line with this partnership, the company aims to enhance the quality of its products to meet the latest requirements. Such initiatives by the regional companies are expected to promote market growth.

- Furthermore, multiple infrastructure projects, such as executing high voltage lines and power generation plants, are anticipated to drive the region's demand for electrical testing equipment. For instance, in August 2022, China's State Grid plans to fund more than CNY 150 billion (USD 22 billion) in UHV power transmission lines in the second half of 2022. The construction of 8 new UHV projects is expected to connect China's far western regions, where solar, wind, and hydropower plants are primarily located, to its major cities, further driving market growth.

Electrical and Electronic Test Equipment Market Overview

The electrical and electronic test equipment market is characterized by a high degree of fragmentation, featuring key players like Fortive Corporation, Keysight Technologies Inc., Rohde & Schwarz GmbH & Co. KG, National Instruments Corporation, and Anritsu Corporation. Market participants are strategically leveraging partnerships and acquisitions to bolster their product portfolios and establish a sustainable competitive edge.

August 2023: Yokogawa Test & Measurement Corporation, a subsidiary of Yokogawa Electric Corporation, introduced the DLM5000HD series of precision oscilloscopes. Positioned as an advanced iteration of the DLM5000 series, the DLM5000HD series broadens Yokogawa's oscilloscope offerings, encompassing models with 500 MHz and 350 MHz frequency bandwidths. These models offer enhanced resolution for precise waveform analysis and incorporate user-friendly features that streamline setup and operation.

June 2023: Advantest Corporation unveiled its collaboration with Arizona State University (ASU) to establish a novel test engineering program in partnership with NXP. The program's curriculum, initially developed by ASU's Ira and Fulton Schools of Engineering faculty, was enriched through laboratory experiments devised by Advantest. These experiments are administered jointly by Advantest and NXP, marking a significant educational milestone.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technological Advancements Leading to the need for Test and Measurement Equipment

- 5.1.2 Emerging Trend of Electric and Hybrid Vehicle

- 5.2 Market Challenge/Restraint

- 5.2.1 Price Sensitivity and Increasing Preference for Rental Services

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Semiconductor Automatic Test Equipment (ATE)

- 6.1.2 Radio Frequency (RF) Test Equipment

- 6.1.3 Digital Test Equipment

- 6.1.4 Electrical and Environmental Test

- 6.1.5 Data Acquisition (DAQ)

- 6.2 By End-user Industry

- 6.2.1 Communications

- 6.2.2 Semiconductors and Computing

- 6.2.3 Aerospace and Defense

- 6.2.4 Consumer Electronics

- 6.2.5 Electric Vehicles (EVs)

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 VENDOR MARKET SHARE ANALYSIS

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Fortive Corporation

- 8.1.2 Keysight Technologies Inc.

- 8.1.3 Rohde & Schwarz GmbH & Co. KG

- 8.1.4 National Instruments Corporation

- 8.1.5 Anritsu Corporation

- 8.1.6 Teledyne Lecroy (Teledyne Technologies Incorporated)

- 8.1.7 Yokogawa Test & Measurement Corporation (Yokogawa Electric Corporation)

- 8.1.8 Teradyne Inc.

- 8.1.9 Chauvin Arnoux Group

- 8.1.10 Advantest Corporation